Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.39 Billion |

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Nut-Based Spreads Market Analysis by Mordor Intelligence

European nut-based spreads market size in 2026 is estimated at USD 2.54 billion, growing from 2025 value of USD 2.39 billion with 2031 projections showing USD 3.41 billion, growing at 6.08% CAGR over 2026-2031. The market growth is driven by increasing consumer demand for convenience foods, plant-based alternatives, and dairy-free options. Health-conscious consumers recognize the nutritional benefits of nut-based spreads, including essential fatty acids, high protein content, and beneficial carbohydrates. Manufacturers have introduced low-fat and reduced-sugar variants to meet the needs of calorie-conscious consumers. The rising focus on healthier lifestyles has accelerated market growth, with consumers showing particular interest in hazelnut-based products for their heart health benefits. The market is expected to continue growing as consumer preferences evolve.

Key Report Takeaways

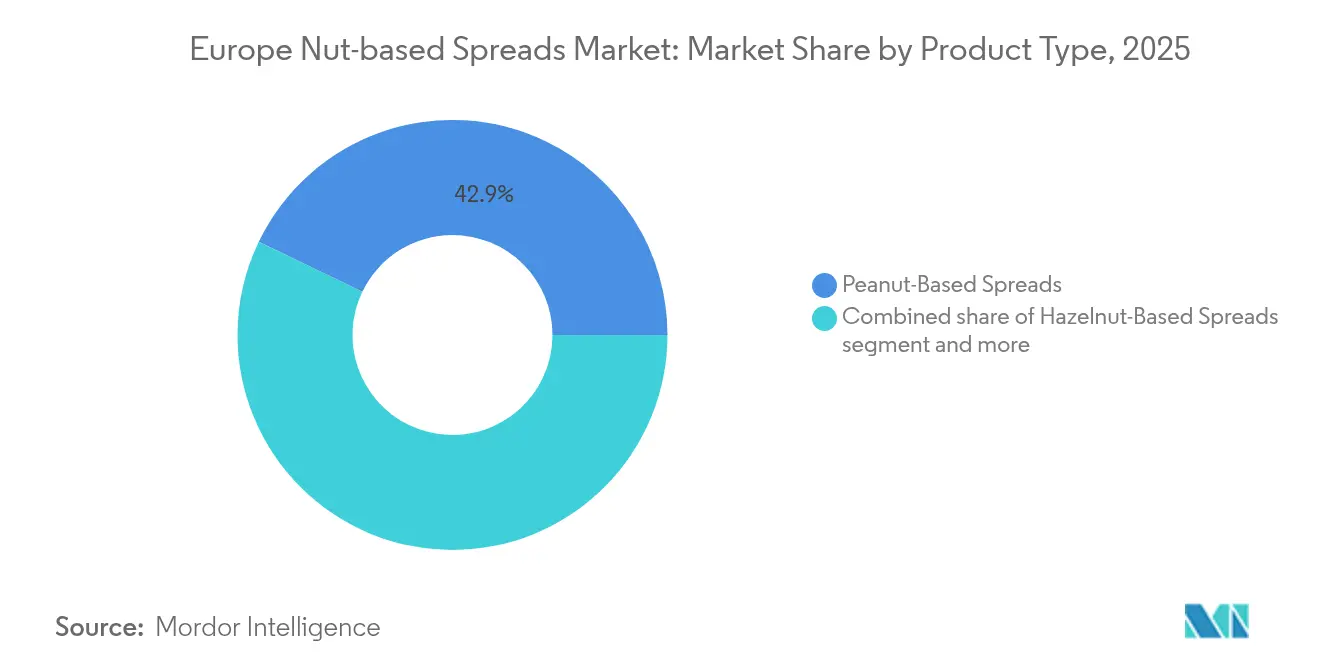

- By product type, peanut-based spreads led with 42.86% of the European nut-based spreads market share in 2025; cashew spreads are projected to expand at 6.18% CAGR between 2026-2031.

- By nature, conventional products held 87.55% share of the European nut-based spreads market size in 2025, while the organic segment is forecast to grow at a 7.22% CAGR through 2031.

- By packaging type, jars commanded 65.05% share in 2025, whereas sachets and pouches are advancing at a 6.62% CAGR to 2031.

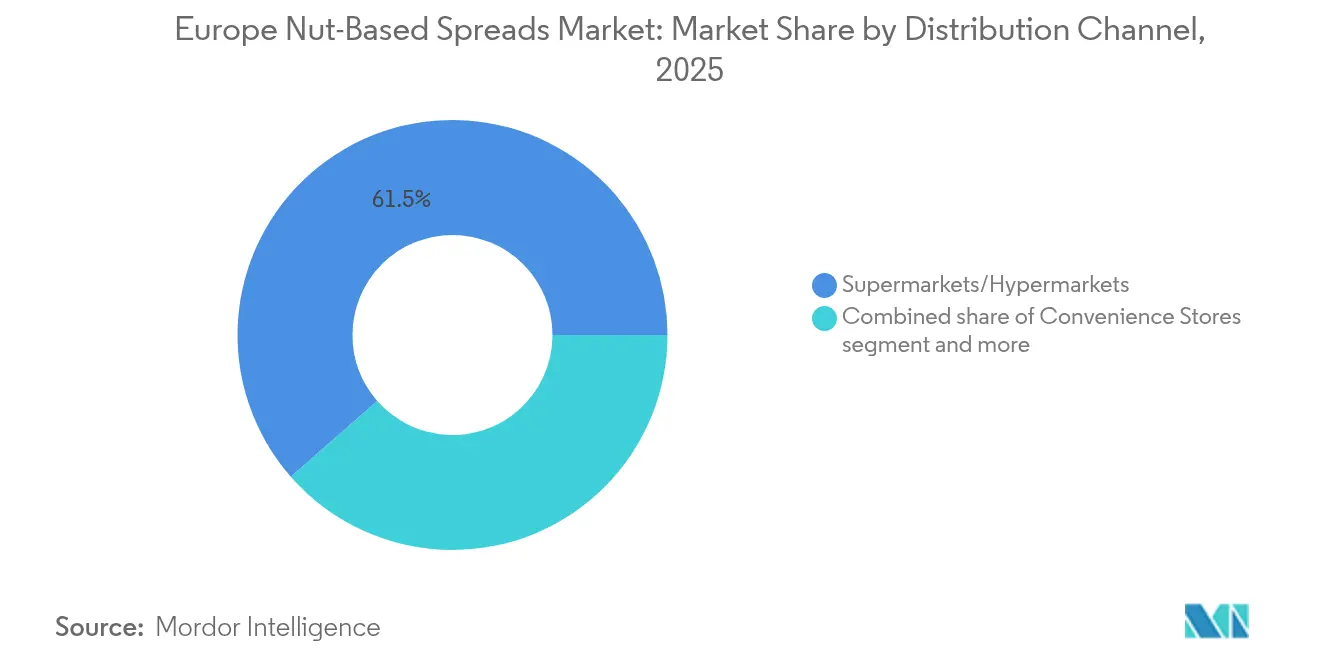

- By distribution channel, supermarkets/hypermarkets accounted for 61.45% share in 2025; online retail is rising fastest at a 7.58% CAGR over the forecast period.

- By geography, the United Kingdom held an 10.92% market share in 2025, while Italy recorded a 3.98% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Nut-Based Spreads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of health benefits associated with nuts fuels consumption | +1.8% | Pan-European, with stronger impact in UK, Germany, France | Medium term (2-4 years) |

| Rising demand for exotic and regionally sourced fruit flavors drives product innovation | +1.5% | Western Europe, particularly UK, France, Italy | Short term (≤ 2 years) |

| Expansion of clean label and natural product offerings aligns with european consumer trends | + 1.2% | Pan-European, with stronger impact in Nordic countries and Germany | Medium term (2-4 years) |

| Aggressive marketing and branding influences market growth | +0.9% | Pan-European, with stronger impact in urban centers | Short term (≤ 2 years) |

| Innovation in flavors, ingredients appeals to millennials and health-focused consumers | +0.7% | Pan-European, with stronger impact in UK, France, Germany | Medium term (2-4 years) |

| Expansion of retail and online channels increases availability of nut based spreads across Europe | +0.9% | Pan-European, with stronger impact in Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Health Benefits Associated with Nuts Fuels Consumption

Growing consumer awareness of the nutritional benefits of nuts is driving manufacturers to transform their products from snacks to functional foods. According to the National Library of Medicine [1]Source: PubMed, “Intake of nuts was associated with reduced risk of cardiovascular disease,” pubmed.ncbi.nlm.nih.gov, regular nut consumption reduces the risks of cardiovascular disease, cancer mortality, and all-cause mortality, providing scientific support for product claims. This understanding influences manufacturers to develop formulations that maintain nuts' natural nutritional properties, emphasizing protein content, healthy fats, and micronutrients. In March 2024, Whole Earth launched a limited-edition protein-enhanced peanut butter featuring crunchy pea protein pieces, which provides higher protein content than standard crunchy peanut butter, meeting the criteria for a "high in protein" claim. These developments indicate a continued shift toward healthier, nutrient-dense spreads that align with consumer preferences for functional foods.

Expansion of clean label and natural product offerings aligns with European consumer trends

The clean label movement is transforming product development priorities across the food and beverages industry. Manufacturers are eliminating artificial additives, preservatives, and palm oil from their formulations, which presents technical challenges while offering differentiation opportunities. According to research by CBI ministry of foreign affairs [2]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," www.cbi.eu, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, increasing from 52% in 2021. Companies are adopting transparent sourcing practices and simplified ingredient declarations, while also emphasizing ethical sourcing through certification schemes and supply chain transparency initiatives. This comprehensive approach to clean label positioning enables premium pricing strategies, expanding category margins despite rising input costs. In response to this trend, companies continue to innovate, as demonstrated by Pip & Nut's May 2025 release of new Chocolate Hazelnut Spread with 63% nuts and over six times less sugar than Nutella. Free from palm oil and ultra-processed fillers, it’s the UK’s first chocolate spread using ethically sourced cocoa from Tony’s Chocolonely’s Open Chain.

Innovation In Flavors, Ingredients Appeals to Millennials and Health-Focused Consumers

Innovative products with unique flavors and convenient formats are reshaping consumption habits and attracting diverse consumers. Manufacturers are blending exotic and locally-sourced ingredients to craft premium signature flavors. For example, Campo d'Oro will launch Pistachio Sweet Cream with Truffle in January 2025, a spread featuring black truffle flakes and artificial truffle aroma, expanding its pistachio product line. To cater to on-the-go lifestyles, manufacturers are introducing squeezable bottles, single-serve sachets, and portable pouches, appealing to younger consumers while addressing sustainability through material reduction and recyclability. Whole Earth offers such packaging options, and in March 2025, Printzells Confectionery, in partnership with Huhtamaki, launched its nut-based spread in recyclable paper cups and lids, suitable for local paper waste management.

Expansion of retail and online channels increases availability of nut based spreads across Europe

The shift toward online retail channels is transforming competitive dynamics in the nut-based spreads market. Digital platforms enable direct-to-consumer business models that streamline supply chains and improve margins, particularly benefiting premium and niche products. According to Eurostat, [3]Source: Eurostat, “E-commerce statistics for individuals,” ec.europa.eu the percentage of online buyers in the European Union increased from 59% in 2014 to 77% in 2024, demonstrating the growing significance of e-commerce. Social media platforms have become essential discovery channels for innovative nut-based spreads, with visual content driving consumer engagement. This digital transformation has led to new market entries, as evidenced by Voyage Foods' launch of allergen-free nut-based spreads through Amazon UK in June 2024. The increased accessibility of online markets is intensifying competition, prompting established companies to adapt through direct-to-consumer initiatives, subscription models, and digital-first product launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high sugar and fat content in certain spread restricts growth | -0.8% | Pan-European, with stronger impact in Nordic countries and Germany | Medium term (2-4 years) |

| Fluctuating prices of raw nuts impact production costs and profit margins | -0.6% | Pan-European | Short term (≤ 2 years) |

| Allergies to peanuts and tree nuts restrict potential consumer base | -0.5% | Pan-European, with stronger impact in UK and Nordic countries | Long term (≥ 4 years) |

| Competition from chocolate and fruit-based spreads challenges market share | -0.4% | Pan-European, with stronger impact in Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergies To Peanuts and Tree Nuts Restrict Potential Consumer Base

The prevalence of nut allergies in Europe influences regulatory frameworks and product development in the market. The European Food Safety Authority's focus on Precautionary Allergen Labelling (PAL) requires manufacturers to meet strict compliance requirements. Industry participants seek unified standards to replace diverse national regulations. The absence of uniform quantitative risk assessment methods creates regulatory uncertainty and potential trade barriers. Manufacturers are responding by developing hypoallergenic processing methods to reduce allergen levels while maintaining nutritional content. Companies are also producing alternative spreads using seeds and legumes to provide comparable taste and texture without allergen risks. These adaptations in regulatory compliance and product innovation demonstrate the market's responsiveness to addressing allergen-related challenges while ensuring consumer safety.

Fluctuating Prices of Raw Nuts Impact Production Costs and Profit Margins

European nut-based spreads, particularly premium single-origin products, are feeling the impact of supply chain vulnerabilities and commodity price fluctuations. According to the International Nut and Dried Fruit Council, Turkey supplied approximately 70% of global hazelnut production in 2023, creating concentration risks that can lead to price volatility during harvest shortfalls [4]Source: International Nut and Dried Fruit Council, “Sustainability Update: May 2025,” inc.nutfruit.org. Additionally, climate change is casting a shadow on almond production in crucial sourcing areas, further complicating the supply landscape. These rising input costs hit smaller producers the hardest, as they often lack the means to hedge against price swings or exert significant pricing power. Consequently, this ongoing volatility in raw material costs stifles innovation and growth, particularly for brands eyeing a foothold in the premium or clean-label markets. Moreover, erratic input prices can upend long-term pricing strategies, compelling manufacturers to shift costs onto consumers, which could dampen demand in markets sensitive to price changes.shadow

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Peanut Dominance Faces Specialty Nut Challenge

Peanut-based spreads dominate the European market with a 42.86% share in 2025, leveraging their established consumer acceptance and cost advantages over other nut varieties. While peanut spreads maintain their market leadership, they face growing competition from emerging alternatives, particularly cashew-based products, which are projected to grow at a 6.18% CAGR from 2026 to 2031. Cashew spreads are gaining popularity due to their creamy texture and versatile flavor profile, supported by sustainable farming initiatives in regions like Ghana, according to Olam Food Ingredients.

The nut spread market demonstrates diverse regional preferences, with hazelnut-based products maintaining strong positions in Italy and France due to cultural traditions and local sourcing. Almond spreads attract health-conscious consumers through their nutritional benefits, while walnut spreads serve premium market segments. The market landscape continues to evolve as manufacturers develop hybrid formulations, combining different nut varieties to create unique flavor profiles and nutritional offerings.

By Nature: Organic Growth Outpaces Conventional Despite Premium Pricing

The conventional segment maintains a commanding 87.55% share of the European nut-based spreads market in 2025, leveraging its established production infrastructure and competitive pricing. While conventional products dominate current sales, the organic segment is experiencing rapid growth, with a projected CAGR of 7.22% from 2026 to 2031, driven by consumers increasingly willing to pay premium prices for products they perceive as healthier and more environmentally sustainable.

The organic segment's growth has catalyzed significant changes in the market, with manufacturers investing in supply chain transparency and certification programs to verify organic compliance. Companies like Rapunzel Naturkost, Jean Herve, and Campo d'Oro are capitalizing on this trend by offering organic spreads that align with the clean label movement. This combination of organic certification and clean label attributes creates compelling product positioning that appeals to health-conscious consumers seeking premium food options.

By Packaging Type: Sustainable Innovations Challenge Jar Dominance

Traditional jars maintain their dominance in the European nut-based spreads market, holding a 65.05% share in 2025. These conventional formats benefit from consumer familiarity while offering superior product protection and shelf presentation. Tub formats retain significant market share, particularly in premium segments where their structural integrity supports brand perception, while smaller manufacturers utilize distinctive packaging designs to differentiate their products in competitive retail environments.

Sachets and pouches are emerging as the fastest-growing packaging format, with a projected CAGR of 6.62% from 2026 to 2031. This growth stems from their convenience and portion control benefits, which align with on-the-go consumption patterns and single-household demographics. The format's evolution includes functional improvements such as corner spout designs for enhanced dispensing. Across all packaging formats, sustainability considerations are influencing manufacturer strategies, driving the adoption of recyclable and renewable materials.

By Distribution Channel: Digital Acceleration Reshapes Retail Dynamics

Supermarkets/hypermarkets maintain their dominant position in European nut-based spread distribution, holding a 61.45% market share in 2025. Their extensive physical presence enables broad product assortments that drive consumer discovery and trial. Convenience stores remain important for impulse purchases and immediate consumption, while specialty retailers provide platforms for premium and artisanal products. The physical retail landscape continues to adapt through hybrid models, including click-and-collect services and rapid delivery options.

Online retail is experiencing significant growth at 7.58% CAGR from 2026 to 2031, transforming competitive dynamics and distribution strategies. The digital channel enables direct-to-consumer business models that streamline supply chains and improve margins for both established companies and new market entrants. This shift particularly benefits premium and niche products that may face challenges securing traditional retail shelf space. The evolving digital landscape has also fostered new partnerships, with some specialty producers adopting co-manufacturing arrangements to supply retailer brands while maintaining premium direct-to-consumer offerings through digital channels.

Geography Analysis

The United Kingdom holds an 10.92% share of the European nut-based spreads market in 2025, driven by its established breakfast culture and consumer adoption of plant-based proteins. British consumers show increasing preference for diverse nut butters beyond traditional peanut varieties. Companies like Pip & Nut and ManiLife have gained market presence through their focus on clean-label products and flavor innovations. The UK distribution landscape continues to evolve, with growing online sales channels and specialty retailers offering platforms for premium products.

Italy demonstrates the highest growth potential with a projected CAGR of 3.98% from 2026 to 2031. This growth stems from increased consumer awareness of nut-based products' nutritional benefits and their integration into Italian cuisine. Local manufacturers like Caporaso Group have expanded their product range to 80 items, including hazelnut, pistachio, and peanut spreads. The market operates under varying regulatory frameworks, which influence market dynamics.

Germany, France, and Spain present significant market opportunities with unique consumption patterns. German consumers prioritize organic and sustainable products, creating demand for clean-label and ethically sourced options. In France, consumers use nut spreads across various culinary applications beyond breakfast. Spain shows increasing demand for specialty nut varieties, particularly almond-based products that align with local agricultural heritage.

Competitive Landscape

The European nut-based spreads market maintains a moderately consolidated competitive structure, dominated by established multinational companies alongside emerging specialty producers. Major players such as Unilever, The Hershey Company, and SHS Group utilize their advantages in procurement, manufacturing, and distribution networks. Meanwhile, specialty producers like Pip & Nut and ManiLife create market differentiation through product purity, innovative flavors, and authentic brand positioning.

The market presents opportunities in specialized formulations targeting specific dietary needs, particularly in protein-enhanced, reduced-sugar, and allergen-friendly variants. Digital capabilities and direct-to-consumer models are reshaping market entry strategies, allowing companies to bypass traditional retail channels. The competitive landscape continues to evolve through strategic acquisitions and new product development.

Manufacturers are actively expanding their product portfolios through innovative flavor combinations. A notable example is Ferrero’s announcement of a new Nutella variant, set to launch in 2026, its first flavor innovation in 60 years, combining the classic cocoa-hazelnut spread with roasted peanuts to offer a richer, more layered taste experience.

Europe Nut-Based Spreads Industry Leaders

-

The Hershey Company

-

Unilever PLC

-

SHS Group

-

PIP & NUT LTD.

-

The Hain Celestial Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Printzells Confectionery partnered with Huhtamaki to introduce nut-based spread in recyclable paper cups with matching lids.

- January 2025: Ferrero has introduced Nutella Plant-Based in the German market, offering a vegan alternative that maintains the brand’s signature taste. The reformulated spread features ingredients like chickpeas and rice syrup, while still incorporating carefully selected hazelnuts and cocoa to deliver the familiar Nutella experience in a plant-based format.

- November 2024: Intersnack, through its KP Snacks division, acquired Whole Earth Foods from Ecotone to expand its healthy product range and strengthen its peanut-butter capability.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe nut-based spread market as the annual value of peanut, almond, hazelnut, cashew, walnut, and mixed-nut spreads that contain at least forty percent nut solids and are sold for direct human consumption across the EU-27, the United Kingdom, Norway, and Switzerland. Products may be shelf-stable or chilled and reach consumers through retail or foodservice channels.

Scope Exclusions: Seed-only pastes, chocolate creams with less than 40 percent nut content, coconut or soy spreads, and industrial ingredients are kept outside our scope.

Segmentation Overview

-

By Product Type

- Peanut-Based Spreads

- Hazelnut-Based Spreads

- Almond-Based Spreads

- Walnut-Based Spreads

- Cashew-Based Spreads

- Other Product Types

-

By Nature

- Conventional

- Organic

-

By Packaging Type

- Jars

- Tubs

- Sachets/Pouches

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews with European brand managers, private-label buyers, specialty-store owners, and logistics intermediaries helped us validate nut content thresholds, average selling prices, and emerging flavors. Conversations spanned the United Kingdom, Germany, Italy, and Spain, ensuring regional nuances were captured before finalizing assumptions.

Desk Research

Mordor analysts first compile harmonized production and trade codes from Eurostat, UN Comtrade, and FAOSTAT, then reconcile them with retail audit snapshots published by Eurostat's Household Budget Survey and the Agriculture & Agri-Food Canada commodities monitor. We also review nutrition claims and pack sizes cataloged by the EU Food and Feed Safety Register, plus macro-level consumption cues drawn from OECD Health Data. Company revenues for leading brand owners are screened in D&B Hoovers, while import parity prices are sampled through Volza shipment records. This list is illustrative; many additional open and paid sources informed our desk work.

Market-Sizing & Forecasting

A top-down model converts net production plus imports minus exports into apparent consumption, which is then priced using weighted average shelf prices to yield market value. Results are pressure-tested through bottom-up roll-ups of sampled supplier revenues and e-commerce channel checks, letting us fine-tune leakage between wholesale and retail. Key variables, such as per-capita spread intake, private-label share, tree-nut cost trends, plant-based diet penetration, and disposable income, feed a multivariate regression that drives the forecast. Scenario analysis adjusts for nut price shocks and regulatory sugar targets whenever variance exceeds a specified threshold.

Data Validation & Update Cycle

Outputs pass a two-level analyst review, anomaly flags trigger re-checks with respondents, and every report is refreshed annually; interim updates occur when raw-nut tariffs, major M&A, or crop failures materially shift any driver.

Why Mordor's Europe Nut-Based Spreads Baseline Commands Reliability

Published estimates often differ because firms pick unlike product mixes, price points, or refresh cadences.

Key gap drivers include: some studies fold chocolate hazelnut and honey blends into the same pool, others quote retail scanner totals without netting promotions, while a few upscale forecasts simply inflate Europe's share of global value.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.39 Bn (2025) | Mordor Intelligence | - |

| USD 7.65 Bn (2024) | Regional Consultancy A | Combines sweet spreads and uses unadjusted shelf prices across 35 countries |

| USD 0.82 Bn (2024) | Global Consultancy B | Excludes hazelnut-chocolate and foodservice, relies on limited consumer survey panels |

| USD 1.33 Bn (2023) | Trade Journal C | Derives Europe value as a fixed share of global sales, no primary validation |

In sum, our balanced top-down build, selective bottom-up cross-checks, and annual refresh give decision-makers a transparent, reproducible baseline that sits comfortably between optimistic retail scans and narrow product-line tallies.

Key Questions Answered in the Report

What is the current value of the European nut-based spreads market?

The market is valued at USD 2.54 billion in 2026 and is forecast to grow to USD 3.41 billion by 2031.

Which product type holds the largest share in Europe?

Peanut-based spreads led with 42.86% share in 2025, sustained by accessible pricing and broad household acceptance.

How fast is the organic segment growing?

Organic nut-based spreads are projected to expand at a 7.22% CAGR between 2026 and 2031, outpacing the conventional segment.

How significant is online retail to future growth?

Online retail channels are rising at a 7.58% CAGR, offering direct-to-consumer access and accelerating flavor experimentation.

Page last updated on: