Botswana Automotive Engine Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

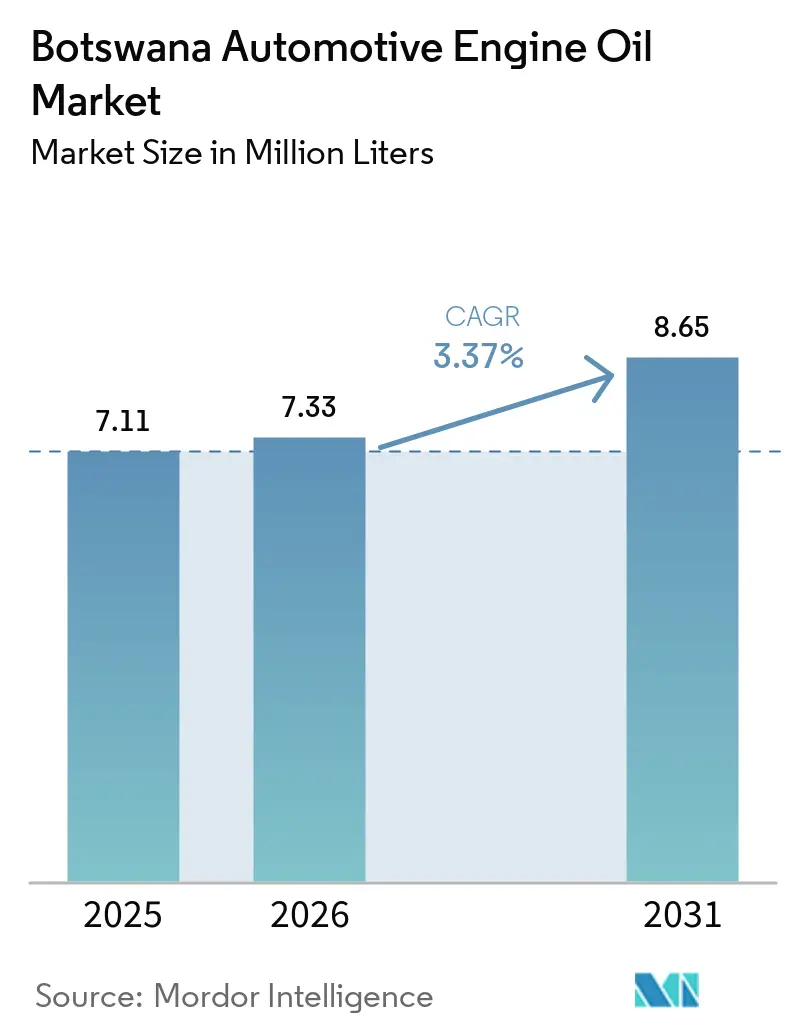

| Base Year Market Size (2025) | 7.11 Million liters |

| Market Volume (2026) | 7.33 Million liters |

| Market Volume (2031) | 8.65 Million liters |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

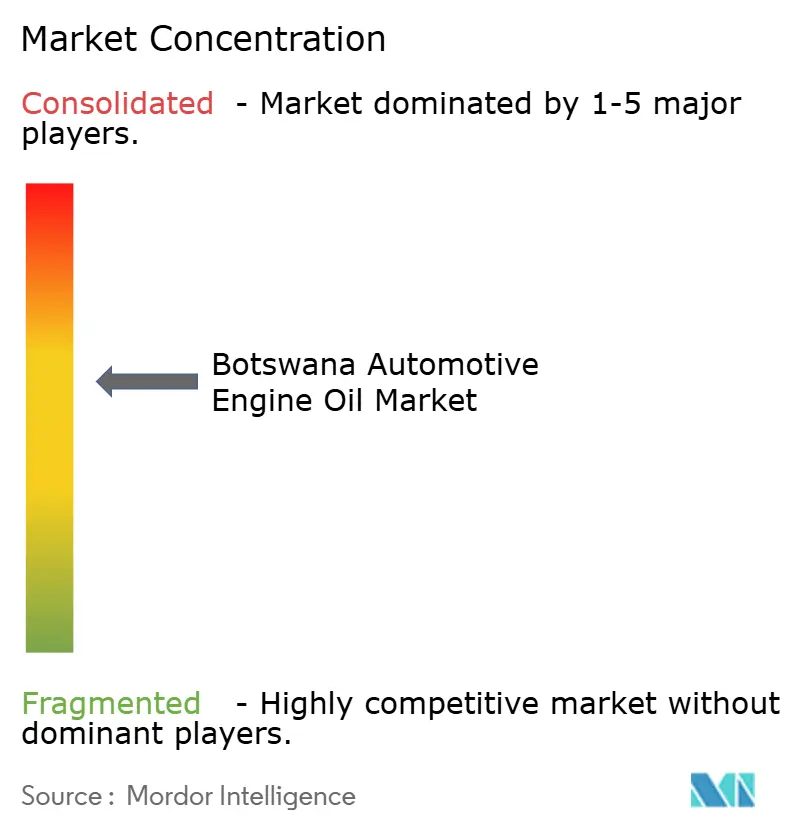

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botswana Automotive Engine Oil Market Analysis by Mordor Intelligence

The Botswana Automotive Engine Oil Market size is projected to be 7.11 million liters in 2025, 7.33 million liters in 2026, and reach 8.65 million liters by 2031 and is expected to grow at a CAGR of 3.37% from 2026 to 2031. Passenger car motor oil demand remains significant, as 77%-85% of first registrations in 2025 were used Japanese imports requiring more frequent oil top-ups due to engine aging. Mineral formulations currently dominate sales; however, synthetic grades are experiencing the fastest growth, driven by the adoption of turbocharged engines and the shift of mining fleets to long-drain specifications. Supply security remains a concern following the shutdown of South Africa’s National Petroleum Refiners (NATREF), which disrupted the supply of unleaded gasoline 93 and base oil. This has forced Botswana Oil to depend on imports from Namibia and Mozambique. Distributors offering Original Equipment Manufacturer (OEM)-approved synthetics alongside field oil-analysis services are achieving higher margins, as fleets prioritize uptime on the Trans-Kalahari and North-South corridors.

Key Report Takeaways

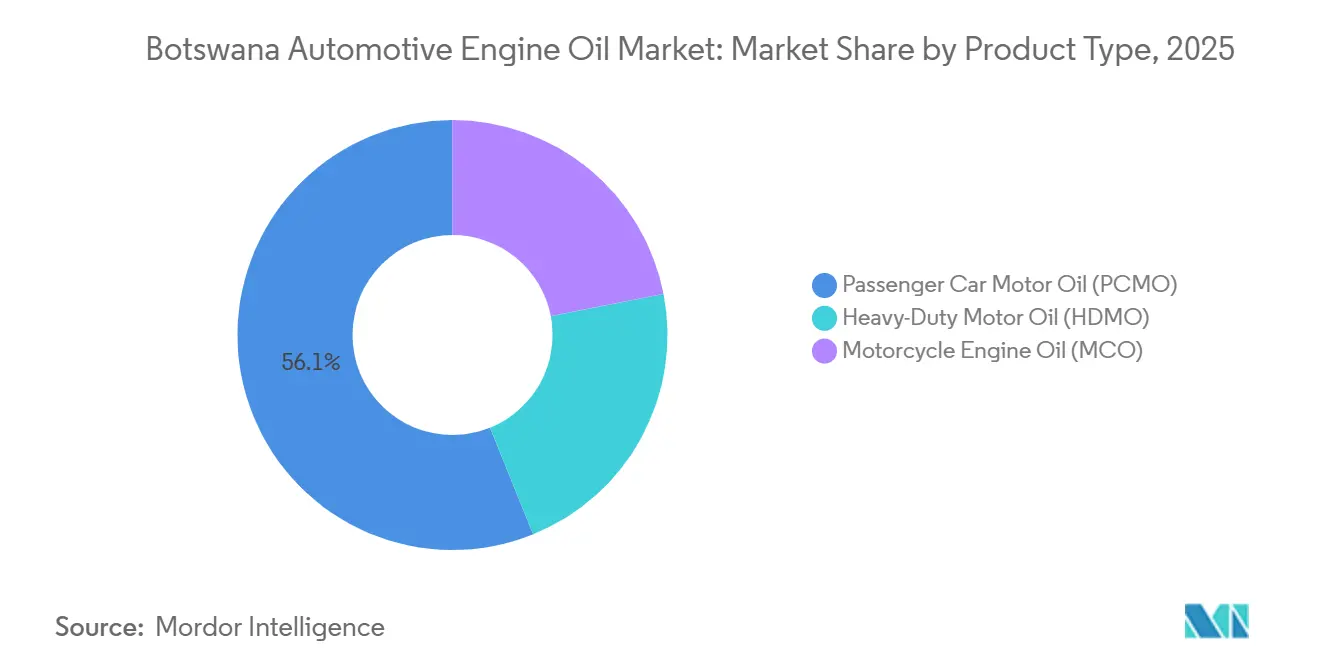

- By product type, passenger car motor oil held 56.12% of the Botswana automotive engine oil market share in 2025, while motorcycle engine oil is set to advance at a 3.42% CAGR through 2031.

- By base stock type, mineral oil commanded 68.02% of the Botswana automotive engine oil market share in 2025, while synthetic oil is expected to record the fastest 3.81% CAGR through 2031.

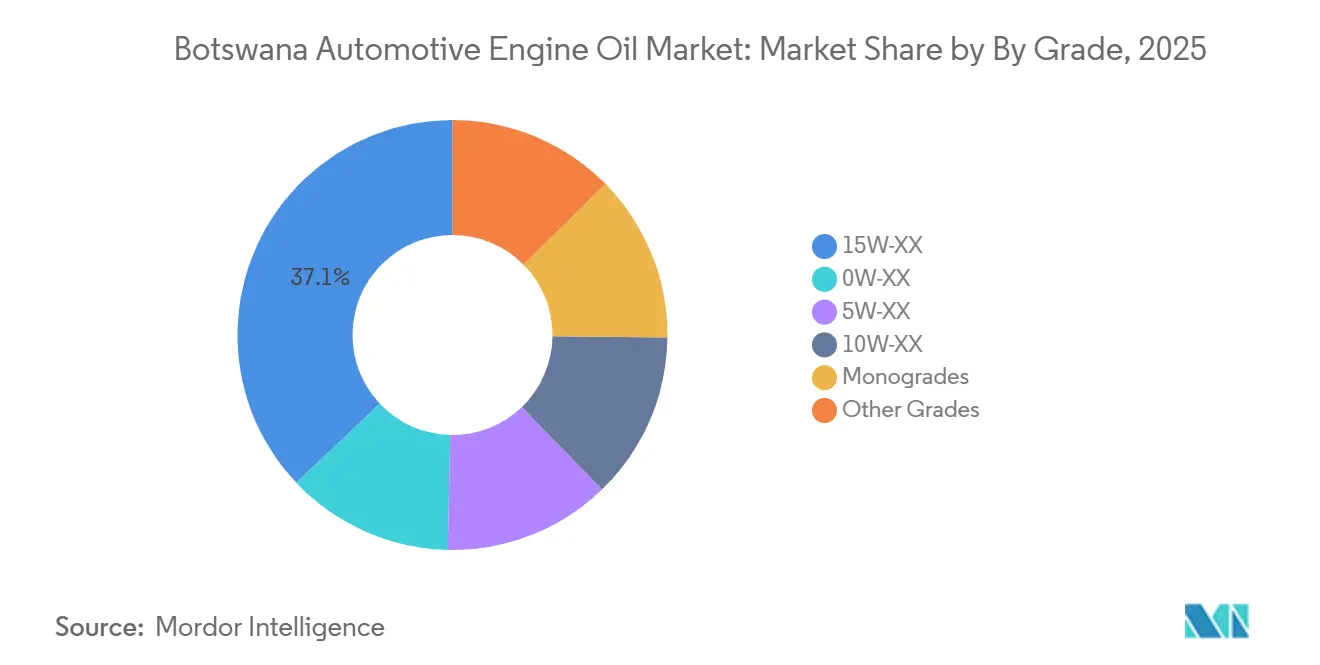

- By grade, 15W-XX captured 37.05% of the Botswana automotive engine oil market share in 2025, while the 5W-XX grade is set to rise at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Botswana Automotive Engine Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing average vehicle age in Botswana | +0.9% | National, concentrated in Gaborone and Francistown | Medium term (2–4 years) |

| Growth in vehicle parc and used-vehicle imports | +0.8% | National, with spillover to SADC cross-border routes | Short term (≤ 2 years) |

| Expansion of mining and cross-border logistics fleets | +1.1% | National, focused on Jwaneng, Orapa, Trans-Kalahari Corridor | Long term (≥ 4 years) |

| Rise of synthetic-ready turbocharged engines in new imports | +0.7% | National, early adopters in Gaborone and mining operators | Medium term (2–4 years) |

| Government plan for mandatory lubricant quality labeling | +0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Average Vehicle Age in Botswana

First-registration data indicate consecutive quarterly declines through 2025, with 77%-85% of imports being pre-owned Japanese vehicles that are already over ten years old. Older engines consume more oil and require frequent 15W-40 mineral oil top-ups, increasing per-vehicle lubricant demand. A projected 0.3% decline in total vehicle sales for 2026 is expected to extend replacement cycles. Workshops catering to high-mileage sedans and pickups continue to see strong demand for budget mineral oils, contributing to the growth of the Botswana automotive engine oil market despite weak new-car sales.

Growth in Vehicle Parc and Used-Vehicle Imports

While imported vehicles often include OEM manuals recommending synthetic oils, local garages frequently switch to more affordable mineral grades to reduce customer costs. This practice sustains the dominance of Group I products in the market. Additionally, the 2025 implementation of 24-hour border posts inadvertently increased customs dwell times, leading to longer idling periods for trucks and higher lubricant consumption per trip.

Expansion of Mining and Cross-Border Logistics Fleets

Debswana’s three-year lubricant tender, awarded in August 2025, covers operations at Jwaneng, Orapa, Letlhakane, and Damtshaa, highlighting ongoing heavy-duty lubricant demand under extreme field conditions of up to 40 °C. Haulers operating on the Trans-Kalahari route are increasingly adopting synthetic heavy-duty motor oils (HDMO) combined with oil analysis to extend drain intervals to 75,000-100,000 miles. While this reduces the volume of oil used per vehicle, it increases the value per liter, driving growth in the premium segment of the Botswana automotive engine oil market.

Rise of Synthetic-Ready Turbocharged Engines in New Imports

Over 60% of new SUVs and pickups in comparable African markets now feature turbocharged engines, a trend reflected in Botswana’s 2026 import mix. Turbocharged systems require 5W-30 or 0W-20 full-synthetic oils capable of withstanding high exhaust-gas temperatures. Castrol’s 2026 launch of American Petroleum Institute (API) SP-compliant GTX addresses this need, further expanding synthetic oil adoption in the Botswana automotive engine oil market. The upcoming API PC-12 upgrade, scheduled for 2027, is expected to accelerate this transition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of EVs and hybrids after 2029 | -0.4% | National, government and commercial fleets initially | Long term (≥ 4 years) |

| Counterfeit/re-refined oil circulation in informal trade | -0.5% | National, concentrated in peri-urban and rural areas | Short term (≤ 2 years) |

| OEM-approved long-drain synthetic oils reducing volume per vehicle | -0.6% | National, mining and logistics fleets leading adoption | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of EVs and Hybrids After 2029

In 2025, the government procured 33 electric buses and 20 electric SUVs under Presidential Directive CAB 5EX0/2024. However, electric vehicles (EVs) currently account for less than 1% of the total vehicle parc, according to Botswana Institute for Technology Research and Innovation[1]Botswana Institute for Technology Research and Innovation, “EV Fleet Pilot 2025,” bitri.co.bw. Limited infrastructure, with only one public charger in Gaborone, and a coal-dependent energy grid, reduces environmental incentives for EV adoption. ETH Zürich has ranked Botswana as a “lower-risk” destination for EV financing. The impact on the Botswana automotive engine oil market is expected to materialize after 2029, when the public-sector fleet begins its first drain-free operational cycles.

Counterfeit and Re-Refined Oil Circulation in Informal Trade

In 2022, Botswana Energy Regulatory Authority (BERA) seized 47,850 liters of illicit fuel, marking an 88.5% year-on-year increase. Counterfeit lubricants follow similar informal trade routes, undercutting legitimate brands by 30%-40%. This practice compromises engine reliability for end users and damages brand equity. A January 2026 confiscation of 20,000 liters in neighboring South Africa highlights the porous nature of Southern African Development Community (SADC) borders. While mandatory labeling could help address this issue, its implementation remains pending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Motor Oil (PCMO) Anchors Volume, Motorcycle Engine Oil (MCO) Accelerates

Passenger car motor oil (PCMO) represented 56.12% of the Botswana automotive engine oil market share in 2025. Heavy-duty motor oil (HDMO) drives disproportionate value because mines and corridor haulers buy in bulk under long-term tenders. Debswana’s 2025 award covers four diamond operations that each run haul trucks requiring 200-300 liters per fill, pushing HDMO toward premium synthetic oils that survive 2,000-hour duty cycles.

Motorcycle engine oil (MCO) is expected to post the fastest growth at a 3.42% CAGR through 2031 as peri-urban riders expand delivery services along Francistown-Gaborone routes. Electric two-wheelers could temper this rise after 2029, but current penetration is negligible. The Botswana automotive engine oil market size for PCMO is driven by older Japanese sedans still demanding affordable 15W-40 mineral blends, keeping workshops stocked with large-pack options.

By Base Stock Type: Synthetic Oil Gain Despite Mineral Oil Dominance

Mineral oil supplied 68.02% of the 2025 demand, yet synthetic oil is projected to advance at a 3.81% CAGR through 2031. The Botswana automotive engine oil market size tied to synthetics lifts as turbocharged imports arrive with original equipment manufacturer (OEM) long-drain requirements, and mining fleets value reduced downtime over price. Semi-synthetics occupy the midpoint, while bio-based oils remain experimental despite PETRONAS–Bosch Rexroth R&D on biodegradable hydraulic fluids.

Counterfeit risk skews heavily toward low-cost mineral grades circulating in rural areas. Branded synthetics carry International Organization for Standardization (ISO) and OEM seals that are harder to fake and easier for buyers to verify. The Botswana automotive engine oil market share for premium Group III and polyalphaolefin (PAO) formulations, therefore, expands most quickly in urban workshops and mine depots.

By Grade: Turbocharged Imports Drive 5W-XX Grade Uptake

The 15W-XX grade held 37.05% of volume in 2025, a legacy of naturally aspirated engines that dominate the aging parc. Yet 5W-XX grade is projected to advance at a 4.12% CAGR through 2031 because turbocharged SUVs arriving from Japan need lower cold-start viscosity. American Petroleum Institute (API) PC-12 rules due in 2027 will accelerate the shift, compelling distributors to stock more 5W-30 and 0W-20 synthetics.

Monograde Society of Automotive Engineers (SAE) 40 still appears in stationary compressors at mine sites, but its Botswana automotive engine oil market share is slipping as multigrades deliver better fuel economy. Zero-weight oils remain limited to luxury European cars and the small hybrid cohort.

Geography Analysis

Gaborone and Francistown generate the majority of retail and workshop sales, while Jwaneng, Orapa, Letlhakane, and Damtshaa mines underpin bulk HDMO demand. NATREF’s 2025 closure in South Africa forced Botswana Oil to draw finished lubricants through Walvis Bay and Maputo, raising landed costs amid 4.7% pula depreciation forecast for 2026. The Botswana automotive engine oil market size consequently remains sensitive to foreign-exchange swings.

Mining locales contribute concentrated, high-value consumption. Jwaneng’s fleet of Komatsu 930E haul trucks alone may account for 10%-15% of national HDMO use, given each fill exceeds 200 liters and drains stretch to 3,000 hours under synthetic programs. Oil suppliers winning these tenders secure a predictable baseline volume over three-year cycles.

The Trans-Kalahari and North-South corridors shape cross-border fleet behavior. Haulers idle longer at borders despite 24-hour operations because added customs checks slow clearance. Extended idling burns extra oil and elevates demand for premium synthetics that resist oxidation in 40 °C ambient heat, thereby scaling the Botswana automotive engine oil market in logistics nodes such as Sekoma, Kang, and Lobatse.

Competitive Landscape

The market exhibits moderate concentration, with the top five players including BP p.l.c. (Castrol), Shell plc, TotalEnergies, Botswana Oil, and Puma Energy. FUCHS invested EUR 26 million upgrading its Isando plant in February 2025, growing regional capacity 40% and tightening delivery times to Botswana through its August 2025 Gqeberha hub[2]FUCHS, “Isando Plant Expansion Press Release Feb 2025,” fuchs.com. These players combine ISO 9001 and ISO 14001 certifications with field engineering support, positioning them favorably once compulsory labeling arrives.

Strategic maneuvers intensify. Saudi Aramco evaluated a USD 6-8 billion bid for BP’s Castrol in March 2025, a move that could integrate Castrol with Aramco’s 2023 Valvoline purchase to build a pan-African lubricant platform targeting the Botswana automotive engine oil market. Cummins advances service-linked offerings such as OilGuard, bundling telematics and lab analytics to guarantee 75,000-mile drains, shifting value capture from commodity liters to uptime assurance.

Counterfeit infiltration remains the biggest competitive headache. Adams & Adams intercepted 20,000 liters of fake oil in South Africa in January 2026, and BERA’s 88.5% seizure spike in 2022 indicates widening risk locally. Brands that supply tamper-proof QR labeling and partner with BERA on spot testing will likely secure incremental Botswana automotive engine oil market share as enforcement tightens.

Botswana Automotive Engine Oil Industry Leaders

BP p.l.c. (Castrol)

Botswana Oil

TotalEnergies

Puma Energy

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Botswana Energy Regulatory Authority (BERA), in partnership with Botswana Oil, quarantined over 3 million liters of unleaded petrol (ULP95) imported from Namcor. The fuel was suspected to have contained lead and manganese additives at levels that violated local standards.

- August 2025: BP p.l.c. (Castrol) launched its next-generation GTX 5W-30 and 10W-40 engine oils in Botswana. These products were formulated to enhance vehicle durability and address increasing fuel expenses for local drivers.

Botswana Automotive Engine Oil Market Report Scope

Automotive engine oil minimizes friction, cools engine components, and prevents sludge accumulation. Key considerations include viscosity grades, such as 5W-30, and compliance with API or ACEA specifications, such as API SP.

The Botswana Automotive Engine Oil Market is segmented into product type, base stock type, and grade. By product type, the market is segmented into passenger car motor oil (PCMO), heavy-duty motor oil (HDMO), and motorcycle engine oil (MCO). By base stock type, the market is segmented into mineral, semi-synthetic, synthetic, and bio-based. By grade, the market is segmented into 15W-XX, 0W-XX, 5W-XX, 10W-XX, monogrades, and other grades. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| Passenger Car Motor Oil (PCMO) |

| Heavy-Duty Motor Oil (HDMO) |

| Motorcycle Engine Oil (MCO) |

| Mineral |

| Semi-Synthetic |

| Synthetic |

| Bio-Based |

| 15W-XX |

| 0W-XX |

| 5W-XX |

| 10W-XX |

| Monogrades |

| Other Grades |

| By Product Type | Passenger Car Motor Oil (PCMO) |

| Heavy-Duty Motor Oil (HDMO) | |

| Motorcycle Engine Oil (MCO) | |

| By Base Stock Type | Mineral |

| Semi-Synthetic | |

| Synthetic | |

| Bio-Based | |

| By Grade | 15W-XX |

| 0W-XX | |

| 5W-XX | |

| 10W-XX | |

| Monogrades | |

| Other Grades |

Key Questions Answered in the Report

What is the size of the Botswana automotive engine oil market?

The Botswana Automotive Engine Oil Market size is projected to be 7.11 million liters in 2025, 7.33 million liters in 2026, and reach 8.65 million liters by 2031 and is expected to grow at a CAGR of 3.37% from 2026 to 2031.

Which product type leads volume in 2025?

Passenger car motor oil holds 56.12% of the 2025 volume.

What is driving synthetic oil growth in Botswana?

Turbocharged vehicle imports and mining fleets seeking longer drain intervals are pushing synthetics, which expand at a 3.81% CAGR to 2031.

How vulnerable is the market to counterfeit lubricants?

Informal trade remains a major issue, with BERA reporting an 88.5% surge in illicit fuel seizures and legal raids in South Africa, uncovering 20,000 liters of fake oil in 2026.

Page last updated on: