E-bike Conversion Kit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

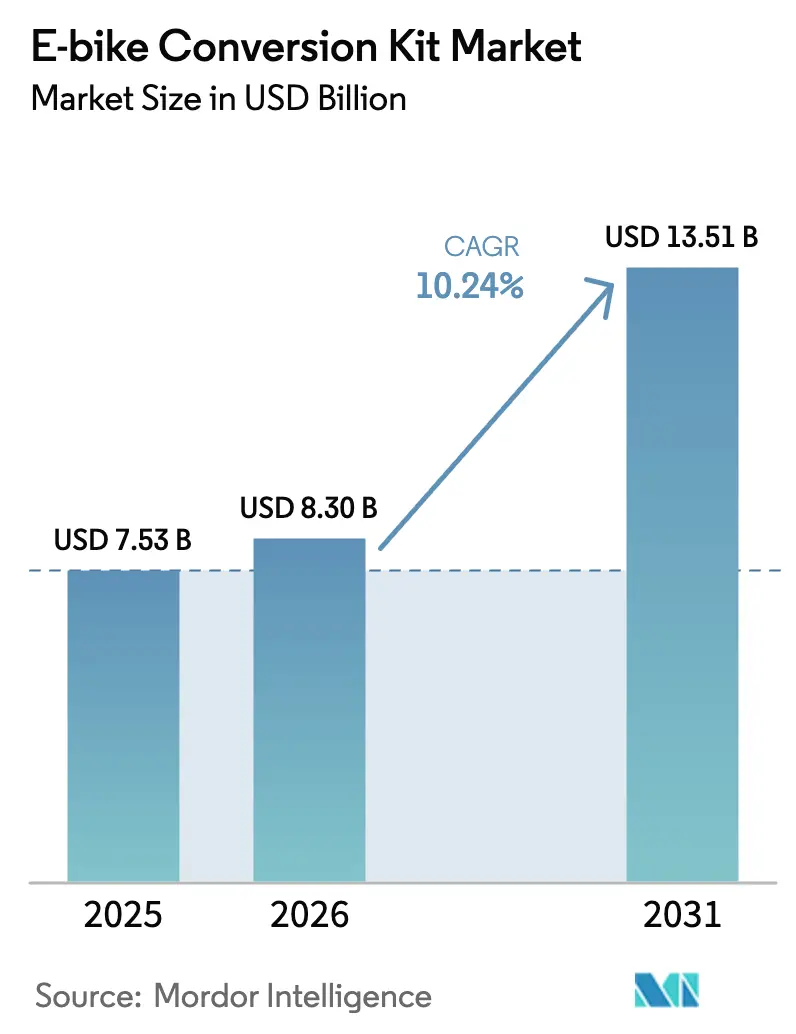

| Market Size (2026) | USD 8.3 Billion |

| Market Size (2031) | USD 13.51 Billion |

| Growth Rate (2026 - 2031) | 10.24% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-bike Conversion Kit Market Analysis by Mordor Intelligence

The E-bike conversion kit market size was valued at USD 7.53 billion in 2025 and estimated to grow from USD 8.3 billion in 2026 to reach USD 13.51 billion by 2031, at a CAGR of 10.24% during the forecast period (2026-2031). Growth reflects the confluence of steep battery cost deflation, pro-repair regulation, and sustained urbanisation that redirects daily trips toward micromobility. Falling lithium-ion cell prices have pushed retrofit economics below the cost of purchasing a new e-bike, while European right-to-repair directives encourage owners to upgrade existing bicycles rather than replace them. Asia-Pacific manufacturing hubs continue to deliver scale efficiencies, and governments in North America and Europe are broadening voucher programmes to include conversion kits.

Key Report Takeaways

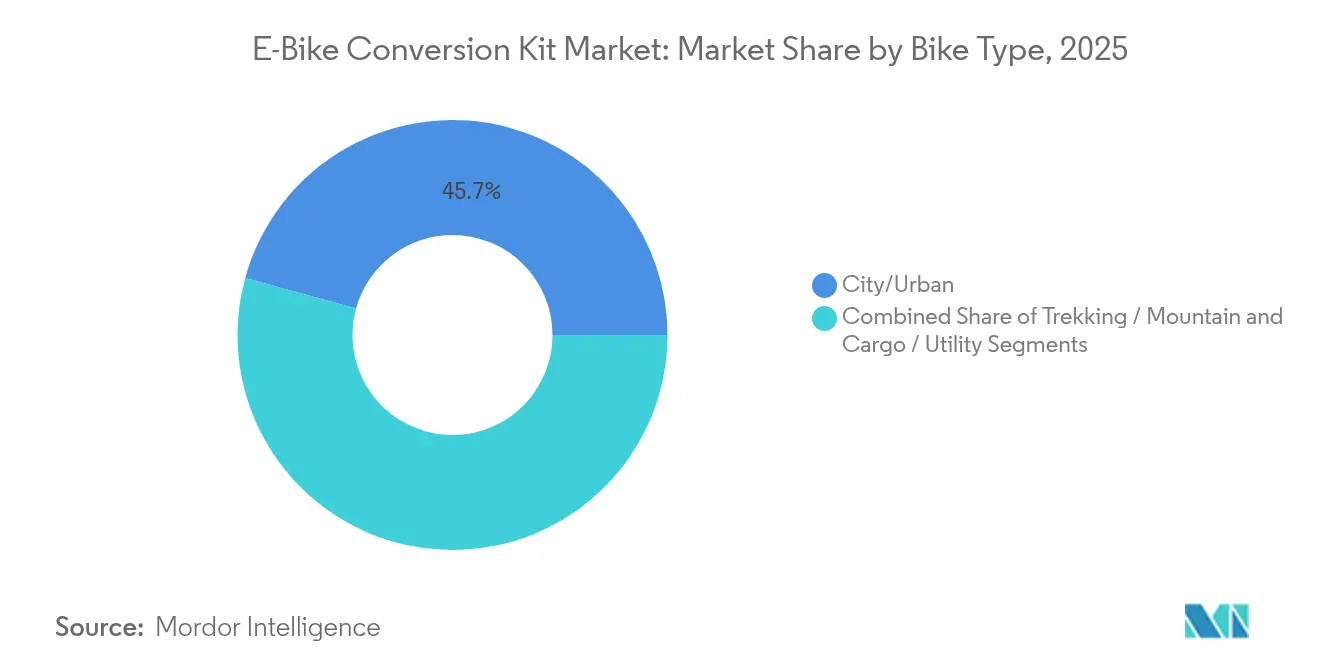

- By bike type, city and urban conversions led with 45.72% of the E-bike conversion kit market share in 2025; cargo and utility kits are projected to grow at a 13.62% CAGR through 2031.

- By component, motors accounted for 33.88% share of the E-bike conversion kit market size in 2025, while battery packs registered the fastest pace at 12.41% CAGR to 2031.

- By motor type, hub-geared systems held 61.45% of the E-bike conversion kit market share in 2025; mid-drive units will expand at 14.66% CAGR during the outlook period.

- By battery chemistry, lithium-ion dominated with 78.92% revenue share in 2025; sodium-ion solutions are forecast to rise at 17.88% CAGR through 2031.

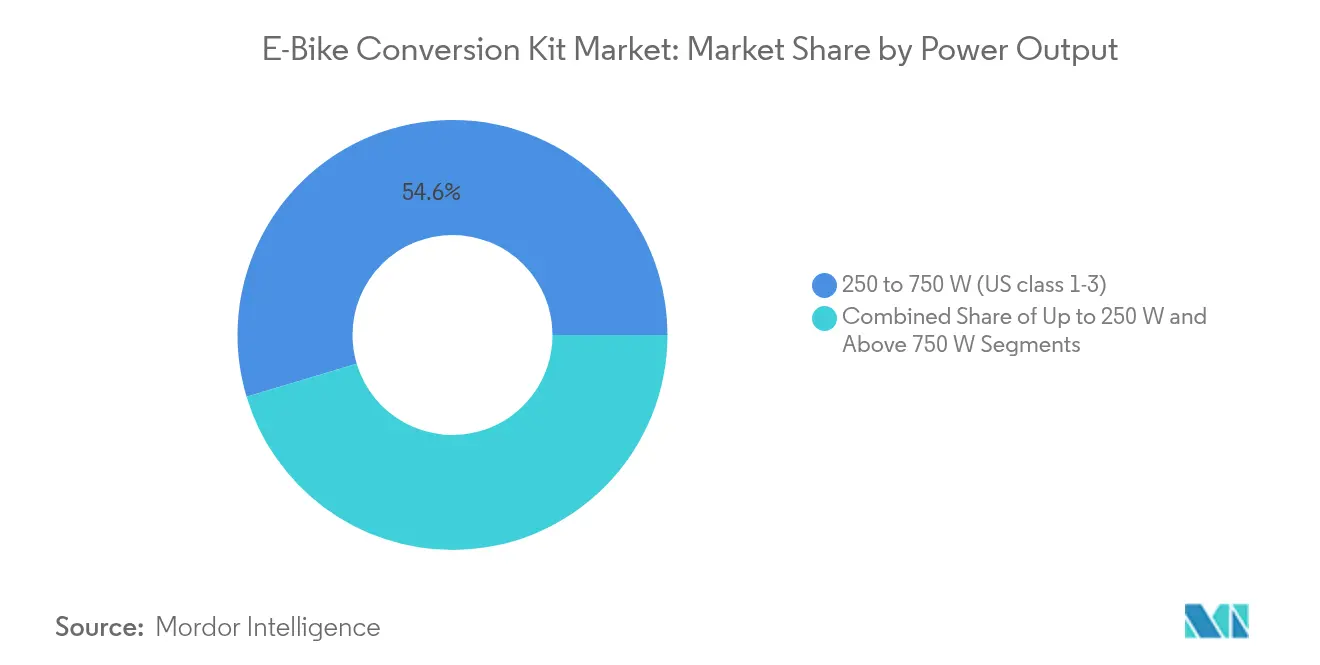

- By power output, 250 to 750-watt kits captured 54.63% of the E-bike conversion kit market size in 2025; outputs above 750 watts present the fastest 13.97% CAGR.

- By sales channel, aftermarket kits held an 82.41% share in 2025, while OEM factory-installed solutions are set to grow at 11.06% CAGR to 2031.

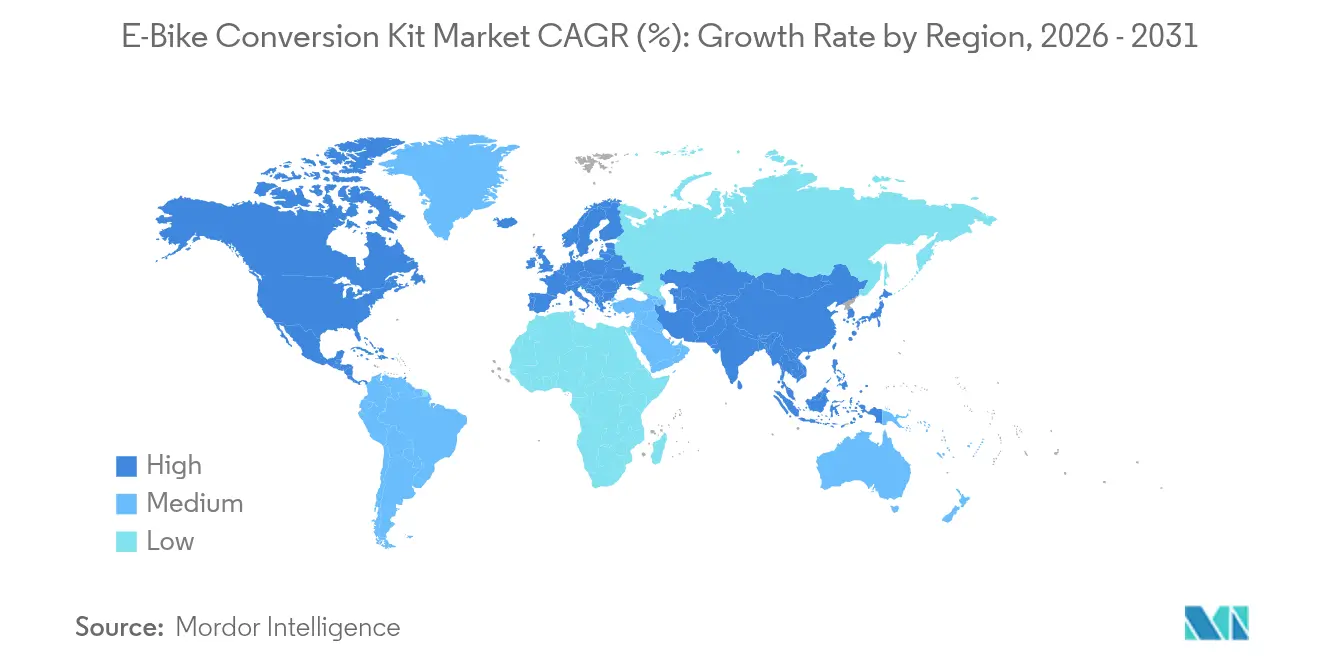

- By geography, Asia-Pacific led with a 44.02% share in 2025; Europe is the fastest-growing region with a 11.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-bike Conversion Kit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-Led Modal Shift To E-Mobility | +2.8% | Global, European cities and North American metropolitan areas | Medium term (2-4 years) |

| Declining Battery Cost Curve | +2.5% | Global, led by Chinese manufacturing scale and European adoption | Short term (≤ 2 years) |

| Government Purchase and Retrofit Incentives | +2.2% | North America & EU, with emerging programs in APAC | Medium term (2-4 years) |

| Micro-Fleet Demand for Last-Mile Delivery | +1.8% | Global urban centers, particularly dense European and Asian cities | Short term (≤ 2 years) |

| DIY Culture and Right-To-Repair Legislation | +1.3% | EU core, spill-over to North America and developed APAC markets | Long term (≥ 4 years) |

| Plug-And-Play Wiring Standards | +0.9% | Global, with early adoption in European and North American markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization-led modal shift to e-mobility

European and North American cities continue reallocating road space toward bicycles, triggering a surge in retrofit activity. In the Netherlands, consumer awareness of e-bikes reached 96.66%, with 83.33% ranking cost and mileage as top purchase factors. Urban cyclists often retain emotional attachment to existing bicycles, and conversion kits offer an affordable path to electric assistance without discarding a valued frame. These attributes strengthen the E-bike conversion kit market as planners enact low-emission zones and curb automobile parking.

Declining battery cost curve

Lithium-ion cell prices fall slashing the largest cost component in a kit and lifting gross margins for suppliers. Argonne National Laboratory forecasts further reductions aided by tax credits under the US Inflation Reduction Act. Conversion specialists, therefore, bundle larger-capacity packs at legacy price points, enhancing range and meeting cargo fleet requirements. The cost collapse underpins premium segment expansion and reinforces the competitive position of the E-bike conversion kit market versus new e-bike purchases.

Government purchase and retrofit incentives

California, Massachusetts, and Washington State allocated more than USD 40 million in 2024–2025 vouchers that explicitly cover retrofit kits, encouraging low-income riders to electrify existing bikes. Poland introduced a programme offering up to 50% reimbursement on qualifying kits from 2025–2029. These schemes compress payback periods to fewer than 18 months for frequent commuters and generate predictable demand spikes tied to application windows.

Micro-fleet demand for last-mile delivery

Urban logistics operators retrofit cargo cycles to circumvent congestion charges and meet corporate emissions targets. New York City authorised commercial e-cargo bikes in 2024, and the OECD reports that two e-cargo bikes can replace one diesel van, cutting about 14 tons of CO₂ annually[1]“The Final Frontier of Urban Logistics: Tackling the Last Metres,” International Transport Forum, itf-oecd.org . Fleet managers prefer conversion kits because they minimise capital outlay, extend asset life, and support proprietary cargo-box geometries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Recalls & Fire-Risk Perception | -1.2% | Global, with acute impact in North America and EU | Short term (≤ 2 years) |

| Impending EU/UK Kit Type-Approval Rules | -0.8% | EU and UK | Medium term (2-4 years) |

| Warranty Conflicts With OEM Bike Brands | -0.7% | Global, particularly affecting premium bicycle segments | Medium term (2-4 years) |

| Rare-Earth Magnet Price Volatility | -0.6% | Global, with supply chain concentration in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety recalls and fire-risk perception

The US Consumer Product Safety Commission urged riders to stop using specific replacement batteries linked to fires between 2018 and 2024, citing multiple injuries[2]“CPSC Warns Consumers to Stop Using Unit Pack Power E-Bike Batteries Due to Fire Hazards,” U.S. Consumer Product Safety Commission, cpsc.gov. The Guardian attributed 11 deaths in the UK to e-bike fires over the same period. Such incidents heighten scrutiny of aftermarket kits, increase insurance premiums for retailers, and prompt some city authorities to propose indoor-charging restrictions that could dampen short-term adoption.

Impending EU/UK kit type-approval rules

The UK Product Safety and Metrology Bill and European trade body recommendations would require kits to carry UKCA or CE marks and maintain technical files for 10 years. Compliance costs could squeeze smaller suppliers, steering market share toward established component brands that already possess certified quality-management systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bike Type: Urban Conversions Retain Leadership

The E-bike conversion kit market size for city and urban bicycles held a 45.72% market share in 2025, underscoring the dominance of daily utility use cases. Cargo and utility formats represent the most dynamic niche, expanding at 13.62% CAGR as delivery platforms electrify last-mile fleets. Uptake accelerates in cities where low-emission zones restrict combustion vans and where micro-hubs enable short-range routing. Kit suppliers tailor offerings with heavy-duty racks, torque-sensing mid-drives, and automatic gear hubs to satisfy payload and stop-start cycling profiles.

Growing attention to inclusivity also spurs kits for adaptive trikes and long-tail cargo frames, opening new addressable cohorts to the E-bike conversion kit industry. Major brands leverage premium drivetrains such as Bafang’s five-speed automatic hub that handles 200 Nm, simplifying use for riders unfamiliar with manual shifting. The technology marries low-maintenance appeal with urban performance, reinforcing conversion relevance among commuting and logistics users.

By Component: Batteries Drive Incremental Value

Motors captured 33.88% of 2025 revenue market share, yet batteries are forecast to add the greatest absolute value as falling cell costs enable higher capacities without price escalation. The battery segment is projected to climb at 12.41% CAGR through 2031, lifting its proportion of the E-bike conversion kit market size beyond 30% by decade’s end. Higher-energy packs extend ride range beyond 100 km, a milestone that erases residual range anxiety in suburban corridors.

Smaller yet strategic sub-systems, such as control units and PAS sensors, integrate Bluetooth and GPS, creating in-app diagnostics that fleet operators require for asset monitoring. Smartphone connectivity also supports over-the-air firmware upgrades, allowing brands to roll out safety patches that address regulatory expectations in key markets. Suppliers pairing secure battery management systems with connected controllers position themselves to capture premium price tiers as the E-bike conversion kit market matures.

By Motor Type: Mid-drive Systems Gain Momentum

Hub-geared motors maintained a 61.45% market share in 2025 due to simple installation and lower retail cost. Mid-drive units, however, will secure the fastest 14.66% CAGR on superior hill-climb torque and centralised weight distribution. Riders in hilly metropolitan areas such as Seattle or Zurich consider the mid-drive upgrade essential for confidence on steep gradients, and cargo operators appreciate drivetrain synergy that reduces chain wear relative to high-torque hub systems.

Motor suppliers invest in magnet optimisation and integrated reduction gearing to raise efficiency by 5-7%, offsetting the added kit complexity. Neo Performance Materials expanded European sintered magnet production to support this shift, reinforcing supply security for premium mid-drive assemblies. Adoption spreads from enthusiast circles into mainstream commuting as retailers simplify installation fixtures and publish compatibility certifications for leading derailleur brands.

By Battery Chemistry: Lithium-ion Consolidates While Sodium-ion Emerges

Lithium-ion packs held 78.92% market share in 2025, reflecting energy density and proven cycle life. Chemistry refinements such as higher-nickel NMC and LFP variants sustain incremental gains while containing thermal-runaway risk. Sodium-ion batteries, though nascent, attract interest with 17.88% CAGR projections, particularly in emerging economies where raw-material costs must remain low. Chinese cell producers lead commercialisation, shipping pilot volumes to value-focused kit brands serving Southeast Asia.

Safety remains a priority as public agencies scrutinise battery failure cases. Manufacturers adopt redundant temperature sensors and ceramic separators, and many offer UL2271 or EN15194 certified packs to reassure retailers and insurers. Compliance advantages bolster established lithium-ion vendors yet do not preclude sodium-ion’s long-term prospects, provided certification pathways evolve.

By Power Output: Mid-range Remains the Regulatory Sweet Spot

Kits rated 250 to 750 watts controlled 54.63% of 2025 revenue market share, aligning with EU and North American e-bike legislation. Policy revision under consultation in the United Kingdom to raise the ceiling to 500 watts would legitimise many current-generation kits and could stimulate retrofits among riders previously deterred by perceived legal ambiguity.

High-power kits above 750 watts are on track for a 13.97% CAGR, propelled by cargo operators requiring extra torque for 200 kg payloads and recreation users on off-road terrain. Brands mitigate overheating by integrating oil-cooled mid-drives and multi-stage planetary reduction, ensuring reliability despite sustained heavy loads. Low-power segments up to 250 watts still serve ultra-light racing and folding bikes where weight trumps sheer output.

By Sales Channel: Aftermarket Leads but OEMs Accelerate

Aftermarket kits retained an 82.41% revenue market share in 2025 but will cede ground to bicycle-manufacturer pre-installs that rise at 11.06% CAGR. OEM adoption confirms electric assist as a core feature rather than a retrofit accessory and answers warranty conflicts that previously deterred some premium frame suppliers. Yamaha’s acquisition of Brose’s e-bike drive business illustrates this pivot and grants access to a 600-location service network across Europe.

Retail workshops remain pivotal because riders value expert guidance on compatibility and legal compliance. Many shops now bundle certified battery options and provide disposal schemes aligned with EU Extended Producer Responsibility directives, differentiating service propositions even as OEM volumes climb.

Geography Analysis

Asia-Pacific dominated the E-bike conversion kit market with a 44.02% share in 2025, underpinned by integrated supply chains and rising domestic adoption in China, India, Vietnam, and Indonesia. Yadea’s USD 100 million investment in a Vietnamese factory capable of 2 million units annually exemplifies regional expansion beyond China while supporting Vietnam’s 22% electric motorcycle adoption target for 2030. Competitive advantage stems from the co-location of cell, motor, and controller production, compressing lead times and containing costs. Intra-regional exports also rise as ASEAN free-trade pacts remove tariff barriers on electric mobility components.

Europe delivered the fastest 11.82% CAGR and benefits from policy synergy: the EU Directive 2024/1799 enshrines repair rights, and incentive schemes now encompass retrofits. Poland’s 50% subsidy commencing in 2025 spreads financial support eastward, while mature markets such as Germany sustain demand through cycling infrastructure upgrades. Impending EU type-approval, however, may curtail non-compliant imports, encouraging local assembly and boosting opportunities for certification-ready suppliers.

North America growth is backed by state-level voucher funding exceeding USD 40 million in 2024–2025. California’s E-Bike Incentive Project increased base awards to USD 1,750, and Massachusetts rolled out a USD 1,200 rebate programme. The market wrestles with fragmented regulations that vary between states and cities, yet proposed federal battery safety legislation could harmonise standards and accelerate distribution partnerships. Cargo operators in dense hubs, including New York and Toronto, lead high-power kit adoption for last-mile logistics.

Competitive Landscape

The E-bike conversion kit market exhibits moderate concentration with established players maintaining significant market shares through technological differentiation and distribution network advantages. Leaders leverage vertically integrated motor-battery platforms, patented control algorithms, and global service networks to defend their share while expanding into mid-drive and cargo applications.

Strategic moves underscore convergence between automotive and bicycle supply chains. Yamaha’s purchase of Brose’s drive unit portfolio grants access to automotive-grade controllers, positioning the firm to address stricter EU safety requirements. Bosch expanded its Smart System platform with over-the-air diagnostics that alert riders to battery health, addressing fire-risk concerns raised by regulators. Shimano invested in European after-sales training academies that certify independent workshops, improving install quality and mitigating warranty disputes.

Niche innovators target whitespace rather than challenge incumbents head-on. US-based Swytch pioneered ultra-light friction-drive kits for folding bicycles, while Dutch firm Pendix focuses on centrally mounted motors for adaptive tricycles. Component specialists such as Neo Performance Materials shore up supply of sintered magnets, ensuring resilience against Chinese export volatility. Competitive intensity is expected to climb once EU type-approval crystallises, rewarding players with certified designs and robust technical documentation.

E-bike Conversion Kit Industry Leaders

Bafang Electric (Suzhou) Co., Ltd.

Shimano Inc.

Robert Bosch GmbH

Swytch Bike

Tongsheng Motor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Yamaha Motor agreed to acquire Brose’s e-bike drive business, forming Yamaha Motor eBike Systems and inheriting a 600-location European service network.

- January 2025: Yadea invested USD 100 million in a Vietnam production facility with 2-million-unit annual capacity to support Southeast Asian expansion and R&D localisation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the e-bike conversion kit market covers every aftermarket assembly, motor, battery, controller, sensors, cabling, and mounting hardware sold to retrofit a standard bicycle so it delivers electric assist while retaining pedal function. Kits shipped pre-installed on new frames or sold as stand-alone batteries are outside this scope.

Scope exclusion: Factory-built e-bikes, replacement batteries, and ride-share fleet retrofits are not quantified in this study.

Segmentation Overview

- By Bike Type

- City / Urban

- Trekking / Mountain

- Cargo / Utility

- By Component

- Motor

- Battery Pack

- Control Unit and Display

- Throttle / PAS Sensors

- Wiring Harness and Ancillaries

- By Motor Type

- Hub-Geared

- Hub-Gearless (Direct Drive)

- Mid-Drive

- Friction and All-in-One Wheel

- By Battery Chemistry

- Lead-Acid

- Lithium-iron-phosphate (LFP)

- Others

- By Power Output

- Up to 250 W

- 250 to 750 W (US class 1-3)

- Above750 W (performance / off-road)

- By Sales Channel

- Aftermarket (DIY and Pro-shops)

- OEM / Factory-installed

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed kit manufacturers, regional distributors, independent bike shops, and repair collective mechanics across North America, Europe, and Asia-Pacific. These conversations validated shipment volumes, typical selling prices, warranty burden, and real-world installation time, filling gaps that secondary data alone could not resolve.

Desk Research

Our desk work began with traffic-related datasets from bodies such as Eurostat, the U.S. Bureau of Transportation Statistics, China Customs, and the European Cyclists' Federation, which reveal underlying bicycle stock, import values, and regulatory cues that influence kit uptake. We then tracked battery price trajectories, rare-earth magnet supply, and lithium policies through the International Energy Agency and UN Comtrade, before mapping urban micromobility incentive schemes published by the OECD and national energy ministries. Mordor analysts complemented these with company filings mined on D&B Hoovers, news streams from Dow Jones Factiva, and patent families pulled via Questel to gauge product pipeline density. The sources listed are illustrative; many further public and proprietary references informed our evidence base.

Market-Sizing & Forecasting

A top-down demand pool was reconstructed from national bicycle stock and annual replacement rates, which were then filtered through modeled kit penetration ratios and average selling price bands. Select bottom-up checks, supplier roll-ups, retail channel audits, and sampled ASP times unit triangulation tempered the totals. Key variables inside the model include lithium-ion battery $/kWh, urban congestion indices, disposable household income, bicycle import tariffs, and subsidy voucher uptake rates. Multivariate regression projected each driver through 2030, with scenario analysis reflecting battery price and policy swings. Data gaps in emerging markets were bridged by analog adoption curves and expert corroboration.

Data Validation & Update Cycle

Outputs pass variance screens against trade statistics and bike shop sales surveys; anomalies trigger re-checks before senior review signs off. Models refresh annually, and we push interim updates whenever policy shifts or material recalls alter the demand picture.

Why Mordor's E-Bike Conversion Kit Baseline Stands Up to Scrutiny

Published figures often diverge because firms slice the market differently, assume contrasting kit penetration, or refresh at uneven intervals.

Our disciplined scope, dual-track modeling, and yearly refresh cadence narrow those gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.53 B (2025) | Mordor Intelligence | - |

| USD 1.85 B (2025) | Regional Consultancy A | Focuses on ≤250 W kits in five mature economies; neglects growth in Asia and mid-drive segments |

| USD 2.50 B (2025) | Trade Journal B | Counts hardware only, omits installation labor and replacement batteries; relies on press release tallies |

| USD 0.78 B (2024) | Industry Association C | Tracks online DIY sales under 750 W and freezes 2022 ASP, ignoring inflation and premium kit shift |

The comparison shows how narrower scopes, static pricing, or limited geography compress external estimates, whereas Mordor's balanced approach, rooted in transparent drivers and live feedback loops, delivers a dependable baseline for planners seeking clear, reproducible numbers.

Key Questions Answered in the Report

What is the current size of the E-bike conversion kit market?

The E-bike conversion kit market size reached USD 8.3 billion in 2026 and is set to approach USD 13.51 billion by 2031.

Which region leads the market today?

Asia-Pacific commands a 44.02% share, supported by vertically integrated manufacturing clusters and growing urban adoption.

Which segment is growing fastest?

Cargo and utility bike kits are forecast to grow at 13.62% CAGR, fuelled by last-mile delivery demand in dense cities.

How are falling battery prices influencing adoption?

Falling Lithium-ion cell costs enabling larger-capacity packs at stable prices and lowering payback periods for retrofits.

What regulatory changes could impact suppliers?

Proposed EU and UK type-approval rules will mandate CE or UKCA certification for kits, potentially consolidating market share among compliance-ready brands.

Are safety concerns slowing growth?

Battery fire incidents prompt stricter oversight, but leading suppliers mitigate risk with certified battery management systems and consumer education initiatives.

Page last updated on: