Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

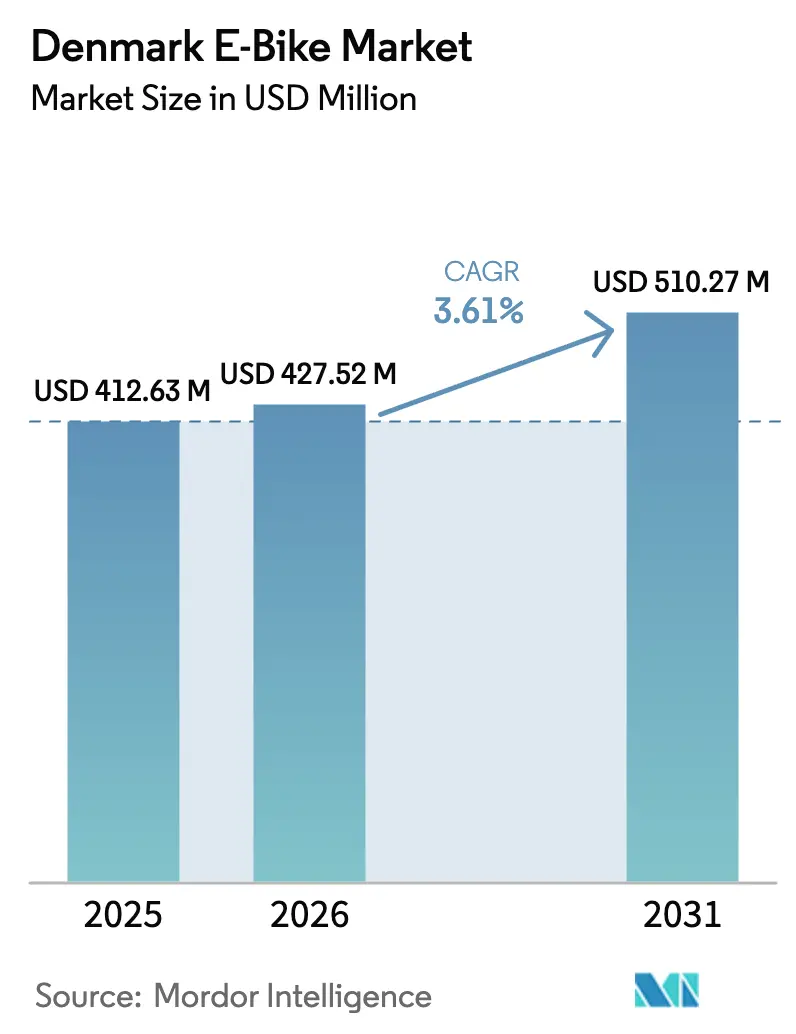

| Base Year Market Size (2025) | USD 412.63 Million |

| Market Size (2026) | USD 427.52 Million |

| Market Size (2031) | USD 510.27 Million |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark E-Bike Market Analysis by Mordor Intelligence

The Denmark e-bike market size is expected to grow from USD 412.63 million in 2025 to USD 427.52 million in 2026 and is forecast to reach USD 510.27 million by 2031 at 3.61% CAGR over 2026-2031. This outlook reflects a mature cycling culture that is steadily electrifying as government incentives align with sustained investment in protected infrastructure. Copenhagen’s cycle superhighways, expansion of suburban lanes, and integrated charging hubs raise the practicality of longer commutes and reduce range anxiety. Corporate leasing programs further accelerate uptake by lowering upfront costs and offering tax advantages, while premiumization trends lift average selling prices as riders favor mid-drive motors and belt drives for a natural feel and low maintenance. Intensifying consolidation pressure after the VanMoof bankruptcy signals scope for stronger brands to capture share, with technology, service reach, and supply-chain resilience emerging as key competitive levers.

Key Report Takeaways

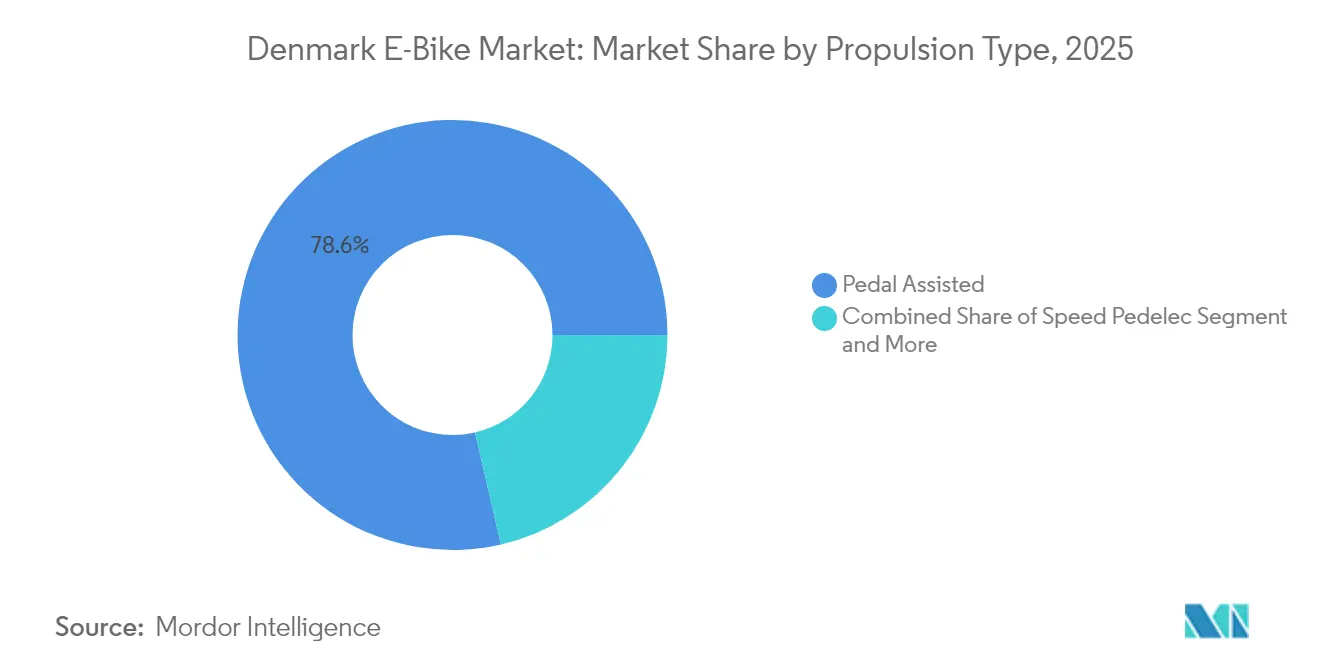

- By propulsion type, Pedal Assisted systems held 78.62% of the Denmark e-bike market share in 2025, while Speed Pedelecs are projected to grow at a 3.71% CAGR to 2031.

- By application type, City/Urban commuting held 76.20% of the Denmark e-bike market share in 2025, while Cargo/Utility segment is projected to grow at a 3.72% CAGR to 2031.

- By battery type, Lithium-Ion Battery accounted for 99.32% of the Denmark e-bike market size in 2025, and is forecast to expand at a 3.74% CAGR during 2026-2031.

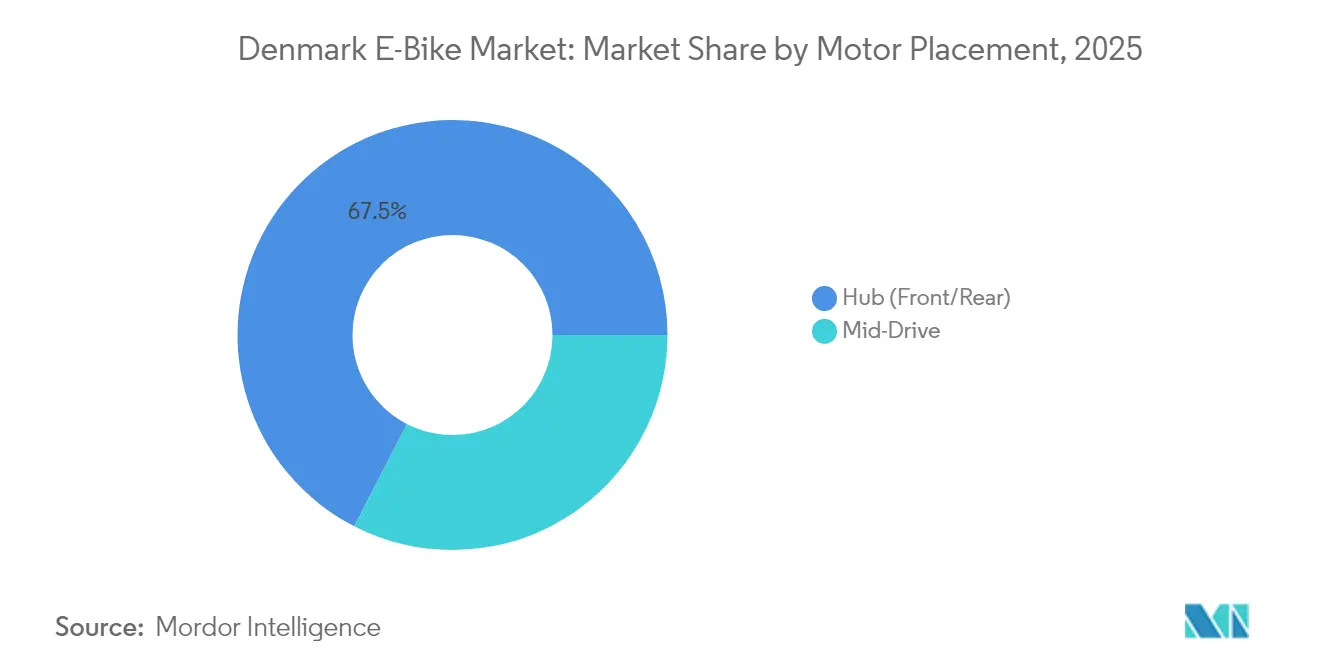

- By motor placement, hub motors accounted for 67.45% of the Denmark e-bike market size in 2025, but mid-drive models are forecast to expand at a 4.1% CAGR during 2026-2031.

- By drive systems, Chain Drives accounted for 72.60% of the Denmark e-bike market size in 2025, but Belt Drive model is forecast to expand at a 4.83% CAGR during 2026-2031.

- By motor power, Bikes Below 250 W accounted for 54.60% of the Denmark e-bike market size in 2025, but 351-500 W models are forecast to expand at a 5.05% CAGR during 2026-2031.

- By price band, the USD 1,500-2,499 segment dominated with 29.60% share in 2025, whereas the USD 3,500-5,999 tier is anticipated to grow at a 4.43% CAGR up to 2031.

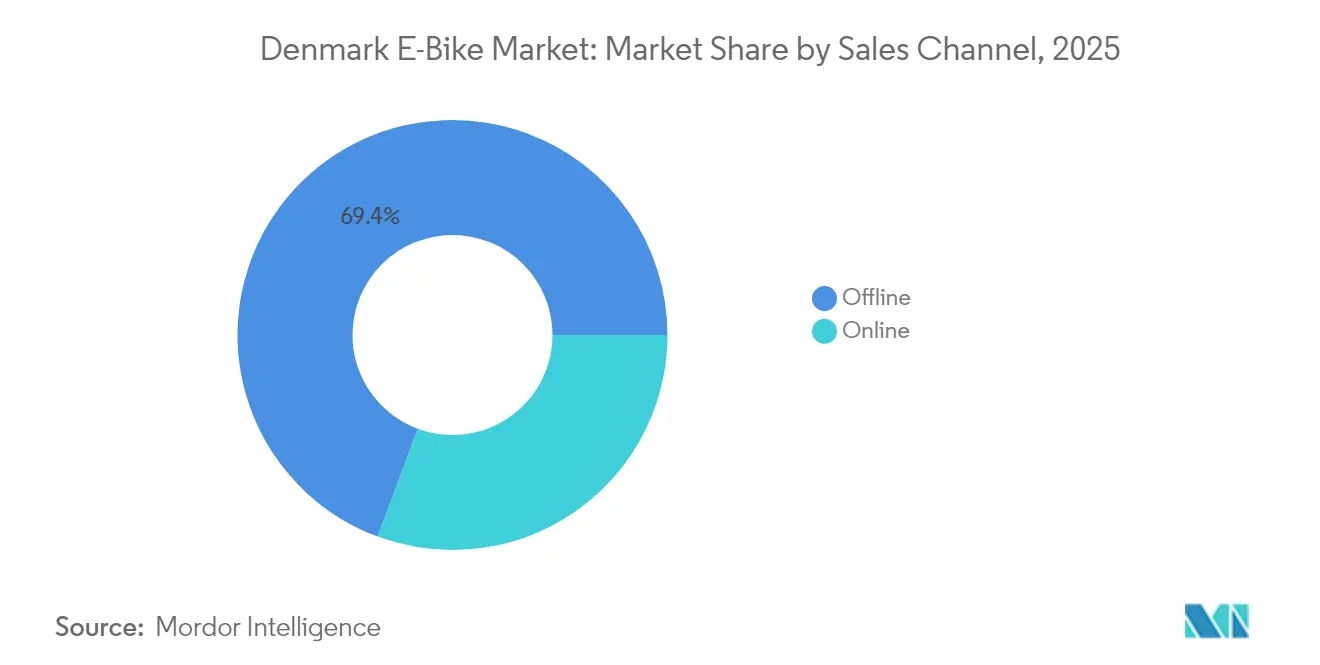

- By sales channel, Offline Retail captured 69.35% revenue in 2025, yet Online Platforms are expected to post the highest 6.05% CAGR over the same period.

- By end user, Personal and Family Use led with a 58.80% share of the Denmark e-bike market in 2025, whereas Commercial Delivery is set to register the fastest 5.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark E-Bike Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric Mobility Incentives | +0.8% | National, with early gains in Copenhagen, Aarhus, Odense | Medium term (2-4 years) |

| Cycle Infrastructure Expansion | +0.7% | National, concentrated in Greater Copenhagen and major cities | Long term (≥ 4 years) |

| Mobility-as-a-Benefit Programs | +0.6% | National, strongest in urban employment centers | Short term (≤ 2 years) |

| Growth of Last-Mile Delivery | +0.5% | Urban areas, Copenhagen metropolitan region | Short term (≤ 2 years) |

| Urban Congestion-Charge Expansion | +0.4% | Copenhagen city center, possible spread to Aarhus | Medium term (2-4 years) |

| Advances in Mid-Drive Motors | +0.3% | National, premium segment focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Light Electric Mobility

Denmark’s tax code grants favorable treatment to employer-sponsored e-bike leases, allowing staff to access units below retail prices through salary sacrifice plans. National cycling strategy funds earmark protected lanes, secure parking, and public charging, which broadens access beyond central Copenhagen. These measures align with the 2030 carbon-neutrality goal and directly bolster the Personal and Family Use segment by reducing net ownership costs. Moreover, a planned subsidy extension for cargo e-bikes is expected to support commercial fleets that pursue zero-emission delivery targets. Collectively, these levers raise affordability, expand infrastructure, and improve perception of e-bikes as viable car alternatives.

Expansion of Protected Cycle Infrastructure

Copenhagen’s cycle superhighway grid already links suburban zones, with another scheduled before 2030. Weather shelters, priority signals, and high-maintenance standards increase year-round reliability, particularly for rides exceeding 10 km—a distance where e-assist provides clear benefits. Network effects magnify utility because each added route multiplies safe, continuous trip options. Complementary projects by DSB to station parking upgrades and first-mile connections, encouraging multimodal journeys that pair trains with e-bikes[1]“Station Access and Parking Masterplan,” Danish State Railways, dsb.dk. This integrated approach reduces congestion, cuts travel time, and supports the gradual shift from acoustic cycles to electrified models that better suit longer suburban commutes.

Corporate Mobility-as-a-Benefit Schemes

Employers introduce all-inclusive leases that bundle maintenance, insurance, and end-of-term purchase options into fixed monthly deductions, addressing the chief barrier of upfront cost. Typical contracts, creating predictable demand for manufacturers while offering staff hassle-free use. Companies report reduced parking expenses and improved employee satisfaction when car allowances are partially replaced with e-bike benefits, particularly in city districts with high parking costs [2]“Corporate Commuter Benefits Guide,” Copenhagen Municipality, kk.dk. As firms race for talent, sustainable mobility perks become differentiators, stimulating premium segment growth and solidifying recurring revenue streams for leasing providers. The schemes also familiarize non-cyclists with assisted riding, broadening the addressable base.

Growth of Last-Mile Delivery Platforms

Wolt’s Better Cities Fund supplies couriers with cargo models for a monthly fee that includes servicing and full-risk coverage [3]“Better Cities Fund: Courier Cargo Bike Program,” Wolt, wolt.com . Entry-level SmartVelo L units and VOK S high-capacity bikes enable contractors to perform more deliveries than on muscle-powered bicycles. The approach underpins the Commercial Delivery, demonstrates credible total cost of ownership advantages, and raises public visibility of e-cargo solutions. Success stories have prompted competing platforms to trial similar models, expanding the installed fleet and spreading maintenance know-how across dealer networks. These demonstration effects translate into household interest, as families observe the efficiency of electrically assisted cargo transport.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Bicycles | -0.9% | National, strongest in rural and lower-income segments | Short term (≤ 2 years) |

| Battery-Cell Supply Constraints | -0.6% | Global supply chain, affecting all Danish segments | Medium term (2-4 years) |

| Regulatory Ambiguity for Pedelecs | -0.4% | National, particularly affecting commuters | Short term (≤ 2 years) |

| Competition from E-Scooter Fleets | -0.3% | Urban areas, Copenhagen and major cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs. Acoustic Bicycles

In rural towns, where the journey length often doesn't necessitate motor support, first-time buyers face significant cost challenges. Retail prices for these cycles are considerably higher compared to conventional cycles. Battery replacement every three to five years significantly impacts lifetime ownership costs, and tighter consumer spending during economic slowdowns amplifies reluctance. While leasing dilutes the shock, private buyers without employer backing still weigh amortized benefits against immediate outlay. The price gap narrows for high-mileage commuters who can offset fuel and parking costs, yet broader nationwide adoption hinges on further cost declines or financing innovation.

Battery-Cell Supply Constraints

Lithium spot prices have experienced significant fluctuations over time, subjecting manufacturers to unpredictable packing costs, which constitute a substantial portion of a unit's bill of materials. Reliance on Asian cell suppliers means shipping delays and geopolitical events can stretch lead times, prompting stockouts in peak spring selling periods. Mid-price brands struggle to absorb surcharges, risking either margin squeeze or retail hikes. Limited domestic recycling infrastructure slows the return of critical minerals, tempering circular-economy gains and heightening raw-material risk premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Pedal Assist Dominance Faces Speed Evolution

Pedal-assisted units held 78.62% of the Denmark e-bike market in 2025 as riders prefer seamless motor support that amplifies human power. The Denmark e-bike market size for this segment is projected to progress steadily in line with commuter and leisure demand that values exercise and extended range. Pedal sensors and adaptive assistance now match torque to cadence with near-instant response, heightening ride satisfaction in urban traffic. Though forming a smaller base, speed-pedelec models are forecast to record a 3.71% CAGR through 2031 as workplace journeys grow longer and congestion charges rise. If regulators confirm permanent significant access on protected lanes, commuter adoption could accelerate, but ongoing insurance debates restrain immediate volume expansion.

Rider profile distinctions grow clearer: pedal-assist suits daily errands, school runs, and recreational tours below 25 km/h, while speed variants target commuters needing quick cross-suburb travel. Leasing companies differentiate packages accordingly, bundling higher insurance and advanced lighting for speed-pedelecs. Component suppliers invest in dual-mode software that downshifts power for shared-path etiquette, safeguarding acceptance among acoustic cyclists. Meanwhile, hub-driven pedal-assist bikes continue to serve entry tiers, ensuring price accessibility. Collectively, these trends reaffirm the Denmark e-bike market as a laboratory for proportionate motorization calibrated to local infrastructure and policy.

By Application Type: Urban Utility Drives Commercial Growth

City and urban riding accounted for 76.20% of the Denmark e-bike market size in 2025, as dense infrastructure and short trip chains position electrified two-wheelers as logical car substitutes. Households embrace step-through frames with integrated racks for groceries and child seats, reflecting lifestyle integration rather than sport. Cargo and utility bikes, while still niche, are forecast to deliver a leading 3.72% CAGR through 2031, propelled by delivery platforms and families replacing second cars. Commercial courier pilots document notable productivity gains when shifting from acoustic bikes, and their visibility normalizes high-capacity frames in residential streets.

Municipal procurement increasingly specifies e-cargo formats for park maintenance and waste patrols, underpinning base demand even if consumer budgets tighten. Trekking and mountain e-bikes lag due to Denmark’s flat topography, yet brands court the tourism segment with weekend rental bundles along coastal routes. Such diversification broadens revenue resilience as seasonal commuting dips in winter, but leisure demand persists. The Denmark e-bike market thus evolves toward purpose-built form factors aligned with distinct urban, family, and logistics tasks.

By Battery Type: Lithium-Ion Monopolizes Performance

Lithium-ion packs supplied 99.32% of e-bike assemblies in 2025, underpinning the Denmark e-bike market share dominance of high-energy chemistries that deliver long range without significant weight. This segment is also projected to witness the fastest growth of 3.74% CAGR by 2031. NMC and NCA cells lead mainstream adoption, yet LFP variants gain momentum in cargo fleets prioritizing durability and thermal safety. Lead-acid options retreat to price-sensitive corners and rental fleets, where performance trade-offs remain acceptable.

Cell advances push average capacity, shrinking charging sessions to under three hours on 4 A chargers. Danish buyers favor removable packs to permit indoor charging, given apartment living norms, and dual-battery options emerge in touring and delivery categories. Manufacturers experiment with modular housings so riders can swap form factors without frame redesigns. Europe-wide recycling mandates requiring significant material recovery by 2025 spur local processing projects, which, once scaled, could mitigate raw-material exposure that constrains the Denmark e-bike market.

By Motor Placement: Mid-Drive Innovation Challenges Hub Dominance

Hub motors delivered 67.45% units in 2025, sustaining cost-efficient offerings that meet basic urban needs. The Denmark e-bike market nevertheless shows a 4.1% CAGR for mid-drive systems owing to their balanced weight distribution and superior torque management on Copenhagen’s modest inclines. Premium commuters perceive smoother gear shifts and less drag above 25 km/h, increasing willingness to pay a price premium.

Cargo builders value center-mounted torque peaks to handle 80 kg payloads without overheating, while software updates optimize assistance curves under variable loads. Entry-level hub designs answer with integrated planetary gears and regenerative braking, narrowing the performance gap. Dealers expand technician training to service both architectures, easing consumer transition barriers. Over time, the Denmark e-bike market will likely support a bifurcated structure: budget hubs for casual rides and advanced mid-drives for heavy-duty or performance-oriented use.

By Drive Systems: Belt Drive Emerges Despite Chain Dominance

Chain systems retained a 72.60% share in 2025, backed by global supply standardization and broad mechanical familiarity. However, belt drives are projected to climb at a 4.83% CAGR through 2031 as urban riders value grease-free operation and minimal maintenance. Carbon-fiber reinforced belts stretch service intervals, slashing total cost even at higher acquisition prices.

Frame makers redesign rear triangles to accommodate belt tensioners and split dropouts, signaling a long-term pivot toward that system in mid and premium tiers. Chains hold ground in performance mountain builds where derailleur compatibility and field reparability matter. Belt systems promote a clean office arrival for the everyday commuter, fitting Denmark’s professional dress norms. The Denmark e-bike market thus mirrors a broader consumer shift toward convenience over marginal drivetrain efficiency.

By Motor Power: Performance Segments Drive Premium Growth

Motors rated below 250 W captured 54.60% of 2025 volume, matching EU limits for unlicensed operation on public paths. Though smaller, the 351-500 W band is set to advance at 5.05% CAGR, fueled by cargo bikes and speed-pedelec commuters needing higher torque. Software governors allow dynamic wattage caps to comply with legal thresholds while supplying overdraft bursts for hills or heavy loads.

Manufacturers court versatility by offering firmware unlocks under dealer supervision for private land use, balancing compliance and performance. Above-600 W units remain marginal, restricted to sports niches and fenced facilities. As battery energy density rises, even 250 W systems achieve greater range, tempering the need for higher continuous power outside specialized contexts.

By Price Band: Premium Segments Capture Growth

The USD 1,500-2,499 bracket represented 29.60% of 2025 spending, positioning it as the accessible entry point for mass consumers. Yet the USD 3,500-5,999 tier is forecast to expand at a 4.43% CAGR through 2031 as leasing schemes flatten sticker shock and riders reward quality hardware. Premium buyers demand integrated lights, GPS security, and connectivity that cheaper models lack, propelling average selling prices upward.

Dealers offer tiered maintenance packages and extended warranties that further justify the premium, while subscription models bundle hardware, software, and service into a monthly fee. Budget categories feel pressure as mid-range features trickle down, narrowing differentiation. The Denmark e-bike market reflects a maturing consumer base that weighs holistic value over entry cost alone.

By Sales Channel: Digital Transformation Accelerates

Physical dealers commanded 69.35% of transaction value in 2025, underlining the importance of test rides and local servicing for complex products. Online volumes, however, are rising at a 6.05% CAGR as brand sites streamline configurators and home delivery. Direct-to-consumer startups seed demand via influencer marketing and 100-day return guarantees that ease hesitation.

Hybrid click-and-collect models allow buyers to research online, place orders, and pick up fully prepped bikes in partner shops, marrying convenience with professional setup. Dealers respond with virtual showrooms and at-home demo vans to defend relevance. Warranty claims still require physical workshops, anchoring brick-and-mortar importance even as digital growth outpaces the broader Denmark e-bike market.

By End Use: Commercial Delivery Drives Segment Transformation

Personal and Family Use secured 58.80% of 2025 volume, with multi-child cargo bikes replacing second cars for grocery runs and school drop-offs. Commercial Delivery exhibits the sharpest 5.45% CAGR as platform economies scale and municipalities restrict van access in dense cores. Leasing bundles that include high-capacity boxes, priority servicing, and insurance create predictable cost structures for gig workers.

Institutional users such as facility managers and postal services adopt electrified fleets to meet sustainability goals and lower operating expenses. Service providers leverage data-logging to optimize routing and preventative maintenance, enhancing reliability. The Denmark e-bike market thus shifts from purely consumer-driven to a balanced ecosystem where commercial fleets push technological boundaries and volume.

Geography Analysis

In 2024, an extensive superhighway network, a dense population, and aggressive climate policies significantly boosted Copenhagen's contribution to the nation's unit sales. Protected lanes, seamless rail integration, and subsidies for secure bike parking amplify daily convenience, supporting the highest per-capita penetration in Europe. Suburban commuters benefit as new routes extend beyond city limits, turning short-distance journeys into quick rides with minimal effort.

Aarhus, Odense, and Aalborg represent the next growth wave as municipal budgets prioritize traffic decongestion and air-quality improvement. E-bike uptake in these cities mirrors the Copenhagen playbook: targeted infrastructure, employer incentives, and parking reforms. Due to lower density and service gaps, rural districts show slower adoption, yet improved digital retail channels and portable battery tech reduce logistical hurdles. The Denmark e-bike market continues to broaden geographically, driven by an integrated national vision that positions cycling as a pillar of carbon neutrality.

Speed-pedelec trials centered in Copenhagen offer valuable performance and safety data that guide policy across the country. Successful outcomes could spill into other metropolitan areas, encouraging faster commute corridors and specialized parking hubs. These geographic clusters of expertise attract foreign component suppliers and stimulate domestic innovation, reinforcing Denmark’s status as a living laboratory for electrified micro-mobility.

Competitive Landscape

The market remains moderately fragmented. Established European players rely on mature dealer networks and strong warranty reputations, while younger Danish firms such as STRØM Bikes and Nørdic Bikes exploit agile direct-to-consumer models. The VanMoof bankruptcy in 2023 exposed the risk of overexpansion without service depth, prompting acquirers to prioritize financial stability and after-sales capabilities.

Technological differentiation now centers on mid-drive integration, IoT connectivity, and predictive maintenance rather than pure cost. Companies with proprietary motor and battery relationships secure supply during shortages, maintaining launch schedules and brand credibility. Leasing arms and subscription programs provide recurring revenue that buffers cyclical retail demand, giving integrated players an advantage.

Shared-mobility operators form a parallel channel, buying fleets directly from OEMs and demanding telemetry-enabled hardware for fleet optimization. Suppliers who tailor ruggedized frames and swappable powertrains win these contracts, boosting volume and visibility. Overall, competition emphasizes lifecycle services and digital engagement, reflecting a consumer base that expects seamless ownership experiences.

Denmark E-Bike Industry Leaders

Giant Manufacturing Co. Ltd

Van Moof BV

Royal Dutch Gazelle

A. Winther A/S

Batavus BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Donkey Republic partnered with Mastercard to enable tap-and-go bike rentals across Copenhagen, simplifying multimodal travel for residents and visitors.

- February 2024: Wolt launched its Better Cities Fund in Copenhagen, offering couriers access to purpose-built cargo e-bikes under all-inclusive monthly leases.

Denmark E-Bike Market Report Scope

Pedal Assisted, Speed Pedelec, Throttle Assisted are covered as segments by Propulsion Type. Cargo/Utility, City/Urban, Trekking are covered as segments by Application Type. Lead Acid Battery, Lithium-ion Battery, Others are covered as segments by Battery Type.By Propulsion Type

| Pedal Assisted |

| Speed Pedelec |

| Throttle Assisted |

By Application Type

| Cargo/Utility |

| City/Urban |

| Trekking/Mountain |

By Battery Type

| Lead Acid Battery |

| Lithium-ion Battery |

| Others |

By Motor Placement

| Hub (Front/Rear) |

| Mid-Drive |

By Drive Systems

| Chain Drive |

| Belt Drive |

By Motor Power

| Below 250 W |

| 251-350 W |

| 351-500 W |

| 501-600 W |

| Above 600 W |

By Price Band

| Up to USD 1,000 |

| USD 1,000-1,499 |

| USD 1,500-2,499 |

| USD 2,500-3,499 |

| USD 3,500-5,999 |

| Above USD 6,000 |

By Sales Channel

| Online |

| Offline |

By End Use

| Commercial Delivery | Retail and Goods Delivery |

| Food and Beverage Delivery | |

| Service Providers | |

| Personal and Family Use | |

| Institutional | |

| Others |

| By Propulsion Type | Pedal Assisted | |

| Speed Pedelec | ||

| Throttle Assisted | ||

| By Application Type | Cargo/Utility | |

| City/Urban | ||

| Trekking/Mountain | ||

| By Battery Type | Lead Acid Battery | |

| Lithium-ion Battery | ||

| Others | ||

| By Motor Placement | Hub (Front/Rear) | |

| Mid-Drive | ||

| By Drive Systems | Chain Drive | |

| Belt Drive | ||

| By Motor Power | Below 250 W | |

| 251-350 W | ||

| 351-500 W | ||

| 501-600 W | ||

| Above 600 W | ||

| By Price Band | Up to USD 1,000 | |

| USD 1,000-1,499 | ||

| USD 1,500-2,499 | ||

| USD 2,500-3,499 | ||

| USD 3,500-5,999 | ||

| Above USD 6,000 | ||

| By Sales Channel | Online | |

| Offline | ||

| By End Use | Commercial Delivery | Retail and Goods Delivery |

| Food and Beverage Delivery | ||

| Service Providers | ||

| Personal and Family Use | ||

| Institutional | ||

| Others | ||

Market Definition

- By Application Type - E-bikes considered under this segment include city/urban, trekking, and cargo/utility e-bikes. The common types of e-bikes under these three categories include off-road/hybrid, kids, ladies/gents, cross, MTB, folding, fat tire, and sports e-bike.

- By Battery Type - This segment includes lithium-ion batteries, lead-acid batteries, and other battery types. The other battery type category includes nickel-metal hydroxide (NiMH), silicon, and lithium-polymer batteries.

- By Propulsion Type - E-bikes considered under this segment include pedal-assisted e-bikes, throttle-assisted e-bikes, and speed pedelec. While the speed limit of pedal and throttle-assisted e-bikes is usually 25 km/h, the speed limit of speed pedelec is generally 45 km/h (28 mph).

| Keyword | Definition |

|---|---|

| Pedal Assisted | Pedal-assist or pedelec category refers to the electric bikes that provide limited power assistance through torque-assist system and do not have throttle for varying the speed. The power from the motor gets activated upon pedaling in these bikes and reduces human efforts. |

| Throttle Assisted | Throttle-based e-bikes are equipped with the throttle assistance grip, installed on the handlebar, similarly to motorbikes. The speed can be controlled by twisting the throttle directly without the need to pedal. The throttle response directly provides power to the motor installed in the bicycles and speeds up the vehicle without paddling. |

| Speed Pedelec | Speed pedelec is e-bikes similar to pedal-assist e-bikes as they do not have throttle functionality. However, these e-bikes are integrated with an electric motor which delivers power of approximately 500 W and more. The speed limit of such e-bikes is generally 45 km/h (28 mph) in most of the countries. |

| City/Urban | The city or urban e-bikes are designed with daily commuting standards and functions to be operated within the city and urban areas. The bicycles include various features and specifications such as comfortable seats, sit upright riding posture, tires for easy grip and comfortable ride, etc. |

| Trekking | Trekking and mountain bikes are special types of e-bikes that are designed for special purposes considering the robust and rough usage of the vehicles. These bicycles include a strong frame, and wide tires for better and advanced grip and are also equipped with various gear mechanisms which can be used while riding in different terrains, rough grounded, and tough mountainous roads. |

| Cargo/Utility | The e-cargo or utility e-bikes are designed to carry various types of cargo and packages for shorter distances such as within urban areas. These bikes are usually owned by local businesses and delivery partners to deliver packages and parcels at very low operational costs. |

| Lithium-ion Battery | A Li-ion battery is a rechargeable battery, which uses lithium and carbon as its constituent materials. The Li-Ion batteries have a higher density and lesser weight than sealed lead acid batteries and provide the rider with more range per charge than other types of batteries. |

| Lead Acid Battery | A lead acid battery refers to sealed lead acid battery having a very low energy-to-weight and energy-to-volume ratio. The battery can produce high surge currents, owing to its relatively high power-to-weight ratio as compared to other rechargeable batteries. |

| Other Batteries | This includes electric bikes using nickel–metal hydroxide (NiMH), silicon, and lithium-polymer batteries. |

| Business-to-Business (B2B) | The sales of e-bikes to business customers such as urban fleet and logistics company, rental/sharing operators, last-mile fleet operators, and corporate fleet operators are considered under this category. |

| Business-to-Customers (B2C) | The sales of electric scooters and motorcycles to direct consumers is considered under this category. The consumers acquire these vehicles either directly from manufacturers or from other distributers and dealers through online and offline channel. |

| Unorganized Local OEMs | These players are small local manufacturers and assemblers of e-bikes. Most of these manufacturers import the components from China and Taiwan and assemble them locally. They offer the product at low cost in this price sensitive market which give them advantage over organized manufacturers. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Dockless e-Bikes | Electric bikes that have self-locking mechanisms and a GPS tracking facility with an average top speed of around 15mph. These are mainly used by bike-sharing companies such as Bird, Lime, and Spin. |

| Electric Vehicle | A vehicle which uses one or more electric motors for propulsion. Includes cars, scooters, buses, trucks, motorcycles, and boats. This term includes all-electric vehicles and hybrid electric vehicles |

| Plug-in EV | An electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. In this report we use the term for all-electric vehicles to differentiate them from plug-in hybrid electric vehicles. |

| Lithium-Sulphur Battery | A rechargeable battery that replaces the liquid or polymer electrolyte found in current lithium-ion batteries with sulfur. They have more capacity than Li-ion batteries. |

| Micromobility | Micromobility is one of the many modes of transport involving very-light-duty vehicles to travel short distances. These means of transportation include bikes, e-scooters, e-bikes, mopeds, and scooters. Such vehicles are used on a sharing basis for covering short distances, usually five miles or less. |

| Low Speed Electric Vehicls (LSEVs) | They are low speed (usually less than 25 kmph) light vehicles that do not have an internal combustion engine, and solely use electric energy for propulsion. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms