Cashew Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

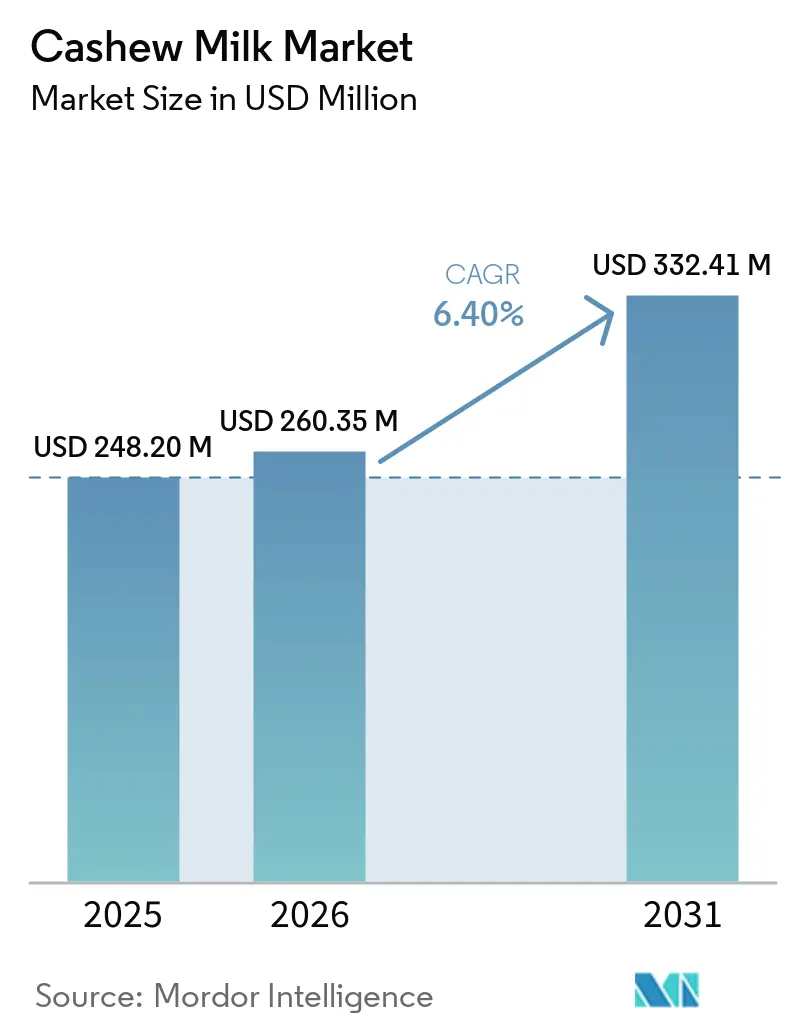

| Market Size (2026) | USD 260.35 Million |

| Market Size (2031) | USD 332.41 Million |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cashew Milk Market Analysis by Mordor Intelligence

The cashew milk market size is projected to be USD 248.2 billion in 2025, USD 260.35 billion in 2026, and reach USD 332.41 billion by 2031, growing at a 6.4% CAGR from 2026 to 2031. As lactose intolerance rates climb and more consumers adopt vegan and flexitarian diets, cashew milk has transitioned from niche shelves to the forefront of mainstream supermarkets, cafés, and e-commerce platforms. This shift is driven by the beverage’s naturally creamy texture and its appeal as a plant-based alternative to traditional dairy. To compete nutritionally with dairy and cater to the preventive health demands of millennials and Gen Z, manufacturers are enriching their products with calcium, vitamin D, vitamin B12, probiotics, and omega-3s. These fortifications not only enhance the nutritional profile but also align with the growing consumer preference for functional foods that support overall well-being. Producers are managing rising kernel costs, thanks to premium pricing linked to organic certifications, functional claims, and the convenience of single-serve formats. Moreover, technological advancements like enzymatic extraction and concentrated “just-add-water” pouches are not only boosting margins but also enhancing sustainability by reducing packaging waste and transportation costs. While multinationals ramp up competitive intensity through mergers and acquisitions for scale and procurement advantages, regional specialists are carving out their market share with clean-label formulations and direct-to-consumer strategies, which resonate strongly with health-conscious and environmentally aware consumers.

Key Report Takeaways

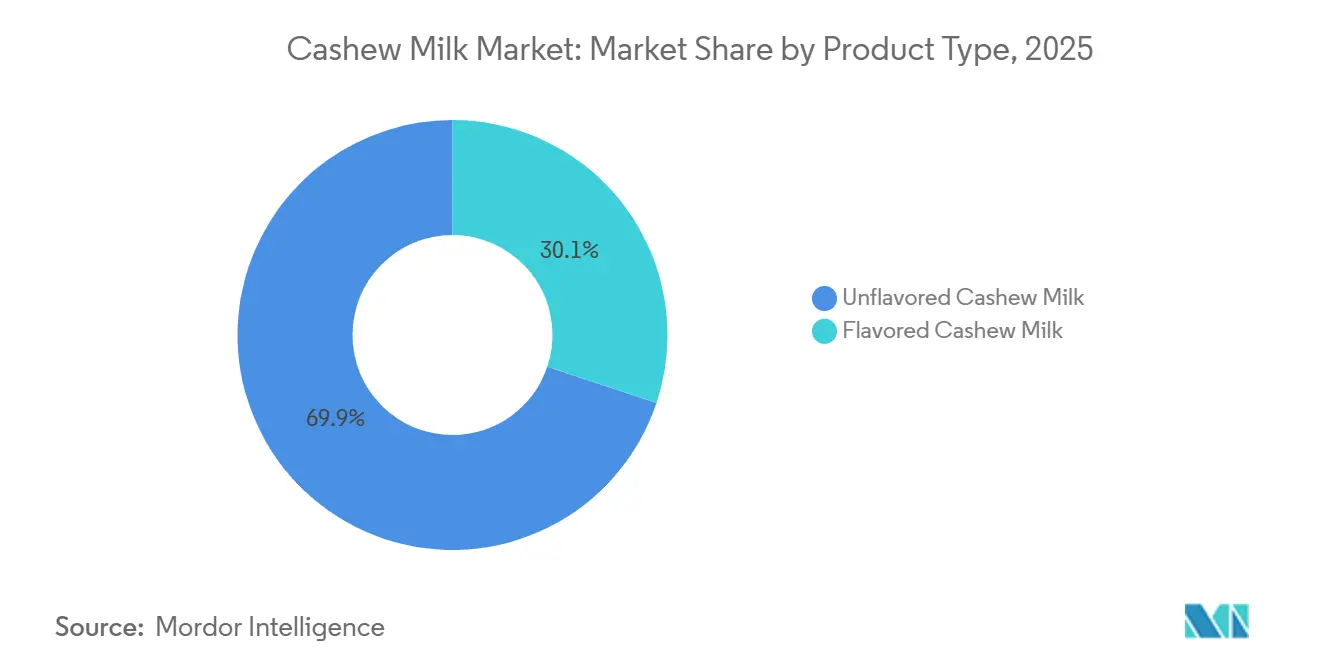

- By product type, unflavored led with 69.87% of cashew milk market share in 2025, while flavored variants are forecast to advance at a 7.10% CAGR through 2031.

- By nature, conventional accounted for 87.43% share in 2025 and organic offerings are projected to expand at a 7.94% CAGR over 2026-2031.

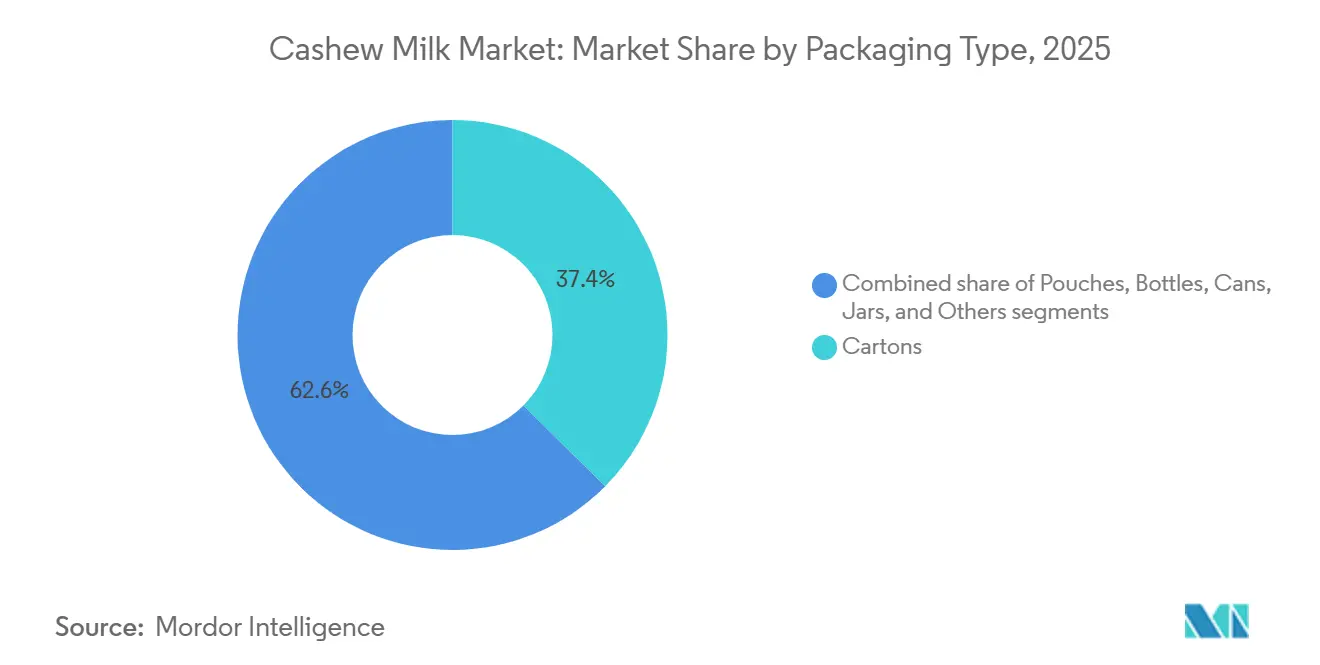

- By packaging, cartons commanded 37.43% share in 2025, whereas pouches will register an 8.12% CAGR, the fastest among all formats.

- By distribution channel, off-trade outlets held 59.10% share in 2025, but on-trade foodservice is set to grow at a 7.30% CAGR to 2031.

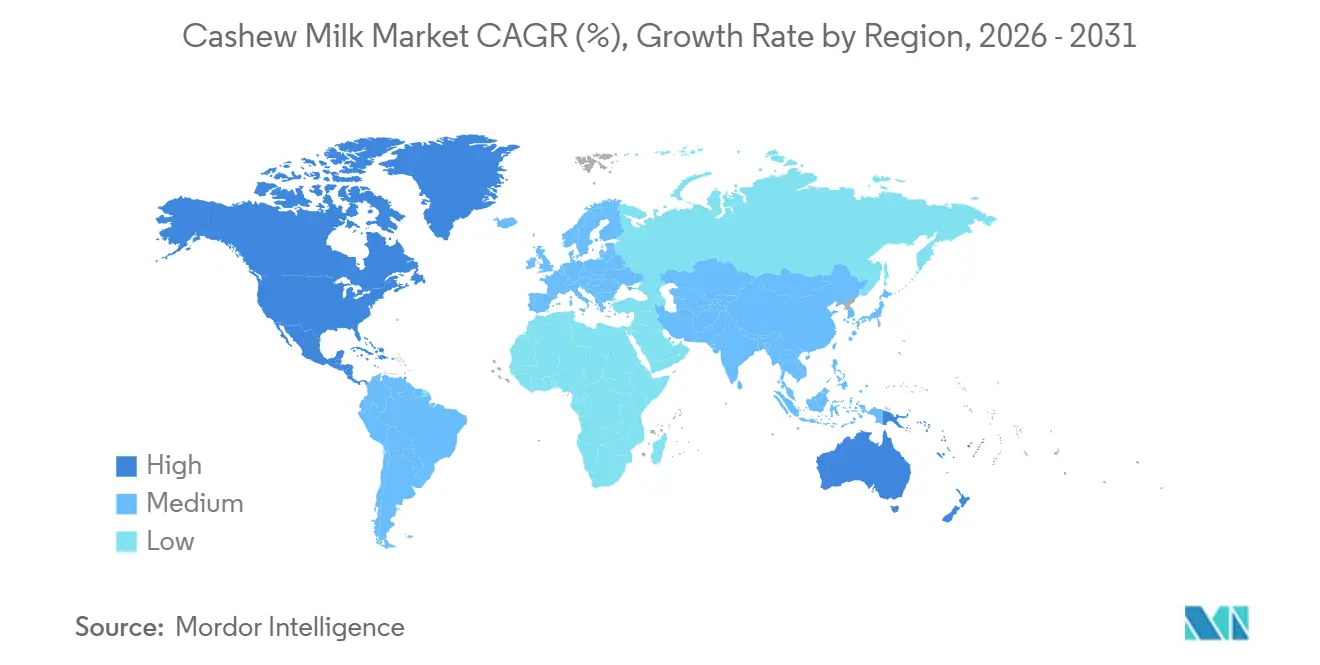

- By region, North America captured 41.16% share in 2025, and Asia-Pacific is positioned for the quickest climb with a 7.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cashew Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Well-Being Focus | +1.2% | Global, premium intensity in North America and Europe | Medium term (2-4 years) |

| Growing Lactose-Intolerant Population | +1.0% | Global, highest in Asia-Pacific, Africa, and Hispanic/African-American U.S. groups | Long term (≥ 4 years) |

| Expansion of Vegan and Flexitarian Diets | +1.1% | Core in North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Up-cycling of Cashew Apple By-Products | +0.4% | India, Vietnam, West Africa | Long term (≥ 4 years) |

| Asia-Pacific Government Incentives | +0.8% | Singapore, Thailand, India, China | Short term (≤ 2 years) |

| Integration into Functional Foods | +0.6% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health and well-being focus

Driven by preventive nutrition priorities, consumers are increasingly gravitating towards dairy alternatives. Cashew milk, in particular, is gaining traction for its heart-friendly oleic acid profile, which is known to support cardiovascular health. Brands are fortifying these alternatives to bridge nutrient gaps, allowing them to boast parity with dairy in terms of calcium and vitamin D content, which are essential for bone health. A prime example of this trend is Silk Protein, offering 13 grams of complete plant protein per serving. This product caters to both athletes seeking muscle recovery and GLP-1 users aiming for better metabolic health with its higher-protein recipes. Regulatory bodies like EFSA and the FDA are intensifying scrutiny, mandating companies to document bioavailability to ensure that nutrients are effectively absorbed by the body. This requirement bolsters their clean clinical messaging, enhancing consumer trust. Retailers, in turn, are rewarding such substantiated claims with premium shelf space, creating a reinforcing cycle of fortification, consumer confidence, and enhanced pricing power.

Growing lactose-intolerant population

Globally, 68% of people grapple with lactose malabsorption, a figure that soars past 90% in East Asia. This widespread issue bolsters the demand for cashew milk, which boasts a naturally lactose-free profile, making it a suitable alternative for individuals with lactose intolerance. Cashew milk's thicker consistency, compared to rice or oat milk, makes it a preferred choice for coffee and baking, where viscosity is key to achieving desired textures and flavors. In 2025, Mexican watchdog Profeco highlighted mislabeling in competing nut milks. This scrutiny has made transparency a pivotal factor, benefiting cashew formulations that prioritize purity and allergen-free standards, thereby building consumer trust. With just 25 kcal per unsweetened cup, cashew milk appeals to calorie-conscious consumers seeking healthier beverage options. However, it's essential to fortify the milk to ensure adequate protein intake for both children and seniors, addressing their specific nutritional needs.

Expansion of vegan and flexitarian diets

OECD economies' climate commitments, alongside the WHO's push for diverse proteins, bolster the legitimacy of plant-based milk. These initiatives aim to reduce environmental impact and promote sustainable dietary choices, driving consumer interest in alternatives like plant-based milk. Brands like Califia Farms, which offer concise ingredient lists and boast USDA Organic seals, are favored by younger consumers, even at a 40-60% price premium. Argentina's INTI agency lends technical backing to cashew-based dulce de leche, highlighting its cross-category traction and potential for innovation in plant-based products. Retail insights reveal rising repeat purchases of cashew milk in lattes, smoothies, and cooking, cementing its place in flexitarian diets. Highlighting this trend, the Good Food Institute reported that U.S. sales of plant-based foods reached an impressive USD 7.9 billion for the year 2025[1]Source: The Good Food Institute," U.S. retail market insights for the plant-based industry", gfi.org. This trend underscores the growing consumer preference for plant-based options that align with health, sustainability, and versatility, further driving the market's expansion. In a 2025 GFI Europe consumer study, 21% of German respondents identified with the 'More Plants, Less Meat and Dairy' segment, driven largely by environmental and animal welfare concerns[2]Source: The Good Food Institute, "Mainstreaming healthier, more sustainable diets: the motivations and dynamics driving plant-based uptake in Germany and the UK", gfi.org.

Up-cycling of cashew apple by-products

Historically, the cashew apple, which makes up 90% of the fruit's total mass, would rot away unused due to the lack of viable processing methods. However, pilots in India and Vietnam have begun transforming it into value-added products such as juice concentrate, animal feed, and fermented beverages. This initiative not only generates new revenue streams for the industry but also significantly reduces agricultural waste, addressing a long-standing inefficiency in cashew production. Additionally, this approach aligns with the growing demand for sustainable practices in the food and beverage sector. Furthermore, brands that integrate both milk and apple-processing lines are able to share capital expenditures across their product families, optimizing operational costs and improving profitability. By doing so, they bolster their image as zero-waste suppliers, a distinction that holds weight with institutional buyers keen on ESG scorecards and sustainability-focused procurement practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cashew Kernel Input Costs | -0.9% | Global, acute in import-dependent North America and Europe | Short term (≤ 2 years) |

| Taste and Mouthfeel Optimization Challenges | -0.5% | Global, especially markets with strong dairy benchmarks | Medium term (2-4 years) |

| Enzyme Supply Volatility | -0.3% | Global, enzyme hubs concentrated in Europe and Asia | Medium term (2-4 years) |

| Honey Adulteration Scandals | -0.2% | Global, category trust ripple effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cashew kernel input costs

In March 2026, benchmark WW320 kernels surged to EUR 6.30 per kg, driven by yield reductions in Vietnam and India due to El Niño, which disrupted agricultural production in these key regions[3]Source: Commodity Board Europe," Cashew Market 2026: Firm Prices, Strong Demand, Limited Downside", commodity-board.com. This price increase significantly impacted brands that lacked vertical integration or multi-year contracts, as they faced a squeeze in gross margins due to higher procurement costs and limited pricing power. Meanwhile, Refresco's anticipated USD 829 million acquisition of SunOpta underscores a growing trend in the industry: scale-driven mergers and acquisitions aim to bolster procurement leverage, enhance supply chain efficiency, and broaden geographic reach to mitigate risks associated with supply disruptions and price volatility. However, smaller independent players remain highly vulnerable to the unpredictability of spot-market fluctuations, which can severely affect their profitability, operational stability, and long-term competitiveness.

Taste and mouthfeel optimization challenges

To achieve a dairy-like creaminess, it's crucial to meticulously manage the nut-to-water ratios and choose the right emulsifiers, as these factors significantly impact the final product's texture, consistency, and overall sensory appeal. While enzymatic hydrolysis enhances stability by breaking down complex molecules, it also drives up costs, making it less accessible for smaller players in the market. Technologies like HydroRelease, which streamline the production process and improve efficiency, along with an expanding array of organic-certified flavors that cater to evolving consumer preferences, present viable solutions. However, capital expenditure and research and development challenges hinder swift adoption, especially for niche brands that often operate with limited resources and budgets. Ultimately, the key to long-term loyalty lies in sensory-driven repeat purchases, as consumers increasingly prioritize products that replicate the texture, mouthfeel, and overall experience of traditional dairy. This underscores the importance of achieving textural parity with dairy as a non-negotiable objective for success in this competitive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavored Variants Drive Premium Positioning

In 2025, unflavored cashew milk dominated the market, capturing 69.87% of total revenue. This stronghold is largely attributed to cafés and foodservice operators favoring it as a neutral base for both beverages and culinary uses. Its widespread adoption in these sectors stems from its ability to seamlessly blend with other ingredients without altering the intended flavor profile. Additionally, unflavored cashew milk enjoys consistent household usage due to its versatility in various recipes, including smoothies, soups, and baked goods. While the segment enjoys a staple positioning, its market share is poised for a slight dip. This is due to retailers increasingly dedicating shelf space to value-added alternatives, such as flavored or fortified options that cater to evolving consumer preferences. Yet, even with this minor decline, unflavored variants remain central to the category, bolstered by their versatility, affordability, and broad consumer appeal.

Flavored cashew milk is set to emerge as the fastest-growing segment, boasting a projected CAGR of 7.10% through 2031. This surge is driven by a growing appetite for fortified and indulgent flavors, with favorites like vanilla, matcha, and seasonal spice blends leading the charge. These flavored options not only cater to taste preferences but also align with the increasing demand for functional beverages that offer added health benefits. In a bid to bridge nutritional gaps and cater to health-conscious consumers, brands are rolling out protein-enhanced versions, blending cashew with soy, peas, and other legumes. These premium offerings, often priced 15–25% higher, not only counterbalance raw material cost challenges but also bolster marketing endeavors. Furthermore, innovative flavor-function pairings, such as chocolate with adaptogens, empower brands to craft unique “dual-benefit” propositions, striking a chord with the younger, health-savvy demographic. The introduction of limited-edition seasonal flavors and collaborations with popular health influencers further amplifies the appeal of flavored cashew milk, ensuring sustained growth in this segment.

By Nature: Organic Certification Captures Premium Tier

In 2025, conventional cashew milk dominated the market, securing 87.43% of the total share. This stronghold is attributed to its competitive pricing and robust sourcing and supply chain networks. Conventional cashew milk benefits from its affordability, making it a preferred choice among cost-conscious consumers. Additionally, its established distribution channels ensure widespread availability, further solidifying its market position. The product enjoys a significant presence in both retail outlets and foodservice sectors, catering to diverse consumer needs. While organic cashew milk is on the rise, conventional variants are set to retain their volume leadership for the foreseeable future, bolstered by cost-sensitive consumers and the scalability of their production systems.

Organic cashew milk is on track to be the fastest-growing segment, with a projected CAGR of 7.94% during the forecast period. Despite its relatively modest current market size, organic cashew milk promises higher profit margins and significant export potential, especially in regulated markets like the EU and Japan. This growth is driven by consumers' increasing willingness to invest in certified products, buoyed by clean-label positioning and sustainability narratives. Yet, the path isn't without challenges: certification mandates lead to the need for segregated supply chains and investments in traceability technologies, complicating operations. Industry leaders like Califia Farms and MALK Organics are seizing this opportunity, rolling out premium products with straightforward ingredient lists, often fetching a 40–60% price premium.

By Packaging Type: Pouches Gain Traction on Sustainability

In 2025, carton packaging led the cashew milk market, securing 37.43% of the total share. This dominance is bolstered by the widespread adoption of shelf-stable aseptic packaging, seamlessly integrating with established retail distribution systems and planograms. Cartons not only provide convenience and an extended shelf life but also align perfectly with large-scale manufacturing and logistics. Additionally, their lightweight nature and ease of stacking make them a preferred choice for retailers, as they optimize shelf space and reduce handling costs. Consumers also perceive cartons as a reliable and familiar packaging option, further strengthening their market position. While alternative packaging formats are emerging, cartons are poised to maintain their leadership for the next five years, bolstered by retailer familiarity and consumer trust.

Pouches are set to emerge as the fastest-growing packaging segment, boasting a projected CAGR of 8.12% during the forecast period. Though they currently hold a smaller market share, their appeal is surging, thanks to benefits like reduced packaging weight and diminished transportation emissions. This format shines in e-commerce channels, where last-mile delivery efficiency is paramount. Moreover, innovations like concentrated flat-pack pouches, which need water reconstitution, are resonating with sustainability-minded consumers. With brands increasingly focusing on ESG goals and expanding in online retail, pouches are on track to secure a larger slice of the market.

By Distribution Channel: On-Trade Foodservice Accelerates

In 2025, off-trade channels dominated the cashew milk market, capturing 59.10% of the total value. Supermarkets, hypermarkets, and online platforms drove this dominance, offering the highest accessibility and variety to consumers. These channels benefit from extensive product availability, competitive pricing, and the convenience of one-stop shopping, which appeals to a broad customer base. Factors like strategic shelf placement, targeted promotional efforts, and integration into the rapidly expanding plant-based sections have significantly boosted sales in these outlets. Additionally, the growing trend of health-conscious consumers seeking plant-based alternatives has further strengthened the position of off-trade channels. While off-trade channels remain pivotal to the market, their share is set to see a slight dip as alternative consumption avenues, such as direct-to-consumer models and specialty stores, gain traction. Despite this shift, off-trade will continue to serve as the primary distribution backbone for cashew milk, ensuring widespread availability and consistent consumer engagement.

On-trade channels are on track to be the fastest-growing segment, with a projected CAGR of 7.30% during the forecast period. This growth is fueled by rising adoption in coffee shops, quick-service restaurants, and workplace cafeterias, where cashew milk's foam stability and sensory appeal are highly valued. The increasing demand for plant-based beverages in these settings is driven by evolving consumer preferences for dairy-free options and the growing awareness of sustainability and health benefits. Major chains expanding their dairy-free defaults and plant-based menu options further drive this trend, creating more opportunities for cashew milk to penetrate the market. Brands that secure spots in café beverage programs not only enjoy premium pricing but also gain consistent consumer visibility, as these programs often feature cashew milk prominently in specialty drinks. Moreover, this channel serves as a trial platform, allowing consumers to experience the product in a curated setting, which helps in converting occasional users into loyal consumers. The on-trade segment also benefits from collaborations with foodservice providers, enabling brands to tap into a wider audience and enhance their market presence.

Geography Analysis

By 2025, North America is set to command a 41.16% share, driven by its established distribution networks, Canada's endorsement of plant proteins in dietary guidelines, and Mexico's prevalent lactose intolerance. In the U.S., while the overall plant-milk volume shows signs of softening, premium cashew SKUs stand out, underscoring the success of fortified and flavored innovations. Meanwhile, corporate maneuvers, like the Refresco-SunOpta deal, highlight a trend of consolidation as companies pursue procurement synergies. These factors collectively position North America as a mature and stable market for cashew milk, with innovation and strategic partnerships driving growth. Additionally, the region's focus on premiumization and health-conscious consumer trends continues to fuel demand for plant-based alternatives.

Europe, holding the second spot, benefits from the European Parliament's nod to use dairy terminology for plant-based alternatives. This, coupled with a strong organic demand in Germany, France, and the Nordic countries, bolsters the region's position. While the EFSA's claim verifications and specific country sugar taxes necessitate careful formulation, they also serve to filter out non-compliant players, inadvertently enhancing the category's credibility. The region's regulatory environment and consumer preferences create a competitive yet promising landscape for market players. Furthermore, the increasing availability of plant-based options in mainstream retail channels is making these products more accessible to a broader audience.

Asia-Pacific is set for significant growth, with a projected CAGR of 7.53%. Policy incentives, such as Singapore's food-security grants and APEDA rebates in India, are easing scaling challenges. With a domestic kernel supply, India and Vietnam offer opportunities for vertical integration. Urban consumers in China increasingly prefer lactose-free beverages in cafes. Countries like Australia, South Korea, and Japan, supported by vibrant café cultures and health-conscious trends, further enhance the region's potential. These market dynamics and supportive policies position Asia-Pacific as a key hotspot for cashew milk investments. In South America, Brazil and Argentina are witnessing growing interest. Government-backed research and development and rising plant-based lifestyle trends are driving trials. While still nascent, increasing consumer awareness and supportive policies indicate steady growth potential. In the Middle East and Africa, cashew milk is gaining traction in upscale retail outlets in the Gulf and South Africa. However, broader adoption faces challenges like price sensitivities and cold-chain logistics. Despite this, premium retail segments and evolving consumer preferences reveal niche opportunities for market expansion.

Competitive Landscape

The cashew milk market is moderately fragmented, featuring both multinational giants and regional players. Global entities like Danone, Hain Celestial, and Refresco (after acquiring SunOpta assets) harness vast product portfolios, robust research and development, and notable procurement advantages. Danone's move to acquire Kate Farms, a medical nutrition firm, underscores its ambition to broaden cashew milk's reach into clinical nutrition and sports. Such maneuvers spotlight how major players aim to harness value through diversification and innovative product functionalities.

Meanwhile, regional brands like Vinut Group, Ruby Food Products, and MALK Organics are carving out their niches. By championing clean-label products, distinctive flavors, and direct-to-consumer approaches, they're cultivating dedicated consumer bases. Their nimbleness lets them swiftly adapt to shifting consumer tastes, especially in premium and health-centric markets. This creates a competitive arena where branding and innovation are as pivotal as scale.

As rising costs and enzyme supply challenges emerge, larger, vertically integrated players with robust sourcing capabilities gain an edge. This shift has spurred consolidation trends, with mid-sized firms eyeing mergers and partnerships to bolster raw material access and marketing prowess. Innovations like HydroRelease processing, 2-D concentrate printing, and enzyme-assisted extraction offer avenues for product distinction. Looking ahead, thriving brands are poised to meld health benefits with sensory allure, forge stable sourcing agreements, and broaden their reach in retail and foodservice sectors.

Cashew Milk Industry Leaders

-

Danone S.A.

-

Califia Farms

-

The Hain Celestial Group

-

Forager Project, LLC

-

Elmhurst 1925

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Califia Farms plans to launch its barista-blend cashew milk in 2025, aiming to replicate the creamy froth quality of dairy while adhering to strict clean-label and vegan standards.

- August 2024: Elmhurst has launched its unsweetened cashew milk, emphasizing its simplicity with just two ingredients: cashews and water. This product, devoid of emulsifiers and gums, comes in eco-friendly recyclable cartons. Owing to Elmhurst’s HydroRelease method, the milk achieves a creamy texture, perfect for coffee and cereal. It's received praise for its barista-friendly qualities and dedication to a clean-label approach.

- March 2024: MALK Organics has launched "cashew MALK," an unsweetened, shelf-stable cashew milk. The company markets it as a clean-label product, made from just four organic ingredients: filtered water, organic cashews, Himalayan pink salt, and organic almonds. MALK Organics highlights that their offering is not only shelf-stable and unsweetened but also free from gums or oils. Prioritizing transparency and simplicity, the product first appeared at Whole Foods and has rapidly spread to major retailers, highlighting a rising consumer demand for natural formulations.

- January 2024: JOI introduced an ultra-concentrated cashew milk base, now available in jars and pails, catering to both foodservice professionals and home chefs. The company claims that a single container can produce up to 60 quarts of cashew milk, allowing users to craft fortified beverages, sauces, or vegan cheeses, all while enjoying cost savings and greater production flexibility.

Global Cashew Milk Market Report Scope

Cashew milk is defined as a plant-based, dairy-free beverage made by blending cashew nuts with water and straining the mixture to achieve a smooth, creamy consistency. Based on the product type, the market is segmented into unflavored and flavored cashew milk. By nature, the market is segmented into conventional and organic. Based on packaging type, the market is segmented into bottles, cartons, pouches, jars, cans, and others. By distribution channel, the market is segmented into foodservice/horeca and retail. The study provides a detailed analysis on major economies across North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Unflavoured Cashew Milk |

| Flavoured Cashew Milk |

| Conventional |

| Organic |

| Bottles |

| Cartons |

| Pouches |

| Jars |

| Cans |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Unflavoured Cashew Milk | |

| Flavoured Cashew Milk | ||

| By Nature | Conventional | |

| Organic | ||

| By Packaging Type | Bottles | |

| Cartons | ||

| Pouches | ||

| Jars | ||

| Cans | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the cashew milk market growth between 2025 and 2030?

Rising health consciousness, expanding vegan diets, and growing awareness of lactose intolerance are the primary growth catalysts, supporting a projected 6.40% CAGR.

How large will cashew milk sales be in 2031?

The category is expected to reach USD 332.41 billion worldwide by 2031, reflecting a 6.4% CAGR from 2026-2031.

Which region is growing the fastest for cashew beverages?

Asia-Pacific leads with a projected 7.53% CAGR, fueled by supportive food-security and sustainability policies

Why do cafés prefer cashew milk over almond or rice?

Cashew’s higher fat level produces creamier microfoam that withstands espresso pressure, delivering better latte art and mouthfeel.

What packaging formats will gain share over the next five years?

Lightweight pouches and concentrated flat packs are set for the quickest uptake thanks to reduced shipping emissions and online retail convenience.

Page last updated on: