Dips and Spreads Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 114.64 Billion |

| Market Size (2031) | USD 148.82 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

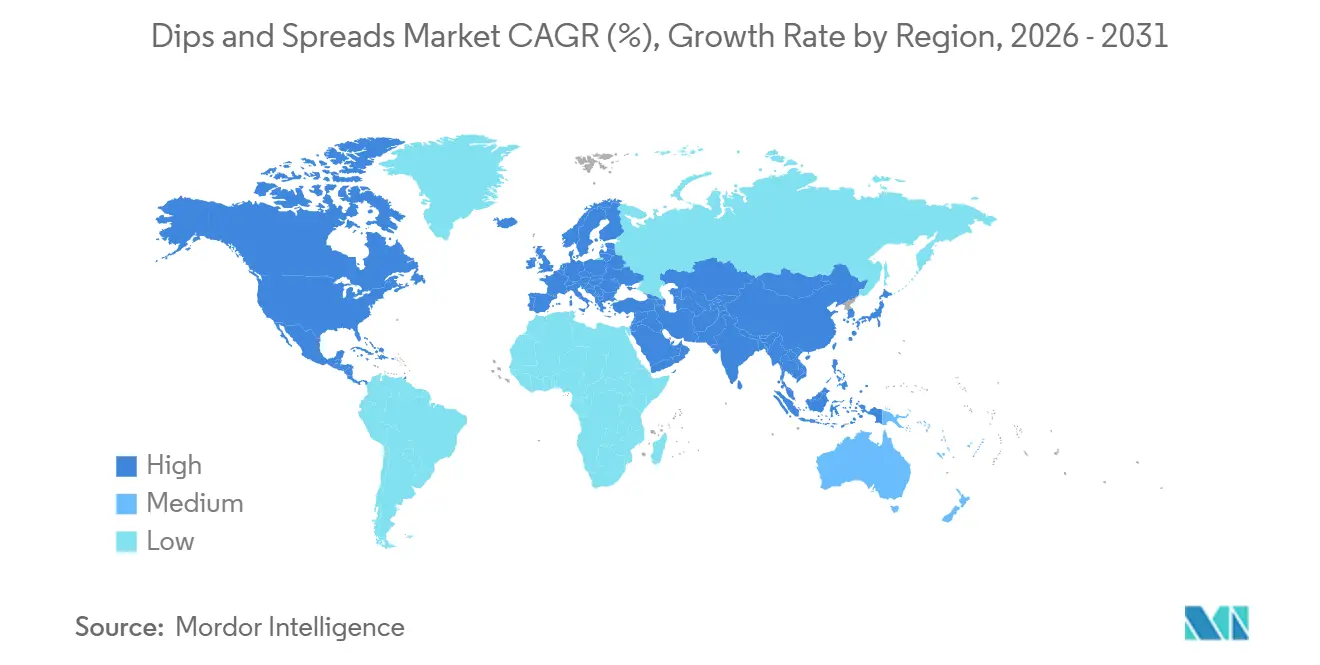

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dips and Spreads Market Analysis by Mordor Intelligence

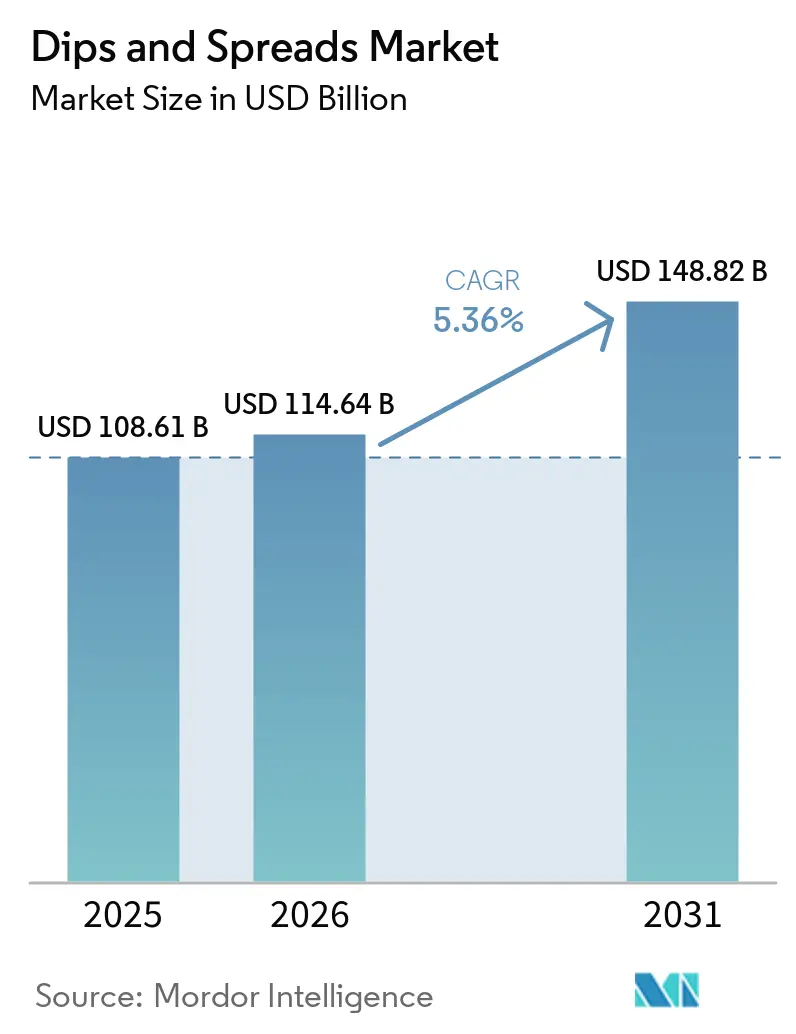

The Dips and spreads market size is projected to be USD 108.6 billion in 2025, USD 114.6 billion in 2026, and reach USD 148.8 billion by 2031, growing at a CAGR of 5.4% from 2026 to 2031. The dips and spreads market is benefiting from a steady shift toward frequent snacking, lighter eating occasions, and more flexible meal habits across both households and foodservice. Premium demand is also supporting value growth, because consumers are moving toward refrigerated, clean-label, plant-based, and functional products that carry higher selling prices than standard shelf-stable formats. The dips and spreads market is also gaining from the wider retail acceptance of Mediterranean and Tex-Mex flavors, which have moved hummus, guacamole, salsa, and related products into regular grocery baskets rather than occasional specialty purchases. Competition is becoming more structured around scale, fresh-case execution, supply control, and product renovation, which is pushing both large food groups and specialist brands to defend shelf space more actively. This keeps the dips and spreads market attractive for companies that can balance premium positioning with reliable sourcing, cold-chain execution, and broad channel reach.

Key Report Takeaways

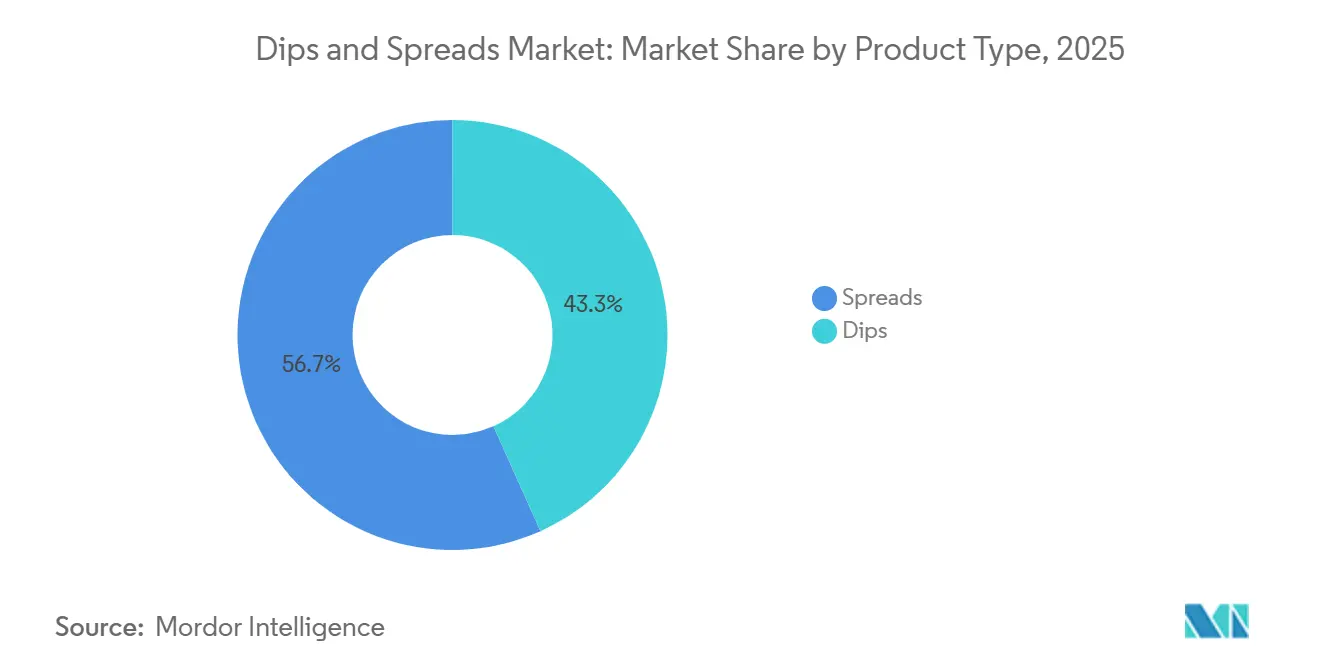

- By product type, spreads accounted for the largest share of the dips and spreads market, at 56.7% in 2025, while dips are projected to grow at the fastest CAGR of 7.0% during 2026-2031.

- By nature, conventional products retained 83.6% share of the dips and spreads market in 2025, whereas organic products are forecast to expand at a 7.1% CAGR through 2031.

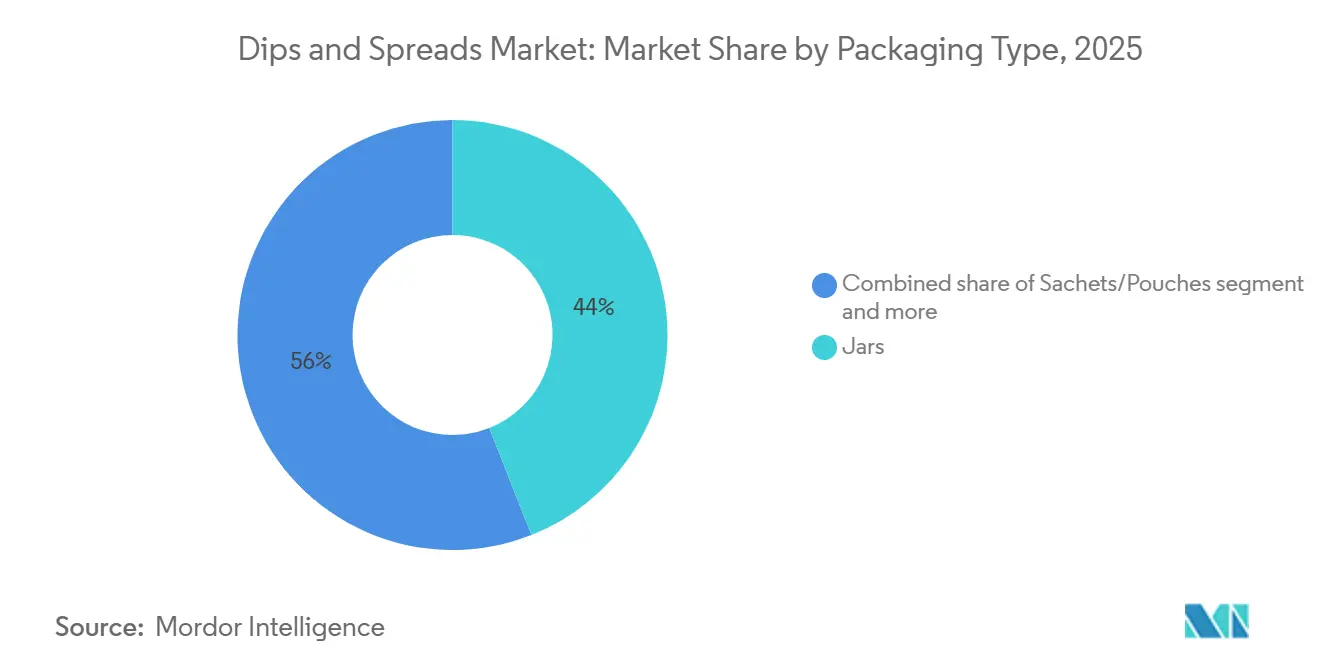

- By packaging type, jars led the dips and spreads market with a share of 44.0% in 2025, while sachets and pouches are anticipated to register the fastest CAGR of 6.7% during 2026-2031.

- By distribution channel, retail accounted for the largest share of the dips and spreads market, at 65.1% in 2025, while foodservice is projected to grow at the fastest CAGR of 7.5% during 2026-2031.

- By geography, North America accounted for the largest share of the dips and spreads market, at 36.4% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 7.0% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dips and Spreads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Snacking Frequency and Meal Occasion Substitution | +1.4% | Global | Short term (≤ 2 years) |

| Premiumization of Clean-Label and Refrigerated Dips | +1.1% | North America & Europe | Medium term (2-4 years) |

| Growth of Mediterranean and Tex-Mex Food Penetration | +0.9% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| E-Commerce Enabled Trial of Niche and Premium SKUs | +0.6% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Micro-Pack Formats Supporting Portion Control and On-The-Go Use | +0.5% | Global | Short term (≤ 2 years) |

| Expansion of Protein-Forward and Veggie-Forward Formulations | +0.7% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising snacking frequency and meal occasion substitution

Rising snacking frequency and the growing replacement of traditional meals with snack-based eating occasions are significantly driving demand in the global dips and spreads market. Consumers increasingly seek convenient, portable, and flavorful foods that fit busy lifestyles, making dips and spreads a natural accompaniment to snacks such as chips, crackers, vegetables, and bread. According to the International Food Information Council's 2025 Food & Health Survey, snacking has become a daily habit in the United States, with 30% of consumers snacking once a day, 28% twice a day, and 12% three or more times daily[1]Source: International Food Information Council, "Food & Health Survey 2025: A Focus on Food & Nutrition", International Food Information Council, ific.org. This indicates that nearly 70% of consumers snack at least once every day, creating frequent consumption opportunities for dips and spreads. The trend is further validated by PepsiCo’s USD 244 million acquisition of full ownership of Sabra, where the company specifically cited the growth of on-the-go eating occasions as a key strategic rationale[2]Source: PepsiCo, “PepsiCo Acquires Remaining Stake in Sabra and Obela,” PepsiCo, pepsico.com. As consumers increasingly substitute smaller snack occasions for conventional meals, demand is rising for versatile, ready-to-eat dips and spreads that enhance convenience, taste, and portion flexibility.

Premiumization of clean-label and refrigerated dips

Consumers are now willing to pay a premium of 30–100% for products boasting clean-label credentials, plant-based claims, and ingredients from authentic sources. This shift is influencing how shelf space is allocated in refrigerated sections. In the U.S., the clean-label movement is gaining traction, driven by consumer sentiment against ultra-processed foods and bolstered by state-level legislative actions. As a result, manufacturers of dips and food spreads are responding by simplifying ingredient lists, removing seed oils, and seeking third-party certifications. For instance, in June 2026, Cedar's Foods certified its entire Reserve line as seed-oil-free, directly addressing this consumer demand. Meanwhile, in Europe, the EU Green Deal's Packaging and Packaging Waste Regulation, overseen by ECHA, mandates manufacturers to shift to recyclable mono-material packaging. While this presents a cost challenge, it sets apart brands that are genuinely committed to sustainability, fostering long-term trust with consumers.

Growth of Mediterranean and Tex-Mex food penetration

Global enthusiasm for Mediterranean and Tex-Mex cuisines is propelling the dips and spreads market. Central to these culinary traditions are staples like hummus, salsa, guacamole, cheese dips, olive tapenades, and other spreadable delights. The Mediterranean diet, celebrated for its health benefits, has spurred a surge in the popularity of plant-based and vegetable-centric spreads. In 2025, the International Food Information Council (IFIC) highlighted that 57% of Americans adhered to a specific diet, underscoring a heightened focus on health-conscious eating. Globally, the Mediterranean diet stands out, lauded for its focus on legumes, vegetables, olive oil, and whole foods. Meanwhile, Tex-Mex flavors, once confined to North America, have found a global audience, boosting the popularity of salsa, queso, guacamole, and bean dips in both retail and dining establishments. As Mexican-inspired dishes gain traction and the appetite for global flavors grows, dips and spreads have evolved from being mere party staples to essential components of daily meals and snacks. With a rising demand for authentic international tastes and convenient meal enhancements, the allure of Mediterranean and Tex-Mex cuisines ensures a robust global appetite for their accompanying dips and spreads.

Expansion of protein-forward and veggie-forward formulations

The growing popularity of protein-rich and vegetable-based ingredients is reshaping innovation in the global dips and spreads market, as consumers increasingly seek products that combine convenience with perceived nutritional benefits. Rather than viewing dips solely as indulgent accompaniments, consumers are embracing formulations that incorporate vegetables, legumes, nuts, and dairy proteins, allowing dips and spreads to serve as snack enhancers, meal complements, and better-for-you alternatives to traditional condiments. Spinach-artichoke dips, hummus, bean-based spreads, avocado-based products, and yogurt-based dips have gained traction because they provide flavor while also featuring recognizable, nutrient-dense ingredients. The trend is evident in retail product development, with offerings such as Marketside Premium Heatable Spinach Artichoke Dip offered across the United States, highlighting vegetable-based ingredients in a convenient, ready-to-serve format, reflecting growing consumer demand for vegetable-forward snacking solutions. The product is positioned as a premium refrigerated dip designed for easy consumption occasions, demonstrating how retailers are expanding their portfolios beyond traditional cheese- or mayonnaise-based formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold Chain Dependency for Fresh and Refrigerated Formats | -0.8% | Global, critical in the Middle East and Africa, and Asia-Pacific | Long term (≥ 4 years) |

| Short Shelf Life and Spoilage Risk at Retail | -0.6% | Global | Short term (≤ 2 years) |

| Ingredient Price Volatility in Avocado, Dairy, and Oils | -0.7% | Global, significant in North America and Europe | Medium term (2-4 years) |

| Reformulation Friction from Clean-Label and Allergen Constraints | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cold chain dependency for fresh and refrigerated formats

The elevated growth potential of refrigerated dips, the sub-segment attracting the most investment and commanding the highest price points, is directly constrained by cold chain infrastructure, particularly across Middle Eastern, African, and parts of Asian markets. Without consistent refrigerated logistics from production to point of sale, brands cannot sustain the spoilage and quality standards demanded by modern retail and food safety regulators. This infrastructure gap is not merely a distribution inconvenience; it functions as a structural ceiling on how rapidly the refrigerated sub-category can penetrate markets where the greatest incremental volume opportunity exists. High-pressure processing (HPP), used by Good Foods Group to extend shelf life without preservatives, offers a partial solution but requires capital-intensive processing lines that limit adoption to well-funded manufacturers. In practice, the cold chain barrier concentrates premium refrigerated dips growth in mature markets while leaving shelf-stable spreads as the primary growth vector in developing economies.

Ingredient price volatility in avocado, dairy, and oils

Input cost exposure is disproportionately concentrated in a narrow set of commodities, avocado, olive oil, dairy fats, and nut oils, whose price behavior is driven by climate vulnerability, export concentration, and demand surges that are difficult to hedge at the SKU level. Olive oil prices increased more than 60% between 2023 and 2024 due to drought across Iberian and Italian growing regions, creating sustained margin compression for Mediterranean dip producers. Avocado supply cycles tied to Mexican and Californian harvests introduce quarterly price swings that complicate planning for guacamole brands. Mission Produce's acquisition of Calavo Growers, completed in May 2026 for USD 430 million, is partly a strategic response to this volatility, building a vertically integrated supply base that provides greater control over avocado input costs for prepared dips and guacamole[3]Source: Mission Produce, “Mission Produce Completes Acquisition of Calavo Growers,” Mission Produce, missionproduce.com. Dairy input costs for cheese dips and cream-based spreads face comparable inflationary cycles tied to feed-grain pricing, creating compounded raw-material risk for multi-protein-source dip formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dips Emerge as Value-Creation Engine Within a Spreads-Led Market

In 2025, entrenched daily habits for breakfast, sandwiches, and snacks anchored spreads, capturing 56.71% of the dips and spreads market. Within this segment, honey, chocolate-based spreads, and nut-and-seed-based varieties stand as volume pillars. In 2024, France witnessed a surge in peanut butter volumes, signaling the nut-spread category's expansion beyond almond to include cashew, hazelnut, and peanut varieties across Europe. Notably, brands like Andros and Bonne Maman have joined category leader Menguy's in this growing arena. While fruit-based spreads continue to enjoy steady penetration in European and North American breakfasts, a shift is underway. Clean-label pressures are nudging consumers towards low-sugar formats, a trend bolstered by FDA and EU EFSA's guidance on sugar content labeling.

Dips are not just popular; they're driving significant value, expanding at a CAGR of 6.96% through 2031. Once paired primarily with chips, salsa dips have evolved into a versatile ingredient, finding a place in premium and club-store formats worldwide. Guacamole has transitioned from a niche North American specialty to a mainstream refrigerated staple. Cheese and sour cream-based dips are not only strong in North American retail but are also making waves in foodservice through portioned servings. The "others" sub-segment of dips, which includes plant-based and yogurt-based variants, is emerging as a frontier. Brands are keenly developing dairy-free formats, catering to both lactose-intolerant and flexitarian consumers.

By Nature: Organic Rapidly Narrowing Conventional's Dominance

In 2025, conventional formulations dominated the market, holding an 83.62% share. This stronghold was bolstered by factors such as price accessibility, widespread retail presence, and the deep-rooted brand loyalty that traditional spreads, like peanut butter and fruit jam, have cultivated over generations. While this dominance appears stable in the near term, private labels have begun to carve out a significant margin share in the conventional jar-format segment, especially in Europe. This shift has diminished the pricing power of branded manufacturers in shelf-stable categories. In response, these established brands are channeling investments into premium and organic product-line extensions, steering clear of price competition in commodity segments.

Forecasted to grow at a CAGR of 7.11% through 2031, the organic segment is set to nearly double the growth pace of its conventional counterpart. This surge underscores a consumer trend: a heightened appreciation for certification credentials, which in turn justifies premium pricing. Regulatory frameworks, such as the USDA Organic and the EU's Council Regulation (EC) No 834/2007 on organic production, not only influence the market but also signal entry points. Brands boasting certified supply chains are reaping rewards, securing prime shelf space in mainstream supermarkets as organic allocations broaden. A testament to this trend, Ferrero invested USD 75 million in April 2026 to launch a new Nutella Peanut production line in Franklin Park, Illinois. This move underscores how even traditional brands are pivoting towards premium segments, marking the brand's first flavor innovation in its 62-year journey. The organic segment's robust growth is further fueled by a growing alignment between organic certification standards and the sustainability reporting frameworks that major food retailers are adopting in their supplier qualifications.

By Packaging Type: Sachets and Pouches Outpacing Jars as Occasion Diversification Accelerates

Sachets and pouches are rapidly becoming the preferred packaging format, projected to grow at a CAGR of 6.73% through 2031. This surge is driven by the rising demand for on-the-go snacking, the efficiency of e-commerce fulfillment, and a pronounced preference among Asia-Pacific consumers for single-serve, disposable formats. In the U.S., online sales of sauces, dips, and condiments have seen a consistent year-on-year rise. Notably, pouch packaging, optimized for direct-to-consumer (DTC) channels, has emerged as the favored choice for subscription services and meal kits. Furthermore, tubes and sachets are proving invaluable to foodservice operators. These formats ensure consistent portion control and efficient dispensing, especially crucial for high-throughput quick-service restaurants (QSRs) and delivery-centric dining establishments. Aligning with retail sustainability goals, mono-material polypropylene pouches are gaining traction. They not only use less material but also boast a smaller carbon footprint compared to traditional multi-layer rigid packaging.

In 2025, jars commanded a significant 44.01% share of the packaging market. Their dominance is attributed to functional benefits in refrigerated dips, enhanced preservation, and visibility. Consumers often associate glass and rigid formats with freshness and premium quality. Yet, jars face a structural challenge: their traditional association with household use conflicts with the consumption occasions driving the most growth. Meanwhile, other packaging formats, such as tubes and resealable tubs, are carving out a niche in European retail. Here, single-serve and trial-size formats are gaining traction on shelves as retailers experiment with optimized product assortments. While there's a noticeable shift from rigid to flexible packaging, it's expected to be slow. This is largely because dominant jar and tub formats in the refrigerated dip category carry strong consumer quality associations, making brands hesitant to make a switch.

By Distribution Channel: Foodservice Accelerating as Retail Maintains Scale

Foodservice, the fastest-growing distribution channel, is projected to expand at a CAGR of 7.51% through 2031. This growth is largely driven by the incorporation of Mediterranean and globally-inspired dips into mainstream restaurant menus. Hummus, once a staple of Greek restaurants, has now found its way into sandwich chains, grain bowl formats, and as a shared appetizer in casual dining settings. A testament to this trend, Good Foods partnered with Taylor Farms in July 2025, crafting Elote Style Dip snack packs for Walmart's deli section. This move underscores the evolving landscape where foodservice-inspired flavors seamlessly transition into retail, often through collaborative product development. Such channel-blurring dynamics are rapidly becoming a standard go-to-market strategy. Furthermore, the line between foodservice and retail continues to fade. Manufacturers are now crafting dual-channel products, catering to both institutional bulk buyers and individual consumers with nearly identical formulations. This approach not only enhances product appeal but also drives co-manufacturing efficiencies.

In 2025, retail dominated the market, accounting for 65.13%, with supermarkets and hypermarkets leading as the primary sub-channel. By Q1 2026, the online retail segment, a subset of the broader retail channel, witnessed notable growth in the US market for dips and condiments. This surge was largely attributed to branded suppliers like Campbell's and General Mills, who spearheaded the online assortment expansion. Online platforms offer a distinct advantage for niche and premium SKUs. These products, often sidelined in mainstream retail due to volume constraints, can cultivate dedicated consumer followings through direct-to-consumer (DTC) and marketplace channels. This strategy often paves the way for eventual national retail distribution. In urban markets, convenience stores are emerging as a significant channel for dips and spreads. They're particularly popular for single-serve and snack-occasion formats. Here, refrigerated snack kits and grab-and-go dip portions are increasingly overshadowing traditional impulse snack offerings.

Geography Analysis

In 2025, North America commanded a dominant 36.4% share of the dips and spreads market, outpacing all other regions. This leadership can be attributed to its well-established snack culture, robust refrigerated retail infrastructure, and widespread product familiarity. The U.S. stands as the primary regional force, bolstered by the popularity of chilled deli sections, spread aisles, and convenience-driven snacking. Highlighting the region's value, PepsiCo noted that Sabra, prior to its full acquisition, boasted nearly USD 400 million in U.S. retail sales. Furthermore, Mexico plays a dual role, acting as both a significant demand market and a pivotal sourcing hub for salsa and guacamole, enriching North America's ties to both consumption and raw material sourcing.

Europe's dips and spreads market showcases a diverse yet significant landscape. Western Europe leans towards hummus and plant-based chilled dips, the U.K. favors a premium deli assortment, and various markets see consistent household use of fruit and nut spreads. Germany emerges as a hotspot for refrigerated plant-based dips, while the U.K.'s developed grocery formats champion a premium chilled selection. Eastern Europe, though in the nascent stages of adoption, is witnessing improved growth conditions as urban consumers access modern retail and global food options. Throughout Europe, market dynamics are influenced by a preference for cleaner labels, recycling initiatives, and a heightened interest in premium fruit, nut, and Mediterranean offerings.

Asia-Pacific is set to lead the charge, with projections indicating a 7% CAGR growth through 2031, marking it as the fastest-growing major region in the dips and spreads market. Urban consumers in China and India are increasingly embracing a diverse array of global snacks and meal formats. In this region, packaging plays a pivotal role; formats like tubes, pouches, and bottles cater to households favoring smaller portions and ease of handling. South America is witnessing a surge in demand for nut-based and health-oriented spreads. Meanwhile, the Middle East and Africa, buoyed by local mezze traditions and increasing urban retail penetration, present a promising long-term outlook. However, the expansion of chilled products in these regions hinges on the quality of infrastructure, suggesting that shelf-stable and easily distributable formats will dominate in the short term.

Competitive Landscape

At the global level, the dips and spreads market exhibits moderate concentration. Large packaged food groups vie for dominance across a wide array of products, while specialists carve out significant niches in premium and refrigerated segments. Heavyweights like PepsiCo, Kraft Heinz, Conagra Brands, Unilever, Nestlé, and Ferrero leverage their scale for advantages in distribution, sourcing, and brand visibility, making it challenging for newcomers to penetrate mainstream channels. Meanwhile, players like Cedar’s Foods, Good Foods Group, and La Terra Fina, along with regional contenders, emphasize chilled freshness, clean-label positioning, and cuisine-specific credibility, all of which resonate strongly with consumers. In a strategic move, PepsiCo fully acquired Sabra and Obela in late 2024, gaining direct oversight of a leading refrigerated dip platform and reinforcing its ties between fresh dips and its broader snack portfolio. This acquisition underscores a market trend: competition is increasingly centered on scale, portfolio alignment, and cold-case execution, rather than solely on flavor innovation.

Market dynamics in dips and spreads are shifting, with a pronounced emphasis on portfolio refinement, capacity growth, and securing supply chains. Kraft Heinz is consolidating its Philadelphia and Heinz brands under a dedicated "Global Taste Elevation" umbrella, signaling a heightened focus on flavor-centric categories. Meanwhile, Ferrero's USD 75 million investment in a new Nutella Peanut line in Illinois underscores the strategy of legacy brands: by expanding formulations and production, they're not only safeguarding their relevance but also tapping into adjacent demand pools. Mission Produce's acquisition of Calavo Growers bolstered its prepared-food capabilities and avocado control, spotlighting the growing importance of ingredient access as a competitive edge in the dips and spreads arena.

Opportunities abound in the dips and spreads market for brands that can adeptly address specific unmet needs, outpacing established players. There's noticeable potential in allergen-aware products, probiotic or fermented offerings, and convenient formats that don't solely depend on the chilled chain. However, as products trend towards being fresher, more premium, and widely distributed, the stakes rise. Food safety, traceability, and process discipline are paramount, favoring well-capitalized operators. Yet, the door remains ajar for challengers: the category continues to reward distinct products that secure repeat purchases through superior ingredients, fresher appeal, or heightened cuisine relevance.

Dips and Spreads Industry Leaders

-

PepsiCo, Inc.

-

The Kraft Heinz Company

-

Conagra Brands, Inc.

-

Hormel Foods Corporation

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mission Produce completed its acquisition of Calavo Growers for USD 430 million, creating a vertically integrated avocado and prepared-foods platform that includes Calavo's guacamole and salsa product lines. The deal gives Mission direct access to Calavo's prepared food manufacturing capabilities and expands its Mexico sourcing network to four packinghouses, improving supply reliability for the guacamole dips segment.

- April 2026: Ferrero opened a USD 75 million Nutella Peanut production line in Franklin Park, Illinois, the brand's first US manufacturing site, creating 50 new jobs and marking Nutella's first flavor innovation in its 62-year history. The peanut-cocoa hazelnut spread is available nationally at Walmart and other retailers, targeting lunchtime and evening snacking occasions.

- April 2026: Cedar's Foods debuted at Target stores nationwide, expanding to over 1,500 Target locations. Cedar's, the world's largest hummus producer with over 145 million pounds of annual production across 13,500+ retail locations, introduced Cucumber Garlic Dill Tzatziki, Hot Honey Dip, and Feta Dip to Target shoppers.

Global Dips and Spreads Market Report Scope

Dips and spreads are thick, semi-solid, or fluid condiments used to add flavor, moisture, and texture to other foods, such as bread, crackers, chips, vegetables, or meats. The global dips and spreads market is segmented by product type, nature, packaging type, distribution channel, and geography. By product type, the market is segmented into dips and spreads. The dips segment is further sub-segmented into salsa dips, cheese dips, guacamole, sour cream-based dips, and others. Similarly, the spreads segment is further sub-segmented into honey, chocolate-based spreads, fruit-based spreads, nut- and seed-based spreads, dairy and cheese spreads, and other spread types. By nature, the market is segmented into conventional and organic. By packaging type, the market is segmented into jars, tubes, sachets/pouches, and others. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, online retail, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Dips | Salsa Dips |

| Cheese Dips | |

| Guacamole | |

| Sour Cream-Based Dips | |

| Others | |

| Spreads | Honey |

| Chocolate-based Spreads | |

| Fruit-based Spreads | |

| Nut- and Seed-based Spreads | |

| Dairy and Cheese Spreads | |

| Other Spread Types |

| Conventional |

| Organic |

| Jars |

| Tubes |

| Sachets/Pouches |

| Other Packaging Types |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Dips | Salsa Dips |

| Cheese Dips | ||

| Guacamole | ||

| Sour Cream-Based Dips | ||

| Others | ||

| Spreads | Honey | |

| Chocolate-based Spreads | ||

| Fruit-based Spreads | ||

| Nut- and Seed-based Spreads | ||

| Dairy and Cheese Spreads | ||

| Other Spread Types | ||

| Nature | Conventional | |

| Organic | ||

| Packaging Type | Jars | |

| Tubes | ||

| Sachets/Pouches | ||

| Other Packaging Types | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the dips and spreads space?

The Dips and spreads market size is USD 114.6 billion in 2026 and is forecast to reach USD 148.8 billion by 2031 at a 5.4% CAGR.

Which product category leads sales, and which one is growing faster?

Spreads led with 56.7% share in 2025, while dips are growing faster at a 7% CAGR through 2031.

Why is foodservice becoming more important for dips and spreads demand?

Foodservice is projected to grow at 7.5% CAGR because dips now appear more often in bowls, wraps, appetizers, and shared plates, which expands usage beyond traditional snacking.

Which region is the largest, and which region is expanding fastest?

North America held 36.4% of revenue in 2025, while Asia-Pacific is set to post the fastest growth at 7% CAGR through 2031.

Page last updated on: