Camel Milk Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

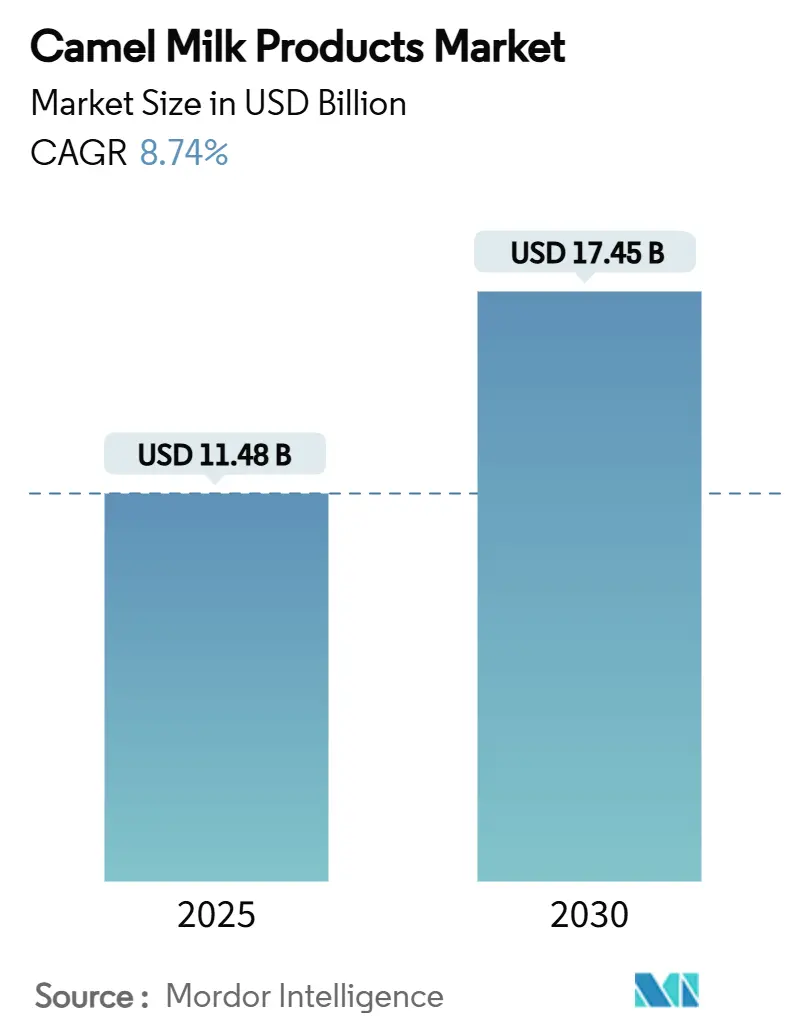

| Market Size (2025) | USD 11.48 Billion |

| Market Size (2030) | USD 17.45 Billion |

| Growth Rate (2025 - 2030) | 8.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Camel Milk Products Market Analysis by Mordor Intelligence

The camel milk products market size reached USD 11.48 billion in 2025 and is forecast to attain USD 17.45 billion by 2030, advancing at an 8.74% CAGR. These headline numbers confirm a sturdy growth runway built on wider therapeutic recognition, rising functional-food demand, and formal regulatory acceptance. The camel milk products market is moving from informal, pastoral supply chains toward organized commercial dairies that can meet stringent food-safety standards and export protocols. Government programs—most visibly Saudi Arabia’s “Year of the Camel” initiative—are channelling grants and veterinary services into herd expansion, while breakthrough freeze-drying and packaging technologies remove cold-chain bottlenecks. Competitive intensity is moderate, giving well-capitalized processors room to consolidate fragmented production clusters and secure downstream distribution rights across high-growth urban markets.

Key Report Takeaways

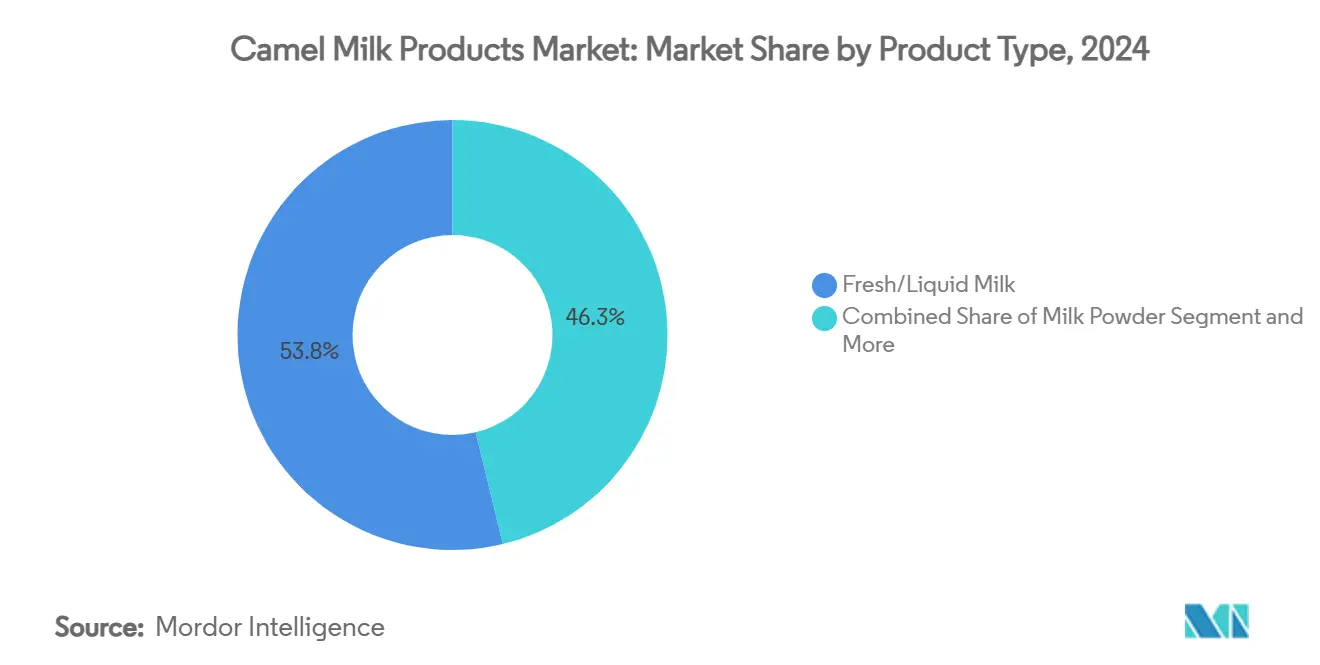

- By product type, fresh milk held 53.75% of the camel milk products market share in 2024, whereas milk powder is projected to register the fastest 9.58% CAGR through 2030.

- By distribution channel, supermarkets and hypermarkets captured 38.91% revenue in 2024, while online retail is forecast to post the strongest 11.26% CAGR over 2025-2030.

- By packaging type, bottles accounted for 47.32% of the camel milk products market size in 2024; sachets and pouches are on track to expand at an 8.48% CAGR to 2030.

- By geography, Middle East & Africa led with 32.70% revenue share in 2024, yet Asia-Pacific is set to log a swift 9.24% CAGR, the highest regional growth rate.

Global Camel Milk Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of lactose-intolerance & dairy allergies | +1.2% | Global (high in North America & Europe) | Medium term (2-4 years) |

| Growing demand for functional foods & “super-foods” | +1.8% | Global (North America, Europe, urban Asia-Pacific) | Short term (≤ 2 years) |

| Government support for camel farming in GCC | +1.5% | Middle East & Africa | Long term (≥ 4 years) |

| Expansion of organized camel dairy chains in Africa | +0.9% | Sub-Saharan Africa | Medium term (2-4 years) |

| Breakthrough freeze-drying technologies | +0.6% | Global (early GCC uptake) | Short term (≤ 2 years) |

| Product innovation and diversification | +0.8% | Global (developed markets first) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Functional Foods & “Super-Foods”

Rapid adoption of diabetic nutrition protocols has vaulted camel milk into the functional-food spotlight. Clinical trials show that daily intake can trim blood-glucose readings and insulin needs by 30-35% in patients with both major diabetes types[1]Mohammadabadi, Taherah, and Rajesh Jain. "Camel milk; A potent superfood for diabetes complications." Journal of Food Science and Nutrition Therapy, March 23, 2024. www.foodscigroup.us.. Healthcare endorsements enable premium pricing that offsets higher farm-gate costs and reassure risk-averse consumers of verified efficacy. The super-food narrative is further anchored by camel milk’s high vitamin C and insulin-like peptide content, benefits that bovine milk cannot match. Digital marketing campaigns are amplifying medical journal findings, accelerating trial among fitness enthusiasts and metabolic-disorder patients. In response, processors are bundling small-volume packs for direct-to-consumer subscription services, a move that broadens the camel milk products market beyond heritage communities.

Expansion of Organized Camel Dairy Chains in Africa

The expansion of organized camel dairy chains in Africa has strengthened supply consistency by improving herd management and formalizing milk collection networks, as seen in Kenya’s emerging cooperatives and large processors like Vital Camel Milk Ltd. Countries such as Somalia and Ethiopia have accelerated cold-chain development, helping reduce spoilage and enabling producers to meet basic safety and hygiene standards required for exports. These structured systems have supported higher product quality and certification, illustrated by Kenya’s regulatory push to standardize camel milk processing. Organized chains have also encouraged the rise of value-added products—such as powdered camel milk from producers in Mauritania and pasteurized and flavored variants in Sudan, broadening market presence.

Increasing Prevalence of Lactose-Intolerance & Dairy Allergies

Camel milk lacks β-lactoglobulin, the bovine protein most often implicated in milk allergies, positioning it as a natural solution for sensitive consumers. Up to 90% of East Asian adults experience lactase non-persistence[3]Konuspayeva, Gaukhar, and Bernard Faye. "Recent Advances in Camel Milk Processing." Animals 2021, 11, 1045. doi.org., creating a large opportunity pool where goat and oat alternatives have already gained traction. Camel milk’s enzyme profile not only improves digestibility but also contributes antimicrobial peptides that support gut health, making it attractive to immunity-focused shoppers. Retailers are consequently carving dedicated shelf space for allergy-friendly dairy, a visibility boost that feeds back into brand recall. As knowledge spreads through physician recommendations, the camel milk products market gains a rare medical endorsement channel that plant-based beverages seldom enjoy.

Government Support for Camel Farming in GCC

Saudi Arabia’s “Year of the Camel” declared in 2024 injected sizeable grants for breeding centres[2]Bailey, Tom. "2024 an eventful year for dairy companies on the global stage." Dairy News, January 6, 2025. dairynews.today., mobile veterinary clinics, and export facilitation programmes. Similar subsidies are being mirrored by the UAE and Oman, which collectively host large-scale desert megafarms able to milk 8,000-plus animals year-round. Policy harmonisation across the Gulf Cooperation Council reduces cross-border paperwork, encouraging processors to site plants near trade hubs such as Jebel Ali Port. Public-sector backing also eases access to preferential bank loans, lowering the capital barrier for automated milking parlours. Over the long term, these initiatives are expected to stabilise raw-milk supply, thereby underpinning the camel milk products market’s expansion into value-added formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs vs. bovine milk | -1.2% | Global, most acute in developed markets with established dairy infrastructure | Long term (≥ 4 years) |

| Limited cold-chain infrastructure in emerging markets | -0.9% | Africa, Asia-Pacific emerging markets, Latin America | Medium term (2-4 years) |

| Ethical/biodiversity concerns over intensive camel farming | -0.7% | Global, with higher scrutiny in Europe and North America | Medium term (2-4 years) |

| Tariff anomalies for non-bovine milk imports | -0.6% | International trade corridors, particularly US-GCC and EU-Africa routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs vs. Bovine Milk

Camels yield only 3-10 litres daily compared with 25-40 litres from intensively bred cows, saddling producers with higher unit costs. Longer 13-month gestation cycles slow herd turnover, while specialised veterinary care further inflates overheads. In price-sensitive markets, this premium constrains penetration into mainstream grocery channels. Processors therefore depend on functional-food positioning and clinical validation to sustain margins. Unless continued scale economies shave costs, the camel milk products market may struggle to compete head-to-head with low-cost bovine staples.

Limited Cold-Chain Infrastructure in Emerging Markets

Sub-Saharan logistics are hampered by inadequate refrigeration capacity, triggering spoilage and safety concerns that shrink retail windows. Liquid milk therefore rarely travels beyond regional hubs, capping producer revenues. Although powder technology mitigates this for export markets, domestic consumers still prefer fresh formats when available. Public-private partnerships are beginning to fund solar-powered chillers and insulated transport, but coverage remains patchy. Until infrastructure gaps close, the camel milk products market will grow unevenly across emerging geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fresh Milk Holds Tradition while Powder Accelerates Trade

In 2024, fresh and liquid milk captures a 53.75% share of the market, underscoring traditional consumption habits and its appeal to health-conscious consumers who value minimal processing. Camel milk, celebrated for its therapeutic properties, leads this segment. Many consumers believe that fresh consumption enhances the retention of beneficial bioactive compounds, such as insulin-like proteins and immunoglobulins, which are thought to aid in diabetes management. Yet, fresh milk's distribution is hampered by its short shelf life and the need for a cold chain, restricting its market reach to regional confines. While yogurt and cheese segments lag, camel milk's distinct protein profile demands specialized processing. However, recent advancements, particularly in microbial transglutaminase applications, hint at a brighter future for these categories.

Milk powder stands out as the segment with the most rapid growth, boasting a 9.58% CAGR projected through 2030. This surge is fueled by innovations in freeze-drying technology, which not only safeguard nutritional value but also sidestep cold-chain dependencies. The powdered form paves the way for broader international trade. A case in point is Camelicious, which exports two-thirds of its powder output to China, capitalizing on a demand that outstrips the local supply in the UAE. Meanwhile, ice cream and frozen desserts are carving out a niche, as innovations cater to taste preferences in regions where liquid camel milk isn't as culturally embraced. The cheese and butter markets eye premium positioning, but face hurdles in processing that necessitate ongoing technological advancements for large-scale commercial success.

By Distribution Channel: Digital Transformation Accelerates Market Access

Online retail channels are on track to grow at a robust 11.26% CAGR through 2030, underscoring the sector's shift towards digital platforms and direct-to-consumer models, sidestepping traditional retail middlemen. E-commerce platforms empower producers to tap into niche markets, especially those keen on functional foods and therapeutic products. The digital realm resonates strongly with health-conscious consumers, who often research product benefits pre-purchase. This trend not only opens doors for premium product positioning but also fosters direct relationships with customers. Meanwhile, food service channels are witnessing consistent growth, with restaurants and cafes creatively integrating camel milk into specialty drinks and desserts, broadening its consumption beyond the conventional home setting.

In 2024, supermarkets and hypermarkets command a significant 38.91% market share, leveraging their established distribution networks and ingrained consumer shopping habits. However, their growth rates trail behind the digital surge, hindered by limited shelf space and a hesitance to stock niche products. Specialty stores emerge as vital touchpoints for new consumers, offering expert insights and product education that larger retailers often overlooks. Here, convenience and access to product information reign supreme. As a result, distribution strategies are increasingly leaning towards omnichannel methods, blending online direct sales with selective retail collaborations to optimize market reach while safeguarding profit margins.

By Packaging Type: Convenience Drives Innovation

In 2024, bottles capture a 47.32% share of the market, underscoring a consumer tilt towards premium packaging. This preference is especially pronounced for products marketed as therapeutic beverages, where conveying quality and freshness is paramount. Glass and premium plastic bottles not only safeguard the product but also set brands apart. Their unique designs often echo a brand's heritage and authenticity. In Middle Eastern markets, where camel milk holds cultural significance, the bottle format resonates with gift-giving traditions, bolstering premium pricing strategies. Yet, while bottle packaging grapples with sustainability issues and rising transportation costs, these challenges pave the way for alternative packaging formats.

Sachets and pouches are the packaging segment to watch, boasting an impressive 8.48% CAGR through 2030. Their rise is fueled by a consumer shift towards convenience and a push for cost-effective distribution in emerging markets. This flexible packaging not only trims transportation and storage costs but also offers portion control, appealing to both trial users and the price-sensitive. Thanks to advancements in barrier films, product quality is preserved, and packaging costs are slashed, broadening camel milk's appeal. Meanwhile, cartons hold their ground, buoyed by established supply chains and consumer trust. However, their growth is stymied by sustainability dilemmas and challenges in premium positioning. Yet, the industry buzzes with potential, eyeing innovations in sustainable materials and smart technologies that promise longer shelf lives with a smaller environmental footprint.

Geography Analysis

Asia-Pacific, led by China's health-conscious consumers, is set to grow at a 9.24% CAGR through 2030, largely due to the rising embrace of camel milk for diabetes management and overall wellness. This growth is bolstered by strategic market entries from established players like Camelicious, who shifted their focus to cater to Asia's burgeoning demand, outpacing the traditional Middle Eastern appetite. Producers are eyeing Japan and South Korea as prime markets, seeking franchise partnerships to cement their local foothold. Meanwhile, India is ramping up domestic production, and negotiations with Brazil underscore the global acknowledgment of Indian camel milk's quality and production prowess.

In 2024, the Middle East & Africa commands a 32.70% market share, underscoring its deep-rooted cultural ties and traditional production of camel milk. Ethiopia stands out with a staggering annual output of 1.4 billion liters, showcasing the region's vast production capabilities. Furthermore, government-backed initiatives across GCC nations are pushing for industrial-scale advancements. In Morocco, camel-based livestock systems are not just a cultural staple but also a significant economic driver, with average household incomes touching MAD 120,000 (USD 12,460).

North America and Europe, while representing premium markets driven by health-conscious lactose-intolerant and diabetic consumers, grapple with high production costs that stifle local supply growth. South America's interest is piqued, evident from Brazil's talks for Indian camel milk imports, hinting at a potential market expansion beyond its traditional confines.

Competitive Landscape

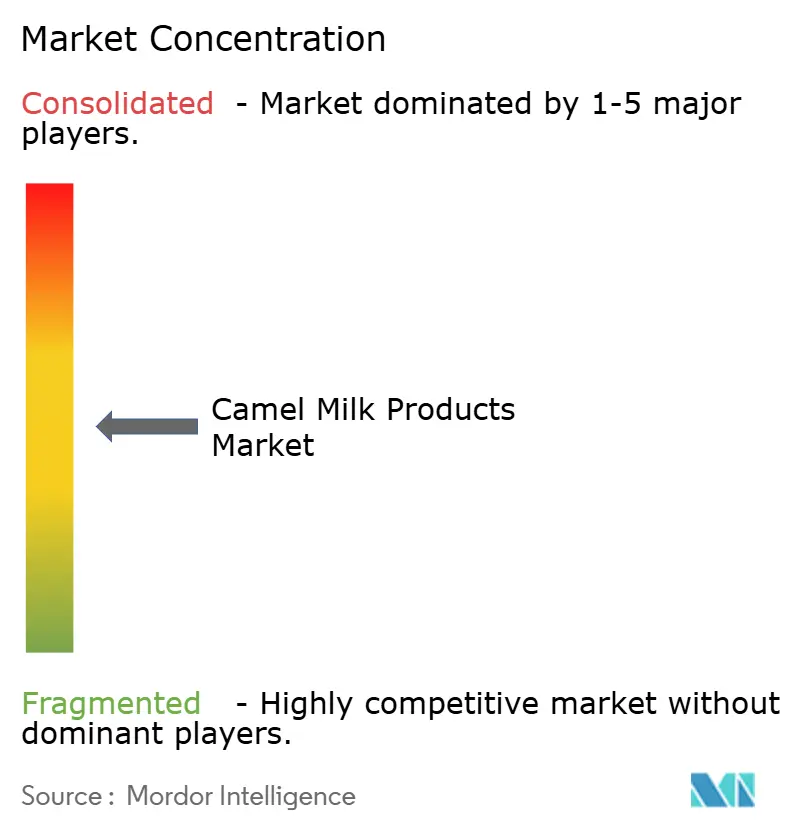

The camel milk products market shows signs of moderate fragmentation, boasting a concentration score of 5 out of 10. This score hints at significant consolidation opportunities, especially as the sector shifts from its traditional pastoral roots to more industrial-scale operations. Market leaders, like Camelicious, are not just focusing on the number of camels – operating 8,000 across integrated production facilities – but are also making strategic international moves. Instead of opting for licensing arrangements, they're forging direct export relationships. The competition isn't just about quantity; it's heating up around technological prowess. Innovations in freeze-drying and processing are pivotal, allowing for shelf-stable products that can be distributed globally. This tech edge poses challenges for smaller producers, who often lack the capital for such investments.

In this landscape, companies are steering their strategic positioning towards highlighting therapeutic benefits and premium quality. It's not just about being the cheapest; it's about being the best. To back their health claims and justify premium pricing, these companies are pouring resources into clinical research and ensuring they meet regulatory standards. A case in point: the FDA's 2023 revision of the Pasteurized Milk Ordinance, which now formally acknowledges camel milk production standards. This move bestows a competitive edge to producers already equipped with robust quality systems and a deep understanding of regulatory nuances.

There's a vast expanse of untapped potential beyond just liquid milk. Al Nassma's foray into camel milk chocolate is a testament to this, showcasing successful product diversification. Meanwhile, the Asia-Pacific region is emerging as a promising frontier, presenting geographic expansion opportunities for established producers, especially those with robust distribution networks. Companies that have forged research partnerships and honed their processing skills are reaping the benefits. Breakthroughs in cheese production and powder processing aren't just innovations; they're avenues for differentiation in a market that's becoming increasingly crowded.

Camel Milk Products Industry Leaders

-

Camelicious (Emirates Industry for Camel Milk & Products)

-

Desert Farms

-

Al Ain Dairy

-

Aadvik Foods

-

QCamel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Beder Camel Farm introduced its first camel milk yogurt in Somalia. According to the company, the yogurt is produced using milk from camels raised on its expansive farm, where animal welfare and sustainable practices are prioritized.

- January 2025: Camelicious announced expansion plans targeting 30 global markets by 2030, with China identified as the largest market, surpassing UAE domestic consumption. The company aims for 15-20% organic growth annually while exploring franchise partnerships in Japan and South Korea to establish local market presence.

- October 2020: Amul launched camel milk ice cream as part of its value-added camel milk product line, which also includes camel milk powder.

Global Camel Milk Products Market Report Scope

| Fresh/Liquid Milk |

| Milk Powder |

| Yogurt |

| Cheese and Butter |

| Ice-cream & Frozen Desserts |

| Food Service | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail | |

| Others |

| Bottles |

| Cartons |

| Sachets and Pouches |

| Others (Tubs, Jars) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fresh/Liquid Milk | |

| Milk Powder | ||

| Yogurt | ||

| Cheese and Butter | ||

| Ice-cream & Frozen Desserts | ||

| By Distribution Channel | Food Service | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail | ||

| Others | ||

| By Packaging Type | Bottles | |

| Cartons | ||

| Sachets and Pouches | ||

| Others (Tubs, Jars) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the camel milk products market?

The camel milk products market size was USD 11.48 billion in 2025 and is projected to reach USD 17.45 billion by 2030.

Which region is growing fastest for camel milk products?

Asia-Pacific is forecast to expand at a 9.24% CAGR, the quickest regional pace through 2030 due to rising health-focused demand in China, Japan, and South Korea.

Why is camel milk considered beneficial for diabetics?

Clinical studies show that regular camel milk consumption can lower blood-glucose levels and reduce insulin requirements by up to 35% thanks to insulin-like proteins and antioxidant vitamins

What packaging formats are gaining popularity?

Sachets and pouches are the fastest-rising format, posting an 8.48% CAGR as consumers seek convenient, portion-controlled options that cut transport and storage costs.

Page last updated on: