Kids And Nursery Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

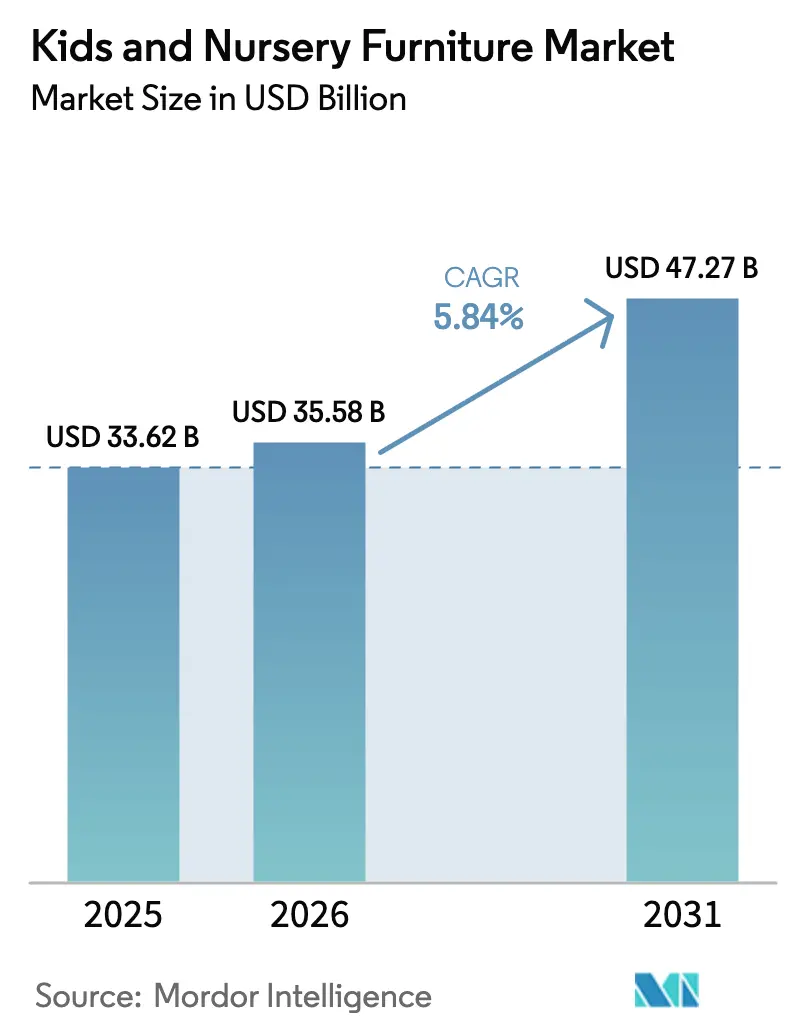

| Market Size (2026) | USD 35.58 Billion |

| Market Size (2031) | USD 47.27 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

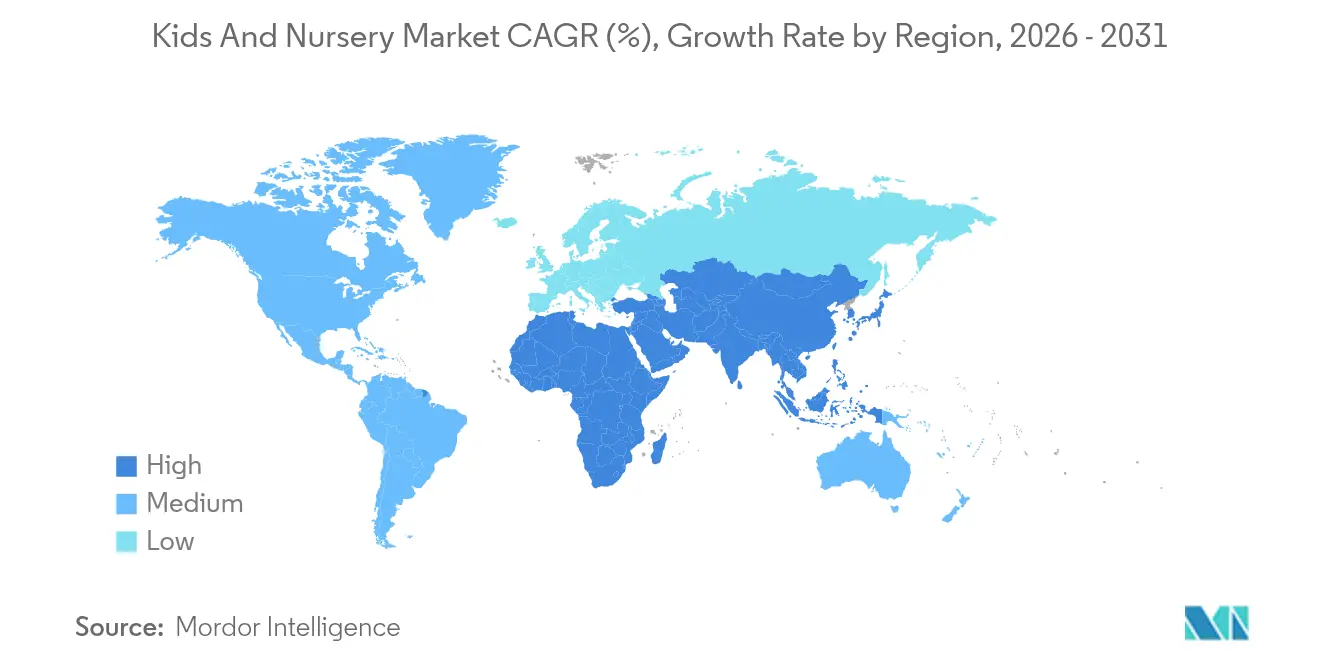

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kids And Nursery Furniture Market Analysis by Mordor Intelligence

Kids and nursery furniture market size in 2026 is estimated at USD 35.58 billion, growing from 2025 value of USD 33.62 billion with 2031 projections showing USD 47.27 billion, growing at 5.84% CAGR over 2026-2031. Rising digital-first shopping habits, stronger sustainability commitments from brands, and the steady integration of smart functions into core pieces are sustaining demand even as raw-material costs remain volatile. Multi-functional designs that evolve with the child, certified low-emission finishes, and direct-to-consumer (D2C) business models that trim retail mark-ups are reshaping competitive dynamics. North American consumers continue to anchor premium sales, while rapid urbanization in Asia-Pacific channels growth toward space-efficient, convertible solutions.

Key Report Takeaways

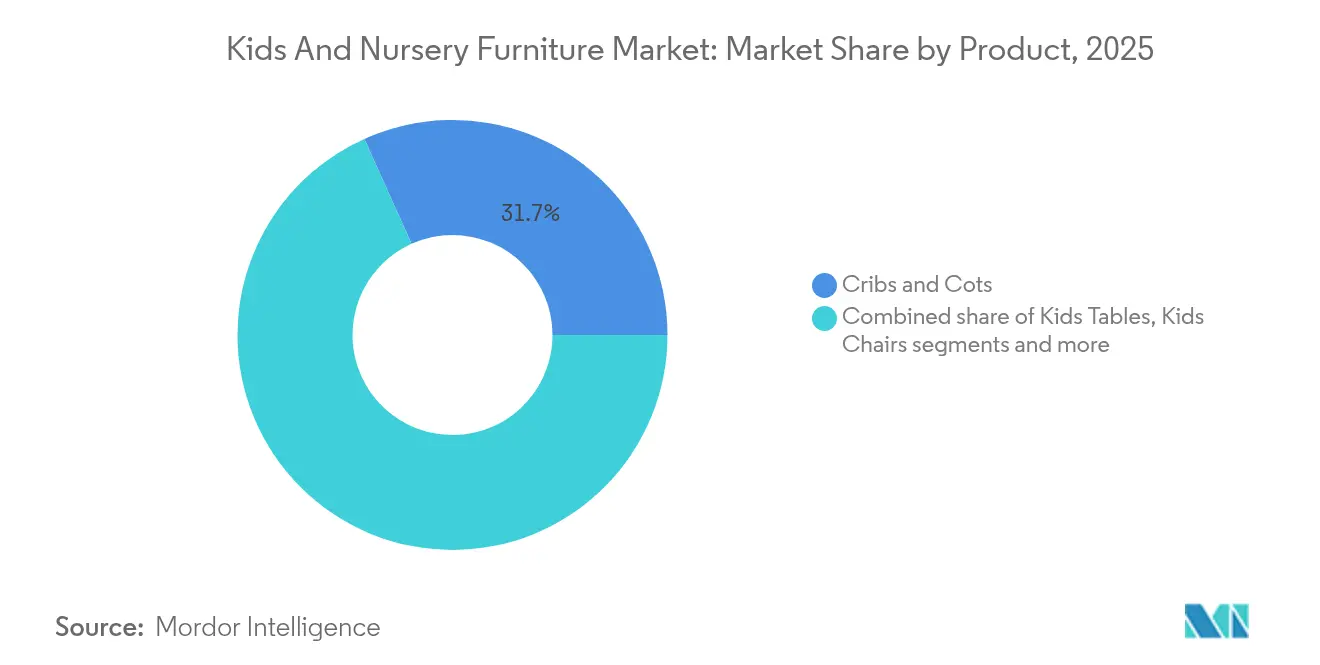

- By product, cribs and cots led with 31.72% of kids and nursery furniture market share in 2025, while kids' chairs posted the fastest 6.08% CAGR outlook to 2031.

- By material, wood accounted for 59.45% share of the kids and nursery furniture market size in 2025; plastics & polymers are projected to grow at 6.28% CAGR through 2031.

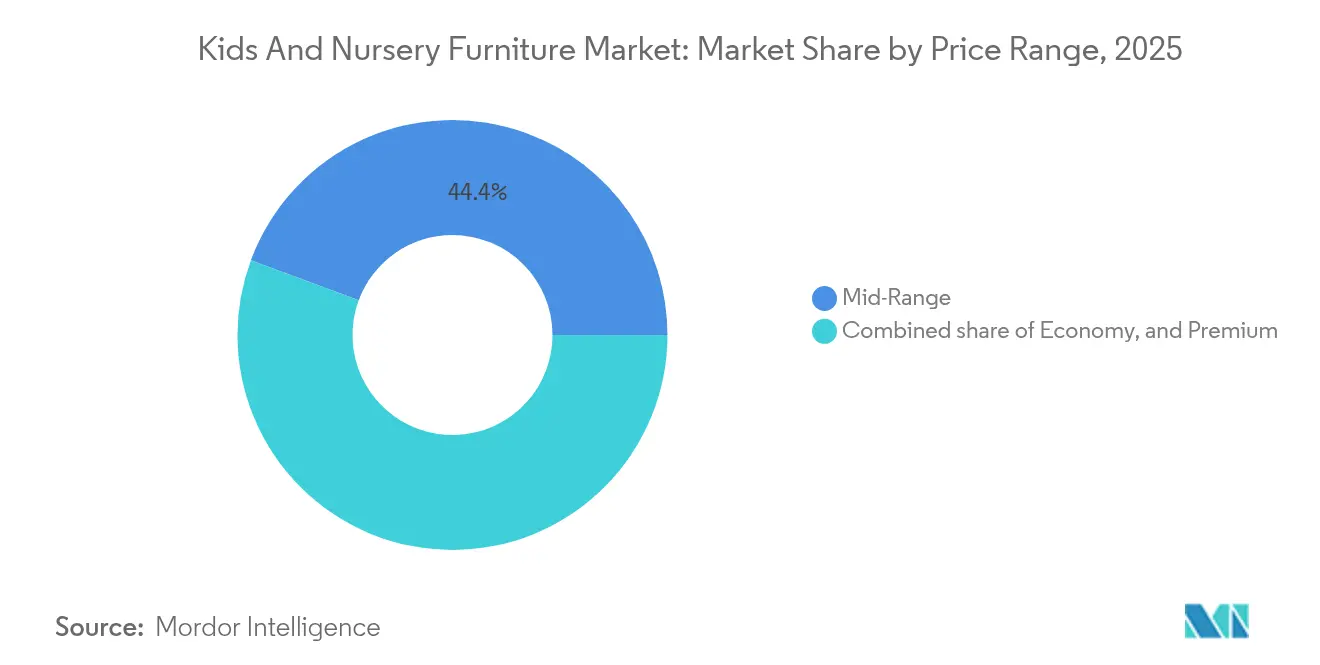

- By price range, the premium tier is on track for 5.95% CAGR (2026-2031) as parents pay extra for certified materials and smart features.

- By distribution, offline channels retained a 69.10% share in 2025, yet online outlets are accelerating at a 7.05% CAGR through 2031.

- By region, North America dominated with 32.68% revenue share in 2025; Asia-Pacific is forecast to record the highest 6.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kids And Nursery Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in D2C brands offering customizable nursery sets | +2.1% | North America, Western Europe | Medium term (2–4 years) |

| Preference for multi-functional, space-saving furniture | +1.8% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Demand for sustainable, non-toxic materials | +1.5% | North America, Europe, Urban Asia-Pacific | Medium term (2–4 years) |

| Rising global birth rates among higher-income parents | +1.2% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Integration of IoT & smart safety features | +0.9% | North America, Europe, and high-income Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in D2C Brands Offering Customizable Nursery Sets

Digital-native brands are compressing traditional retail mark-ups by shipping directly to households and using social media for micro-targeting. Their online configurators let parents mix finishes, fabrics, and safety add-ons before checkout, boosting attachment rates for matching dressers and storage. Global incumbents are now rolling out their headless-commerce sites with AI-driven style advice, aiming to recapture margin leakage to start-ups.

Multi-Functional, Space-Saving Furniture Innovations

High-density city living is driving demand for convertible designs that fold, stack, or reconfigure as children grow. A modular crib-to-desk system showcased at global trade fairs in 2024 demonstrated 40% space savings and a 35% lifecycle cost reduction versus buying six single-purpose items. Manufacturers that fail to embed convertibility into new catalog launches are losing up to 15% unit share in top-tier cities such as Shanghai and Paris. The kids and nursery furniture market increasingly rewards producers that patent hinge mechanisms and telescopic rails, allowing quick transitions without tools.

Sustainable Materials Driving Premium Segment Growth

Parents are scrutinizing emissions, finish chemistry, and forest stewardship labels when choosing nursery products. Brands that publish annual progress toward Forest Stewardship Council (FSC) sourcing or GREENGUARD Gold indoor-air certifications are gaining shelf priority at upscale retailers. Circular design is spreading as companies recycle post-consumer plastic toys into new seating lines and publicize carbon-footprint reductions of 20-25% per piece. The link between sustainability commitments and price realization is tightening, with certified products fetching premiums of 10–18% even in the mid-range.

Millennial and Gen Z Parenting Preferences

Younger parents want friction-free omnichannel journeys: they browse room-set photos, compare user reviews, and book click-and-collect within minutes. Social proof via short-form video is pivotal; influencer walk-throughs of fully styled nurseries drive measurable spikes in web traffic. Interactive showrooms that overlay QR-coded product specs on augmented-reality displays have lifted in-store conversions by more than 20% across several specialty chains. The preference for experience over transaction means retailers are redesigning floor layouts around lifestyle vignettes rather than aisles of boxed inventory.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile lumber and resin prices | −1.1% | North America, Europe | Short term (≤ 2 years) |

| Competition from second-hand & rental platforms | −0.8% | North America, Europe, Urban Asia-Pacific | Medium term (2–4 years) |

| Stringent flammability & chemical compliance | −0.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility Challenges

Lumber prices swung up to 25% in 2024, eroding margins for furniture makers locked into fixed contracts. Leading timber supplier Weyerhaeuser recorded a 7.2% revenue decline in 2024 as softwood pricing eased alongside weaker construction demand. Firms without hedging programs saw gross-margin compression of 3–5 points and accelerated their move toward engineered panels and recycled composites that offer steadier cost bases. Larger players are forging multi-year offtake agreements with sawmills to stabilize input costs.

Second-Hand and Rental Platform Disruption

Furniture-as-a-service models are gaining traction for items with naturally short usage windows, such as cribs and highchairs. Recommerce specialist AptDeco processed USD 84 million in gross merchandise volume in 2024 and now refurbishes mainstream brands for resale partnerships with select retailers. Subscription packages offering periodic upgrades create recurring revenue streams but cannibalize new unit sales. In response, several established manufacturers have piloted trade-back programs, designing components for easy refurbishment and secondary-market certification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Features Drive Chair Innovation

Kids chairs, including highchairs and gliders, are on course for the strongest 6.08% CAGR through 2031. Height-adjustable trays, posture-support inserts, and Bluetooth-enabled weight sensors differentiate premium launches, lifting average selling prices by 25–30%. Cribs and cots retained 31.72% of kids and the nursery furniture market share in 2025 amid ongoing improvements in sleep-monitoring add-ons and toddler-bed conversion kits. Organizers and storage units are rising fastest in high-rent metros where every square foot counts, while change tables and specialty nursing seats remain smaller but profitable niches.

Industry makers who positioned chairs as long-term companions—converting from infant feeding to junior study seating—extended product lifespans to 7–10 years and reduced replacement churn. That strategy aligns with the kids and nursery furniture market's emphasis on sustainability because parents perceive multi-phase use as waste reduction.

By Material: Wood Dominates, Polymers Gain Ground

Wood held 59.45% of the kids and nursery furniture market size in 2025, thanks to its perceived warmth, durability, and timeless styling. FSC-verified supply chains and water-based finishes now headline marketing campaigns. Regional initiatives such as the Welsh Government’s Timber Industrial Strategy underscore timber’s low embodied-carbon advantage for consumer goods.

Plastic & Polymer, however, are forecast to clock a 6.28% CAGR as advances in non-phthalate formulations drive acceptance among safety-conscious buyers. Wood-plastic composites meeting EN71 criteria marry the tactile appeal of wood grain with the scratch resistance of thermoplastics, opening design freedom for bold color palettes. Metal frames continue to provide structural reinforcement, while emerging materials like bamboo and cork draw niche interest among eco-focused households.

By Price Range: Premium Segment Leads Growth

The premium tier achieves a leading 5.95% CAGR by layering smart functions, designer collaborations, and handcrafted joinery. Growth is amplified by urban dual-income families who view nursery décor as an extension of personal style. Mid-range lines, which commanded 44.35% share of the kids and nursery furniture market in 2025, are steadily absorbing features once exclusive to flagship ranges, raising the baseline for safety and sustainability. Economy offerings focus on essential certifications and flat-pack formats to curb freight costs and widen accessibility in emerging economies.

By Distribution Channel: Digital Transformation Accelerates

Online portals are expanding at 7.05% CAGR on the back of virtual room planners and 360-degree product spins that mitigate the inability to touch or test. Online-first labels exploit fast-feedback loops, releasing limited runs and iterating designs every season. Yet brick-and-mortar still accounts for 69.10% of 2025 revenue because parents often insist on a final tactile quality check before purchase. The strongest performers integrate both realms, offering buy-online-pick-up-in-store services and tablet-based kiosks that bridge inventory visibility between channels.

Geography Analysis

North America retained the largest regional slice at 32.68% in 2025, underpinned by high spending power and rapid uptake of IoT-enabled nursery gear. Updated US safety standards for non-full-size cribs and play yards, effective April 2025, further raise the baseline for compliance and reinforce consumer trust. The kids and nursery furniture market size for smart-equipped models is therefore scaling fastest in the United States and Canada, where baby-monitoring apps are commonplace.

Asia-Pacific is projected to deliver a 6.64% CAGR through 2031, making it the foremost growth engine. Chinese city dwellers favor modular systems that fold flat or extend vertically, while Indian parents are gravitating toward natural materials paired with compact footprints. E-commerce penetration is widening its reach beyond tier-one cities, enabling premium brands to court customers who previously lacked access to specialty stores. Southeast Asia’s youthful demographic profile adds long-run tailwinds for crib and storage categories.

Europe presents a mature but innovation-driven landscape where sustainability, design longevity, and compliance with stringent REACH chemical standards dominate purchase criteria. South America, led by Brazil, is seeing mid-range imported nursery suites gain favor as middle-class households expand. In the Middle East and Africa, premium European labels enjoy cachet among affluent buyers, and local producers are beginning to localize convertible designs to suit compact urban apartments in the Gulf Cooperation Council states.

Competitive Landscape

Global incumbents, regional specialists, and agile D2C challengers all compete in the kids' and nursery furniture market. Delta Children expanded production in South Carolina in 2025 to shorten lead times and deepen community engagement via partnerships with parenting organizations. One competitor promotes GREENGUARD Gold certification, REPREVE recycled fabrics, and FSC wood to reinforce a sustainability-first positioning.

Smart-furniture adoption distinguishes premium offerings; connected cribs that track sleep metrics, recliners with USB-charging armrests, and app-linked height-adjustable desks command margins of 8–10 points above category averages. Larger brands leverage scale to absorb R&D and regulatory testing outlays demanded by the newest ASTM F406-2023 requirements for play yards, which tightened cord-length rules and updated warning labels in 2025.[3]SGS North America, “ASTM F406-23 Adoption Updates,” sgs.com Smaller makers are responding by licensing modular designs to bigger partners or focusing on bespoke carpentry outside strict crib standards.

Barriers to entry are rising because electronic components bring additional certification layers for electromagnetic compatibility and data privacy. Meanwhile, raw material hedging and vertical integration into sawmills or polymer compounding plants help industry leaders mitigate cost swings.

Kids And Nursery Furniture Industry Leaders

Delta Children

Ashley Furniture Industries

Graco (Newell Brands)

Dorel Juvenile

IKEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dorel Juvenile USA extended its Maxi-Cosi brand into premium nursery furniture with four convertible collections featuring cribs, pre-assembled dressers, and recliners equipped with USB charging ports.

- February 2025: The US Consumer Product Safety Commission adopted ASTM F406-23 as the mandatory standard for non-full-size cribs, effective 5 April 2025, updating definitions and strangulation warning labels.

- April 2024: Delta Children enlarged its Orangeburg, South Carolina, facility and debuted a low twin loft bed plus sports-themed umbrella strollers to broaden its youth portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the kids and nursery furniture market as the annual revenue generated from new cribs, cots, beds, tables, chairs, storage units, lighting, rugs, and décor items built for children up to twelve years of age and sold through offline and online retail channels worldwide.

Scope Exclusion: second-hand furniture sales and rental subscriptions remain outside our scope.

Segmentation Overview

- By Product

- Kids Tables (Including Changing Tables)

- Kids Chairs (Including Highchairs, Gliders, etc.)

- Cribs and Cots

- Organizers and Storage

- Other Products

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Offline

- Supermarkets and Hypermarkets

- Home Centers

- Specialty Furniture Stores

- Online

- Offline

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed manufacturers, big-box buyers, specialty e-tailers, pediatricians, and interior designers across North America, Europe, and Asia-Pacific. These conversations clarified material cost swings, emerging design themes, and typical product lifespans, helping us plug data gaps and fine-tune adoption curves before numbers were frozen.

Desk Research

We began with macro datasets from UNICEF live birth statistics, World Bank household expenditure tables, UN Comtrade trade codes for wooden and plastic furniture, and Eurostat retail furniture turnover reports, which let us size the potential demand pool and map import totals. We then scanned consumer spending surveys and product recall databases such as those of the US CPSC for safety-related replacement cycles. Company filings, IPO prospectuses, and investor presentations provided blended average selling prices that underpin segment margins. Input on retailer footfall and web traffic was drawn from D&B Hoovers and Dow Jones Factiva for cross-checks. This list is illustrative; many additional open and proprietary sources were consulted for validation.

Market-Sizing & Forecasting

A top-down model built on birth cohorts, parental spending per child, and furniture replacement rates produces the first cut, which is then balanced with selective bottom-up supplier roll-ups and channel checks. Key variables include national live-birth volumes, median disposable income per household, urban apartment share, furniture penetration per child, average selling price shifts, and online channel share growth. Forecasts through 2030 rely on multivariate regression that links these drivers to historical sales and adjusts for policy incentives or safety-standard updates flagged by experts. Where supplier data fall short, we impute volumes from customs declarations and apply conservative utilization factors.

Data Validation & Update Cycle

Outputs pass a multi-layer review in which analysts test variance against independent indicators, flag anomalies, and revisit respondents when thresholds are breached. Reports are refreshed every twelve months and updated sooner if material recalls, tariff changes, or macro shocks alter demand.

Why Mordor's Kids And Nursery Furniture Baseline Commands Reliability

Published estimates often diverge because firms slice the market differently, apply varied price ladders, and refresh at uneven intervals.

Key gap drivers include whether used goods are counted, whether accessories like rugs are folded into totals, the aggressiveness of online-channel growth assumptions, currency translation dates, and the cadence at which analysts revisit supplier guidance.

External figures of USD 36.9 billion, USD 53.31 billion, and USD 78.03 billion for 2025 illustrate this spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.62 B | Mordor Intelligence | - |

| USD 36.90 B | Regional Consultancy A | Omits décor items; uses single ASP for all materials |

| USD 53.31 B | Global Consultancy B | Includes second-hand sales and rental subscriptions |

| USD 78.03 B | Trade Journal C | Applies aggressive e-commerce growth and year-old FX rates |

Taken together, the comparison shows that Mordor's disciplined scope, annually refreshed inputs, and dual-approach modeling deliver a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the kids and nursery furniture market?

The kids and nursery furniture market size is USD 35.58 billion in 2026 and is projected to reach USD 47.27 billion by 2031.

Which product segment is growing the fastest?

Kids chairs, including highchairs and gliders, are forecast to grow at a 6.08% CAGR through 2031 due to ergonomic upgrades and smart-sensor integration.

Why are sustainable materials important in nursery furniture?

Parents increasingly demand FSC-certified wood and low-VOC finishes, allowing brands to charge 10–18% premiums while meeting stricter indoor-air standards.

How are online sales channels changing the industry?

E-commerce is rising at a 7.05% CAGR as augmented-reality tools let parents visualize furniture at home, pushing brands to refine omnichannel strategies.

What are the main restraints on market growth?

Volatile lumber prices, the rise of second-hand rental platforms, and tighter flammability regulations add cost and competitive pressure for manufacturers.

Which region will drive future demand?

Asia Pacific is expected to post a leading 6.64% CAGR through 2031, propelled by urbanization, growing disposable incomes, and expanding e-commerce access.

Page last updated on: