Ethiopia Automotive Engine Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

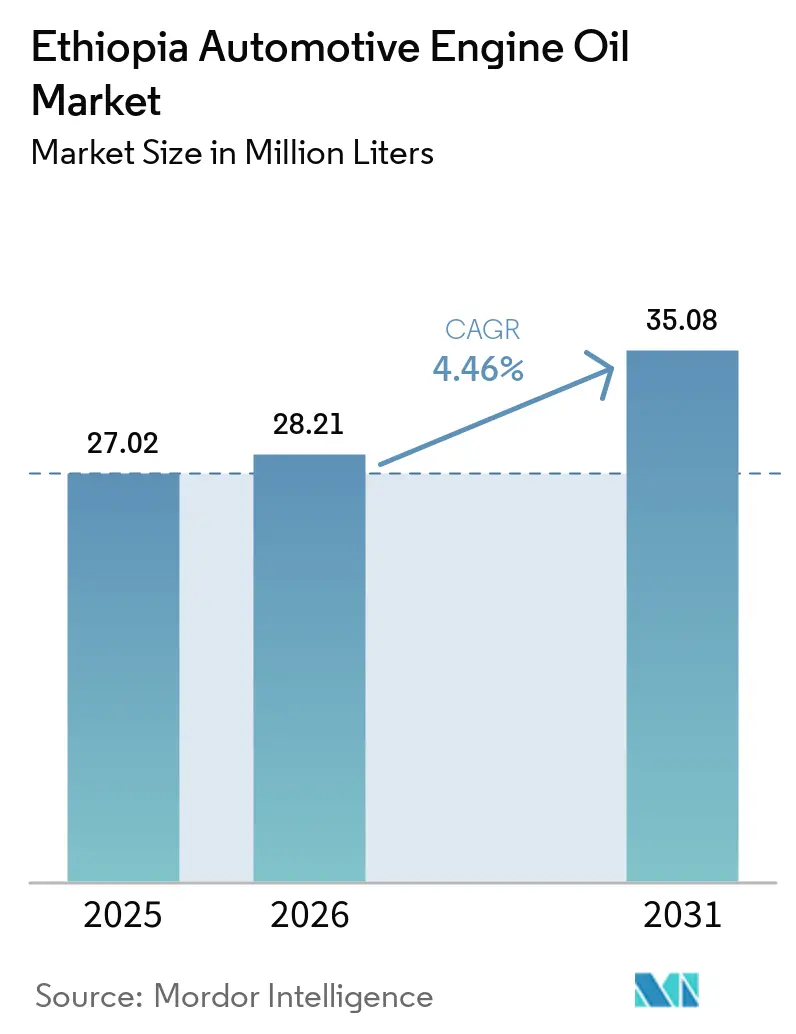

| Base Year Market Size (2025) | 27.02 Million liters |

| Market Volume (2026) | 28.21 Million liters |

| Market Volume (2031) | 35.08 Million liters |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethiopia Automotive Engine Oil Market Analysis by Mordor Intelligence

The Ethiopia Automotive Engine Oil Market size is expected to grow from 27.02 million liters in 2025 to 28.21 million liters in 2026 and is forecast to reach 35.08 million liters by 2031 at 4.46% CAGR over 2026-2031. Even with the swift rise of electric vehicles, the demand for affordable mineral grades remains robust. This is largely due to an aging fleet, heavily reliant on imports, and the challenging road conditions that necessitate more frequent maintenance. The Addis-Djibouti corridor, which handles a significant portion of Ethiopia’s external trade, is expanding the market for premium synthetic lubricants, which are known to minimize vehicle downtime. However, challenges loom: foreign-exchange shortages and unexpected fuel supply disruptions are squeezing profit margins, pushing some traders towards counterfeit lubricants. As local brands ramp up their distribution efforts, international giants are countering by introducing electric vehicle charging services and implementing anti-counterfeiting packaging, intensifying the competitive landscape.

Key Report Takeaways

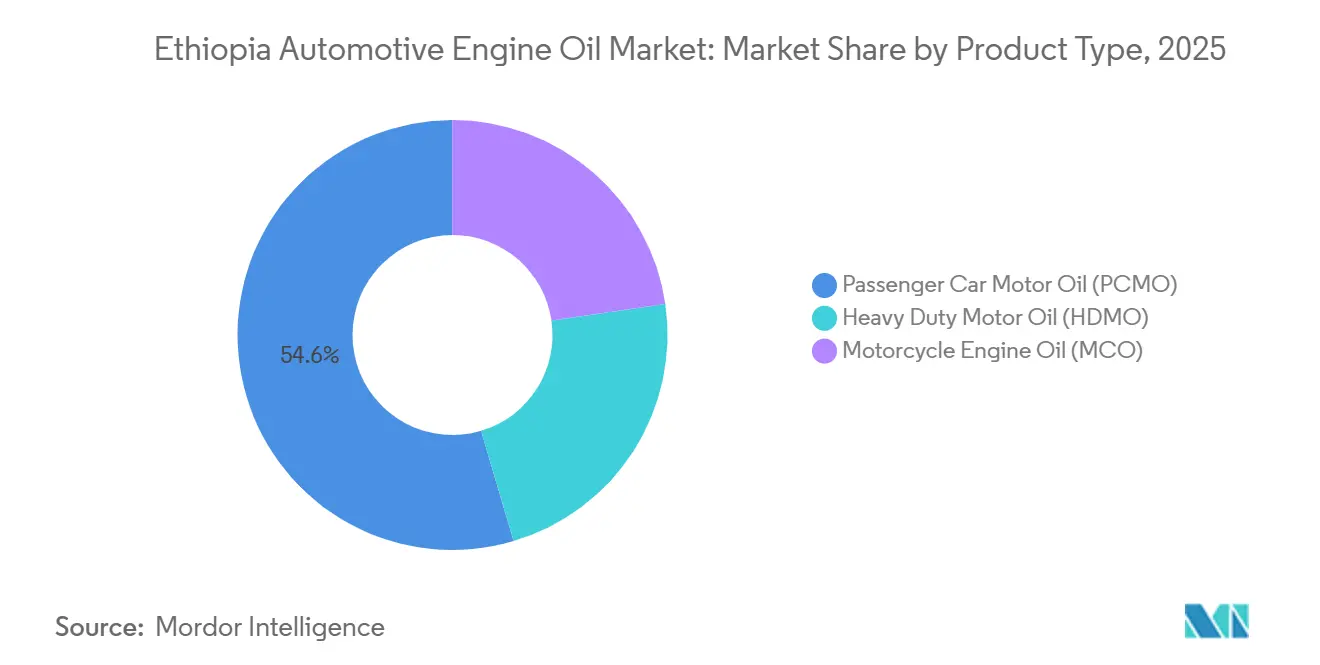

- Passenger Car Motor Oil led with a 54.59% share of the Ethiopia automotive engine oil market size in 2025. Motorcycle Engine Oil is projected to post the fastest 5.12% CAGR through 2026 to 2031, reflecting rapid last-mile-delivery growth.

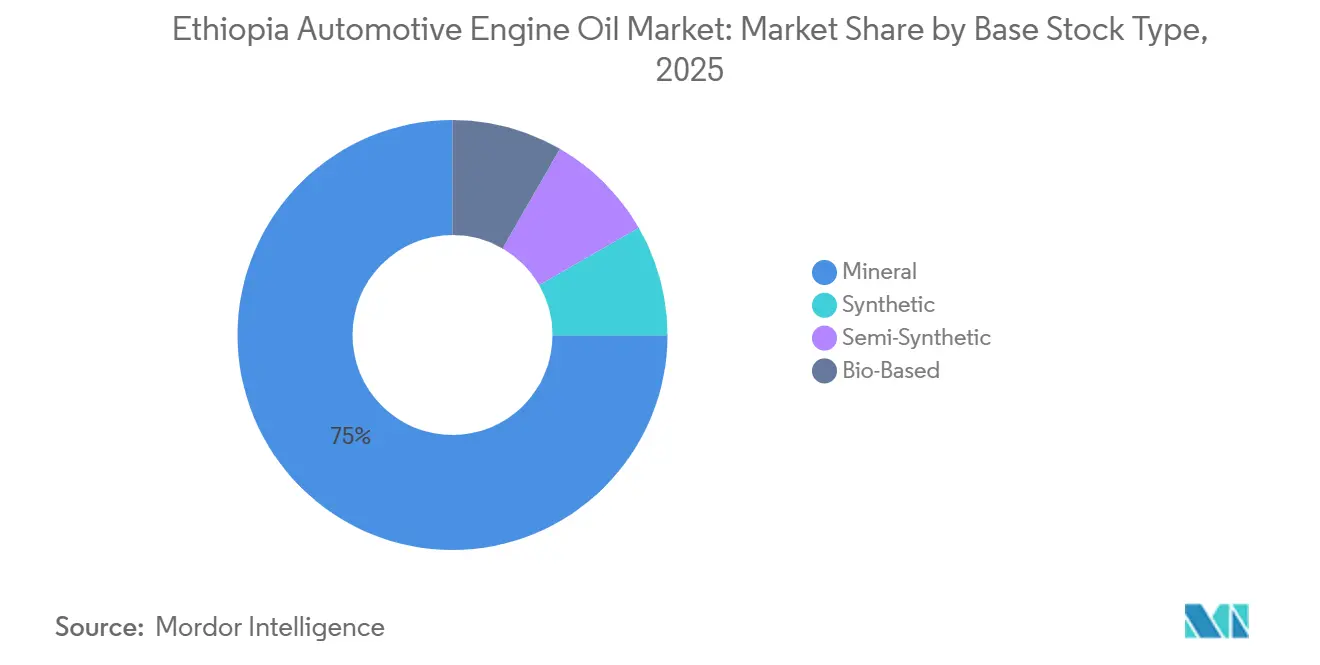

- Mineral formulations accounted for 74.98% of the Ethiopia automotive engine oil market share in 2025, while synthetics are advancing at a 5.68% CAGR between 2026 to 2031on the Addis–Djibouti logistics corridor.

- 15W-XX led with a 42.26% share of the Ethiopia automotive engine oil market size in 2025. 5W-XX is projected to post the fastest 5.01% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ethiopia Automotive Engine Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in used-vehicle imports is aging the national fleet | +0.90% | National, concentrated in Addis Ababa and Oromia | Medium term (2-4 years) |

| Expansion of public transport & logistics fleets on the Addis-Djibouti corridor | +0.70% | National, with primary impact along the Addis Ababa-Dire Dawa-Djibouti route | Medium term (2-4 years) |

| Construction boom raising HDMO demand in earth-moving equipment | +0.60% | National, early gains in Gode (Somali Region), Addis Ababa, and industrial park zones | Long term (≥ 4 years) |

| Industrial-park program accelerating commercial-vehicle kilometers | +0.50% | National, concentrated in 10 SEZ cities, including Adama, Hawassa, Kilinto, Mekelle | Long term (≥ 4 years) |

| Last-mile motorcycle growth in Addis & secondary cities | +0.40% | Urban centers, primarily Addis Ababa, Jimma, Mojo, and Bishoftu | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Used-Vehicle Imports Aging the National Fleet

In Ethiopia, a significant majority of annual vehicle additions are second-hand, predominantly Toyotas arriving via Djibouti. These older engines, often subjected to dusty road conditions, frequently require oil changes, driving demand for mineral-grade engine oils with higher viscosity. While imports of new internal combustion engine cars have ceased, the influx of used vehicles continued until foreign exchange scarcity significantly reduced their value. Consequently, even with a rise in electric vehicle numbers, the aging fleet bolsters the volumes in Ethiopia's automotive engine oil market. Distributors focusing on high-viscosity multi-grades are capturing a larger share in smaller garages, where pricing often overshadows original equipment manufacturer specifications.

Expansion of Public-Transport & Logistics Fleets on the Addis-Djibouti Corridor

Once completed, the expressway between Mieso and Dire Dawa is set to significantly reduce truck transit times. Currently, a large number of heavy trucks ply the route, frequently exceeding load limits, which heightens maintenance demands[1]World Bank, “Horn of Africa Initiative Corridor Project,” documents1.worldbank.org. Once completed, the expressway between Mieso and Dire Dawa, supported by the World Bank, is set to significantly reduce truck transit times. Currently, a large number of heavy trucks ply the route, frequently exceeding load limits, which heightens maintenance demands. To maximize road time, fleet operators are increasingly turning to long-drain synthetic oils, propelling the premium segment of Ethiopia's automotive engine oil market. Suppliers forming partnerships with emerging truck stops and freight terminals along the corridor stand to gain both captive volumes and reduced last-mile costs.

Construction Boom Raising HDMO Demand in Earth-Moving Equipment

Excavators, dumpers, and support trucks are mobilizing for large-scale projects such as a refinery and a urea plant. Additionally, road projects targeting significant expansion are further driving the demand for heavy-duty motor oil. Contractors are gravitating towards engine oil grades known for their ability to manage high loads and extended idle hours. As these megaprojects transition to operational phases, the ensuing maintenance cycles will solidify the demand for heavy-duty motor oil. Suppliers strategically positioning bulk storage near project sites and offering used-oil analysis services are poised for a competitive advantage.

Industrial-Park Program Accelerating Commercial-Vehicle Kilometers

Several industrial parks have been designated as Special Economic Zones, attracting foreign direct investment with incentives like customs one-stop shops and subsidized utilities. As freight traffic rises within these parks, so does the consumption of lubricants for trucks and forklifts. Notably, the pharmaceutical cluster in Kilinto has attracted significant investments. Establishing blending or packaging facilities within Special Economic Zones can significantly reduce lead times and circumvent congestion at Djibouti port, a vital consideration in Ethiopia's automotive engine oil landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign-exchange controls are disrupting lubricant import flows | -0.80% | National, acute for importers in the Addis Ababa and Djibouti corridor | Short term (≤ 2 years) |

| High price sensitivity curbs uptake of synthetics | -0.50% | National, most pronounced in a fragmented after-sales channel | Medium term (2-4 years) |

| Counterfeit/sub-standard lubricants in informal channels | -0.30% | National, concentrated in urban independent garages and rural retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Foreign-Exchange Controls Disrupting Lubricant Import Flows

In March, a fuel shortfall significantly reduced daily diesel supply, prompting authorities to ration fuel to priority fleets. While a central-bank auction provided some liquidity relief, certain suppliers found themselves waiting several months for hard currency[2]Birr Metrics, “News Archive,” birrmetrics.com . As a result, the Ethiopian automotive engine oil market grapples with extended lead times and elevated landed costs. This situation is steering buyers towards gray-market imports, jeopardizing brand equity. However, once the Gode refinery comes online, local blending with its base stocks could alleviate forex-related challenges.

High Price Sensitivity Curbs Uptake of Synthetics

With government-regulated low margins, suppliers depend heavily on turnover for profitability. Small garages favored mineral engine oils priced at lower rates. While premium synthetic oils are gaining popularity, especially among urban fleets mindful of total ownership costs, mid-tier semi-synthetic oils in smaller packs are bridging the affordability gap, broadening the customer base for Ethiopia's automotive engine oil industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Offset by MCO Velocity

Passenger Car Motor Oil held 54.59% of volume in 2025, anchored by a significant number of cars, predominantly aging imports. Despite the ban on ICE imports, Ethiopia's automotive engine oil market, particularly for PCMO, remains robust due to harsh road conditions that shorten drain intervals. Heavy Duty Motor Oil benefits from road and refinery megaprojects, which mobilize extensive earth-moving fleets. Meanwhile, Motorcycle Engine Oil is projected to see growth at 5.12% through 2026 to 2031 as formal delivery platforms scale in Addis and secondary cities.

E-two-wheelers threaten future mineral-oil volumes, yet the installed ICE base keeps near-term demand solid. Suppliers that couple MCO with brake fluids and chain lubes deepen wallet share. PCMO resilience hinges on slow fleet turnover, high used-car taxes, and limited credit, while MCO trajectory reflects the balance between delivery growth and e-mobility penetration in the Ethiopia automotive engine oil market.

By Base Stock Type: Mineral Entrenchment Challenged by Synthetic Momentum

Mineral grades captured 74.98% in 2025 as cost-conscious garages stick to 20W-50 and 15W-40. Synthetics are expanding at 5.68% through 2026 to 2031 as corridor fleets chase long-drain savings. The Ethiopia automotive engine oil market size for synthetics should widen once local blending trims import costs.

Semi-synthetics offer a price-performance bridge, while bio-based oils stay niche, limited to sensitive eco-zones. Education campaigns on total cost of ownership and OEM approvals can accelerate mineral-to-synthetic shifts, raising the overall Ethiopia automotive engine oil market value without sacrificing volumes.

By Grade: 15W-XX Ubiquity Versus 5W-XX OEM Alignment

The 15W-XX family commanded 42.26% in 2025, balancing cold-start flow with high-temperature film strength across Ethiopia’s altitude extremes. 10W-XX and single grades cater to vintage engines and stationary machinery. The 5W-XX category is growing at 5.01% through 2026 to 2031. Lower-viscosity multi-grades will keep gaining as Gode refinery output enables local blending of higher-quality base stocks. Suppliers that secure API SP and ACEA approvals and train mechanics on grade selection will capture a share in the evolving Ethiopia automotive engine oil market.

Geography Analysis

Addis Ababa hosts a significant portion of the nation's petrol stations, establishing itself as the central lubricant hub and a key indicator of trends in Ethiopia's automotive engine oil market. Oromia follows closely, serving a considerable share of the fleet, supported by the development of industrial parks in areas such as Jimma, Mojo, and Bishoftu. Logistics activities along the Addis-Djibouti corridor drive demand into truck stops and highway service centers, where high-quality heavy-duty motor oil volumes are concentrated.

The Somali Region is emerging as a new demand center with the construction of the Gode refinery, which is attracting equipment fleets and creating potential for local blending in the future. Special Economic Zones in locations like Adama, Hawassa, Kilinto, Mekelle, and Kombolcha are enhancing regional freight loops, leading to increased lubricant throughput. Future fuel-allocation policies, such as prioritizing commercial fleets during shortages, are expected to continue shaping geographic sales patterns in Ethiopia's automotive engine oil market.

Competitive Landscape

The Ethiopia Automotive Engine Oil Market is moderately concentrated. Mid-tier challengers such as Oil Libya and Kobil leverage local blending plants to offset forex volatility and undercut imports. Anti-counterfeiting tech QR codes, tamper-evident seals, and revamped packaging have become table stakes after licensed suppliers lost volumes to gray-market oils. Emerging disruptors include Dodai’s battery-swap network and ExxonMobil’s new aviation-lubricant foothold via a five-year Ethiopian Airlines contract.

Ethiopia Automotive Engine Oil Industry Leaders

TotalEnergies

Shell plc

BP p.l.c. (Castrol)

Chevron Corporation (Caltex)

Puma Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ethiopian Airlines, with the help of Aeroservices, had secured a five-year deal to source aviation lubricants from ExxonMobil. This move is poised to boost the demand for high-performance lubricants in Ethiopia's aviation sector, potentially reverberating throughout the country's broader automotive lubricant market.

- January 2026: Ethio Telecom sought expressions of interest (EOI) from GPS-enabled motorcycle delivery partners for its Zemen GEBEYA logistics service. This development is expected to positively impact the Ethiopia Automotive Engine Oil Market, as increased demand for motorcycles in logistics operations could drive the need for regular engine maintenance and oil consumption.

Ethiopia Automotive Engine Oil Market Report Scope

Ethiopia Automotive Engine Oil refers to lubricants specifically formulated for vehicles operating within Ethiopia’s diverse climate and road conditions. It reduces friction, prevents wear, and ensures smooth engine performance in passenger cars, trucks, and motorcycles. This market encompasses local distributors and global brands supplying oils that meet international standards, supporting Ethiopia’s growing automotive sector and ensuring reliability, efficiency, and extended engine life.

The Ethiopia Automotive Engine Oil Market is segmented by product type, base stock type, grade, and vehicle type. By product type, the market is segmented into passenger car motor oil (PCMO), heavy duty motor oil (HDMO), and motorcycle engine oil (MCO). By base stock type, the market is segmented into mineral, synthetic, semi-synthetic, and bio-based. By grade, the market is segmented into 0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades. By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and growth forecasts have been done on the basis of volume (liters).

| Passenger Car Motor Oil (PCMO) |

| Heavy Duty Motor Oil (HDMO) |

| Motorcycle Engine Oil (MCO) |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| 0W-XX |

| 5W-XX |

| 10W-XX |

| 15W-XX |

| Monogrades |

| Other Grades |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Passenger Car Motor Oil (PCMO) |

| Heavy Duty Motor Oil (HDMO) | |

| Motorcycle Engine Oil (MCO) | |

| By Base Stock Type | Mineral |

| Synthetic | |

| Semi-Synthetic | |

| Bio-Based | |

| By Grade | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers |

Key Questions Answered in the Report

What is the projected volume for Ethiopia automotive engine oil market in 2031?

The Ethiopia Automotive Engine Oil Market size is expected to grow from 27.02 million liters in 2025 to 28.21 million liters in 2026 and is forecast to reach 35.08 million liters by 2031 at 4.46% CAGR over 2026-2031.

Which product category is growing the fastest?

Motorcycle Engine Oil is set to expand at a 5.12% CAGR through 2031, driven by last-mile delivery demand.

How large is the mineral-oil segment today?

Mineral formulations accounted for 74.98% of total volume in 2025, reflecting strong price sensitivity.

Which corridor is most critical for premium synthetic uptake?

The Addis-Djibouti trade route, where fleets demand long-drain synthetics to cut downtime.

Page last updated on: