Humectant Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 28.04 Billion |

| Market Size (2031) | USD 35.99 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Humectant Market Analysis by Mordor Intelligence

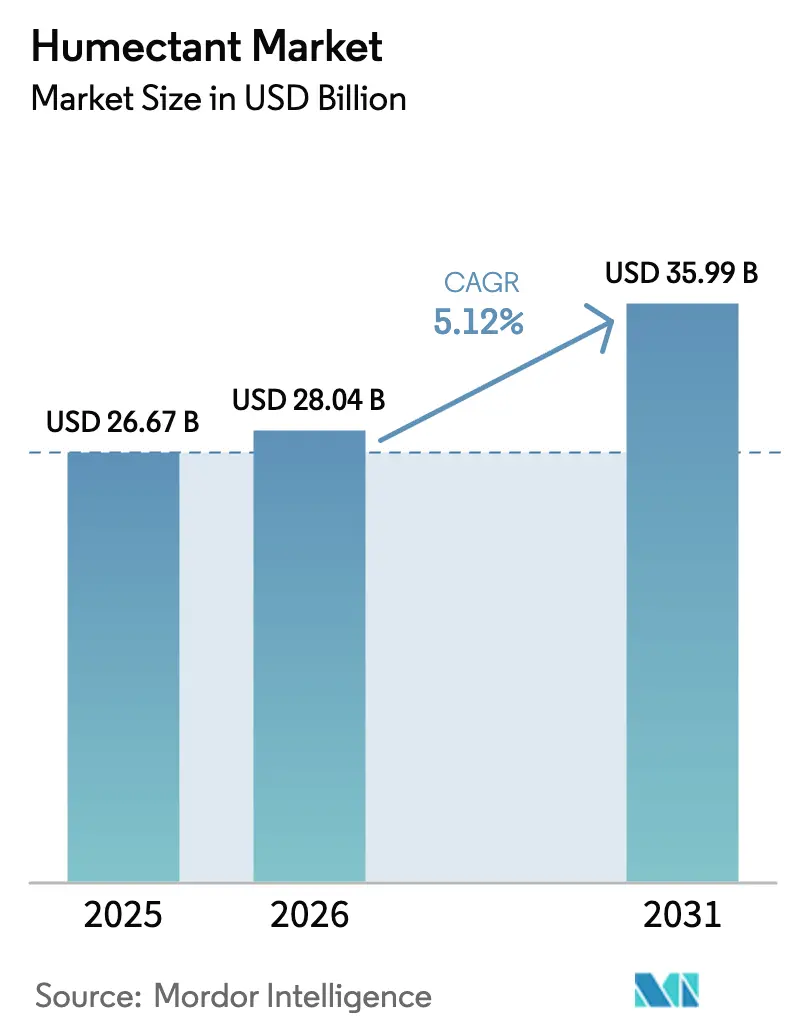

The Humectant Market size is expected to increase from USD 26.67 billion in 2025 to USD 28.04 billion in 2026 and reach USD 35.99 billion by 2031, growing at a CAGR of 5.12% over 2026-2031. Clean-label mandates in cosmetics, functional-food texture engineering, and structural glycerol oversupply from biodiesel refining are the three forces that keep the humectant market expanding despite propylene-glycol cost swings. Sorbitol’s wider usage approvals, together with pharmaceutical-grade humectant demand from the fast-rising nicotine-pouch segment, continue to lift volumes in North America and Scandinavia. Asia-Pacific retains pricing power by integrating excess glycerol from Indonesian and Malaysian biodiesel output into high-value hyaluronic-acid exports. Meanwhile, suppliers hedge feedstock risk by certifying bio-circular propylene glycol and locking in long-term crude-glycerol offtake contracts.

Key Report Takeaways

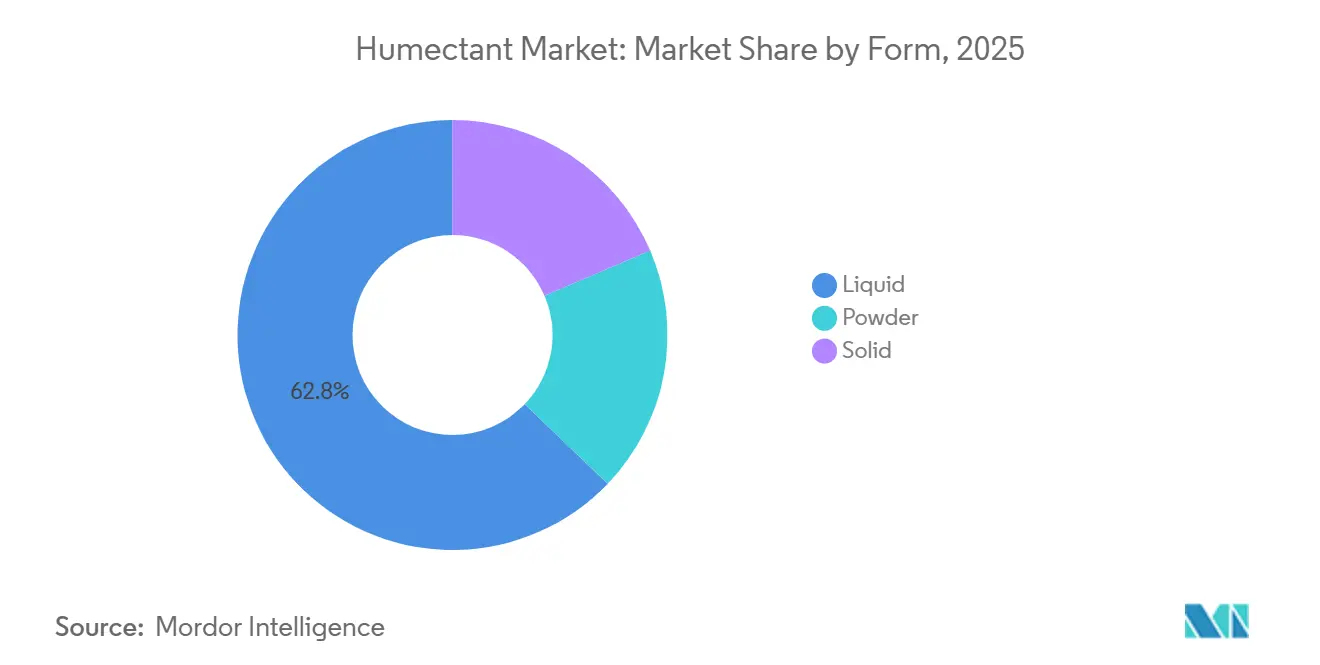

- By form, liquid humectants led with 62.84% of the Humectant market share in 2025. Powder formats are forecast to expand at a 5.21% CAGR between 2026 and 2031.

- By product form, glycerol commanded 44.36% of the Humectant market share in 2025. Sodium PCA is projected to record the fastest 6.12% CAGR during the forecast period (2026-2031).

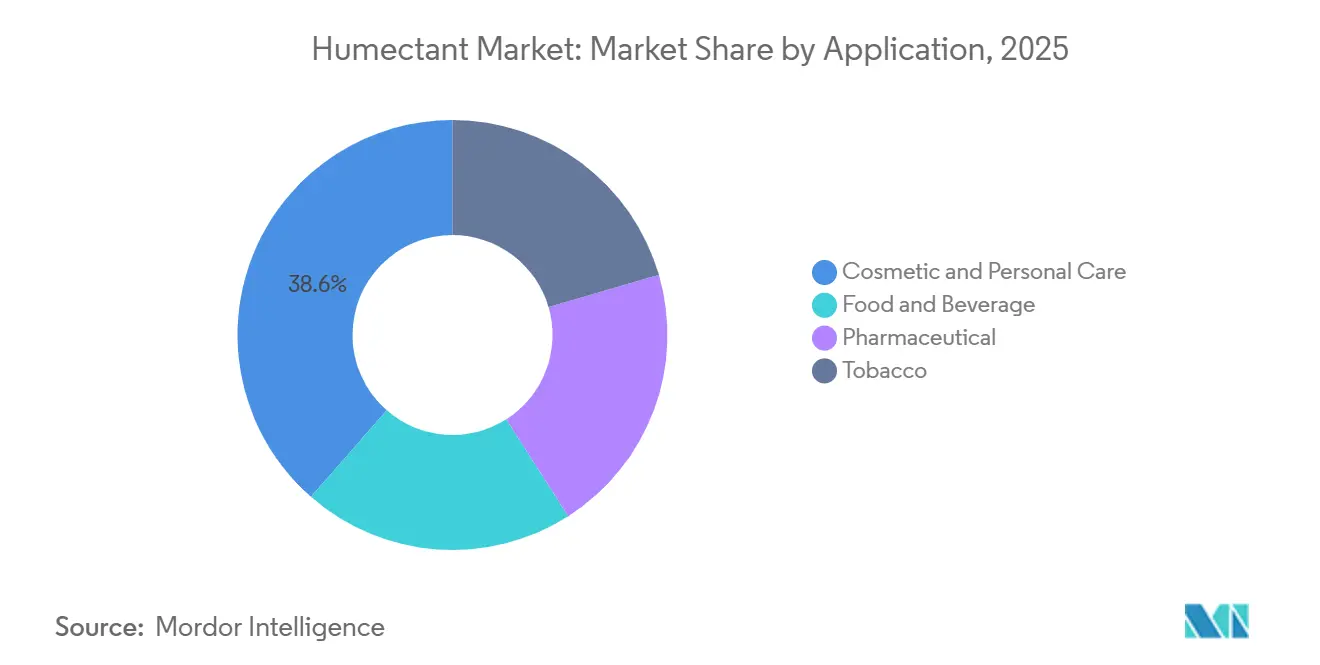

- By application, cosmetic and personal care applications captured 38.57% of 2025 revenue, while food and beverage is set to grow at a 5.74% CAGR during the forecast period (2026-2031).

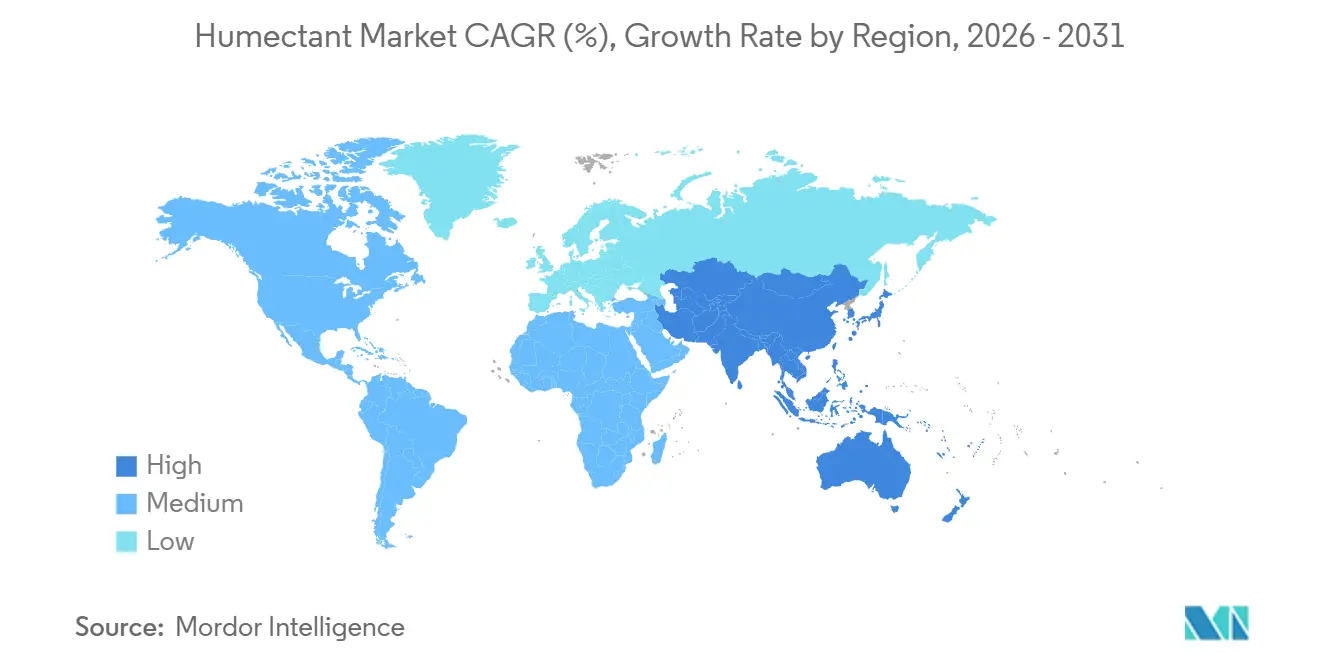

- By geography, Asia-Pacific accounted for 39.42% of 2025 revenue and is advancing at a 5.96% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Humectant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label moisturizers in cosmetics | +1.4% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific (China, South Korea, Japan) | Medium term (2-4 years) |

| Growth of functional food and beverage formulations for texture/shelf-life | +1.2% | Global, with early adoption in North America and Europe; accelerating in Asia-Pacific plant-based segments | Medium term (2-4 years) |

| Expansion of glycerol output from biodiesel refining | +1.0% | Europe, North America, Southeast Asia (Indonesia, Malaysia), and Brazil | Long term (≥ 4 years) |

| Moisture-managed nicotine-pouch boom | +0.9% | North America (U.S. dominant), Scandinavia, emerging in SSEA and Middle East | Short term (≤ 2 years) |

| Regulatory expansion of sugar-alcohol (sorbitol) usage | +0.7% | Global, with regulatory clarity from FDA (U.S.), EFSA (EU), and NMPA/CFDA (China) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label Moisturizers in Cosmetics

To meet the transparency demands of millennials and Gen Z, brands are shifting from synthetic emollients to more recognizable humectants like glycerol, sodium PCA, and hyaluronic-acid salts[1]U.S. Food & Drug Administration, “Cosmetics Modernization Act Updates,” fda.gov. In response to this trend, ADM completed a USD 26 million upgrade in Erlanger, Kentucky, in January 2026, adding pharmaceutical-grade glycerol and sodium PCA to its offerings. Stricter safety dossier requirements from the U.S. Modernization of Cosmetics Regulation Act of 2022 (MoCRA) and the European Union (EU) Cosmetics Regulation increase compliance costs for lesser-known synthetics. This shift benefits well-characterized humectants, which already possess International Nomenclature of Cosmetic Ingredients (INCI) clearance. While premium brands are willing to shoulder a 10-15% increase in ingredient costs, mass-market players are reformulating their products to maintain their presence on retailer shelves, especially those enforcing clean-label standards. Suppliers are capitalizing on their pricing power, especially for fermentation-derived variants that boast International Sustainability and Carbon Certification (ISCC) PLUS bio-based certification, further distancing themselves from petro-derived alternatives.

Growth of Functional Food and Beverage Formulations for Texture/Shelf-Life

Food formulators are using sorbitol and glycerol to keep sugar-reduced bakery items soft and to mimic the mouthfeel of full-sugar in plant-based protein bars. Beverage brands are increasingly relying on propylene glycol as a solvent and antimicrobial co-factor in natural flavor systems, moving away from sorbates and benzoates without compromising shelf life. Hyaluronic-acid hydrogels are now encapsulating probiotics and flavor oils for a timed release in functional shots, backed by peer-reviewed studies confirming their oral compatibility. Despite a 20-30% price discount compared to cosmetic grades, volume expansion is making it worthwhile. Ingredion is investing in this trend with a dedicated spray-drying line for powdered humectants at its USD 100 million plant in Indianapolis, set to open in H2 2026[2]Ingredion Inc., “Indianapolis Texture-Solutions Facility,” ingredion.com. This trend is first gaining traction in North America and Europe, but is set to accelerate in the Asia-Pacific, driven by the demand for water-activity control in plant-based meat analogues.

Expansion of Glycerol Output from Biodiesel Refining

Mandatory biodiesel blend targets in the EU, U.S., and Indonesia have created a structural surplus of glycerol. This surplus depresses feedstock prices but simultaneously increases the need for purification investments. In 2025, European crude glycerol spot values surged by 28% following revisions to Indonesian palm-oil exports. Meanwhile, in China, prices skyrocketed by 50%. This volatility compelled formulators to secure multi-year offtake deals, ensuring a stable supply. Integrated refiners, like Cargill, are upgrading crude streams to USP grades, reaping 3-4 times the value compared to technical grades. Qore’s QIRA project, which has been operational since May 2025, showcases a shift towards corn-dextrose derived 1,4-butanediol, completely bypassing glycerol. Looking ahead, renewable-diesel mandates suggest that glycerol availability will see the fastest rise in Europe and Brazil, providing a buffer for the humectant market against potential shortages.

Moisture-Managed Nicotine-Pouch Boom

In 2025, Philip Morris International reported shipping 879.6 million nicotine-pouch cans, marking a significant 36.6% increase from the previous year. Notably, a staggering 90% of this volume was concentrated in the United States. Each nicotine pouch, containing between 0.3 to 0.5 grams of either glycerol or propylene glycol, is driving an annual demand surge of 130,000 to 220,000 tons for pharmaceutical-grade humectants. The Food and Drug Administration's (FDA) guidelines for e-vapor liquids endorse a 30/70 ratio of propylene glycol to vegetable glycerin. Pouch manufacturers are adopting this standard, optimizing both flavor release and the product's shelf life. While Scandinavia witnesses a robust double-digit growth in pouch sales, regions like South & South-East Asia (SSEA) and the Middle East celebrated an impressive near-100% surge in 2025. In response to these trends, suppliers are now channeling their efforts, dedicating purification columns to meet nicotine-grade specifications, which are notably more stringent than those for cosmetic or food products. With volumes of heated tobacco stabilizing, nicotine pouches are poised to dominate as the primary driver of new volume growth in the near future.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile propylene-glycol feedstock prices | -0.8% | Global, with acute impact in Europe and North America due to energy-linked propylene pricing | Short term (≤ 2 years) |

| Stringent EU REACH limits on petro-humectants | -0.6% | Europe (primary), with spillover to export-oriented producers in Asia and North America | Medium term (2-4 years) |

| Allergen scrutiny of corn-based derivatives | -0.4% | Global, with heightened focus in North America and EU due to food-safety labeling mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Propylene-Glycol Feedstock Prices

Propylene glycol's (PG) reliance on propylene oxide makes it vulnerable to fluctuations in refinery utilization and natural gas costs, squeezing margins for independent humectant formulators. In Q4 2025, European spot PG prices surged 22% due to widening naphtha crack spreads, while North America experienced similar price swings linked to outages along the Gulf Coast. Dow and Evonik's HYPROSYN pilot, operational since November 2023 in Hanau, Germany, sidesteps the need for propylene oxide, achieving a 30-40% reduction in capital costs and ensuring more consistent output. Dow's bio-circular propylene glycol, certified by ISCC PLUS and introduced in March 2024 in Freeport, Texas, further distances PG pricing from traditional fossil-propylene sources. However, when formulation parity is reached, cost-sensitive food brands are pivoting to glycerol and sorbitol, resulting in a 0.8 percentage point reduction in the near-term forecast CAGR.

Stringent EU REACH Limits on Petro-Humectants

In 2024, the European Chemicals Agency bolstered its assessments on propylene glycol ethers, deepening the dossier and hiking registration fees to a staggering EUR 500,000 per tonnage band. Following the synthetic-polymer microparticle ban in October 2023, European brands are now favoring bio-based glycerol and sodium PCA, reflecting heightened consumer caution towards all petro-derived cosmetic ingredients. In a strategic move, BASF inked a long-term agreement with INOCAS in December 2024, aiming to source Macaúba kernel oil for its personal-care lines in Brazil and Europe, with pilot volumes set for 2025. Non-EU producers face a dilemma: either invest in Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) submissions or risk losing ground to their integrated European rivals. This scenario is pushing buyers to consolidate their volumes with suppliers who can guarantee cradle-to-gate traceability. As a result, this constraint is projected to shave off 0.6 percentage points from the CAGR of the humectant market between 2026 and 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominance Meets Powder Logistics Gains

In 2025, liquid humectants dominated the market, accounting for 62.84% of total revenue. Their direct metering into beverage syrups and cosmetic emulsions highlights their convenience. The liquid format of humectants, buoyed by Dow's March 2024 launch of bio-circular propylene glycol, which aligns with personal-care sustainability, remains the primary revenue driver. In high-throughput pharmaceutical and cosmetic plants, the batch-to-batch reproducibility of liquids is crucial, especially when closed-loop pumping minimizes contamination risks. Meanwhile, powder variants, expanding at a 5.21% CAGR, cater to distributors in emerging markets. These distributors, lacking refrigerated storage, find powders more cost-effective. Ingredion's new spray-drying line in Indianapolis is set to supply Asia-Pacific contract packers, who will transform these powders into ready-to-drink vegan shakes, underscoring the logistical profitability of powders.

Functional-food brand owners are increasingly turning to powders, as they seek shelf-stable sachets for e-commerce without the need for a cold chain. While solid formats like crystalline sorbitol and mannitol pellets remain niche, they command premium prices in biologics blister packs and moisture-sensitive drug capsules. Regulatory bodies show a preference for solids in modified-release oral forms, but these still lag behind liquids and powders in volume. Looking ahead, while the humectant market is set to maintain its liquid lead, both powder and solid formats present nimble players with opportunities for double-digit margins, especially in Southeastern Asia and the Middle East, where shipping at room temperature is essential.

By Product Type: Glycerol's Cost Edge Versus Sodium PCA's Premium Trajectory

In 2025, glycerol commanded a dominant 44.36% share of the revenue, bolstered by abundant biodiesel coproduct streams that kept its average spot prices below those of other polyols. Even with a 28% price spike in Europe in 2025, glycerol held its ground as the most economical humectant per kilogram, securing its foothold in the bakery, confectionery, and industrial sectors. While propylene glycol carves out niche roles as a solvent in injectable drugs and botanical extracts, its feedstock volatility poses a risk of substitution. Meanwhile, the HYPROSYN pilot in Germany, which offers an alternative to propylene oxide, holds promise in stabilizing PG cost fluctuations, though commercial scalability is still a couple of years away. Sorbitol, with its Generally Recognized As Safe (GRAS) status and low glycemic index, is fueling the launch of diabetic-friendly candies, bolstering its presence in North American convenience stores.

Sodium PCA is projected to achieve a 6.12% CAGR by 2031, carving out a niche in prestige skincare where bio-identical humectants command a 10-15% price premium. BASF's strategic supply agreement for Macaúba kernel oil not only provides a renewable feedstock for sodium-PCA synthesis but also aligns with EU brand buyers keen on steering clear of petrochemical inputs. Hyaluronic acid derivatives, rounding out the premium segment, are gaining traction in Asian derma-cosmetics, especially with a surge in registrations in China. While the market size for premium-grade humectants is modest, their lucrative margins empower suppliers to balance commodity risks with high-value offerings in dermatology and transdermal applications. Looking ahead, while glycerol is set to lead in volume, sodium PCA is poised for significant profit growth.

By Application: Cosmetics Lead, Food Accelerates, Tobacco Disrupts

In 2025, cosmetic and personal-care lines dominated the humectant market, accounting for 38.57% of the total demand. The surge in clean-label preferences and the rising popularity of hyaluronic acid in Asia have solidified cosmetics' leading position. Meanwhile, the food and beverage sector is witnessing a quicker ascent, boasting a 5.74% CAGR. This growth is driven by the demand for humectants in sugar-reduced confections and plant-based proteins, which rely on these agents to maintain texture post-sucrose removal. Although the food sector's humectant market lags behind cosmetics in sheer size, it compensates with a higher incremental volume, even if margins per kilogram are slimmer. The pharmaceutical sector's demand remains consistent, largely due to the need for United States Pharmacopeia (USP)-grade glycerol in vaccine cryoprotectants and biologic excipients.

As smokeless alternatives gain traction, nicotine pouches emerge as a game-changing sub-segment. PMI's projection of 879.6 million cans in 2025 translates to a demand of up to 220,000 tons of USP-grade humectants. The FDA's emphasis on diethylene glycol testing bolsters quality standards, alleviating buyer concerns. Consequently, the tobacco sector experiences a significant uptick, boasting double-digit growth rates that surpass those of cosmetics and food. Looking ahead to 2030, while cosmetics continue to lead in revenue generation, it's the tobacco and functional food sectors that are poised to make the most substantial contributions to the market's growth rate, diversifying the humectant market's reach into broader consumer health domains.

Geography Analysis

In 2025, Asia-Pacific accounted for 39.42% of total revenue and is projected to lead with a 5.96% CAGR from 2026 to 2031. Key drivers include surging hyaluronic-acid registrations in China, scale-oriented generic-drug excipient plants in India, and a biodiesel-linked glycerol glut in Indonesia. In a strategic move, BASF expanded its operations in Bangpakong, Thailand, in November 2025, boosting the output of alkyl-polyglucoside and humectant-compatible surfactants. This ensures a steady local supply for Association of Southeast Asian Nations (ASEAN) manufacturers. The sheer volume of the Asia-Pacific market acts as a buffer, shielding suppliers from margin declines seen in more mature markets.

The United States stands as the dominant force in the nicotine pouch market, accounting for over 90% of Philip Morris International’s (PMI) volume. This dominance is also driving a notable surge in the demand for pharmaceutical-grade glycerol. Meanwhile, in Europe, amendments to the REACH regulations are steering formulators towards bio-circular glycerol and sodium PCA. Responding to this trend, Dow has introduced ISCC PLUS-certified propylene glycol from its Stade, Germany, facility, commanding a premium price. This pricing strategy helps narrow the CAGR gap with Asia. Both North America and Europe benefit from strict sustainability standards, allowing them to pass on costs and enhance margins.

While South America, the Middle East, and Africa represent smaller markets, they exhibit significant growth potential. In South America, Brazil takes the lead as BASF channels Macaúba-kernel inputs into its local personal-care plants, simultaneously establishing an export route to Europe. The Middle East witnessed a doubling of pouch volumes in 2025, signaling a growing demand for humectants in tobacco harm reduction. In Africa, the pharmaceutical expansions in Nigeria and Kenya are spurring a localized demand for USP-grade glycerol, although logistical challenges hinder wider adoption. Looking ahead, Asia-Pacific is set to achieve the largest absolute revenue gains, North America and Europe will bolster profitability, and emerging regions will offer strategic opportunities for nimble entrants.

Competitive Landscape

The Humectant market remains moderately concentrated. Integrated majors chase bio-circular certifications; Dow’s March 2024 ISCC PLUS propylene-glycol launch in Freeport aligns with brand owner scope-3 mandates. Competitive leverage hinges on feedstock optionality and vertical integration; firms that secure both outrun peers tied to single-route petro-derivatives.

Humectant Industry Leaders

Dow

BASF

Cargill, Incorporated

ADM

Croda International Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Philip Morris International confirmed 879.6 million nicotine-pouch cans shipped in 2025, up 36.6% year-over-year, implying 130,000-220,000 tons of extra humectant demand.

- January 2026: ADM completed a USD 26 million expansion at Erlanger, Kentucky, adding capacity for reformulation-grade glycerol and sodium PCA aimed at clean-label cosmetics.

Global Humectant Market Report Scope

A humectant is a hygroscopic (water-attracting) substance used to retain moisture in products such as cosmetics, food, and medicine. They draw water from the air or deeper skin layers to the surface, enhancing skin hydration. Common examples include glycerin, hyaluronic acid, sorbitol, propylene glycol, and honey.

The Humectant market report is segmented by form, product type, application, and geography. By form, the market is segmented into liquid, powder, and solid. By product type, the market is segmented into glycerol, propylene glycol, sodium PCA, and sorbitol. By application, the market is segmented into cosmetic and personal care, food and beverage, pharmaceutical, and tobacco. The report also covers the market size and forecasts for humectants in 17 countries across major regions. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Liquid |

| Powder |

| Solid |

| Glycerol |

| Propylene Glycol |

| Sodium PCA |

| Sorbitol |

| Cosmetic and Personal Care |

| Food and Beverage |

| Pharmaceutical |

| Tobacco |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Liquid | |

| Powder | ||

| Solid | ||

| By Product Type | Glycerol | |

| Propylene Glycol | ||

| Sodium PCA | ||

| Sorbitol | ||

| By Application | Cosmetic and Personal Care | |

| Food and Beverage | ||

| Pharmaceutical | ||

| Tobacco | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What are the primary growth drivers behind humectant demand after 2025?

Clean-label reformulation in cosmetics, functional-food texture engineering, expanded glycerol supply from biodiesel refining, and the fast-growing nicotine-pouch category collectively lift demand.

Which form factor is gaining share within the humectant landscape?

Powder formats, supported by 5.21% CAGR through 2031, gain share because they cut cold-chain costs in emerging markets while retaining functionality after reconstitution.

Why is sodium PCA growing faster than glycerol in value terms?

Sodium PCA commands premium pricing in anti-aging skincare and transdermal platforms, enabling a 6.12% CAGR despite lower absolute volume compared with commodity glycerol.

How will EU REACH revisions influence supplier strategies?

REACH dossier costs advantage integrated European suppliers and bio-based variants, prompting non-EU producers to either fund registrations or pivot toward certified renewable feedstocks.

What is the current market size of Humectant Market?

The Humectant Market size is expected to increase from USD 26.67 billion in 2025 to USD 28.04 billion in 2026 and reach USD 35.99 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

Page last updated on: