Dairy Spreads Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dairy Spreads Market Analysis by Mordor Intelligence

The Dairy Spreads Market was valued at USD 4.62 billion in 2025 and is projected to reach USD 4.85 billion in 2026, eventually growing to USD 6.26 billion by 2031, with a CAGR of 5.23% during the forecast period of 2026–2031. This growth is primarily attributed to the increasing consumer demand for convenient, ready-to-use, and value-added dairy products that align with changing consumption patterns. Additionally, the rising emphasis on health and nutrition is driving market expansion, as consumers seek dairy products with improved nutritional profiles, natural ingredients, and balanced formulations. The growing demand for clean-label products has further prompted manufacturers to minimize artificial additives and focus on producing spreads with simple, recognizable ingredients.

Key Report Takeaways

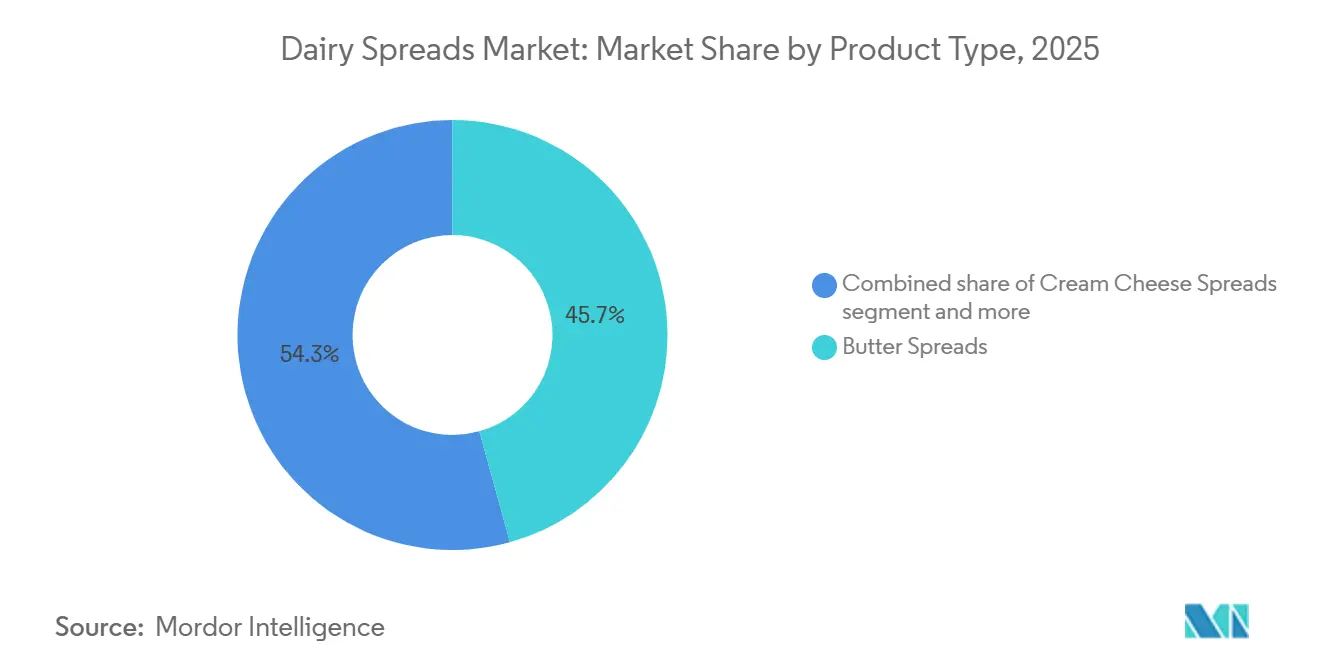

- By product type, butter spreads held 45.69% of the dairy spreads market size in 2025, while cream cheese spreads are projected to grow at 6.54% CAGR through 2031.

- By fat content, full-fat spreads accounted for 58.92% of total revenue in 2025, while reduced-fat spreads are forecast to expand at 6.51% CAGR through 2031.

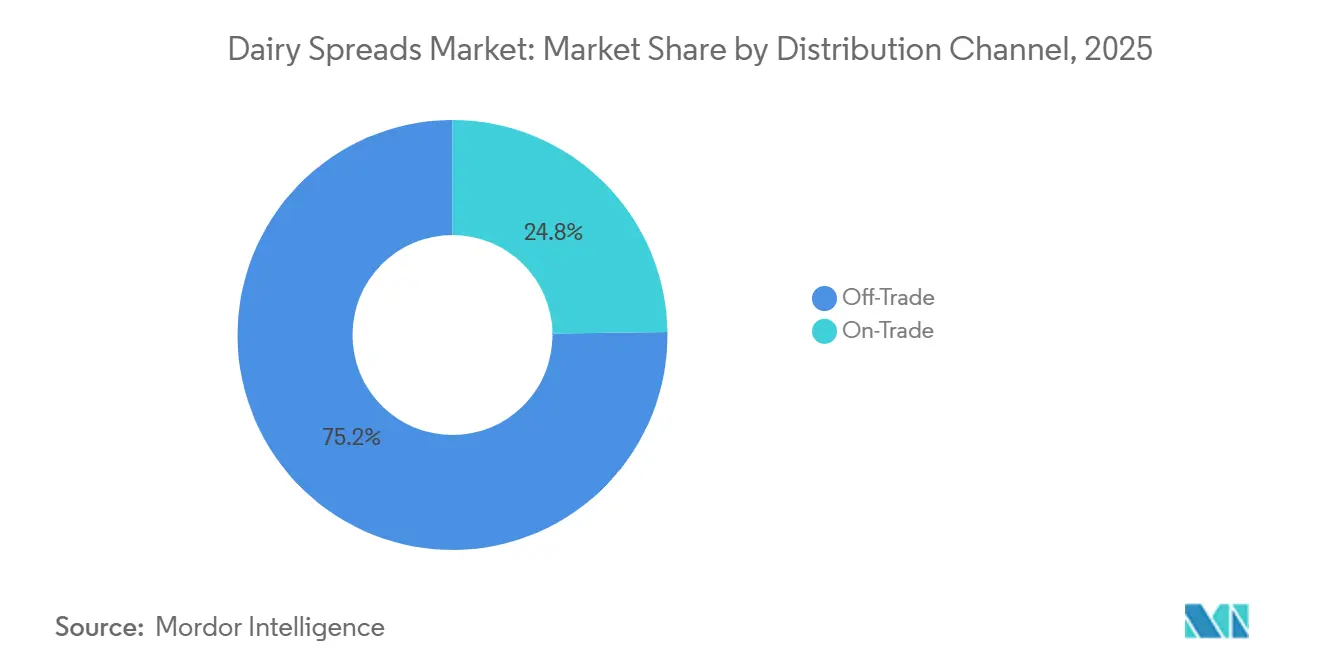

- By distribution channel, off-trade accounted for 75.23% of revenue in 2026, while on-trade is projected to grow at 5.92% CAGR through 2031.

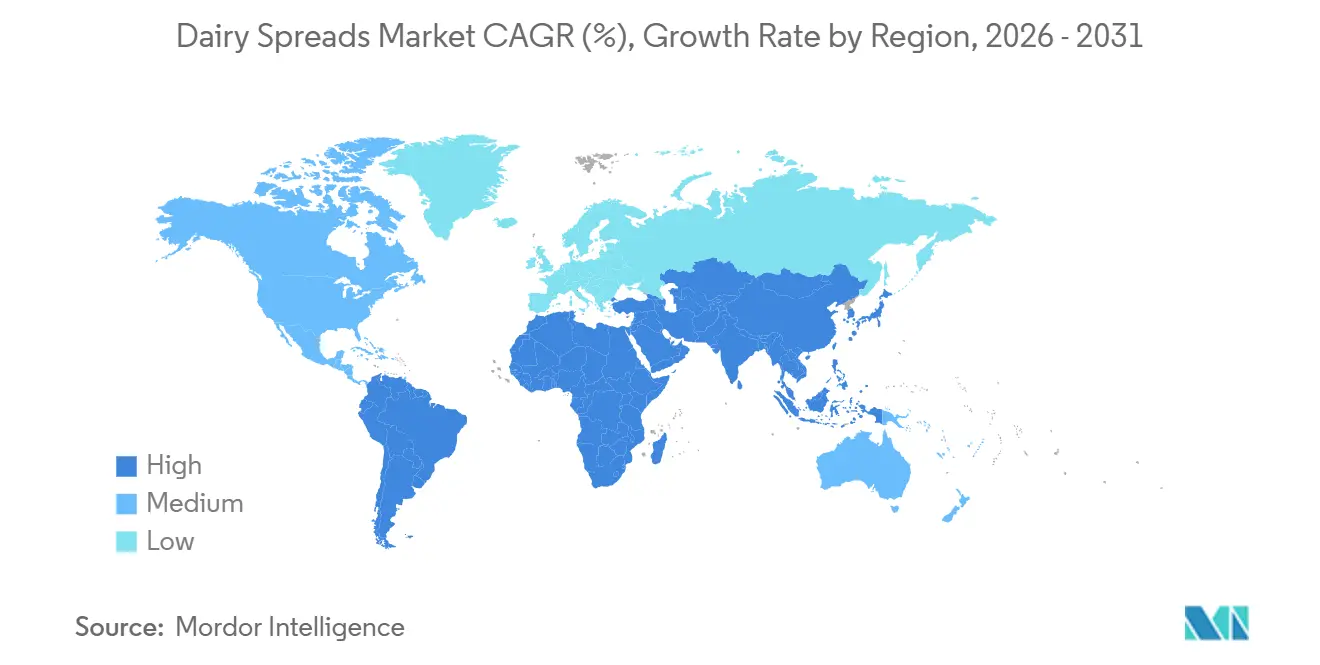

- By geography, Europe held 32.21% of revenue in 2025, while Asia-Pacific is expected to grow at 7.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dairy Spreads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for convenient and ready-to-use food products | +1.2% | Global, with pronounced effect in North America, Western Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Demand for premium and flavored dairy spreads | +1.0% | North America and Europe core; spill-over to Asia-Pacific and Middle East and Africa premium urban retail | Medium term (2–4 years) |

| Health awareness and demand for nutritional dairy products | +0.9% | Global; highest intensity in North America, Northern Europe, Australia | Medium term (2–4 years) |

| Innovation in clean label and natural ingredient-based spreads | +0.8% | Europe and North America, with growing regulatory influence shaping Asia-Pacific reformulation | Long term (≥ 4 years) |

| Demand for organic and grass-fed dairy products | +0.6% | North America, Western Europe; compliance framework under EU Regulation (EU) 2018/848 | Long term (≥ 4 years) |

| Advancements in dairy processing and packaging technologies | +0.5% | Global; innovation hubs in Europe, Asia-Pacific, North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Preference for convenient and ready-to-use food products

The increasing demand for convenient and ready-to-use food products is a key driver of the dairy spreads market. Consumers are prioritizing products that save preparation time while delivering taste, versatility, and ease of use. Dairy spreads offer benefits such as smooth spreadability, portion convenience, and immediate usability, making them well-suited to changing consumption patterns. The growing need for quick meal solutions and easy-to-use food ingredients has prompted manufacturers to develop innovative dairy spread varieties with improved textures, extended shelf life, and enhanced flavors. Additionally, the introduction of fortified dairy spreads with added nutrients and the use of sustainable packaging solutions are further enhancing the market. Furthermore, the rising popularity of packaged and value-added dairy products has driven the adoption of convenient formats, including resealable tubs, single-serve portions, and ready-to-spread options.

Demand for premium and flavored dairy spreads

The increasing demand for premium and flavored dairy spreads is driving growth as consumers seek unique taste experiences, innovative flavors, and high-quality dairy products. The rising preference for differentiated spread options has prompted manufacturers to go beyond traditional flavors by introducing herb-infused, spicy, sweet, and specialty dairy spread varieties. Premiumization trends are further encouraging the development of products with improved textures, natural ingredients, clean-label formulations, and enhanced nutritional profiles. Companies are prioritizing flavor innovation to appeal to consumers seeking indulgent and customized dairy experiences. For example, in June 2025, Bel Group introduced The Laughing Cow Spicy Chilli, the country’s first chili-flavored cheese spread portion, underscoring the growing focus on bold flavor innovations and product diversification.

Health awareness and demand for nutritional dairy products

Rising health awareness and the growing demand for nutritional dairy products are key factors driving the growth of the dairy spreads market. Consumers are increasingly seeking products that combine taste with enhanced nutritional value. The emphasis on balanced diets has led to a preference for dairy spreads with attributes such as reduced fat content, higher protein levels, calcium enrichment, and formulations using natural ingredients. This trend has prompted manufacturers to develop healthier options, including low-fat, reduced-salt, fortified, and clean-label dairy spreads that meet evolving consumer expectations. Furthermore, advancements in dairy processing technologies are enabling manufacturers to enhance nutritional profiles while preserving creamy texture, flavor, and spreadability. The demand for functional and health-oriented dairy products continues to drive innovation and support the adoption of nutritious dairy spreads in the market.

Innovation in clean label and natural ingredient-based spreads

Innovation in clean-label and natural ingredient-based spreads is a key factor driving the dairy spreads market. Consumers are increasingly favoring products made with recognizable ingredients, minimal processing, and fewer artificial additives. Growing awareness of ingredient transparency has prompted manufacturers to reformulate dairy spreads by reducing synthetic preservatives, artificial flavors, and unnecessary additives, while emphasizing natural dairy ingredients. The rising demand for authentic and healthier food options is fostering the development of organic, non-GMO, preservative-free, and naturally flavored dairy spreads. Additionally, manufacturers are utilizing advanced processing techniques to preserve freshness, texture, and shelf stability without compromising clean-label attributes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of lactose intolerance and dairy allergies | -0.7% | Asia-Pacific (China, SE Asia), Middle East and Africa, Sub-Saharan Africa; growing awareness in North America | Long term (≥ 4 years) |

| Fluctuations in milk prices and raw material availability | -0.8% | Global; sharpest in Europe, Oceania, and North America as major production hubs | Short term (≤ 2 years) |

| Short shelf life and storage challenges of dairy products | -0.5% | Asia-Pacific emerging markets, Middle East ad Africa, South America where cold chain infrastructure is limited | Medium term (2–4 years) |

| Stringent food safety and quality regulations | -0.4% | Global, with compliance factors most complex in the EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing prevalence of lactose intolerance and dairy allergies

The rising prevalence of lactose intolerance and dairy allergies poses a significant challenge for the dairy spreads market, as it restricts the consumption of milk-based products among individuals with digestive sensitivities or allergic reactions to dairy ingredients. Consumers with lactose intolerance often reduce or avoid traditional dairy spreads due to discomfort associated with lactose digestion, creating obstacles for manufacturers of conventional dairy-based products. Additionally, increasing awareness of food sensitivities has driven a shift toward lactose-free and plant-based alternatives, intensifying competition for traditional dairy spreads. According to the Food Standards Agency (FSA), in 2024, approximately 12% of consumers in England, Wales, and Northern Ireland reported having a food intolerance, underscoring the growing concern over dietary restrictions [1]Source: Food Standards Agency (FSA), "Prevalence of different types of food hypersensitivity among consumers in the United Kingdom", food.gov.uk.

Fluctuations in milk prices and raw material availability

Fluctuations in milk prices and raw material availability serve as significant constraints for the dairy spreads market. Milk and milk-derived ingredients are critical components in producing butter spreads, cheese spreads, and other dairy-based spread products. Variations in milk supply, driven by factors such as seasonal production changes, feed availability, climate conditions, and supply chain disruptions, directly influence manufacturing costs and production consistency. Increasing costs of essential dairy ingredients, including cream, butterfat, and milk solids, pose challenges for manufacturers in maintaining stable pricing while ensuring product quality. Furthermore, unpredictable raw material availability affects production planning, inventory management, and the ability to respond to shifting consumer demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cream Cheese Drives Category Premiumization

Butter spreads accounted for 45.69% of market revenue in 2025, driven by their widespread consumer preference, rich taste profile, smooth spreadability, and versatility compared to traditional dairy formats. The segment's growth is attributed to increasing demand for convenient dairy products that offer improved texture, extended usability, and enhanced flavor experiences. Manufacturers are focusing on innovations such as reduced-fat, lightly salted, organic, and blended butter spread formulations to align with changing consumer preferences for healthier and premium dairy choices. The natural dairy origin, creamy consistency, and strong consumer familiarity of butter spreads continue to reinforce their position in the overall dairy spreads market. According to the United States Department of Agriculture (USDA), India produced over 7.4 million metric tons of butter in 2025/26, making it the leading butter-producing nation globally and underscoring the robust production base supporting the availability and growth of butter-based spread products [2]Source: United States Department of Agriculture (USDA), "Major butter producing countries worldwide", usda.gov.

Cream cheese spreads are projected to be the fastest-growing segment in the dairy spreads market, with a CAGR of 6.54% during 2026–2031. This growth is driven by rising consumer preference for premium, smooth-textured, and flavorful dairy spread products. The segment's expansion is supported by increasing demand for innovative dairy formats that offer enhanced taste, convenience, and improved nutritional profiles. Growing consumer interest in indulgent yet versatile dairy products has led to the development of various cream cheese spread variants, including reduced-fat, protein-enriched, and clean-label formulations. Advances in dairy processing technologies have further improved product consistency, spreadability, freshness retention, and shelf stability, making cream cheese spreads increasingly appealing to modern consumers.

By Fat Content: Full-Fat Resilience Reframes Health Trade-Offs

Full-fat dairy spreads accounted for 58.92% of the market share in 2025, driven by consumer preference for rich flavor, creamy texture, and the enhanced sensory experience provided by higher-fat dairy formulations. This segment benefits from the natural taste profile and superior mouthfeel associated with full-fat products, which continue to influence consumer choices despite the availability of lower-fat alternatives. The growing demand for premium and indulgent dairy products has further supported the consumption of full-fat spreads, as consumers increasingly prioritize authentic dairy experiences with improved quality and taste. Additionally, advancements in dairy processing techniques have enabled manufacturers to enhance spreadability, consistency, and product freshness while preserving the traditional characteristics of full-fat dairy spreads.

Reduced-fat dairy spreads are expected to be the fastest-growing fat content segment in the dairy spreads market, with a projected CAGR of 6.51% during 2026–2031. This growth is driven by increasing consumer preference for balanced nutrition and healthier dairy alternatives that do not compromise on taste and texture. Rising awareness of dietary choices and the demand for lower-fat products are encouraging the adoption of reduced-fat formulations. The segment's growth is further supported by advancements in dairy processing technologies, enabling manufacturers to maintain creaminess, smooth consistency, and flavor while reducing fat content. Innovations focusing on reduced calories, enhanced nutritional profiles, clean-label ingredients, and improved formulations are also contributing to increased consumer acceptance.

By Distribution Channel: Foodservice Signals a Structural Shift

Off-trade channels accounted for 75.23% of the dairy spreads market share in 2025, driven by consumers' preference for convenient purchasing options, broader product accessibility, and the availability of diverse dairy spread varieties through retail formats. This segment's growth is supported by strong product visibility, organized shelf placement, attractive packaging, and the ability to offer multiple choices across flavors, fat levels, and product formulations. The expansion of modern retail infrastructure and advancements in cold-chain storage capabilities have improved the availability and freshness of dairy spreads, enhancing consumer confidence in off-trade purchases. Additionally, promotional activities, private-label growth, and the increasing availability of premium and specialty dairy spread products have further boosted consumer engagement.

The on-trade segment is projected to be the fastest-growing distribution channel in the dairy spreads market, with a CAGR of 5.92% during 2026–2031. This growth is driven by the rising demand for premium-quality dairy spread products through commercial consumption channels. The segment benefits from a growing preference for consistent taste, smooth texture, and high-performance dairy ingredients that enhance food preparation quality. The increasing adoption of customized dairy spread solutions, including flavored, specialty, and improved-texture formulations, is encouraging greater usage in professional environments. Manufacturers are focusing on bulk packaging formats, improved shelf stability, and tailored product offerings to meet the evolving needs of large-scale buyers.

Geography Analysis

Europe accounted for the largest share of the dairy spreads market, holding 32.21% in 2025. This dominance is attributed to strong consumer preference for high-quality dairy products, well-established dairy processing capabilities, and ongoing innovation in premium and specialty spread formulations. The region benefits from a robust dairy culture, rising demand for clean-label and natural dairy products, and advancements in processing technologies that improve texture, flavor, and overall product quality. According to the Department for Environment, Food and Rural Affairs (Defra), the United Kingdom produced 512,000 metric tons of cheese in 2025, up from 490,000 metric tons in 2024[3]Source: Department for Environment, Food and Rural Affairs (Defra), "", gov.uk. This highlights the region’s strong dairy manufacturing base, which supports the growth of dairy spread products.

Asia-Pacific is projected to be the fastest-growing region in the dairy spreads market, with a CAGR of 7.03% during 2026–2031. This growth is driven by shifting consumer preferences toward convenient, packaged, and value-added dairy products. Factors such as the adoption of modern food habits, increasing demand for flavored and innovative dairy formats, and improvements in dairy processing and cold-chain infrastructure are accelerating market expansion. Additionally, product diversification, including premium, reduced-fat, and plant-based spread alternatives, is enhancing consumer adoption, positioning Asia-Pacific as a dynamic growth region for dairy spreads during the forecast period.

North America remains a mature yet resilient market for dairy spreads. Innovation-led premiumization continues to sustain value growth, even as household penetration nears saturation. Consumer demand for healthier formulations, organic ingredients, and specialty dairy products drives ongoing product development across the region. South America offers selective growth opportunities, particularly in countries like Brazil, Argentina, and Chile. The increasing adoption of packaged dairy alternatives over traditional unprocessed fats is strengthening market demand in these regions. The Middle East and Africa region is experiencing gradual market expansion, supported by evolving dietary preferences, improved retail availability, growing interest in premium dairy products, and rising demand for convenient spreadable dairy formats.

Competitive Landscape

The dairy spreads market is fragmented, with key companies cofmpeting through product innovation, premium offerings, and advancements in dairy processing technologies. Prominent players such as Flora Food Group B.V., Groupe Lactalis S.A., Arla Foods amba, Fonterra Co-operative Group Limited, and Royal FrieslandCampina N.V. maintain strong market positions by leveraging extensive dairy expertise, diversified product portfolios, and the continuous development of value-added spreads. Companies are increasingly focusing on enhancing texture, taste, nutritional profiles, and clean-label formulations to meet evolving consumer preferences and achieve brand differentiation.

Innovation serves as a critical competitive strategy, with manufacturers investing in advanced processing methods, sustainable production practices, and next-generation ingredient technologies to improve product quality and functionality. Companies are increasingly targeting reduced-fat variants, plant-based alternatives, premium flavors, and convenient packaging solutions to align with changing consumption patterns. Beyond product formulation, technology is becoming a key differentiator. For example, in May 2026, Yili Group launched its Global Innovation Vanguard initiative in Cambridge, United Kingdom, emphasizing precision fermentation and AI-assisted ingredient combination, underscoring the growing role of advanced technologies in shaping the future of dairy-based products.

Market participants are also focusing on strategic partnerships, research and development initiatives, and portfolio expansion to enhance their competitiveness in the dairy spreads industry. Established companies are capitalizing on strong manufacturing capabilities and supply networks, while emerging brands concentrate on specialized offerings such as natural, sustainable, and health-oriented spread solutions. As demand continues to shift toward premium, functional, and innovative dairy spreads, companies are expected to prioritize technological advancements, sustainability, and product differentiation to strengthen their market presence.

Dairy Spreads Industry Leaders

-

Flora Food Group B.V.

-

Groupe Lactalis S.A.

-

Arla Foods amba

-

Fonterra Co-operative Group Limited

-

Royal FrieslandCampina N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bertolli introduced Bertolli Spreadable with Butter and Olive Oil, a versatile blend intended for cooking, baking, and spreading. The product consists of 57% dairy butter, 23% olive oil, water, and salt.

- May 2025: Lactalis has launched a new spreadable cheese under its Leerdammer brand, expanding beyond its traditional sliced cheese offerings. The Leerdammer Original Spreadable (125g) retains the brand's characteristic mild and nutty flavor in a soft, spreadable format.

- February 2025: Kerrygold launched sweet spreadable butters. These products are positioned as suitable toppings for various breakfast items, including pancakes, croissants, waffles, and bagels.

Global Dairy Spreads Market Report Scope

A dairy spread is a soft, malleable food product made from milk or milk constituents. It is primarily designed to be easily spreadable at room temperature or straight from the refrigerator. The dairy spreads market is segmented by product type, fat content, distribution channel, and geography. Based on product type, the market is segmented into butter spreads, cheese spreads, cream cheese spreads, and yogurt-based spreads. Based on fat content, the market is segmented into full-fat, reduced-fat, low-fat, and fat-free. Based on distribution channel, the market is segmented into off-trade and on-trade channels. The off-trade segment is further categorized into supermarkets/hypermarkets, convenience and grocery stores, specialty stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Butter Spreads |

| Cheese Spreads |

| Cream Cheese Spreads |

| Yogurt-Based Spreads |

| Full-Fat |

| Reduced-Fat |

| Low-Fat |

| Fat-Free |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Butter Spreads | |

| Cheese Spreads | ||

| Cream Cheese Spreads | ||

| Yogurt-Based Spreads | ||

| By Fat Content | Full-Fat | |

| Reduced-Fat | ||

| Low-Fat | ||

| Fat-Free | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for dairy spreads demand through 2031?

The dairy spreads market is projected to move from USD 4.9 billion in 2026 to USD 6.3 billion by 2031 at a 5.2% CAGR. Growth is supported by convenience, premium products, and broader foodservice use.

Which product type leads revenue, and which one is growing fastest?

Butter spreads led with 45.7% of revenue in 2025. Cream cheese spreads are growing faster and are forecast to expand at 6.5% CAGR through 2031.

Which regions are most important for future expansion?

Europe remained the largest regional contributor with 32.2% share in 2025. Asia-Pacific offers the strongest growth outlook and is forecast to expand at 7.0% CAGR through 2031.

How important is foodservice to future value growth?

Off-trade remains the main route with 75.2% share in 2026, but on-trade is growing faster at 5.9% CAGR. Foodservice matters because it supports premium formats, specialist pack sizes, and higher-value usage occasions.

Page last updated on: