United States OTT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

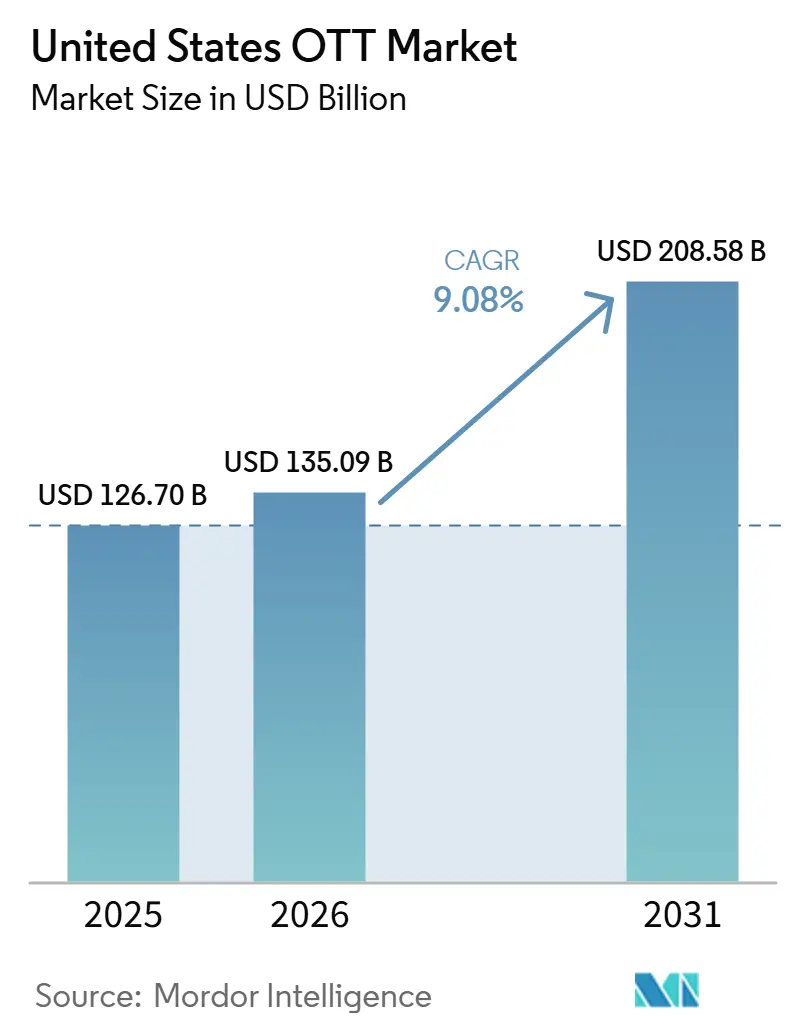

| Base Year Market Size (2025) | USD 126.70 Billion |

| Market Size (2026) | USD 135.09 Billion |

| Market Size (2031) | USD 208.58 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

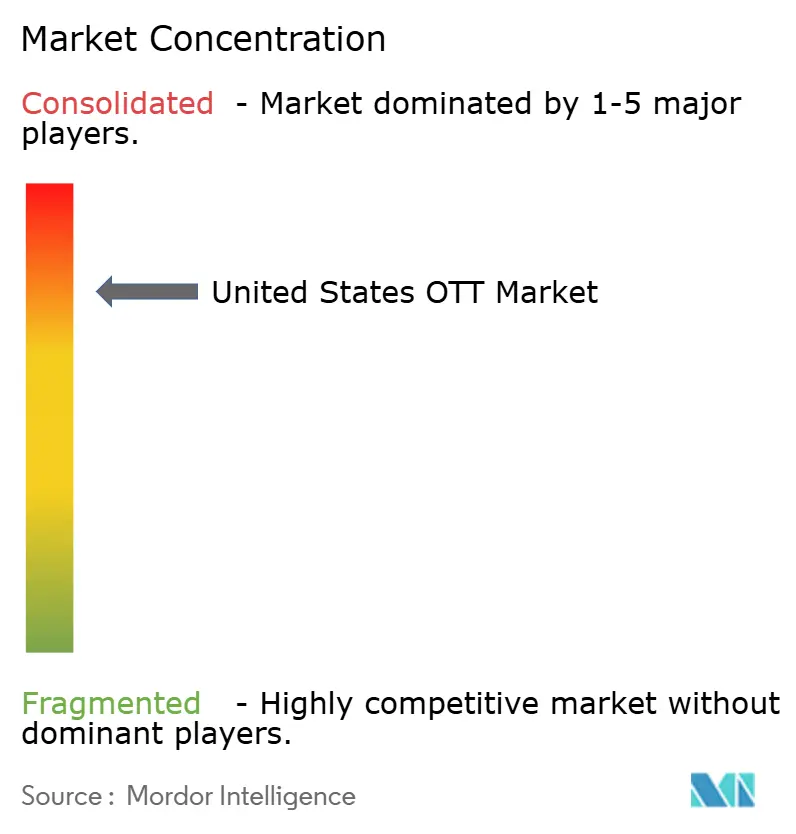

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States OTT Market Analysis by Mordor Intelligence

The United States OTT market size reached USD 135.09 billion in 2026 and is projected to climb to USD 208.58 billion by 2031, advancing at an 9.08% CAGR. Accelerating cord-cutting, ubiquitous fiber and 5G rollouts, and the rapid mainstreaming of ad-supported tiers that now rival pure subscriptions are reshaping video consumption. Smart-television penetration tops 88% in US households, shifting viewing back to the living room, where advertisers prize co-viewing and larger screens. Exclusive sports rights are fragmenting across digital platforms, drawing younger fans away from legacy pay-TV bundles. Meanwhile, consolidation led by Netflix’s USD 72 billion bid for Warner Bros. Discovery signals that scale in both production and distribution is now a defensive requirement against surging content costs. Regulatory scrutiny of that megadeal, sustainability concerns over data-center emissions, and subscriber frustration with search times longer than 12 minutes are the headline risks tempering otherwise strong growth.

Key Report Takeaways

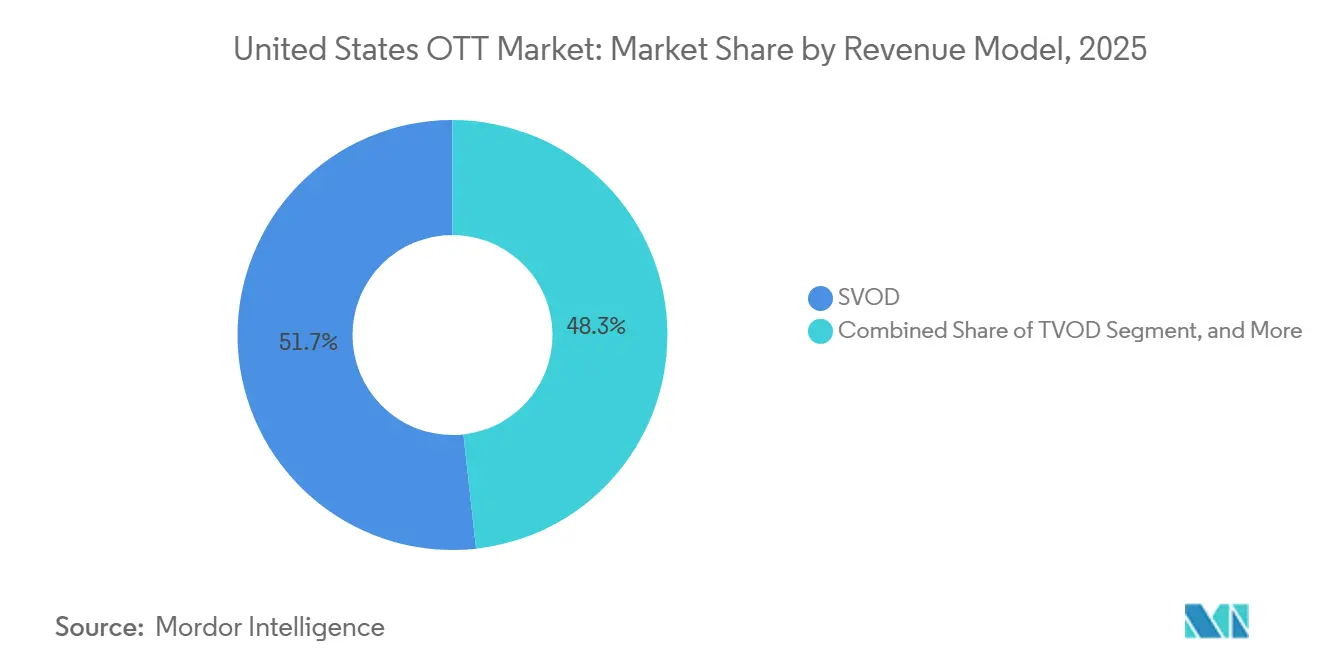

- By revenue model, SVOD held 51.75% of the United States OTT market share in 2025, while AVOD is projected to expand at a 9.71% CAGR through 2031.

- By device type, smartphones and tablets accounted for 53.62% of device-type revenue in the United States over-the-top (OTT) market in 2025, while smart TVs are projected to expand at a 9.86% CAGR through 2031.

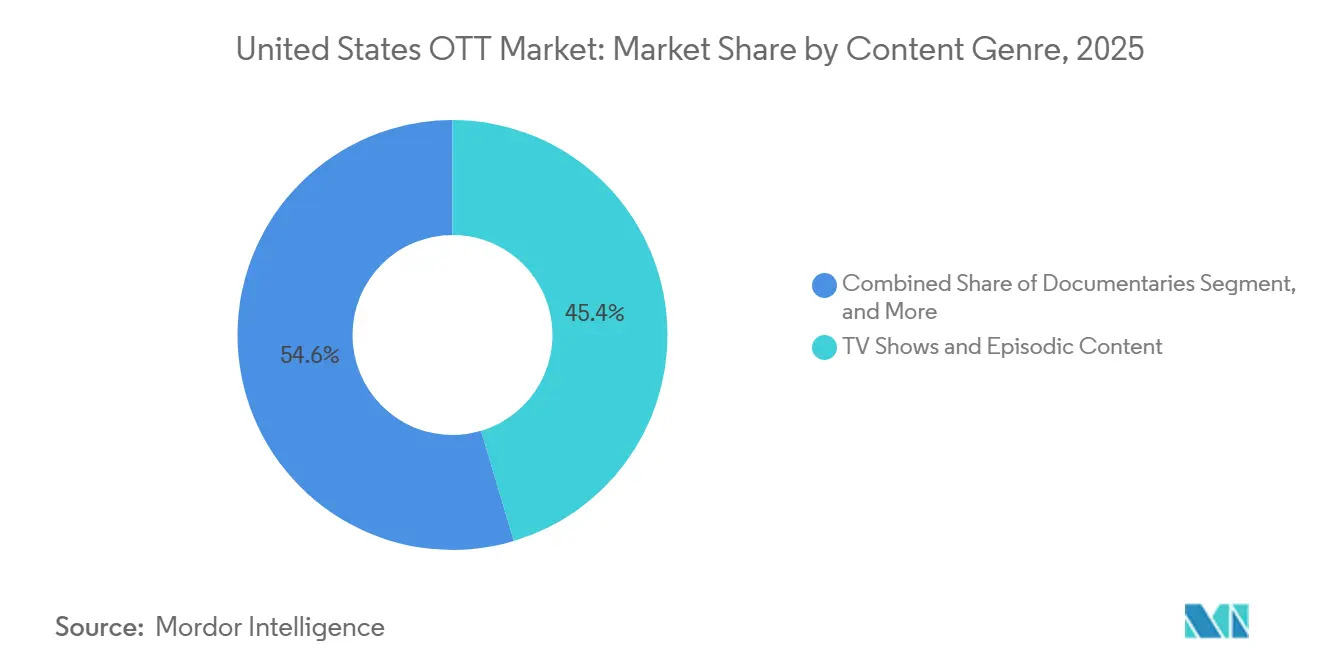

- By content genre, TV shows and episodic content accounted for 45.39% of revenue in 2025, while documentaries are projected to expand at a 9.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States OTT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cord-Cutting and Direct-to-Consumer Adoption | +2.4% | National, with highest intensity in West Coast and Northeast metro corridors | Short term (≤ 2 years) |

| Fiber and 5G Expansion for Higher-Quality Streaming | +1.9% | National, with early gains in Sun Belt metro areas and rural fixed wireless access markets | Medium term (2-4 years) |

| Ad-Supported and Hybrid Models Expanding Audience Reach | +1.7% | National | Short term (≤ 2 years) |

| Niche SVOD Services for Multicultural and Faith-Based Audiences | +1.1% | National, concentrated in Sun Belt states with high Hispanic and faith community populations | Medium term (2-4 years) |

| State Tax Incentives for Original Content Production | +0.7% | State-level, with early gains in California, New Jersey, Hawaii, and Pennsylvania | Medium term (2-4 years) |

| AI-Powered Personalization Improving Watch Time and Retention | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cord-Cutting Rates Among US Households Accelerate Direct-to-Consumer Adoption

Cord-cutting became a defining force for the United States OTT market in 2025, when non-pay-TV households outnumbered pay-TV households. The Video Advertising Bureau reported that 77.2 million US households had cut the cord in 2025, and it expects the total to reach 80.7 million by the end of 2026.[1]Video Advertising Bureau, “2026 Streaming Report,” Video Advertising Bureau, thevab.com Streaming accounted for 47.5% of total US television viewing in December 2025, compared with 20.2% for cable and 21.4% for broadcast. Each household that leaves traditional pay television becomes a direct customer of one or more OTT services. The change gives platforms more control over billing, plan selection, and advertising exposure. It also makes retention more important, as consumers can switch providers with little effort.

Rapid Expansion of Fiber and 5G Networks Enables Higher-Quality Streaming

Broadband quality supports the United States OTT market by improving the reliability of high-resolution video delivery. Faster fixed and wireless connections reduce buffering and can improve completion rates for 4K programming. Better viewing experiences can reduce cancellations caused by poor service quality and increase advertising inventory on connected television services. Fiber and fixed wireless access can extend premium streaming to exurban and rural areas where legacy cable networks may not support consistent high-bandwidth viewing. The Federal Communications Commission has continued to direct broadband support toward rural coverage and infrastructure expansion. These investments can enlarge the addressable household base over the forecast period if platforms offer services and content that meet the needs of newly connected households.

Shift Toward Ad-Supported and Hybrid Models Expands Audience Reach

Ad-supported viewing is becoming a core part of the United States OTT market rather than a secondary option for lower-priced plans. The Video Advertising Bureau projects 209.4 million AVOD viewers in the United States in 2026, equal to 62% of the population. Hybrid models allow a single service to serve subscribers who prefer an ad-free option and viewers who prefer a lower monthly price. Streaming upfront commitments increased to USD 13.2 billion for the 2025-2026 cycle, while broadcasters faced lower commitments. Netflix launched its in-house advertising technology platform in January 2026, giving the company more direct control over audience targeting and campaign delivery. Advertising expansion creates a growth path but may widen the operational advantage of leading platforms, which have stronger measurement, inventory management, and sales capabilities.

Niche SVOD Services Targeting Multicultural and Faith-Based Audiences Unlock New Subscriber Pools

Niche services give the United States OTT market a way to reach audiences whose interests may not be reflected in broad entertainment catalogs. Faith-based and multicultural programming can build a clearer connection with viewers than a general-purpose service. Focused services can use defined catalogs and familiar titles to enter a specific audience segment. They can also use lower-cost programming formats to manage content spending. Larger platform marketplaces make specialized subscriptions easier to find and purchase. Texas and Florida offer a large, meaningful audience for Spanish-language and culturally specific programming due to their large Hispanic populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Content Licensing Costs and Competition for Premium IP | -0.9% | Global | Medium term (2-4 years) |

| Market Saturation and Churn From Low Switching Costs | -0.7% | National | Short term (≤ 2 years) with sustained impact |

| Declining Discoverability From App Overload | -0.4% | National | Medium term (2-4 years) |

| Carbon Footprint Scrutiny of Streaming Workloads | -0.2% | National, with spillover to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Content Licensing Costs and Competition for Premium IP Squeeze Margins

Content licensing costs remain a significant restraint on the United States OTT market. Netflix and Sony Pictures Entertainment finalized a global Pay-1 licensing agreement valued above USD 7 billion in January 2026, while Disney increased its fiscal 2026 content budget by USD 1 billion to USD 24 billion, with NBA rights identified as a major driver. These commitments show the continuing importance of premium franchises, theatrical rights, and live sports to leading platforms. New AVC, or H.264, streaming fee structures can also add fixed annual expenses for large platforms. Smaller services may lack the scale needed to spread content and technology costs across a large subscriber base. Platforms are responding through pricing, advertising income, disciplined content spending, licensing partnerships, and acquisitions.

Market Saturation and Subscriber Churn Fueled by Low Switching Costs

Market saturation changes the challenge for the United States over-the-top (OTT) market from acquiring subscribers to keeping them. US households maintained an average of 5.8 streaming subscriptions in 2025, while premium SVOD subscriber growth slowed to 7%, and weighted-average monthly churn was 4.6%. These figures show that households are adjusting their service portfolios rather than adding subscriptions without limit. The draft identifies 29.5 million Americans as serial churners who canceled 3 or more services over 2 years, representing 23% of subscribers and 42% of cancellations. Release timing, bundles, advertising-supported plans, and better discovery can reduce churn but cannot remove it. Platforms must balance higher prices with perceived value because households can move to another service without a long contract or equipment change.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Model: SVOD Remains the Main Revenue Base While Advertising Tiers Expand

SVOD held 51.75% of the United States OTT market share in 2025, making it the largest revenue model. Recurring monthly subscriptions remain central to platform economics because they provide a predictable revenue base. Serialized programming and broad content libraries support reuse across major releases. Disney's USD 29.99 monthly bundle for Disney+, Hulu, and ESPN+ illustrates how combined services can increase value for households. The bundle reportedly added 11 million domestic subscribers since January 2026. TVOD serves viewers who prefer to pay for individual titles or live events rather than maintain a recurring service. Its role is more limited as subscription services move recent releases into their catalogs faster.

Hybrid subscription and advertising plans are changing the way leading platforms serve households across different budgets. The draft states that 80.4% of sub-OTT viewers are expected to have at least 1 advertising-supported subscription in 2026, compared with 71.5% in 2024. AVOD is the fastest-growing revenue model, with the United States OTT market size for AVOD projected to expand at a 9.71% CAGR through 2031. The Video Advertising Bureau projects that there will be 209.4 million AVOD viewers in the United States in 2026.[2]Video Advertising Bureau, “2026 Streaming Report,” Video Advertising Bureau, thevab.com FAST viewership is also projected to exceed 125 million viewers in 2026. Greater scale can attract advertisers, fund content acquisitions, and improve the appeal of free or low-cost services. Netflix's in-house advertising platform shows that the largest subscription services now treat advertising infrastructure as a strategic capability.

By Device Type: Mobile Devices Lead Revenue While Smart TV Viewing Gains Momentum

Smartphones and tablets accounted for 53.62% of device-type revenue in 2025. Their leading position reflects mobile and second-screen viewing habits, particularly among consumers aged 18-34. Mobile devices allow users to watch content while traveling, commuting, or using another screen at home. These sessions can be shorter than connected television sessions, which can limit advertising value per viewing hour. Laptops and desktops continue to support news, documentaries, and work-adjacent viewing. Their relative contribution is declining as more leisure viewing moves to television screens. Game consoles, set-top boxes, and media streamers remain relevant in households that have not upgraded to smart television hardware.

Smart TVs are the fastest-growing device type, with the United States OTT market size for the category projected to advance at a 9.86% CAGR through 2031. Smart TV adoption reached 82% of US television households in 2026, according to data cited in the draft. Built-in applications have become the default television interface for 30% of viewers, compared with 10% in 2020. Roku accounted for 28% of US connected television platform usage, while Samsung Tizen accounted for 23%. Larger living-room screens can support longer sessions and more valuable advertising inventory. This creates a commercial reason for platforms to optimize applications, advertising formats, and discovery tools for connected television environments.

By Content Genre: Episodic Programming Leads While Documentaries Gain Pace

TV shows and episodic content accounted for 45.39% of content genre revenue in 2025. Serialized drama, reality programs, and procedurals help services sustain recurring engagement over several weeks. Weekly releases can create a reason for subscribers to remain active between major catalog additions. This type of programming can also produce social discussion that improves audience awareness without relying only on paid promotion. Movies and films remain important to OTT catalogs, but their relative role is affected by shorter theatrical windows and stronger investment in series. The draft notes that major studios have reduced some theatrical-to-streaming windows from 90 days to 45 days, which refreshes catalogs but can reduce the sense of exclusivity.

Documentaries are the fastest-growing content genre, with the United States over-the-top (OTT) market size projected to grow at a 9.75% CAGR through 2031. The genre can offer a more favorable relationship between content spending and audience engagement than large scripted productions. True-crime, investigative, cultural, and sports documentaries can serve different age groups and viewing interests. Streaming services account for a large share of new documentary releases and can use catalog titles to sustain ongoing engagement. Netflix added more than 50 podcasts through partnerships with Spotify, iHeartMedia, and Barstool Sports as of January 2026. The expansion shows that services are broadening content formats beyond television series and films. Documentary releases can also support music, gaming, and merchandise activity when a title draws attention to a related artist or franchise.

Geography Analysis

The United States OTT market is national in scope, but regional patterns in broadband access, income, production activity, and content preferences affect how services compete. The West Coast and Northeast remain important areas for premium SVOD consumption because of their high broadband penetration and income density. California has a central role because it hosts production operations for major OTT platforms and a large share of the US production ecosystem. California's expanded tax credit program supported 170 projects in fiscal year 2025-2026 and was projected to generate USD 6.6 billion in economic activity.[3]Office of Governor of California, “First Year of California’s Expanded Film and TV Tax Credit Projected to Bring USD 6.6 Billion in Economic Impact,” Office of Governor of California, gov.ca.gov Demand in these established coastal areas is supported by strong household willingness to pay for premium, ad-free services.

Sun Belt states, especially Texas, Florida, and Georgia, offer a different opportunity for the United States over-the-top (OTT) market. These states have growing populations and substantial Hispanic communities that may respond to stronger Spanish-language and multicultural catalogs. Dallas-Fort Worth and Houston showed subscription penetration gaps relative to coastal markets in 2025, according to the draft. This gives AVOD, SVOD, and specialized channels a possible route to add households without relying on the same content mix used in established coastal markets. Texas and Florida contain the 2 largest concentrations of Hispanic households in the country. Services that tailor programming and pricing to these audiences can improve relevance while managing content costs. New Jersey also became a more significant production location in 2026 as its incentive structure attracted production investment away from higher-cost locations.

The Midwest and the Mountain West have different viewing and distribution profiles. Hulu leads in 20 states, primarily in the Midwest and South, reflecting the continued relevance of live television and sports programming. Montana and Maine recorded high binge-viewing engagement in a March 2026 study described in the draft. Montana adults averaged 3.52 hours of daily viewing across all demographic groups. Higher engagement can make smaller markets more attractive for advertising-supported services, even when the total population is lower. Rural broadband funding and wider fiber deployment can improve access to premium streaming in exurban counties. These infrastructure improvements can expand the addressable audience by enabling consistent high-quality viewing in places where bandwidth had previously constrained adoption.

Regulatory Landscape

In the United States, OTT and online video distribution services generally operate without a dedicated federal licensing regime for carriage or content, with oversight applied through adjacent frameworks such as copyright, consumer protection, and advertising rules. The Federal Communications Commission (FCC) also administers obligations that can touch OTT distribution, including closed-captioning requirements for Internet video programming when the same content previously aired on US television with captions.

In 2026, the FCC increased policy attention on streaming-adjacent topics through inquiries that, among other items, examined consistency of TV parental guidelines and ratings across platforms. The agency’s move to build a formal record reflects regulatory uncertainty in areas where it has limited direct statutory authority over streaming content. Separately, the FCC released a 2026 strategic plan that references leveling the playing field between traditional and non-traditional media ecosystems, keeping regulatory uncertainty elevated for large platforms as consumer-protection and content-classification debates move into public proceedings.

Value Chain Analysis

The US OTT value chain begins with IP sourcing (original commissions, studio output deals, and third-party licensing) and runs through production, post-production and localization, content packaging, and marketing, followed by platform operations such as apps, identity, billing, and recommendations. Monetization then occurs through subscriptions, transactional purchases, and advertising. Distribution depends on broadband and mobile networks (fiber and 5G), app stores and device operating systems (smart TVs, streamers, game consoles), and ad-tech layers for CTV, including dynamic ad insertion and programmatic sales.

Key bottlenecks concentrate at integration and experience layers. Non-standardized APIs, complex authentication, and fragmented measurement can extend operator and bundle integration timelines, while discoverability issues have pushed personalization and UI placement to the center of conversion and retention. Scale and control over upstream assets are also becoming more important, reflected in high content spending (for example, Netflix earmarking USD 17 billion for content in 2025) and consolidation activity aimed at reducing reliance on third-party licensing and improving distribution leverage across devices and ad supply.

Competitive Landscape

The United States OTT market is concentrated among a small number of leading platforms, but competition remains active among smaller services. Netflix, Amazon Prime Video, Disney+, and Apple TV+ accounted for 65% of US streaming engagement in Q2 2026, based on more than 45 million streaming interactions in the draft. Netflix held 20% of engagement, the highest among individual platforms. Netflix also reported USD 12.25 billion in revenue in Q1 2026 and more than 325 million global subscribers. Its broad catalog, global scale, and advertising investment give it a strong position in the United States OTT market. Apple TV+ recorded the fastest annual engagement growth among major platforms in the year to Q2 2026, adding 5 percentage points and overtaking Hulu for fourth place.

Several strategic moves show how companies are responding to changing market conditions. Netflix and AMC Global Media announced a multiyear co-exclusive agreement for all 7 series in The Walking Dead Universe, giving Netflix expanded international rights beginning in 2027.[4] Video Advertising Bureau, “2026 Streaming Report,” Video Advertising Bureau, thevab.com Netflix also launched its own advertising technology platform in January 2026, reducing its reliance on an external technology partner. Paramount Skydance and Warner Bros. Discovery signed a definitive merger agreement valued at USD 110 billion in February 2026. Warner Bros. Discovery stockholders approved the transaction in April 2026, while the US Department of Justice closed its investigation without requiring divestitures or behavioral remedies. These actions reflect the value placed on large catalogs, advertising capacity, and greater scale.

Bundling is another major response to household subscription limits. Comcast expanded its StreamSaver bundle in April 2026 to include Disney+, Hulu, HBO Max, Peacock, Netflix, and Apple TV+. The approach recreates some of the benefits of a television package while keeping streaming services as separate brands. Platforms are also using proprietary intellectual property and recommendation systems to improve retention. Live sports, multicultural programming, and technology services for broadcasters remain areas where participants can differentiate their offers.

United States OTT Industry Leaders

Netflix Inc.

The Walt Disney Company

Amazon.com, Inc

Warner Bros. Discovery, Inc

Hulu, LLC (The Walt Disney Company)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ad-supported and hybrid monetization continues to be the clearest whitespace, as FAST and AVOD have broadened beyond early adopters and connected-TV ad inventory has become a core monetization lever for large-screen viewing. Platforms that combine first-party identity with unified ad decisioning across apps and devices can improve yield while aligning with consumer price sensitivity that is already shifting sign-ups toward ad tiers, including more than half of new Disney+ sign-ups in 2025 choosing the ad-supported tier.

Sports fragmentation and control of TV operating systems are also reshaping go-to-market strategies. Rights splits across multiple apps are increasing demand for aggregation, bundles, and cross-service discovery, while smart TVs (88%+ household penetration and 39.86% device share in 2025) concentrate viewing where placement, voice search, and home-screen merchandising affect audience capture. On the supply side, in-state production incentives and new studio capacity add channels to secure differentiated originals and reduce unit costs; Netflix reaching a major construction milestone in June 2026 at its Fort Monmouth, New Jersey studio campus underscores continued investment in owned production infrastructure that can support release cadence and library depth.

Recent Industry Developments

- July 2026: Netflix announced deals to bring curated short-form video from major digital publishers to the Netflix experience, with programming scheduled to start appearing from August 3, 2026. The company broadened content formats beyond long-form series and films, adding snackable viewing that can increase daily time spent and create additional ad-adjacent inventory in markets where Netflix operates an ad tier.

- May 2026: The Walt Disney Company introduced profile linking for eligible bundle subscribers so Hulu watch history, recommendations, and watchlists can sync into the Disney+ app. This unifies identity and personalization signals across services, supporting retention and cross-promotion as Disney moves toward a more integrated streaming interface.

- December 2025: Netflix agreed to acquire Warner Bros. Discovery in a USD 72 billion cash-and-stock transaction, with closing targeted within 18 months. If completed, the combination would expand owned content libraries and strengthen negotiating leverage across distribution and advertising, while also raising the level of US regulatory scrutiny around scale in streaming.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, we size the United States OTT market as revenues earned from streaming video and audio services delivered over the internet to end users, across subscription, transactional, and advertising-funded models, and consumed on connected devices.

Scope exclusions: Hardware sales (such as smart TVs, streaming sticks, and set-top boxes) and traditional pay TV channel distribution revenues are excluded.

Segmentation Overview

- By Revenue Model

- SVOD

- TVOD

- AVOD

- Hybrid Subscription and Ads

- By Device Type

- Smartphones and Tablets

- Smart TVs

- Laptops and Desktops

- Game Consoles

- Set-Top Boxes and Media Streamers

- By Content Genre

- Movies and Films

- TV Shows and Episodic Content

- Documentaries

- Other Content Genres

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, identify demand signals, and build the base data series that can be checked year over year. We referenced public sources such as FCC broadband deployment and subscription indicators, Bureau of Economic Analysis consumer spending series, U.S. Census datasets for households and income bands, and Bureau of Labor Statistics inflation trends to keep pricing logic realistic.

On the market and policy context side, we also used FTC publications, IAB materials for ad market direction, and research articles in peer reviewed media and telecom journals. On the supply side, we reviewed company filings, earnings transcripts, investor presentations, and reputable business press for service launches, price changes, ad tier adoption, and major content rights cycles. Where needed, we also used paid subscriptions for company financial intelligence, news and financials screening, and patent databases to cross-check platform feature shifts that can change monetization.

This list is illustrative, and many other sources were consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating which portion of streaming revenues should be counted as OTT, and how quickly pricing and ad loads are moving in the United States. We spoke with a mix of platform, ad sales, content distribution, and device ecosystem stakeholders, and then reconciled their input with observed price points, subscriber trends, and ad market direction. When inputs disagreed, we re-contacted selected experts so the final model reflects a practical middle ground rather than a single viewpoint.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 20% | |

| Mid tier: 51% | Functional/Unit leaders: 37% | |

| Smaller Players: 20% | Managers: 43% |

Market-Sizing & Forecasting

The core sizing logic starts from a top-down build where broadband-enabled households and user penetration trends are translated into a paying and ad-supported demand pool, which is then priced using observed subscription rates and advertising yield ranges. To keep it grounded, results are corroborated with selective bottom-up approximations, including sampled subscription price points times estimated subscriber counts, plus reasonableness checks on ad-funded revenues using ad load direction and CPM movement discussed in interviews.

A few inputs that materially move the model include the mix shift between SVOD, AVOD and FAST, average monthly price changes and churn sensitivity, the share of plans sold via bundles, ad tier adoption rates, and inflation adjusted pricing progression. For forecasting, we use scenario analysis with a base case anchored on expert consensus for price increases, ad tier expansion, and subscriber saturation, followed by sensitivity bands for ad demand softness or stronger bundling. When company disclosures are not fully comparable, gaps are handled through conservative ranges that are tightened only after multiple source confirmations.

Data Validation & Update Cycle

Outputs are checked against independent signals such as household broadband trends, publicly discussed subscriber movements, and the implied revenue per user, so that any outlier year is questioned before it is accepted. Variances are reviewed in steps, starting with input checks, then assumption reviews, and then a second analyst pass for calculation integrity.

Reports refresh annually, and interim updates are triggered when material events occur, such as major pricing resets, large bundle launches, or shifts in ad-supported strategy. Before delivery, we run a final update pass so the numbers reflect the latest available disclosures and market signals.

Mordor Intelligence's United States Ott Market Size Measured Against Other Published Estimates

Published market values for US OTT can look far apart because sources do not always count the same revenue streams, and they also anchor their models to different timing and pricing assumptions. Differences usually come from whether the estimate is video-only or includes audio, whether ad-funded viewing is fully counted, and whether the year shown is a historical actual or a forward-looking step-up.

Hardware revenue is outside Mordor Intelligence's scope, and that single exclusion can materially change totals when other estimates blend device sales with streaming service revenues, or when they treat platform ecosystem revenues as one bucket. Another common gap is revenue model coverage, since some figures capture subscription-only revenue, while others include FAST and broader advertising, which can move the market size even if user counts look similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 136.67 B (2026) | |

| Trade Journal A | USD 69.00 B (2024) | This figure is described as OTT subscription revenue, so it excludes advertising-funded viewing and transactional revenue, and it is not aligned to the 2026 base year shown in the report. |

| Industry Outlook B | USD 112.70 B (2029) | This estimate focuses on OTT streaming video and emphasizes SVOD plus video ad-supported components, which can differ from a broader OTT view that also counts streaming audio and uses a different year and price progression path. |

The spread in the table is mainly explained by what is being counted, and by the year each source highlights, which changes the implied pricing and adoption level. By tying the model to a clear demand pool, revenue model mix, and checkable price and advertising assumptions, we keep the size traceable and repeatable for planning use.

Key Questions Answered in the Report

What is the size of the United States OTT market?

The United States OTT sector is estimated at USD 135.09 billion in 2026 and is projected to reach USD 208.58 billion by 2031, at a 9.08% CAGR.

What is driving OTT adoption in the United States?

Cord-cutting, broader advertising-supported viewing, improved broadband access, and demand for more specialized content are supporting adoption.

Which revenue model leads US OTT services?

SVOD led with a 51.75% revenue share in 2025, while AVOD is projected to record the highest growth at a 9.71% CAGR through 2031.

Which devices are most important for streaming services?

Smartphones and tablets held 53.62% of device-type revenue in 2025, while smart TVs are projected to grow at a 9.86% CAGR through 2031.

Which content genre leads US streaming platforms?

TV shows and episodic content held 45.39% of content genre revenue in 2025, while documentaries are projected to expand at a 9.75% CAGR through 2031.

What are the main challenges for OTT platforms?

Rising content costs, subscriber churn, discovery challenges, and environmental scrutiny can limit profitability and engagement.

Page last updated on: