Market Overview

| Study Period | 2021 - 2031 |

|---|---|

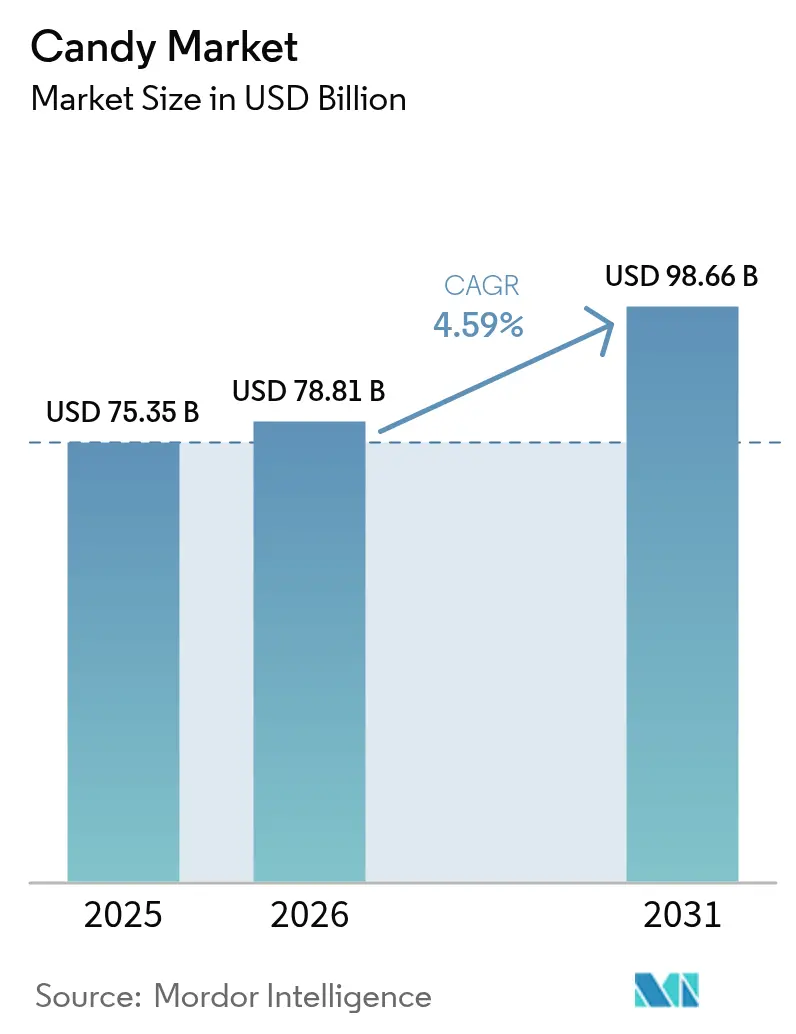

| Market Size (2026) | USD 78.81 Billion |

| Market Size (2031) | USD 98.66 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Candy Market Analysis by Mordor Intelligence

The Candy Market size was valued at USD 75.35 billion in 2025 and estimated to grow from USD 78.81 billion in 2026 to reach USD 98.66 billion by 2031, at a CAGR of 4.59% during the forecast period (2026-2031). Despite inflationary pressure and fast-evolving wellness habits, the candy market preserves demand by anchoring products to cultural rituals, celebratory gifting, and indulgent snacking. Rising premiumization, continuous flavor experimentation, and digital commerce adoption underpin steady value gains, while acute cocoa price swings and tighter sugar-reduction rules influence cost structures. Category resilience also reflects the candy market’s balanced product mix, with chocolate commanding the largest revenue pool and non-chocolate segments absorbing texture-driven innovation waves. Competitive intensity remains moderate as global majors pursue acquisitions and manufacturing upgrades to secure scale benefits and shield margins from raw-material

Key Report Takeaways

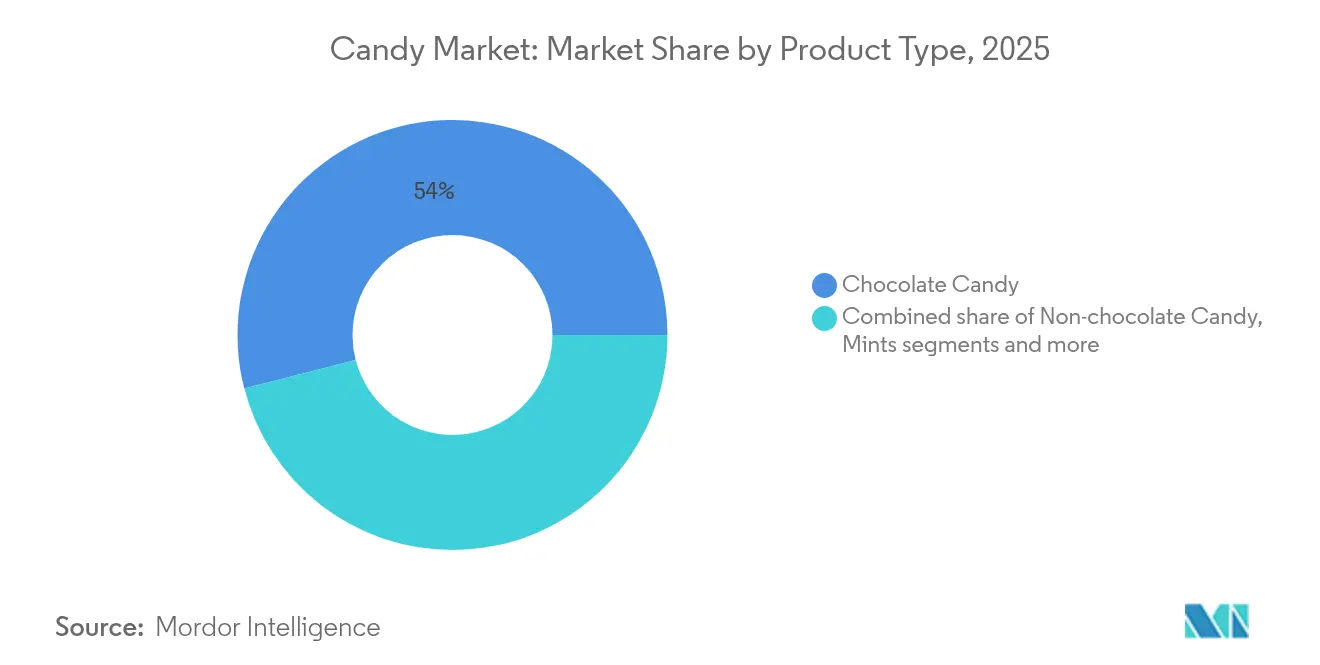

- By product type, chocolate candy led with 54.01% of candy market share in 2025, while pastilles, gums, jellies, and chews are forecast to grow at an 8.30% CAGR to 2031.

- By ingredient, sugar-based candies accounted for 79.15% of candy market share in 2025; sugar-free formats are projected to scale at a 7.12% CAGR by 2031.

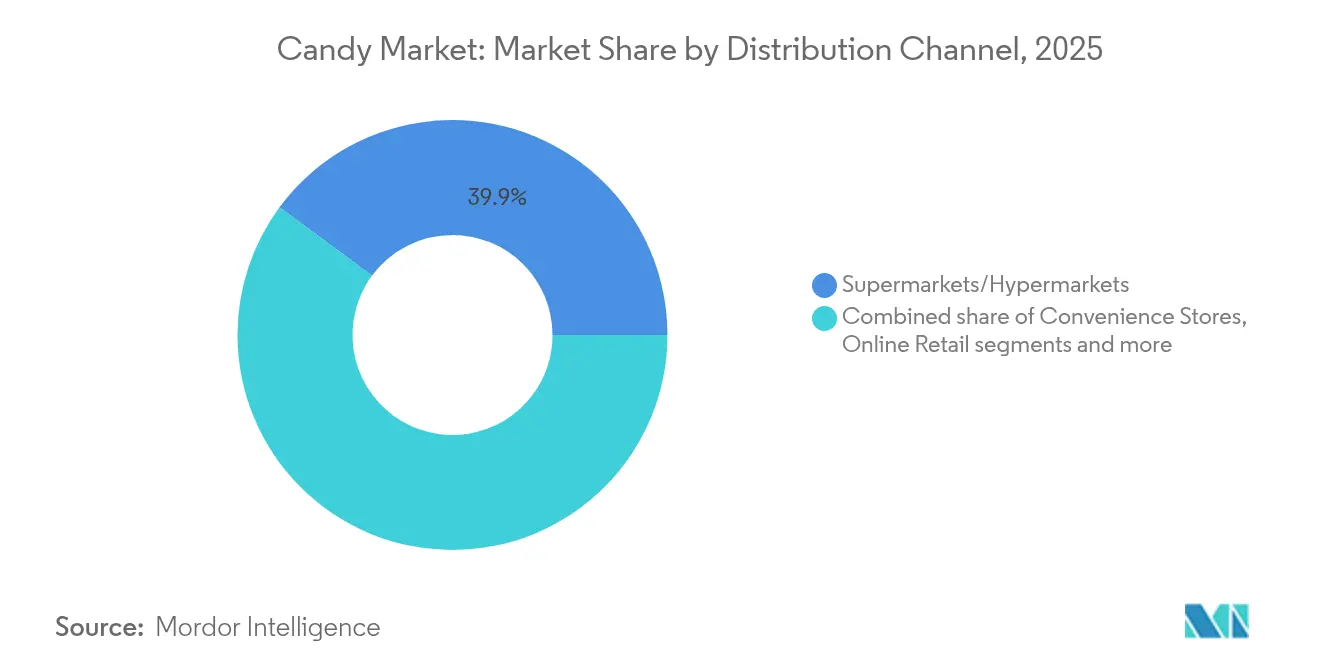

- By distribution channel, supermarkets and hypermarkets held 39.88% of the candy market size in 2025, whereas online retail is expanding at a 6.58% CAGR through 2031.

- By category, mass offerings represented 72.10% of candy market size in 2025; premium offerings are advancing at a 6.32% CAGR through 2031.

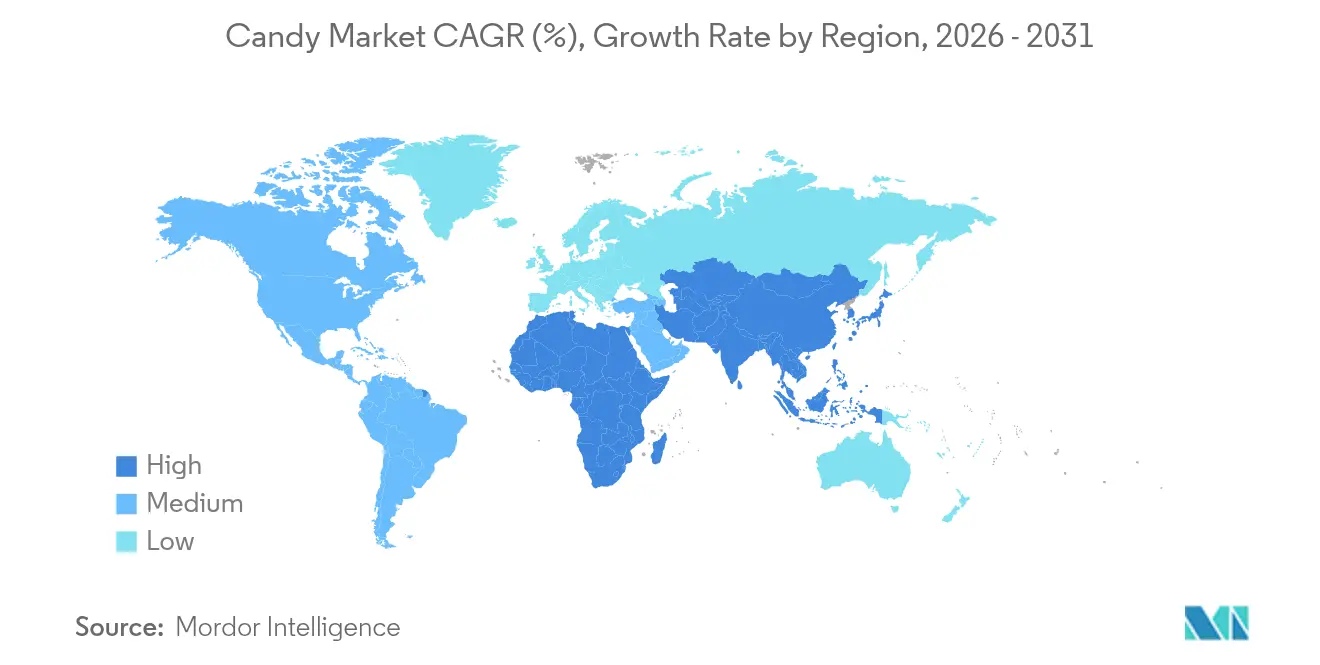

- By geography, North America accounted for 35.92% of candy market size in 2025; Asia-Pacific is projected to grow at a CAGR of 7.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Candy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium and artisanal candy demand surge | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of organized retail and e-commerce | +0.9% | Global, with strongest growth in Asia-Pacific and South America | Short term (≤ 2 years) |

| Continuous flavour and texture innovation | +0.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing gifting culture and seasonal spikes | +0.7% | Global, particularly strong in Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Functional / nutraceutical candy launches | +0.5% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| AI-driven micro-batch manufacturing adoption | +0.3% | Global, concentrated in developed markets initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium and artisanal candy demand surge

The candy market is witnessing a significant boost due to the rising demand for premium and artisanal candies. Consumers are increasingly seeking high-quality, unique, and handcrafted confectionery products that offer superior taste and innovative flavors. This trend is driven by a growing preference for indulgent experiences and the willingness to pay a premium for products perceived as luxurious or exclusive. Additionally, the emphasis on natural and organic ingredients in artisanal candies aligns with the evolving consumer focus on health and wellness. Artisanal candies often feature clean labels, free from artificial additives, which further attract health-conscious consumers. The premium and artisanal candy segment is also benefiting from the growing trend of gifting premium confectionery items during festive seasons, celebrations, and special occasions, as these products are often seen as thoughtful and sophisticated gifts. Furthermore, the expansion of e-commerce platforms and direct-to-consumer channels has enabled manufacturers to reach a broader audience, including niche markets, while offering personalized and customizable options.

Expansion of organized retail and e-commerce

The rapid expansion of organized retail and e-commerce is a significant driver of the global candy market. Organized retail chains provide consumers with easy access to a wide variety of candy products, while e-commerce platforms offer the convenience of purchasing these products online. The growth of these channels is further fueled by impulse buying, facilitated by social media integration, subscription box services, and personalized recommendation algorithms that increase basket sizes. Additionally, the expansion of organized retail in emerging markets, particularly in the Asia-Pacific region, is creating a robust distribution infrastructure that supports the penetration of both domestic and international brands. Modern trade formats in these regions also provide temperature-controlled environments, which are essential for preserving chocolate in tropical climates. This dual-channel growth is enhancing product availability and accessibility, thereby fueling market demand.

Continuous flavour and texture innovation

Ongoing innovations in flavor and texture are driving the growth of the global candy market. Manufacturers are continuously experimenting with new flavor combinations and textures to cater to evolving consumer preferences. This trend is particularly evident in the premium and gourmet candy segments, where unique and exotic flavors, along with innovative textures, are gaining popularity. Additionally, advancements in food technology are enabling companies to create candies with enhanced sensory experiences, further boosting consumer interest and market demand. According to the National Confectioners Association, 98% of shoppers in the United States reported purchasing confectionery products at some point in 2024 [1]Source: National Confectioners Association, "NCA: Candy Dollar Sales Up, Unit Sales Decline in 2024", candyusa.com. This statistic highlights that consumers continue to allocate a portion of their budgets for treats like chocolate and candy, which are often associated with enhancing special moments. Such consumer behavior underscores the importance of continuous innovation in flavor and texture to maintain engagement and drive sales in the candy market.

Growing gifting culture and seasonal spikes

Seasonal spikes play a significant role in driving the growth of gifting culture. Gifting behaviors have evolved beyond traditional holidays to include emerging celebrations like "Summerween," which are driven by Gen Z social media trends. These trends create additional sales opportunities throughout the year by encouraging consumers to participate in non-traditional gifting occasions. Asia-Pacific markets, in particular, showcase a strong adoption of gifting culture, where chocolate is increasingly positioned as a premium gift item. This trend supports higher price points and contributes to market expansion, especially in regions with historically lower per-capita consumption. According to the National Confectioners Association, the big four candy seasons (Valentine’s Day, Easter, Halloween, and the winter holidays) accounted for 62% of all confectionery sales in 2024 in the United States, highlighting the significant role of seasonal gifting in driving market growth [2]Source: National Confectioners Association, "NCA: Candy Dollar Sales Up, Unit Sales Decline in 2024", candyusa.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and sugar reduction | -0.6% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Volatile cocoa and sugar commodity prices | -1.2% | Global, most severe impact on chocolate segments | Short term (≤ 2 years) |

| Stricter single-use plastic-waste regulation | -0.3% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Climate-linked cocoa yield variability | -0.8% | Global supply impact, West Africa production zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and sugar reduction

Health-conscious consumers push for reduced sugar intake, which acts as a significant restraint in the candy market. With increasing awareness of the adverse effects of excessive sugar consumption, consumers are shifting toward healthier alternatives. According to the International Diabetes Federation (IDF), approximately 589 million adults (20-79 years) were living with diabetes in 2024, and this number is projected to rise to 853 million by 2050 [3]Source: International Diabetes Federation, "Diabetes around the world in 2024", idf.org . This alarming increase in diabetes cases highlights the growing need for sugar-free or low-sugar products, as individuals with diabetes and those at risk are actively avoiding high-sugar foods, including traditional candies. Additionally, governments and health organizations worldwide are implementing stricter regulations and campaigns to reduce sugar consumption, further pressuring candy manufacturers to adapt. These factors collectively compel candy producers to invest in research and development to create healthier alternatives, such as candies made with natural sweeteners or sugar substitutes.

Volatile cocoa and sugar commodity prices

Volatile cocoa and sugar prices act as a significant restraint in the global candy market. The frequent fluctuations in the prices of these key raw materials directly impact production costs, leading to challenges for manufacturers in maintaining consistent pricing and profit margins. Such volatility is often driven by factors like unpredictable weather conditions, geopolitical tensions, currency fluctuations, and supply chain disruptions, which affect the availability and cost of these commodities. For instance, adverse weather conditions in cocoa-producing regions can lead to reduced yields, driving up prices. Similarly, geopolitical tensions or trade restrictions can disrupt the supply chain, further exacerbating price instability. As a result, manufacturers face difficulties in long-term planning, budgeting, and maintaining product affordability, which can ultimately hinder market growth. Additionally, the rising demand for sustainable and ethically sourced cocoa and sugar adds further pressure on manufacturers to manage costs effectively while adhering to consumer expectations and regulatory requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chocolate Candy Dominates While Pastilles, Gums, Jellies and Chews Surge

In 2025, chocolate candy dominates the candy market with a substantial 54.01% share. This dominance highlights its established consumer preference, driven by its rich taste, variety, and cultural significance across global markets. The segment benefits from strong brand loyalty, frequent product innovations, and seasonal demand spikes during holidays and celebrations. Additionally, the increasing availability of premium and artisanal chocolate options has further solidified its position in the market. Manufacturers are also focusing on health-conscious consumers by introducing low-sugar, organic, and vegan chocolate variants, which are gaining traction.

On the other hand, the pastilles, gums, jellies, and chews segment is projected to grow at a robust 8.30% CAGR through 2031. This growth is primarily attributed to advancements in texture innovation, which enhance the sensory experience for consumers. Social media trends also play a pivotal role in driving demand, as visually appealing and unique products gain popularity among younger demographics. The segment's versatility in flavors and formats, coupled with its appeal as a fun and convenient snack option, continues to attract a diverse consumer base globally. Additionally, the increasing focus on functional candies, such as those infused with vitamins or other health benefits, is expanding the segment's reach.

By Ingredient Type: Sugar-based Candies Leads, Sugar-free Gains Momentum

In 2025, sugar-based candies dominate the candy market with a substantial 79.15% share. This dominance can be attributed to their widespread consumer appeal, affordability, and extensive product variety. Sugar-based candies continue to attract a broad demographic, ranging from children to adults, due to their traditional flavors, textures, and nostalgic value. Additionally, the strong presence of established brands and their consistent innovation in flavors and packaging further bolster the segment's market position. Despite growing health concerns, sugar-based candies remain a staple in the confectionery industry, particularly in emerging markets where regulatory pressures are less stringent.

Conversely, sugar-free and reduced-sugar alternatives are gaining significant traction, recording a notable CAGR of 7.12% through 2031. This growth reflects a shift in consumer preferences driven by increasing health awareness and the rising prevalence of lifestyle-related diseases such as diabetes and obesity. Regulatory pressures in developed markets, including stricter labeling requirements and sugar reduction initiatives, are also propelling the demand for these alternatives. Manufacturers are responding by introducing innovative products that use natural sweeteners, such as stevia and monk fruit, to cater to health-conscious consumers without compromising on taste. This segment is expected to witness sustained growth as consumers prioritize healthier options and governments continue to enforce sugar reduction policies globally.

By Category: Premium Segment Outpaces Mass Market

In 2025, mass market products dominate the candy market with a substantial 72.10% share. These products primarily cater to price-sensitive consumers who prioritize affordability and accessibility. Mass market candies are designed for everyday consumption, making them a popular choice for a wide range of consumers, including children, families, and individuals seeking quick, affordable treats. Their availability across various retail channels, such as supermarkets, convenience stores, vending machines, and online platforms, further strengthens their market presence. Manufacturers in this segment focus on cost-effective production methods, leveraging economies of scale to offer competitive pricing while maintaining consistent quality. Additionally, mass market candies often feature familiar flavors and recognizable branding, which resonate with consumers seeking comfort and nostalgia.

On the other hand, premium candy offerings are experiencing significant growth, projected to expand at a 6.32% CAGR through 2031. This growth is driven by a rising consumer preference for artisanal quality, unique flavor profiles, and a more indulgent experience. Premium candies often use high-quality ingredients, such as organic, fair-trade, or sustainably sourced components, which appeal to health-conscious and ethically minded consumers. These products are frequently handcrafted or produced in small batches, emphasizing exclusivity and attention to detail. Premium candies also stand out through innovative packaging designs, which enhance their appeal as luxury items or gifting options. The segment targets niche markets, including consumers seeking indulgence, special occasions, or gourmet experiences.

By Distribution Channel: Supermarkets/Hypermarkets Dominates While Digital Disruption Accelerates

In 2025, supermarkets and hypermarkets hold a dominant 39.88% share of the candy market. This significant market presence is attributed to their ability to leverage impulse purchase behavior effectively. By strategically placing candy products near checkout counters and high-traffic areas, these retail formats encourage unplanned purchases, which are a key driver of candy sales. Additionally, their broad consumer reach, supported by extensive physical store networks, ensures accessibility to a wide demographic, including urban, suburban, and rural consumers. Supermarkets and hypermarkets also benefit from offering a diverse range of candy products, catering to varying consumer preferences, dietary needs, and price points, which further solidifies their position in the market.

Online retail, on the other hand, is projected to grow at a CAGR of 6.58% through 2031, driven by evolving consumer shopping habits and technological advancements. The integration of social media platforms into online retail strategies has played a pivotal role in this growth, enabling targeted marketing, influencer collaborations, and personalized product recommendations that resonate with specific consumer segments. Subscription service models have also gained traction, offering consumers convenience, cost savings, and regular delivery of their favorite candy products, which fosters customer loyalty. Furthermore, the increasing adoption of e-commerce platforms, coupled with the rising preference for home delivery, has expanded the reach of online retail, making it a key growth driver in the candy market.

Geography Analysis

In 2025, North America holds a 35.92% share of the candy market, driven by established consumption patterns, a robust distribution network, and strong seasonal gifting traditions that boost premium pricing during major holidays. The region benefits from a well-developed retail infrastructure, which supports the availability of a wide range of candy products, catering to both mass-market and premium consumers. Additionally, high per-capita consumption rates and a preference for innovative product offerings further solidify North America's position as a key player in the global candy market. The mature nature of the market allows companies to implement sophisticated marketing strategies and leverage consumer loyalty effectively.

Europe represents a significant segment of the candy market, underpinned by its premium chocolate traditions, artisanal production heritage, and increasingly stringent sustainability regulations shaping industry practices. Diverse consumer preferences across countries create opportunities for localized product development and flavor innovation. EU packaging regulations further drive sustainable packaging adoption, influencing global industry standards. Major markets such as Germany, the United Kingdom, France, and Italy exhibit distinct consumption patterns and regulatory requirements, while Eastern Europe shows growth potential due to rising disposable incomes and the spread of Western consumption trends.

Asia-Pacific emerges as the fastest-growing region in the candy market, with a projected CAGR of 7.06% through 2031. Urbanization, rising middle-class incomes, and increasing market penetration in countries with historically low per-capita candy consumption drive this growth. China leads the region with double-digit growth in candy consumption, attracting significant investments from multinational companies in production and distribution. India, Japan, Australia, and Southeast Asia present unique opportunities and challenges, ranging from regulatory compliance to cultural preferences influencing product formulation and marketing strategies. South America, Middle East, and Africa represent emerging markets with significant long-term potential despite current smaller market shares, benefiting from economic development, population growth, and increasing exposure to global confectionery brands through improved distribution networks and digital connectivity.

Competitive Landscape

The candy market operates within a moderately consolidated competitive landscape, where established multinational players such as Mars, Mondelez, Hershey, and Ferrero hold significant market shares. These companies maintain their dominance through extensive brand portfolio management, continuous innovation, and strategic acquisitions. Such strategies enable these players to diversify their product categories and enhance their geographic reach, ensuring sustained growth in a competitive environment.

Regional players and artisanal producers also play a crucial role in shaping the market dynamics. These companies leverage their specialized positioning and deep understanding of local consumer preferences to capture market share. For example, artisanal chocolate makers in Europe focus on premium, handcrafted products that appeal to niche markets, while regional brands in Asia cater to unique flavor profiles preferred by local consumers. This localized approach allows smaller players to compete effectively against global giants, particularly in markets where cultural preferences heavily influence purchasing decisions.

Competition in the candy market is further intensified by vertical integration strategies adopted by leading companies. To mitigate supply chain risks and manage cost volatility, firms are increasingly investing in cocoa sourcing and processing capabilities. For example, Hershey has implemented sustainable cocoa sourcing programs to secure a stable supply of raw materials while addressing ethical concerns. Similarly, Ferrero has invested in its own cocoa processing facilities to reduce dependency on third-party suppliers. These initiatives not only strengthen supply chain resilience but also provide a competitive edge in terms of cost efficiency and product quality, further shaping the industry's competitive dynamics.

Candy Industry Leaders

-

The Hershey Company

-

Mondelez International, Inc.

-

Mars, Incorporated

-

Nestlé SA

-

Ferrero International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ukrainian confectionery brand Vitamin Candy by Alex-IS has partnered with The Smurfs to offer healthier snacking options for children globally. Facilitated by Art Nation Licensing, the collaboration has resulted in sugar-free fruit pastilles featuring nutritious ingredients and playful packaging. The product line includes three fruit combinations—pomegranate and apple, white grape and apple, and cherry and apple—each showcasing popular Smurf characters and providing natural sweetness without artificial additives.

- May 2025: Ferrera's SweeTarts has unveiled its latest creation: SweeTarts Gummy Halos. These Gummy Halos boast a light, fluffy gummy base, crowned with a chewy pink and blue layer, and are enveloped in a delightful mix of sweet and tart flavors. The new offering introduces two tantalizing flavor pairings to the SweeTARTS lineup: Blue Punch and Strawberries & Cream.

- April 2025: Disneyland® Paris and Mars Wrigley bolster their collaboration, introducing a vibrant gourmet experience for visitors at the Boardwalk Candy Palace. Initiated in 2023, the alliance has successfully integrated Mars Wrigley's renowned brands, including M&M’S®, Skittles®, Twix®, Snickers®, and Maltesers®, into the majority of the park's retail outlets.

- May 2024: Ferrero International SpA launched Tic Tac Chewy, a new addition to its iconic Tic Tac brand, blending the brand's signature freshness with a chewy texture. Tic Tac Chewy came in two enticing varieties: Fruit Adventure and Sour Adventure. Each variety boasted a delightful medley of five fruity flavors: Cherry, Apple, Orange, Lemon, and Grape.

Global Candy Market Report Scope

Candy, often known as sweets or lollies, is a sweet confection made primarily of sugar. Any sweet confection including chocolate, chewing gum, and sugar candy, falls under the genre of sugar confectionery. The global candy market is segmented by Type, Distribution Channel, and Geography. Based on type, the candy market is segmented into Chocolate candy and Non-chocolate candy. The Non-chocolate candy segment is further segmented into Hard-boiled Candies, Pastilles, Gums, Jellies, Chews, Toffees, Caramels, Nougat, Mints, and other Non-Chocolate Candies. The other types of Non-chocolate candies include Licorice, Lollipops, and Medicated confectionery. Based on Distribution Channels, the market is segmented into Supermarkets/Hypermarkets, Convenience stores, Specialist Retailers, Online retail, and Other Distribution channels. To provide a broader perspective, the market is studied for potential and promising countries across different regions including North America, Europe, Asia-Pacific, South America, Middle-East, and Africa. For each Segment, the market sizing and forecasts are carried out based on value (in USD millions).

By Product Type

| Chocolate Candy |

| Non-chocolate Candy |

| Hard-boiled Candies |

| Pastilles, Gums, Jellies and Chews |

| Toffees, Caramels and Nougat |

| Mints |

| Other Non-chocolate Candies |

By Ingredient Type

| Sugar-based Candies |

| Sugar-free / Reduced-sugar Candies |

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Specialist Retailers |

| Online Retail |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Chocolate Candy | |

| Non-chocolate Candy | ||

| Hard-boiled Candies | ||

| Pastilles, Gums, Jellies and Chews | ||

| Toffees, Caramels and Nougat | ||

| Mints | ||

| Other Non-chocolate Candies | ||

| By Ingredient Type | Sugar-based Candies | |

| Sugar-free / Reduced-sugar Candies | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the candy market by 2031?

The candy market is forecast to reach USD 98.66 billion by 2031, reflecting a 4.59% CAGR from 2026.

Which product group is growing fastest within the category?

Pastilles, gums, jellies, and chews lead growth at an 8.30% CAGR through 2031.

How large is the online channel’s contribution to confectionery sales?

While supermarkets hold 39.88% of revenue, online retail is expanding fastest, registering a 6.58% CAGR to 2031.

What factors are fueling Asia-Pacific demand?

Urbanization, middle-class income gains, and modern grocery expansion are driving a 7.06% CAGR for regional candy sales.

Page last updated on: