East Asia Automotive Engine Oils Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

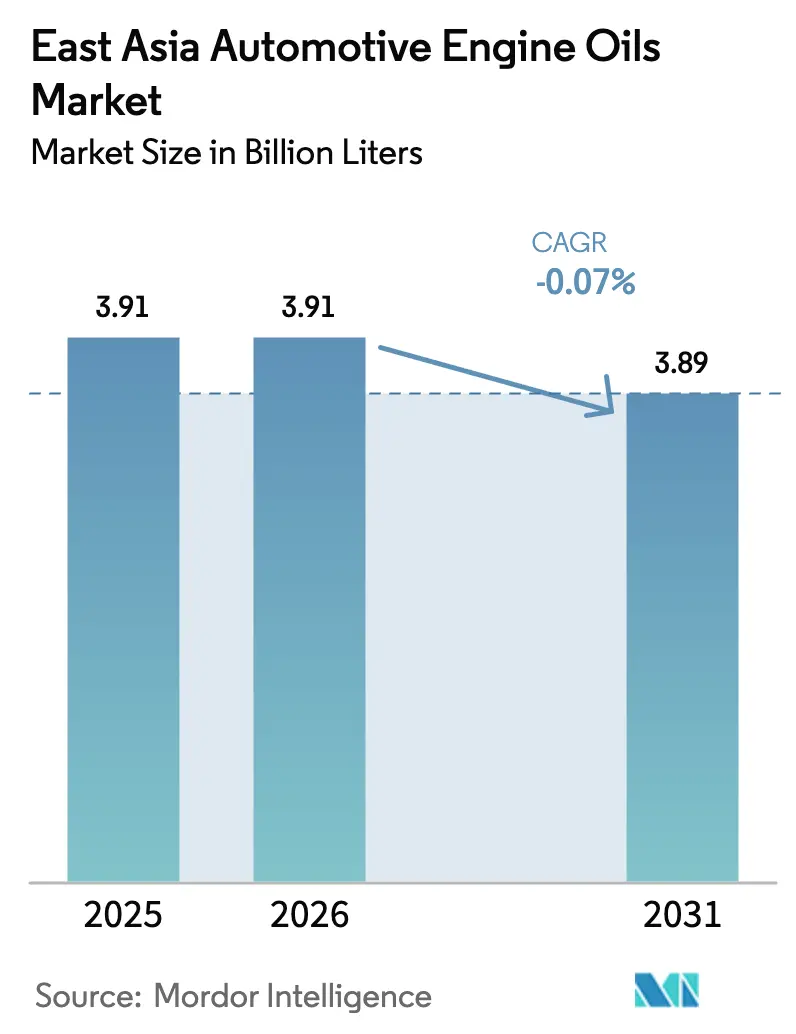

| Base Year Market Size (2025) | 3.91 Billion liters |

| Market Volume (2026) | 3.91 Billion liters |

| Market Volume (2031) | 3.89 Billion liters |

| Growth Rate (2026 - 2031) | -0.07% CAGR |

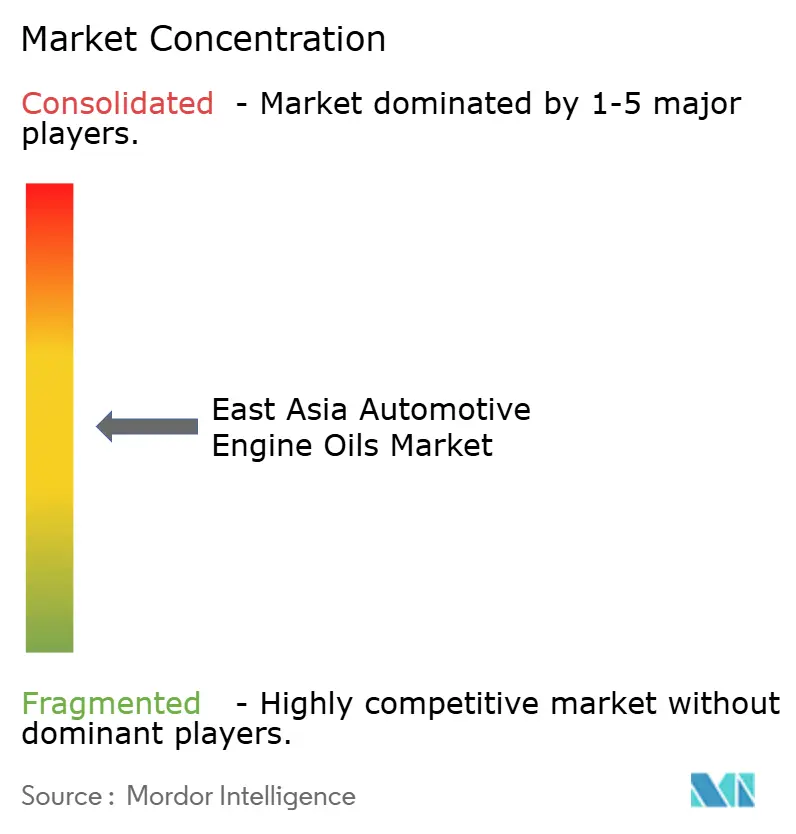

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

East Asia Automotive Engine Oils Market Analysis by Mordor Intelligence

East Asia Automotive Engine Oils Market size in 2026 is estimated at 3.91 billion liters, growing from 2025 value of 3.91 billion liters with 2031 projections showing 3.89 billion liters, growing at -0.07% CAGR over 2026-2031. Stagnant aggregate growth conceals deep structural changes as battery-electric vehicles gain market share and reduce lubricant consumption in major urban centers. The market’s high concentration in China keeps overall volumes sizeable, yet it also amplifies exposure to policy shifts that accelerate electrification. Meanwhile, niche opportunities emerge in motorcycles, light commercial vehicles, and marine applications where internal-combustion engines remain favored. Competitive pressures intensify as operators confront shrinking volumes, rising feedstock costs, and supply-chain volatility linked to the region’s heavy reliance on imported premium base oils. To defend profitability, players are pivoting toward synthetic grades, forging closer OEM alliances, and diversifying into faster-growing geographies such as Taiwan.

Key Report Takeaways

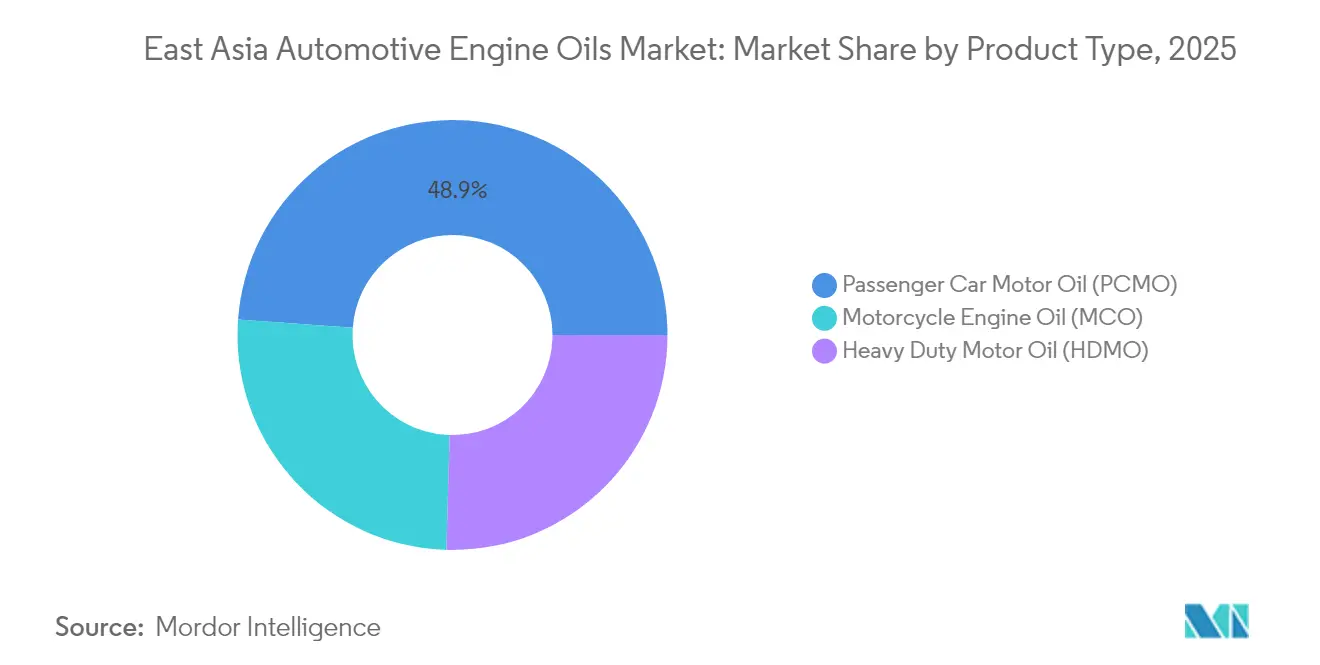

- By product type, passenger car motor oil held 48.85% of the East Asia automotive engine oils market share in 2025, while motorcycle engine oil is set to grow at the fastest 0.93% CAGR to 2031.

- By base stock, mineral oils accounted for 61.85% share of the East Asia automotive engine oils market size in 2025, with synthetic grades projected to expand at a 1.05% CAGR between 2026 and 2031.

- By geography, China captured 73.65% of the East Asia automotive engine oils market in 2025, and Taiwan is forecast to record the highest 0.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

East Asia Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger-vehicle parc recovery and replacement cycles | +0.5% | China, Japan, South Korea | Medium term (2-4 years) |

| Large two-wheeler parc sustaining MCO demand | +0.3% | Taiwan, urban China, South Korea | Long term (≥ 4 years) |

| Expansion of LCV and last-mile fleets | +0.2% | China e-commerce hubs, Japan logistics corridors | Short term (≤ 2 years) |

| Industrial and port growth boosting HDMO/marine | +0.1% | China coastal areas, South Korea shipyards | Medium term (2-4 years) |

| OEM push for low-viscosity fuel-saving oils | +0.15% | Japan premium, China tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Passenger-Vehicle Parc Recovery and Replacement Cycles

Maintenance deferrals during the pandemic created pent-up service demand that surfaced in 2024 as owners rushed to protect aging vehicles. China’s passenger-car parc increased, a trend that leads to higher per-vehicle oil consumption as older engines require thicker formulations for wear protection. In Japan, consumers prefer to extend the life of their vehicles over replacement, which reinforces demand for premium synthetic oils that enable quieter operation and lower emissions. Replacement-cycle momentum provides a two- to four-year buffer, cushioning the East Asia automotive engine oils market against the wave of electrification in urban areas. Rural and suburban drivers, who are less served by charging infrastructure, tend to keep their internal-combustion vehicles longer, thereby prolonging the need for lubricants.

Large Two-Wheeler Parc Sustaining MCO Demand

Two-wheelers remain a cost-effective mode of transportation in congested Asian cities. Taiwan’s motorcycle density underpins a stable pool of engines that need lubrication every 3,000–5,000 kilometers. In China, food-delivery platforms operate through bikes, each clocking high idle times and frequent cold starts that accelerate oil degradation. South Korea’s recreational touring culture props up high-performance synthetic demand for weekend riding. Because electric scooters struggle with range and battery longevity, internal-combustion two-wheelers retain popularity, helping the East Asia automotive engine oils market counterbalance losses in passenger cars.

Expansion of LCV and Last-Mile Fleets Shortening Drain Intervals

E-commerce parcel volume in China continues to rise, serviced by light commercial vehicles (LCVs) that idle and restart frequently in dense traffic. Such duty cycles shorten oil change intervals to 5,000-7,500 kilometers, effectively doubling the lubricant demand per vehicle compared to standard passenger use. Japan’s aging population is driving the growth of grocery and medicine home-delivery fleets, while South Korea’s same-day shipping race intensifies urban van mileage. Fleet operators adopt predictive maintenance apps that flag viscosity drops, prompting more timely oil changes and safeguarding engines, thereby sustaining volume despite overall vehicle efficiency gains.

Industrial and Port Growth Lifting HDMO/Marine Demand

Manufacturing revival and port capacity additions in coastal China and South Korea require heavy-duty motor oil (HDMO) for cranes, trucks, and auxiliary ship systems. China’s industrial production expanded in 2024. LNG carrier and container-vessel orders at Korean shipyards revive marine lubricant off-take, offsetting automotive declines. Infrastructure tied to the Belt and Road Initiative fuels demand for hydraulic and gear oils used in construction equipment. These industrial segments yield higher margins and longer contracts, providing lubricant suppliers with a hedge against declining passenger-vehicle sales.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV and e-2W uptake in cities | −0.6% | Shenzhen, Shanghai, Seoul, Tokyo | Short term (≤ 2 years) |

| Extended-drain synthetics and longer service | −0.5% | Japan and South Korea premium segments, China luxury | Medium term (2-4 years) |

| Import dependence for select base stocks | −0.25% | China, Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV and e-2W Uptake in Urban Clusters

Battery-electric vehicles accounted for a significant portion of China’s 2024 new-vehicle sales[1]China Association of Automobile Manufacturers, “China Auto Industry Statistics 2024,” caam.org.cn. Urban adoption strikes hardest at high-frequency oil-change segments, disproportionately eroding lubricant volume. Seoul and Tokyo accelerate zero-emission mandates for taxis and municipal fleets, while local subsidies cut the total cost of ownership gaps. Electric two-wheelers gain share in short-haul personal mobility, removing small-engine motorcycles from service lanes. The substitution effect compounds yearly, shrinking the East Asia automotive engine oils market base in the most profitable territories.

Extended-Drain Synthetics and Longer OEM Service Intervals

The wide adoption of high-quality synthetics reduces oil changes from three per year to one or two, thereby trimming per-vehicle consumption. Premium manufacturers market drain intervals of 20,000 kilometers, backed by advanced additive chemistries that resist oxidation. Consumers appreciate lower maintenance hassle, reinforcing the shift. Because all brands utilize extended drains, suppliers cannot offset lost liters by gaining market share. The restraint weighs heavily on volumes but also raises per-liter values, nudging producers to chase margins over tonnage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Faces MCO Growth

Passenger car motor oil commanded 48.85% of the 2025 volume in the East Asia automotive engine oils market, thanks to China’s huge passenger fleet. The segment’s outlook dims as battery-electric cars cannibalize new-vehicle sales, particularly in tier-1 cities. Nevertheless, aging internal-combustion vehicles outside urban cores still require traditional 5W-30 oils, slowing the pace of decline. In contrast, motorcycle engine oil is projected to post a 0.93% CAGR to 2031, buoyed by Taiwan’s dense bike ownership and China’s burgeoning delivery-rider economy. MCO premiumization gains momentum as enthusiasts and delivery platforms specify synthetic blends for better clutch performance and thermal stability. The PCMO segment remains critical for scale but is shifting toward low-viscosity synthetics, while MCO offers modest volume upside with healthy margins.

By Base Stock: Synthetic Momentum Challenges Mineral Dominance

Mineral oils retained 61.85% of 2025 volume, dominating cost-sensitive rural and high-mileage taxi operators. However, synthetic grades are expected to grow at a 1.05% CAGR as OEMs tighten fuel-economy targets and consumers seek longer drain intervals. Semi-synthetics bridge the affordability gap, while bio-based lubricants remain nascent but gather regulatory support. Group III output in South Korea expands to serve regional demand, yet persistent import reliance keeps pricing at a premium.

Geography Analysis

China accounted for 73.65% of the regional volume in 2025; however, the steepest decline risk stems from its aggressive electrification roadmap. BEVs' new-car sales in 2025 are expected to erode incremental oil demand in the country’s wealthiest markets. Rural provinces with less charging infrastructure still favor internal-combustion vehicles, offering a buffer. China’s base-oil deficit adds cost pressure. Lubricant producers consolidate as margins tighten and smaller blenders exit the market.

Japan and South Korea together hold a significant share. Both exhibit flat volumes but high synthetic penetration, supporting superior per-liter pricing. Japanese OEMs set global lubricant benchmarks, fostering export opportunities for approved formulations. South Korea’s integrated refining players leverage Group III dominance to serve both domestic and Chinese demand, partially offsetting contracting local sales.

Taiwan posts the fastest growth rate of 0.66% through 2031. The island’s unparalleled motorcycle density and resilient semiconductor and shipping sectors sustain demand. Mountainous terrain and inter-city distances limit the range of electric scooters, keeping combustion bikes relevant. Taiwan’s open trade policy eases feedstock sourcing, while local blenders ramp up premium MCO lines to capture enthusiast upgrades.

Competitive Landscape

The East Asia automotive engine oils market is moderately fragmented. Global majors align with leading regional firms. Shell leverages its global Pennzoil-based synthetic technology to win OEM factory-fill contracts in China and Korea[2]Shell plc, “Lubricants Business Strategy Update 2024,” shell.com . ExxonMobil promotes Mobil 1 extended-drain packages in Japan’s performance-car circles. Strategy pivots center on higher-margin synthetics, niche specialty products, and aftermarket digitalization. Leading firms are piloting AI-enabled oil-as-a-service models, offering fixed-price subscriptions bundled with telematics-verified drain alerts. Base-oil vertical integration and long-term offtake contracts mitigate raw-material volatility. Regional challengers exploit white space in bio-lubricants and marine blends, leveraging local regulatory incentives. Mergers and acquisitions activity intensifies as contraction spurs economies of scale.

East Asia Automotive Engine Oils Industry Leaders

China Petrochemical Corporation

China National Petroleum Corporation

Shell plc

ENEOS Corporation

ExxonMobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. began exploring a sale of its Castrol lubricants unit, valued up to USD 10 billion, as part of a larger USD 20 billion divestment program slated for completion by 2027.

- November 2024: PTT Lubricants launched EVOTEC Technology engine oils in Taiwan, targeting extended service life and improved fuel efficiency across the motorcycle and passenger car segments.

East Asia Automotive Engine Oils Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| China |

| South Korea |

| Japan |

| Taiwan |

| Others (Mangolia, Hongkong) |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | China | |

| South Korea | ||

| Japan | ||

| Taiwan | ||

| Others (Mangolia, Hongkong) | ||

Key Questions Answered in the Report

What is the size of the East Asia automotive engine oil market in 2026?

The East Asia automotive engine oil market size is expected to reach 3.91 billion liters by 2026.

What is the growth outlook through 2031?

Volume is forecast to decline slightly to 3.89 billion liters, implying a -0.07% CAGR over 2026-2031.

Which segment grows fastest in the next five years?

Motorcycle engine oil leads with a projected 0.93% CAGR, buoyed by urban delivery fleets and dense two-wheeler ownership.

Why are synthetics gaining share?

OEM mandates for low-viscosity oils, longer drain intervals, and fuel economy gains drive demand for synthetic base stocks.

How will electrification affect lubricant suppliers?

Battery-electric vehicle uptake in tier-1 cities accelerates volume contraction, forcing suppliers to pivot toward premium segments and industrial niches.

Which country in East Asia shows the best growth potential?

Taiwan tops the growth chart at a 0.66% CAGR, driven by resilient motorcycle ownership and expanding industrial demand.

Page last updated on: