Coconut Milk And Cream Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

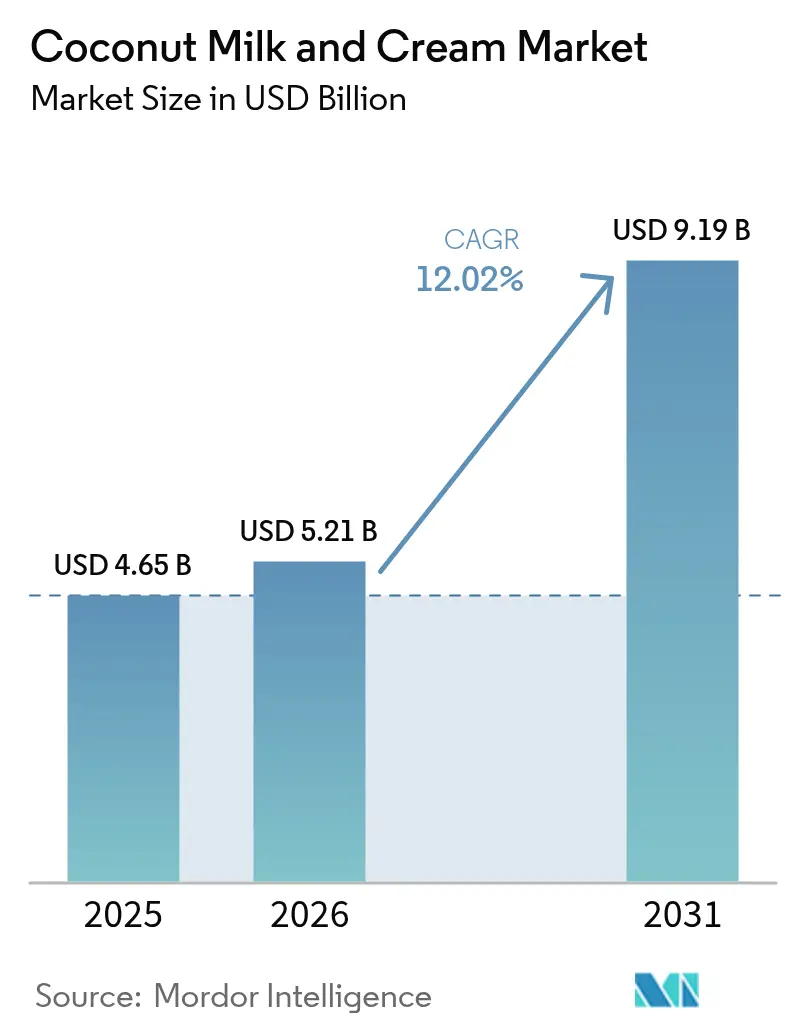

| Market Size (2026) | USD 5.21 Billion |

| Market Size (2031) | USD 9.19 Billion |

| Growth Rate (2026 - 2031) | 12.02% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coconut Milk And Cream Market Analysis by Mordor Intelligence

The coconut milk and cream market size in 2026 is estimated at USD 5.21 billion, growing from 2025 value of USD 4.65 billion with 2031 projections showing USD 9.19 billion, growing at 12.02% CAGR over 2026-2031. The market growth is driven by increasing demand for plant-based nutrition, broader culinary applications, and expansion of organized retail channels. The products' functional benefits, including medium-chain triglycerides, natural electrolytes, and clean ingredient profiles, contribute to their market appeal. The sustainability aspects of coconut cultivation, characterized by long-productive palm trees and minimal irrigation needs, further support market growth. The market expansion is also supported by increased production capacity among integrated processors and the implementation of traceability and ethical sourcing certifications, leading to greater premium retail presence. Despite El Niño-related harvest disruptions causing price fluctuations, consumers' association of higher prices with quality and origin has positively influenced the market's value growth.

Key Report Takeaways

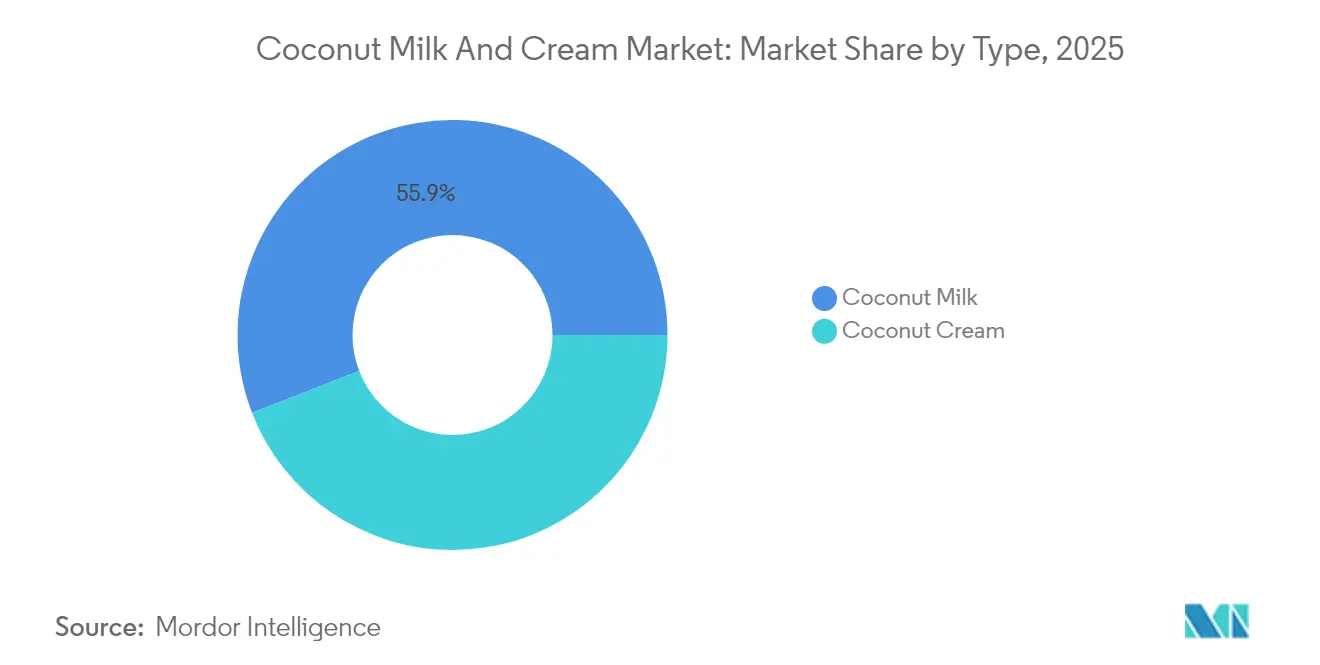

- By product type, coconut milk held 55.88% of the coconut milk and cream market share in 2025, whereas coconut cream is forecast to expand at a 13.05% CAGR between 2026-2031.

- By category, conventional offerings accounted for 65.92% of the coconut milk and cream market size in 2025, while organic lines are set to rise at a 16.18% CAGR through 2031.

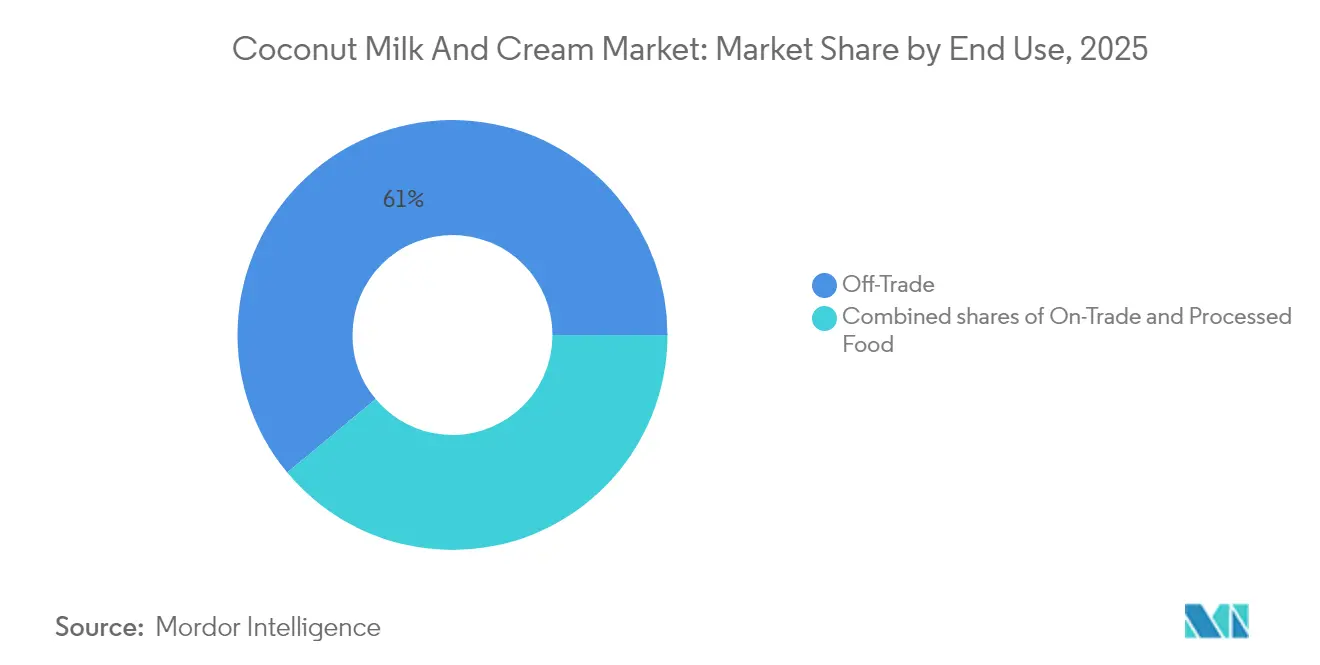

- By end use, off-trade channels captured 61.05% revenue share in 2025, and processed food applications are positioned for the highest 13.52% CAGR over the forecast window.

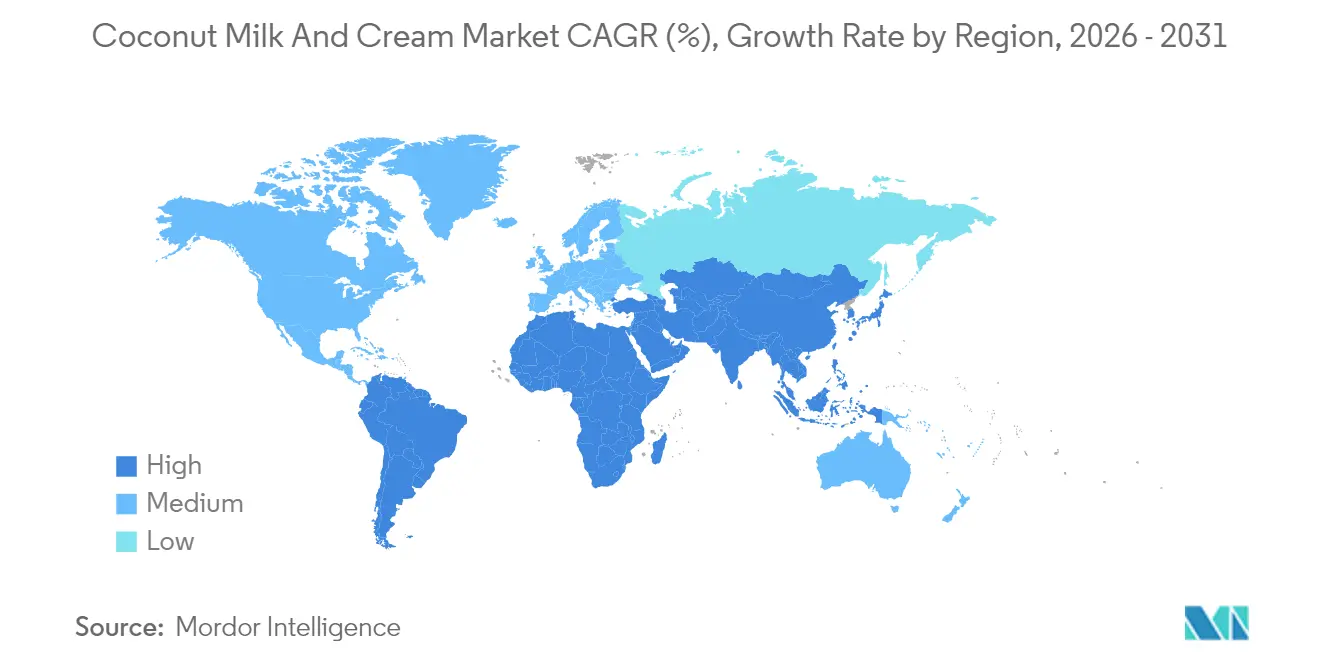

- By geography, Asia-Pacific led with 54.62% value share in 2025, but North America is projected to deliver the fastest 13.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coconut Milk And Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plant-based and vegan diet adoption | +2.1% | North America, Europe, Global | Medium term (2-4 years) |

| Increasing lactose intolerance | +1.8% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Clean-label ingredient preference | +1.5% | North America, EU, APAC | Medium term (2-4 years) |

| Ethical and sustainable sourcing focus | +1.2% | EU, North America, Urban APAC | Long term (≥ 4 years) |

| Packaging formats that extend shelf life | +0.9% | Developed markets worldwide | Short term (≤ 2 years) |

| Established food certifications | +0.8% | EU, North America, Emerging APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Plant-Based and Vegan Diets

The coconut milk market has undergone a remarkable transformation, evolving from a specialized health product into a widely embraced dairy alternative in the global food and beverage industry. This shift reflects changing consumer preferences, as individuals increasingly value the product's distinctive functional attributes and sensory characteristics. The rich, creamy texture of coconut milk, combined with its exceptional performance in high-temperature cooking applications, has established it as a versatile ingredient in both commercial and household kitchens. Market acceptance has expanded beyond traditional plant-based consumers to encompass a broader demographic, including flexitarians and health-conscious individuals who seek to reduce dairy consumption while maintaining familiar taste and texture experiences. This trend is particularly evident in European markets, as highlighted by GFI Europe's 2024 report, which documents consistent growth across major countries including France, Germany, Italy, Spain, the Netherlands, and the UK. The market's expansion has been notably supported by the introduction of affordable private-label products, especially in the plant-based milk and beverages category, making these alternatives more accessible to a wider consumer base [1]Source: Good Food Institute, “Plant-based retail sales in six European countries, 2022 to 2024,” gfieurope.org.

Growing Lactose Intolerance Fueling Demand for Dairy Alternatives

Lactose intolerance affects a significant portion of the global adult population, creating a substantial market for coconut-based dairy alternatives. Unlike trend-driven consumption, the medical necessity of lactose-intolerant individuals ensures consistent demand across various product categories. Coconut milk offers advantages over soy and nut-based alternatives due to its natural enzyme composition and lack of common allergens, particularly in markets where multiple food sensitivities are prevalent. The Asia-Pacific region shows strong market potential due to high rates of genetic lactose intolerance and established coconut milk consumption patterns. The growing medical recognition and diagnosis of lactose intolerance as a cause of digestive issues continues to expand the market beyond traditional consumer segments, as healthcare providers increasingly recommend suitable dairy alternatives to their patients. This medical validation strengthens market growth prospects, as consumers seek long-term solutions for their dietary requirements rather than following temporary food trends. According to Boston Children's Hospital, approximately 30-50 million Americans are lactose intolerant. This includes 80% of African-Americans and Native Americans, and over 90% of Asian-Americans [2]Source: Boston’s Children’s Hospital, “Lactose Intolerance,” childrenshospital.org.

Consumer Preference for Natural Ingredients and Clean-Label Products

Coconut milk's straightforward ingredient composition and minimal processing requirements give it a distinct competitive advantage in the plant-based alternatives market. Its formulation remains simple and uncomplicated, contrasting significantly with alternatives that depend on stabilizers, emulsifiers, and flavor masking agents. Consumer studies demonstrate that coconut-based products consistently receive higher naturalness ratings, primarily because consumers recognize and trust coconut as a familiar whole food ingredient. This positive market perception enables companies to implement premium pricing strategies, as consumers demonstrate strong willingness to pay more for products they consider minimally processed. In response to this market dynamic, major brands have begun implementing comprehensive traceability systems to document coconut sourcing from farms and processing facilities, addressing the growing consumer demand for ingredient transparency.

Increasing Interest in Sustainable and Ethically Sourced Food Products

The growing emphasis on sustainability has transformed from an aspirational goal to a key purchasing factor, with coconut cultivation offering environmental advantages compared to dairy production and other nut alternatives. Coconut palms demonstrate environmental benefits through their multi-generational productive lifespan and contribution to tropical ecosystem preservation, unlike annual crops that require frequent soil disturbance and agricultural inputs. The sustainability profile, however, faces challenges due to child labor issues in major producing countries, particularly the Philippines, where the industry is implementing certification programs and farmer partnerships to improve supply chain ethics. The European Union's Deforestation Regulation presents opportunities for compliant coconut suppliers to access premium European markets, while creating barriers for non-compliant sources. The impact of sustainability certifications on consumer behavior varies by region, with European and North American markets showing the strongest connection between environmental certifications and purchasing decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory challenges in labeling and food safety standards | -1.2% | EU & North America primarily, expanding globally | Medium term (2-4 years) |

| Limited availability of high-quality raw coconuts in some regions | -0.8% | Global supply chain, acute in processing regions | Short term (≤ 2 years) |

| High cost of coconut milk and cream compared to conventional dairy | -0.6% | Global, particularly price-sensitive emerging markets | Long term (≥ 4 years) |

| Challenges in ensuring sustainable and ethical sourcing across the supply chain | -0.4% | EU & North America compliance markets, APAC production regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Challenges in Labeling and Food Safety Standards

Regulatory complexity surrounding plant-based milk nomenclature creates market entry barriers and compliance costs that disproportionately impact smaller coconut milk producers while benefiting established players with regulatory expertise and resources. The European Union's restrictions on dairy terminology usage for plant-based alternatives require careful labeling strategies that avoid consumer confusion while maintaining product appeal, creating ongoing legal and marketing expenses that reduce profitability margins. Food safety standards variations across jurisdictions necessitate multiple production protocols and testing regimens, particularly challenging for coconut milk products that require specific pathogen controls due to their neutral pH and nutrient profiles that can support microbial growth. The FDA's evolving guidance on plant-based milk nutritional labeling requirements creates uncertainty for product development timelines and marketing strategies, as companies must balance regulatory compliance with competitive positioning needs. Organic certification requirements add additional complexity layers, as coconut sourcing must meet diverse national organic standards that may conflict or require separate supply chain management systems for different export markets.

Limited Availability of High-Quality Raw Coconuts in Some Regions

The concentration of supply chains in tropical coconut-producing regions exposes the industry to risks from weather disruptions, political instability, and agricultural disease outbreaks, which can limit global coconut milk production. El Niño weather patterns in 2024 have affected coconut yields in the Philippines, Indonesia, and Sri Lanka, causing raw material price increases that reduce processor margins and restrict market growth in price-sensitive segments. The requirement for premium coconut varieties in milk production creates supply constraints, as food-grade coconut milk needs specific maturity levels, fat content, and flavor profiles from select coconuts. Fresh coconut transportation and preservation challenges restrict processing facility locations and pose quality degradation risks, particularly affecting smaller processors without advanced supply chain management systems. The long-term supply stability faces threats from climate change impacts on coconut palm productivity, with rising sea levels and changing precipitation patterns affecting traditional growing regions, while new cultivation areas require decades to become productive. In 2025, the coconut industry faces limited availability of high-quality raw coconuts in some regions, hindering market growth. Challenges like declining productivity, extreme weather, aging plantations, and poor agronomic practices restrict supply, affecting the industry's capacity to meet rising demand for diverse coconut-based products, thereby limiting expansion potential [3]Source: International Coconut Community, “Coconut,” coconutcommunity.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cream Segment Drives Premium Growth

Coconut milk maintains its dominant position in product type segmentation, capturing 55.88% market share in 2025. This substantial market presence stems from its widespread application in various culinary preparations and strong consumer acceptance as a reliable dairy milk alternative. The versatility of coconut milk in both household and commercial kitchens has established it as an essential ingredient across multiple food categories.

Meanwhile, coconut cream demonstrates remarkable growth potential, advancing at a CAGR of 13.05% through 2031. This growth is primarily driven by its increasing adoption in professional food service environments and its superior functional characteristics in cooking and baking applications. Professional chefs consistently choose coconut cream for its exceptional performance in high-heat cooking, sauce preparation, and dessert making, where standard coconut milk alternatives often fall short. Food manufacturers increasingly incorporate coconut cream into their premium product formulations, particularly in ice cream, chocolate, and confectionery items, where its rich texture and stable emulsification properties significantly enhance the final product quality. The segment's evolution continues with innovative developments, exemplified by companies like Whole Moon, which has introduced whole coconut meat formulations that deliver complete protein profiles while maintaining the premium market positioning that fuels category expansion.

By Category: Organic Segment Captures Health-Conscious Premium

Conventional coconut products hold 65.92% market share in 2025, driven by established supply chains and competitive pricing that enables widespread consumer adoption across economic segments. The organic segment is projected to grow at 16.18% CAGR through 2031, as consumers demonstrate willingness to pay 30-50% premiums for certified organic coconut products that meet health and environmental preferences. This growth pattern highlights a market division between cost-conscious mainstream consumers and premium segment buyers.

The growth in organic coconut milk consumption stems from improved supply chain efficiency, which has enhanced product availability and decreased price differentials compared to conventional options. The segment's expansion is further supported by increased shelf space allocation in mainstream grocery retailers, as consumer demand validates premium positioning beyond traditional natural food stores.

By End Use: Retail Dominance with B2B Innovation Growth

The off-trade segment commands a substantial 61.05% market share in 2025, encompassing a diverse network of retail channels including supermarkets, hypermarkets, convenience stores, and online retailers. This dominant position reflects the successful transformation of coconut milk from a niche ingredient to an essential household item, supported by comprehensive retail expansion strategies and targeted consumer education initiatives. The widespread availability across multiple retail touchpoints has enabled consumers to easily incorporate coconut milk into their daily cooking routines, while retailers have optimized shelf placement and promotional activities to drive both trial purchases and customer retention.

The processed food segment exhibits remarkable growth potential with a projected CAGR of 13.52% through 2031, underscoring the increasing adoption of coconut milk by food manufacturers as a versatile ingredient solution. This growth trajectory is driven by manufacturers' strategic initiatives to reformulate existing product lines, replacing conventional additives and dairy components with coconut-based alternatives. The shift aligns with consumer preferences for recognizable, natural ingredients while maintaining product functionality and performance standards. Within the distribution landscape, traditional supermarkets and hypermarkets maintain their leadership position, while online retail platforms continue to capture increasing market share through innovative offerings such as subscription models and bulk purchase programs designed to serve regular coconut milk consumers.

Geography Analysis

The Asia-Pacific region commands a substantial 54.62% of the global market share in 2025, building on its strong foundation in coconut cultivation and deeply rooted consumption patterns. The region's market leadership is a direct result of its competitive advantages in production costs and well-established supply chain networks, supported by generations of expertise in coconut cultivation and processing.

North America has emerged as the most dynamic market, achieving a remarkable 13.72% CAGR through 2031. This growth is primarily fueled by consumers increasingly embracing plant-based diets and their willingness to invest in premium coconut milk products, creating favorable conditions for manufacturers to maintain healthy profit margins. European markets continue to evolve with stringent requirements for organic and sustainable products, particularly with the implementation of the EU Deforestation Regulation in 2024-2025. Meanwhile, South America shows promising developments despite infrastructure limitations, while the Middle East and Africa represent emerging opportunities driven by urbanization and changing consumer preferences. Recent market activities, including Dehusk's introduction of fortified coconut milk in the Philippines, demonstrate the industry's response to growing regional demand while building export capabilities.

Competitive Landscape

The coconut milk and cream market demonstrates moderate fragmentation, presenting significant opportunities for both established companies seeking market share consolidation and new entrants aiming to grow through differentiation strategies. Major industry players such as Thai Coconut, Vita Coco, and Goya Foods maintain their market positions through vertical integration advantages and well-established distribution networks. In contrast, emerging brands have successfully captured market share by focusing on premium product offerings, obtaining organic certifications, and implementing direct-to-consumer sales channels that circumvent traditional retail barriers.

Strategic partnerships between coconut processors and major food companies continue to reshape the competitive landscape of the industry. A notable example is Century Pacific's expanded agreement with Vita Coco, which includes a substantial USD 40 million investment in production capacity announced in July 2024, aimed at securing long-term supply relationships. The market has evolved beyond traditional competition based on price and distribution, as companies like Nestlé invest in product innovation, developing specialized fruit fat-based formulations that enhance both sensory characteristics and functional performance in plant-based milk applications.

The market presents numerous opportunities in specialized segments, particularly in developing barista-grade coconut milk formulations, creating fortified products that address specific nutritional requirements, and implementing sustainable packaging solutions that balance environmental concerns with product protection. Companies that invest in advanced supply chain traceability systems and sustainable sourcing verification mechanisms are gaining competitive advantages, as both regulatory requirements and consumer preferences increasingly demand greater transparency in ingredient sourcing and production methodologies.

Coconut Milk And Cream Industry Leaders

Thai Coconut Public Co. Ltd.

Theppadungporn Coconut Co., Ltd.

Goya Foods Inc.

Danone S.A.

McCormick & Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Whole Moon launched the first coconut milk made using whole coconut meat without creams or oils, distributed nationwide at Sprouts and select US retailers including ShopRite, Fairway and Central Markets. The innovation delivers complete protein profiles while maintaining premium positioning in the plant-based beverage segment

- November 2024: Dehusk launched as the Philippines' first locally-produced fortified coconut milk, founded by actress Nadine Lustre and entrepreneur Christophe Bariou. The product is enriched with calcium and essential nutrients while emphasizing sustainable local production using abundant Philippine coconuts

- July 2024: Century Pacific Food Inc. announced plans to raise capital expenditures to PHP 4-5 billion in 2024 to fund investments and expand capacity in its coconut business. The company signed an expanded agreement with Vita Coco including a USD 40 million investment in additional capacity to serve both OEM and domestic markets

Global Coconut Milk And Cream Market Report Scope

Coconut milk and cream are ingredients made from the simmering of shredded coconut and water in different ratios. The market studied has been segmented by category, application, and geography. Based on the category, the market is segmented into organic and conventional. Based on the application, the market is segmented into processed food, retail/packaged coconut cream and coconut milk, and food service. The processed food segment is further sub-segmented into the bakery, confectionery, dairy products, frozen desserts, and other processed foods. The report also outlines insights into major countries from all the major regions, including North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done in value (in USD million) terms.

| Coconut Milk |

| Coconut Cream |

| Organic |

| Conventional |

| Processed Food | |

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience and Grocery Stores | |

| Online Retailers | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Coconut Milk | |

| Coconut Cream | ||

| By Category | Organic | |

| Conventional | ||

| By End Use | Processed Food | |

| On-Trade | ||

| Off-Trade | Supermarket/Hypermarket | |

| Convenience and Grocery Stores | ||

| Online Retailers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the coconut milk and cream market in 2026?

The coconut milk and cream market size is valued at USD 5.21 billion in 2026 and is projected to reach USD 9.19 billion by 2031.

What is the growth rate forecast through 2031?

The market is expected to register a 12.02% CAGR between 2026 and 2031, driven by plant-based diet adoption and clean-label demand.

Which region leads global sales?

Asia-Pacific holds the largest share at 54.62% of 2025 revenue thanks to integrated supply chains and traditional consumption.

What segment is growing the fastest?

Coconut cream is forecast to grow at a 13.05% CAGR through 2031 because of premium applications in food-service and confectionery.

How are companies addressing sustainability concerns?

Leading processors are investing in traceable sourcing, fair-trade certification, and satellite monitoring to meet new EU deforestation rules.

Page last updated on: