Market Overview

| Study Period | 2020 - 2031 |

|---|---|

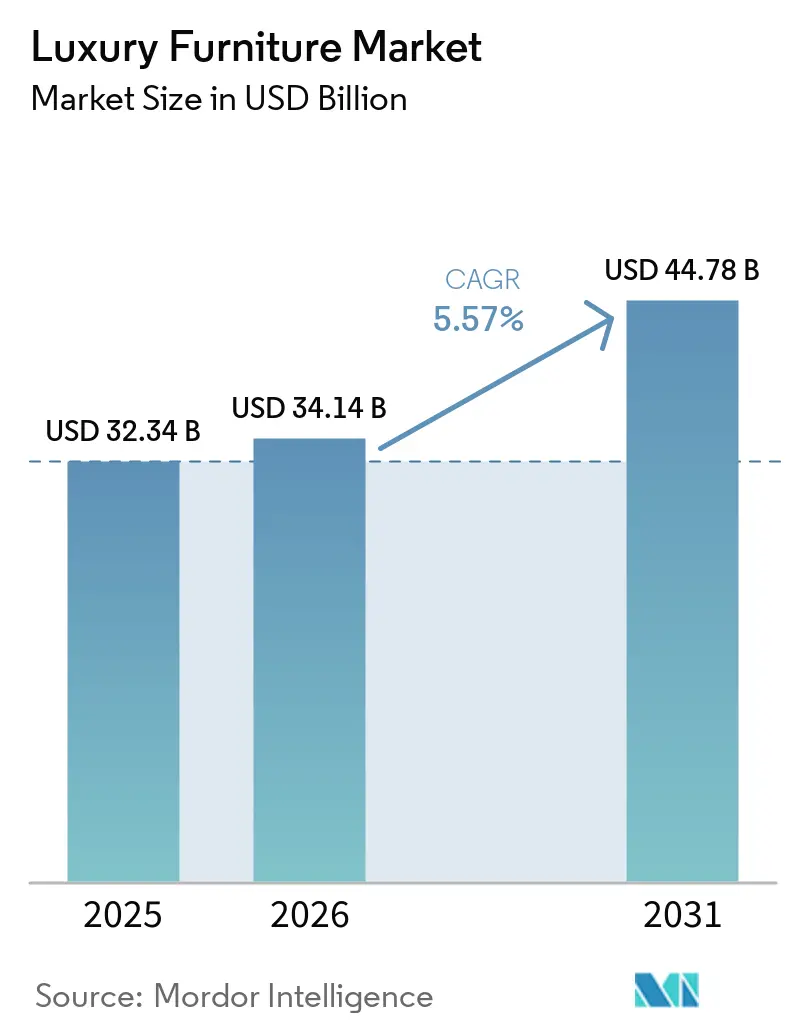

| Market Size (2026) | USD 34.14 Billion |

| Market Size (2031) | USD 44.78 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

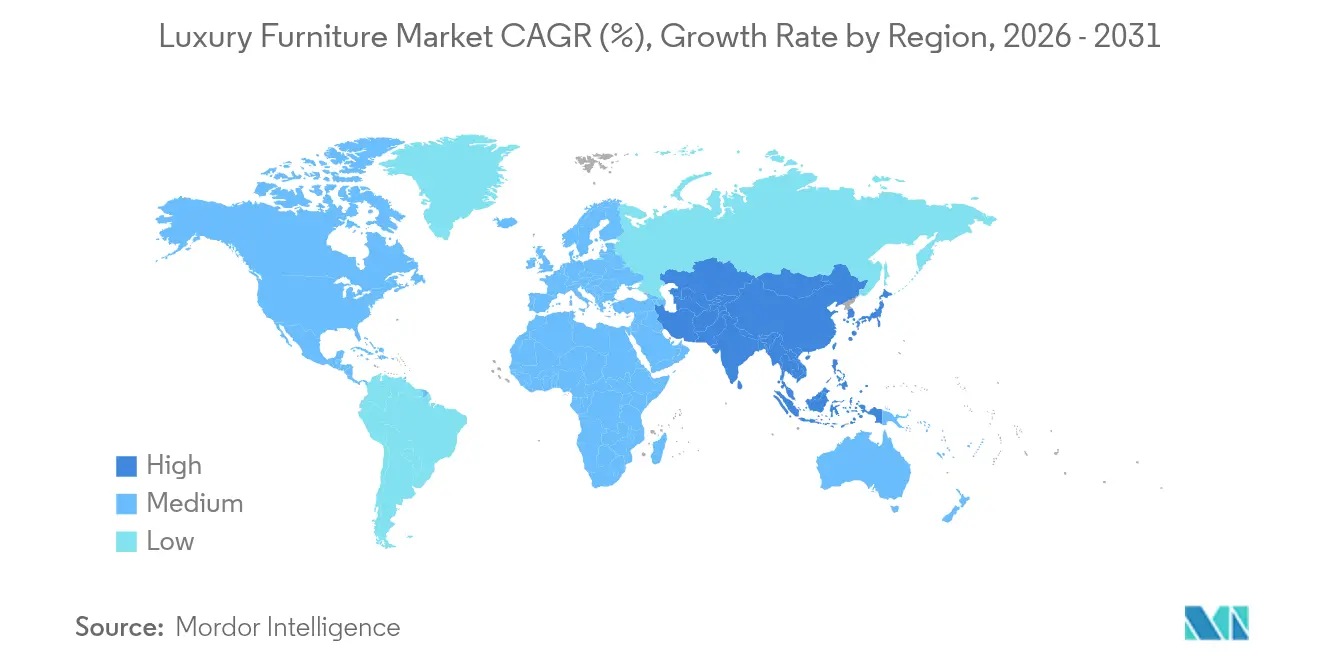

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Furniture Market Analysis by Mordor Intelligence

Luxury Furniture market size in 2026 is estimated at USD 34.14 billion, growing from 2025 value of USD 32.34 billion with 2031 projections showing USD 44.78 billion, growing at 5.57% CAGR over 2026-2031.

Rising high-net-worth individual wealth, post-pandemic lifestyle shifts that prioritize premium residential interiors, and vigorous luxury hospitality pipelines underpin demand resiliency. Heritage European craftsmanship, omnichannel retail advances that fuse immersive galleries with augmented reality visualization, and accelerating material innovation reinforce the luxury furniture market growth outlook. Brands intensify differentiation through provenance storytelling, smart-home functionality, and limited-edition collaborations that lift average selling prices while drawing younger affluent cohorts. Consolidation among regional chains unlocks scale efficiencies without diluting exclusivity, supporting faster penetration of high-growth Asian wealth hubs and steady expansion in mature North American design centers.

Key Report Takeaways

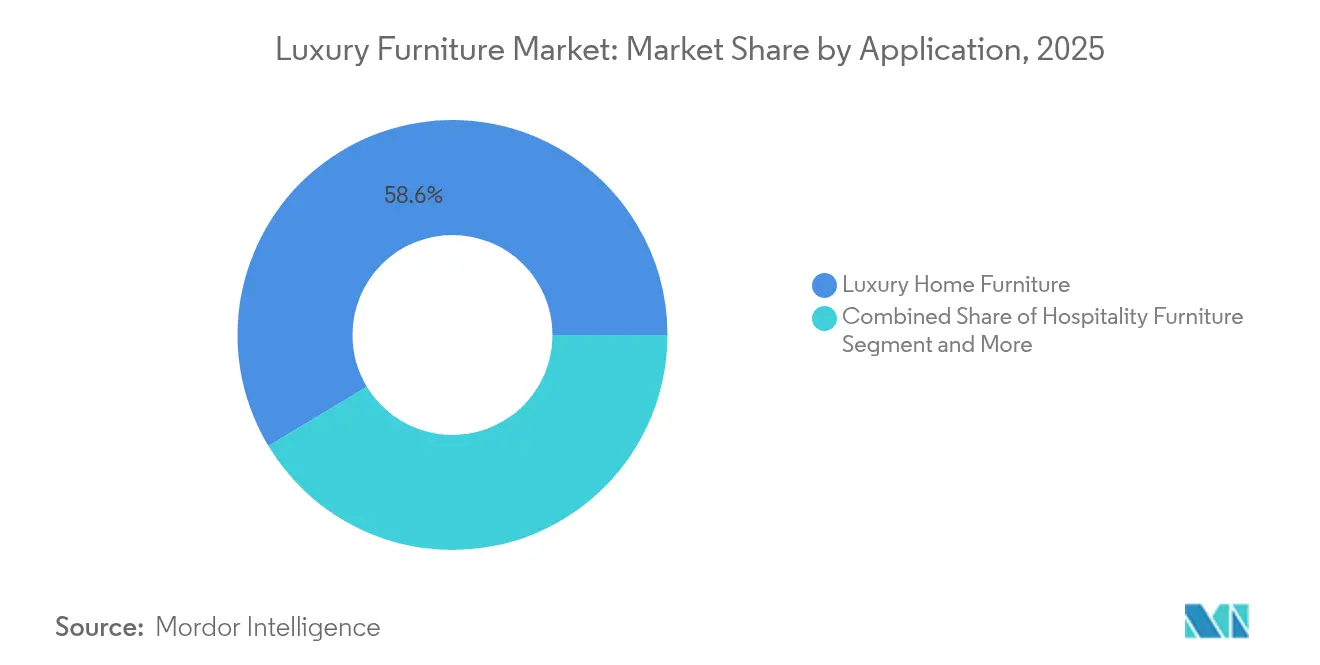

- By application, luxury home furniture held 58.64% of the luxury furniture market share in 2025; hospitality furniture is poised to expand at a 5.96% CAGR through 2031.

- By material, wood commanded 45.87% of the luxury furniture market size in 2025, while glass is projected to register a 6.33% CAGR between 2026 and 2031.

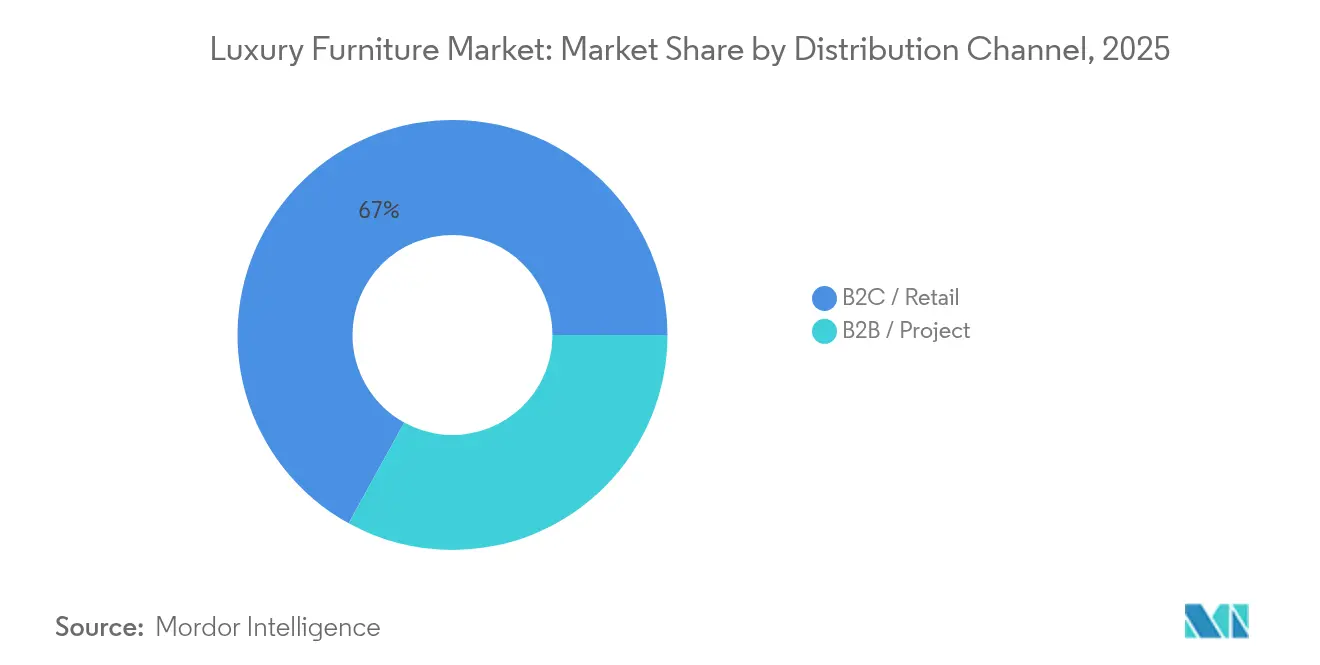

- By distribution channel, B2C retail captured 66.98% share of the luxury furniture market size in 2025, and online retail is advancing at a 6.55% CAGR through 2031.

- By geography, Europe accounted for 36.88% of the luxury furniture market share in 2025, whereas Asia-Pacific is set to climb at a 6.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes of HNWIs | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Expansion of luxury real estate & hospitality projects | +0.9% | Middle East, Asia-Pacific, North America | Long term (≥ 4 years) |

| Growth of online luxury furniture retail | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Smart-home integration boosts ASPs | +0.7% | North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Adoption of bio-based sustainable materials | +0.5% | Europe, North America | Long term (≥ 4 years) |

| 3-D printing enables on-demand customization | +0.4% | North America, Europe, with pilots in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes of HNWIs Drive Premium Demand

Global expansion of millionaire households feeds a steady influx of first-time luxury furniture buyers[1]Jessica Binns, “What a US recession would mean for global luxury,” Vogue Business, voguebusiness.com. These consumers treat statement pieces as portable investments that signal cultural capital, spurring demand for limited production runs and bespoke craftsmanship. Designer collaborations and heritage provenance stories resonate strongly with this segment, allowing brands to raise average selling prices without noticeable volume erosion. Technology and finance entrepreneurs, now a dominant share of new HNWIs, favor contemporary silhouettes with discreet smart-home features that harmonize with connected lifestyles. Geographic hotspots include Shenzhen, Bengaluru, and Miami, where rapid wealth generation aligns with premium real-estate purchases, embedding furniture orders within broader interior design contracts. As wealth distribution broadens, tier-two cities emerge as incremental growth nodes, encouraging brands to adopt franchise showrooms and mobile pop-up concepts to capture local demand.

Expansion of Luxury Real Estate and Hospitality Projects

Record pipelines of five-star hotels, branded residences, and ultra-prime resorts create recurring, large-volume procurement streams that smooth cyclical swings in retail demand. Developers in Saudi Arabia’s NEOM, Indonesia’s Bali west coast, and Florida’s Gulf Coast specify contract-grade furniture that must combine exquisite aesthetics with commercial-use durability. Purchase orders often bundle guestroom case goods, public-area seating, and outdoor cabanas, pushing order values into seven-figure ranges and locking suppliers into multi-year service agreements. Brands with in-house design studios and BIM-ready digital libraries gain an edge in tender processes that prioritize speed and compliance documentation. Hospitality clients increasingly mandate ESG disclosures, favoring suppliers using FSC-certified woods and low-VOC finishes. These projects offer built-in showrooms that expose international travelers to the furniture brand, driving post-stay residential sales.

Growth of Online Luxury Furniture Retail

High-fidelity 3D configurators, AR room-placement tools, and live video consultations have pushed affluent buyers to finalize USD 20,000-plus purchases entirely online[2]London Dynamics, “AR & 3D Furniture Visualization,” londondynamics.com. Digital channels now account for double-digit revenue share at leading brands, backed by white-glove logistics that deliver assembled pieces, remove packaging, and provide in-home styling tweaks. Customer data gathered through clickstream analytics informs limited-edition drops released first to high-engagement cohorts, generating wait-list dynamics without markdown risk. Brands remain wary of generic marketplaces, opting for invitation-only digital flagships that preserve exclusivity while enabling international expansion without capital-heavy real estate. The model is particularly potent in Australia and Canada, where showroom coverage is sparse but broadband penetration is high. Seamless returns, insured transit, and carbon-neutral shipping upgrades further reassure discerning buyers, cementing online’s role as a strategic growth lever.

Smart-Home Integration Boosts ASPs

Embedding IoT sensors, wireless charging pads, and biometric tracking transform traditional furniture into functional hubs commanding price premiums of 15-30%[3]Shaping Tomorrow, “Smart Home Technology Integration in Furniture,” shapingtomorrow.com. Luxury beds that adjust lumbar zones via app, dining tables with inductive surface charging, and credenzas that conceal climate-controlled wine storage exemplify the new hybrid category. Brands partner with chipset makers and wellness platforms to create proprietary ecosystems that deliver firmware updates, enabling upsell of digital services long after initial sale. Early adopters enjoy reduced competitive intensity and higher switching costs as clients become locked into specific software environments. Integration also drives larger room-bundle sales because buyers seek aesthetic coherence across multiple smart pieces. Premium retailers train in-house technicians to calibrate connected features during delivery, strengthening customer satisfaction and repeat purchase likelihood.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity during macro-economic slowdowns | -0.8% | Global, pronounced in emerging markets | Short term (≤ 2 years) |

| Volatile hardwood and leather prices | -0.6% | Global, concentrated sourcing regions | Medium term (2-4 years) |

| Counterfeit luxury furniture trade | -0.4% | Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Shortage of master artisans for bespoke output | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity During Macro-Economic Slowdowns

Luxury furniture demand, though resilient, remains tethered to sentiment; affluent consumers often defer major purchases when equity markets wobble or property transactions stall. 2024’s housing downturn in the United States illustrated this dynamic when showroom traffic fell even as household net worth stayed intact. Retailers countered by introducing phased delivery plans that allow clients to furnish priority rooms first and complete the ensemble later, preserving cash flow without overt discounting. Marketing shifted to emphasize timeless value and emotional well-being rather than conspicuous consumption, aligning with the subdued public mood. Brands with diversified geographic footprints cushioned the impact as Middle East and Southeast Asian sales offset softness in Western markets. After macro clouds clear, pent-up demand often releases abruptly, underscoring the importance of inventory flexibility to capture rebound windows.

Volatile Hardwood and Leather Prices

Input-cost surges compress margins because luxury positioning limits straightforward pass-through of price hikes. Horváth's research cited 30% hardwood cost inflation since late 2020 and predicts further escalation amid tight supply[4]Horváth, “Supply Chain Disruptions in the Furniture Industry,” horvath-partners.com. Premium leather follows similar volatility, driven by ranch-level disease outbreaks and tannery capacity constraints. Manufacturers hedge via multi-year contracts and species substitution—moving from American walnut to sustainably farmed sapele, or from Italian full-grain leather to Scandinavian semi-aniline hides with comparable feel. Some brands pilot dynamic pricing indexed to commodity benchmarks, but risk confusing consumers accustomed to fixed luxury tags. Investments in engineered veneers and mushroom-based leathers promise long-term mitigation yet require customer education to maintain perceived opulence. Meanwhile, operational efficiency—robotic cutting, yield-optimizing nesting software—becomes decisive in defending profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Home Dominance Meets Hospitality Acceleration

Luxury home furniture generated 58.64% of 2025 revenue, cementing its primacy within the luxury furniture market. Living-room seating remains the top contributor as modular sectionals adapt to hybrid entertainment-work patterns, while dining suites regain relevance amid at-home hosting resurgence. Bedroom ensembles incorporate wellness sensors and ambient lighting that sync with circadian rhythms, turning private quarters into restorative sanctuaries. Outdoor collections witness double-digit growth in temperate zones where pandemic-era patio upgrades matured into full alfresco living concepts, often specifying weather-resistant teak and quick-dry performance fabrics. Entry-level luxury buyers gravitate toward curated “room packages” that simplify decision-making yet preserve bespoke fabric and finish options. Designers leverage virtual stagers to upsell ancillary décor—rugs, lighting, art—raising order values and strengthening brand stickiness.

Hospitality furniture is forecast to advance at a 5.96% CAGR, overtaking office as the fastest-growing commercial application by 2027. Global resort pipelines—covering Red Sea islands, Japanese wellness ryokans, and Caribbean eco-lodges—demand differentiated aesthetics reflecting local culture while adhering to international durability standards. Suppliers with in-house testing labs certify abrasion, UV, and salt-spray resistance, winning long-term maintenance contracts that include refurbishment cycles. Branded residence developers bundle furniture packages into unit prices, simplifying buyer move-in and ensuring interior cohesion. Cruise ship refurbishments present niche opportunities for modular, lightweight pieces engineered to withstand marine regulations. Collectively, these trends diversify revenue streams and reduce reliance on discretionary residential cycles.

By Material: Traditional Wood Leadership Versus Modern Glass Innovation

Wood retained 45.87% share in 2025, reaffirming its status as the luxury furniture market’s touchstone material. European oak and American black walnut headline premium catalogs, prized for grain clarity and dimensional stability. Brands emphasize provenance of origin, seasoning duration, artisanal joinery—to justify multi-thousand-dollar price lifts. Sustainability imperatives prompt wider use of certified tropical species and reclaimed beams re-milled into contemporary forms, marrying eco-credibility with heritage narratives. Precision CNC routers deliver complex marquetry at scale, while hand-applied oils preserve tactile warmth, sustaining wood’s emotional appeal in digitally saturated homes.

Glass, advancing at a 6.33% CAGR, transforms from accent surface to structural hero in ultramodern interiors. Low-iron compositions achieve crystalline clarity, and anti-smudge nano-coatings ease maintenance concerns for high-touch items such as dining tables. Smart-glass partitions toggle opacity via voice command, offering privacy on demand without heavy drapery. Laminated glass layers embed LED matrices, creating luminous coffee tables that double as ambient lighting. Designers exploit glass’s visual lightness to balance heftier stone or timber elements, achieving spatial equilibrium in compact urban apartments. Freight specialists adopt custom-crating and vibration sensors to mitigate transit breakage, enabling wider geographic reach for fragile yet high-margin pieces.

By Distribution Channel: Omnichannel Retail Excellence

B2C retail commanded 66.98% revenue of 2025 in the luxury furniture market, anchored by flagship galleries where curated vignettes immerse visitors in cohesive lifestyle narratives. Brands replicate boutique-hotel atmospheres complete with cafés and rooftop gardens, encouraging dwell time that correlates with higher basket sizes. Sales associates armed with tablets render real-time fabric swaps and dynamic pricing scenarios, shortening decision cycles. Loyalty programs offer design concierge services and early access to capsule collections, deepening engagement across the customer life cycle. Financing partnerships with private banks allow high-net-worth clients to bundle multi-room purchases into interest-free plans, reducing sticker shock for six-figure invoices.

Digital-first transactions post a 6.55% CAGR in luxury furniture industry as immersive technologies narrow the trust gap once inherent to online luxury purchases. Virtual avatars guide clients through 360-degree room mock-ups populated with true-scale furniture, while AI algorithms suggest accessory pairings based on visual-style recognition. Return rates stay below 4% because augmented-reality previews accurately map dimensions and color fidelity. Partners in last-mile logistics specialize in climate-controlled trucks and dual-technician setups to maneuver oversized pieces through high-rise elevators without damage. Brands still view e-commerce as complementary—an on-ramp to in-person consultations rather than a full replacement—preserving the high-touch DNA essential to luxury positioning.

Geography Analysis

Europe preserved 36.88% global revenue of 2025 in the luxury furniture market, leveraging centuries-old craft clusters in Italy’s Brianza, France’s Alsace, and Germany’s North Rhine-Westphalia. Italian exports of EUR 19.4 billion demonstrate robust external demand despite labor-cost headwinds. Regional brands capitalize on proximity to design capitals—Milan, Paris, and Cologne, which host influential fairs that set global trend agendas. EU regulations on deforestation, chemical finishes, and waste recovery push manufacturers toward transparent supply chains, reinforcing Europe’s reputation for responsible luxury. However, a shrinking artisan workforce threatens capacity; apprenticeship subsidies and robotic assistive devices emerge as parallel solutions to sustain output while safeguarding craftsmanship DNA.

Asia-Pacific registers the fastest trajectory in luxury furniture industry at a 6.92% CAGR through 2031, propelled by urban affluence in China, India, and Southeast Asia. Chinese tier-two cities foster fresh showroom expansion as rising professionals remodel newly acquired apartments to reflect global taste. Japan’s weak yen continues to attract inbound shoppers who take advantage of duty-free schemes to ship Italian sofas home, creating a transactional bridge between European makers and Asian consumers. Australia’s design-savvy homeowners drive demand for outdoor teak ensembles that withstand coastal climates, while Singapore and Hong Kong maintain hub status for regional e-commerce fulfillment thanks to efficient port systems.

North America holds a steady share in the luxury furniture industry, buoyed by coastal metropolitan wealth and resilient renovation activity. California leads showroom innovation: Restoration Hardware’s Palm Desert design hub integrates architectural planning, landscape design, and furniture curation under one roof, capturing complete project spend. East-Coast pent-up demand surfaces in vacation-home corridors from the Hamptons to Palm Beach, where clients favor transitional styles that bridge classical detailing with modern comfort. Canadian luxury purchases benefit from favorable currency hedging versus European imports, making Montreal and Toronto critical distribution nodes. Integrated supply chains across Mexico provide upholstered frames, underscoring NAFTA’s role in cost and lead-time optimization.

The Middle East and Africa evolve into opportunity frontiers driven by sovereign diversification strategies. Saudi Arabia’s Vision 2030 giga-projects specify museum-grade interiors for hotels and cultural institutions, while the UAE’s luxury retail ecosystem channels European brands into wider Gulf Cooperation Council demand. In Africa, Nigeria’s burgeoning upper-middle class fuels interest in statement dining sets, albeit constrained by import duties and logistical hurdles. South Africa’s hospitality upgrades ahead of international sporting events open contract channels for European and local manufacturers partnering on mixed-material lounge collections adapted for harsher UV exposure. Collectively, these markets, though smaller, offer outsized margins when paired with localized service models and compliant import documentation.

Competitive Landscape

The luxury furniture industry remains moderately fragmented; the top five players command roughly half of the combined share, preventing runaway dominance yet conferring meaningful scale advantages. European heritage houses—Roche Bobois, B&B Italia, Poltrona Frau—continue to leverage designer collaborations and artisan cachet to justify premiums. Restoration Hardware exemplifies the vertically integrated American model, incorporating hospitality venues and architecture services to capture ancillary revenue layers. Austrian retailer XXXLutz extended its upscale competence by absorbing 140 Central European outlets, unlocking cross-border procurement synergies and private-label potential.

Technology serves as a competitive fulcrum: cloud-based product-lifecycle systems accelerate design iterations, while blockchain provenance certificates reassure buyers wary of counterfeits. Sustainability credentials evolve into table stakes as luxury buyers scrutinize carbon footprints; FSC certification and chrome-free tanning headline marketing campaigns. Cross-industry collaborations—Maserati with Giorgetti—expand brand halos beyond traditional décor audiences, attracting auto enthusiasts into furniture showrooms.

Private-equity inflows, evidenced by CBPE taking majority of sofa.com, facilitate omnichannel rollout and backend automation, intensifying competitive pressure on smaller ateliers. Nonetheless, micro-brands with agile digital storytelling and hyper-local artisan partnerships continue carving profitable niches in bespoke and eco-avant-garde segments. Across all players, brand narratives increasingly weave together heritage, innovation, and responsible sourcing to resonate with multi-generationally affluent households.

Luxury Furniture Industry Leaders

Restoration Hardware (RH)

Roche Bobois

Herman Miller-Knoll

Poltrona Frau (Lifestyle Design)

Luxury Living Group (Fendi Casa)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: XXXLutz finalized the takeover of 140 stores spanning Germany, Czech Republic, and Slovakia, boosting its Central European footprint and integrating premium lines into newly acquired showrooms. The move gives XXXLutz greater bargaining leverage with high-end suppliers and accelerates omnichannel deployment across the region.

- April 2025: ScS reported a wave of employee resignations after acquiring Italian sofa specialist Poltronesofà, signaling cultural misalignment that could disrupt production schedules and decrease service quality in the competitive luxury upholstery segment.

- March 2025: Maserati teamed with Giorgetti to unveil a furniture capsule blending automotive cues with artisanal woodcraft, broadening both brands’ lifestyle ecosystems and tapping cross-selling potential among luxury car owners.

- March 2025: Roche Bobois released its Spring 2025 Sourcebook, packed with new designer collaborations, ensuring continual showroom refreshes and reinforcing its lead in narrative-driven collection launches.

Global Luxury Furniture Market Report Scope

Luxury furniture is something that is conducive to sumptuous living and that includes elements that are elegant, customize, and indulgent. This report aims to provide a detailed analysis of the global luxury furniture market. It focuses on the market dynamics, technological trends, and insights into various product and application types. Also, it analyses the key players and the competitive landscape in the global luxury furniture market.The Luxury Furniture Market is segmented by Product (Lighting, Tables, Chairs and Sofas, Beds, Cabinets, Accessories, and Other Products), by Distribution Channel (Home Centers, Flagship Stores, Specialty Stores, Online, and Other Distribution Channels), by End-User (Residential and Commercial), and by Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report offers market size and forecast values for the Luxury Furniture Market in USD billion for the above segments.

By Application

| Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (Bathroom, Outdoor, etc.) | |

| Luxury Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas and Other Soft Seating | |

| Other Office Furniture | |

| Luxury Hospitality Furniture | |

| Other Applications (Educational Furniture, Healthcare Furniture, Retail Malls, Government Offices, etc.) |

By Material

| Wood |

| Metal |

| Glass |

| Leather |

| Plastic and Other Synthetics |

| Sustainable / Green Materials |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Flagship Store | |

| Other Distribution Channels | |

| B2B / Project |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Application | Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (Bathroom, Outdoor, etc.) | ||

| Luxury Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas and Other Soft Seating | ||

| Other Office Furniture | ||

| Luxury Hospitality Furniture | ||

| Other Applications (Educational Furniture, Healthcare Furniture, Retail Malls, Government Offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Glass | ||

| Leather | ||

| Plastic and Other Synthetics | ||

| Sustainable / Green Materials | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Flagship Store | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What value will the luxury furniture market reach by 2031?

The luxury furniture market size forecast to hit USD 44.78 billion by 2031

Which application segment is growing fastest?

Hospitality furniture is expanding at a 5.96% CAGR through 2031.

Which region has the highest growth potential?

Asia-Pacific leads with a projected 6.92% CAGR.

How does sustainability influence material selection?

Certified woods, eco-tanned leathers, and bio-based composites gain share as regulations tighten and affluent buyers value responsible luxury.

Why are smart-home features important?

They raise average selling prices and create ongoing service revenue while enhancing user experience.

Which retail model dominates sales?

Flagship galleries complemented by omnichannel digital tools capture 66.98% of revenue.

Page last updated on: