Organic Cheese Powder Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

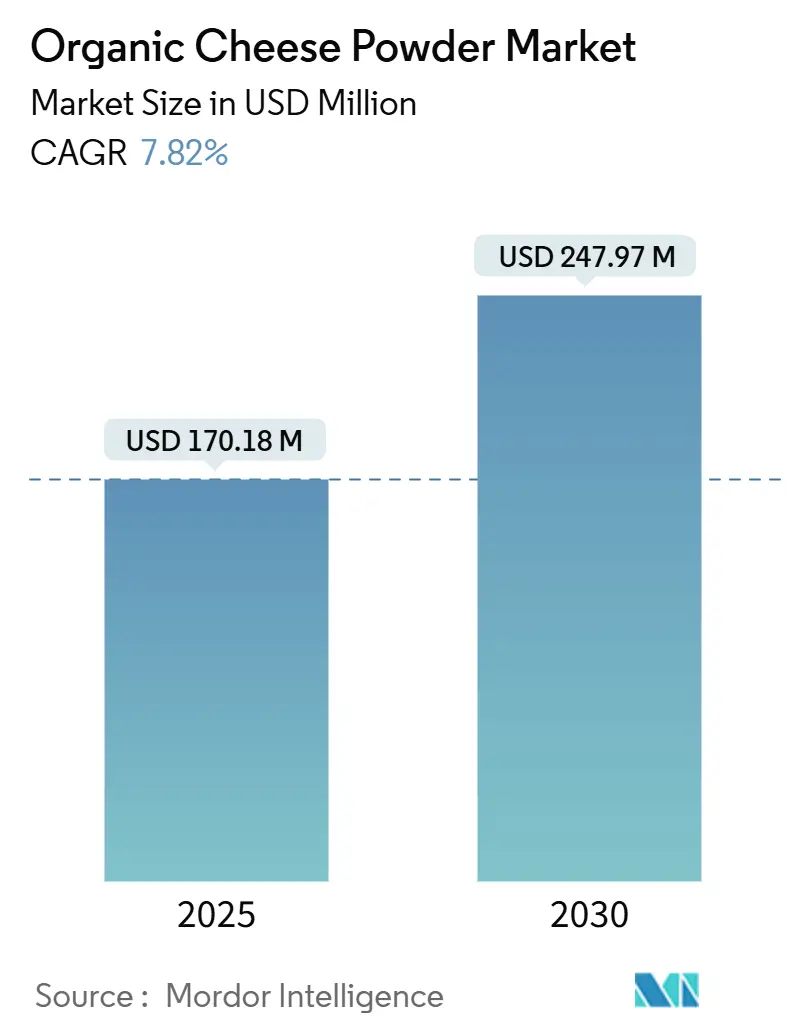

| Market Size (2025) | USD 170.18 Million |

| Market Size (2030) | USD 247.97 Million |

| Growth Rate (2025 - 2030) | 7.82% CAGR |

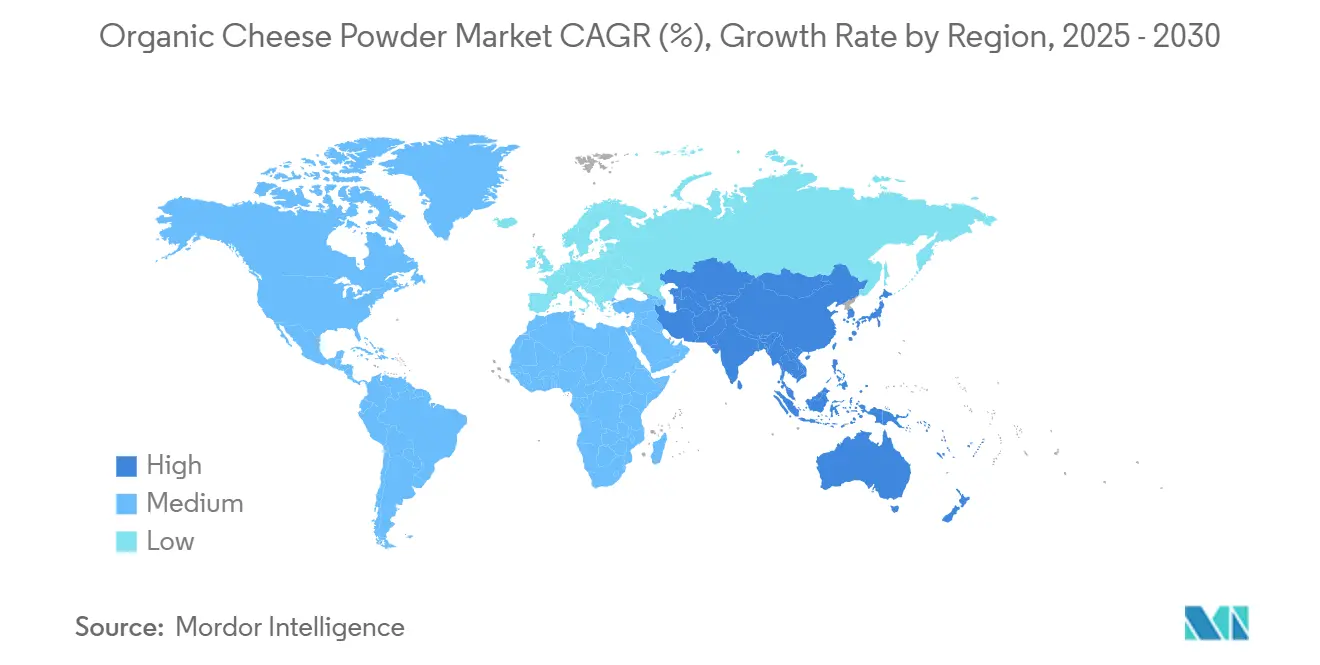

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

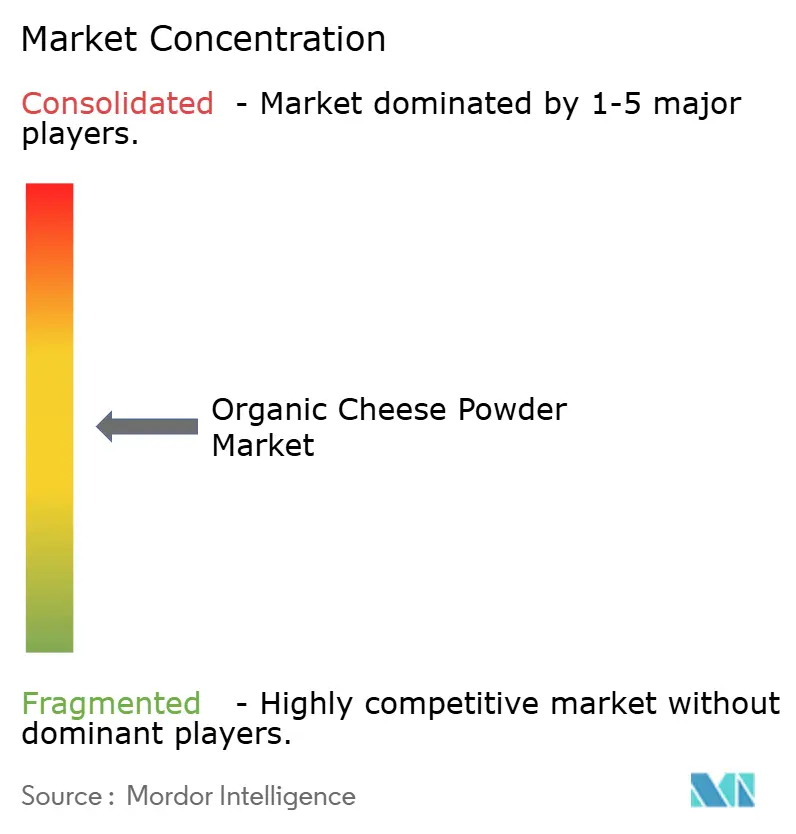

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Cheese Powder Market Analysis by Mordor Intelligence

The organic cheese powder market size is estimated to be USD 170.18 million in 2025 and is forecast to advance at a 7.82% CAGR to reach USD 247.97 million in 2030. Robust growth is shaped by health-focused consumers demanding clean-label foods, tighter organic enforcement that elevates supply-chain trust, and broader foodservice use of premium natural ingredients. Companies respond with capacity expansions that secure certified milk supplies, integrate vertical processes, and install automated traceability systems that comply with the USDA Strengthening Organic Enforcement rule. Rising flexitarian diets and hybrid plant-dairy recipes amplify demand as flavor houses seek organic cheese powders that deliver familiar taste without synthetic additives. Although price volatility in organic milk creates procurement risks, programs such as the USDA Organic Dairy Market Assistance Program help stabilize inputs and encourage processor participation. Competitive intensity is moderate because no single firm exceeds a dominant share, yet the entrance of precision-fermented proteins is nudging incumbents to differentiate through ingredient purity, functional performance, and regional diversification.

Key Report Takeaways

- By product type, cheddar led with 42.55% of the organic cheese powder market share in 2024, while parmesan is projected to grow at an 8.71% CAGR through 2030.

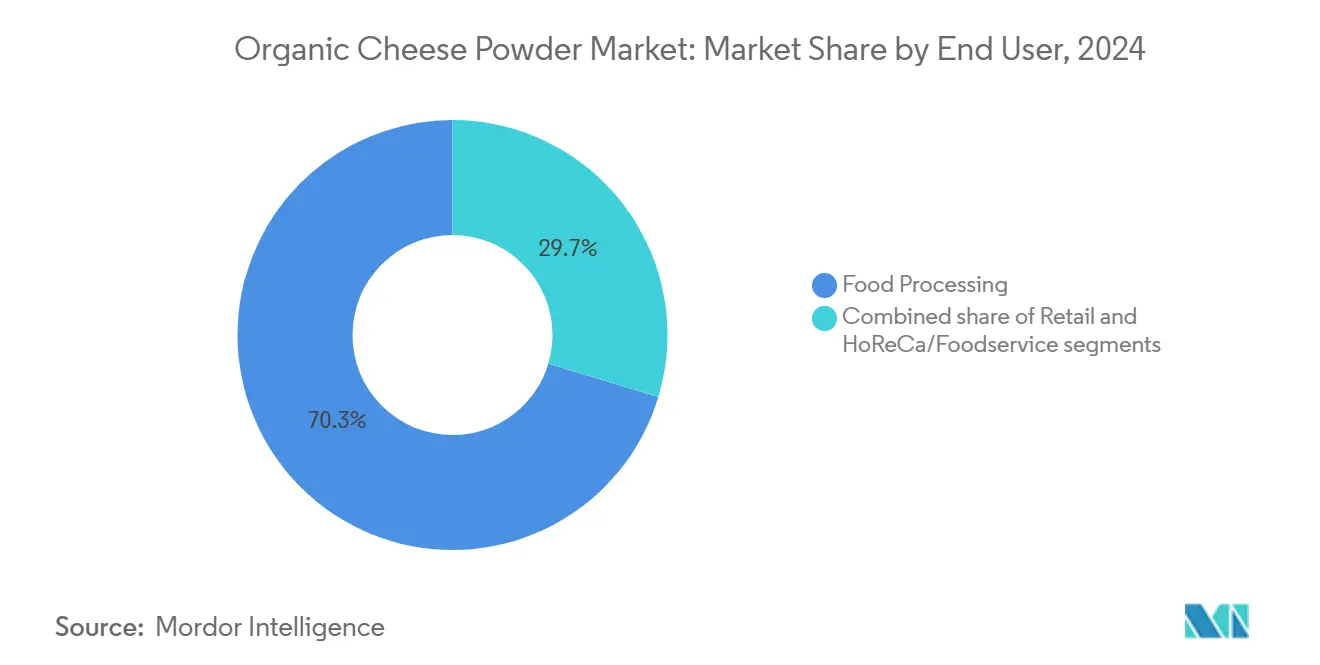

- By end user, food processing accounted for a 70.34% share of the organic cheese powder market size in 2024, whereas retail channels are advancing at a 9.23% CAGR to 2030.

- By geography, North America captured 38.19% of the organic cheese powder market share in 2024, and Asia-Pacific is poised for an 8.45% CAGR through 2030.

Global Organic Cheese Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer awareness about health and environmental benefits of organic food | +2.1% | Global, with strongest impact in North America and European Union | Medium term (2-4 years) |

| Emerging demand from plant-forward flexitarians | +1.8% | North America and European Union core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Consumer preference for clean-label and natural ingredients in food products | +1.5% | Global | Long term (≥ 4 years) |

| Innovation in product development catering to niche dietary preferences and food trends | +1.3% | North America and European Union, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing demand in foodservice and specialty outlets for organic ingredients | +1.0% | Global, with early gains in North America, European Union, urban Asia-Pacific | Medium term (2-4 years) |

| Certification and transparency boosting consumer trust (e.g., USDA Organic) | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing consumer awareness about health and environmental benefits of organic food

Increasing consumer awareness of the health and environmental advantages of organic food is driving a significant shift in demand for organic dairy ingredients. High levels of trust in certifications, such as the USDA organic seal, are enabling food manufacturers to adopt premium positioning strategies by emphasizing ingredient transparency and health benefits in their sourcing decisions. For example, the USDA's Organic Transition Initiative, introduced in June 2022 with a USD 300 million investment over five years, supports producers by funding market development and expanding processing capacities [1]Source: U.S. Department of Agriculture (USDA), "USDA to Invest up to $300 million in New Organic Transition Initiative", usda.gov. This initiative allows organic cheese powder producers to scale operations while maintaining strict certification compliance. Additionally, the program aligns with rising environmental awareness, as organic farming practices improve soil health and biodiversity while appealing to sustainability-conscious consumers who prioritize eco-friendly purchasing decisions. The combination of health-focused consumer education and environmental priorities is driving market growth, extending beyond traditional organic buyers. This integrated approach, supported by public policy and evolving consumer preferences, is accelerating the adoption of organic cheese powder globally. Companies like Lactosan are leveraging consumer trust and sustainability commitments to expand their market presence. This alignment is critical, enhancing production capacity, reinforcing the importance of certifications, and sustaining growth in the global organic cheese powder market.

Emerging demand from plant-forward flexitarians

Flexitarian dietary patterns are driving shifts in demand dynamics within the global organic cheese powder market, as consumers increasingly favor plant-dairy blend formulations and clean-label convenience products. In the UK, the flexitarian demographic expanded from 20.4% in 2022 to 23.2% in 2024, according to the Agriculture and Horticulture Development Board (AHDB), outpacing growth in strictly vegetarian or vegan segments [2]Source: Agriculture and Horticulture Development Board (AHDB), "Flexitarian trends: Shifting Diets and Changing Preferences", ahdb.org.uk. This trend is spurring product innovation, with manufacturers developing versatile organic cheese powders that enhance flavor profiles in plant-forward applications while meeting clean-label requirements, a critical factor for both consumer packaged goods and foodservice operators. As flexitarians seek ingredient flexibility within single menu offerings, foodservice providers are increasingly sourcing organic cheese powders that align with diverse dietary preferences, supporting sustainable demand and hybrid menu strategies. Companies like Lactosan are leading this innovation by offering pure and blended cheese powders designed for maximum versatility, clean-label compliance, and food safety, making them suitable for industrial and restaurant use. The alignment of flexitarian preferences with organic sourcing is driving manufacturers to focus on product differentiation, formulation adaptability, and transparent labeling. Organic cheese powders are positioned not as competitors but as complementary components in plant-dairy blends. This evolving market landscape is fostering sustained growth, as the expanding flexitarian segment drives further research, collaboration, and supply chain integration in organic cheese powder production and distribution.

Consumer preference for clean-label and natural ingredients in food products

In the global organic cheese powder market, clean-label and natural ingredient preferences have become critical drivers for market entry. This trend is particularly evident as premium food categories increasingly emphasize transparent and traceable sourcing. With the USDA's Strengthening Organic Enforcement rule taking effect in March 2024, manufacturers must meet stricter verification standards. Companies that excel in ensuring traceability and implementing robust fraud prevention measures across the supply chain are positioned to gain a competitive advantage. This regulatory shift aligns with growing consumer demand for clean-label formulations, pushing organic cheese powders to deliver full functionality without artificial additives. Initiatives such as the U.S.-Japan Organic Equivalence Arrangement and ongoing updates to EU organic regulations facilitate cross-border trade while maintaining clean-label standards, thereby expanding opportunities for compliant brands. As a result, segments like snacks, bakery products, and ready meals are experiencing tangible benefits. Consumers are increasingly scrutinizing ingredient lists, favoring simplicity and familiarity, which has driven demand for organic cheese powders with recognizable and pronounceable names. Brands like Frontier Co-op have leveraged these trends by launching organic cheese powders designed to meet clean-label requirements. These efforts have secured premium shelf placements and expanded distribution networks. Companies that prioritize transparency and certification compliance are capturing greater market share and achieving premium pricing, reinforcing clean-label initiatives as a key driver of innovation and growth in the global organic cheese powder market.

Increasing demand in foodservice and specialty outlets for organic ingredients

The increasing demand for organic ingredients in foodservice and specialty outlets is driving growth in the organic cheese powder market. In the UK, the Office for National Statistics reports a rise in foodservice businesses, increasing from 144,721 in 2020 to 152,598 in 2023 [3]Source: Office for National Statistics (UK), "Annual Business Survey - 2023 Results, Section I", ons.gov.uk. This expansion highlights an ecosystem increasingly focused on sourcing high-quality organic inputs. Consequently, foodservice operators are turning to organic cheese powders to meet consumer preferences for health and sustainability. This shift aligns with broader trends favoring natural and transparent ingredient sourcing, fostering menu innovation and competitive differentiation. Brands like Bluegrass Ingredients, Inc. are capitalizing on this demand by offering certified organic cheese powders that meet stringent quality and clean-label standards, building trust and encouraging repeat purchases. Specialty outlets dedicated to organic and natural foods further support this trend by emphasizing ingredient provenance and environmental responsibility. Together, these factors are enhancing the role of organic cheese powders across diverse culinary applications, from casual dining to upscale gastronomy. As foodservice operators continue to grow in number and sophistication, their demand for organic dairy ingredients, including cheese powders, is expected to accelerate. This trend is driving sustained global market growth and reinforcing the value proposition of certified organic products. The resulting positive feedback loop, driven by improved supply chain capabilities and increased consumer awareness, is further advancing market development in this segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight organic milk supply and price volatility | -1.2% | Global, with acute impact in North America and European Union | Short term (≤ 2 years) |

| Complex and costly organic certification process adds production overhead | -0.8% | Global, with higher barriers in developing markets | Long term (≥ 4 years) |

| Limited awareness and education in emerging markets restraining adoption | -0.6% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Competition from plant-based "cheeze" powders | -0.5% | North America and European Union core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight organic milk supply and price volatility

Supply constraints and price volatility in organic milk affect organic cheese powder production, impacting both manufacturers and food industry customers. The organic dairy sector's growth remains constrained by fundamental factors, including the mandatory three-year farm conversion period and elevated costs for certification and organic feed. USDA and industry data indicate that supply shortages in organic commodity crops limit organic dairy feed availability, creating a recurring pattern where demand exceeds available supply. These conditions impede organic cheese powder manufacturers from securing consistent milk quality and volume necessary for stable production and reliable customer delivery. Horizon Organic and other manufacturers have documented how variable organic milk prices, influenced by weather conditions, feed costs, and seasonal factors, necessitate frequent adjustments to pricing and delivery schedules. This instability affects food manufacturers' ability to plan budgets and maintain consistent formulations, as increased input costs can disrupt procurement strategies. The situation creates opportunities for suppliers who can maintain reliable organic milk sources, as retailers and foodservice operators prioritize stable, long-term supply contracts. The combination of supply constraints and price fluctuations necessitates strategic value chain partnerships, enhanced sourcing strategies, and improved inventory management, which collectively influence the market's development and pricing dynamics.

Competition from plant-based “cheeze” powders

Plant-based "cheeze" powders are increasingly influencing the competitive dynamics of the organic cheese powder market. These dairy-free alternatives are gaining significant traction among vegan and lactose-intolerant consumers, driven by a growing focus on health, sustainability, and animal welfare. Innovations in plant-based formulations now closely replicate the taste, texture, and meltability of traditional cheese powders. Brands such as Daiya Foods are leading this shift by offering an extensive portfolio of plant-based cheese powders for snacks, sauces, and ready meals, targeting both retail and foodservice sectors. In response, organic cheese powder manufacturers are enhancing product differentiation by focusing on clean-label, organic, and functional benefits while addressing consumer demands for transparency and allergen-free options. The increasing availability of plant-based cheese alternatives in supermarkets and specialty stores presents both challenges and opportunities for innovation, prompting organic producers to revisit ingredient sourcing and product development strategies. This competitive landscape highlights the need for organic cheese powder brands to emphasize the unique attributes of authentic dairy while exploring hybrid plant-dairy offerings to align with evolving dietary preferences. The rapid growth of plant-based powders is reshaping consumer expectations and competitive positioning, making it imperative for organic cheese powder manufacturers to adapt their branding, marketing, and innovation strategies to maintain and expand their market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cheddar Dominance Drives Market Maturity

Cheddar variants hold a 42.55% market share in 2024, highlighting their strong consumer appeal and versatility in food manufacturing. Parmesan, on the other hand, is the fastest-growing category, with an 8.71% CAGR projected through 2030. The success of Cheddar-based organic cheese powders is attributed to their alignment with American taste preferences and widespread use in snack foods, prepared meals, and foodservice applications, where familiar flavors drive consumer acceptance. Healthier Comforts' expansion of its specialized Cheddar variants demonstrates how established organic dairy companies are leveraging product innovation to capture premium market segments. Parmesan's rapid growth reflects premiumization trends and increasing sophistication in organic food applications, particularly in gourmet and artisanal product categories, where authentic Italian cheese flavors command higher margins.

Mozzarella and other specialty cheese powder variants collectively account for the remaining market share. Mozzarella benefits from its popularity in pizza and Italian cuisine, while specialty variants address niche dietary preferences and ethnic food applications. Product type segmentation reveals strategic opportunities for manufacturers to develop organic cheese powder blends that combine multiple cheese varieties to create unique flavor profiles and functional characteristics. Companies like Lactalis Ingredients have demonstrated market development strategies through participation in international trade shows such as Gulfood 2025 and FIE 2024, signaling an industry focus on expanding product portfolios and geographic reach. Additionally, the Japanese Agricultural Standards (JAS) expansion in July 2020 to include organic processed foods containing animal-origin ingredients has created new export opportunities for organic cheese powder manufacturers aiming to diversify beyond traditional North American and European markets.

By End User: Food Processing Leadership Faces Retail Channel Disruption

Food processing applications dominate with a 70.34% market share in 2024. However, retail channels are experiencing significant growth, with a 9.23% CAGR projected through 2030. This trend highlights a critical shift toward direct consumer engagement and the convenience-driven consumption of organic foods. The food processing segment's leadership is driven by technical requirements and scale advantages, particularly in business-to-business applications. Organic cheese powders serve as essential functional ingredients in manufactured foods, meeting demands for consistent quality, extended shelf life, and regulatory compliance. The HoReCa/foodservice sector represents a stable middle segment, benefiting from the growing adoption of organic ingredients in restaurants and institutional food preparation. This growth is fueled by consumer demand for transparency and premium dining experiences. The retail segment's rapid expansion reflects changing consumer behavior, with increased direct purchases of organic cheese powder for home cooking and meal preparation, indicating rising culinary sophistication and health consciousness among organic food consumers.

Within the retail subsegment, supermarkets and hypermarkets maintain their traditional leadership in distribution. However, online retail stores are experiencing accelerated growth, driven by the convenience of shopping and subscription-based organic food delivery services. The expansion of retail channels introduces new demands for packaging, branding, and consumer education, which differ significantly from the requirements of business-to-business applications in food processing. Regulatory frameworks, such as the Canadian Organic Standards, expected to be published in November 2020, and the implementation of Canada's Safe Food for Canadians Act in 2019, support the growth of retail channels by ensuring consumer protection and maintaining organic integrity standards.

Geography Analysis

North America holds a dominant 38.19% share of the organic cheese powder market in 2024. This leadership is rooted in decades of organic agriculture evolution, bolstered by strong regulatory initiatives. Notably, the USDA's Organic Transition Initiative, with its USD 300 million five-year commitment, aims to enhance processing and market development for organic foods. Furthermore, the U.S.-Japan Organic Equivalence Arrangement boosts export prospects, permitting USDA-certified organic products to carry the organic label in Japan, thus unlocking new revenue avenues for North American producers. Complementing these efforts, Canada's 2019-enacted Safe Food for Canadians Act fortifies regulatory alignment, streamlining cross-border trade in North America and fostering a unified market for organic dairy ingredients, cheese powders included.

Europe maintains a robust market foothold, driven by discerning consumer demands and stringent regulations prioritizing traceability and protection in organic marketing. The EU's 2022 organic regulation (EU 2018/848) mandates electronic certifications through the TRACES system and tightens group certification rules, influencing organic imports and supply chain checks. Such stringent measures elevate organic cheese powders to a premium status in the region. Moreover, European companies are heavily investing in North American production to cater to global demands. A prime example is Lactalis USA's USD 55 million investment in its California feta cheese facility, showcasing a blend of advanced manufacturing techniques like 3D ergonomic analysis and automation to boost product quality and efficiency.

Asia-Pacific emerges as the fastest-growing market, set to achieve an 8.45% CAGR through 2030. This growth is fueled by a burgeoning middle class, urbanization, and Western dietary trends favoring organic and clean-label foods. Regional governments are backing organic agriculture with evolving regulations, promoting both domestic production and the import of organic cheese powders. In China, there's a surging appetite for organic dairy in snacks, sauces, and baked goods, bolstered by government-led clean-label and safety campaigns. This vibrant landscape showcases a maturing market where heightened consumer awareness, innovative products, and regulatory backing converge, positioning Asia-Pacific's organic cheese powder segment as a pivotal growth driver on the global stage. Meanwhile, South America and the Middle East and Africa present nascent opportunities, with a budding awareness of organic foods, yet necessitating substantial investments in consumer education and certification infrastructure for deeper market penetration.

Competitive Landscape

The competitive landscape of the organic cheese powder market is moderately fragmented. Dominating the scene, companies like Land O'Lakes, Lactosan, and Arla Foods leverage their extensive product portfolios, innovative formulations, and robust distribution networks. These industry leaders are heavily investing in research and development, focusing on enhancing flavor, texture, and ensuring compliance with organic certifications. This strategy aligns them with the rising consumer preference for natural and sustainably sourced products. For instance, Lactosan's emphasis on innovative cheese powder formulations has solidified its reputation for superior flavor quality.

Regional dairy cooperatives and niche organic ingredient suppliers play a pivotal role in the market's competitive dynamics. They provide tailored organic cheese solutions that cater to a spectrum of needs, from food processing and retail to the HoReCa sector. Companies such as Frontier Co-op and DairiConcepts prioritize bespoke product development, addressing specific customer demands. This strategy not only fortifies their position but also enhances their appeal in niche segments. Such a diverse approach to product offerings and market engagement fuels competition, driving both innovation and market expansion.

Sustainability initiatives and broadening distribution channels are foundational to these competitive strategies. Take Arla Foods, for instance: it capitalizes on its global presence and a strong commitment to sustainability, granting it a foothold in the burgeoning markets of Asia-Pacific and Europe. On the other hand, smaller entities like Commercial Creamery Company and Cheesepop Food Group resonate with health-conscious consumers, championing organic authenticity and transparent labeling. Together, these dynamics cultivate a balanced market landscape, where innovation, certification, and sustainability converge, propelling growth and distinction in the global organic cheese powder arena.

Organic Cheese Powder Industry Leaders

-

Lactosan A/S

-

Kerry Group plc

-

Land O'Lakes, Inc.

-

Frontier Co-op

-

Arla Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Kerry Group completed the first phase of a EUR 500 million transaction, selling Kerry Dairy Holdings (Ireland) Limited to Kerry Co-Operative Creameries Limited. This move reinforced Kerry's position as a dedicated B2B player in the taste and nutrition sector. Through this strategic shift, Kerry directed investments into organic ingredient innovations and tailored applications, aligning with the evolving needs of the food industry.

- October 2024: Lactalis USA invested USD 55 million to expand its facility in Tulare, California, aiming to enhance its feta cheese production capacity. The expansion integrated advanced Group technologies, such as automated airflow control and in-line production automation. This initiative created 20 full-time jobs and underscored Lactalis's commitment to strengthening its organic-capable dairy processing infrastructure.

- April 2024: Researchers from the University of Copenhagen, in collaboration with Lactosan A/S, conducted a study to evaluate cheese powder's potential to enhance umami flavors and the kokumi mouthfeel in plant-based dishes. The research analyzed the umami and kokumi characteristics of selected mature Danish cheeses and their powdered forms, aiming to drive the adoption of plant-based foods.

Global Organic Cheese Powder Market Report Scope

| Cheddar |

| Parmesan |

| Mozzarella |

| Other Types |

| Food Processing | |

| HoReCa/Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cheddar | |

| Parmesan | ||

| Mozzarella | ||

| Other Types | ||

| By End User | Food Processing | |

| HoReCa/Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the organic cheese powder market?

The organic cheese powder market size stands at USD 170.18 million in 2025, expanding toward USD 247.97 million by 2030.

Which product type leads sales?

Cheddar variants hold 42.55% market share, benefiting from wide use in snacks and ready meals.

Which region grows the fastest?

Asia-Pacific posts the highest forecast growth at an 8.45% CAGR through 2030 due to rising disposable income and supportive organic regulations.

Why do processors invest heavily in certification compliance?

The Strengthening Organic Enforcement rule increases audit rigor, and processors that demonstrate transparent traceability earn retailer trust and secure premium shelf placement.

Page last updated on: