Online Video Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

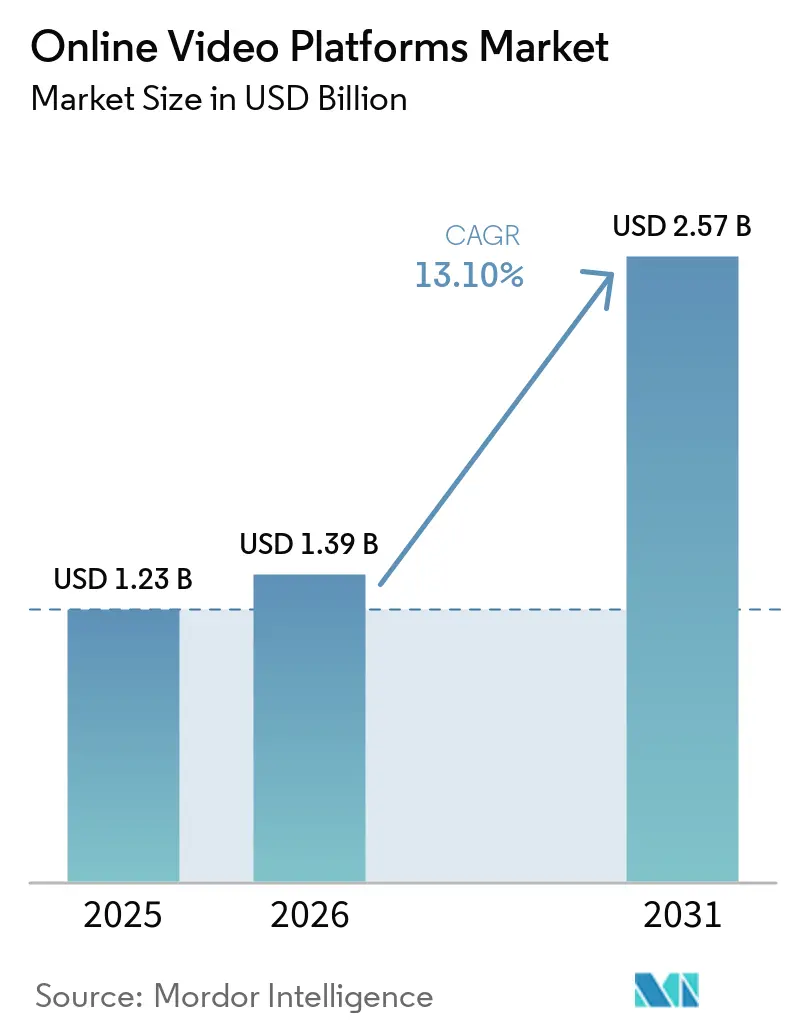

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 13.10% CAGR |

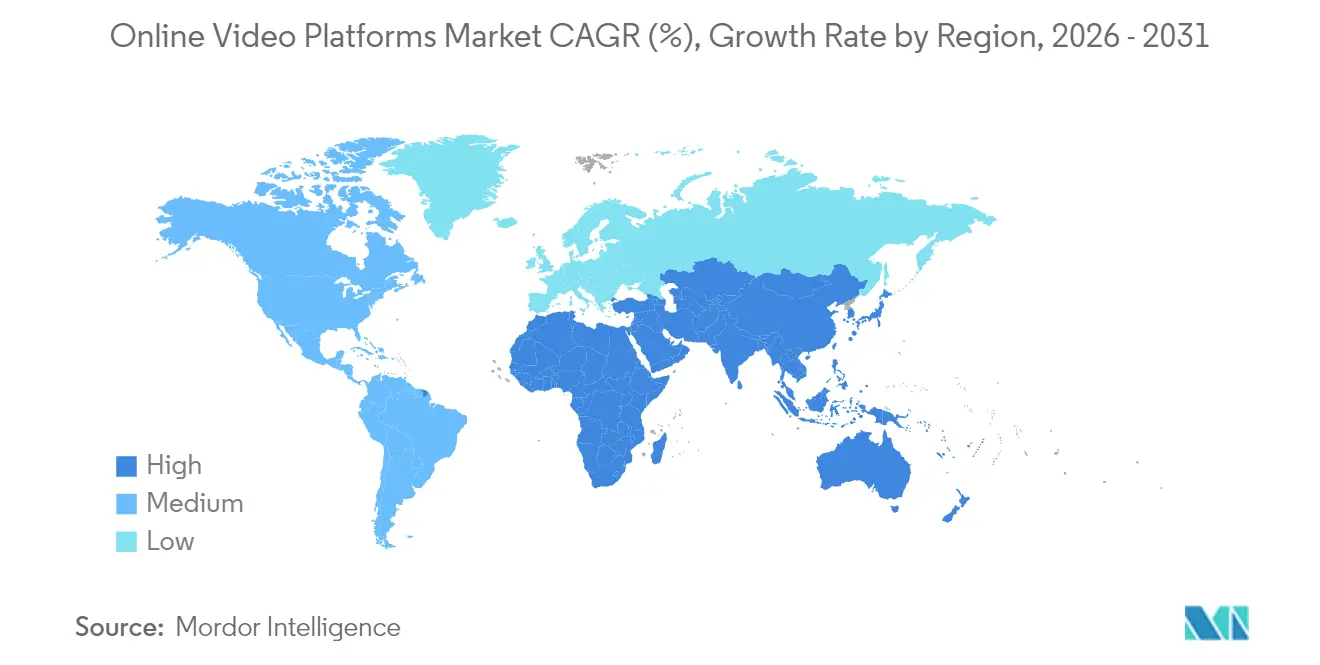

| Fastest Growing Market | Asia |

| Largest Market | North America |

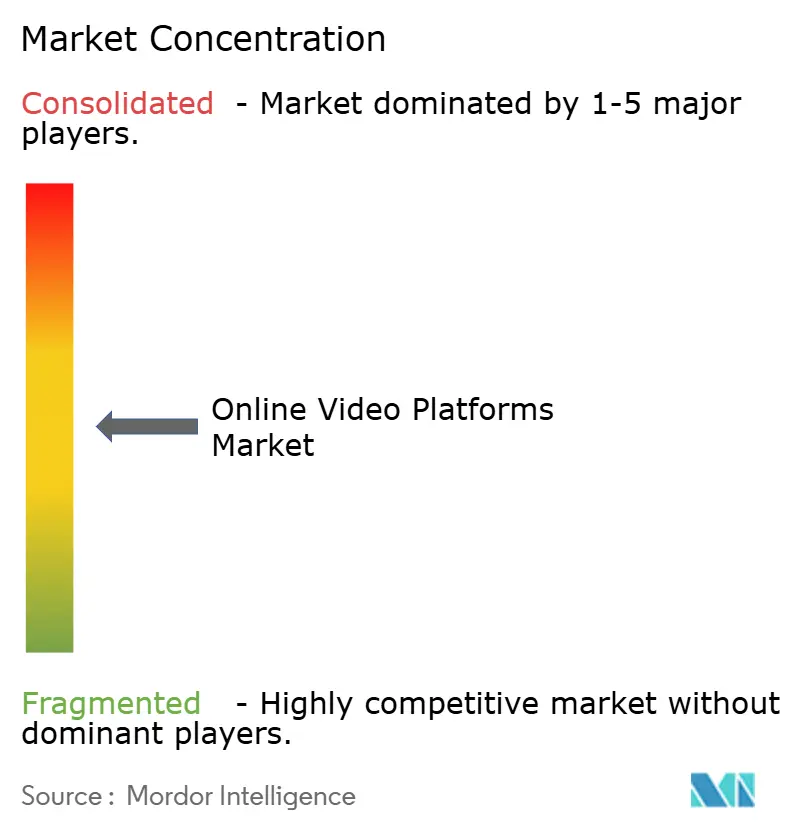

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Video Platforms Market Analysis by Mordor Intelligence

online video platforms market size in 2026 is estimated at USD 1.39 billion, growing from 2025 value of USD 1.23 billion with 2031 projections showing USD 2.57 billion, growing at 13.1% CAGR over 2026-2031. Growth reflects a decisive shift from legacy content delivery to AI-enabled ecosystems that weave together programmatic advertising, data analytics, and multi-revenue streams. Commercial 5G roll-outs are lowering latency thresholds, allowing live and interactive formats to flourish. Enterprises are embedding video across functions—training, communications, and marketing—accelerating demand for feature-rich, security-compliant platforms. Meanwhile, regulatory pressure for local content is prompting sizable investment in regional production hubs, thereby creating differentiated supply in underserved languages. Rising adoption of cloud-native services anchors scalability, but a pivot toward hybrid deployments signals mounting concern over compliance, cost, and data sovereignty.

Key Report Takeaways

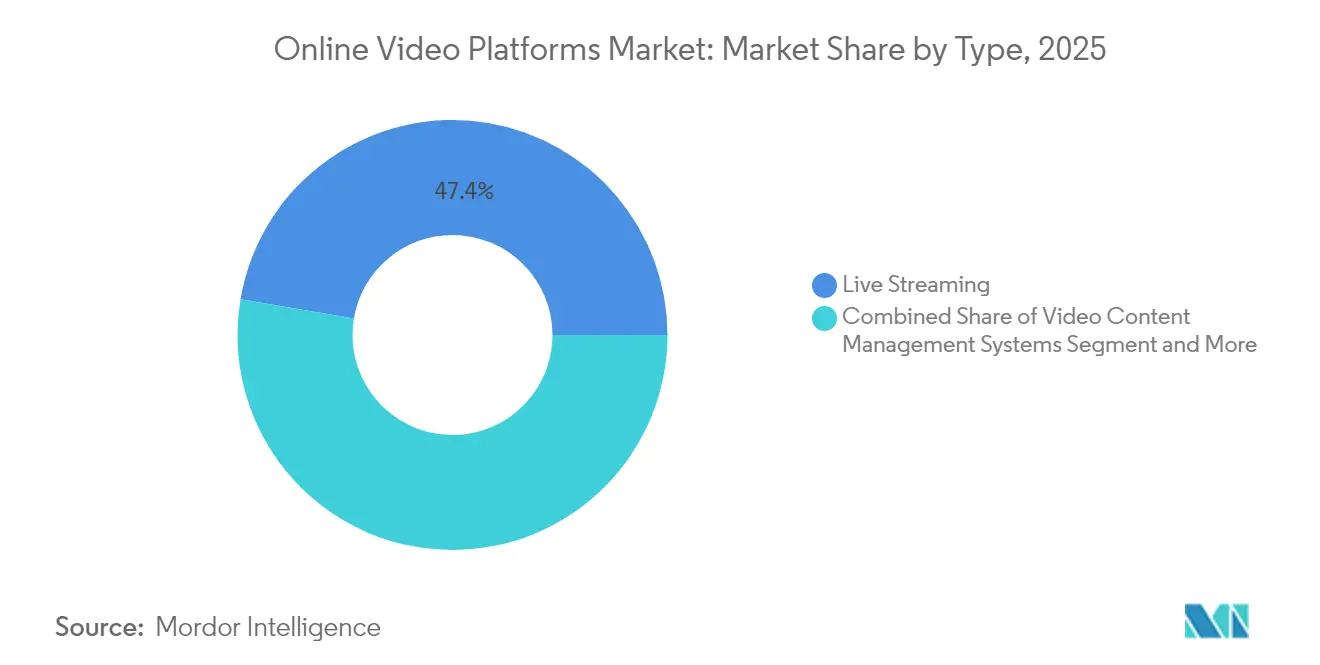

- By type, Live Streaming led with 47.35% of the online video platforms market share in 2025, while Video Analytics is set to expand at an 17.8% CAGR through 2031.

- By component, Solutions held 69.20% revenue share in 2025, whereas Services are projected to post a 14.5% CAGR to 2031.

- By streaming type, Video on Demand accounted for 59.10% share of the online video platforms market size in 2025; Live Streaming is growing faster at 13.8% CAGR to 2031.

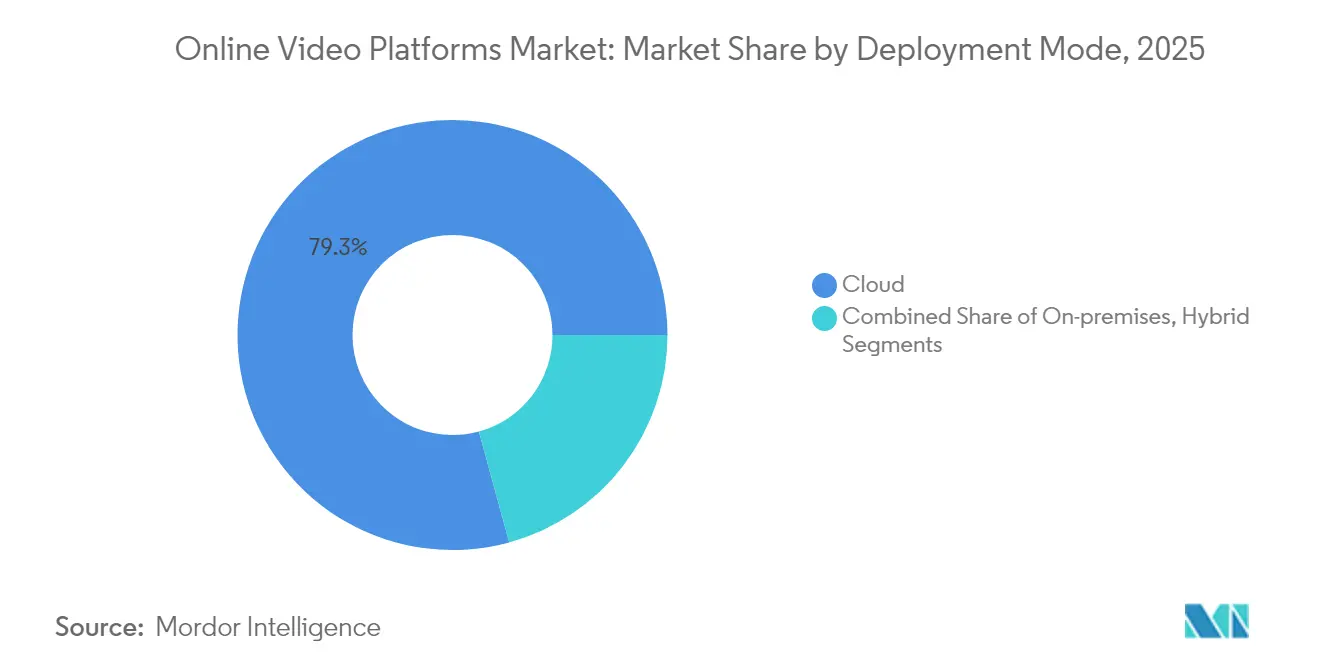

- By deployment mode, cloud models captured 79.25% share in 2025, but hybrid deployment is advancing at an 17.8% CAGR through 2031.

- By end user, Media and Entertainment commanded 39.45% share in 2025, while E-learning and Education is forecast to grow at 16.6% CAGR.

- By geography, North America contributed 34.72% revenue in 2025; Asia-Pacific is the fastest-growing region at a 14.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Video Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Programmatic advertising adoption | +1.9% | North America, Western Europe | Medium term (2-4 years) |

| Short-form mobile video surge | +1.7% | Asia-Pacific, Global | Short term (≤2 years) |

| 5G-enabled ultra-low-latency streaming | +1.4% | Global; early uptake in North America, China, Korea | Medium term (2-4 years) |

| Corporate video for training and communications | +1.2% | Europe, North America | Medium term (2-4 years) |

| AI-powered video analytics | +1.6% | Developed markets worldwide | Medium term (2-4 years) |

| Local content quotas in emerging markets | +1.6% | Middle East, Europe, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Programmatic Advertising Revolutionizes Video Monetization

Programmatic buying now underpins nearly 60% of TV and video ad spend in 2025, streamlining transactions between advertisers and publishers. [1]Interactive Advertising Bureau, “Digital Video Is Set to Capture Nearly 60% of All TV/Video Ad Spend in 2025,” streamingmedia.com Automated auctions integrate first-party data, boosting targeting accuracy across connected-TV and mobile inventory. Self-serve tools widen access, enabling small businesses to compete alongside global brands. As a result, content owners unlock incremental revenue without expanding sales teams. The New York Times recorded a 30% uplift after adopting programmatic video in 2024, confirming the model’s scalability

Mobile-First Video Consumption Reshapes Content Strategies

More than 70% of viewers watch streaming content on smartphones; in many emerging markets the ratio exceeds 80% . [2]Project Aeon, “8 Innovative Video Ads for Publishers: Monetization in 2025,” project-aeon.comPublishers are optimizing vertical formats and sub-60-second clips to suit scroll-based behavior. Implementation of mobile-centric ad units—including rewarded and interactive overlays—improves completion rates, driving CPM premiums for short-form inventory. Monetization success stories, such as BuzzFeed’s 40% revenue spike following a vertical-video push in 2024, encourage broader adoption. [3]Firework, “Short-Form Video Statistics 2024,” firework.comThe trend also lowers production costs, supporting higher content cadence and granular audience segmentation.

5G Infrastructure Enables Next-Generation Experiences

Commercial 5G networks deliver sub-10-millisecond latency and 100-fold capacity gains, permitting 8K live feeds, multi-angle sports streams, and immersive AR/VR session. Early field tests—such as BT Sport’s 8K broadcasts—proved that near-real-time interactivity boosts viewer retention. Edge computing alliances between cloud providers and telcos further reduce transport costs, making advanced formats viable in cost-sensitive geographies. These capabilities directly raise the ceiling for premium subscriptions and advertising rates.

Corporate Adoption Accelerates Digital Transformation

Enterprises are standardizing video for onboarding, compliance, and executive messaging, moving beyond sporadic webcast usage. The enterprise video segment is projected to climb from USD 23.8 billion in 2024 to USD 35.8 billion by 2029, powered by AI avatars and automated translation that cut production timelines. Corporate buyers now demand secure, LMS-integrated platforms with analytics that link content to employee performance, reinforcing platform stickiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CDN costs in emerging markets | −1.1% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Widespread ad-blocking | −1.2% | Developed markets globally | Short term (≤2 years) |

| Fragmented DRM standards | −0.9% | Global | Medium term (2-4 years) |

| Expanding data-privacy compliance burden | −0.8% | Europe, North America; global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Content Delivery Costs Challenge Emerging-Market Expansion

Limited backbone capacity inflates CDN fees, compressing margins for ad-supported services in Asia and Latin America. While 5G and edge nodes promise relief, current cost structures complicate freemium strategies where ARPU lags developed regions. Vendors experiment with peer-assisted delivery and Media over QUIC to tame bandwidth bills

Ad-Blocking Technologies Threaten Revenue Models

Roughly 40% of desktop users and 18% of mobile users block ads, translating into billions in foregone impressions. SSAI solutions stitch ads into the stream, reducing client-side detection and improving playback quality. Platforms are also diversifying toward subscriptions and in-stream commerce to buffer against lost ad inventory. Rewarded video formats post completion rates near 80%, illustrating alternative value exchange paths for viewers

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Video Analytics Drives Enterprise Adoption

Live Streaming captured 47.35% share of the online video platforms market in 2025, underscoring its ubiquity across entertainment, sports, and corporate events. Adoption widened as 5G decreased latency and boosted reliability, allowing platforms to position live video as a premium engagement lever. The segment continues to attract brands seeking real-time interaction with audiences. Video Analytics, although smaller in revenue, is advancing at an 17.8% CAGR, reflecting higher enterprise spending on data-driven optimization. The availability of cloud APIs that automate object detection, sentiment analysis, and content moderation is transforming video into a decision-support asset. As enterprises quantify ROI through engagement metrics and conversion lift, analytics budgets rise accordingly, further diversifying revenue inside the online video platforms market.

The remaining categories—User-Generated Content, DIY platforms, and SaaS-based professional suites—serve varied user personas yet benefit from the same underlying infrastructure. Consumer-facing UGC apps emphasize social virality and creator tools, whereas professional suites integrate workflows like asset management and multi-CDN routing. Collectively, these niches reinforce platform choice and keep competitive intensity high.

By Component: Services Segment Accelerates Through Managed Offerings

Solutions commanded 69.20% revenue in 2025, led by video delivery and distribution toolkits essential for high-quality streaming. Security modules such as multi-DRM vaults and watermarking complement delivery pipelines, especially for studios and sports leagues. Analytics add-ons unlock incremental subscription or licensing revenue, incentivizing vendors to bundle features. The online video platforms market size for services, however, is scaling quickly as organizations shift from capital expenditure to operating expenditure models. Managed Services show 14.5% CAGR because enterprises prefer outsourcing encoding, localization, and 24/7 monitoring to specialists with economies of scale.

Professional Services remain indispensable when integrating video stacks into complex IT environments. Custom player development, API orchestration, and compliance audits ensure that platform rollouts meet both technical and regulatory requirements. This consultative layer differentiates full-service vendors from pure-play software providers.

By Streaming Type: Live Streaming Narrows the Gap

Video on Demand still holds 59.10% share of the online video platforms market size in 2025 owing to its convenience and evergreen content libraries. Yet Live Streaming’s 13.8% CAGR until 2031 signals converging demand curves. Sports, esports, and shoppable video events rely on immediacy to command premium CPMs and membership fees. Enhanced chat overlays, polls, and synchronized watch parties deepen time-spent metrics, driving monetization beyond simple pre-roll ads.

As algorithms mature, platforms surface live streams to users with contextual cues, smoothing discovery friction that once restrained growth. These advances shorten the viewership divide between VoD and live formats. Advertisers capitalize by booking dynamic mid-roll placements linked to real-time data, validating live’s revenue potential.

By Deployment Mode: Hybrid Models Bridge Security and Scalability

Cloud architectures delivered 79.25% of workflows in 2025, aligning with industry preferences for elastic capacity and global reach. Nevertheless, industries with stringent security or predictable traffic models increasingly blend private infrastructure with cloud burst capacity. Hybrid deployments, expanding at 17.8% CAGR, marry cost predictability with compliance mandates. For example, financial institutions retain encryption keys on-premises while serving public assets via multi-CDN meshes, minimizing latency without exposing sensitive data.

On-premises installations remain relevant where data sovereignty laws or existing server investments dictate localized control. Selecting deployment architecture therefore hinges on risk tolerance, workload spikiness, and regulatory context rather than a uniform best practice.

By End User: Education Sector Embraces Video-First Learning

Media and Entertainment preserved 39.45% revenue share in 2025, leveraging large content catalogs, marquee IP, and established fan bases. Monetization spans subscriptions, advertising, and transactional pay-per-view, giving established networks the scale to negotiate favorable bandwidth and rights agreements. The education segment, expanding at 16.6% CAGR, embraces video to deliver micro-lessons, instructor-led MOOCs, and immersive virtual labs. Institutions integrate captioning, quizzes, and analytics into learning-management systems, fulfilling accessibility mandates and measuring learning outcomes.

Adjacent verticals such as BFSI and healthcare deploy secure video channels for customer onboarding and telemedicine, respectively. Retailers incorporate live shoppable streams to entice buyers, while government agencies disseminate citizen messaging and emergency broadcasts. The breadth of use cases cements video as an indispensable communication layer across the online video platforms market.

Geography Analysis

North America generated 34.72% of global revenue in 2025, fueled by mature broadband, high ARPU, and deep penetration of connected-TV devices. Media buyers in the region allocate nearly 60% of combined TV and video budgets to digital video in 2025, a trend that amplifies platform revenue streams. The robust ecosystem of cloud providers, software vendors, and content creators fosters rapid experimentation with AI-driven personalization and interactive formats.

Asia-Pacific is advancing fastest at a 14.8% CAGR and is projected to add USD 16.2 billion in revenue between 2024 and 2029. The surge stems from smartphone ubiquity, lower data tariffs, and escalating demand for local-language content. India alone is forecast to deliver over one quarter of incremental premium video revenue, helped by regional language originals and sports rights. Chinese platforms leverage super-app ecosystems to cross-sell subscriptions and micro-transactions, reinforcing user stickiness. In Southeast Asia, bundled mobile-data plans stimulate first-time streaming adoption among price-sensitive consumers.

Europe retains solid position owing to enterprise adoption and regulatory impetus. The EU’s Audiovisual Media Service Directive obliges global platforms to invest in European storytelling, channeling funds into regional studios and jobs. Meanwhile, Latin America sees accelerating growth as fiber deployments reach secondary cities, lifting streaming quality and ad inventory. The Middle East and Africa remain nascent but promising; expanding 4G and 5G coverage, plus rising youth populations, underpin demand for culturally relevant content.

Competitive Landscape

The online video platforms market features moderate fragmentation. Consumer reach is concentrated among a handful of global networks, yet the enterprise tier hosts dozens of specialized vendors. Alphabet’s YouTube and Vimeo maintain scale advantages in traffic, creator ecosystems, and ad-delivery infrastructure. Vimeo recently introduced AI-based text-to-video translation, positioning the service as a global corporate communication hub.

Brightcove and Kaltura lead in modular, API-first architectures tailored to media, sports, and education clients. Consolidation is accelerating: JW Player merged with Connatix, broadening its monetization stack, while Banzai acquired Vidello to bolster virtual-event capabilities. Niche disruptors such as Descript lower editing barriers through text-based workflows, expanding the addressable creator base.

Strategic differentiation now hinges on AI. Vendors embed auto-chaptering, personalized previews, and predictive bitrate selection to lift engagement and reduce churn. Integration depth with CRM, CMS, and e-commerce platforms also influences buying decisions, enabling video to fit seamlessly into broader digital-experience stacks. Vertical-specific compliant solutions—for instance, HIPAA-ready modules for healthcare—offer defendable positions against horizontal giants.

Online Video Platforms Industry Leaders

YouTube LLC

Brightcove Inc.

Panopto Inc.

Catenoid Inc.

Vimeo.com, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: uebec introduced legislation mandating higher French-language content quotas on streaming platforms, signaling expanding global quota regimes

- April 2025: Adobe unveiled Generative Extend and Media Intelligence in Premiere Pro, accelerating AI-assisted editing workflows

- March 2025: Adobe debuted the AI Platform at Summit 2025 to orchestrate personalized customer experiences across channels

- January 2025: Media Partners Asia projected USD 16.2 billion revenue growth for Asia-Pacific streaming between 2024 and 2029

Global Online Video Platforms Market Report Scope

The online video platform is a video hosting service that helps users to upload, view, store, and stream video content over the internet. Videos generally get uploaded via. hosting services sites or any mobile or desktop applications.

The Online Video Platforms Market is segmented by type (live streaming, video content management systems, video analytics), by end-user (e-learning, media & entertainment, BFSI, retail, IT & communication), by geography (North America, Europe, Asia Pacific, Latin America and Middle East & Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Live Streaming |

| Video Content Management Systems |

| Video Analytics |

| User-Generated Content Platforms (UGC) |

| Self-service/DIY Platforms |

| SaaS-based Professional Platforms |

| Solutions | Transcoding and Processing |

| Video Delivery and Distribution | |

| Video Analytics and Engagement | |

| Video Security and DRM | |

| Video Content Management | |

| Services | Professional Services |

| Managed Services |

| Live |

| Video on Demand (VoD) |

| Cloud |

| On-premises |

| Hybrid |

| Media and Entertainment |

| E-learning and Education |

| BFSI |

| Retail and eCommerce |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Type | Live Streaming | |

| Video Content Management Systems | ||

| Video Analytics | ||

| User-Generated Content Platforms (UGC) | ||

| Self-service/DIY Platforms | ||

| SaaS-based Professional Platforms | ||

| By Component | Solutions | Transcoding and Processing |

| Video Delivery and Distribution | ||

| Video Analytics and Engagement | ||

| Video Security and DRM | ||

| Video Content Management | ||

| Services | Professional Services | |

| Managed Services | ||

| By Streaming Type | Live | |

| Video on Demand (VoD) | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| Hybrid | ||

| By End User | Media and Entertainment | |

| E-learning and Education | ||

| BFSI | ||

| Retail and eCommerce | ||

| IT and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current Online Video Platforms Market size?

In 2026, the Online Video Platforms Market size is expected to reach USD 1.39 billion.

Who are the key players in Online Video Platforms Market?

Vimeo Inc. (Inter Active Corp.), YouTube LLC, Brightcove Inc., Panopto Inc. and Kaltura Inc. are the major companies operating in the Online Video Platforms Market.

Which is the fastest growing region in Online Video Platforms Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Online Video Platforms Market?

In 2025, the North America accounts for the largest market share in Online Video Platforms Market.

What years does this Online Video Platforms Market cover, and what was the market size in 2025?

In 2025, the Online Video Platforms Market size was estimated at USD 1.39 billion. The report covers the Online Video Platforms Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Online Video Platforms Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: