Aggregates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

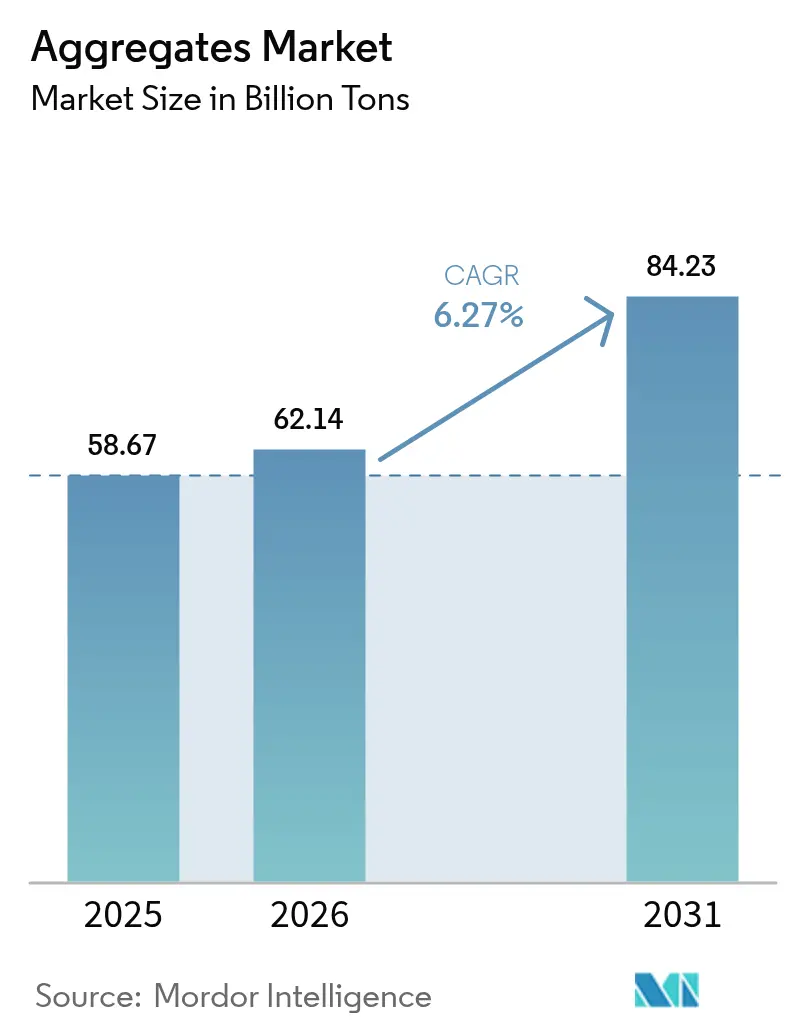

| Market Volume (2026) | 62.14 Billion tons |

| Market Volume (2031) | 84.23 Billion tons |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aggregates Market Analysis by Mordor Intelligence

The Aggregates Market size is projected to expand from 58.67 billion tons in 2025 and 62.14 billion tons in 2026 to 84.23 billion tons by 2031, registering a CAGR of 6.27% between 2026 to 2031. Public investment programs, low-carbon procurement rules, and rapid urban migration combine to lift long-term demand for quarried and recycled stone. National infrastructure plans in the United States, India, and Saudi Arabia translate policy budgets into steady tender pipelines that favor producers with assured reserves and multi-modal logistics. Growing reliance on ready-mix concrete raises quality thresholds for particle size and moisture content, which intensifies the need for washed and screened feedstock. Emissions reporting moves from voluntary to mandatory status in key buying regions, so aggregate suppliers that publish Environmental Product Declarations gain a pricing premium.

Key Report Takeaways

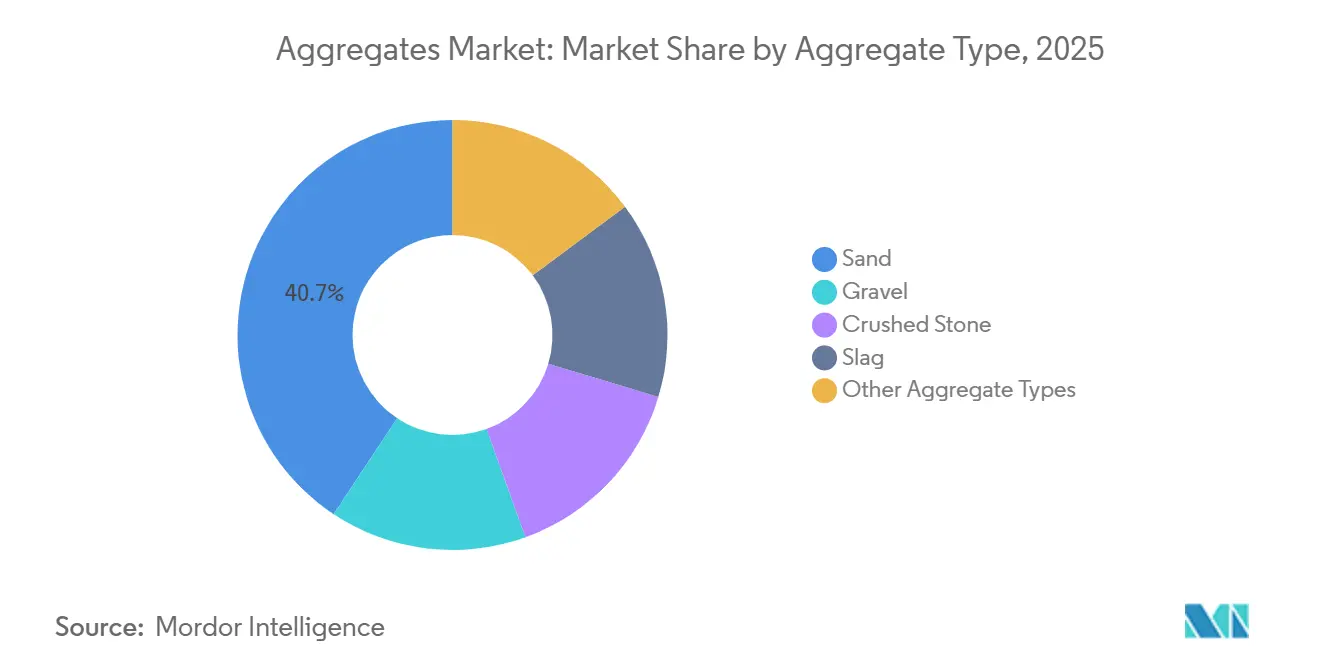

- By aggregate type, sand led with 40.69% revenue share in 2025, while other aggregate types are projected to expand at a 7.90% CAGR through 2031.

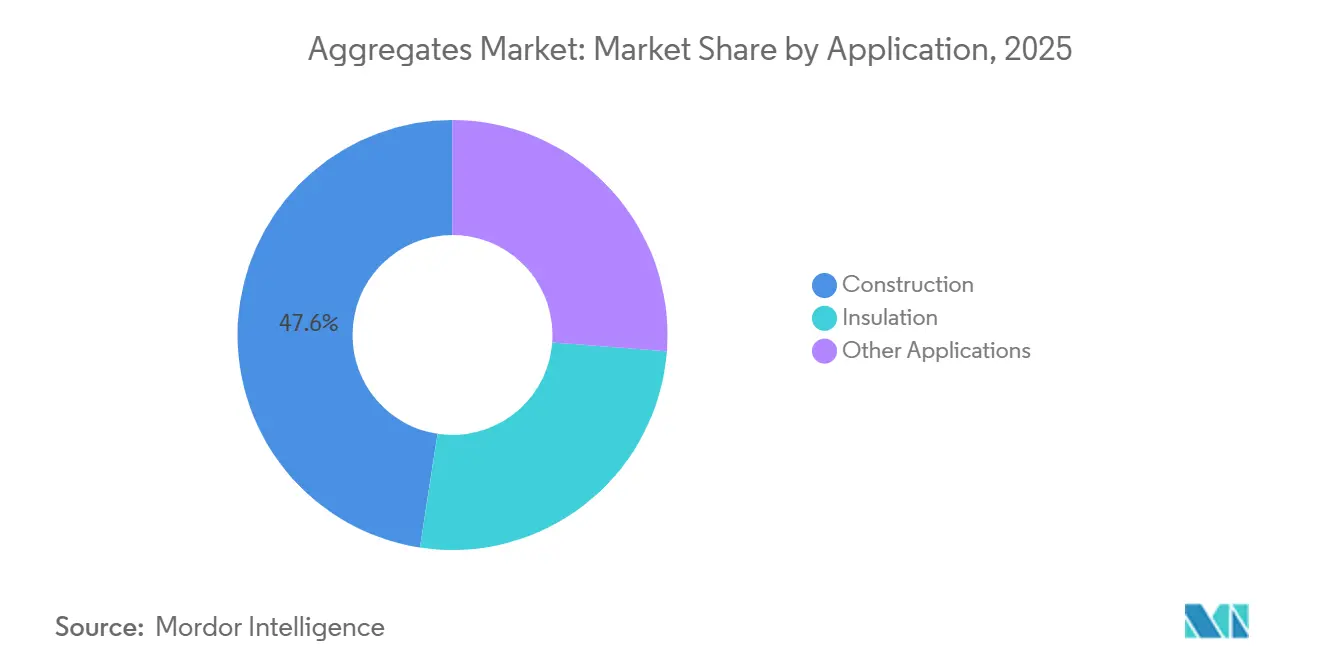

- By application, construction accounted for 47.59% of the Aggregates market share in 2025 and other applications are forecast to grow at 7.82% CAGR to 2031.

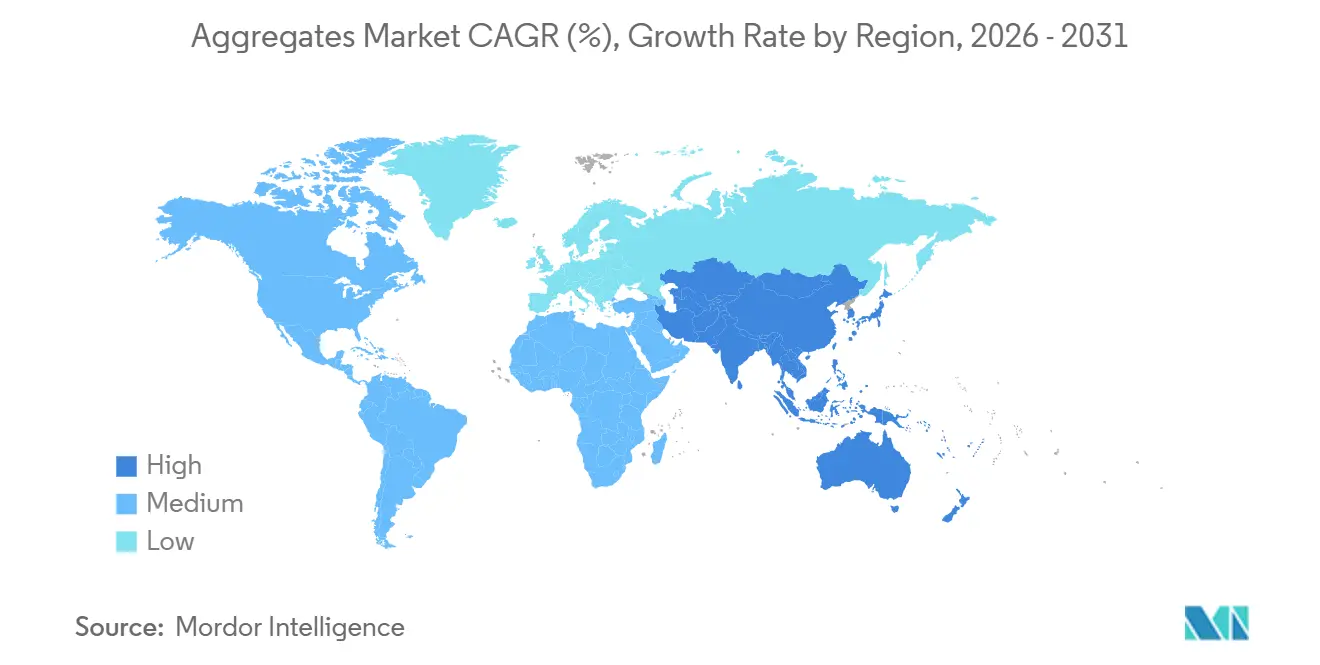

- By geography, Asia-Pacific captured 52.60% of the Aggregates market in 2025 and is advancing at a 7.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aggregates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued infrastructure megaproject pipeline | +1.8% | Global, with concentration in Asia-Pacific, Middle East, and North America | Long term (≥ 4 years) |

| Accelerating shift to ready-mix and high-spec concrete mixes | +1.2% | Global, led by urban centers in Asia-Pacific and Europe | Medium term (2-4 years) |

| Government incentives for low-carbon building materials | +0.9% | North America and EU, early adoption in select Asia-Pacific markets | Medium term (2-4 years) |

| Urbanization-led demand growth in cities | +1.5% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Heavyweight radiation-shielding aggregates for SMR programs | +0.3% | North America, Europe, and select Asia-Pacific countries with nuclear expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued Infrastructure Megaproject Pipeline

Quarry investments now benefit from a decade-long visibility, thanks to extended infrastructure budgets. Under the Infrastructure Investment and Jobs Act, the U.S. allocated a hefty sum for roads, bridges, and utilities, leading to a surge in aggregate contracts by 2025. Meanwhile, India's National Infrastructure Pipeline is channeling significant investments into highways and freight corridors, emphasizing the need for robust crushed-stone bases. In the Gulf, Saudi Arabia's ambitious NEOM project, alongside other megaprojects, is projected to consume substantial amounts of stone by 2030, putting a strain on regional reserves. These substantial investments not only justify the capital expenditure on high-capacity crushers and automated conveyors, boosting hourly output, but also encourage producers to secure long-term supply contracts with contractors, effectively managing price and volume risks.

Accelerating Shift to Ready-Mix and High-Spec Concrete Mixes

By 2025, ready-mix concrete is projected to account for a significant portion of concrete placements in major cities. Batching plants, adhering to a ±3% sieve tolerance for aggregates and capping moisture at 5%, show a clear preference for washed and graded materials. The Federal Highway Administration's updated guidelines advocate for calcined-clay blends, reducing cement content and simultaneously increasing aggregate volume per cubic meter. While European standard EN 206 mandates reactive-silica testing—incurring compliance costs but enhancing durability—producers investing in on-site laboratories and automated grading equipment gain an edge, achieving preferred-bidder status on public tenders that penalize variations.

Government Incentives for Low-Carbon Building Materials

In 2025, embodied-carbon reporting transitioned from a mere aspiration to a legal mandate. The Inflation Reduction Act allocates substantial funding towards low-carbon concrete initiatives, emphasizing the need for verified environmental declarations[1]Environmental Protection Agency, “Low-Carbon Concrete Grants,” epa.gov . Meanwhile, Canada has set an ambitious target: a significant reduction in embodied carbon for federal projects by 2030, a move that bolsters the adoption of recycled aggregates. The General Services Administration is now prioritizing suppliers who can document emissions from extraction energy and logistics. This shift creates a lucrative opportunity for quarries harnessing renewable electricity. Producers who electrify their haul trucks or integrate solar arrays into their crusher lines are reaping the benefits, enjoying price premiums and recouping their capital investments within a decade.

Urbanization-Led Demand Growth

Between 2025 and 2050, the United Nations forecasts an influx of city residents, predominantly in Asia and Africa, accounting for most of this growth. Each new urban dweller contributes to stone consumption, primarily for housing and transport infrastructure. In 2025, India's Smart Cities Mission spurred a surge in demand across tier-2 municipalities. Southeast Asian metropolitan areas invested in transit and sanitation projects, heavily reliant on sand, gravel, and crushed rock. Notably, high-rise constructions consume more concrete per square meter than their low-rise counterparts, intensifying the per-capita demand for aggregates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile haulage and fuel cost volatility | -1.1% | Global, acute in regions with dispersed quarries and limited rail infrastructure | Short term (≤ 2 years) |

| Lengthy and restrictive environmental permitting for new quarries | -0.8% | North America and EU, emerging in select Asia-Pacific markets | Medium term (2-4 years) |

| Crack-downs on river-sand mining causing regional shortages | -0.6% | Asia-Pacific (India, China, Southeast Asia), localized in coastal and riparian zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Haulage and Fuel Cost Volatility

Transporting aggregates, heavy and low in value, becomes uneconomic beyond a 50-kilometer truck journey. Diesel accounted for a significant portion of the delivered cost, and fluctuations in crude oil prices squeezed margins for haulers lacking hedge programs. While rail transport becomes cost-effective after 150 kilometers, only a small percentage of U.S. stone was transported by train, primarily because numerous quarries were without rail sidings. Due to higher diesel duties in Europe, operators began experimenting with electric and hydrogen haul trucks. In 2025, pilot fleets were successfully delivered to quarries in Sweden and Germany. Integrated firms that own their fleets and can optimize backhauls stand to benefit from the volatility in logistics.

Lengthy and Restrictive Environmental Permitting for New Quarries

In North America and Europe, obtaining permits now demands an environmental review, public hearings, and appeals, stretching over four to six years[2]European Aggregates Association, “Sustainable Quarrying Practices,” uepg.eu. In 2024, procedures under the National Environmental Policy Act in the U.S. tacked on an additional 18 months to the expansion of a limestone pit. In Germany, new gravel pits must provide biodiversity offsets that are double the disturbed area, leading to an increase in upfront capital costs. Such regulatory challenges not only hinder new market entrants but also bolster the position of established players with existing permits. This dynamic curtails regional price competition and dampens supply responsiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aggregate Type: Recycled Material Gains as Sand Dominance Erodes

Sand held a 40.69% share of the aggregates market in 2025, reflecting its central role in mortar and concrete finishing. Other aggregate types are projected to post a 7.90% CAGR, the highest across categories, as policy measures limit natural-sand extraction. Manufactured sand's share of India's fine-aggregate needs surged significantly in 2025, largely due to tightened supplies from river-sand bans. Crushed stone continues to be the primary choice for road bases and rail ballast. Gravel finds its niche in drainage layers, where its rounded particles enhance infiltration. Slag aggregates, known for their latent hydraulic properties that boost durability, remain influenced by trends in steel output.

By 2025, the European Union Waste Framework Directive aims to boost recycled concrete usage in Germany and the Netherlands, setting a recovery target for construction and demolition waste. Adhering to ISO 10426 quality norms, which mandate reactivity and chloride testing, is fostering standardized laboratory protocols. Producers investing in mobile crushers close to demolition sites are not only slashing haul distances but also trimming emissions – a metric increasingly monitored by public buyers. As municipal procurement departments prioritize contracts with higher recyclate content, the market for alternative materials in aggregates is poised for steady growth.

By Application: Construction Dominates while Specialty Uses Accelerate

In 2025, construction accounted for 47.59% of the global volume, with roadway projects alone utilizing substantial amounts of base layer per kilometer. Railway upgrades relied on high-strength granite ballast, ensuring abrasion values stayed below a certain threshold. To meet the stricter R-value codes introduced in 2025, building insulation turned to lightweight expanded clay and pumice. Meanwhile, other applications, including offshore wind and nuclear power, are anticipated to expand at a 7.82% CAGR through 2031, especially with the growing prominence of acoustic panels.

Offshore wind is poised to boost the aggregates market, as each turbine foundation requires substantial amounts of scour-protection rock. Additionally, small modular reactors are opting for barite or magnetite stone for radiation shielding, with prices significantly outpacing standard construction materials. While these specialty niches may be modest in tonnage, they offer margin advantages that can counterbalance the tighter margins seen in the more commoditized construction supply. Producers who can certify density and mineralogy find themselves well-positioned in these lucrative segments.

Geography Analysis

Asia-Pacific commanded 52.60% of the global aggregates market volume in 2025 and is forecast to advance at a 7.46% CAGR through 2031. Under the current Five-Year Plan, China's domestic demand has stabilized, bolstered by investments in urban rail and renewable energy grids. India's Bharatmala highway initiative is set to consume a substantial amount of crushed stone by 2027. Indonesia, Vietnam, and the Philippines have collectively committed significant funding towards transit and sanitation projects. Notably, Jakarta's MRT extension has placed an order for a considerable amount of ballast. Despite facing sporadic environmental restrictions on river-sand extraction, these initiatives firmly anchor the aggregates market in the region.

In 2025, North America saw a notable uptick in volume, spurred by the Infrastructure Investment and Jobs Act's enactment. The U.S. alone consumed a significant amount, with demand concentrated in Texas, California, and Florida—states that are pivotal growth corridors for both population and freight. In Canada, climate-adaptation initiatives heightened demand in British Columbia and Alberta. Simultaneously, Mexico's trend towards near-shoring has catalyzed a surge in industrial-park construction in Nuevo León and Guanajuato. Given the undersupply of rail infrastructure, the aggregates market heavily relies on truck fleets, making it sensitive to fluctuations in fuel prices.

Europe's aggregates market held steady in 2025. While Germany topped the volume charts, it channeled a larger share of its investments into rail electrification—a move that demands less stone compared to highway resurfacing. Between 2024 and 2026, the UK's HS2 project utilized a significant amount of crushed rock, bolstering regional quarries. Meanwhile, Nordic nations allocated resources to Arctic infrastructure, necessitating frost-resistant aggregates with an absorption rate below two percent. Though South America and Sub-Saharan Africa command smaller volumes, they present lucrative growth opportunities. By 2030, Saudi Arabia's NEOM mega-city and the UAE's Expo 2030 preparations are projected to create an annual demand surge, straining local supply chains.

Competitive Landscape

The aggregates market is moderately fragmented. Technology adoption separates leaders from laggards. Drone surveys reduce inventory error, predictive algorithms lift crusher uptime, and GPS dispatch cuts idle fuel burn. Mid-size operators that delay digitization face shrinking bid lists as contractors favor suppliers with real-time inventory portals. Meanwhile, white-space growth is visible in recycled aggregates and carbon-negative materials. Waste-management firms and cleantech startups challenge incumbents in urban recycling hubs, but quarry operators that deploy mobile crushing units close to demolition sites protect share. Incumbents monitor this risk by investing in specialty aggregates that retain relevance in advanced composites. Capital allocation now tilts toward reserves in regions with shorter permit windows, low carbon-intensity power grids, and proximity to megaprojects, underscoring a strategic pivot from raw volume to resilience.

Aggregates Industry Leaders

HOLCIM

CRH

Heidelberg Materials AG

Cemex S.A.B DE C.V.

Vulcan Materials Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Summit Materials, Inc. entered into a definitive agreement to be acquired by Quikrete Holdings, Inc. for USD 11.5 billion, including debt. The transaction combines Summit Materials, Inc.'s aggregates, cement, and ready-mix concrete businesses.

- July 2024: Heidelberg Materials AG announced a definitive purchase agreement to acquire Highway Materials, Inc., one of the largest independent aggregates and asphalt producers in the Greater Philadelphia market. The acquisition encompasses four crushed stone quarries, nine hot-mix asphalt plants, two clean fill operations, a concrete recycling facility, and a construction services business.

Global Aggregates Market Report Scope

Aggregate is a broad category of coarse to medium-grained particulate material used in construction activities, which includes sand, gravel, crushed stone, slag, recycled concrete, and geosynthetic aggregates.

The aggregates market is segmented by aggregate type, application, and geography. By aggregate type, the market is segmented into sand, gravel, crushed stone, slag, and other aggregate types (e.g., recycled, manufactured). By application, the market is segmented into construction, insulation, and other applications. The report also covers the market sizes and forecasts for the aggregates market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done in terms of volume (Tons).

| Sand |

| Gravel |

| Crushed Stone |

| Slag |

| Other Aggregate Types (Recycled, Manufactured, etc.) |

| Construction | Buildings |

| Railways | |

| Roadways | |

| Others | |

| Insulation | |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Aggregate Type | Sand | |

| Gravel | ||

| Crushed Stone | ||

| Slag | ||

| Other Aggregate Types (Recycled, Manufactured, etc.) | ||

| By Application | Construction | Buildings |

| Railways | ||

| Roadways | ||

| Others | ||

| Insulation | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What tonnage does the global aggregates market reach by 2031?

Forecasts indicate 84.23 billion tons by 2031, reflecting a 6.27% CAGR from 62.14 billion tons in 2026.

Which region contributes the most to aggregate demand today?

Asia-Pacific leads with 52.60% of global volume in 2025 and remains the fastest-growing area.

How large is the sand segment within the aggregates market?

Sand represented 40.69% of the aggregates market share in 2025, making it the dominant single category.

What trend supports rising recycled-aggregate adoption?

Tightened sand-mining regulations and circular-economy targets drive a projected 7.90% CAGR for recycled and manufactured alternatives.

How are fuel prices influencing aggregate suppliers?

Diesel swings increase delivered costs, so integrated producers hedge fuel and test electric haul trucks to protect margins.

Which application outside construction is growing quickest?

Offshore wind and nuclear shielding push other applications toward a 7.82% CAGR through 2031 due to their heavy stone requirements.

Page last updated on: