Organic Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.2 Billion |

| Market Size (2031) | USD 35.5 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Milk Market Analysis by Mordor Intelligence

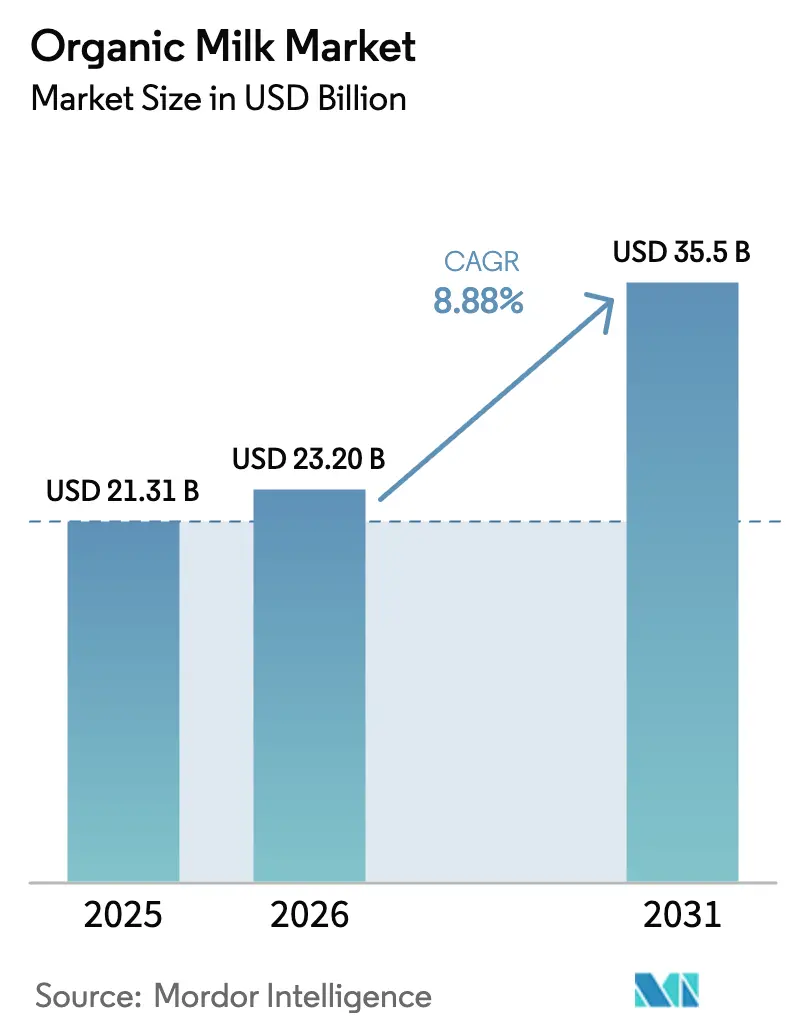

The organic milk market size is expected to grow from USD 21.31 billion in 2025 to USD 23.2 billion in 2026 and is forecast to reach USD 35.5 billion by 2031 at 8.88% CAGR over 2026-2031. This growth is driven by increasing consumer awareness regarding the health benefits of organic milk, such as its higher nutritional content and absence of synthetic hormones or antibiotics. Additionally, the rising demand for sustainable and environmentally friendly dairy products is further propelling market expansion. The growing preference for organic food and beverages, coupled with supportive government initiatives promoting organic farming practices, is expected to create significant opportunities for market players. Furthermore, the increasing availability of organic milk through various distribution channels, including supermarkets, online platforms, and specialty stores, is enhancing accessibility and contributing to the market's growth trajectory. Europe remains the revenue leader, while Asia-Pacific shows the strongest pace as disposable incomes and lactose-sensitivity solutions converge. Although the market is moderately fragmented, rising compliance costs are accelerating consolidation among scale-efficient producers.

Key Report Takeaways

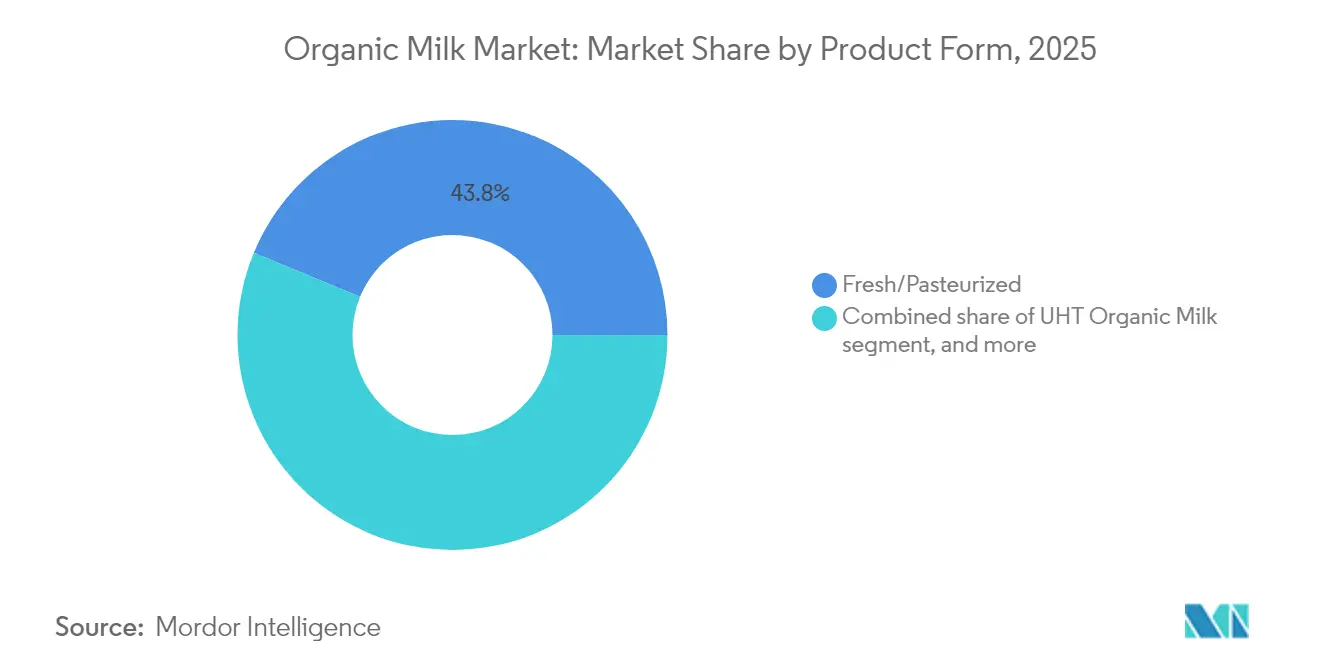

- By product form, fresh/pasteurized milk led with 43.75% revenue share in 2025; UHT milk is projected to grow at 9.67% CAGR through 2031.

- By source, cow-derived milk held 86.05% of the organic milk market share in 2025, while goat milk is advancing at a 10.25% CAGR to 2031.

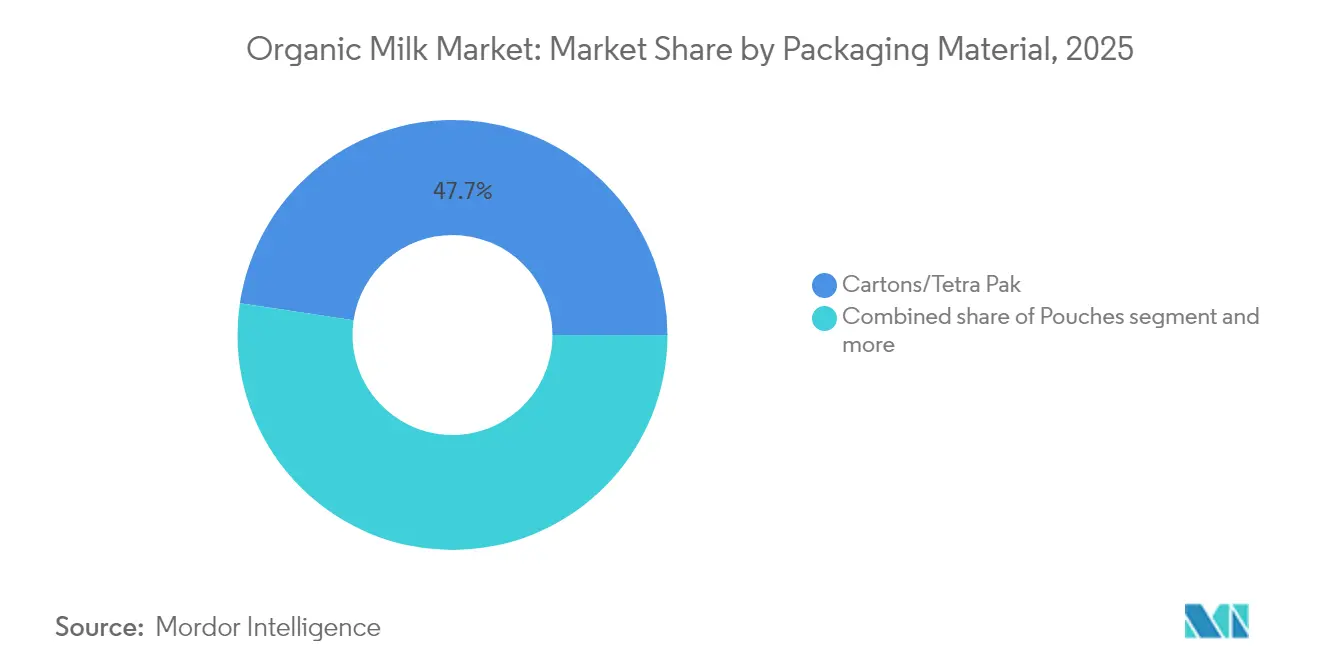

- By packaging, cartons/Tetra Pak accounted for 47.65% of the organic milk market size in 2025, and pouches are forecast to rise at an 11.1% CAGR.

- By distribution channel, off-trade controlled 57.75% revenue in 2025; on-trade is set to expand at an 11.15% CAGR.

- By geography, Europe held 33.85% of global revenue in 2025, whereas Asia-Pacific is expected to register a 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for chemical-free dairy driven by antibiotic and hormone residue concerns | +2.1% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Rising demand for organic and natural products | +1.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Growing preference for clean-label products | +1.5% | North America and Europe primarily | Medium term (2-4 years) |

| Government support for organic farming | +1.2% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| A2-beta casein organic milk gaining traction among lactose-sensitive consumers | +0.9% | Global, with early adoption in Asia-Pacific and North America | Short term (≤ 2 years) |

| Rapid uptake of UHT organic milk via e-commerce platforms | +0.7% | Global, accelerated in rural and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for chemical-free dairy driven by antibiotic and hormone residue concerns

Consumer awareness of antibiotic resistance and hormone disruption has elevated organic milk from a niche product to a mainstream health necessity, particularly as regulatory bodies tighten residue monitoring protocols. Under the 2024 SOE rule, the USDA has ramped up testing requirements, instituting stricter screenings for prohibited substances. This move not only fortifies a quality assurance framework but also validates consumer apprehensions regarding the safety of conventional dairy. By ensuring compliance with these enhanced standards, the rule aims to build greater consumer trust in organic dairy products. With this regulatory endorsement, organic certification evolves from merely a marketing assertion to a credible health assurance, offering tangible benefits that consumers can rely on. This shift has bolstered acceptance of premium pricing across diverse demographic groups, as consumers increasingly prioritize health and safety in their purchasing decisions. Furthermore, the ban on synthetic hormones, such as rBST, in organic milk directly addresses concerns about endocrine disruptions, which have been linked to potential long-term health risks. This heightened awareness and demand for safer alternatives create a defensive moat around organic milk's market share, enabling it to maintain a competitive edge in the broader dairy market.

Rising demand for organic and natural products

Organic milk purchases often act as a gateway, leading consumers to explore a wider range of organic food categories. This trend not only boosts consumer interest but also reinforces retailers' commitment to dedicating shelf space for organic products. The USDA's Organic Transition Initiative, with its USD 300 million allocation for producer support, underscores the government's acknowledgment of organic agriculture's pivotal role in ensuring food system resilience and promoting environmental sustainability [1]Source: United States Department of Agriculture, "USDA Easing Producers’ Transition to Organic Production with New Programs and Partnerships, Announces Investments to Create and Expand Organic Markets", www.nrcs.usda.gov. During times of economic uncertainty, consumers exhibit a heightened willingness to pay premium prices for organic products. This behavior underscores a prioritization of health investments over discretionary spending, resulting in a counter-cyclical demand pattern. Furthermore, the appeal of natural products has expanded. It's no longer limited to just organic certification; consumers are increasingly drawn to claims of regenerative agriculture, grass-fed sourcing, and carbon-neutral production methods. This shift is particularly pronounced among environmentally conscious consumers. As these trends converge, they create diverse value propositions within the organic milk category. This not only facilitates price segmentation but also paves the way for broader market expansion strategies.

Growing preference for clean-label products

In the realm of organic milk, clean-label positioning goes beyond just ingredient transparency. It now includes visibility into production methods, traceability within the supply chain, and disclosures about environmental impacts—all of which resonate with today's informed consumers. The EU, through its Regulation 2018/848, has set forth mandatory organic labeling requirements. These standardized transparency protocols not only bolster consumer confidence across borders but also pave the way for market expansion for producers who adhere to them. Organic milk boasts clean-label advantages, notably the absence of synthetic additives, artificial preservatives, and processing aids—common in conventional dairy for extending shelf life and optimizing costs. With the rise of digital platforms, consumers can easily scrutinize ingredients and compare brands. This digital empowerment rewards producers who champion transparency and penalizes those with convoluted additive profiles. The clean-label premium associated with organic milk justifies its higher price point, positioning it as a minimally processed and nutritionally superior choice over conventional options. This trend is gaining momentum in developed markets, bolstered by regulatory frameworks that champion transparency and a consumer base that's increasingly educated and discerning in their purchasing choices.

Government support for organic farming

In the European Union, the Common Agricultural Policy dedicates a quarter of its direct payments to eco-schemes, incentivizing organic farming practices. This move not only rewards eco-friendly practices but also spurs land conversion and boosts production capacity. Meanwhile, in the U.S., the USDA's Organic Certification Cost Share Program alleviates financial burdens by covering up to 75% of certification costs [2]Source: United States Department of Agriculture, "Financial Resources for Organic Farmers and Ranchers", www.usda.gov. This support paves the way for smaller producers, granting them access to markets they once deemed economically out of reach. Beyond direct subsidies, government backing encompasses research funding, technical assistance, and market development grants. These efforts bolster the organic supply chain and enhance producer capabilities. A testament to this targeted support, the Organic Dairy Marketing Assistance Program allocated a substantial USD 104 million in 2023, specifically aiding small organic dairy operations [3]Source: United States Department of Agriculture, "USDA Created Organic Assistance Programs From 2021–23 in Response to Disruptions, Decreased Organic Transitioning Acreage", www.ers.usda.gov. Such policy alignment between environmental goals and agricultural backing not only stabilizes organic farming investments but also steers capital towards expanding organic production. On the international front, trade agreements are increasingly acknowledging the equivalency of organic standards. This recognition not only smooths the path for export market access but also fosters the global supply chain growth of organic dairy products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shorter shelf-life vs conventional UHT milk limits rural distribution | -1.4% | Global, particularly emerging markets with limited cold chain | Medium term (2-4 years) |

| Complex certification compliance (NOP, EU 2018/848) elevates small-farm costs | -1.1% | Global, with higher impact in fragmented farming regions | Long term (≥ 4 years) |

| Limited availability of organically raised livestock constrains raw milk supply | -0.8% | Global, concentrated in regions with limited organic feed supply | Long term (≥ 4 years) |

| Price sensitivity among consumers hindering the market growth | -0.6% | Global, with higher impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shorter shelf-life vs conventional UHT milk limits rural distribution

Organic milk's reduced shelf-life compared to conventional UHT products creates distribution bottlenecks in rural markets where cold chain infrastructure remains underdeveloped and delivery frequencies are constrained by economic viability. This shelf-life difference is especially evident in tropical climates, where temperature variations hasten spoilage and amplify product losses during distribution. To penetrate these rural markets, investments in specialized cold storage and transportation are essential, driving up per-unit distribution costs by an estimated 15-25% over conventional milk logistics. Retailers in remote areas hesitate to stock organic milk due to concerns over inventory turnover and the financial implications of spoilage, creating barriers that restrict organic milk's market access. This challenge is magnified in developing regions, where organic milk is viewed as a premium product, yet the distribution infrastructure falls short of ensuring the necessary cold chain consistency. While advanced packaging technologies and enhancements in UHT processing present viable solutions, their adoption is hampered by cost and the need for specialized technical expertise.

Complex certification compliance (NOP, EU 2018/848) elevates small-farm costs

Organic certification costs increased 10-20% following implementation of enhanced enforcement requirements, creating financial barriers that disproportionately impact smaller dairy operations with limited administrative resources.The USDA's SOE rule mandates expanded documentation, fraud prevention plans, and enhanced traceability systems that require specialized expertise and technology investments beyond the reach of many family-scale operations. Compliance complexity extends beyond initial certification to ongoing monitoring, annual inspections, and supply chain verification that creates recurring administrative burdens and professional service costs. Small-farm consolidation accelerates as certification requirements favor larger operations with dedicated compliance staff and integrated supply chain control, reducing market diversity and producer competition. The regulatory burden creates barriers to entry for new organic producers while forcing existing small operations to either scale up, exit the market, or accept lower margins through cooperative arrangements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Fresh Milk Dominates, UHT Organic Milk Accelerates

Fresh and pasteurized milk captured 43.75% of the revenue in 2025, establishing itself as a key segment in the organic milk market. Its dominance is attributed to its familiar taste, which appeals to a wide range of consumers, particularly those seeking traditional dairy options. The segment also benefits from a robust cold chain infrastructure that ensures the consistent availability and quality of fresh organic milk. Urban consumers, who prioritize freshness and nutritional value, are the primary drivers of demand for this segment. Additionally, fresh organic milk is often perceived as a healthier and more natural choice, aligning with the growing consumer preference for minimally processed food products. The segment's strong performance is further supported by its presence in retail outlets, supermarkets, and specialty organic stores, where it remains a staple product for health-conscious buyers.

UHT organic milk, on the other hand, is expected to witness significant growth, with a projected CAGR of 9.67% during the forecast period. This growth is fueled by increasing demand in rural areas, where the lack of cold chain infrastructure makes UHT milk a practical alternative due to its extended shelf life. Additionally, the growing penetration of online platforms has enhanced the accessibility of UHT organic milk, broadening its consumer base. The convenience and longer storage capability of UHT milk make it an attractive option for consumers with limited access to fresh milk, further driving its adoption. UHT organic milk is also gaining traction among working professionals and households with unpredictable consumption patterns, as it eliminates the need for refrigeration and reduces wastage.

By Source: Cow Milk Leads, Gota Milk Gain Momentum

In 2025, cow milk accounted for a significant 86.05% of the revenue in the organic milk market, underscoring its well-established supply-chain maturity. The dominance of cow milk can be attributed to its widespread availability, consumer familiarity, and extensive distribution networks. Additionally, cow milk remains a staple in many households due to its versatility in various applications, including direct consumption, dairy-based products, and culinary uses. The strong presence of cow milk in the organic segment is further supported by advancements in organic farming practices and certifications, which ensure product quality and safety, thereby driving consumer trust and preference.

Goat milk, on the other hand, is emerging as a rapidly growing segment within the organic milk market, advancing at a robust CAGR of 10.25%. This growth is primarily driven by its unique nutritional profile, including the presence of A2 protein, which is easier to digest compared to the A1 protein found in most cow milk. Goat milk is particularly appealing to consumers with lactose sensitivity or digestive issues, as it is known for its lower lactose content and smaller fat globules, which enhance digestibility. Furthermore, the rising awareness of goat milk's health benefits, coupled with its increasing availability in organic variants, is attracting a niche but growing consumer base. This trend is expected to continue as producers expand their offerings and invest in marketing efforts to highlight the advantages of goat milk in the organic segment.

By Packaging Material: Sustainability Shapes Choice

In 2025, cartons and Tetra Pak led the organic milk market, capturing 47.65% of the revenue. Their dominant position stems from their recyclability, resonating with the rising consumer demand for sustainable packaging. Moreover, established supplier networks bolster their market stance, ensuring reliable supply and building trust with stakeholders. Cartons, known for their durability and convenience, have become the go-to choice for organic milk packaging, further cementing their popularity. Additionally, cartons and Tetra Pak provide extended shelf life for organic milk by offering effective protection against external contaminants, which is a critical factor for both manufacturers and consumers. This feature enhances their appeal in the market, especially in regions with limited cold chain infrastructure.

On the other hand, pouches are swiftly carving out a niche in the organic milk arena. With a projected CAGR of 11.1% during the forecast period, their ascent is fueled by being lightweight, cost-effective, and easy to store—qualities that resonate with consumers and manufacturers alike. Pouches' design and size flexibility caters to diverse consumer preferences. Furthermore, their lower production costs compared to other packaging formats make them an attractive option for manufacturers aiming to optimize profit margins. As the appetite for innovative and convenient packaging surges, pouches are poised to solidify their standing in the organic milk market. Their growing adoption is also supported by advancements in material technology, which enhance their barrier properties and ensure the freshness of organic milk.

By Distribution Channel: Off-Trade Leads, On-Trade Gain Momentum

In 2025, off-trade channels accounted for 57.75% of the revenue in the organic milk market, making it the dominant distribution channel. The off-trade segment encompasses supermarkets, hypermarkets, convenience stores, and online retail platforms, which have become increasingly popular due to their accessibility and extensive product offerings. Supermarkets and hypermarkets, in particular, attract a large consumer base by providing a variety of organic milk brands under one roof, often accompanied by promotional deals and discounts. Convenience stores cater to consumers seeking quick and easy access to organic milk, especially in urban areas. Furthermore, the rapid growth of e-commerce platforms has significantly contributed to the segment's success. Online retail channels not only offer the convenience of home delivery but also provide detailed product information, customer reviews, and subscription options, which appeal to tech-savvy and health-conscious consumers.

On the other hand, the on-trade segment is projected to grow at a CAGR of 11.15% during the forecast period. This segment includes hotels, restaurants, cafes, and other food service establishments that are increasingly incorporating organic milk into their menus to meet the growing demand for healthier and more sustainable food and beverage options. The rising consumer preference for organic and natural products has encouraged food service providers to source high-quality organic milk for use in various applications, such as specialty coffees, teas, and desserts. Premium dining establishments and cafes are leveraging the appeal of organic milk to differentiate their offerings and attract health-conscious customers. Additionally, the trend of using organic milk in innovative beverages, such as plant-based milk blends and artisanal lattes, is further driving the segment's growth. The on-trade segment's expansion is also supported by the increasing number of partnerships between organic milk producers and food service providers, ensuring a steady supply of high-quality products to meet the evolving preferences of consumers.

Geography Analysis

In 2025, Europe secures a 33.85% market share in the organic milk market, bolstered by its robust organic farming infrastructure, backing from the Common Agricultural Policy, and consumers' willingness to pay a premium for organic goods. The region benefits from well-established supply chains and stringent regulatory frameworks that ensure the quality and authenticity of organic milk products. Additionally, the growing demand for sustainable and environmentally friendly dairy options further supports market growth in Europe. Countries such as Germany, France, and the United Kingdom are leading contributors, with a strong focus on organic certifications and consumer trust in locally sourced products. The increasing adoption of plant-based diets alongside organic dairy consumption also complements the market's growth trajectory.

Asia-Pacific emerges as the fastest-growing region in the organic milk market, boasting a 10.62% CAGR through 2031. This growth is fueled by increasing disposable incomes, heightened health awareness, and urbanization trends that lean towards premium food offerings. The region's expanding middle-class population and rising preference for organic and natural products contribute significantly to the market's rapid expansion. Governments in countries like China and India are also promoting organic farming practices, which is expected to further drive the demand for organic milk in the forecast period. Additionally, the growing influence of Western dietary habits and the proliferation of e-commerce platforms are making organic milk more accessible to consumers in urban and semi-urban areas. Countries such as Japan and South Korea are also witnessing a surge in demand due to their focus on high-quality, health-oriented food products.

In North America, the United States leads the market due to a strong preference for organic dairy products and the presence of key market players. The region also benefits from advanced farming techniques, government subsidies for organic farming, and a well-developed distribution network that ensures product availability across urban and rural areas. Canada is also contributing to the market with its growing organic dairy sector and consumer inclination towards sustainable food choices. Meanwhile, South America is witnessing steady growth, supported by rising health consciousness and the adoption of organic farming practices in countries like Brazil and Argentina. The region's favorable climatic conditions for organic farming and increasing government initiatives to promote organic agriculture are driving the market.

Competitive Landscape

The organic milk market demonstrates moderate fragmentation, with a concentration rating of 4 out of 10. This rating indicates that while the market is not highly consolidated, it is under significant consolidation pressure. Regulatory compliance costs, which include stringent organic certification requirements and adherence to food safety standards, are becoming increasingly burdensome for smaller operators. Additionally, the growing complexity of supply chains, driven by the need for consistent organic feed sourcing and efficient distribution, further exacerbates challenges for these smaller players. As a result, many smaller operators are exiting the market, leaving room for larger, more established companies to strengthen their competitive positioning. This trend is reshaping the market dynamics, creating a more competitive environment that favors scalability and operational efficiency.

Vertical integration has emerged as a dominant strategy among leading companies in the organic milk market. By securing organic feed supply chains, processing capabilities, and distribution networks, these companies aim to gain greater control over their operations and ensure end-to-end quality management. This approach not only guarantees consistent product quality but also helps in managing costs effectively across the value chain. For instance, controlling feed supply reduces dependency on external suppliers, mitigating risks associated with price volatility and supply shortages. Similarly, owning processing facilities allows companies to maintain stringent quality standards, while direct distribution networks enable them to reach consumers more efficiently. Such integration provides a significant competitive advantage, allowing these players to navigate market challenges more effectively and maintain profitability in a highly regulated environment.

Furthermore, the focus on vertical integration reflects the broader strategic patterns shaping the competitive landscape of the organic milk market. Companies are increasingly investing in infrastructure, technology, and partnerships to enhance their operational efficiency and expand their market reach. For example, investments in advanced processing technologies enable companies to produce a wider range of organic milk products, catering to diverse consumer preferences. Partnerships with local organic farmers ensure a steady supply of high-quality raw materials, while collaborations with retailers strengthen distribution networks. By controlling multiple stages of the value chain, from sourcing organic feed to delivering the final product, these players can respond more effectively to evolving consumer demands and regulatory requirements.

Organic Milk Industry Leaders

-

Nestlé S.A.

-

Groupe Lactalis

-

Arla Foods amba

-

Fonterra Co-operative Group Ltd.

-

Horizon Organic Dairy LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Indonesia’s PT Ultrajaya Milk Industry and Trading (Ultra Milk) has launched its first-ever organic UHT milk. Certified as Organik Indonesia, this new organic milk marks Ultrajaya’s move up the value chain. It is made from 100% organic cow’s milk sourced from certified organic farms.

- October 2024: Tetra Pak and Lactalis launched a carton package using certified recycled polymers linked to used beverage cartons, marking a significant advancement in sustainable packaging for the dairy industry.

- July 2024: Maple Hill Creamery expanded by adding 14 new farms in Central Pennsylvania, increasing its network to 120 small, family farms dedicated to producing 100% grass-fed organic dairy products.

- March 2024: Kaneka introduced Pur Natur™, an organic milk crafted from 100% organic raw milk. The product is made using raw milk sourced from Betsukai Wellness Farm, an organic circular dairy farm operated by the Kaneka Group. This farm emphasizes sustainable practices by integrating organic farming methods with circular dairy farming, ensuring minimal environmental impact while maintaining high-quality organic milk production.

Global Organic Milk Market Report Scope

Organic milk is a type of organic dairy product obtained from livestock raised in an organic agricultural setting.

The global organic milk market is segmented by product form, source, packaging material, distribution channel, and geography. By product form, the market is segmented into fresh/pasteurized organic milk, UHT organic milk, powdered organic milk, flavored organic milk, and others. By source, the market is segmented into cow, buffalo, goat, and others. Based on packaging material, the market is segmented into cartons/tetra pak, plastic bottles (HDPE, PET), glass bottles, pouches, and others. Based on the distribution channel, the market is segmented into off-trade and on-trade channels. Off-trade is further segmented into supermarkets/hypermarkets, convenience stores & specialty stores, online retail stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Fresh/Pasteurized Organic Milk |

| UHT Organic Milk |

| Powdered Organic Milk |

| Flavored Organic Milk |

| Other Product Forms |

| Cow |

| Buffalo |

| Goat |

| Other Sources |

| Cartons/Tetra Pak |

| Plastic Bottles (HDPE, PET) |

| Glass Bottles |

| Pouches |

| Other Packaging Materials |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience and Specialty Stores | |

| Online Retailers | |

| Other Off-Trade Channels | |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Form | Fresh/Pasteurized Organic Milk | |

| UHT Organic Milk | ||

| Powdered Organic Milk | ||

| Flavored Organic Milk | ||

| Other Product Forms | ||

| By Source | Cow | |

| Buffalo | ||

| Goat | ||

| Other Sources | ||

| By Packaging Material | Cartons/Tetra Pak | |

| Plastic Bottles (HDPE, PET) | ||

| Glass Bottles | ||

| Pouches | ||

| Other Packaging Materials | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience and Specialty Stores | ||

| Online Retailers | ||

| Other Off-Trade Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the organic milk market?

The organic milk market is worth USD 23.2 billion in 2026 and is projected to reach USD 35.5 billion by 2031.

Which region leads the organic milk market?

Europe holds the highest revenue share at 33.85% in 2025, supported by harmonized regulations and mature consumer demand.

Which product form is growing the fastest?

UHT organic milk is expanding at a 9.67% CAGR because its long shelf life facilitates rural and e-commerce distribution.

Why is goat organic milk gaining popularity?

Goat milk contains naturally occurring A2 proteins that are easier to digest, driving a 10.25% CAGR between 2026 and 2031.

Page last updated on: