East Africa Automotive Engine Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

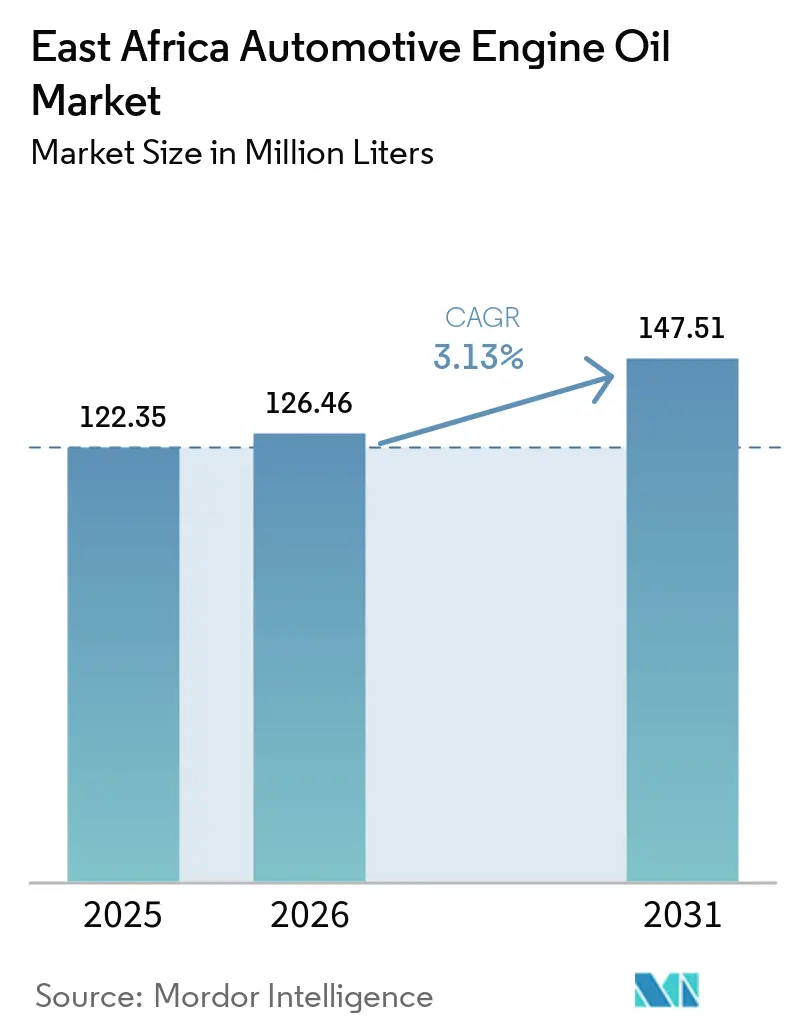

| Base Year Market Size (2025) | 122.35 Million liters |

| Market Volume (2026) | 126.46 Million liters |

| Market Volume (2031) | 147.51 Million liters |

| Growth Rate (2026 - 2031) | 3.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

East Africa Automotive Engine Oil Market Analysis by Mordor Intelligence

The East Africa Automotive Engine Oil Market size is projected to be 122.35 million liters in 2025, 126.46 million liters in 2026, and reach 147.51 million liters by 2031, growing at a CAGR of 3.13% from 2026 to 2031. Mineral oils account for the majority of demand; however, fully synthetic grades are growing at a faster rate due to the implementation of Euro IV homologation standards for new vehicles and stricter annual inspection protocols in Kenya, Tanzania, and Uganda. The increase in motorcycle registrations, particularly Kenya's expanding boda-boda market, is influencing aftermarket channels and driving higher sales of small-pack two-stroke and four-stroke oils. Heavy-duty oil demand is also increasing, supported by large infrastructure projects such as Kenya's Kisumu-Malaba Standard Gauge Railway extension and Tanzania's Mahenge Graphite Project. These projects collectively require thousands of engines that specify premium formulations like 15W-40 or 10W-30. Competitive dynamics are intensifying as global marketers expand local blending operations. For example, TotalEnergies has increased its Mombasa capacity to 47 kilotons, while Puma Energy has entered a blending venture in Kenya. Both initiatives are facilitated by duty-free base-oil remission schemes under the East African Community's tariff program.

Key Report Takeaways

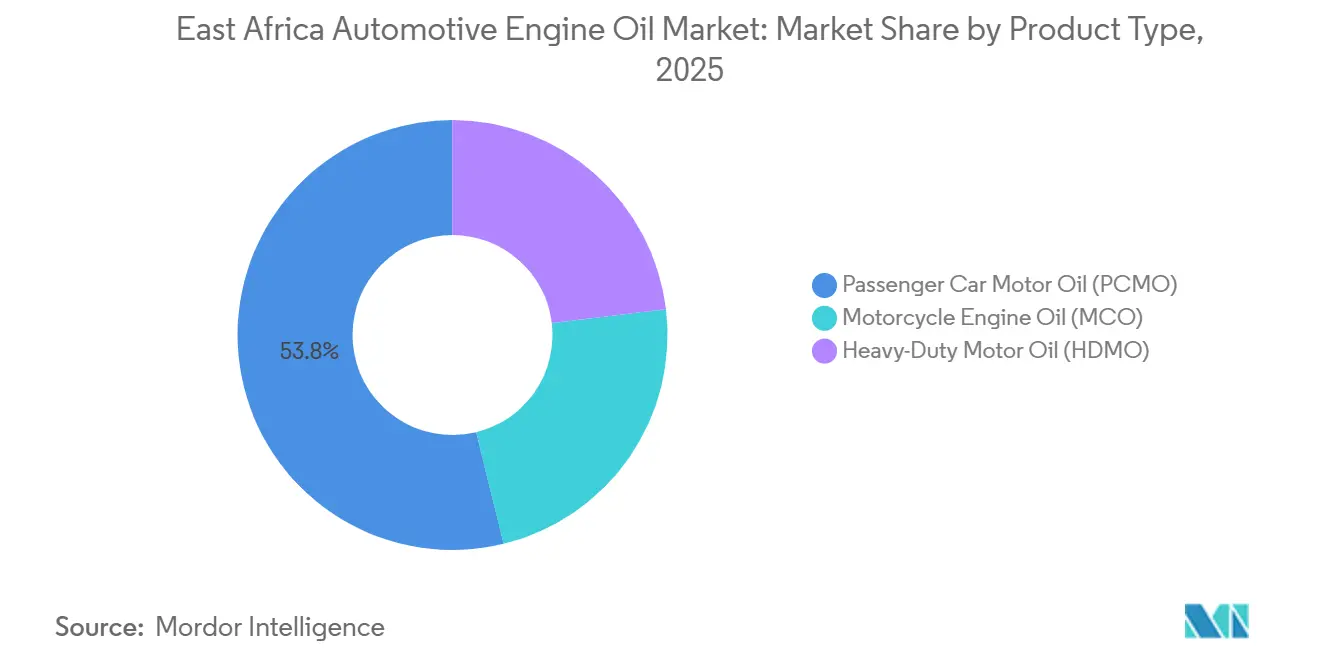

- By product type, passenger car motor oil led with 53.81% of East Africa automotive engine oil market share in 2025, whereas motorcycle engine oil is advancing at a 3.34% CAGR through 2031.

- By base stock type, mineral oils captured 72.27% of the East Africa automotive engine oil market size in 2025, but fully synthetic oils are forecast to grow at a 3.96% CAGR through 2031.

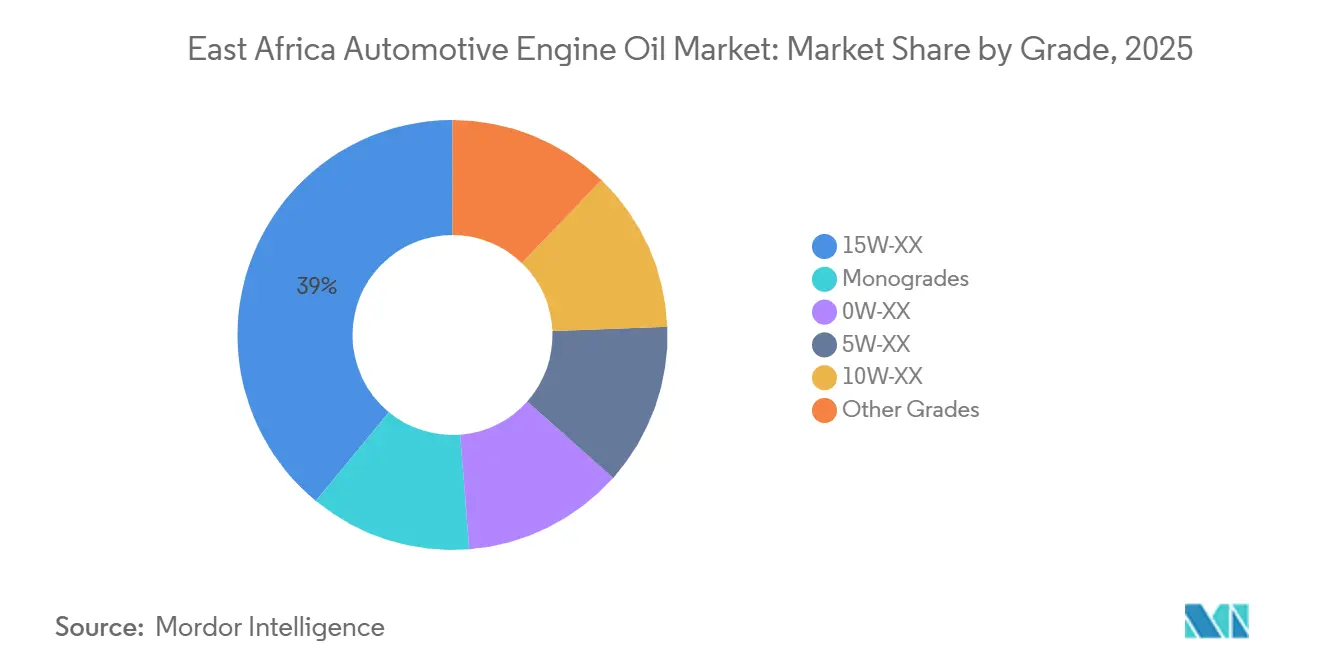

- By grade, the 15W-XX viscosity family held 39.04% of the 2025 volume; however, 5W-XX grades are set to expand at 3.81% CAGR through 2031.

- By geography, Kenya accounted for 40.51% volume in 2025, and Tanzania is advancing at a 3.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

East Africa Automotive Engine Oil Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising average vehicle age | +0.6% | Kenya, Tanzania, Uganda, highest in rural and peri-urban areas | Medium term (2-4 years) |

| Growing vehicle parc & used-car imports | +0.7% | Kenya, Tanzania, Uganda; spillover to Rwanda, Burundi | Short term (≤ 2 years) |

| Boom in logistics, mining & infrastructure projects | +0.5% | Tanzania (Mahenge, SGR), Kenya (Kisumu-Malaba SGR, Voi-Taveta railway) | Medium term (2-4 years) |

| Rapid shift toward synthetic & semi-synthetic oils | +0.4% | Urban centers in Kenya, Tanzania; OEM-driven in Uganda | Long term (≥ 4 years) |

| EAC duty-remission scheme catalyzing local blending | +0.3% | Tanzania, Rwanda, Kenya, and localized to blending hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Average Vehicle Age

Kenya's eight-year import cap, effective from January 2026, allows the import of vehicles manufactured in 2018. This results in fleets with service lives ranging from 6 to 15 years, which consume higher volumes of 15W-40 and 20W-50 lubricants due to increased wear, leaks, and oil burn[1]Kenya Revenue Authority, “Vehicle import age restrictions,” kra.go.ke. In the first eight months of 2024, Tanzania imported 46,944 used cars, while Uganda imported 19,440, with most vehicles showing odometer readings exceeding 100,000 km. Kenya's DKS 1515:2025 annual inspection regulations now include checks on engine oil levels, pressure, and leak integrity, prompting more frequent oil drain cycles for commercial fleets. Although logistics operators are experimenting with oil condition monitoring, adoption remains below 5%, leaving significant potential for premium-grade lubricant sales. As engines age, recommended drain intervals often shorten, despite consumer efforts to extend them, contributing to an overall increase in lubricant consumption.

Growing Vehicle Parc and Used-Car Imports

In December 2025, Kenya registered 31,595 new vehicles, while the national vehicle parc surpassed 3 million units, including over 1.4 million motorcycles, significantly increasing lubricant demand[2]Kenya National Transport and Safety Authority, “Vehicle registration statistics 2025,” ntsa.go.ke. The influx of vehicles from Japan and the United Arab Emirates has introduced turbocharged gasoline and diesel powertrains, which require low-sulfated ash, phosphorus, and sulfur (SAPS), low-viscosity oils as specified in original equipment manufacturer (OEM) manuals. However, these oils are rarely available in rural areas, leading mechanics to rely on mineral 15W-40 oils. Motorcycle registrations surged by 128.2% year-on-year to 163,112 units in 2025, with motorcycles consuming oil at three to five times the per-kilometer rate of passenger cars. Pack-size preferences are shifting, with 1-liter and 500-mL bottles dominating roadside sales as boda-boda riders opt for smaller, more affordable quantities. The East Africa automotive engine oil market benefits from both the growth in the vehicle parc and the higher frequency of oil top-ups across different vehicle categories.

Boom in Logistics, Mining, and Infrastructure Projects

The Kisumu-Malaba railway extension, launched in March 2026, has mobilized excavators and haul trucks requiring API CK-4 or ACEA E6 lubricants. Similarly, Tanzania's Mahenge Graphite Project, which is creating 900 full-time jobs, involves continuous heavy-equipment operations, collectively increasing demand for heavy-duty oil. In January 2026, Africa Global Logistics (AGL) added 32 Sinotruk prime movers, while DHL deployed 25 Euro 5 biodiesel trucks in March 2025, upgrading fleet lubricant requirements to synthetic-blend 10W-30 or 5W-30 grades. Extended drain intervals of 20,000-40,000 km are becoming standard along the Northern Corridor, increasing the value per oil change despite reduced frequency. While mining electrification remains in its early stages, the adoption of electric drill rigs by international contractors is unlikely to significantly impact diesel-engine oil demand before 2031. Overall, construction and logistics activities provide a stable demand base for the East Africa automotive engine oil market.

Rapid Shift Toward Synthetic and Semi-Synthetic Oils

The adoption of Euro IV emissions standards has led Original Equipment Manufacturers (OEMs) to recommend low-viscosity, low-Sulfated Ash, Phosphorus, and Sulfur (SAPS) formulations. TotalEnergies' Mombasa facility upgrade now enables local production of American Petroleum Institute (API) SN Plus and ACEA C3 grades, reducing lead times and lowering retail prices for synthetic oils. Fleet operators are increasingly using telematics-driven oil analytics, which can extend drain intervals by up to 30% when premium-grade oils are utilized, enhancing the cost-effectiveness of synthetics. Marketers achieve approximately 20% higher gross margins on synthetic products, driving efforts to promote these options. While end-user awareness remains limited, warranty requirements from truck OEMs are compelling service centers to transition away from straight mineral oils for newer engines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit/adulterated oils | -0.4% | Kenya, Tanzania, Uganda, are concentrated in informal retail and border towns | Short term (≤ 2 years) |

| High price sensitivity & import reliance | -0.3% | Uganda, Burundi, South Sudan, rural Kenya, and Tanzania | Medium term (2-4 years) |

| Forex shortages causing lubricant stock-outs | -0.2% | Ethiopia, South Sudan, Burundi, episodic in Kenya and Tanzania | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit or Adulterated Oils

Kenya’s Anti-Counterfeit Authority seized KES 65 million (USD 0.50 million) worth of illicit lubricants over five years, while Tanzania’s Fair Competition Commission confiscated 5,000 gallons in Kariakoo in February 2026. These incidents indicate a persistent gray market that affects branded equity. Counterfeiters refill branded cans with downgraded mineral or recycled oil and distribute them through informal kiosks in border towns and peri-urban areas. Low penalties and limited forensic laboratories hinder effective prosecution, allowing offenders to resume operations quickly. Marketers are testing QR-code or Short Message Service (SMS) validation seals, but informal retailers resist due to compliance costs. Without stricter legal deterrents, counterfeit products will continue to reduce legitimate market volumes and impact the East Africa automotive engine oil industry.

High Price Sensitivity and Import Reliance

Retail prices for 4-liter 15W-40 packs average USD 15-20 in Kenya, while unbranded alternatives are priced at USD 10-12, offering a significant discount for cost-sensitive consumers such as boda-boda riders and small fleet owners. Uganda and Burundi rely on imports for over 90% of finished lubricants, making them subject to 35-36% import tariffs and freight surcharges. Parallel smuggling channels undermine official distributors, but quality inconsistencies from these sources lead to premature engine wear. Multinational companies are introducing local blending to stabilize supply chains, but smaller importers lack the scale to mitigate global base-oil price fluctuations. As a result, persistent price differences limit the adoption of higher-spec synthetic lubricants among consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motorcycle Oils Accelerate

Passenger car motor oil is projected to account for 53.81% of the East Africa automotive engine oil market size in 2025, reflecting the prevalence of sedans and SUVs in urban fleets. Motorcycle engine oil is expected to be the fastest-growing segment, with a compound annual growth rate (CAGR) of 3.34% through 2031, driven by Kenya’s 163,112 new motorcycle registrations in 2025 and the expansion of two-wheeler taxi networks in Uganda. Demand for heavy-duty motor oil is supported by freight growth along the Northern Corridor and ongoing railway projects that require continuous operation of excavators and bulldozers.

Roadside mechanics are increasingly opting for 1-liter and 500 mL packs for two-wheelers, as riders prefer smaller, more affordable packaging. This shift in packaging has improved per-liter margins by 20-30%. Fleet modernization in the trucking sector, such as DHL’s adoption of Euro 5 biodiesel vehicles, is driving higher viscosity and performance requirements, steering the East Africa automotive engine oil market toward synthetic blends. Meanwhile, passenger car drain intervals are lengthening as owners reduce maintenance expenses, partially offsetting growth driven by the expansion of the vehicle population.

By Base Stock Type: Synthetics Chip Away at Mineral Dominance

Mineral formulations accounted for 72.27% of the projected 2025 volume; however, fully synthetic grades are expected to grow at an annual rate of 3.96%, exceeding the overall growth of the East Africa automotive engine oil market. Semi-synthetic oils, offering a balance between cost and performance, are increasingly adopted by logistics fleets seeking cost-effective protection. Bio-based oils remain in the early stages of development due to limited feedstock availability and the lack of supportive incentives.

The 47-ton TotalEnergies facility in Mombasa now manufactures American Petroleum Institute (API) SN Plus and European Automobile Manufacturers' Association (ACEA) C3 lubricants, significantly reducing lead times for synthetic oil supply across the region. Synthetic oil blenders achieve higher gross margins, enabling increased investment in consumer education initiatives. Additionally, original equipment manufacturer (OEM) warranty clauses are increasingly voiding coverage if mineral oils are used in turbocharged or gasoline direct injection (GDI) engines, driving a faster shift toward synthetic alternatives.

By Grade: 5W-XX Gains Traction

The 15W-XX family is expected to account for 39.04% of the market share in 2025, supported by older, high-mileage vehicles that are compatible with thicker oils. In comparison, 5W-XX multigrades are projected to grow at an annual rate of 3.81%, driven by Kenya's eight-year import rule. This regulation enables the entry of newer Euro IV engines, which require lower viscosity oils. The adoption of these oils is particularly observed in cities such as Nairobi, Dar es Salaam, and Kampala, where original equipment manufacturer (OEM)-certified workshops promote compliance with engine specifications.

Cold-climate 0W-XX grades and specialized racing or marine oils together represent a small share of market demand, limited by inadequate technical support. For example, DHL's Euro V trucks require 5W-30 low-sulfated ash, phosphorus, and sulfur (low-SAPS) lubricants, illustrating how fleet upgrades are influencing the East Africa automotive engine oil market toward higher-specification products. Meanwhile, monogrades, which were previously common in heavy equipment, are declining as extended drain intervals make multigrades a more cost-effective option.

Geography Analysis

In 2025, Kenya, Tanzania, and Uganda dominated the regional volume landscape. Kenya accounted for a 40.51% share in 2025, with fuel consumption reaching 6.55 million cubic meters, up from 2024. This increase in fuel consumption drove a rise in lubricant throughput, solidifying Kenya's status as the top consumer in East Africa's automotive engine oil market. Between January and August 2024, Tanzania imported 46,944 used cars and, as a logistics hub for six landlocked neighbors, facilitated the movement of heavy-duty motor oil along key trade routes. Tanzania is projected to register the fastest compound annual growth rate (CAGR) of 3.37% during the forecast period (2026-2031). Uganda's 2024 decision to reverse the zero-rated duty on electric vehicles (EVs) has supported the continued dominance of internal combustion engines, sustaining lubricant demand.

While Rwanda and Burundi are smaller markets, they are experiencing above-average growth, driven by the rapid expansion of urban motorcycle taxi fleets. Rwanda's duty-remission policy for its two blending plants, with a combined capacity of 7.1 million liters, has reduced retail prices and improved access to original equipment manufacturer (OEM)-approved lubricant grades. Conversely, Ethiopia, South Sudan, and Somalia face challenges such as foreign exchange shortages, political instability, and weak regulatory enforcement. These issues lead to periodic shortages, pushing buyers toward informal markets.

TotalEnergies' hub in Mombasa caters to Kenya, Uganda, Tanzania, Seychelles, Rwanda, Burundi, and the eastern Democratic Republic of Congo (DRC), establishing Kenya as the production center for East Africa's automotive engine oil sector. Puma Energy, with over 90 retail stations in Tanzania, launched its first hybrid compressed natural gas (CNG) outlet in Dar es Salaam in October 2025. This move highlights a shift toward gaseous fuels, which may moderate the demand for liquid lubricants. However, despite the implementation of a harmonized external tariff, non-tariff barriers, such as roadblocks and informal payments, add up to 15% to freight costs, limiting lubricant trade within the East African Community (EAC).

Competitive Landscape

The East Africa automotive engine oil market is moderately fragmented. Multinational companies such as TotalEnergies, Shell plc, BP p.l.c., and Puma Energy dominate the formal channels of the East Africa automotive engine oil market, while local blenders and gray-market traders share the remaining market. TotalEnergies expanded its operations in Mombasa, doubling its synthetic oil production capacity, and now supplies products meeting International Lubricant Standardization and Approval Committee (ILSAC) and European Automobile Manufacturers' Association (ACEA) specifications to seven East African Community (EAC) member countries. Puma Energy’s 2025 blending partnership in Kenya focuses on offering Original Equipment Manufacturer (OEM)-approved product ranges, targeting fleet accounts that prioritize warranty compliance.

Vivo Energy commissioned its 336th Shell-branded station in Kenya in July 2025 and introduced the Vivo Energy-Customer Experience Management (VE-CEM) telematics platform, which reduces drain intervals by up to 30%, creating data-driven switching costs for large fleet operators. Local blenders, including Lake Group, Mogas, and Delta Lubricants, leverage duty-free base oil imports to offer mineral-grade oils at lower prices than multinational competitors. Emerging players such as India’s Maximus International plan to invest USD 25 million to expand East Africa’s production capacity to 60,000 kiloliters per annum by 2027. Additionally, low-cost Chinese suppliers are entering the market, offering American Petroleum Institute (API)-certified products priced 20-30% below global brands.

Counterfeit oils remain a significant challenge in the market. Kenya’s Anti-Counterfeit Authority and Tanzania’s Fair Competition Commission seized substantial volumes of counterfeit products during 2025-2026. However, limited laboratory capacity and lenient penalties contribute to repeat offenses. In response, marketers have introduced track-and-trace packaging and consumer Short Message Service (SMS) verification systems, though adoption remains slow in informal retail channels. Technology advancements, localized blending, and duty regimes are expected to be key competitive factors in the near-term development of the East Africa automotive engine oil market.

East Africa Automotive Engine Oil Industry Leaders

Shell plc

TotalEnergies

BP p.l.c.

Chevron Corporation

Puma Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: WearCheck launched its Lubrigard condition-monitoring website, providing oil analysis services and predictive maintenance solutions for fleets, mining operations, and industrial plants across Africa. This platform supports operators in optimizing drain intervals and reducing overall costs, which is particularly relevant for the East Africa automotive engine oil industry, where efficient maintenance practices are critical.

- March 2025: DHL collaborated with Scania to introduce 25 Euro 5 biodiesel trucks in Kenya, which require 5W-30 low-SAPS (Low-Sulfated Ash, Phosphorus, and Sulfur) lubricants to safeguard diesel particulate filters. This development reflects how fleet modernization in East Africa is influencing demand for lower-viscosity, higher-specification grades, creating opportunities for synthetic oil suppliers in the automotive engine oil market.

East Africa Automotive Engine Oil Market Report Scope

Automotive engine oil, a lubricant for internal combustion engines, reduces friction, cools components, seals the combustion chamber, and cleans internal parts. By preventing metal-to-metal contact, it extends engine life. Engine oils, available as synthetic or conventional, are classified based on their viscosity.

The East Africa automotive engine oil market is segmented by product type, base stock type, grade, and geography. By product type, the market is segmented into passenger car motor oil (PCMO), heavy-duty motor oil (HDMO), and motorcycle engine oil (MCO). By base stock type, the market is segmented into mineral, semi-synthetic, fully synthetic, and bio-based. By grade, the market is segmented into 0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades. The report also covers the market size and forecasts for automotive engine oil in 7 countries across the region. The market sizes and forecasts are provided in terms of volume (Liters).

| Passenger Car Motor Oil (PCMO) |

| Heavy-Duty Motor Oil (HDMO) |

| Motorcycle Engine Oil (MCO) |

| Mineral |

| Semi-Synthetic |

| Fully Synthetic |

| Bio-Based |

| 0W-XX |

| 5W-XX |

| 10W-XX |

| 15W-XX |

| Monogrades |

| Other Grades |

| Kenya |

| Tanzania |

| Uganda |

| Ethiopia |

| Rwanda |

| Burundi |

| Democratic Republic of Congo |

| By Product Type | Passenger Car Motor Oil (PCMO) |

| Heavy-Duty Motor Oil (HDMO) | |

| Motorcycle Engine Oil (MCO) | |

| By Base Stock Type | Mineral |

| Semi-Synthetic | |

| Fully Synthetic | |

| Bio-Based | |

| By Grade | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| By Geography | Kenya |

| Tanzania | |

| Uganda | |

| Ethiopia | |

| Rwanda | |

| Burundi | |

| Democratic Republic of Congo |

Key Questions Answered in the Report

What is current market size of East Africa Automotive Engine Oil Market?

The East Africa Automotive Engine Oil Market size is projected to be 122.35 million liters in 2025, 126.46 million liters in 2026, and reach 147.51 million liters by 2031, growing at a CAGR of 3.13% from 2026 to 2031.

Which product category will grow fastest through 2031?

Motorcycle engine oil leads with a 3.34% CAGR because of rapid two-wheeler fleet expansion.

How dominant are mineral oils today?

Mineral grades held 72.27% of 2025 volume but gradually cede share to synthetics.

Why are synthetics gaining momentum?

Euro IV emission rules, OEM warranty clauses, and higher fleet total-cost-of-ownership savings are driving a 3.96% annual growth rate for fully synthetic oils.

Page last updated on: