Dry Whole Milk Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 19.82 Billion |

| Market Size (2031) | USD 23.99 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

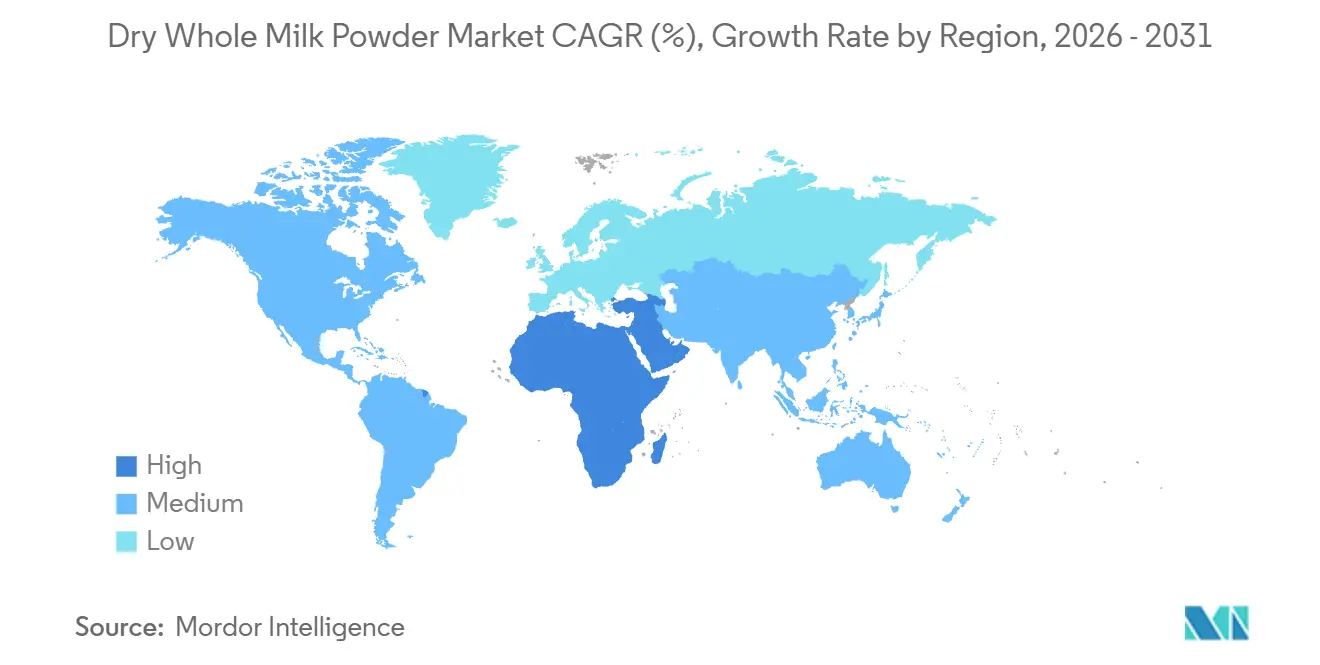

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

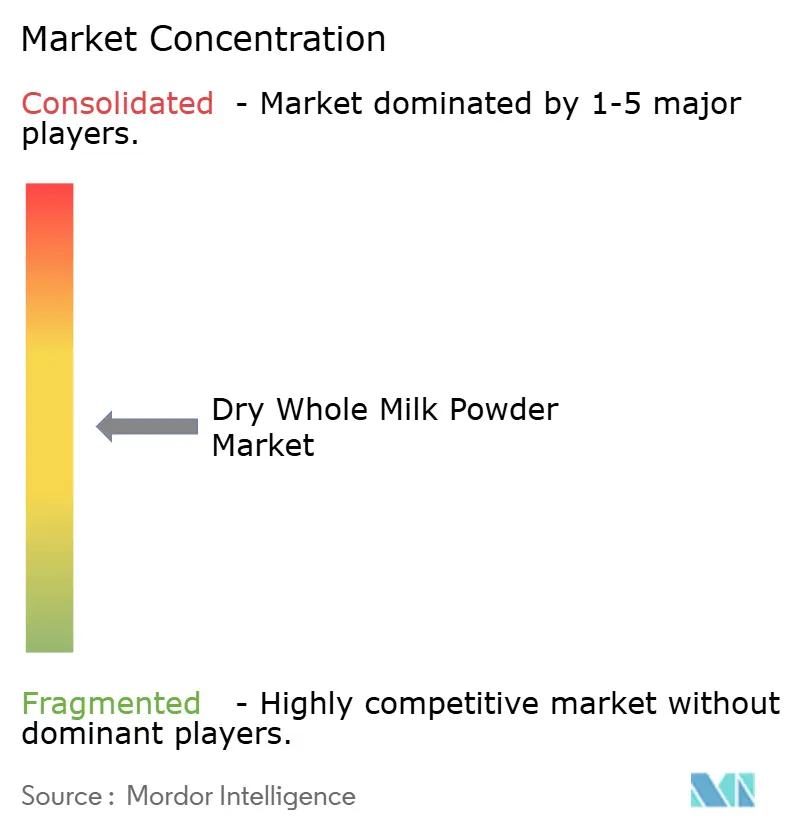

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dry Whole Milk Powder Market Analysis by Mordor Intelligence

The dry whole milk powder market size is projected to expand from USD 19.08 billion in 2025 and USD 19.82 billion in 2026 to USD 23.99 billion by 2031, registering a 3.89% CAGR between 2026 and 2031. Heightened infant-formula procurement in Asia-Pacific, food-security programs in emerging economies, and technology upgrades in spray-drying collectively lift demand even as lactose-intolerance prevalence, plant-based dairy competition, and raw-milk price swings temper momentum. Consolidation among vertically integrated processors intensifies competitive rivalry, while packaging and channel shifts toward stand-up pouches and direct-to-consumer e-commerce create premium-pricing pockets. Supply-side concentration in New Zealand, Europe, and a handful of cooperative giants exposes the dry whole milk powder market to weather events and regulatory shocks, raising the strategic value of diversified sourcing agreements and inventory hedging.

Key Report Takeaways

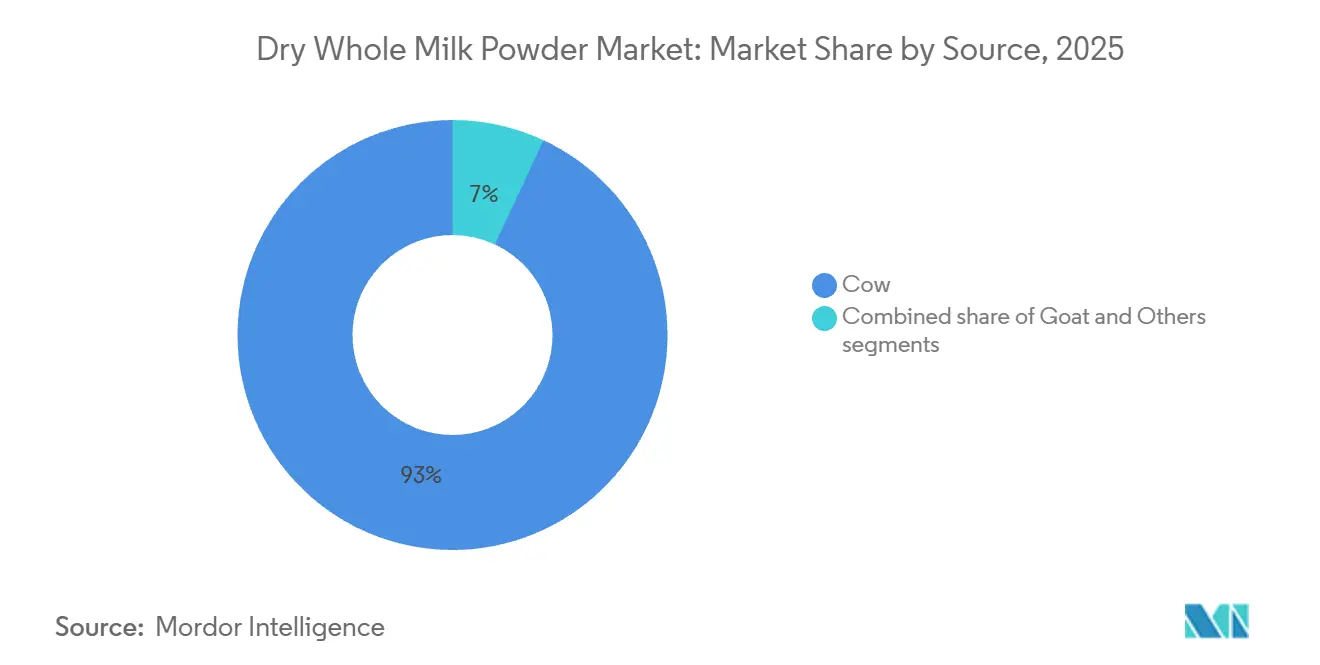

- By source, cow milk led with 93.04% of the dry whole milk powder market share in 2025, whereas goat milk derivatives are forecast to record a 4.01% CAGR through 2031.

- By category, conventional grades accounted for 96.12% of the value in 2025, while organic products are projected to grow at a 4.58% CAGR to 2031.

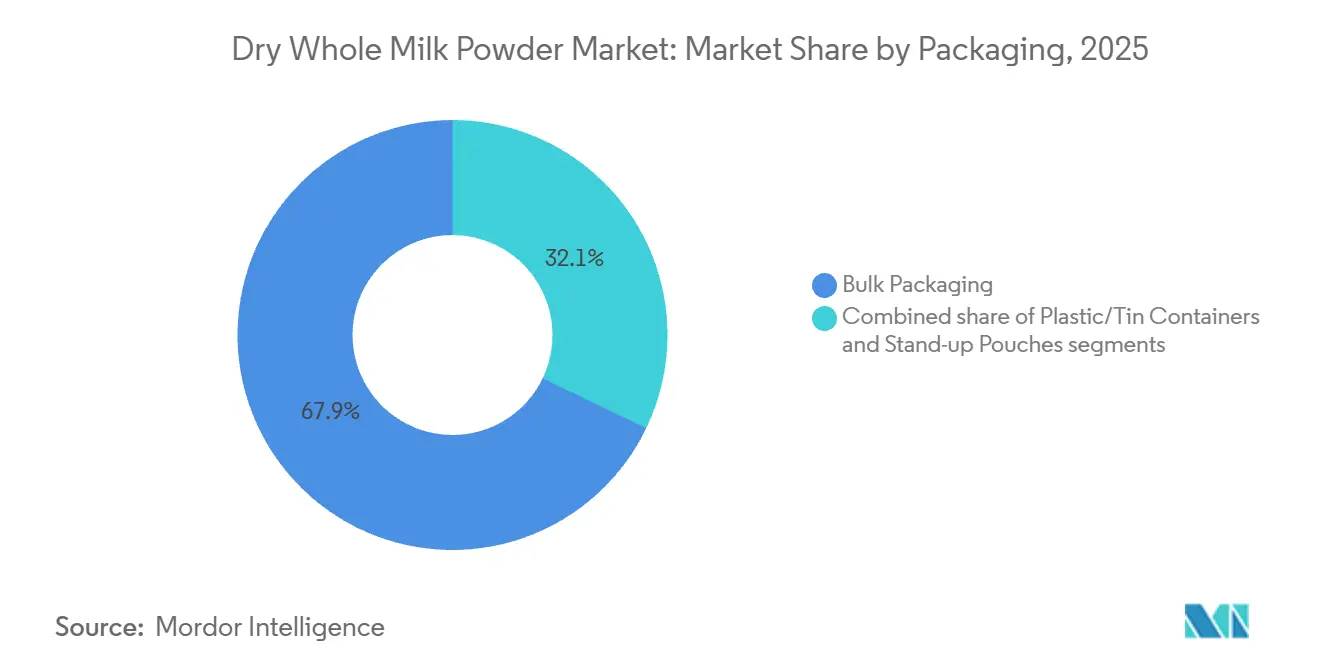

- By packaging, bulk formats dominated with 67.87% share in 2025, whereas stand-up pouches are poised for a 3.98% CAGR through 2031.

- By distribution channel, the industrial segment held 51.37% of value in 2025, while retail sales are estimated to climb at a 5.01% CAGR to 2031.

- By geography, Asia-Pacific captured 38.65% of 2025 revenue, whereas the Middle East & Africa region is set for the fastest 4.33% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dry Whole Milk Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for infant formula and baby foods due to nutritional needs and breastfeeding challenges | +1.2% | Global, with concentration in Asia-Pacific (China, India, Southeast Asia) and Middle East | Medium term (2-4 years) |

| Long shelf life aiding food security programs | +0.8% | Global, strongest in Sub-Saharan Africa, South Asia, Middle East, and Latin America | Long term (≥4 years) |

| Convenience in reconstitution for beverages, cooking, and baking | +0.5% | Global, with higher adoption in North America, Europe, and urban Asia-Pacific | Short term (≤2 years) |

| Popularity of fortified milk powders with added vitamins | +0.6% | Global, led by India, Canada, European Union, and Southeast Asia | Medium term (2-4 years) |

| Rise of high-protein convenience nutrition | +0.4% | Global, with technology adoption concentrated in New Zealand, Europe, and North America | Long term (≥4 years) |

| Convenience for foodservice and institutional use | +0.5% | Global, particularly North America, Europe, and institutional buyers in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Infant Formula and Baby Foods Due to Nutritional Needs and Breastfeeding Challenges

Infant formula is the largest driver for dry whole milk powder, with annual production exceeding 1.5 million metric tons, 90% of which is dairy-based. In the U.S., infant formula manufacturing uses about 1.2 billion pounds of milk annually, ensuring steady demand despite declining birth rates in developed markets. In China, births dropped 17% year-on-year to 7.92 million in 2025, but premium and super-premium infant formula segments grew. Products priced above RMB 350 per can saw 10.8% value growth, and goat milk powder experienced significant expansion. This reflects parents' focus on immune support, digestibility, and functional ingredients like human milk oligosaccharides and lactoferrin, which require higher milk-solids content and stricter quality standards. China's GB 19644-2024 regulation, effective February 2025, sets stricter requirements for whole milk powder, including at least 26% fat, a maximum of 5% moisture, and protein making up at least 34% of non-fat solids. These changes favor vertically integrated producers. While volume growth may slow due to declining births, higher spending per unit will benefit brands with clinical evidence, traceability, and investments in genetics and consumer education.

Long Shelf Life Aiding Food Security Programs

Dry whole milk powder's shelf stability makes it essential for humanitarian and government nutrition programs, especially in areas with logistical and climate challenges. The World Food Programme uses it in fortified blended foods and ready-to-use therapeutic foods, following Codex Alimentarius guidelines that require at least 50% of protein in these foods to come from milk for treating severe acute malnutrition. In 2024, the Food and Agriculture Organization reported that 28% of the global population faced moderate to severe food insecurity, driving demand for shelf-stable dairy in emergency and school feeding programs. Government procurement and multilateral agency tenders stabilize demand but focus on cost over premium features, reducing profit margins. New processing methods, including no-heat spray drying technologies, reduce energy consumption by over 40% while maintaining nutritional value[1]Source: United States Department of Energy, “No Heat Spray Drying Technology,” energy.gov. These energy-efficient processes create advantages for production in energy-abundant regions, especially when serving markets with high energy costs.

Popularity of Fortified Milk Powders with Added Vitamins

Regulatory changes are transforming product formulations and competitive strategies in the fortification market. In Canada, a new rule effective January 2026 will require milk to contain 5 micrograms of vitamin D per 250 milliliters, aligning with updated dietary guidelines and public health goals for bone and immune health. India’s Food Safety and Standards Authority has proposed labeling rules mandating clear nutrition details and a milk logo, increasing focus on ingredient transparency. The European Union has approved iron milk caseinate for use in various foods, expanding options for fortified dairy products. These changes raise compliance costs, challenging smaller producers without strong R&D and quality control, while offering opportunities for brands that can prove health benefits through clinical trials. Fortification is shifting from a basic feature to a premium strategy, especially in markets where consumers value added vitamins for preventive health and are willing to pay more for certified products.

Rise of High-Protein Convenience Nutrition

The high-protein nutrition trend significantly influences the dry whole milk powder market growth. Manufacturers of sports nutrition and meal replacement products increasingly select dry whole milk powder as a key ingredient due to its complete amino acid profile and higher digestibility compared to plant-based proteins. The 2025 IFIC Food Health Survey indicates that 23% of Americans follow a high-protein diet, creating substantial demand for protein-rich dairy ingredients[2]Source: International Food Information Council, “2025 IFIC Food Health Survey ,” ific.org. Premium positioning dominates in North America and European markets, while urban centers across Asia-Pacific show increased adoption among health-conscious millennials and Gen Z consumers. Research validating dairy proteins' benefits for muscle synthesis and metabolic health strengthens dry whole milk powder's position as a preferred protein source over synthetic alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-milk price volatility | -0.7% | Global, with acute impact in North America, Europe, and Oceania dairy-exporting regions | Short term (≤2 years) |

| Plant-based dairy substitutes | -0.5% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Rising lactose intolerance | -0.4% | Global, most pronounced in East Asia (85-90% prevalence), Africa (65-90%), and South America (50-70%) | Long term (≥4 years) |

| Stringent food safety and quality regulations | -0.3% | Global, with highest compliance burden in European Union, North America, China, and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Milk Price Volatility

Dry whole milk powder producers face shrinking margins and challenges in forward contracting due to unstable input costs. The USDA forecasts the all-milk price to drop to USD 21.15 per hundredweight in 2026 from USD 21.60 in 2025, while nonfat dry milk prices are expected to decline from USD 1.24 in 2025 to USD 1.215 in 2026. Despite these minor price drops, high feed, labor, and energy costs are causing negative margins for many dairy farms. This financial pressure is driving farm closures in the U.S. and Europe, reducing the raw milk supply base. However, total milk production is projected to rise slightly to 227.9 billion pounds in 2026 from 227.3 billion in 2025, due to higher productivity per cow. Supply concentration in New Zealand and a few European cooperatives increases price volatility, especially during disruptions like weather events or policy changes. For instance, New Zealand’s projected 59% share of global whole milk powder exports by 2034 means a drought or regulatory shift could spike global prices. This creates budgeting challenges for buyers in sensitive markets like government tenders and industrial bakeries, while premium infant formula producers can pass on costs, widening the gap between commodity and value-added products.

Plant-Based Dairy Substitutes

The growing adoption of alternative milk products, particularly plant-based options, is increasingly constraining the growth of the dry whole milk powder market. As consumers become more environmentally conscious and adopt dietary preferences such as vegan or lactose-free lifestyles, demand is gradually shifting toward plant-based substitutes. This competitive pressure is especially pronounced in North America and Europe, where products such as oat, almond, and soy milk have achieved strong retail penetration and well-established distribution networks. Furthermore, according to the 2025 IFIC Food & Health Survey, approximately 18% of Americans follow a plant-based diet, underscoring a structural shift in consumption patterns that is directly impacting demand for traditional dairy products, including dry whole milk powder[3]Source: International Food Information Council, “2025 IFIC Food Health Survey ,” ific.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Goat Milk Powder Gains Premium Positioning

In 2025, cow milk led the dry whole milk powder market, making up 93.04% of the total volume. This dominance was supported by strong supply chains, cost-efficient processing, and broad regulatory approval, particularly in infant formulas and food ingredient uses. The extensive infrastructure, including millions of dairy farms, cooperative collection systems, and specialized drying facilities, ensures cow milk remains the top choice for budget-conscious buyers and large-scale contracts.

Meanwhile, goat milk products are expected to grow at a 4.01% CAGR through 2031. This growth is driven by their popularity in premium infant formulas and functional nutrition products. Goat milk is promoted as easier to digest due to its smaller fat globules and unique protein structure, especially its lower alpha-S1 casein content. This makes it appealing to parents looking for alternatives for infants with cow milk sensitivities. The Asia-Pacific region is the fastest-growing market, fueled by rising demand for infant formulas. Full cream goat milk powder commands a 30-50% higher price than cow milk powder, offering significant profits to producers. These producers successfully manage the fragmented goat dairy supply chain and invest in odor-reduction processes to improve consumer acceptance.

By Category: Organic Dairy Commands Premium Despite Supply Constraints

In 2025, conventional dry whole milk powder held 96.12% of the market share, reflecting the cost and complexity challenges of organic dairy. Synthetic inputs in conventional production improve efficiency and lower costs, keeping bulk prices below USD 3,000 per metric ton. U.S. conventional milk production reached 227.3 billion pounds in 2025 and is expected to rise slightly to 227.9 billion pounds in 2026, driven by higher cow productivity despite farm closures. China's GB 19644-2024 standard requires at least 26% fat and 34% protein in both conventional and organic whole milk powder. Conventional products meet these standards without the added costs of organic certification and supply-chain segregation. Conventional dairy also allows flexible sourcing and blending during demand surges, unlike organic producers who face stricter traceability and single-origin rules.

Organic dairy is expected to grow at a 4.58% CAGR through 2031, driven by consumer demand for health, environmental, and animal welfare benefits. These factors support retail price premiums of 50-100% and reduce price sensitivity during downturns. In December 2025, Germany's organic milk premium reached 15.6 EUR per 100 kilograms, the highest in five years, reflecting strong demand and limited supply. Organic certification requires multi-year transitions, pasture access, and bans on synthetic inputs, discouraging conventional farmers due to volatile premiums. Organic feed costs are 20-40% higher, and herd productivity is lower due to restrictions on growth hormones and antibiotics. Organic-certified drying facilities must prevent cross-contamination with conventional products, requiring dedicated lines or rigorous cleaning, which reduces efficiency.

By Packaging: Stand-Up Pouches Drive Consumer Convenience Innovation

In 2025, bulk packaging accounted for 67.87% of dry whole milk powder volume. This format serves industrial buyers, foodservice distributors, and government agencies that focus on cost efficiency and centralized reconstitution, where packaging aesthetics are unimportant. The 25-kilogram paper sacks and 50-kilogram bags dominate this segment, designed for easy handling and storage rather than retail display. Packaging costs for bulk formats are under 2% of the total product cost, compared to 8-12% for consumer-sized containers. Bulk packaging reflects the market's B2B focus. Infant formula manufacturers use bulk powder for blending, industrial bakeries for dough and cream fillings, and government programs for school feeding and food security, prioritizing reduced waste and higher nutritional value per dollar.

Stand-up pouches are forecast to grow at 3.98% CAGR through 2031, driven by retail channel expansion and consumer demand for portion control, resealability, and shelf appeal that influence point-of-sale purchasing decisions in supermarkets, online grocery platforms, and specialty health stores. Stand-up pouches enable single-serve and family-size SKUs ranging from 200 grams to 2 kilograms that fit retail shelf space, incorporate zip-lock closures that preserve freshness after opening by preventing moisture ingress and oxidation, and provide printable surface area for branding, nutritional messaging, and usage instructions that communicate product differentiation at the moment of purchase. The packaging shift is most pronounced in e-commerce, where lightweight flexible packaging reduces shipping costs by 20-30% compared to rigid containers and minimizes breakage risk during last-mile delivery, a critical consideration as online grocery platforms such as Weee! reported over 70 million orders since 2015 and expanded SKU counts to serve diaspora and health-focused consumer segments.

By Distribution Channel: Retail Growth Outpaces Industrial Dominance

In 2025, the industrial channel held 51.37% of the dry whole milk powder market value, highlighting its importance in B2B applications like infant formula, bakery, processed foods, and nutritional supplements. Here, whole milk powder is used as an ingredient rather than a consumer product. Industrial buyers focus on consistent quality, requiring fat content within ±0.5%, stable protein ratios, and compliance with ISO 22000 and HACCP standards. They also value competitive pricing and reliable supply for efficient production and inventory management. In the U.S., infant formula production uses about 1.2 billion pounds of milk annually, while global production exceeds 1.5 million metric tons, with 90% of ingredients dairy-based. This steady demand protects industrial channels from consumer market fluctuations.

Retail distribution is expected to grow at a 5.01% CAGR through 2031, driven by e-commerce, direct-to-consumer sales, and premium packaged dairy products. Online platforms help niche brands reach health-conscious and diaspora consumers without high brick-and-mortar costs. For example, Weee! has processed over 70 million orders since 2015. Retail prices for whole milk powder range from USD 12.49 for mainstream brands to USD 94.39 for organic multi-packs, showing the potential for higher margins when producers bypass distributors. Supermarkets and hypermarkets offer wide reach but require slotting fees and promotions, which can take 15-20% of gross margins. Pharmacies and drugstores, associated with health and wellness, command 10-15% higher prices for the same products.

Geography Analysis

By 2025, the Asia-Pacific region is set to command a 38.65% share of the market, buoyed by factors like population growth, urbanization, and rising disposable incomes that favor premium dairy purchases. Despite grappling with milk surplus challenges, China remains the dominant player in the market. Meanwhile, in India, a burgeoning middle class is driving a notable surge in demand for convenience foods and infant formulas. The region's growth is further bolstered by maturing food processing industries and enhanced cold-chain infrastructures, facilitating broader product distribution. As economic development progresses, Southeast Asian markets are witnessing robust growth, with urban populations increasingly leaning towards Western dietary preferences.

In the Middle East and Africa, the region is poised to see the highest growth rate at a CAGR of 4.33% through 2031. This growth is underpinned by factors such as population growth, urbanization, and a strengthening economy, all of which are driving up dairy consumption. The MENA region stands out, buoyed by an uptick in per capita dairy availability. However, North African nations face challenges, relying on imported milk powder due to their limited domestic production capabilities and water scarcity issues that hinder dairy farming expansion. Overall, the region's growth trajectory is a testament to its demographic advantages and economic progress, leading to heightened consumption of processed foods.

North America and Europe, as established hubs for production and export, are witnessing steady demand. The U.S. capitalizes on cutting-edge processing technologies and a resilient supply chain. In contrast, European markets are undergoing a phase of consolidation, with companies seeking economies of scale in response to profit pressures. Despite facing global trade uncertainties and stringent environmental regulations curbing expansion, New Zealand's dairy sector is optimistic, anticipating growth driven by export demand. In these mature markets, the focus is shifting from sheer volume growth to value-added products and premium positioning. This shift is evident in their pursuit of differentiation through avenues like organic certifications, tailored formulations, and eco-friendly production practices.

Competitive Landscape

In the dry whole milk powder market, established multinational corporations and emerging regional producers vie for dominance, resulting in moderate fragmentation. With a market intensity rated at 5 out of 10, the landscape neither leans towards excessive fragmentation nor veers into oligopolistic control. Companies are increasingly turning to strategies like vertical integration, technological innovation, and geographic diversification to bolster their competitive edge. Notable players in this arena include Fonterra Co-operative Group Limited, Valio Ltd, Royal FrieslandCampina N.V., Dairygold Co-Operative Society Limited, and Arla Foods amba.

These major players harness economies of scale in both processing and distribution. Yet, they remain agile, catering to a spectrum of customers, from industrial buyers to everyday retail consumers. A clear trend emerges: a focus on consolidation and vertical integration. Furthermore, technology adoption stands out as a key differentiator in this competitive landscape. Companies are channeling investments into energy-efficient processing equipment and innovative packaging solutions, achieving cost reductions while simultaneously enhancing product quality.

Emerging opportunities, or "white-space" prospects, are evident in specialty formulations tailored for lactose-intolerant consumers, the pursuit of organic certification, and the burgeoning direct-to-consumer channels that sidestep traditional distribution intermediaries. Meanwhile, the USDA's rollout of HACCP requirements introduces compliance costs. These costs, while burdensome, may inadvertently favor larger processors with pre-existing quality systems, hinting at a potential acceleration in industry consolidation.

Dry Whole Milk Powder Industry Leaders

Fonterra Co-operative Group Limited

Valio Ltd

Royal FrieslandCampina N.V.

Dairygold Co-Operative Society Limited

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lactalis completed the acquisition of Fonterra's global consumer business (excluding China) for USD 3.69 billion, securing 16 manufacturing facilities across Australia, New Zealand, Sri Lanka, Malaysia, Indonesia, and Saudi Arabia, along with approximately 4,300 employees and brands including Anchor, Mainland, Perfect Italiano, and Western Star.

- June 2025: Darigold opened its USD 1 billion processing facility in Pasco, Washington. The facility processes 8 million pounds of milk daily and produces milk powders for U.S. and international markets. The plant employs 200 people directly and supports more than 1,000 regional jobs. The facility incorporates sustainability features that align with U.S. Dairy 2050 environmental goals.

- April 2025: Arla Foods and DMK Group merged to form Europe's largest farmer-owned dairy cooperative, representing more than 12,000 dairy farmers with an expected annual revenue of EUR 19 billion. The merger strengthens market position and expands product portfolio while advancing dairy technology innovation and market reach.

Global Dry Whole Milk Powder Market Report Scope

| Cow |

| Goat |

| Others |

| Conventional |

| Organic |

| Plastic/Tin Containers |

| Stand-up Pouches |

| Bulk Packaging |

| Retail | Supermarkets/Hypermarkets |

| Pharmacy and Drugstores | |

| Online Retail Stores | |

| Others | |

| Foodservice | |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Cow | |

| Goat | ||

| Others | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging | Plastic/Tin Containers | |

| Stand-up Pouches | ||

| Bulk Packaging | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Pharmacy and Drugstores | ||

| Online Retail Stores | ||

| Others | ||

| Foodservice | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the dry whole milk powder market be by 2031?

The dry whole milk powder market size is forecast to reach USD 23.99 billion by 2031, expanding at a 3.89% CAGR from 2026 to 2031.

Which source segment is growing fastest?

Goat-milk powder is expected to post a 4.01% CAGR through 2031, outpacing cow milk due to digestibility positioning in premium infant-formula channels.

What packaging format offers the strongest retail momentum?

Stand-up pouches are projected to grow at a 3.98% CAGR, reflecting convenience and e-commerce shipping advantages.

Which region is poised for the highest growth?

The Middle East & Africa region is forecast for a 4.33% CAGR through 2031, driven by population growth and import reliance.

Page last updated on: