Digital Video Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

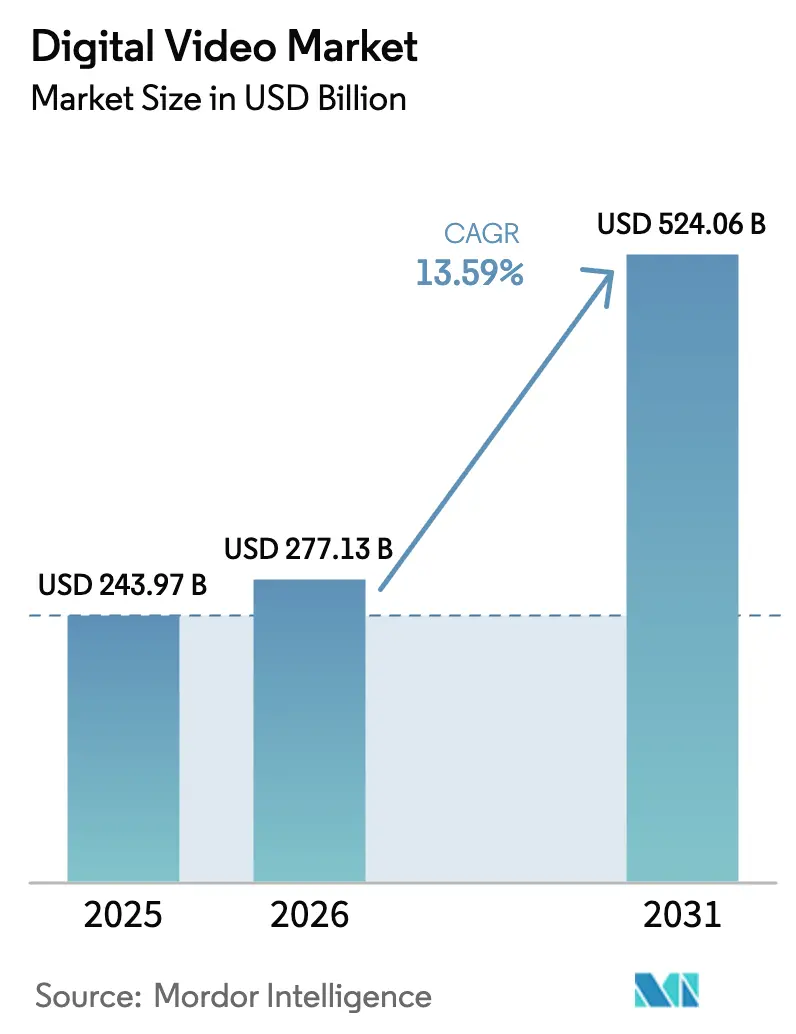

| Market Size (2026) | USD 277.13 Billion |

| Market Size (2031) | USD 524.06 Billion |

| Growth Rate (2026 - 2031) | 13.59% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Video Market Analysis by Mordor Intelligence

The digital video market size is expected to grow from USD 243.97 billion in 2025 to USD 277.13 billion in 2026 and is forecast to reach USD 524.06 billion by 2031 at 13.59% CAGR over 2026-2031. Streaming services continue to pull audiences away from linear television as advertisers redirect budgets toward connected and mobile screens, with digital video set to attract nearly 60% of global TV and video ad spend in 2025. [1]Interactive Advertising Bureau, “Digital Video Is Set to Capture Nearly 60% of All TV/Video Ad Spend in 2025,” streamingmedia.com A plateau in subscription growth inside mature territories is steering platforms toward hybrid tiers that blend subscriptions with advertising, while telco bundles unlock new subscriber pools in emerging regions. Mobile-first viewing dominates in Asia and Africa, yet smart TV adoption is rising quickly, creating parallel large-screen engagement opportunities. Consolidation among major media and technology houses is reshaping competitive dynamics, even as creator-led, user-generated ecosystems disrupt traditional production economics.

Key Report Takeaways

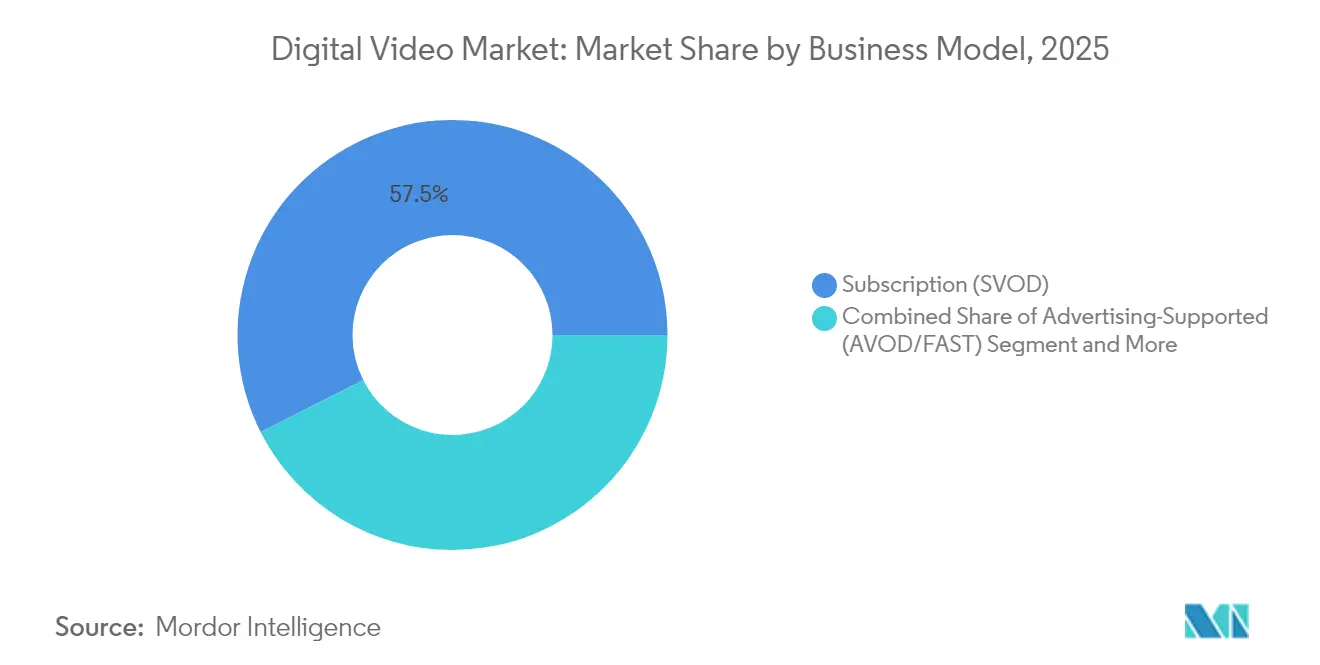

- By business model, the SVOD segment held 57.45% of digital video market share in 2025, while the AVOD/FAST segment is projected to grow at an 17.85% CAGR through 2031.

- By content type, long-form VOD commanded 59.35% share of the digital video market size in 2025, whereas short-form and user-generated video is forecast to expand at a 15.75% CAGR to 2031.

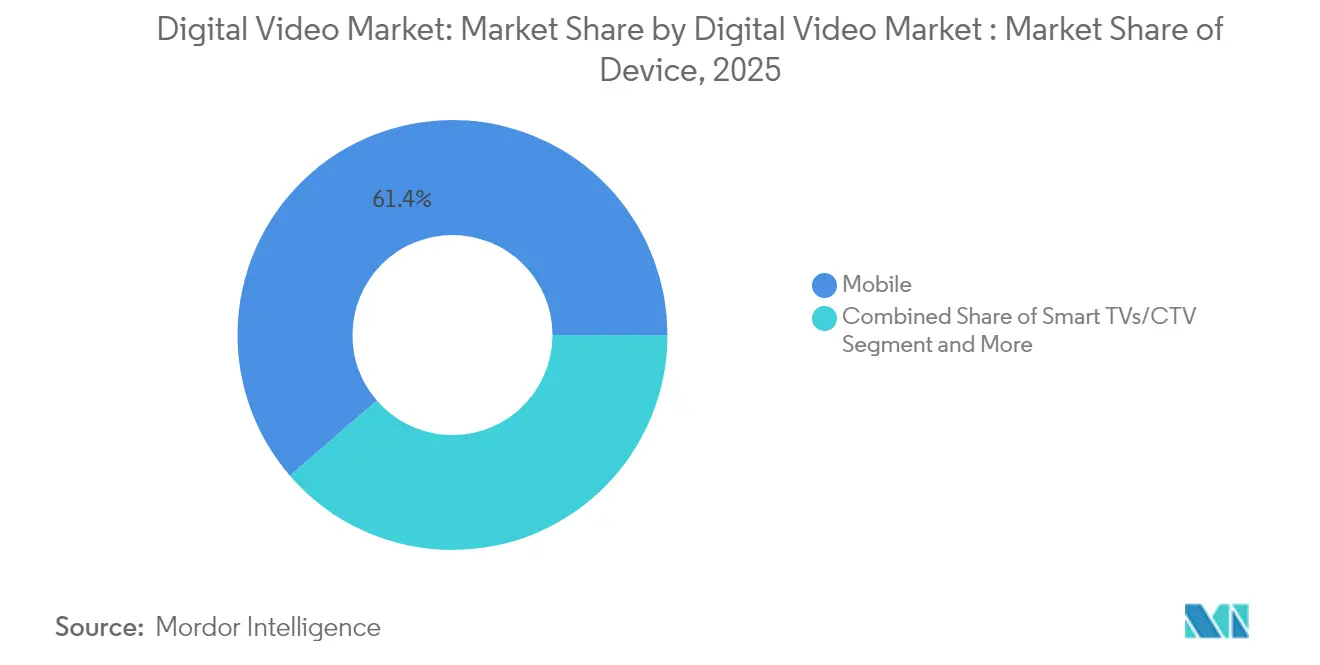

- By device, mobile accounted for 61.35% of the digital video market size in 2025; smart TV and connected TV devices are advancing at a 15.52% CAGR between 2026-2031.

- By geography, North America led with a 34.62% revenue share in 2025, while Asia-Pacific is set to post the fastest regional CAGR of 14.85% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Video Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription saturation plateau pushing hybrid models | +2.8% | North America, Western Europe | Medium term (2-4 years) |

| Telco-bundled SVOD packages accelerating penetration | +2.1% | MENA, Eastern Europe, Latin America | Medium term (2-4 years) |

| FAST channels monetising long-tail content | +1.9% | North America, Western Europe | Short term (≤ 2 years) |

| Mobile-first video consumption surge | +2.4% | ASEAN, Africa, India | Long term (≥ 4 years) |

| AI-driven content localisation cutting churn | +1.6% | Europe, Global | Medium term (2-4 years) |

| Creator-economy-led UGC monetisation | +1.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subscription Saturation Plateau Pushing Hybrid Models

Mature subscription markets now average four paid services per household, prompting platforms to add lower-priced, ad-supported tiers that widen reach without eroding premium pricing. Advertising is forecast to represent 28% of global streaming revenue by 2028, up from 20% in 2023. Netflix demonstrated the viability of this pivot as its ad tier helped lift Q1 2025 revenue by 13% versus the prior year. The strategic shift demands new competencies in dynamic ad insertion, measurement, and brand-safety controls, areas where technology partners and in-house ad platforms are becoming critical. Competitive positioning now rests on the ability to balance premium originals with scalable ad inventory that meets marketer performance benchmarks.

Telco-Bundled SVOD Packages Accelerating Penetration

Operator-led bundles are projected to distribute 365 million SVOD subscriptions by 2029, equivalent to 20% of global subs. In the MENA region, telco partnerships are on track to push the streaming video market to USD 1.5 billion by end-2025. Bundles lower customer acquisition costs, shrink churn, and extend reach into prepaid and rural segments that lack credit cards. For operators, video adds incremental ARPU and strengthens loyalty amid intensifying mobile competition. Streaming services in Latin America and Eastern Europe are adopting similar strategies, signalling a global expansion of carrier billing and data-inclusive plans as a preferred path to scale.

FAST Channels Monetising Long-Tail Content

Free ad-supported streaming television leverages vast back-catalog libraries, generating incremental revenue while offering cost-free entertainment that eases consumer fatigue with paid subscriptions. FAST viewership is expected to climb 15% annually to 2027, with Tubi, Pluto TV, and the Roku Channel leading in session growth. Content owners employ channelised playlists to surface niche genres and franchise spinoffs, creating fresh ad inventory with limited incremental content spend. The model aligns with advertiser demand for brand-safe, contextual placements at scale. Media conglomerates increasingly treat FAST as a complementary bottom-funnel layer that lengthens a title’s monetisation arc and feeds audience discovery for premium tier

Mobile-First Video Consumption Surge

Mobile accounted for 62% of global streaming hours in 2024, and 5G connections surpassed 2 billion by year-end, underpinning accelerated demand for high-definition on-the-go viewi. In Southeast Asia, TikTok leads engagement despite a recent decline in ad reach, illustrating the pivot toward snackable, vertical formats. Producers increasingly shoot simultaneous horizontal and vertical masters while platforms optimise bitrates to cope with inconsistent network conditions. Mobile carriers leverage zero-rating and video-specific data packs to upsell 5G subscriptions. Growth potential remains strongest in India and sub-Saharan Africa, where mobile represents the primary broadband access point.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising content acquisition costs squeezing margins | -1.9% | Global, most acute in North America | Medium term (2-4 years) |

| Fragmented regulatory landscape for cross-border streaming | -1.2% | EU, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Ad-blocking and tracking-prevention reducing AVOD yield | -1.4% | North America, Europe | Medium term (2-4 years) |

| Piracy and password-sharing curtailing SVOD revenue | -1.7% | Latin America, Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Content Acquisition Costs Squeezing Margins

Production inflation continues to outpace revenue growth, with Netflix allocating the majority of its USD 17 billion 2024 budget to originals and premium licenses. Warner Bros. Discovery posted a 25% content revenue decline in Q1 2025 as box-office weakness rippled into streaming performance. Platforms now apply stricter return-on-investment metrics, shorten episode orders, and pursue cheaper reality formats. Intensified bidding for live sports further elevates rights fees, pressuring margins unless offset by advertising or pricing gains. Smaller services feel the squeeze most acutely, often resorting to licensing out exclusives or merging to secure scale.

Fragmented Regulatory Landscape for Cross-Border Streaming

Streaming services face divergent data-localisation, content-quota, and tax rules, raising compliance overhead and delaying market entries. The U.S. Trade Representative lists China’s cloud restrictions and Russia’s local-processing mandates among the toughest barriers to digital trade. The EU Copyright Directive requires proactive infringer controls, complicating user-generated uploads. Services invest heavily in legal, metadata, and localisation workflows to meet overlapping standards. Regulatory uncertainty influences footprint strategies, often favouring joint-venture models with local entities that already hold broadcast licences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Hybrid Strategies Reshape Revenue Streams

SVOD commanded 57.45% of the digital video market size in 2025, yet the AVOD and FAST cohort is projected to accelerate at an 17.85% CAGR during 2026-2031, raising its share of total revenue materially. Advertising revenue is forecast to account for 28% of streaming income by 2028, reflecting intensifying platform efforts to balance premium pricing with broader audience reach. Major incumbents such as Netflix and Disney have launched ad-lite tiers that offer price flexibility while generating high-margin inventory suitable for performance-oriented marketers. The competitive field now rewards ownership of first-party data, dynamic ad-insertion engines, and programmatic marketplaces that meet brand-safety standards.

Transactional models including TVOD and pay-per-view secure premium pricing for live sports, early-release films, and specialty events. Warner Bros. Discovery’s Q1 2025 streaming revenue rose 9% to USD 2.656 billion, buoyed by a 35% surge in advertising tied to ad-lite subscribers. Bundled offerings that combine live channels with SVOD libraries appeal to households looking for a single interface. Virtual MVPD consolidation—the merger of Hulu + Live TV and Fubo under Disney majority control—illustrates scale’s importance for negotiating carriage fees and sustaining content spending. Increased diversification across revenue streams is thus a strategic hedge against macro-economic shifts and fluctuating subscriber sentiment.

By Type: Short-Form Content Disrupts Traditional Viewing

Long-form VOD retained 59.35% share of the digital video market in 2025, underscoring the enduring appeal of serialised dramas, feature films, and documentaries. However, user-generated and short-form video is on course to climb at a 15.75% CAGR, propelled by creator-economy monetisation frameworks and the viral power of social feeds. The creator economy is projected to top USD 600 billion in value by 2030 as direct fan funding, merchandise, and brand sponsorship scale alongside video advertising.

Platforms now integrate tip jars, shoppable overlays, and episodic packaging that elevate short-form franchises into multi-format IP. YouTube’s updated creator tools segment clips into seasons and add multitrack dubbing, thereby attracting connected-TV audiences who prefer lean-back experiences. Meanwhile, traditional studios experiment with mobile-first spin-offs to test story arcs before greenlighting full series. The blend of aspirational and participatory viewing broadens engagement touchpoints and deepens time spent on platform, encouraging marketing teams to allocate budgets across both premium and grassroots content.

By Device: Smart TVs Challenge Mobile Dominance

Mobile devices delivered 61.35% of streaming hours in 2025, yet smart TVs and connected TV hardware form the fastest-growing category, projected at a 15.52% CAGR for 2026-2031. Rising panel quality, voice navigation, and sophisticated home screens are shifting long-form consumption back to the living room environment. The Roku Channel climbed to the #2 app in the United States by engagement in Q1 2025 while platform revenue reached USD 881 million, underscoring CTV’s advertising potential.

For advertisers, connected TV offers addressable ad units within a premium environment, with U.S. spend forecast to hit USD 26.6 billion in 2025. Gaming consoles and PCs retain niche importance for esports streaming and interactive formats that blend gameplay with viewing. Device makers differentiate with AI-powered picture and sound optimisation and integrated FAST hubs that surface curated linear channels. The multi-device reality obliges content owners to ensure seamless authentication, synchronised progress tracking, and codec adaptation so that quality remains consistent as viewers move between screens.

Geography Analysis

North America held 34.62% of digital video market share in 2025, supported by high broadband penetration, advanced advertising infrastructure, and aggressive original-content investment. Consolidation is intensifying, as evidenced by Disney’s 70% stake in the combined Hulu-Fubo entity, which now serves 6.2 million North American subscribers. Connected-TV ad spend will rise 13% to USD 26.6 billion in 2025, confirming advertiser confidence in measurable, premium large-screen inventory. Yet market saturation limits new subscriptions, shifting management focus toward churn reduction and ARPU optimisation via live sports, gaming integrations, and enhanced personalisation.

Asia-Pacific represents the fastest-growing region with a 14.85% projected CAGR, driven by widespread mobile adoption, rapid fibre rollout, and youthful demographics that favour digital-first entertainment. Domestic giants dominate China, where iQIYI’s Q1 2025 earnings signal renewed revenue momentum amid economic recovery. India’s market is buoyed by Amazon’s commissioning of 37 local originals in early 2024, underscoring the scale of localisation investment . Telco bundling proves essential in ASEAN and South Asia, where prepaid user bases rely on carrier billing. Short-form and social video remain dominant in Indonesia and the Philippines, compelling subscription platforms to introduce lower-price mobile-only tiers.

Europe’s digital video landscape shows heterogeneous growth, shaped by regulatory complexity and linguistic diversity. Ad-supported tiers gain ground as household budgets tighten; the continent’s AVOD pivot is projected to reshape revenue mixes through 2025. The French video content market may reach €9.6 billion (USD 10.4 billion) by 2029, propelled by SVOD spending despite strict local-content obligations. Central and Eastern Europe relies heavily on pay-TV and telco packages, which supply 25% of paid streaming subscriptions. AI-enabled localisation trims churn by tailoring metadata, subtitles, and artwork across diverse language clusters, providing a competitive edge to services that master data pipelines and regional compliance.

Competitive Landscape

Competition spans legacy studios, technology platforms, telecommunications operators, and a rapidly maturing creator economy. Strategic consolidation concentrates negotiating clout for premium sports rights and blockbuster IP, evidenced by Disney’s absorption of Hulu alongside Fubo’s vMVPD assets. Vertical integration from production through distribution reduces third-party licensing risk and improves margin capture. At the same time, niche specialists carve white-space territory in anime, faith-based, and regional content, capturing loyal communities overlooked by mass-market services.

Technology serves as a decisive differentiator. Roku’s AI-guided home-screen rows boosted both engagement and ad reach following their rollout in Q1 2025.[2]Roku, “Q1 2025 Shareholder Letter,” roku.com Peacock’s Media EBITDA climbed 21% in the same period, illustrating scale economics once fixed platform costs are defrayed over a sizable subscriber base.[3]Comcast, “Comcast Reports 1st Quarter 2025 Results,” comcast.com Emerging vendors deliver AI localisation, cloud encoding, and contextual ad-replacement services that streamline operations for multi-territory launches.

The creator ecosystem accelerates fragmentation. YouTube and TikTok empower talent to bypass gatekeepers, while rights-tech startups facilitate revenue splits, merchandise, and fan-funded experiences. Studios experiment with talent incubators and short-form pilots to de-risk larger commissions. Competitive boundaries expand into adjacent experiences such as gaming, live commerce, and metaverse environments, encouraging partnerships that cross-pollinate user bases and data sets. The result is a market where incumbents battle on multiple fronts, from blockbuster tentpoles to community-driven micro-channels.

Digital Video Industry Leaders

Apple Inc.

Netflix, Inc.

Walt Disney Company

Comcast Corporation

AT&T Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Warner Bros. Discovery reported Q1 2025 streaming revenue of USD 2.656 billion, up 9%, with advertising from ad-lite subscribers rising 35%

- May 2025: Roku’s Q1 2025 Platform revenue increased 17% to USD 881 million as streaming hours rose 84% year over year

- May 2025: Paramount added 1.5 million Paramount+ subscribers in Q1 2025, lifting direct-to-consumer revenue 9% to USD 2.04 billion

- April 2025: Comcast posted a 21% Media EBITDA increase, supported by a 16% rise in Peacock revenue

Global Digital Video Market Report Scope

Digital video is an electronic representation of moving visual images (video) in the form of encoded digital data. Publishers can monetize video content with advertising which can appear before, during, or after the videos.

The digital video market is segmented by business model (subscription, advertising, download-to-own (DTO), other business models), by type (video on demand, online video), by device (laptop/PC, mobile, other devices), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Subscription Video-on-Demand (SVOD) |

| Advertising-Supported Video (AVOD and FAST) |

| Download-to-Own / Transactional (TVOD) |

| Hybrid / Other Models (Pay-Per-View, Crowdfunded) |

| Video-on-Demand (Long-form) |

| Online Video (Short-form and User-Generated) |

| Mobile Phones and Tablets |

| Smart TVs / Connected TV Devices |

| PCs and Laptops |

| Gaming Consoles and Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | Rest of Africa |

| By Business Model | Subscription Video-on-Demand (SVOD) | ||

| Advertising-Supported Video (AVOD and FAST) | |||

| Download-to-Own / Transactional (TVOD) | |||

| Hybrid / Other Models (Pay-Per-View, Crowdfunded) | |||

| By Type | Video-on-Demand (Long-form) | ||

| Online Video (Short-form and User-Generated) | |||

| By Device | Mobile Phones and Tablets | ||

| Smart TVs / Connected TV Devices | |||

| PCs and Laptops | |||

| Gaming Consoles and Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and | United Arab Emirates | ||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | Rest of Africa | |

Key Questions Answered in the Report

What is the current value of the digital video market?

The digital video market stands at USD 277.13 billion in 2026.

How fast is the digital video market expected to grow?

The market is forecast to expand at a 13.59% CAGR, reaching USD 524.06 billion by 2031.

Which business model is growing quickest within digital video?

Advertising-supported video, including FAST channels, is projected to post an 17.85% CAGR through 2031.

Why are telco bundles important for streaming growth?

Telco packages lower acquisition costs and could account for 20% of global SVOD subscriptions by 2029.

Which region will add the most new digital video revenue?

Asia-Pacific is set to record a 14.85% CAGR between 2026-2031, making it the fastest-growing region.

How does smart-TV growth affect advertising strategies?

Connected-TV ad spend in the United States is projected to rise 13% to USD 26.6 billion in 2025, reflecting advertiser migration to large-screen, addressable environments.

Page last updated on: