Market Overview

| Study Period | 2020 - 2031 |

|---|---|

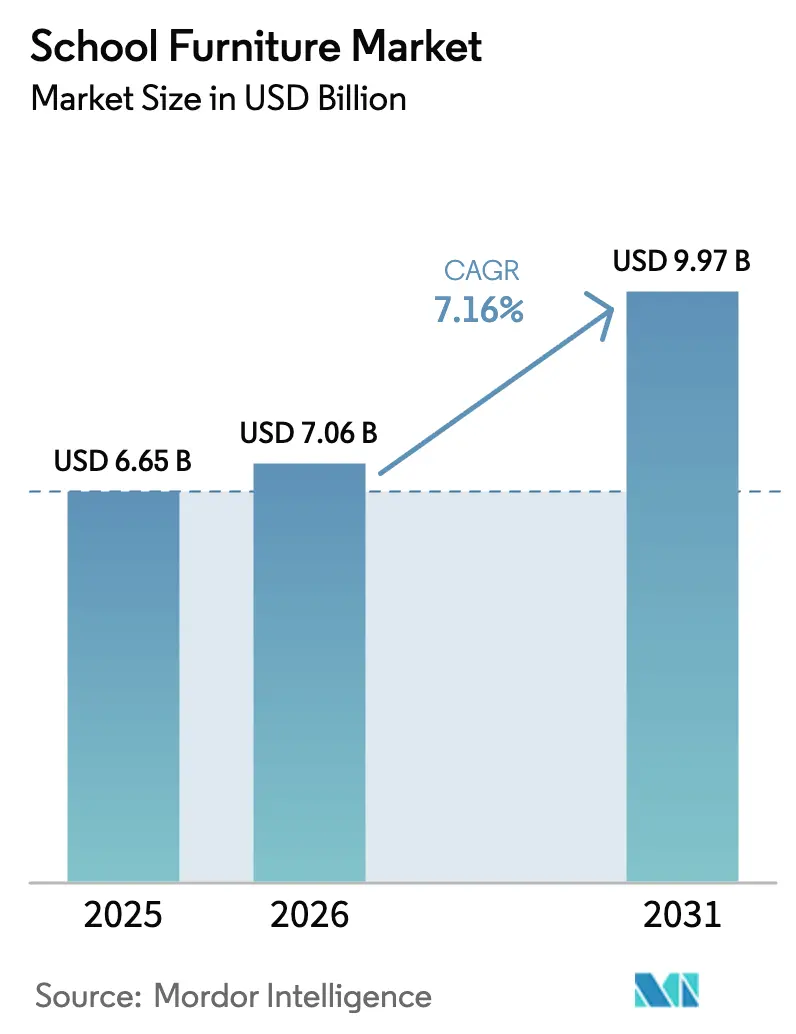

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 9.97 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

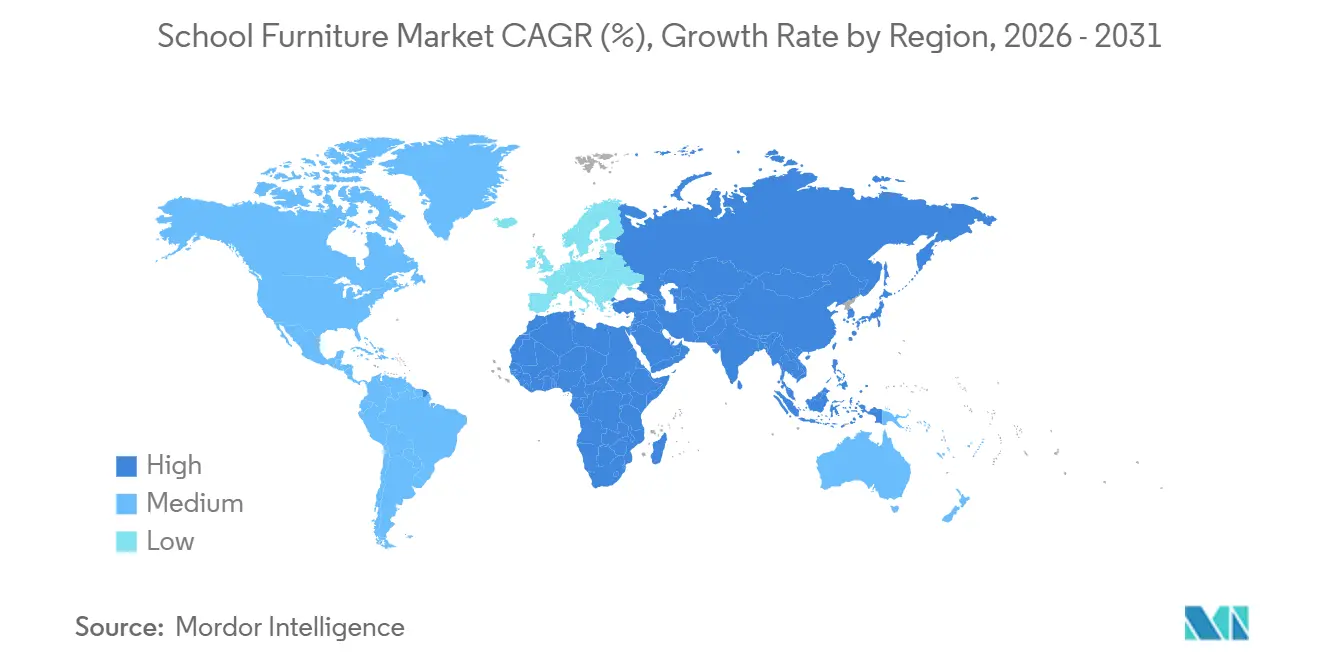

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

School Furniture Market Analysis by Mordor Intelligence

The School Furniture Market size is expected to grow from USD 6.65 billion in 2025 to USD 7.06 billion in 2026 and is forecast to reach USD 9.97 billion by 2031 at 7.16% CAGR over 2026-2031. Growth is anchored in long-cycle institutional demand, capital programs that prioritize learning environments, and continued emphasis on flexible and ergonomic classrooms suited to project-based pedagogy. Procurement specifications now routinely reference standards such as BIFMA X6.1 and GREENGUARD Gold, which are shaping vendor qualification and product development roadmaps for education-focused lines across geographies. Digital device deployment in schools is prompting demand for integrated power and charging, leading institutions to adopt carts, towers, and power-integrated desks that maintain instructional continuity without electrical retrofits. Parallel investments by multilateral agencies in India and Southeast Asia are accelerating laboratory modernization and classroom additions, reinforcing multi-year visibility for the school furniture market across emerging and mature systems.

Key Report Takeaways

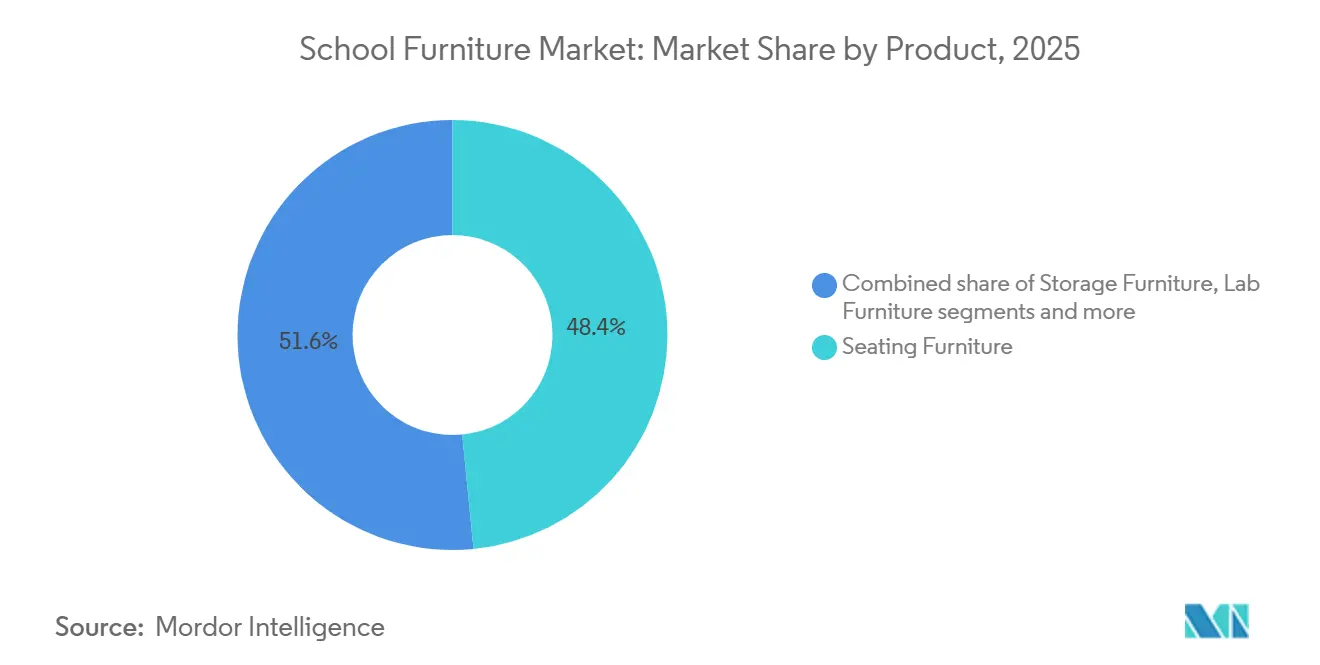

- By product, seating furniture led with 48.44% of the school furniture market size in 2025, and lab furniture is projected to grow at an 8.17% CAGR through 2031.

- By material, wood held 41.64% of the school furniture market share in 2025, and plastic and polymer derivatives are expected to grow at an 8.38% rate through 2031.

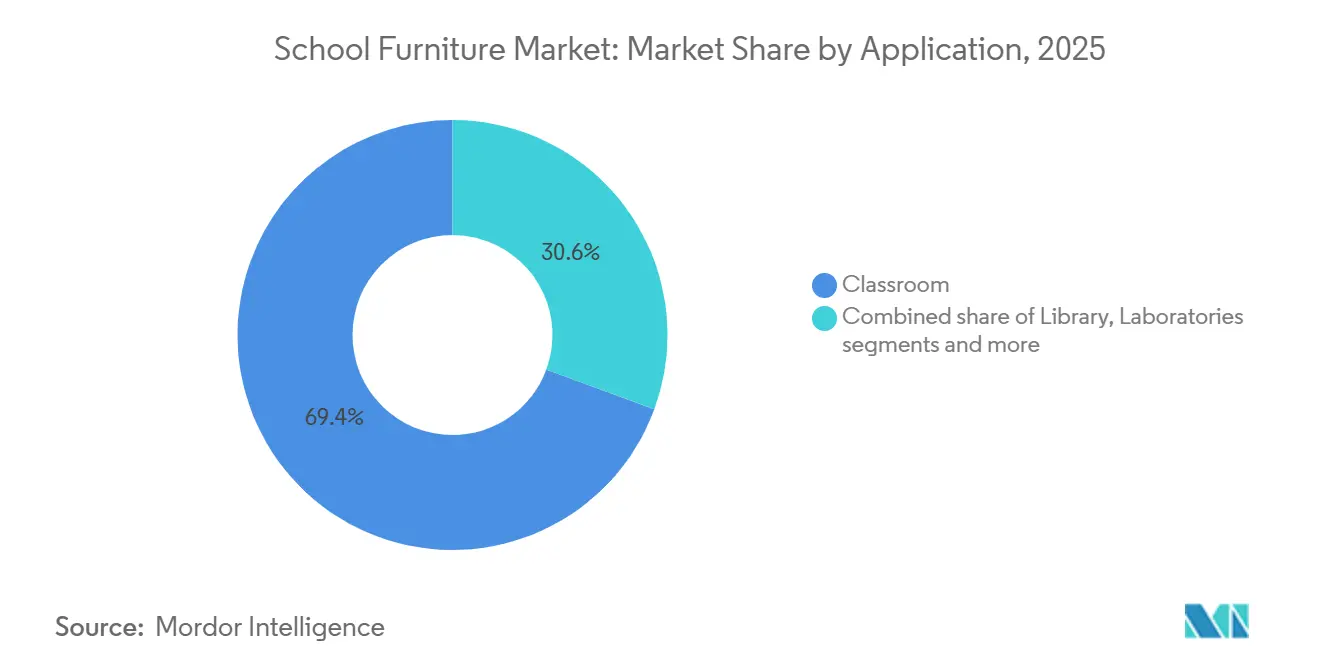

- By application, classrooms accounted for 69.36% of the school furniture market share in 2025, and laboratories are poised to expand at a 9.24% rate through 2031.

- By distribution channel, offline captured 38.33% of the school furniture market share in 2025, and online channels are projected to scale at a 10.39% growth rate through 2031.

- By geography, North America led with 49.37% of the school furniture market share in 2025, and Asia-Pacific is projected to record a 9.73% growth rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global School Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible Learning Pedagogies Driving Modular Furniture Demand | + 1.8% | Global, with early gains in North America, Europe, and Australia | Medium term (2-4 years) |

| Large-scale government stimulus and multilateral funding | + 2.1% | Asia-Pacific core, spill-over to Latin America, and the Middle East & Africa | Short term (≤ 2 years) |

| Heightened focus on ergonomics and student well-being | + 1.5% | Global, particularly Scandinavia, North America, and urban Asia | Medium term (2-4 years) |

| Proliferation of 1-to-1 device programs and power needs | + 1.3% | Global | Short term (≤ 2 years) |

| Sustainability and circular-economy mandates | + 0.9% | Europe & North America | Long term (≥ 4 years) |

| Integration of AI and adaptive learning technologies | + 1.7% | Global, with early adoption in North America, Europe, and East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flexible Learning Pedagogies Driving Modular Furniture Demand

Flexible, project-based teaching models are reshaping purchasing behavior by elevating modularity, tool-free reconfiguration, and storage-efficient designs as core specifications in K-12 and higher education bids. Institutions continue to engage learning-focused partners to design settings that support lecture, breakout, and hybrid activities in the same footprint, reinforcing the resilience of the school furniture market as administrators seek classroom agility. Standards bodies and procurement agencies reinforce durability and safety by referencing BIFMA X6.1 for educational seating and related categories, raising the threshold for performance and lifecycle expectations in public tenders. Product launches for 2025 underscore the shift toward active-learning ergonomics and rapid reconfiguration, including sit-stand, nesting, and motion-friendly formats designed for quick transitions between teaching modes. Higher education pilots in modular classrooms also reinforce a design language flowing back to K-12, sustaining the school furniture market's orientation toward flexible layouts that scale from primary to advanced programs.

Government and Multilateral Funding Unlocking Infrastructure Capital

Dedicated capital programs and multilateral finance are expanding classroom capacity and modernizing laboratories, which sustain near-term installation cycles and broaden multi-year visibility. The Asian Development Bank (ADB) approved three projects totaling USD 381 million in December 2025 to modernize agriculture, strengthen STEM education, and improve healthcare in Pakistan’s Punjab province. The funding includes concessional loans and grants for climate‑resilient, low‑carbon farm mechanization benefiting 220,000 rural households, expanded secondary education access, and nursing workforce reforms with new training facilities, simulation labs, and digital systems to enhance human capital and livelihoods. [1]Asian Development Bank, “ADB Approves $381 Million Financing to Modernize Agriculture Education and Health Services in Punjab,” Asian Development Bank, adb.org. The World Bank’s RIGHT+ framework guides education investment in resilient, inclusive, green, healthy, and teaching & learning conducive physical learning environments (PLEs), emphasizing how quality school infrastructure from classrooms to networks of facilities boosts learning outcomes, supports climate resilience, and addresses global education gaps. It promotes strategic planning, safety, sustainability, accessibility, and effective implementation to enhance education systems, especially in vulnerable regions. [2]World Bank, “RIGHT+ Framework for Physical Learning Environments: Maximizing Investment Impact in Education Spaces and Facilities,” World Bank, worldbank.org.

Ergonomic Design and Student Well-Being Becoming Procurement Mandates

Districts and agencies are embedding ergonomics and height-adjustability into procurement to improve comfort, attention, and inclusive access across learning stages. Consistent references to BIFMA X6.1 performance standards and institutional safety requirements ensure minimum load, stability, and lifecycle thresholds suitable for K-12 and higher education deployment. University procurement standards also reinforce durability and safety in product selection, creating convergence in specifications that benefit the broader school furniture market. Active seating and sit-stand formats have widened adoption as suppliers launch motion-friendly seating and nesting tables that align with evolving classroom layouts. Indoor air quality prerequisites have become common, with GREENGUARD Gold and similar certifications appearing alongside furniture layout and wellness criteria in state and district guidelines, strengthening the compliance profile favored in tenders.

Digital Device Programs Necessitating Power-Integrated Furniture

The expansion of school-issued devices has elevated reliable power access from convenience to requirement, which has expanded demand for carts, towers, and power-ready desks that maintain uptime without costly electrical work. Charging systems optimized for classroom use provide faster and more consistent power delivery, with USB-C-based solutions documented to shorten charge cycles and reduce replacement of AC adapters and cables. Districts are standardizing mobile charging carts that support classroom autonomy and reduce disruptions caused by low-battery devices. The trend extends to furniture-integrated power access for reconfigurable spaces, where manufacturers have introduced mobile power solutions that allow flexible layouts without reliance on fixed outlets. Procurement guidelines now pair low-emission materials with technology functionality, which concentrates vendor evaluation around performance, safety, indoor air quality, and device support in one framework that supports the school furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent volatility in key raw materials | - 0.9% | Global, with higher relevance in supply-chain-constrained regions | Medium term (2-4 years) |

| Geopolitical trade barriers and shipping-capacity crunches | - 0.7% | North America, Europe | Medium term (2-4 years) |

| Budget reallocation toward ed-tech and connectivity | - 0.5% | High-income markets, particularly North America | Short term (≤ 2 years) |

| Limited skilled workforce for EdTech implementation | - 0.6% | Global, especially in emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility Compressing Margins and Project Feasibility

Fluctuations in the prices of steel, lumber, and resin inputs continue to disrupt procurement planning and pricing stability, prompting manufacturers to shorten quote-validity periods and revise list prices more frequently. Ongoing trade measures affecting softwood lumber add uncertainty to cross-border supply, complicating cost assumptions for school furniture tenders and contract execution. Because school districts typically approve capital budgets on multi-year cycles, mid-cycle material surcharges can trigger scope revisions or project delays, shifting deliveries into later fiscal periods and altering backlog visibility. In response, suppliers increasingly offer pre-build or pre-pricing programs that lock in costs earlier when product configurations are standardized, helping protect district budgets when early funding commitments are feasible. At the same time, formaldehyde and emissions standards embedded in public procurement guidelines raise the compliance baseline for composite wood products, increasing material and testing costs while reinforcing health and safety requirements in educational environments.

Trade Barriers and Shipping Disruptions Inflating Landed Costs

Trade-remedy actions and evolving tariff regimes continue to increase costs and planning complexity for school furniture incorporating steel frames and related inputs, particularly across North America. Canada’s imposition of a 25% tariff on certain steel derivative products directly impacts metal-frame seating and other core school furniture categories, prompting manufacturers to reassess sourcing strategies. At the same time, shifts in United States tariff policy require exporters and importers to maintain contingency plans for both components and finished goods, adding operational uncertainty. Persistent softwood lumber duties on Canadian producers further compound cost pressures for North American buyers. Together, these factors contribute to greater volatility in landed costs, influencing bid pricing, procurement timelines, and regional production and capacity planning within the school furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Seating Dominates, Lab Furniture Surges on STEM Push

Seating furniture captured 48.44% of the school furniture market share in 2025, as every learning environment requires chairs and stools in large volumes across grades and use cases. Lab furniture is the fastest-growing product group with an 8.17% CAGR through 2031, reflecting a steady expansion of STEM facilities and maker-space programs that require specialized benching, storage, and easy-to-clean, chemical-resistant surfaces. Manufacturers are updating lab solutions to include integrated power and durable tops while enabling reconfiguration to align with blended theory-and-practice formats, a move visible in education-focused showcases across North America. Design emphasis within seating continues to shift toward motion-friendly and nestable formats that support quick transitions, while preserving durability standards set by education-specific protocols. As more institutions standardize on flexible layouts, the school furniture market sees growing demand for tool-free assembly and storage-efficient seating that reduces the space burden when rooms are reconfigured.

The fastest-growing lab category is also lifted by public investment in science education, where multilateral programs explicitly fund laboratory upgrades that require aligned furnishings and fixtures. In Pakistan’s Punjab province, ADB financing for 100 schools aligns budgets to both classroom and laboratory upgrades, reinforcing multi-year demand for science-ready furniture at the district scale. Seating remains under margin pressure due to input costs and discounting on large projects, which encourages process improvements and disciplined product line management under public tender conditions. District guidelines increasingly consider movable storage and mobile whiteboards instead of built-in casework, facilitating space repurposing while aligning capital stewardship to evolving program needs. Specification language favoring low-emission furniture has become more common, raising demand for certified seating and surfaces across K-12, which reinforces vendor differentiation in the school furniture market.

By Material: Wood Leads, Polymers Gain on Circular-Economy Tailwinds

Wood remained the largest material category, accounting for 41.64% of the market size in 2025, while plastics and polymer derivatives are on an 8.38% annual growth path through 2031, reflecting updated specifications and circular content expectations. Policy actions affecting metals, especially steel derivatives used in frames and lab structures, are contributing to hybrid constructions that reduce metal tonnage and support compliance. Furniture producers and their suppliers are investing in circular material flows that emphasize recycled content and repeatable processes, with some brands quantifying annual diversion of waste through closed-loop programs. Design for circularity also influences portfolio decisions on polymer-based seating, where product icons have transitioned to post-consumer resins, offering a visible signal of recyclability priorities in public tenders. European sustainability requirements, including digital product passports and recycled content thresholds, are also prompting education-focused portfolios to document material provenance and end-of-life handling, aligning with institutional buying criteria.

Across wood, metal, and polymer families, the school furniture industry continues to optimize for durability, maintenance, and ease of reconfiguration so classrooms can support changing lesson formats throughout the day. As compliance for low-emission composite wood is more consistently enforced in public-sector guidelines, product line engineering for panels and tops incorporates adhesives and substrates that meet formaldehyde and VOC expectations for sensitive environments. Hybrid wood-metal designs and mono-material polymer shells both play roles in addressing lifecycle and recyclability expectations while ensuring classroom safety remains paramount in procurement scoring. The move toward end-to-end transparency is also visible in remanufacture and reuse programs that revalidate product safety and warranty coverage after refurbishment, which broadens acceptable options in capital and sustainability plans. In this context, the school furniture market benefits from product families designed for disassembly, consistent parts, and serviceability that keep learning environments productive and compliant.

By Application: Classrooms Command Share, Laboratories Drive Growth

Classroom installations represented 69.36% of the school furniture market size in 2025, and laboratories are on a 9.24% growth trajectory to 2031 as hands-on science becomes central to learning outcomes. Library programs are shifting toward learning commons with multi-zone layouts, which expand demand for modular seating, mobile partitions, and light reconfiguration to support collaboration as well as quiet study. Funding policies that prioritize science and technology facilities reinforce laboratory upgrades and specialized furnishing needs, from surfaces to integrated power and storage aligned to program safety. Procurement documents are also layering indoor air quality and ergonomics alongside function and maintenance, which raises the weight of certifications in evaluations for classroom and lab settings. As a result, the school furniture market continues to add reconfigurable and mobile elements to each application type, supporting modern pedagogy without structural alterations.

Classrooms remain the anchor of demand but now require differentiated layouts across elementary, secondary, and higher education, with the latter adding hybrid lecture and breakout capabilities in the same room. Districts are specifying sit-stand options and inclusive seating to support educator wellness and broader access needs in administrative and faculty settings, which expands the application mix beyond classrooms. Capital plans for large districts include furniture alongside construction programs, aligning refresh cycles with building timelines to optimize procurement and installation windows. Acoustic controls are increasingly integrated in space planning to mitigate noise in open and semi-open layouts, aligning with indoor environmental quality goals already embedded in public guidelines. These shifts continue to inform vendor portfolios and strengthen the school furniture market’s alignment with learning outcomes across age groups and building typologies.

By Distribution Channel: Offline Holds Ground, Online Surges with E-Procurement

Offline channels retained 38.33% of activity in 2025, led by direct institutional tenders that specify compliance and performance standards, while online channels are expanding at a 10.39% growth pace as districts digitize purchasing. Public tenders tend to favor proven compliance with BIFMA and similar benchmarks, which strengthens the position of established education suppliers and contract dealers who can deliver full-scope projects. Offline dealers increasingly differentiate through planning, installation, and post-sale services at campus scale, positioning their expertise as a value premium over pure-play online channels for complex projects. Schools are also adopting vendor portals and configuration tools that shorten quote and fulfillment cycles for standardized items and charging systems, which support faster deployments and reduce out-of-service time. At the same time, procurement guidelines emphasize safety and indoor air quality along with functional performance regardless of channel, narrowing acceptable offerings and keeping the school furniture market focused on certified, education-ready options.

Institutional clients continue to use online marketplaces for replenishment and accessories while routing large, multi-building projects to offline tender processes where on-site services are critical. Manufacturers that maintain domestic assembly, integrated logistics, and education-specific support enjoy an advantage in meeting scheduling and service-level requirements typical of public-sector contracts. Recent consolidation that combines complementary dealer networks and product lines further supports service density and bid competitiveness across regions, with implications for both channel strategies and product availability. Online configurators and standards-based templates also reduce errors and rework in order processing, an operational improvement that aligns with district accountability expectations. These dynamics enable a hybrid channel model where offline partners lead complex installations and online tools support speed and standardization, collectively reinforcing the school furniture market.

Geography Analysis

North America accounted for 49.37% of the school furniture market size in 2025, underscoring a large installed base and consistent capital programming that funds learning environment upgrades on multi-year cycles. Large districts align furniture acquisitions to long-range capital frameworks that include modernization and capacity expansions, stabilizing procurement for education-focused products during each plan horizon. Canadian provincial budgets continue to prioritize school infrastructure investment, with British Columbia planning substantial multi-year funding for K–12 projects. These allocations focus on seismic upgrades, capacity expansions, and modernization initiatives, which are expected to translate into sustained demand for school furniture through ongoing public tenders and refurbishment programs. Trade measures in Canada that target steel derivative products continue to reshape sourcing choices for metal-frame items, supporting the case for diversified supply and local assembly for education customers. Procurement policies within the United States emphasize health and sustainability standards and encourage vendors to document compliance at the point of bid, reinforcing consistent criteria for K-12 purchases across the region.

Asia-Pacific is the fastest-growing region at a 9.73% rate through 2031, supported by new school construction, modernization programs, and broad public investment that expands classroom and laboratory capacity. In Pakistan’s Punjab province, ADB-backed upgrades to 100 schools include both classroom and laboratory improvements, which support standardized purchases at scale and structured delivery timelines. Southeast Asia is also in focus, where World Bank financing for Cambodia is funding more than 900 new classrooms that will require furnishings, teacher work areas, and student desks aligned to inclusive access and WASH improvements. Complementary ADB programs are upgrading technical schools, including disaster-resilient features and modern facilities that will be furnished and equipped during installation phases. These projects focus on resilience, health, and inclusive design standards that mirror international best practices, which helps the school furniture market converge to common specifications across the region.

Europe and other regions reflect heterogeneous patterns shaped by policy, sustainability rules, and capital availability for education assets, and these factors frame multi-year procurement strategies. European buyers anticipate expanded documentation and product transparency, including digital product passports and end-of-life pathways, raising the bar for market participation and supply chain disclosures. Scandinavian practice is widely cited for ergonomics and student wellness orientation, which continues to influence specifications and supplier portfolios across the continent. In the Middle East and other high-investment geographies, new school campuses often call for international-standard furniture and full-scope project management, which concentrates awards with suppliers able to offer integrated delivery. These policies and capital conditions sustain a focused opportunity set for vendors that specialize in education spaces, thereby supporting the school furniture market across policy-driven and growth-oriented regions.

Value Chain Analysis

The value chain begins with upstream inputs, including hardwood and engineered wood panels, steel and aluminum for frames, plastic and polymer resins for shells and edge-banding, and adhesives and finishes that must meet low-emission requirements embedded in school procurement. Component fabrication and sub-assemblies (metal tube and frames, molded shells, laminate or composite tops, casters and glides, and integrated power and charging modules for device programs) feed into OEM and contract manufacturing operations that emphasize durability testing, safety, and documentation aligned with specifications that frequently cite education-relevant standards such as BIFMA X6.1 and indoor air quality certifications such as GREENGUARD Gold.

Midstream activity is driven by education-focused manufacturers and integrated project providers that package design, quoting, and installation into bid-ready offers for districts and universities. Distribution is dominated by offline channels, including contract furniture dealers and specialist education dealers, supported by cooperative purchasing and multi-award contracting that aggregates demand and simplifies buying for public entities. ODP Business Solutions joining a multi-year, multi-award furniture partnership with Region 4 Education Service Center in February 2025 expanded access to furniture and installation services through a large cooperative structure. Downstream, buyers include public school districts, private schools, and higher education institutions that manage multi-layered tenders, site surveys, phased summer installations, and after-sales service for maintenance and replacement parts. Key bottlenecks include raw material price volatility (steel, lumber, and resins) and trade measures affecting landed costs for metal-frame categories, which prompt suppliers to pursue dual sourcing, domestic assembly, and more standardized configurations to lock pricing earlier in the procurement cycle.

Competitive Landscape

The school furniture market remains fragmented, reflected by a moderate market concentration score that indicates a wide field of qualified education-focused suppliers alongside selective consolidation. Recent mergers and partnerships have improved scale for leading players, yet the combined share of top companies remains well below levels associated with high concentration. Consolidation is primarily aligning complementary learning-oriented brands and dealer networks, expanding geographic reach and service consistency across K–12 and higher education. Vertically integrated manufacturers are emphasizing domestic assembly and education-specific operations to meet public-sector service requirements and manage schedule-driven projects. At the same time, evolving trade policies related to steel and derivative products are prompting sourcing adjustments and design optimization across core furniture categories.

Product differentiation in the school furniture market centers on flexibility, active seating, and integrated technology that support multiple learning modes. Classrooms increasingly require furniture systems that can transition easily between lectures, collaboration, and independent study. Charging and power infrastructure has emerged as a key competitive differentiator, with education-optimized solutions reducing device downtime and simplifying IT support. Sustainability has also become a decisive factor in procurement, driving manufacturers to invest in circular design, remanufacturing, and reuse programs that maintain performance and warranties. Broader ESG commitments, including renewable energy use and landfill diversion, are now commonly disclosed and aligned with institutional purchasing criteria.

Dealers continue to play a critical role by coordinating planning, phasing, and installation for complex, multi-building education projects in close partnership with manufacturers. Their involvement helps districts manage timelines, budgets, and operational continuity during large-scale upgrades. At the same time, digital tools such as online configurators and standardized ordering templates are improving quote accuracy and shortening build-to-order cycles for common products. Leading brands are increasingly anchoring growth strategies around education-specific portfolios, compliance-ready documentation, and circular design principles. Together, these trends are raising expectations for service quality, sustainability, and compliance, supporting ongoing consolidation while preserving strong competition across specialized segments of the school furniture market.

School Furniture Industry Leaders

Virco Mfg. Corp.

MillerKnoll Inc.

KI Furniture

HNI Corp.

Haworth Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity lies in scaling fulfillment for large, standardized orders tied to school construction and refurbishment programs, especially where multilateral and government funding is translating into new classrooms and laboratory upgrades. Projects such as the Asian Development Bank approvals totaling USD 381 million in December 2025 for Punjab province (including expanded secondary education access and new training facilities and labs) and the World Bank-backed classroom construction programs in Southeast Asia create repeatable furnishing needs that favor suppliers with documented compliance, fast lead times, and installation capacity. Vendors that can offer lab-ready and classroom-ready packages, including chemical-resistant surfaces, storage, and integrated power for devices, can align bids to these funded project scopes while meeting health and durability requirements referenced in procurement specifications.

A second opportunity centers on technology-enabled, compliance-ready product and production capability that reduces total installed disruption for schools. Power-integrated desks, mobile charging carts, and reconfigurable active-learning layouts drive demand for manufacturers that treat charging, cable management, and serviceability as standard options rather than custom add-ons. On the supply side, capacity and automation investments point to room for scaled, cost-competitive production targeted at education orders, including Liserve operationalizing a 53,000-square-meter smart factory in Henan Province in April 2026 with automated lines and ABB industrial robots designed for high unit output. Procurement rigor around emissions and materials transparency, including GREENGUARD Gold alongside broader chemical restrictions such as REACH, also creates demand for complete submittal packages (VOC, formaldehyde, fire safety, lifecycle testing) as well as refurbishment or reuse programs that keep products in service longer while retaining safety and warranty coverage.

Recent Industry Developments

- June 2026: MillerKnoll, Inc. reported fourth quarter and full fiscal year 2026 results for the year ended May 30, 2026, reflecting performance in its contract-focused operations that supply furniture into institutional environments, including education. The update highlights how large contract players use shared manufacturing and dealer networks across office, healthcare, and education categories, increasing competitive pressure on education-only suppliers to match service levels and compliance documentation.

- May 2026: KI opened a new Inspiration Center at 1045 W. Fulton Street in Chicago and debuted its Cognetic Technology platform for seating. The expanded showroom and technology positioning strengthens front-end specification activity with architects, dealers, and institutional buyers, supporting higher-value selling around ergonomics and user performance rather than commodity seating alone.

- December 2024: MillerKnoll announced elimination of PFAS from its North American brand portfolio of products. The update aligns with tightening chemical management expectations in institutional procurement and supports vendor differentiation where schools and universities increasingly score bids on indoor environmental quality and materials stewardship alongside price and durability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers school furniture that is purchased and used inside K-12 schools and higher education settings for learning and support areas, measured in revenue terms. The scope includes core items used in classrooms, libraries, and labs, where demand is linked to enrollment, education budgets, and refurbishment cycles.

Scope exclusions: Furniture mainly meant for homes or general offices, along with building construction works and stand-alone interior design services, are not counted in this market.

Segmentation Overview

- By Product

- Seating Furniture

- Storage Furniture

- Lab Furniture

- Other Products (Podiums, Whiteboards, Notice Boards)

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Material

- By Application

- Classroom

- Library

- Laboratories

- Others (Administrative & Faculty Offices, Outdoor & Common Areas, etc.)

- By Distribution Channel

- Offline

- Direct Institutional Tenders

- Retail & Specialist Dealers

- Contract Furniture Dealers

- Online

- Company Direct E-Commerce

- Third-Party Marketplaces

- Offline

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Aisa-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the starting demand picture and to avoid guessing on how many learning spaces are being added or upgraded each year. We review public education spending and enrollment series, along with procurement and standards signals that influence buying behavior and replacement timing.

Common inputs include official education statistics (such as UNESCO Institute for Statistics and national education departments), macro indicators from the World Bank and OECD, and trade and shipment clues from UN Comtrade and national customs portals. We also scan non-paywalled standards and guidance material from bodies such as BIFMA, plus public tenders, school district procurement notices, and manufacturer filings and investor updates. When needed, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import-export data help cross-check supplier exposure and product mix trends. These desk sources are illustrative and not exhaustive, and many other references are used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to sanity-check what the desk signals imply about actual buying cycles, price movements, and the practical split between seating, storage, and lab setups. We speak with a mix of manufacturers, distributors, institutional buyers, and channel specialists across key regions so assumptions on procurement lead times, product replacement triggers, and online versus offline ordering behavior are confirmed and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 18% | Managers: 44% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where education infrastructure activity and demand pools are reconstructed from enrollment levels, classroom additions, and refurbishment intensity, then converted into furniture spend using observed procurement patterns. After the total is formed, we corroborate it with selective bottom-up checks such as sampled average selling prices for desks, chairs, and storage items, plus channel checks on order volumes and mix. If gaps show up, we adjust the totals accordingly.

Inputs that matter most for school furniture include student enrollment growth, public and private education capex and opex budgets, new school openings and classroom counts, replacement cycles for seating and desks, the share of lab and library upgrades, and typical material shifts that affect pricing. In forecasting, scenario analysis is used so budget tightening, policy-led infrastructure pushes, and inflation-driven price resets can be reflected without forcing a single straight-line outcome. Where bottom-up inputs are incomplete for smaller countries or fragmented channels, we use regional benchmarks tied to enrollment and spend per student, followed by a fresh expert check.

Data Validation & Update Cycle

Validation happens in layers so the final numbers are not driven by one indicator. We compare model outputs against independent signals such as public procurement volumes, trade flows for relevant furniture categories, and reported revenue exposure from companies that sell into education. When a variance looks unusual, the assumptions behind pricing, replacement rates, or regional splits are reviewed again, and follow-up calls are triggered to confirm what changed.

Before sign-off, the model and its inputs go through peer review so unit logic, currency conversion timing, and year alignment are checked. The report is refreshed annually, and interim updates are made when material events occur, such as large policy programs or sharp raw material price moves. Right before delivery, a final analyst pass is done so clients receive the latest updated view.

Mordor Intelligence's School Furniture Market Estimate Compared With Other Published Estimates

It is normal to see different market sizes for school furniture, even when the titles look similar. The differences usually come from how researchers define the buying locations, whether lab and library furniture are treated as part of the same pool, and how prices are moved forward year by year.

By tracking procurement-led demand signals and refreshing scope boundaries, Mordor Intelligence keeps the sizing focused on education-use furniture across classroom, library, and laboratory settings. This tends to avoid adding adjacent furniture categories that are not consistently purchased through school budgets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.65 B (2025) | |

| Global Consultancy A | USD 4.66 B (2025) | This estimate appears to use a narrower revenue pool, which can happen when school furniture is counted mainly as core classroom items and a smaller share of lab, library, and other learning-area furniture is included. |

| Industry Publisher B | USD 4.75 B (2025) | The spread can be driven by different regional coverage and a different way of projecting price progression, especially if inflation pass-through is averaged broadly rather than checked against education procurement behavior. |

Across the three values, the main takeaway is that definition and conversion logic move the total more than small math differences do. Our approach stays traceable because demand is tied back to education activity indicators, and the final number is cross-checked with practical price and mix feedback before it is finalized for the year.

Key Questions Answered in the Report

What is the global school furniture market size and growth outlook to 2031?

The school furniture market size is USD 7.06 billion in 2026 and is projected to reach USD 9.97 billion by 2031 at a 7.16% CAGR.

Which product categories are leading and which are growing the fastest in school settings?

Seating led with a 48.44% share in 2025, while lab furniture is the fastest-growing category with an 8.17% CAGR through 2031.

How are materials trends evolving for classroom and lab furniture?

Wood held a 41.64% share in 2025, and plastics and polymer derivatives are growing at 8.38% annually, driven by circular content and durability requirements.

Which applications dominate spending in education, and where is growth strongest?

Classrooms accounted for 69.36% of installations in 2025, and laboratories are expected to grow at 9.24% through 2031.

Which region currently leads, and which region is expanding the fastest?

North America led with 49.37% in 2025, and Asia-Pacific is the fastest-growing region at a 9.73% rate through 2031.

How are procurement channels shifting for K-12 and higher education buyers?

Offline channels held 38.33% in 2025 due to full-scope projects, while online channels are expanding at 10.39% as e-procurement accelerates standard purchases.

Page last updated on: