Milk Chocolate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 95.31 Billion |

| Market Size (2031) | USD 121.29 Billion |

| Growth Rate (2025 - 2031) | 4.94% CAGR |

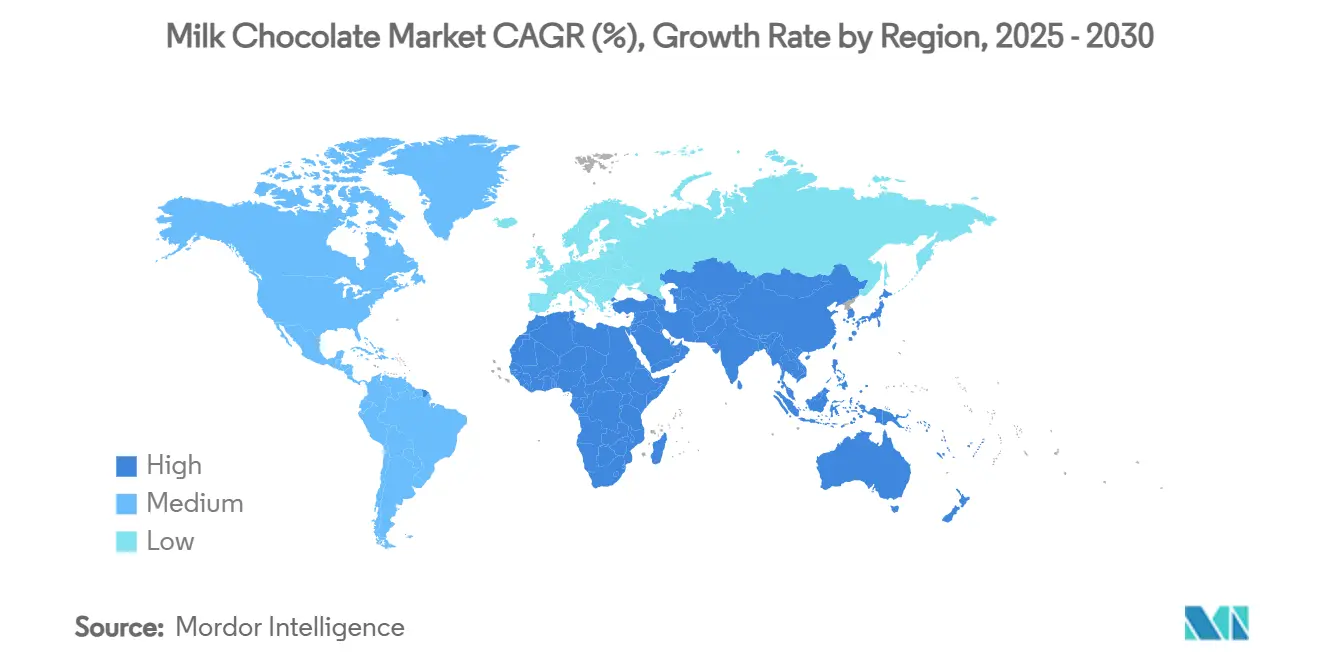

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

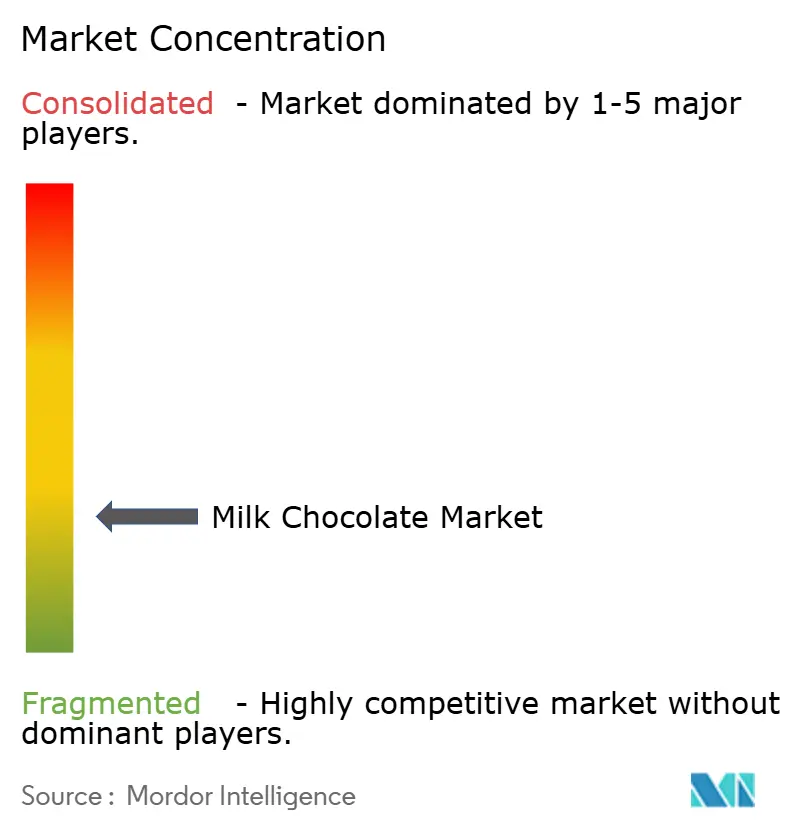

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Milk Chocolate Market Analysis by Mordor Intelligence

The milk chocolate market size is expected to grow from USD 90.82 billion in 2025 to USD 95.31 billion in 2026 and is forecast to reach USD 121.29 billion by 2031 at 4.94% CAGR over 2026-2031. The market is driven by increasing demand for premium, sustainably sourced products. Evolving consumer trends, such as snackification, seasonal gifting, and the expansion of online retail, are transforming product formats and distribution strategies. Manufacturers are strategically managing these shifts by balancing reformulation efforts with maintaining brand equity to protect profit margins. However, the industry faces significant cost pressures stemming from volatile cocoa prices, compounded by supply chain disruptions in West Africa and stricter regulatory requirements related to sugar reduction and deforestation compliance. The rising preference for portion-controlled formats and artisanal products reflects changing consumer lifestyles, while fiscal policies such as sugar taxes are expected to drive further product innovation and reformulation. These factors collectively highlight an industry adapting to both consumer-driven demands and structural supply chain challenges.

Key Report Takeaways

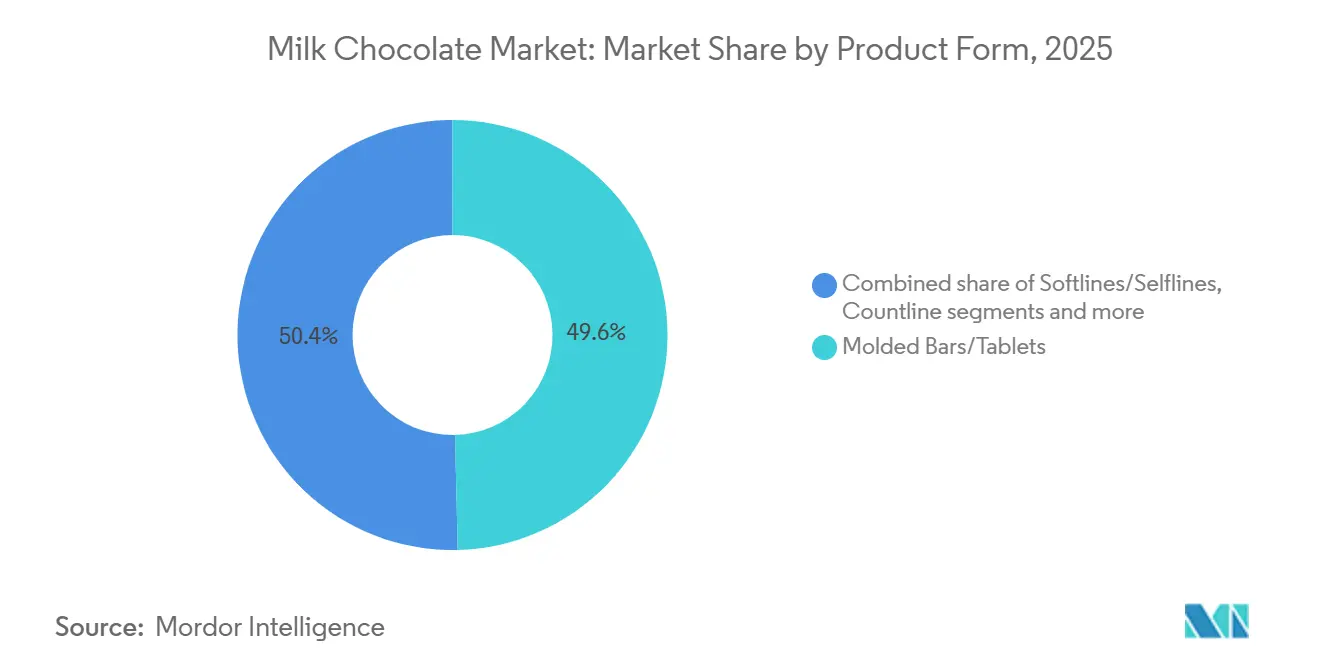

- By product form, molded bars/tablets captured 49.61% of the milk chocolate market share in 2025, while countlines are set to accelerate at a 6.89% CAGR through 2031.

- By packaging, single-serve held a 46.53% share of the milk chocolate market in 2025; multi-serve is forecast to expand at a 6.41% CAGR through 2031.

- By category, the mass segment captured 78.82% share in 2025, and premium/luxury products are forecast to expand at a 7.81% CAGR through 2031.

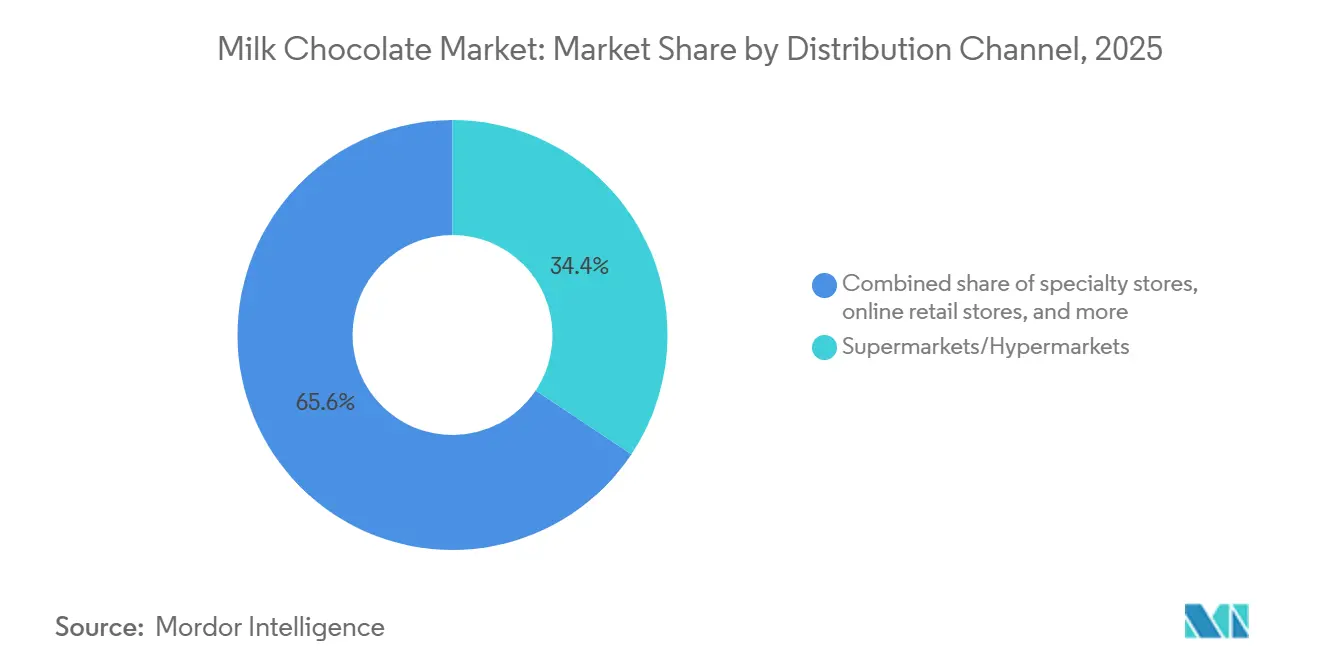

- By distribution channel, supermarkets/hypermarkets captured 34.36% share in 2025, but online retail stores are forecast to expand at a 7.57% CAGR through 2031.

- By geography, Europe led with 39.14% revenue share in 2025, whereas Asia-Pacific is forecast to expand at a 6.23% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Milk Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing trend for organic and clean label products | +0.6% | North America and Europe, spillover to Asia-Pacific urban centers | Medium term (2-4 years) |

| Innovation in flavor combinations and product formats | +0.7% | Global, with early adoption in North America, Europe, and Japan | Short term (≤ 2 years) |

| Rising demand for premium or artisanal chocolate products | +0.9% | Europe, North America, Asia-Pacific (China, India affluent segments) | Long term (≥ 4 years) |

| Increased focus on sustainability initiatives | +0.5% | Global, regulatory-driven in Europe, brand-driven in North America | Long term (≥ 4 years) |

| Sales spike during seasonal and festive demand | +0.4% | Global, peak intensity in North America (Valentine's, Easter, Halloween, Christmas) and Asia (Diwali, Lunar New Year) | Short term (≤ 2 years) |

| Growing online retail penetration for confectionery | +0.8% | Asia-Pacific core, rapid expansion in India, China; mature growth in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Trend for Organic and Clean Label Products

The global milk chocolate market is being increasingly shaped by the growing demand for organic and clean-label products, as consumers prioritize simpler ingredient lists and transparent sourcing. Ethical certifications such as Fairtrade and Rainforest Alliance are gaining momentum, reflecting brand commitments to fair farmer pricing and traceability initiatives that support sustainable supply chains. For example, in June 2024, Nestlé introduced sustainably sourced chocolate tablets in travel retail, featuring four flavors made with responsibly sourced cocoa. This development aligns with a broader trend of values-driven purchasing, where consumers seek products that combine indulgence with responsible consumption. Stricter regulatory frameworks and evolving consumer preferences are driving the market toward premium organic offerings, which deliver higher profit margins while meeting sustainability standards. According to the Research Institute of Organic Agriculture and IFOAM, organic food spending per capita in Europe reached EUR 481 in Switzerland in 2024, highlighting significant demand for organic products in key regions and underscoring the strategic importance of clean-label innovation within the milk chocolate sector[1]Source: Research Institute of Organic Agriculture, "The World of Organic Agriculture Statistics and Emerging Trends 2025", fibl.org.

Innovation in Flavor Combinations and Product Formats

In the global milk chocolate market, brands are increasingly innovating with flavor combinations and product formats to distinguish themselves. Younger consumers, in particular, are gravitating towards adventurous blends that harmonize sweet and savory notes, introduce unexpected textures, and feature global ingredients like matcha and yuzu. Mars is rolling out products like M&M's Peanut Butter and Jelly and Snickers Dark Ice Cream Bars in 2025, aiming to captivate Gen Z with unique flavors. Hershey's is also in on the action, unveiling seasonal treats like Kit Kat Ghost Toast and Reese's Werewolf Tracks for Halloween 2024, underscoring the power of limited-time offerings in boosting consumer engagement and solidifying retail ties. This growing appetite for novelty is prompting companies to not only launch daring new flavors and modernize classic products but also to heavily invest in production capabilities. Moreover, technologies like AI are being harnessed to speed up product development, fine-tune taste and texture, and craft recipes that cater to health-conscious consumers. Collectively, these advancements signal a shift in the milk chocolate realm, moving from mere indulgence to a vibrant landscape shaped by creativity, cultural nuances, and an ever-curious consumer base.

Rising Demand for Premium or Artisanal Chocolate Products

As consumers increasingly prioritize single-origin, organic, and craft-made products, the global milk chocolate market is pivoting towards premium and artisanal offerings. This trend of premiumization is prompting established brands to bolster their high-end portfolios, while artisanal startups gain traction by spotlighting sustainability, craftsmanship, and ethical sourcing. Companies like Fruition Chocolate Works and Omnom Chocolate have carved out a notable market presence, thanks to their transparent production methods and artisanal approach. The rising allure of luxury chocolates is not just reshaping product positioning; it's spurring innovations in flavors and formats, enriched by cultural nuances and regional specialties. Concurrently, a commitment to responsible sourcing and traceability is bolstering consumer trust, positioning premium chocolate as both an indulgent treat and a conscious choice. This shift towards quality-centric products, largely driven by millennials and Gen Z, underscores the industry's evolution. As of 2024, millennials, numbering 74.19 million, stand as the largest generational demographic in the U.S., wielding significant influence over market trends, as highlighted by the US Census Bureau [2]Source: United States Census Bureau, "National Population by Characteristics: 2020-2024", census.gov . This demographic landscape has steered the milk chocolate sector towards crafting premium offerings that marry product excellence with corporate authenticity.

Increased Focus on Sustainability Initiatives

The global milk chocolate market is increasingly driven by sustainability initiatives as manufacturers address environmental, social, and regulatory challenges. The EU Deforestation Regulation, effective December 30, 2025, is set to transform milk chocolate production by mandating full traceability and deforestation-free sourcing across supply chain operations [3]Source: European Commission, "Regulation on Deforestation-free Products", environment.ec.europa.eu. Industry leaders are making significant investments in traceability systems, agroforestry projects, and child labor monitoring, while partnering directly with farmers to enhance incomes and promote sustainable practices. For example, Hershey allocated USD 500 million in 2024 to improve cocoa farming, and Barry Callebaut's Net Zero roadmap targets carbon neutrality by 2050, reflecting the scale of environmental investments required. These measures not only position the industry to comply with stricter regulations, such as deforestation standards, but also enhance consumer confidence by aligning production processes with ethical and environmental principles. As sustainability becomes integral to brand strategies, it is redefining the sourcing, production, and marketing of milk chocolate on a global scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cocoa prices | -1.8% | Global, with acute impact on cost-sensitive markets | Short term (≤ 2 years) |

| Increasing health concerns over sugar content | -0.9% | Developed markets, with regulatory pressure in European Union and United Kingdom | Medium term (2-4 years) |

| Competition from dark and vegan chocolate | -0.7% | North America and Europe, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Stringent food labeling and sugar tax regulations | -0.6% | European Union, United Kingdom, with emerging implementation in Australia and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Cocoa Prices

Global milk chocolate manufacturers grapple with surging cocoa prices, struggling to align rising input costs with consumer price sensitivity. In West Africa, particularly Ghana, supply constraints have not only disrupted cocoa availability but also driven prices higher. Compounding these challenges, financial strains and delayed payments to farmers have emerged. As a result, profit margins are tightening, and trade dynamics are shifting, with international demand waning for beans priced above global benchmarks. Corporate repercussions are evident, with Mondelēz International forecasting a 10% dip in adjusted earnings per share for 2025, a direct fallout of rising cocoa prices. Production shortfalls, coupled with historically low stock levels, underscore the cocoa supply chain's vulnerability. In response, chocolate producers are reevaluating sourcing strategies, considering alternative formulations, and bolstering resilience measures to ensure long-term market stability.

Increasing Health Concerns Over Sugar Content

Health-conscious consumers are driving demand for sugar-reduced and functional ingredients in milk chocolate products. This trend accelerated in 2024 following the UK's sugar tax on soft drinks, which resulted in a 50% reduction in children's sugar consumption. Industry experts are now advocating for the extension of similar regulatory measures to chocolate products. Growing awareness of the health risks associated with high sugar intake is influencing consumer preferences and regulatory frameworks, thereby transforming milk chocolate manufacturing and consumption patterns. Milk chocolate, characterized by higher sugar content and lower cocoa levels compared to dark chocolate, is increasingly viewed unfavorably by health-conscious consumers. Research highlights that while dark chocolate consumption is associated with reduced type 2 diabetes risk and improved weight management, milk chocolate correlates with weight gain and an elevated diabetes risk. With 11-20 grams of added sugar per serving, milk chocolate and chocolate milk products exceed the recommended daily sugar intake for children and women. In response to health concerns such as obesity and heart disease, educational and institutional facilities have implemented restrictions on milk chocolate products. To address these challenges, manufacturers are focusing on developing reduced-sugar formulations and adopting transparent ingredient labeling. The industry is undergoing significant product reformulation efforts to sustain market competitiveness amid rising health awareness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Countlines Drive Convenience-Led Growth

In 2025, molded bars and tablets had dominated the global milk chocolate market, contributing 49.61% of the total revenue. Their broad consumer appeal and frequent consumption established them as the largest segment. While these formats remain the cornerstone of the category, softlines and boxed assortments have gained traction, particularly during seasonal events and gifting occasions. This trend highlights their premium positioning and relevance in cultural celebrations. To strengthen their market presence in these traditional formats, established brands are prioritizing investments in production capacity and innovative packaging strategies.

Meanwhile, countlines have emerged as the fastest-growing segment, with a projected growth rate of 6.89% through 2031. This growth is driven by increasing demand for convenience, portion control, and the broader 'snackification' trend. Consumers are increasingly favoring on-the-go formats, nutrition-enhanced options, and products that combine indulgence with health benefits. Limited-edition and novel varieties are also gaining momentum, supported by impulse-driven retail purchases and curated premium offerings online. This diversification of product formats demonstrates the market's ability to balance traditional preferences with innovative solutions to meet evolving consumer demands.

By Packaging Type: Multi-Serve Gains Amid Household Consumption Shift

In 2025, single-serve packaging dominated the global milk chocolate market, accounting for a significant revenue share of 46.53%. This leadership is driven by factors such as impulse purchases, portion control, and the convenience of on-the-go consumption. Single-serve formats dominate checkout counters and online retail channels, appealing to cost-conscious consumers who prefer smaller packs to manage expenditures while still enjoying indulgent products. Simultaneously, premium brands are enhancing their single-serve offerings by incorporating sustainable packaging solutions, aligning with the preferences of environmentally conscious consumers.

Conversely, multi-serve packaging is positioned as the fastest-growing segment, with a projected CAGR of 6.41% through 2031. This growth is supported by evolving household consumption patterns and value-driven purchasing behavior amid inflationary pressures. Larger packs are increasingly favored by families and groups for shared consumption occasions. Additionally, grocery and specialty retailers are leveraging multi-serve formats to drive seasonal and curated premium product sales. Innovations in frozen bakery and functional chocolate products further enhance the appeal of multi-serve packaging, positioning it as both cost-effective and versatile. This trend underscores the strategic evolution of packaging approaches to balance affordability, sustainability, and lifestyle-oriented consumption.

By Category: Premium Positioning Accelerates Growth

In 2025, mass chocolate commanded a dominant 78.82% share of the global milk chocolate market's revenue, driven by its cost-effectiveness and extensive availability across mainstream retail channels. However, mass-market players face challenges from escalating cocoa prices and consumer resistance to price increases. To address these pressures, companies are implementing strategies such as shrinkflation, recipe modifications, and promotional campaigns to sustain sales volumes. Additionally, private labels are gaining traction by offering competitively priced alternatives that appeal to budget-conscious consumers, further intensifying competition within the segment.

In contrast, the premium and artisanal chocolate segment is expected to grow at a CAGR of 7.81% through 2030, fueled by demand from affluent consumers seeking single-origin, organic, and craft-made products. Established brands are making significant investments in premium production capabilities, while artisanal startups are differentiating themselves through sustainability initiatives, craftsmanship, and innovative flavor profiles. This segment is increasingly perceived as both a luxury indulgence and a lifestyle choice, with younger demographics showing strong interest in exotic flavors, limited-edition offerings, and ethically sourced ingredients. The divergence between the mass and premium segments highlights a shift in consumer preferences, reshaping the competitive dynamics of the milk chocolate market.

By Distribution Channel: Digital Transformation Reshapes Retail

In 2025, supermarkets and hypermarkets accounted for a 34.36% revenue share in the global milk chocolate market. This dominance is driven by their extensive product offerings, competitive pricing strategies, and consistent consumer traffic. These channels not only excel in routine purchases but also play a pivotal role during seasonal sales, particularly for mass-market and gifting products. Traditional retail leverages impulse-driven purchases through strategic checkout placements and endcap displays, while specialty stores establish a competitive edge by offering curated premium and artisanal selections, often supported by expert recommendations.

Online retail is projected to grow at a CAGR of 7.57% through 2031, propelled by the convenience of e-commerce platforms, subscription-based models, and direct-to-consumer strategies. Digital channels are expanding premium access to artisanal and imported chocolates, while quick-commerce platforms address last-minute and impulse-driven demands. The growth of online retail reflects a broader digital transformation, where factors such as consumer reviews, exclusive product launches, and personalized shopping experiences are reshaping the marketing and consumption landscape for milk chocolate. This trend underscores the strategic importance of balancing the established dominance of traditional retail with the rapid growth of digital channels.

Geography Analysis

Europe dominates the milk chocolate market with a 39.14% share in 2025. This leadership is underpinned by established economies such as Germany, the United Kingdom, France, and Switzerland, where strong brand equity and entrenched consumption patterns drive demand. However, the region is navigating increasing regulatory scrutiny, particularly regarding sugar content and deforestation compliance. These pressures are compelling manufacturers to invest in reformulation, traceability, and sustainability initiatives. Leading companies are upgrading production facilities and expanding premium product lines to sustain competitiveness, while growing consumer health awareness continues to influence product strategies.

The Asia-Pacific region is forecasted to grow at a rate of 6.23% through 2031, fueled by rising disposable incomes, urbanization, and increasing demand for premium and artisanal chocolates. India is emerging as a key growth driver, with e-commerce platforms and organized retail channels enhancing access to premium imports and local artisanal brands, which are gaining traction for their focus on sustainability and craftsmanship. In China and Japan, growth is being propelled by product localization efforts, including the adaptation of flavors and textures to align with cultural preferences. Additionally, markets such as Australia are creating opportunities for plant-based and dairy-free chocolate variants. This regional momentum underscores the impact of evolving consumer preferences and cultural factors on market expansion.

North America remains a significant market, supported by strong seasonal demand and substantial investments by leading manufacturers to expand production capacity. However, price-sensitive consumers are resisting cost increases driven by volatile cocoa prices, exerting pressure on margins for mass-market players. Seasonal peaks, such as Valentine’s Day and Halloween, continue to drive sales volumes, while premium and innovative product formats are helping to mitigate challenges in everyday consumption. Meanwhile, South America, the Middle East, and Africa represent smaller but high-potential markets. In these regions, strategies such as offering affordable pack sizes, adopting eco-friendly packaging, and optimizing supply chains are expected to unlock future growth opportunities.

Competitive Landscape

The global milk chocolate market is highly fragmented, with multinational corporations and regional players driving market operations. Leading companies such as Mars, Mondelēz International, Nestlé, Ferrero, and Hershey's are expanding their market presence through strategic mergers, acquisitions, and partnerships. These key players invest in optimizing manufacturing processes, securing high-quality raw materials, and maintaining robust distribution networks across both developed and emerging markets.

Market consolidation continues to be a significant trend, exemplified by Mars' proposed USD 35.9 billion acquisition of Kellanova in 2024. These acquisitions are strategically aimed at enhancing operational efficiencies, diversifying product portfolios, and strengthening bargaining power with commodity suppliers. Companies are streamlining supply chains, adopting digital technologies, and implementing sustainability initiatives to meet regulatory standards and evolving consumer expectations. These strategic measures have enhanced the market's resilience and its ability to respond to dynamic market conditions and consumer demands.

While major corporations dominate the market, regional and artisanal manufacturers effectively compete in niche segments by leveraging product differentiation and localized market expertise. Smaller producers focus on premium product offerings, clean-label formulations, and innovative flavors to cater to consumer preferences for quality and authenticity. This market structure, combining corporate consolidation with regional competition, fosters product diversification and drives innovation in the global milk chocolate market.

Milk Chocolate Industry Leaders

-

Mars, Incorporated

-

Mondelez International

-

Nestlé S.A.

-

Ferrero Group

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nestlé's Aero brand introduced its Aero Caramel flavor bubbles in the United Kingdom and Ireland. This new product from Nestlé Confectionery features caramel-flavored bubbles encased in a milk chocolate and caramel-flavored shell. The Caramel flavor bubbles, part of the Aero product range, are produced using milk supplied by First Milk farmers in southwest Scotland and cocoa certified by the Rainforest Alliance.

- May 2025: The Hershey Company introduced a variant of its traditional milk chocolate bar incorporating a caramel center. The product was distributed in 6-pack formats through United States retail distribution channels for a limited duration.

- March 2025: Cadbury and Lotus Bakeries introduced the Cadbury Dairy Milk Biscoff bar, their first collaborative product, following their partnership announcement in July 2024. The product combined Cadbury Dairy Milk chocolate with Lotus Biscoff biscuit pieces and was available in three variants: a 95g price-marked pack at GBP 1.69, a standard 95g bar, and a 105g bar.

Global Milk Chocolate Market Report Scope

White chocolate is a type of confectionery made from cocoa butter, sugar, and milk solids, but unlike milk or dark chocolate, it does not contain cocoa solids. Its creamy texture and pale ivory color come from the cocoa butter base, while the sweetness is balanced by dairy ingredients.

The

| Softlines/Selflines |

| Countline |

| Molded Bars/Tablets |

| Boxed Assortments |

| Others |

| Wrappers (Foil, Paper, Plastic) |

| Boxes |

| Pouches and Bags |

| Tins/Can |

| Mass |

| Premium/Luxury |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Form | Softlines/Selflines | |

| Countline | ||

| Molded Bars/Tablets | ||

| Boxed Assortments | ||

| Others | ||

| By Packaging Type | Wrappers (Foil, Paper, Plastic) | |

| Boxes | ||

| Pouches and Bags | ||

| Tins/Can | ||

| By Category | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the milk chocolate market by 2031?

The milk chocolate market is expected to reach USD 121.29 billion by 2031, expanding at a 4.94% CAGR.

Which region will grow the fastest in milk chocolate sales?

Asia-Pacific is forecast to record the highest regional CAGR of 6.23% through 2031 as urbanization and disposable income growth lift per-capita consumption.

Why is online retail important for milk chocolate makers?

E-commerce, advancing at a 7.57% CAGR, enables direct-to-consumer sales, better data access, and higher gross margins, turning it into the fastest-growing distribution channel.

What drives the premium segment’s faster expansion?

Consumer willingness to pay for single-origin sourcing, artisanal production, and ethical credentials pushes premium products toward a 7.81% CAGR, well above the mass segment.

Page last updated on: