Video Streaming Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

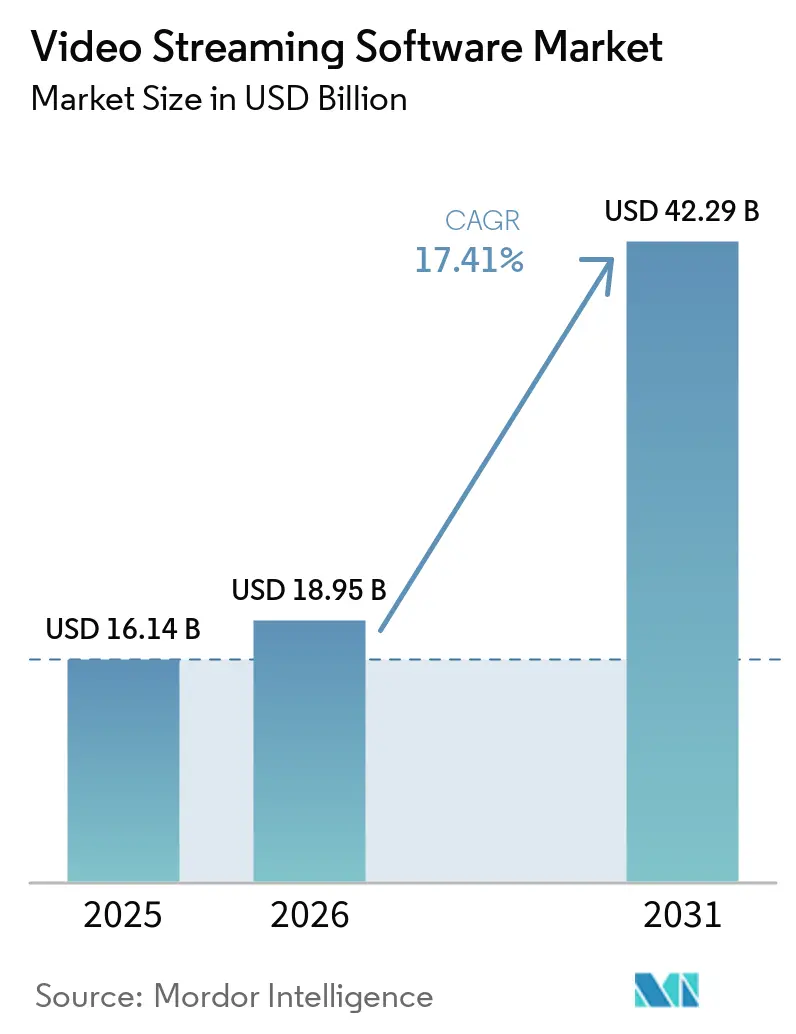

| Market Size (2026) | USD 18.95 Billion |

| Market Size (2031) | USD 42.29 Billion |

| Growth Rate (2026 - 2031) | 17.41% CAGR |

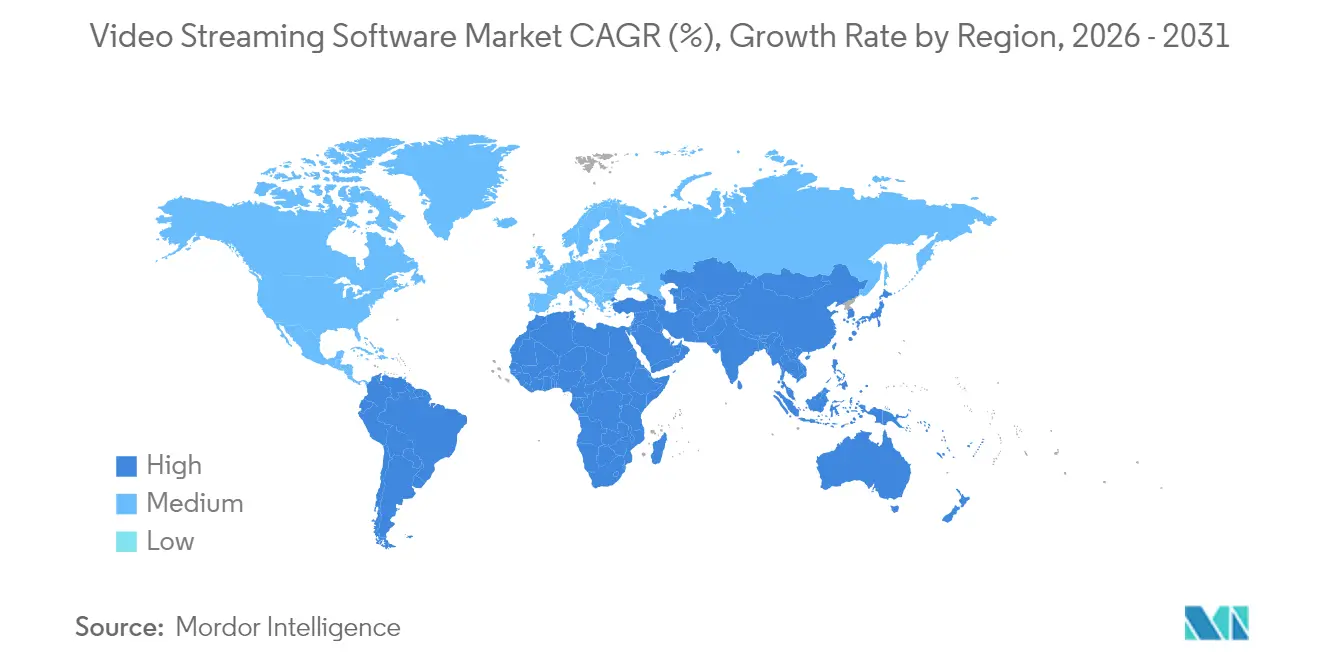

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Streaming Software Market Analysis by Mordor Intelligence

The video streaming software market size in 2026 is estimated at USD 18.95 billion, growing from 2025 value of USD 16.14 billion with 2031 projections showing USD 42.29 billion, growing at 17.41% CAGR over 2026-2031. The expansion of the video streaming software market reflects the migration from fixed-function appliances toward cloud-native stacks that integrate encoding, content management, and analytics inside a single programmable layer. Enterprises view video as essential for customer engagement, employee collaboration, and regulatory compliance, so purchasing decisions now prioritise modular platforms that scale elastically without capital lock-in. A mid-tier university’s 2024 shift to a browser-based lecture-capture suite demonstrated the productivity impact: hardware refresh costs fell while concurrent live classes doubled under an unchanged headcount. Hospitals followed similar logic once authorities ruled that teleconsultation footage forms part of the longitudinal patient record, prompting budget allocations for encrypted archives that double as searchable training assets. Vendors able to wrap these compliance functions inside managed-service bundles have improved recurring revenue visibility and insulated themselves from pure usage pricing pressure, further anchoring growth in the video streaming software market.

Key Report Takeaways

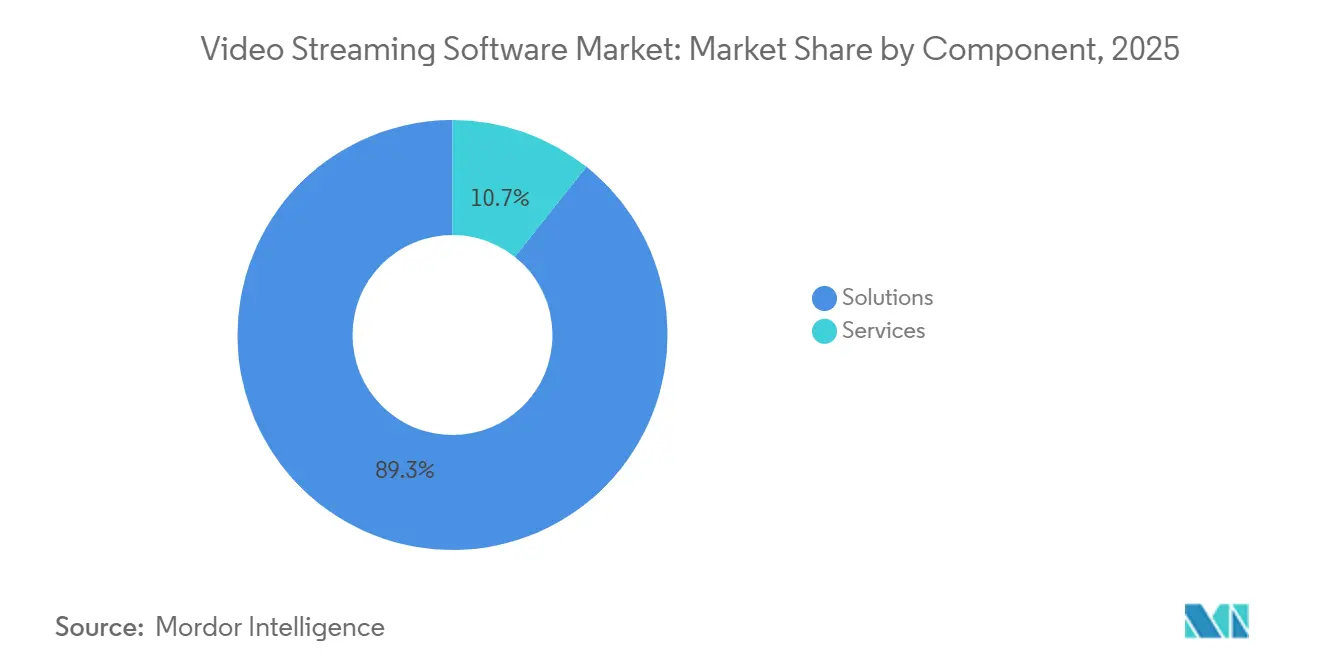

- By Component, solutions accounted for 89.30% of the video streaming software market share in 2025 while services segment was advancing at a 20.9% CAGR through 2031.

- By deployment type, cloud-plus-edge solutions accounted for 68.40% of the video streaming software market share in 2025 while advancing at a 22.1% CAGR through 2031.

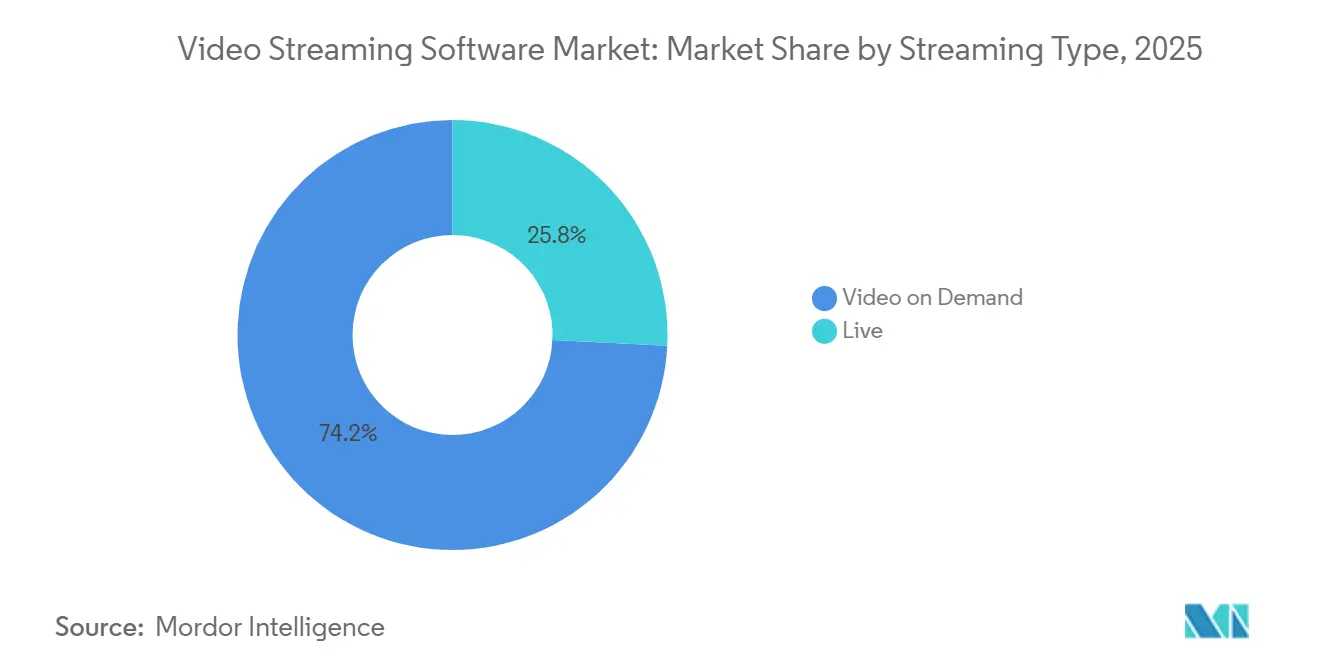

- By streaming type, video-on-demand held 74.20% of the video streaming software market size in delivery minutes in 2025; live streaming is forecast to grow at a 20.35% CAGR through 2031.

- By vertical, media & entertainment commanded 46.30% revenue share in 2025, whereas healthcare is projected to expand at a 23.1% CAGR, the fastest among tracked industries.

- By geography, North America led with 37.60% revenue share in 2025, while Asia-Pacific is on track for roughly 19.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Video Streaming Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G SA networks accelerating low-latency enterprise streaming | +3.20% | Asia-Pacific, with spillover to North America | Medium term (3-4 yrs) |

| Cloud-native micro-services adoption boosting SaaS OTT platforms | +2.80% | North America, with global adoption following | Short term (≤2 yrs) |

| Corporate spend on hybrid-work townhalls fuelling internal live-video platforms | +1.50% | Europe, North America | Short term (≤2 yrs) |

| Shoppable livestream commerce uptake driving interactive streaming tools | +1.80% | Middle East, Asia-Pacific | Medium term (3-4 yrs) |

| US CMS rules mandating secure tele-video archiving | +2.5% | North America, with global regulatory spillover | Short term (≤2 yrs) |

| D2C sports-rights migration energising multi-CDN orchestration | +1.4% | South America, global sports markets | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Rapid 5G stand-alone networks transforming enterprise video in Asia-Pacific

Standalone 5G roll-outs have pushed end-to-end latency below 10 milliseconds in early manufacturing pilots. Factories now stream multi-angle HD feeds from robotic welding lines to remote inspectors, eliminating manual lag and keeping production running. When every fractional second saved translates into extra units produced per hour, management quickly assigns a budget to the video streaming software market for inline quality monitoring solutions. Emerging case studies travel fast across supply-chain consortia, expanding addressable demand beyond initial smart-factory adopters.

Cloud-native microservices shortening feature cycles for North-American OTT platforms

In 2024, many North American providers decomposed monoliths into containerised microservices that handle encoding, recommendation, and server-side ad insertion as independent workloads. Operators can now dial up only the microservice that spikes, such as recommendations during a celebrity live interview, without overspending on the rest of the stack. The resulting pay-as-you-grow economics reduce over-provisioning, fuel incremental R&D allocations, and attract new subscribers, feeding additional momentum into the video streaming software market.

Corporate hybrid-work townhalls fuelling live-video platforms in Europe

European enterprises moved quarterly meetings from conference halls to internal live streams once local networks achieved sub-second start times. Recordings feed searchable hubs where staff jump to chapters tagged by topic, answering repeat field-service questions without new memos. Internal analytics show that 40% of recurring queries now resolve through replay clips, freeing frontline managers for higher-value work and encouraging further investment in enterprise-grade capabilities from the video streaming software market.

Interactive livestream shopping catalysing ultra-low-latency tools in the Middle East

Influencer-led shopping broadcasts overlay purchase links on near-real-time video. Inventory levels adjust inside the same interface, so hosts shift focus the moment a colour variant dips below the threshold. Payment confirmations return by webhook and keep shoppers inside the stream, cutting abandonment. Retailers thus view latency budgets and conversion metrics as inseparable, boosting demand for ultra-low-latency modules in the video streaming software market.

Restraints Impact Analysis of Video Streaming Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating adaptive-bitrate patent royalties squeezing smaller vendors | -1.20% | Global, with higher impact in emerging markets | Long term (≥5 yrs) |

| GDPR / Schrems-II hurdles limiting EU cross-border video data flows | -2.10% | Europe, with global platforms serving EU customers | Medium term (3-4 yrs) |

| Rural last-mile congestion in Africa undermining QoS SLAs | -0.8% | Africa, rural areas globally | Long term (≥5 yrs) |

| High creator churn on freemium platforms eroding SMB ARPU | -0.6% | Global, higher impact in price-sensitive markets | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Patent royalty escalation motivating open codecs among independent vendors

Rising minimum payments for adaptive-bitrate IP compel niche providers to trial royalty-free formats. One learning-management platform offset marginally larger file sizes by re-balancing bitrate ladders, saving licence fees and protecting gross margin. Server-side detection routines down-switch devices that lack support, providing a hedge against royalty hikes, yet placing downward pressure on the video streaming software market in segments most exposed to patent fees.

GDPR data-transfer rulings reshaping EU platform architectures

Stricter enforcement pushes services to duplicate origin objects inside the European Economic Area. A mid-tier provider launched local authentication nodes so PII stays in-region while anonymous analytics flow globally, trading short-term CapEx for faster contract closures with public-sector clients. The added infrastructure cost drags slightly on European-based revenue contribution, but also positions compliant vendors for premium pricing within the video streaming software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Video Streaming Software Market Segment Analysis

By Component:

Platforms anchor spend while services accelerateSolutions contributed the larger slice of 2025 revenue, estimated at 89.3%, because every deployment still needs a platform core to ingest, encode, and manage assets. That core foundation keeps the video streaming software market expanding as feature road-maps layer analytics, AI thumbnails, and automated QC onto the same codebase. Services revenue, however, is forecast to climb at 20.9% CAGR as overstretched IT departments outsource complex integrations such as speech-to-text tagging, event-driven transcodings, and zero-trust access controls. Managed contract, then monitor SLA compliance and patch vulnerabilities, creating sticky annuity streams. Over the forecast horizon, joint go-to-market programmes between platform suppliers and specialised integrators will channel incremental opportunities back into the video streaming software market.

Even with faster services growth, vendors that own the platform architecture preserve pricing power because customers rarely re-platform once content libraries and business logic are embedded. Continuous codec innovation triggers periodic upgrades that renew contracts, while analytics plug-ins feed dashboards correlating churn to buffer events. The interplay stabilises revenue and keeps the solutions layer at the centre of the video streaming software market even as service ecosystems flourish in parallel.

By Deployment Type:

Cloud-plus-edge consolidates leadershipCloud deployment captured 68.40% of the video streaming software market size in 2025 and is projected to grow at a 22.1% CAGR as operators gravitate toward elastic capacity that accommodates unpredictable traffic spikes. Edge nodes now handle just-in-time packaging and ad decisioning nearer to end-users, reducing startup time and offloading origin servers. The approach shone during a 2025 music festival where multi-camera 4K streams retained frame integrity despite fluctuating cellular conditions, reinforcing trust in cloud-edge architectures within the video streaming software market.

On-premise solutions remain viable when data sovereignty or sunk investments dictate local processing. Banks encode sensitive board meetings inside private centres, then push DRM-protected ladders to external CDNs for worldwide playback. Hybrid pipelines, capture on-premise, transcode in regional clouds, enforce geo-blocking at the edge, let operators blend compliance with elasticity. As single-pane consoles converge, decision makers weigh commercial terms rather than architectural philosophy, yet the momentum still favours cloud-first strategies that align with the broader video streaming software market.

By Streaming Type:

VOD dominance, live accelerationVideo on demand delivered 74.20% of total minutes in 2025, reflecting the evergreen value of library assets that amortise production costs across repeated plays. AI-generated trailers, chaptering, and recommendation engines extend dwell times and reinforce the economics, cementing VOD’s weight within the video streaming software market. Live streaming, while smaller, is racing ahead at 20.35% CAGR as enterprises pivot to interactive townhalls, flash-sale commerce, and real-time sports. Advances in parallelised encoders now keep glass-to-glass delay under 1 second on commodity hardware, unlocking use cases that demand sub-second responsiveness.

Boundaries blur when sports clips are sliced in real time and dropped into VOD back catalogues within minutes, multiplying monetisation paths. Unified analytics compares how a single user behaves across modes, feeding insights back into personalisation loops. This feedback mechanism persuades platform owners to maintain single stacks that manage both live and VOD with equal agility, sustaining cross-module licence revenues in the video streaming software market.

By Vertical:

Media and entertainment leads, healthcare races aheadMedia and entertainment commanded 46.30% revenue in 2025 thanks to early OTT adoption, global rights portfolios, and well-funded direct-to-consumer strategies. Studios use AI to time promotions that maintain binge-watch momentum, while sports federations integrate concurrency handling to serve tens of millions of simultaneous viewers. The need for global reach, piracy protection, and premium-grade user interfaces signals consistent spend on advanced modules, thereby anchoring leadership in the video streaming software market.

Healthcare, though smaller, is forecast to grow at a 23.1% CAGR because regulatory clarity has elevated video to a mission-critical status. Hospitals discovered that embedding recordings in electronic medical records slashed nurse callback volumes and accelerated multidisciplinary consultations. Banking, education, and government agencies observe similar governance imperatives, each layering bespoke encryption, indexing, and access-control schemes atop the same codec engines. These cross-sector parallels widen the funnel for the video streaming software market and diversify revenue beyond entertainment.

Geography Analysis

North America Video Streaming Software Market

North America held 37.60% of the video streaming software market in 2025 due to widespread broadband, dense hyperscale capacity, and an early cultural shift toward video-first workflows. Hospitals budget for compliant archives that convert regulatory burdens into searchable knowledge bases, while broadcasters embed predictive analytics that improve customer retention. A publicly listed vendor’s 2024 SEC filing confirmed a strategic pivot toward automated engagement engines, and investors rewarded the move with valuation gains, signalling confidence in differentiated feature sets over commoditised delivery .

APAC Video Streaming Software Market

Asia-Pacific is set for roughly 19.4% CAGR thanks to mobile-first demographics and aggressive 5G stand-alone coverage that brings high-resolution, low-latency experiences into rural districts. Governments subsidise tower build-outs and local content production, turning language-specific subtitles and dubbing into standard bid requirements. Providers deploy multi-tenant regional clouds that segregate workloads by country while sharing control planes, balancing compliance with economies of scale and enlarging the total addressable slice of the video streaming software market.

Europe Video Streaming Software Market

Europe blends advanced consumer expectations with stringent privacy laws. After 2024 judicial rulings, platforms accelerated data-centre build-outs inside the bloc to ensure personal identifiers never exit EU borders. A UK broadcaster’s migration of 7,000-plus hours of heritage content into a cloud-native workflow yielded a ten-fold uptick in parallel processing throughput . Though upfront costs spiked, turnaround times shrink, enabling same-day episodic release that viewers now expect. Advertiser-funded tiers gain traction, driving demand for SSAI modules tuned to European measurement frameworks and enlarging the regional opportunity within the video streaming software market.

Competitive Landscape

The video streaming software market features a handful of integrated platforms and a long tail of specialists. Leading vendors embed engagement engines, AI metadata extraction, and compliance workflows directly into their SaaS cores, shifting differentiation from baseline delivery to intelligence layers. A 2024 SEC filing confirmed this strategic tilt for one major provider. Larger firms broaden revenue with adjacent managed services that promise a single contract for operations, security, and analytics, appealing to overstretched enterprise buyers.

Private-equity groups continue bundling mid-tier enablers, transcoding, player SDKs, DRM, into full-stack alternatives that challenge incumbents on total cost of ownership. Simultaneously, niche vendors flourish in regulated segments such as clinical endoscopy capture, where domain know-how and specialised hardware integration deter generalists. Patent filings around neural compression underline that IP remains a competitive weapon; a recent United States patent grant covers a machine-learning encoder that achieves bandwidth savings without visible artefacts [3]United States Patent and Trademark Office, “Patent Grant 11,323,738,” uspto.report.

Start-ups employ developer-first APIs that drop code snippets into mobile apps in minutes. Their traction stems from transparent pricing and quick proofs of concept, yet enterprise prospects still demand uptime guarantees and compliance attestations. The fragmented landscape creates acquisition targets for larger players looking to fill portfolio gaps, indicating that M&A will remain a core feature of the video streaming software market through the forecast horizon.

Video Streaming Software Industry Leaders

Kaltura, Inc.

Brightcove, Inc.

Panopto, Inc

Haivision Systems Inc.

Vimeo.com, Inc.

- *Disclaimer: Major Players sorted in no particular order

Video Streaming Software Market Companies Covered in this Report

- Brightcove Inc.

- Kaltura Inc.

- Amazon Web Services, Inc. (AWS Elemental)

- IBM Corporation

- Vimeo.com Inc.

- Panopto Inc.

- Haivision Systems Inc.

- Vbrick Systems Inc.

- Qumu Corporation

- Dacast

- Mux

- MediaPlatform, Inc.

- Bitmovin

- Akamai Technologies, Inc.

- Wowza Media Systems, LLC

- JW Player Inc.

- Google LLC (YouTube Live)

- Harmonic Inc.

- Telestream, LLC

- Cloudinary

- Synamedia Ltd.

- Verizon Media (Edgecast)

Recent Industry Developments in Video Streaming Software Market

- May 2025: A tri-state hospital network finished migrating 3 million minutes of telehealth footage to encrypted archives.

- March 2025: A public utility enabled live 5G remote-assist for field repairs, cutting truck rolls by 12%.

- February 2025: Comcast confirmed Dolby Atmos support for Super Bowl LIX broadcasts to Xfinity subscribers.

- January 2025: Arvato Systems released Web Render Engine, enabling simultaneous browser-based compositing.

Video Streaming Software Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the video streaming software market as cloud-based or on-premise platforms that ingest, encode, store, secure, and deliver live or on-demand video over IP networks to any connected device. Revenue covers software licenses, usage-based SaaS fees, and managed service add-ons that sit on top of these platforms.

Scope exclusion: pure-play content providers, consumer hardware, and CDN transit fees are kept outside the model to keep focus on core software value.

Segments Covered in This Report

- By Component

- Solutions

- Video Management

- Transcoding and Processing

- Video Delivery and Post-Production

- Video Analytics

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Type

- Cloud

- On-premise

- By Streaming Type

- Live

- Video on Demand

- By Vertical

- Media and Entertainment

- OTT Platforms

- Broadcast and Cable TV Networks

- Sports and Esports

- Corporate and Enterprise

- Education and eLearning

- Healthcare and Telemedicine

- Banking, Financial Services and Insurance (BFSI)

- Other Verticals

- Media and Entertainment

- By Geography

- North America

- United States

- Canada

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of Latin America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We held structured calls with solution architects at platform vendors, live-event producers, CIOs within media enterprises, and procurement heads across healthcare systems in North America, Europe, and Asia-Pacific. These conversations validated real-world encoder pricing, region-specific latency targets, and the mix shift toward OTA cloud workflows, helping us adjust desk-based assumptions.

Desk Research

Mordor analysts first map the demand pool through publicly available statistics such as ITU broadband subscriptions, Cisco VNI traffic indices, and national 5G SIM penetration. Trade bodies, for example, the Streaming Video Technology Alliance and the Interactive Advertising Bureau, supply adoption benchmarks and cost ranges. Annual reports, investor decks, and S-1 filings help us capture average selling price movements, while patent mining via Questel lets our team monitor codec innovation cycles and likely cost compression. Subscription churn ratios, gleaned from Form 10-K disclosures and Dow Jones Factiva news feeds, round out the baseline. This list is illustrative; many additional secondary sources are reviewed during validation.

Market-Sizing & Forecasting

A top-down build begins with global downstream IP video traffic, splits by live and VOD minutes, and converts minutes to software spend through region-specific monetization rates, then refined with bottom-up cross-checks such as sampled vendor revenue roll-ups and average contract value multiplied by active enterprise accounts. Key variables include 5G standalone coverage, average encoder price per streamed hour, enterprise town-hall frequency, CDN egress cost curves, and interactive commerce adoption. Multivariate regression links these drivers to historic spend, while scenario analysis moderates forecast swings. Data gaps in smaller regions are bridged by applying usage density ratios against confirmed broadband lines before being rerun through the forecast model.

Data Validation & Update Cycle

Outputs undergo three-step variance checks, peer review, and sign-off. Models refresh annually; mid-cycle revisions are triggered when material events such as codec royalty changes or sudden regulatory shifts alter cost structures.

How Mordor Intelligence's Video Streaming Software Market Size Compares to Other Published Estimates

Published numbers differ because firms pick distinct software scopes, driver sets, and refresh cadences.

Key gap drivers include whether professional services are counted, the handling of pass-through CDN charges, currency conversion timing, and how aggressively 5G uptake is baked into forecasts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.14 B (2025) | Mordor Intelligence | - |

| USD 13.96 B (2024) | Global Consultancy A | Excludes managed services and assumes constant ASPs, leading to lower value. |

| USD 14.51 B (2025) | Industry Journal B | Relies on voluntary vendor disclosures, omits healthcare and education use cases. |

| USD 13.30 B (2024) | Regional Consultancy C | Counts only on-premise deployments and applies single-digit churn, understating SaaS expansion. |

The comparison shows that when service layers, fresh ASP trends, and high-growth verticals are fully incorporated, Mordor's figure emerges as a balanced, transparent baseline that decision-makers can replicate and audit.

Key Questions Answered in the Report

What is the size of the video streaming software market in 2026?

The video streaming software market size stands at USD 18.95 billion in 2026.

How fast will the video streaming software market grow by 2031?

Between 2026 and 2031 the market is forecast to expand at a 17.41% CAGR, reaching USD 42.29 billion.

Which deployment model leads the video streaming software market?

Cloud-plus-edge deployments dominate with 68.40% market share in 2025 and maintain a 22.1% CAGR through 2031.

Which vertical is expected to grow the quickest?

Healthcare is projected to expand at a 23.1% CAGR due to regulatory mandates for secure video archiving.

What technological trend most impacts latency-sensitive applications?

Standalone 5G networks delivering sub-10 millisecond latency in Asia-Pacific factories are transforming real-time quality-inspection use cases.

Why are vendors adopting microservice architectures?

Microservices let operators scale only the functions experiencing traffic spikes, lowering cloud fees and accelerating feature releases, advantages that reinforce adoption in the video streaming software market.

Page last updated on: