Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

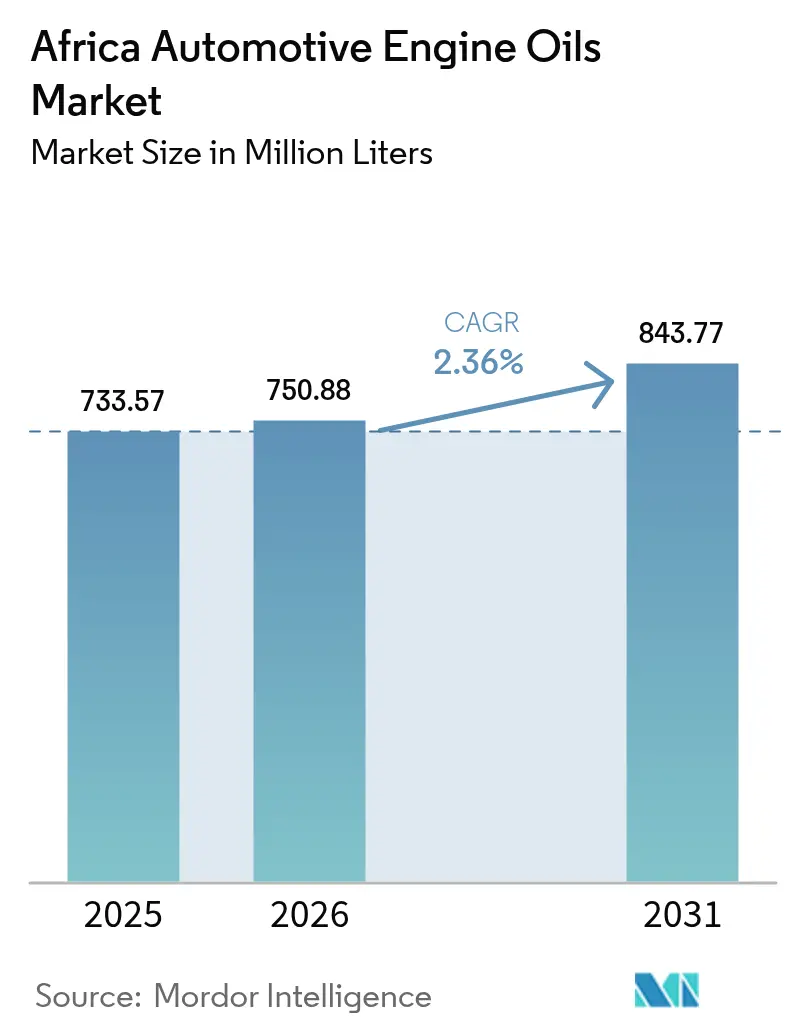

| Base Year Market Size (2025) | 733.57 Million liters |

| Market Volume (2026) | 750.88 Million liters |

| Market Volume (2031) | 843.77 Million liters |

| Growth Rate (2026 - 2031) | 2.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Automotive Engine Oils Market Analysis by Mordor Intelligence

The Africa Automotive Engine Oils Market size was valued at 733.57 million liters in 2025 and is estimated to grow from 750.88 million liters in 2026 to reach 843.77 million liters by 2031, at a CAGR of 2.36% during the forecast period (2026-2031). Refinery shutdowns in South Africa have led to structural supply gaps. Meanwhile, fluctuations in base-oil imports and the swift growth of Chinese OEM assembly plants are altering competitive dynamics in Africa's automotive engine oils market. The African Continental Free Trade Area (AfCFTA) is streamlining tariffs, enabling major blenders to centralize production in South Africa, Morocco, and Kenya. However, a mix of diesel-sulfur and emissions regulations forces companies to juggle parallel product lines. Additionally, motorcycles used by ride-hailing services are increasing their oil drain frequencies, bolstering volumes even as passenger cars trend towards electrification. Corporate fleets are leaning towards synthetic and re-refined blends, prioritizing extended-drain economics and a smaller carbon footprint in their purchasing decisions. In summary, Africa's automotive engine oils market is becoming increasingly fragmented. Vertically integrated giants, adept at globally sourcing Group II/III barrels, find themselves in competition with local independents, who leverage distribution density and competitive pricing to carve out their market niche.

Key Report Takeaways

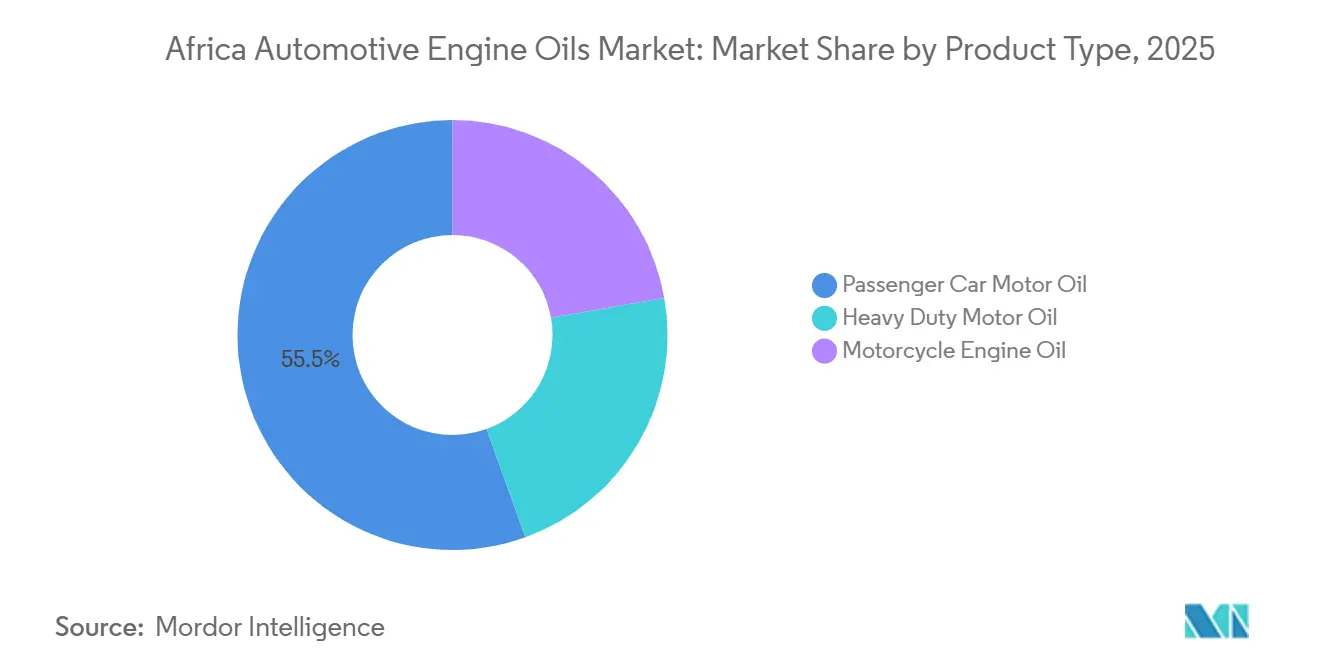

- By product type, passenger car motor oil led with 55.51% of Africa automotive engine oils market share in 2025, while motorcycle engine oil is projected to expand at a 2.69% CAGR through 2031.

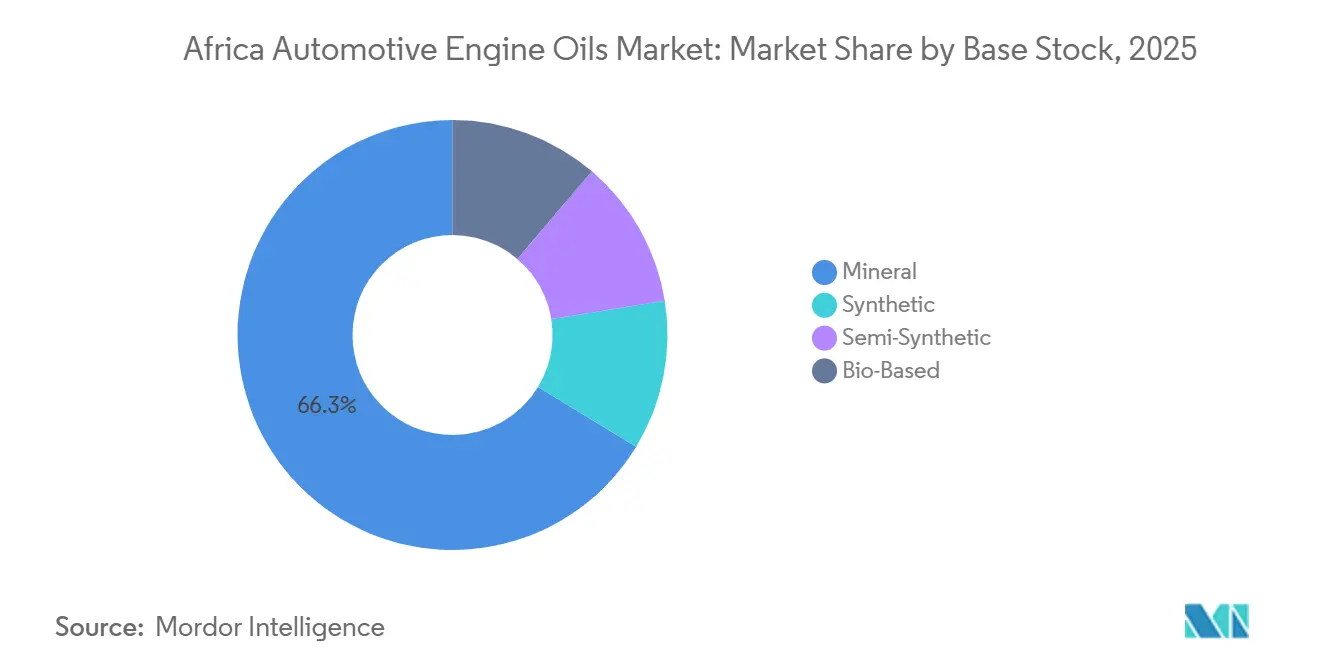

- By base stock, mineral oils captured 66.31% of Africa automotive engine oils market size in 2025; synthetic oils are expected to grow at a 2.78% CAGR between 2026-2031.

- By geography, South Africa accounted for 35.58% volume in 2025 and is advancing at a 2.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward premium and synthetic formulations | +0.60% | South Africa, Algeria, Egypt; spillover to Kenya, Nigeria urban centers | Medium term (2-4 years) |

| Stricter emission norms and advanced engine design | +0.50% | EAC (Kenya, Uganda, Tanzania, Rwanda, Burundi), ECOWAS (Nigeria, Ghana, Côte d'Ivoire), South Africa | Long term (≥ 4 years) |

| Ride-hailing and moto-taxi boom boosting drain frequency | +0.70% | Nigeria, Kenya, Ghana, Senegal, Côte d'Ivoire, Tanzania | Short term (≤ 2 years) |

| Chinese OEM assembly expansion and factory-fill deals | +0.40% | South Africa, Uganda, Kenya, Nigeria | Medium term (2-4 years) |

| AfCFTA tariff cuts enabling regional lubricant hubs | +0.30% | Pan-African, with hubs in South Africa, Morocco, Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Premium and Synthetic Formulations

Algeria, increasingly sourcing from synthetic grades, signals a rising demand for high-performance lubricants, particularly with the shift towards low-sulfur fuel. TotalEnergies’ Rubia EV3R, made from re-refined base oil, highlights the advantages of circular feedstocks: a reduced carbon footprint and a premium price, especially attractive to fleet buyers focused on sustainability. The African Union’s Continental Circular Economy Action Plan (2024-2034) reinforces this trend, tying re-refining goals to producer-responsibility mandates. Local players, such as FFS Refiners in South Africa and Afro-Oil in Uganda, are setting up collection points, transforming waste oil into valuable commodities. Moreover, warranty requirements from turbocharged, downsized engines by Chinese and Indian OEMs are propelling this transition. These engines necessitate oxidation-stable, low-volatility oils, a benchmark that mineral grades often fail to meet. While mineral products dominate Africa's automotive engine oils sector, there is a noticeable shift towards suppliers with access to Group II/III molecules and key additive-technology collaborations.

Stricter Emission Norms and Advanced Engine Design

In 2024, EAC members adopted Euro 4-equivalent standards and 50 ppm diesel. Meanwhile, ECOWAS set a January 2025 deadline for refineries, but compliance remains limited. South Africa aims for a 10 ppm target by July 2027, leading to a divided demand: low-SAPs oils for newer trucks and high-TBN blends for older ones. While ARSO is aligning lubricant testing methods with ISO/TC 28, the speed of this adoption varies by regulator. This inconsistency compels blenders to juggle a range of SKUs and additive combinations. Morocco, at the forefront with Euro 6 operations, has tapped into a profitable market for API CK-4 and ACEA E6 formulations, enjoying substantial margins. As engine downsizing and heightened combustion pressures elevate operating temperatures, multinationals are pushing for PAO-enhanced synthetics to ensure viscosity. These rigorous regulations tend to benefit larger entities, enabling them to distribute R&D expenses across global volumes.

Chinese OEM Assembly Expansion and Factory-Fill Deals

BAIC, Foton, and Chery have established completely knocked-down lines in South Africa and Uganda. Their factory-fill contracts, influenced by specifications, favor full or semi-synthetic grades aligning with OEM standards. Chevron’s Group II hub in Durban strategically positions the company to supply API SN Plus and ILSAC GF-6 oils, both endorsed by these assemblers. The African Association of Automotive Manufacturers, in partnership with Afreximbank, is leading a Pan-African Auto Pact, aiming to streamline assembly operations into five regional hubs. This consolidation of purchasing power presents hurdles for independent players, particularly those without the means for OEM-approval testing. Uganda's local blending to satisfy content mandates hints at a potential shift of factory-fill volumes to domestic lube-oil-blending plants (LOBPs). Moving forward, these contracts are likely to redirect a portion of Africa's automotive engine oils market from retail channels to exclusive supply deals.

AfCFTA Tariff Cuts Enabling Regional Lubricant Hubs

AfCFTA's duty cuts on finished lubricants and base stocks have enabled centralized plants in Durban, Mohammedia, and Nairobi to efficiently cater to multiple nations[1]African Organisation for Standardisation, “Standards Harmonisation Work,” arso-oran.org . Vivo Energy’s takeover of Engen has broadened its reach to various stations, leveraging this logistical edge. TotalEnergies has expanded its Nairobi blender's capacity, turning it into an export center for the Great Lakes and Horn of Africa. Chevron, utilizing a tariff-free pathway, ships Group II barrels from Mohammedia to West Africa, eyeing the ECOWAS market. Yet, the uneven application of unified fuel standards across countries means non-tariff barriers remain a hurdle, highlighting the need for local knowledge in customs, excise codes, and labeling. Blenders who master these challenges can harness AfCFTA as a pivotal advantage in Africa's automotive engine oils arena.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Local refinery and LOBP closures limiting base oil supply | -0.40% | South Africa, Nigeria, Central Africa (Cameroon, Gabon, Congo) | Short term (≤ 2 years) |

| Long-drain interval oils and OEM extended-service packs | -0.30% | South Africa, Kenya, urban centers with OEM dealer networks | Medium term (2-4 years) |

| Accelerating electrification of urban bus fleets | -0.20% | Kenya, Ghana, Rwanda, Ethiopia, South Africa (municipal fleets) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-Drain Interval Oils and OEM Extended-Service Packs

In May 2024, Audi South Africa announced an extension of its Freeway Plan, now covering a span of 15 years or 300,000 kilometers. This move effectively reduces the frequency of oil changes throughout a vehicle's lifespan by half. In a similar vein, JAC Motors has increased the oil change intervals for its T9 bakkie, now set at 20,000 kilometers. Mobil Delvac highlighted the benefits of real-time oil analysis, in conjunction with ACEA E9 chemistry, successfully extending oil drain intervals for mining fleets. These strategic moves underscore the performance value, allowing synthetic oil suppliers to charge a premium per liter, all the while curtailing the usage of mineral oils. For distributors, this trend signifies fewer high-margin service visits, especially in dealer-dominated segments. The reduction in volume is notably sharper in premium and fleet channels, as opposed to informal garages, which still champion the conventional oil change intervals. Consequently, this has led to a bifurcated demand curve in Africa's automotive engine oils market.

Accelerating Electrification of Urban Bus Fleets

In line with municipal zero-emission mandates, Kenya, Ghana, and Rwanda are rolling out battery-electric buses. Bolt’s fleet in Nairobi has made significant strides in electrifying its passenger cars. Although internal-combustion motorcycles remain prevalent, each diesel bus replaced by an electric one diminishes the annual demand for engine oil. The financial viability of electric buses is enhanced by their operation on dedicated urban routes and the establishment of charging depots, with purchases often backed by multilateral lenders. While this transition is curbing the consumption of popular SAE 15W-40 oils, its repercussions on Africa's overall automotive engine oils market are largely confined to urban centers. Meanwhile, long-haul trucks and inter-city coaches persist in their reliance on diesel, a crucial need given Africa’s expansive distances and the challenges of refueling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motorcycle Oils Outpace Passenger-Car Volumes

In Africa automotive engine oils market, motorcycle engine oils led the growth with a 2.69% CAGR during the forecast period of 2026-2031, driven by the rapid expansion of ride-hailing and moto-taxi services in Nigeria, Kenya, and Tanzania. In 2025, passenger car motor oil accounted for the largest share, representing 55.51% of the market. Urban duty cycles, characterized by high temperatures and frequent stops, prompt boda-boda operators to change oil more frequently than private motorists, thereby increasing the demand for JASO MA2 10W-40. While older trucks and off-road equipment continue to rely on heavy-duty diesel oils such as SAE 15W-40 CI-4, ACEA E6 low-SAPs blends are gaining popularity in regions with low-sulfur diesel.

Climate significantly influences viscosity preferences: South Africa and Morocco favor 5W-30 and 5W-40 multigrades, while West and Central Africa prefer 10W-40 and 15W-40. Monogrades remain prevalent in agricultural engines, as rural mechanics often do not perceive the added value of cold-start benefits. Shell’s launch of API SQ motorcycle oil in Egypt highlights a shift, showcasing OEM-level performance now extending to two-wheelers[2]Shell, “Shell Launches New Motorcycle Oil Portfolio in Egypt,” shell.com . As regulations tighten, Africa's automotive engine oils market will evolve based on the pace of motorcycle electrification and passenger-car OEMs advocating for extended oil drains.

By Base Stock: Synthetics Gain Despite Mineral Dominance

In 2025, mineral grades held a 66.31% share of Africa's automotive engine oils market. However, synthetics, driven by OEM factory-fill specifications and fleet tenders prioritizing reduced downtime, demonstrated steady growth with a 2.78% CAGR during the forecast period of 2026-2031. Algeria, with a 70% synthetic penetration, indicates a continental trend as desulfurized fuels gain traction. TotalEnergies’ Rubia EV3R exemplifies how re-refined base oil can align with corporate sustainability goals without compromising performance. Semi-synthetics, which blend Group III and Group I, provide adequate oxidation resistance at a modest premium.

Although bio-based oils remain in the experimental phase, they align with the African Union’s vision for a circular economy. FFS Refiners operates several used-oil collection hubs feeding into re-refineries, ensuring a domestic supply for Group I replacements. Similarly, Uganda’s Afro-Oil follows a smaller-scale version of this model. As the AfCFTA progresses toward tariff harmonization, regional players producing re-refined or semi-synthetic stocks locally, particularly those securing additive supplies and quality certifications, are well-positioned to capture a larger share of Africa's automotive engine oils market.

Geography Analysis

In 2025, South Africa commanded a 35.58% share of Africa's automotive engine oils market and is projected to grow at a 2.53% CAGR during the forecast period of 2026-2031. Despite facing refinery closures, South Africa adeptly imports low-sulfur diesel through Durban. This move has accelerated the uptake of low-SAPs API CK-4 and ACEA E6 oils. Vivo Energy's acquisition of Engen has consolidated numerous stations, allowing for storage and logistics economies of scale, a feat challenging for independent players. Mobil Delvac's promotion of extended-drain programs in mining highlights a market trend: customers are increasingly investing in high-performance synthetics when they see evident lifecycle savings.

Egypt and Nigeria are emerging as significant players, albeit taking different routes. Egypt's closeness to the Suez shipping lanes, combined with Shell's introduction of the API SQ motorcycle oil, is driving the uptake of premium oils in two-wheelers. In contrast, Nigeria presents a mixed scenario: while it predominantly imports finished lubricants, outages at the Dangote refinery have delayed the availability of local base oils. Nevertheless, Abuja is witnessing a rising demand for 5W-30 oils, spurred by an influx of newer passenger vehicles, and Lagos' ride-hailing industry continues to support high motorcycle volumes. East African Community members, such as Kenya, Uganda, and Tanzania, have embraced low-sulfur diesel and Euro 4 engines, leading to a surge in low-SAPs. TotalEnergies' significant capacity boost in Nairobi strategically positions the firm for expansion into the Great Lakes states.

However, Africa's advancements are inconsistent. While ECOWAS has set low-sulfur standards, nations like Senegal and Côte d'Ivoire lag due to financial constraints in upgrading refineries. Central Africa's dependence on outdated plants continues its import reliance. Morocco distinguishes itself with Euro 6 regulations and Chevron's Group II hub in Mohammedia, fostering the growth of ACEA C3 synthetics. Despite ARSO's efforts for regional standardization with SAE J2227 and SAE J357, inconsistent enforcement means distributors must adeptly navigate local labeling and customs to succeed in Africa's automotive engine oils market.

Competitive Landscape

The Africa automotive engine oils market is moderately fragmented. Major players like TotalEnergies, Shell, BP, ExxonMobil, and Chevron are blending global Group II/III refining with branded service stations. This strategy not only ensures feedstock security during shortages but also capitalizes on proprietary additive chemistries licensed from firms like Lubrizol and Infineum. In a move highlighting its sustainability focus and cost-hedging strategy, TotalEnergies brought Tecoil's re-refinery into its fold in 2024. Meanwhile, Shell is strategically targeting Egypt's motorcycle segment, a niche many majors have overlooked, to boost volumes as passenger-car drain cycles extend.

Regional independents, such as Engen (now under Vivo Energy), Astron, Oando, and Afriquia, are leveraging their dense distributor networks and nimble decision-making. Vivo's extensive station presence across multiple nations showcases how aggregation can achieve scale, even without upstream integration. Disruptors like FFS Refiners and Afro-Oil are innovating by transforming waste oil into Group I/II barrels, doing so with notably lower energy consumption, thus reaping both cost and ESG benefits. Concurrently, Chinese additive suppliers are penetrating the market, offering competitively priced products, especially in the API SL/SM grades, challenging established players.

BP's scrutiny of its Castrol unit introduces a layer of strategic uncertainty; a potential private-equity divestment could align Castrol's African operations with a regional blender, reshaping the brand's market stance. ExxonMobil's Baytown facility is on track to amplify Group III supplies by 2028, with early offtake agreements poised to help African importers navigate synthetic price fluctuations. Lubrizol's collaboration with Oil Store, enabling direct shipments of finished fluids, highlights additive manufacturers' ambition to seize downstream margins, circumventing traditional brand owners. Ultimately, the trajectory of Africa's automotive engine oils market will be determined by the depth of capabilities and the assurance of feedstock access.

Africa Automotive Engine Oils Industry Leaders

TotalEnergies

BP p.l.c.

Shell Plc

Chevron Corporation

Engen Petroleum Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Castrol unveiled its upgraded GTX range, introducing GTX 5W-30 and GTX 10W-40, during a launch event in Gaborone, Botswana. These new formulations are designed to elevate the driving experience, providing enhanced protection, cleanliness, and performance for both vintage and modern vehicles.

- April 2025: Engen rebranded its Xtreme lubricants range, now marketed as a premium choice for South African drivers. Tailored to the unique challenges of local roads and climate, the revamped Xtreme range boasts enhanced performance, cutting-edge protection, and a fresh packaging design.

Africa Automotive Engine Oils Market Report Scope

Automotive engine oil, also referred to as motor oil, is a lubricant specifically formulated for internal combustion engines in vehicles, as opposed to lubricants for external moving parts. Designed to withstand the demanding conditions within automotive engines, this petroleum-based fluid is produced using base oils refined from crude oil and combined with various performance additives. Differences in brand, viscosity grade, and specifications result in variations in the quality and composition of the base stock and additive packages.

The Africa Automotive Engine Oils Market is segmented by product type, base stock, and geography. By product type, the market is segmented into passenger car motor oil, heavy duty motor oil, and motorcycle engine oil. By base stock, the market is segmented into mineral, synthetic, semi-synthetic, and bio-based. The report also covers the market size and forecasts for automotive engine oils in 3 countries across major African regions. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

By Geography

| South Africa |

| Egypt |

| Nigeria |

| Rest of Africa |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Africa automotive engine oils market be by 2031?

The Africa automotive engine oils market size stands at 750.88 million liters in 2026, and it is projected to reach 843.77 million liters by 2031 at a 2.36% CAGR.

Which segment is growing fastest inside the African lubricant space?

Motorcycle engine oil leads with a 2.69% CAGR through 2031, propelled by ride-hailing and moto-taxi fleets.

Why are synthetic formulations gaining traction?

OEM factory-fill needs, longer drain intervals, and sustainability mandates favor synthetics despite higher prices.

What share does South Africa hold today?

South Africa contributed 35.58% of the 2025 volume and is advancing at a 2.53% CAGR through 2031.

How will AfCFTA affect lubricant distribution?

Harmonized tariffs allow centralized blending hubs in Durban, Nairobi, and Mohammedia to ship tariff-free across regions, lowering landed costs.

Which restraint could cut future demand most sharply?

Extended-drain service packs from OEMs may halve oil changes per vehicle, trimming mineral-oil volumes in dealer-served markets.

Page last updated on: