Europe Bamboo Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

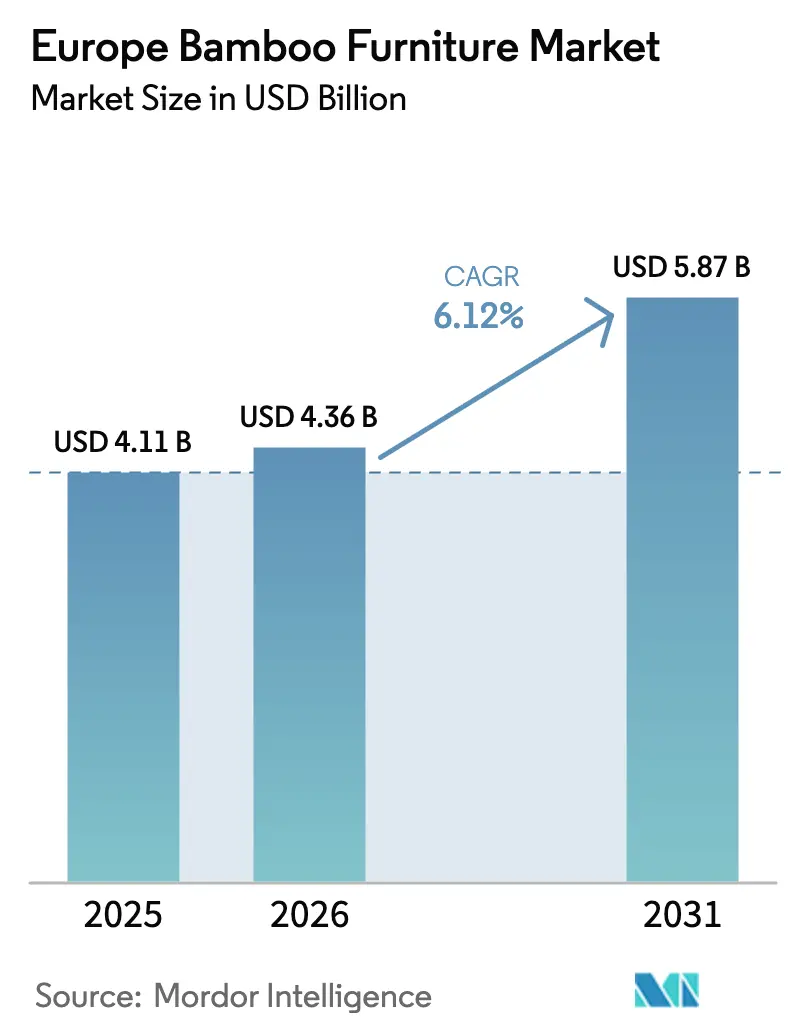

| Base Year Market Size (2025) | USD 4.11 Billion |

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 5.87 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

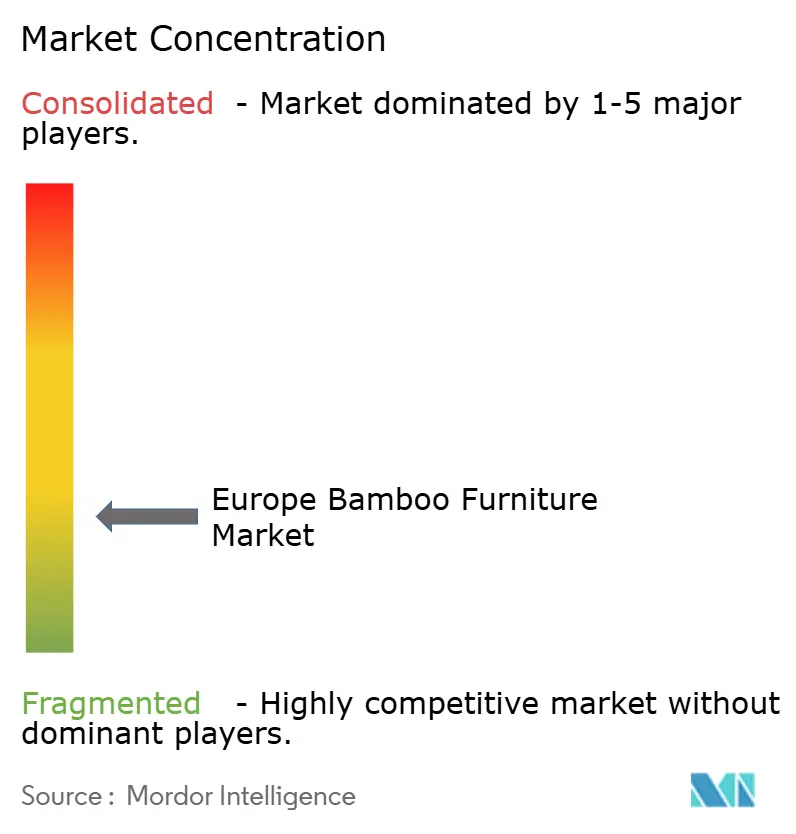

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bamboo Furniture Market Analysis by Mordor Intelligence

The Europe bamboo furniture market size was valued at USD 4.11 billion in 2025 and estimated to grow from USD 4.36 billion in 2026 to reach USD 5.87 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). Regulatory pressure from EU green procurement rules, corporate net-zero commitments, and the region’s strong design heritage jointly propel demand. Vertically integrated suppliers benefit from lower freight risk and better certification control, while smaller importers face margin pressure from shipping volatility. Institutional procurement now values bamboo’s rapid carbon sequestration and low embodied energy, helping the material displace tropical hardwoods in commercial interiors. Spain’s construction rebound, the United Kingdom’s post-Brexit sourcing agility, and the BENELUX focus on circularity all reinforce a positive growth trajectory for the Europe bamboo furniture market.

Key Report Takeaways

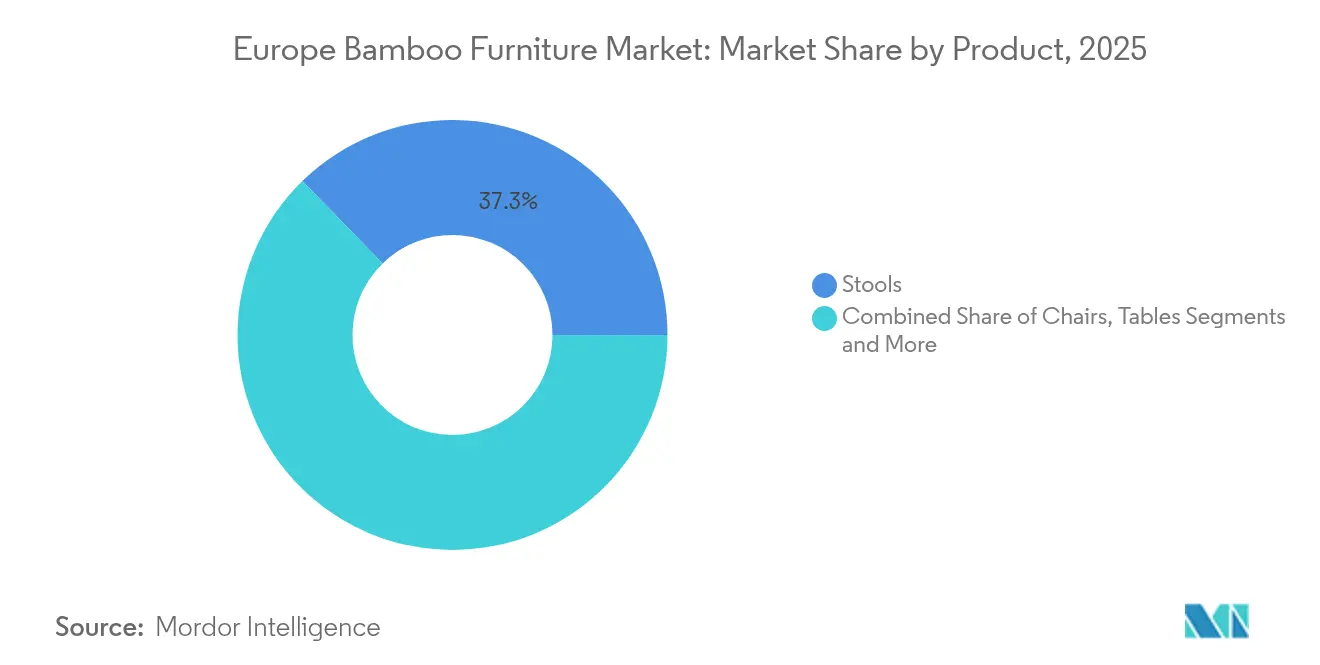

- By product, stools led with 37.30% revenue share in 2025; chairs are advancing at a 7.22% CAGR to 2031.

- By category, indoor furniture accounted for 64.20% share of the Europe bamboo furniture market size in 2025, and outdoor furniture is growing at a 6.95% CAGR to 2031.

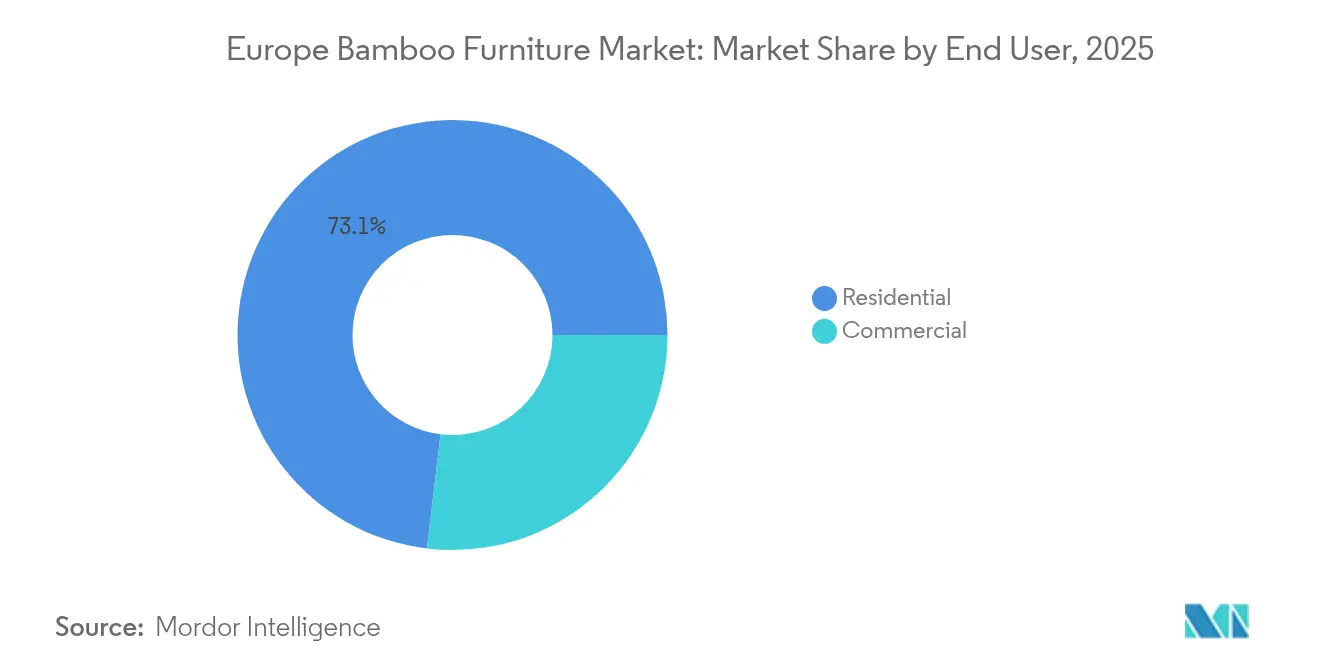

- By end user, residential accounted for 73.10% share of the Europe bamboo furniture market size in 2025, and commercial is growing at a 6.85% CAGR to 2031.

- By distribution channel, B2C retail held 79.10% of the Europe bamboo furniture market share in 2025, whereas online retail records the fastest 7.62% CAGR through 2031.

- By geography, the United Kingdom commanded 24.60% revenue share in 2025, while Spain is projected to expand at a 6.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Bamboo Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory EU Green Public Procurement Criteria Prioritising Bio-based Furniture | +1.2% | EU-wide, strongest in Germany and the Netherlands | Medium term (2-4 years) |

| Expansion of FSC/PEFC-Certified Bamboo Forest Acreage Feeding European Supply Chains | +0.8% | Global supply, EU demand concentration | Long term (≥ 4 years) |

| Continental Growth of Cross-Border E-Commerce Platforms Enhancing Access to Bamboo Furniture | +1.1% | EU-wide, particularly NORDICS and BENELUX | Short term (≤ 2 years) |

| Corporate Sustainability Targets Accelerating Replacement of High-Embodied-Carbon Hardwoods | +0.9% | Western Europe's core markets | Medium term (2-4 years) |

| Advances in Thermo-Modified & Laminated Bamboo Enabling Region-Wide Adoption | +0.7% | Manufacturing hubs in Germany and Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory EU Green Public Procurement Criteria Prioritizing Bio-based Furniture Across the Region

EU Regulation 2024/1781 places furniture among priority categories for mandatory green procurement, introducing a digital product passport that rewards bamboo’s traceable carbon benefits over hardwood alternatives [1]European Commission, “Regulation 2024/1781 establishing ecodesign requirements for sustainable products,” eur-lex.europa.eu. European Office Furniture Federation (FEMB) Level certification now carries preferential scoring in public tenders, turning ministries, universities, and city councils into anchor buyers for the Europe bamboo furniture market. Stable institutional demand has encouraged manufacturers to add capacity, automate finishing lines, and lock in certified-culm supply contracts. Because public buyers apply life-cycle costing, bamboo’s fast growth cycle beats oak or beech on total environmental cost, reinforcing its acceptance in large-scale furniture replacement programs.

Expansion of FSC/PEFC-Certified Bamboo Forest Acreage Feeding European Supply Chains

Forest Stewardship Council’s third transaction-verification loop exposed fraudulent claims and removed several Chinese suppliers, prompting European buyers to pivot toward certified plantations in Vietnam, Indonesia, and Malaysia[2]Forest Stewardship Council, “Transaction Verification Update 2025,” fsc.org. New acreage has come online specifically to serve furniture-grade demand, offering greater culm diameter consistency and reducing quality-rejection rates in European factories. Although premiums for verified culms add 3-4% to raw-material cost, the assurance supports price stability and underpins long-term contracts. The Europe bamboo furniture industry, therefore, gains resilience against future supply shocks while strengthening its sustainability narrative.

Continental Growth of Cross-Border E-Commerce Platforms Enhancing Access to Bamboo Furniture

Cross-border marketplaces now list thousands of certified bamboo SKUs, allowing small Danish or Belgian consumers to order stools or benches directly from Polish or Portuguese assemblers. With many logistics providers offering carbon-neutral shipping options, online orders align with consumer ethics, fueling omnichannel sales momentum throughout the Europe bamboo furniture market. Online retail platforms now provide durability information and care instructions for bamboo furniture. With a virtual storefront, small producers can reach customers across Europe without paying for brick-and-mortar shops, which raises the stakes for the larger brands. Search filters that push eco-friendly items to the top also put bamboo pieces in front of shoppers who want their homes to mirror their environmental values. Importantly, direct-to-consumer pathways lift margins for mid-sized manufacturers who previously relied on retailers and can now reinvest in R&D.

Corporate Sustainability Targets: Accelerating Replacement of High-Embodied-Carbon Hardwoods

Europe’s directive on corporate sustainability reporting legislation obliges large companies to disclose Scope 3 emissions, bringing office furniture into the decarbonization spotlight. Multinationals such as Stora Enso have pledged 50% CO₂ cuts by 2030 and now request bamboo desks, task chairs, and acoustic panels for new headquarters projects. Designers select bamboo to secure LEED (Leadership in Energy and Environmental Design) or BREEAM (Building Research Establishment Environmental Assessment Method) credits, which raise asset value and tenant appeal. This B2B pull effect expands average order sizes and introduces repeat-purchase cycles that stabilize revenue for the Europe bamboo furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Asian Bamboo Culms Causing Logistics-Cost Volatility for European Importers | -1.4% | EU-wide, particularly affecting smaller importers | Short term (≤ 2 years) |

| EU REACH & Low-VOC Compliance Raising Finishing Costs Versus Conventional Hardwoods | -0.9% | EU-wide regulatory compliance | Medium term (2-4 years) |

| Consumer Durability Perception Challenges in Temperate and Humid Northern European Climates | -0.6% | NORDICS, Northern Germany, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dependence on Asian Bamboo Culms Causing Logistics-Cost Volatility for European Importers

UN Trade and Development (UNCTAD) data show Red Sea disruptions pushed container rates 120% higher between October 2023 and June 2024, and costs for smaller importers of bamboo culms could not be hedged [3]UN Conference on Trade and Development, “Global Container Shipping Outlook 2024,” unctad.org . As the Europe bamboo furniture market still sources most culms from Guangxi and Zhejiang, firms with limited scale saw EBITDA margins compress by up to 250 basis points in 2024. Tariffs on finished bamboo furniture entering Italy (5.6%) add an extra burden. To mitigate, integrated players signed multi-year contracts with Southeast Asian plantations and diversified ports of entry, improving supply security yet raising capital requirements for new entrants.

EU REACH & Low-VOC Compliance Raising Finishing Costs Versus Conventional Hardwoods

The formaldehyde limit of 0.062 mg/m³ taking effect in August 2026 forces producers to switch to water-borne or UV-cured lacquers, costing 15-20% more per square meter. Smaller workshops without automated spray lines must outsource finishing, elongating lead times within the Europe bamboo furniture market. The REACH Candidate List expansion to 247 SVHCs adds testing charges every time lacquer formulations change. Because bamboo’s higher porosity absorbs more sealer than oak, compliance expenses are proportionally greater and can price bamboo out of budget segments unless producers drive further process innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Stools Drive Volume While Chairs & Tables Capture Growth

Stools dominate with a 37.30% revenue share, reflecting slim component counts, lower off-cuts, and fast assembly cycles. They fill kitchen-island, bar, and café use cases that require compact seating solutions. The Europe bamboo furniture market size for stools benefits from standardized parts that ship flat-pack, reducing freight cost per unit. By contrast, Chairs post a 7.22% CAGR to 2031 as businesses refurbish meeting rooms and co-working spaces to reflect ESG values. Their higher average selling price justifies investment in CNC-laminated blanks and multi-axis finishing robots. Beds and storage units see moderate take-up as consumers prioritize healthy sleep environments; sofas lag because climate-induced durability concerns persist in damp locales.

A secondary wave of accessory‐led demand appears in shelving, organizer cubes, and plant stands, each leveraging bamboo’s antimicrobial properties that appeal to health-conscious metropolitan buyers. Manufacturers that pre-finish boards with low-VOC stains and include digital product passports position these items for quick-click re-order through online channels across the Europe bamboo furniture market.

By Category: Indoor Dominance Reflects Climate Constraints

Indoor furniture commands 64.20% of 2025 sales. Controlled home and office interiors shield bamboo from freeze–thaw cycles, UV degradation, and seasonal humidity swings. As a result, warranty claims on indoor bamboo pieces sit below those for outdoor counterparts, reinforcing consumer confidence. The European bamboo furniture market share for outdoor products remains small because extra treatments—silicate impregnation, nano-coating—raise retail prices, yet still cannot guarantee multi-year colour stability in Nordic climates. Nonetheless, research into bamboo-scrimber decking and thermally modified lounge chairs suggests a nascent opportunity once performance hurdles ease.

Lab tests show that different bamboo composites behave differently when they get damp, and Bamboo Scrimber keeps its shape better than most alternatives. Because homes and offices stay at steady temperatures and humidity, indoor pieces can play to bamboo’s strengths without the weather-related headaches that come with outdoor use. Many shoppers still do not know how bamboo handles moisture or how to care for it, which leaves room for brands that teach customers and design products for Europe’s varied climate. Demand also benefits from the rise of compact city living, where people look for space-saving, eco-friendly furniture.

By End User: Residential Foundation Supports Commercial Acceleration

Residential consumers supplied 73.10% of the 2025 demand. Purchases are driven by lifestyle alignment: buyers prioritize renewable materials, safe finishes, and minimalist style. Online reviews frequently note bamboo’s warm hue and easy assembly, indicating top-of-funnel influence from social media design content. Still, the Commercial segment’s 6.85% CAGR through 2031 transforms procurement dynamics. Certified bamboo systems furniture now qualifies for points under LEED v4’s Low-Emitting Materials credit, leading architects to specify desks and storage made from laminated bamboo panels. Corporate buyers further leverage bamboo furnishings to communicate a climate-positive identity to employees and visitors, accelerating institutional share gains in the Europe bamboo furniture market.

Hospitality groups experiment with bamboo headboards and lounge seating to improve indoor air quality scores on booking platforms that rank accommodation sustainability. Universities adopt bamboo study pods to meet net-zero campus plans. All these projects generate repeat, bulk orders that smooth revenue seasonality previously tied to consumer holidays.

By Distribution Channel: Online Growth Challenges Retail Tradition

Offline Retail still accounts for 79.10% of sales because furniture remains a tactile category. Shoppers test sturdiness, inspect joint quality, and visualize scale before committing. Store associates demonstrate care routines—oil reapplication, tightening of dowels—thereby alleviating durability doubts. However, Online Retail expands at an 7.62% CAGR as augmented-reality apps allow scale visualization at home and as return policies liberalize. The Europe bamboo furniture market's tradition weekend showroom visits now blend with weeknight tablet browsing, creating a hybrid path to purchase.

Specialty furniture chains in Germany and France add RFID-enabled labels that link to digital passports with forest-of-origin data. Meanwhile, B2B project portals integrate with corporate carbon-accounting tools, letting facility managers instantly see how swapping mahogany desks for bamboo variants trims Scope 3 tonnage. These innovations tilt momentum toward web-first ordering even for high-ticket conference tables.

Geography Analysis

The United Kingdom holds a 24.60% revenue share thanks to the early adoption of sustainable interiors and streamlined import procedures after Brexit. Customs agreements favour direct sourcing from Southeast Asia without EU re-routing, shaving lead times by 7 days on average. London’s commercial real-estate boom further sustains large orders of bamboo desks and break-out furniture during refurbishments.

Germany and France together form the next revenue tier. Germany’s engineering culture demands explicit fire, compression, and emissions certificates, compelling suppliers to exceed EN 17214 performance thresholds. French buyers gravitate to bamboo’s low-carbon image, consistent with the country’s RE 2025 building code. The Benelux cluster serves as a logistics gateway; Rotterdam and Antwerp ports process multimodal bamboo container flows bound for inland assembly hubs, reinforcing their strategic role within the Europe bamboo furniture market. Spain, posting a 6.62% CAGR, benefits from tourism-driven hospitality upgrades. Hotel groups in Barcelona and Madrid adopt bamboo lounge seating to secure Biosphere Responsible Tourism certification. Italy’s design legacy encourages midrange makers in Treviso and Brianza to pair bamboo frames with recycled-textile cushions, carving a boutique niche. Nordic nations appreciate bamboo’s light visual weight, aligning with hygge aesthetics, though exterior-grade sales remain capped by freeze–thaw durability worries. Overall, national demand profiles differ, yet pan-European e-commerce flattens accessibility, letting suppliers scale beyond home markets.

Competitive Landscape

Europe’s bamboo furniture scene is moderately fragmented. The fiercest rivalry shows up in retail, not in the factory, because making high-quality bamboo pieces takes specialized skills and complex supply chains—advantages that established, fully integrated brands already hold. Big retailers keep buying smaller niche distributors to secure shoppers who want planet-friendly furniture.

Winning companies focus on vertical integration. They form direct ties with certified bamboo growers so they can guarantee consistent quality, follow regulations and buffer themselves against swings in freight and raw-material costs.

There is still room for growth in heavy-duty bamboo furniture built for Europe’s varied climate and for workplaces that see hard, everyday use—needs many current products do not yet meet. Makers are turning to advanced techniques such as thermal treatment and engineered composites to close that gap while keeping bamboo’s eco-benefits intact. Recent FSC checks that exposed false certification claims among some Chinese suppliers show how staying fully compliant can become a competitive edge. At the same time, new players are skipping traditional stores by selling online or direct to consumers. Their detailed sustainability disclosures speak to buyers who value transparency and want proof their purchases are genuinely green.

Europe Bamboo Furniture Industry Leaders

MOSO International B.V.

Tikamoon SA

Greenington LLC

Ecofurn Oy

VidaXL International BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: European Chemicals Agency updated the REACH Candidate List to 247 substances, heightening testing needs for furniture coatings.

- July 2024: Herman Miller introduced bamboo-based upholstery for its iconic Eames Lounge Chair and Ottoman, lowering the model’s carbon footprint by 35% and showcasing bamboo’s fast growth and low-water cultivation benefits.

- June 2024: IKEA launched a dedicated online and in-store “bamboo shop” spotlighting a full range of bamboo-based furniture and accessories aimed at naturalistic home styling.

Europe Bamboo Furniture Market Report Scope

The bamboo furniture market refers specifically to the segment within the furniture industry focused on products made primarily from bamboo, a fast-growing, renewable material. This market includes a variety of indoor and outdoor furniture items, such as chairs, tables, beds, and storage units. It is driven by increasing consumer preference for eco-friendly and sustainable home decor options. Key characteristics include innovation in design, distribution through retail and online channels, and challenges related to quality sourcing and supply chain logistics. Overall, it reflects a growing trend toward environmentally conscious furniture choices in European markets.

The European bamboo furniture market is segmented into type, category, application, distribution channel, and country. By type, the market is segmented into chairs, tables, beds, cabinets, desks, and stools. By category, the market is segmented into indoor and outdoor. By application, the market is segmented into residential and commercial. By distribution channel, the market is segmented into online and offline. By country, the market is segmented into Germany, France, United Kingdom, Italy, and Rest of Europe.

The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

| Chairs (includes armchairs, lounge chairs, deck chairs) |

| Tables |

| Beds |

| Sofas |

| Stools |

| Benches |

| Cabinets |

| Other Products (bookshelves, coat rack, shoe rack, etc.) |

| Indoor Furniture |

| Outdoor Furniture |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B /Project |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product | Chairs (includes armchairs, lounge chairs, deck chairs) | |

| Tables | ||

| Beds | ||

| Sofas | ||

| Stools | ||

| Benches | ||

| Cabinets | ||

| Other Products (bookshelves, coat rack, shoe rack, etc.) | ||

| By Category | Indoor Furniture | |

| Outdoor Furniture | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B /Project | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of the Europe bamboo furniture market?

The market is valued at USD 4.36 billion in 2026 and is projected to reach USD 5.87 billion by 2031.

Which product category leads sales?

Stools hold 37.30% of 2025 revenue thanks to material efficiency and fast production cycles.

Why is Spain the fastest-growing national market?

Aggressive sustainability requirements in construction and hospitality push Spain to a 6.62% CAGR through 2031.

How will EU formaldehyde limits affect manufacturers?

From August 2026, producers must adopt low-VOC finishes, lifting processing costs by up to 20% yet improving indoor-air quality compliance.

What supply-chain risks face European buyers?

Heavy reliance on Asian culms exposes importers to freight volatility and certification fraud, prompting a strategic pivot toward verified Southeast Asian plantations.

Page last updated on: