Multi-Function Printers (MFP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

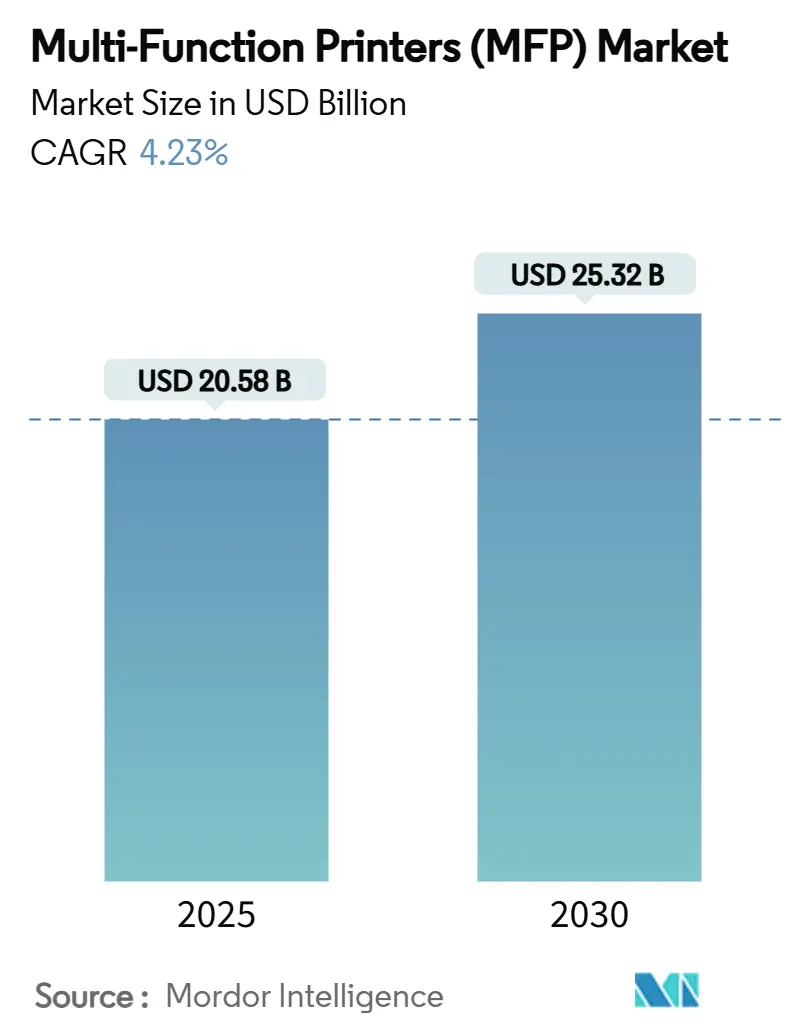

| Market Size (2025) | USD 20.58 Billion |

| Market Size (2030) | USD 25.32 Billion |

| Growth Rate (2025 - 2030) | 4.23% CAGR |

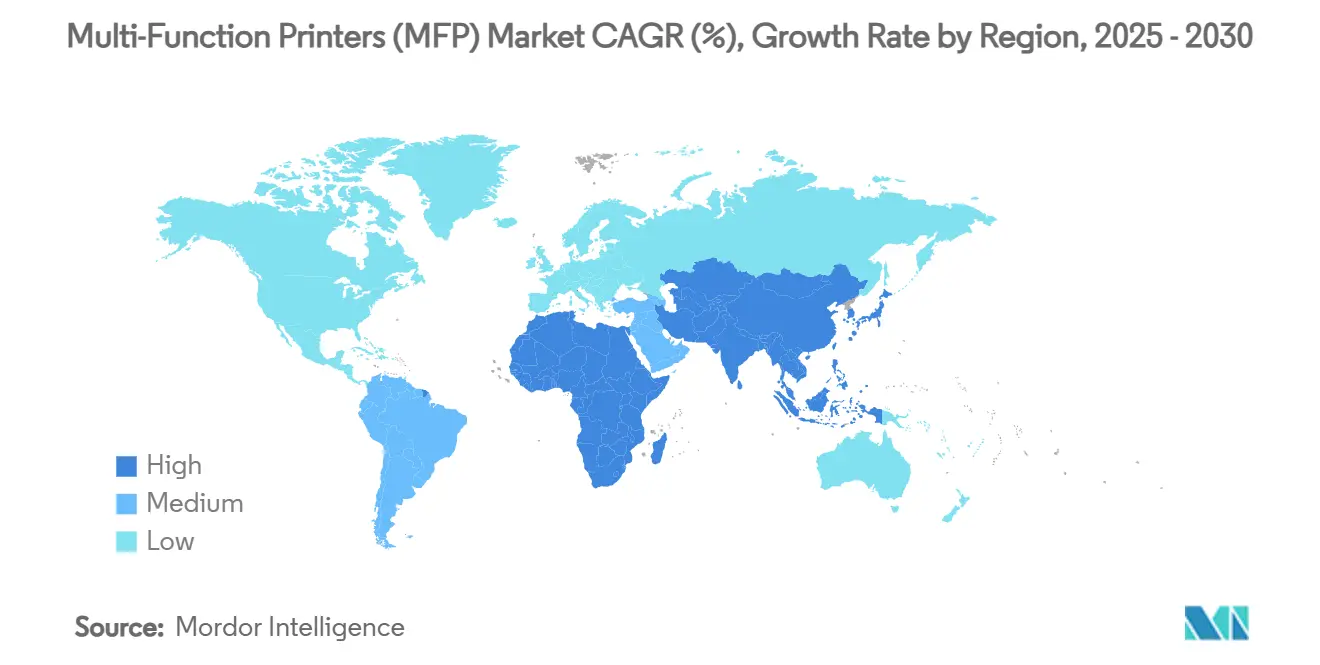

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

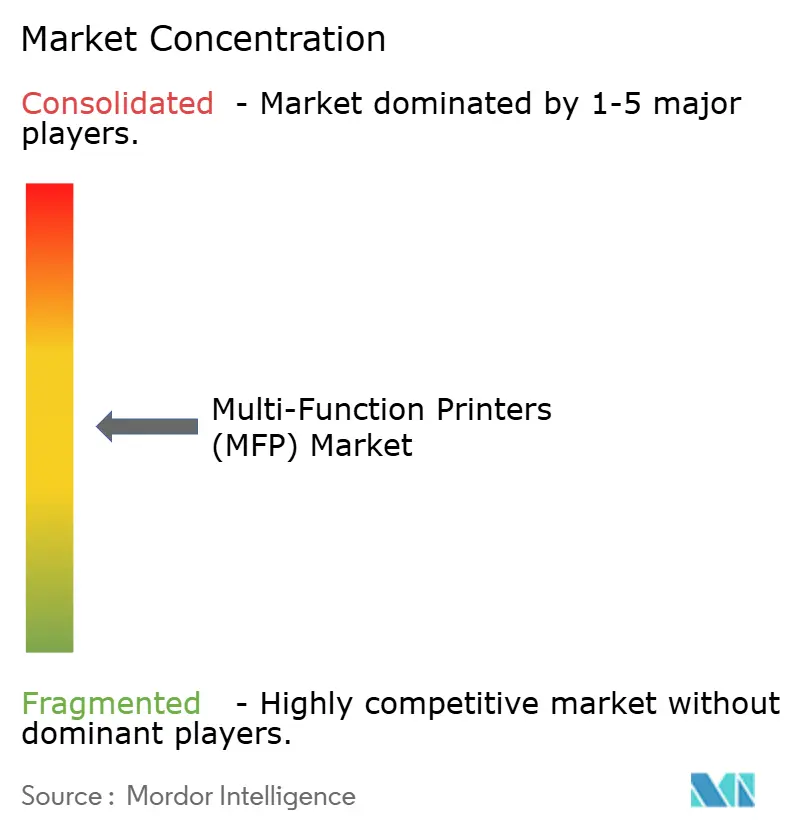

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Function Printers (MFP) Market Analysis by Mordor Intelligence

The Multi-Function Printers (MFP) market is valued at USD 20.58 billion in 2025 and, at a forecast CAGR of 4.23%, is set to reach USD 25.32 billion by 2030. Enterprise print strategies are recalibrating around hybrid-work realities, managed print services (MPS), and energy-efficient platforms. Compact office devices that can be centrally administered are moving to the top of procurement lists, while subscription-based MPS contracts anchor predictable spending. Technology migration to high-efficiency laser and ink-tank engines supports lower cost per page and smaller environmental footprints. Small and medium enterprises (SMEs) in emerging economies add an additional layer of demand as they formalize operations and digitize supply chains. Ongoing consolidation, illustrated by Xerox’s plan to acquire Lexmark, underscores a competitive landscape where scale and software capabilities matter more than raw hardware throughput.

Key Report Takeaways

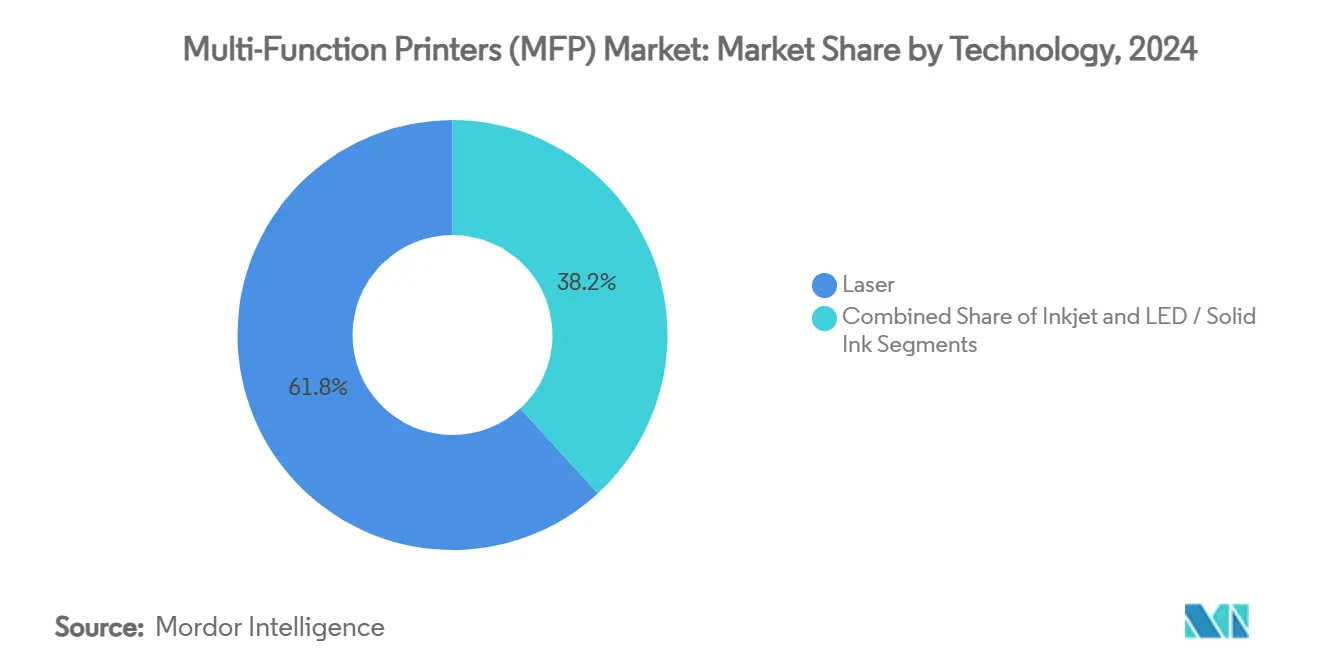

- By technology, laser devices held 61.83% share of the Multi-Function Printers (MFP) market in 2024.

- By form factor, A4 office models are projected to grow at 6.16% CAGR between 2025-2030.

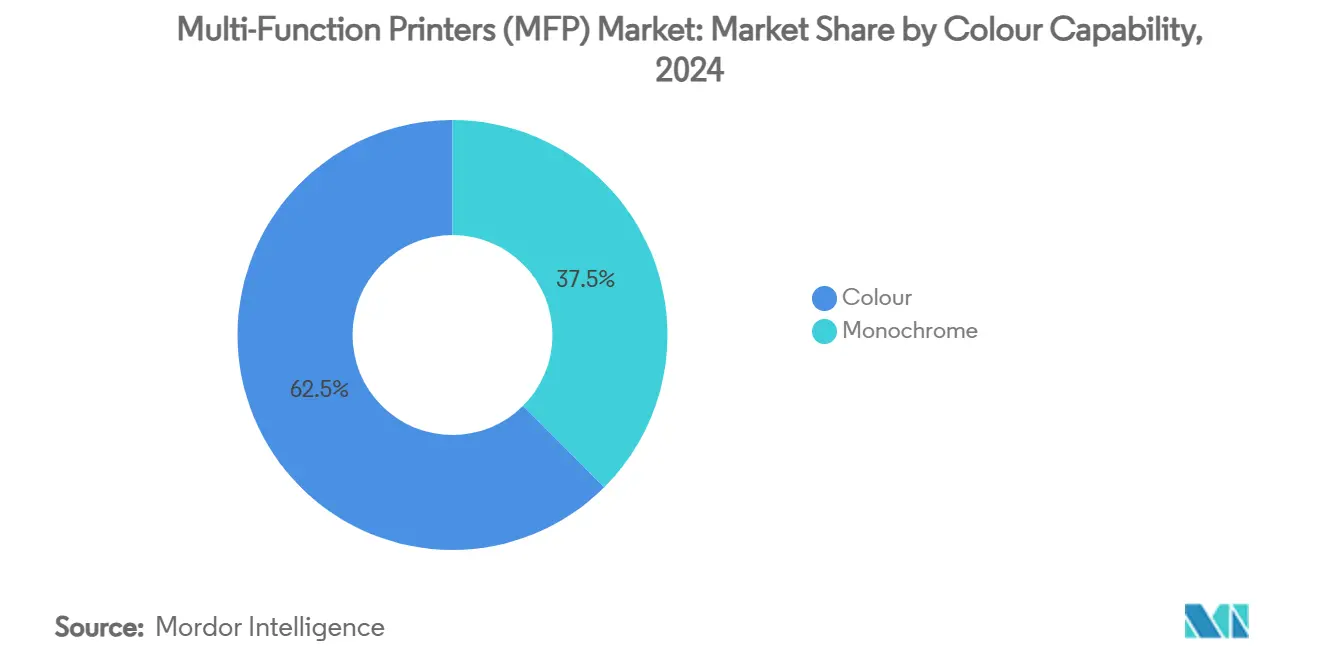

- By colour capability, colour units accounted for 62.47% share of the Multi-Function Printers (MFP) market size in 2024.

- By end-user industry, the Small and Medium Business segment contributed 35.48% of the Multi-Function Printers (MFP) market in 2024.

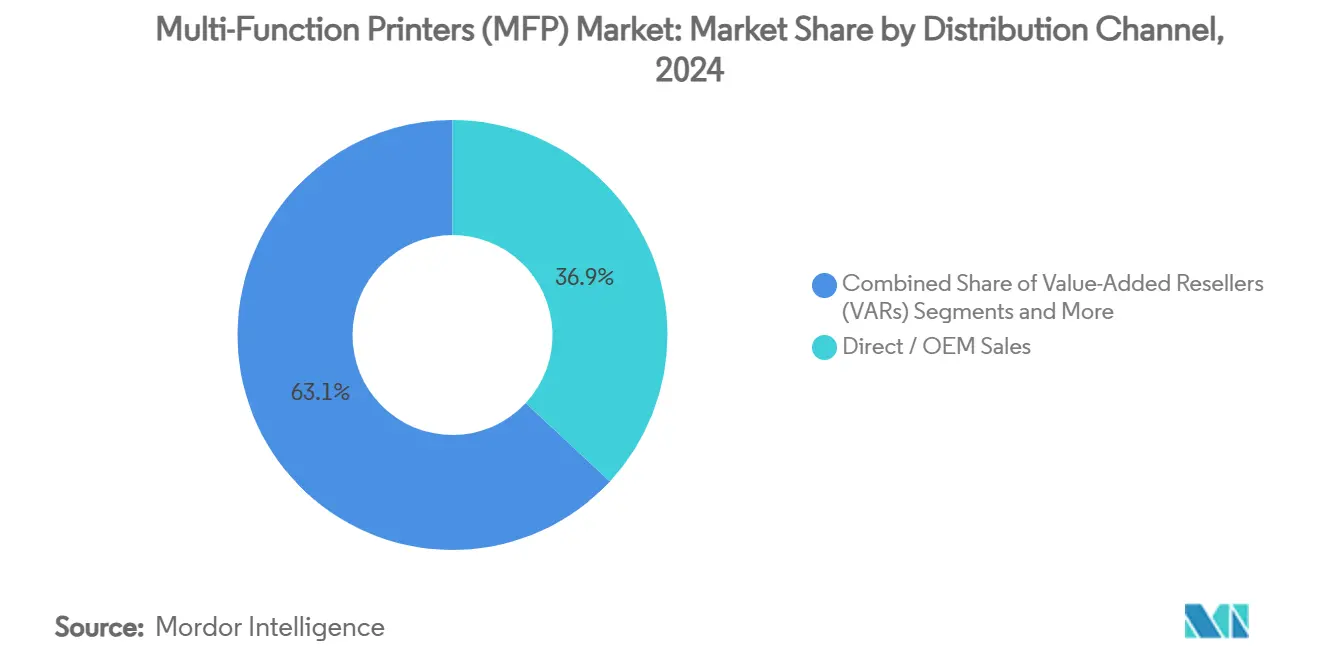

- By distribution channel, direct / OEM sales controlled 36.92% share of the Multi-Function Printers (MFP) market in 2024.

- By geography, Asia-Pacific is projected to grow at 6.17% CAGR between 2025-2030.

Global Multi-Function Printers (MFP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-work shift fuelling demand for compact office MFPs | 1.2% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| Rapid uptake of Managed Print Services (MPS) for cost and security | 0.9% | Global, APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Technology migration to high-efficiency laser and ink-tank platforms | 0.8% | Global | Medium term (2-4 years) |

| SME expansion in emerging markets needing entry-level MFPs | 1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-embedded "smart" MFPs automating document workflows | 0.7% | Global | Long term (≥ 4 years) |

| Circular-economy pull for remanufactured / refurbished MFPs | 0.4% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid-work shift fuelling demand for compact office MFPs

Enterprises now spread employees across corporate hubs, co-working spaces, and homes, so the Multi-Function Printers (MFP) market is pivoting to smaller A4 devices that fit easily under a desk yet remain network-manageable. Canon’s imageFORCE C7165, launched in October 2024, packs machine-learning features into a compact frame aimed squarely at hybrid environments. Ricoh’s IM C320F series follows the same path with a 7-inch panel and 50% post-consumer recycled plastic content.[1]Ricoh USA, “IM C320F Multifunction Printer Specifications,” ricoh.comSecurity has kept pace: HP’s quantum-resistant printers released in March 2025 embed ASIC chips to block future cryptographic threats.

Rapid uptake of Managed Print Services (MPS) for cost and security

Global MPS revenue is on a steep climb as organizations bundle hardware, supplies, and analytics into unified contracts that lower the total cost of ownership. Konica Minolta, a four-year Quocirca Leader, reports that 66% of clients cite cybersecurity and 64% cite AI as top investment priorities inside MPS engagements Konica Minolta.[2]Konica Minolta, “Konica Minolta Named Leader in Managed Print Services,” konicaminolta.comSoftware such as Printerpoint automates meter reads and invoicing, while Microsoft’s Windows Protected Print Mode, launched in October 2024, supports zero-trust print architectures.

SME expansion in emerging markets needing entry-level MFPs

MSMEs account for 98.7% of firms and 64.6% of jobs in developing Asia, so their hardware choices ripple through the Multi-Function Printers (MFP) market Asian Development Bank. The 2024 ASEAN SME Policy Index spotlights office automation as a cornerstone of post-COVID competitiveness. Canon generated USD 6.03 billion from Asia-Oceania sales in 2024, backing tailored low-price bundles to meet local budgets.

AI-embedded “smart” MFPs automating document workflows

Xerox’s AltaLink 8200 series, released in July 2024, uses onboard AI to summarise documents, convert handwriting, and redact sensitive data. HP’s Print AI suite adds Perfect Output for web pages and HP Scan AI for data extraction. Kyocera’s TASKalfa 3554ci supports predictive maintenance and handwriting recognition to curb downtime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating document digitisation cutting print volumes | -0.8% | Global | Short term (≤ 2 years) |

| Semiconductor and logistics bottlenecks inflating device cost | -0.6% | Global | Short term (≤ 2 years) |

| Shifts in device mix (A3 vs A4) | -0.3% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| OEM controls on supplies impacting aftermarket economics | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating document digitisation cutting print volumes

Paperless initiatives push more traffic into digital workflows, trimming page counts even as demand for secure scanning and cloud connectors expands. Microsoft’s driverless print approach drops legacy drivers entirely, reducing both attack surfaces and paper dependency.[3]Microsoft, “Introducing Windows Protected Print Mode,” microsoft.com Asian governments are funding digital literacy campaigns that discourage unnecessary printouts Asian Productivity Organization.

Semiconductor and logistics bottlenecks inflating device cost

Chip shortages have forced firmware redesigns: Epson now tracks ink levels through droplet counting rather than cartridge chips. Tariffs of up to 60% on imported printers risk adding inflationary pressure, so HP is relocating more than 90% of North American production outside China by fiscal 2025. A3 colour models saw average price jumps of 42% to 44% between Q1 2023 and Q4 2024, OpenBrand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Laser Dominance Amid Inkjet Acceleration

Laser engines generated 61.83% of the Multi-Function Printers (MFP) market share in 2024, underscoring entrenched preferences for durable, high-volume output. The segment’s installed base keeps toner ecosystems profitable, and service partners are familiar with maintenance cycles. Inkjet, however, is racing ahead at a 5.87% CAGR, powered by bulk-ink tanks and precision printheads that cut energy use. The Multi-Function Printers (MFP) market size for inkjet solutions is projected to climb sharply as Epson’s quadrupled printhead capacity reaches the channel by late 2025. Canon and Brother are meanwhile aligning roadmaps so clients can swap between laser and inkjet without retraining staff or renegotiating consumables contracts. Chip shortages have spurred both camps to strip out non-essential electronics, standardising boards and firmware to reclaim margin.

A second wave of efficiency is emerging via low-temperature fusing for laser and advanced micro-piezo heads for inkjet. These technologies shrink warm-up times, a non-trivial benefit when hybrid workers power-cycle devices more often. On the service side, predictive analytics pings technicians before a roller fails, prolonging duty cycles and locking in managed service renewals. As page volumes taper off in Europe, vendors are shifting their print-for-pay models toward analytics and process automation, ensuring that every printed page is either revenue-generating or value-adding.

By Form Factor: A4 Compact Solutions in the Spotlight

A4 devices commanded 68.28% of revenue in 2024 and are tracking a brisk 6.16% CAGR to 2030, a direct reflection of smaller office footprints and mobile work policies. The Multi-Function Printers (MFP) market size attached to A4 models is therefore expanding faster than the overall average, especially in North America, where floor space carries a premium. Portable units, once a niche, are now viable for field sales teams who need to print contracts on demand. Manufacturers are embedding full-colour touchscreens and NFC authentication even on sub-30 ppm models, ensuring consistent user experiences across fleets.

A3 machines still rule central reprographics rooms but manage flatter growth as departments decentralise. Some vendors are bridging the gap with “compact A3” devices offering A3 capability in chassis close to A4 dimensions, chasing verticals such as architecture and engineering. Light-production MFPs, in contrast, focus on print-on-demand booklets and in-store signage. They draw on the same software stack as office models, so operators can queue jobs from any workstation, reinforcing the platform effect now central to vendor strategy.

By Colour Capability: Colour Continues to Outpace Monochrome

Colour captured 62.47% of sales in 2024 and is riding a 6.05% CAGR, buoyed by richer marketing materials and falling toner price differentials. Where the cost gap persists, print policies route draft copies to monochrome and client-facing pages to colour, maximising asset utilisation. Production firmware now automates this routing based on metadata, removing the burden from end-users. The Multi-Function Printers (MFP) market finds additional headroom in sectors like education, where colour aids retention in digital textbooks and blended-learning materials.

Monochrome remains the workhorse for legal and government archives. Vendors reinforce this niche with secure-erase hard drives and tamper-resistant firmware, features initially born in colour flagships and later cascading down the line. Consolidation means R&D investments can service both colour and mono variants, allowing global giants to meet compliance requirements without inflating the bill of materials.

By End-User Industry: SMBs Dominate, Retail and Logistics Surge

SMBs held 35.48% of sales in 2024, confirming their central role in the Multi-Function Printers (MFP) market. These firms need affordable devices that scale with headcount rather than enterprise-grade behemoths. Subscription bundles that roll hardware, service, and supplies into a single monthly fee resonate strongly here. Retail and logistics is the growth champion at 5.94% CAGR as e-commerce warehouses print labels, invoices, and return slips in real time. The Multi-Function Printers (MFP) market size attributed to this vertical is swelling fastest in Southeast Asia, where cross-border fulfilment hubs proliferate.

Large enterprises, government, education, and healthcare continue to anchor global demand. Public-sector bids hinge on security certifications such as Common Criteria, pushing vendors to harden devices. Healthcare, for its part, leverages MFPs for integrated digitisation, scanning bar-coded patient files straight into electronic medical record (EMR) systems. New SoHo sub-segments emerged post-2024 when knowledge workers equipped home offices with near-enterprise features, a trend likely to stabilise but not retract.

By Distribution Channel: E-commerce Accelerates

Direct / OEM sales captured 36.92% of revenue in 2024, a legacy of large fleet deals and global framework agreements. E-commerce, however, is the channel to watch with a 6.09% CAGR. Buyers appreciate transparent pricing, next-day delivery, and click-to-configure leasing calculators. Meanwhile, value-added resellers pivot from box-moving to solutions integration, blending print fleets with digital workflow software. Retail storefronts keep a foothold by offering same-day pickup and demo units, critical for micro-businesses that cannot wait for shipping.

Vendor marketplaces blur the lines: HP’s online store, for example, lists refurbished “HP Renew” devices alongside new inventory, answering corporate sustainability targets while absorbing used-fleet returns. Distributors invest in automated warehouses and API-driven inventory feeds so resellers can promise tighter service-level agreements (SLAs). As tariffs and shipping delays roil international trade, proximity inventory becomes a competitive hedge, nudging even traditional channels to adopt omnichannel fulfilment tactics.

Geography Analysis

North America generated 33.24% of 2024 turnover on the strength of early hybrid-work adoption, mature managed print services penetration, and tight security requirements. Federal mandates, such as those prompting HP to launch quantum-resistant devices, guarantee premium hardware rotation. Regional reshoring plans are in motion to dampen tariff exposure, with HP pledging to move most assembly for the US market out of China by fiscal year 2025. While the United States dominates absolute volumes, Canada and Mexico supply incremental gains through seamless cross-border logistics under USMCA.

Asia-Pacific is the prime growth engine, charting a 6.17% CAGR. SMEs in Indonesia, Vietnam, and the Philippines are onboarding formal accounting systems that drive print demand. China’s incumbency in component manufacturing remains, yet diversification to India and Malaysia is underway to buffer geopolitical risk. Japan retains innovation leadership via Epson’s expanded printhead plant, due online by September 2025. Government grants that underwrite SME digitisation further inflate baseline demand in ASEAN economies.

Europe exhibits steady though slower expansion. The EU’s voluntary ecodesign agreement for imaging equipment claims energy savings of 10 TWh per year European Commission. Sustainability clauses in public procurement are steering buyers toward remanufactured gear, creating a circular-economy subplot in the Multi Function (MFP) Printers market. Ricoh’s new UK-based Ricoh Printing Solutions Europe Limited centralises industrial printing operations, bolstering regional customer support ahead of Brexit-related supply challenges Ricoh. Geopolitical tensions constrain Eastern-European prospects, but Germany and France stay resilient through automation grants to mid-cap manufacturers.

Competitive Landscape

Competition remains moderately concentrated as legacy imaging giants leverage scale and software ecosystems. HP Inc., Canon Inc., Seiko Epson Corp., Brother Industries Ltd., and Ricoh Company Ltd. collectively cover most price points from entry A4 to light-production A3. Xerox’s December 2024 decision to buy Lexmark for USD 1.5 billion will add 24,000 field technicians and deepen managed print services coverage in 170 countries. Ricoh and Toshiba Tec folded print operations into the ETRIA joint venture in July 2024, later joined by OKI in February 2025, pooling R&D and parts procurement to combat rising component costs.

Technology is the new battleground. Vendors infuse devices with AI for proactive maintenance and document intelligence, layering subscription software on top of hardware sales. Brother’s CS B2027 plan allocates about 200 billion yen for M&A to expand industrial printing and labelling. Sustainability also differentiates: Europe’s ecodesign rules reward manufacturers who offer certified remanufactured lines, an area where Canon’s “Green Edition” program re-markets returned devices with identical warranties.

Barriers for newcomers are high due to entrenched dealer networks and firmware security requirements. Niche entrants focus on single-function label or photo printers, leaving multifunction bread-and-butter volumes to established conglomerates. That said, component vendors in Taiwan and South Korea are supplying turnkey controller boards, hinting at potential white-label challengers that could unsettle low-end tiers if tariff scenarios alter cost structures.

Multi-Function Printers (MFP) Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corp.

Brother Industries Ltd.

Ricoh Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: OKI joined Ricoh and Toshiba Tec’s ETRIA joint venture for multifunction printer development and manufacturing, with Ricoh holding 80.74%, Toshiba Tec 14.25% and OKI 5.01%.

- October 2024: Ricoh established Ricoh Printing Solutions Europe Limited in Telford, UK, to consolidate industrial printing sales and support from April 2025.

- October 2024: Microsoft rolled out Windows Protected Print Mode, eliminating third-party drivers and embracing Mopria-certified hardware.

- July 2024: Xerox introduced the AI-enabled AltaLink 8200 Series, featuring document summarization and handwriting conversion.

- June 2024: Epson allocated 5.1 billion yen to expand inkjet printhead capacity in Sakata City, Japan, quadrupling output by September 2025 Epson.

- May 2024: Brother set a 1 trillion-yen revenue target under its CS B2027 strategy, earmarking 200 billion yen for growth investments.

Global Multi-Function Printers (MFP) Market Report Scope

| Laser |

| Inkjet |

| LED / Solid Ink |

| A4 Office MFP |

| A3 Office MFP |

| Portable / Compact MFP |

| Light-Production / Departmental MFP |

| Colour |

| Monochrome |

| Home Office / SoHo |

| Small and Medium Business |

| Large Enterprise |

| Government and Public Sector |

| Education |

| Healthcare |

| BFSI |

| Retail and Logistics |

| Direct / OEM Sales |

| Value-Added Resellers (VARs) |

| E-commerce / Online |

| Retail Stores |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | Laser | ||

| Inkjet | |||

| LED / Solid Ink | |||

| By Form Factor | A4 Office MFP | ||

| A3 Office MFP | |||

| Portable / Compact MFP | |||

| Light-Production / Departmental MFP | |||

| By Colour Capability | Colour | ||

| Monochrome | |||

| By End-User Industry | Home Office / SoHo | ||

| Small and Medium Business | |||

| Large Enterprise | |||

| Government and Public Sector | |||

| Education | |||

| Healthcare | |||

| BFSI | |||

| Retail and Logistics | |||

| By Distribution Channel | Direct / OEM Sales | ||

| Value-Added Resellers (VARs) | |||

| E-commerce / Online | |||

| Retail Stores | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Multi Function (MFP) Printers market?

The market stands at USD 20.58 billion in 2025 and is forecast to reach USD 25.32 billion by 2030.

Which technology segment dominates sales?

Laser devices command 61.83% of 2024 revenue, yet inkjet engines are growing faster at a 5.87% CAGR.

Why are A4 printers gaining ground over A3 models?

Hybrid-work policies and space constraints push buyers toward compact A4 units that still deliver enterprise-grade functions.

Which region is set for the fastest growth?

Asia-Pacific leads with a projected 6.17% CAGR through 2030, supported by rapid SME digitisation.

How are vendors differentiating products in a mature market?

Manufacturers embed AI for workflow automation, bolster security with quantum-resistant hardware and promote remanufactured devices to meet sustainability goals.

What impact do semiconductor shortages have on printer pricing?

Component scarcity and tariffs have lifted A3 colour prices by more than 40% since 2023, prompting firmware redesigns and regional supply-chain shifts.

Page last updated on: