Advertising Based Video On Demand (AVOD) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 104.35 Billion |

| Market Size (2031) | USD 175.01 Billion |

| Growth Rate (2026 - 2031) | 10.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advertising Based Video On Demand (AVOD) Market Analysis by Mordor Intelligence

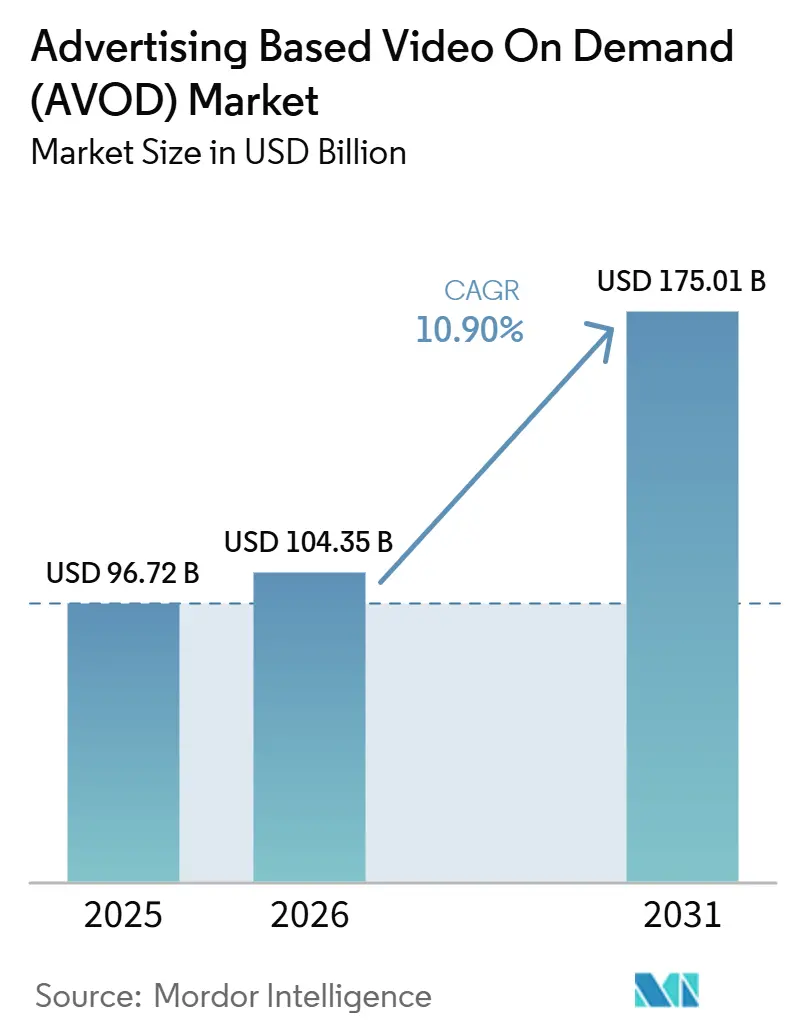

The advertising based video on demand (AVOD) market size is expected to grow from USD 96.72 billion in 2025 to USD 104.35 billion in 2026 and is forecast to reach USD 175.01 billion by 2031 at 10.90% CAGR over 2026-2031. The main expansion pattern comes from advertising budgets shifting out of linear television and into streaming environments that now attract a larger share of total viewing time. The category is also evolving in quality, as connected TV is no longer treated as a side channel and is now planned alongside broader television and digital video campaigns. Retail media links, commerce measurement, and stronger first-party data assets are making the advertising-based video on demand (AVOD) market more useful for both brand building and performance spending. At the same time, premium inventory is becoming more valuable where platforms can combine audience identity, household reach, and automated buying tools. The main limits remain viewer fatigue from repetitive ads, privacy rules that reduce targeting flexibility, and rising pressure on platforms to keep content libraries deep without weakening monetization efficiency.

Key Report Takeaways

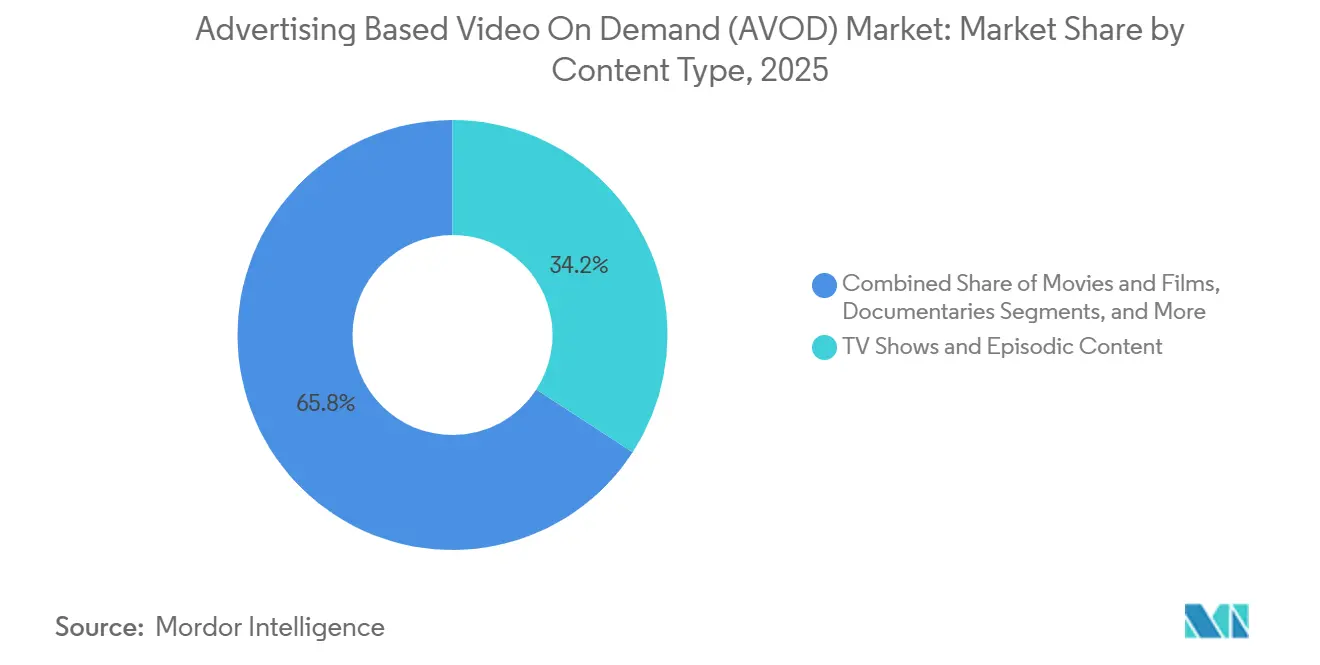

- By content type, TV shows and episodic content held 34.17% share of the advertising based video on demand (AVOD) market in 2025, while other content types are projected to expand at an 11.62% CAGR through 2031.

- By device type, smart TVs accounted for 41.59% of revenue in 2025, while smartphones and tablets are expected to record the fastest growth at an 11.76% CAGR through 2031.

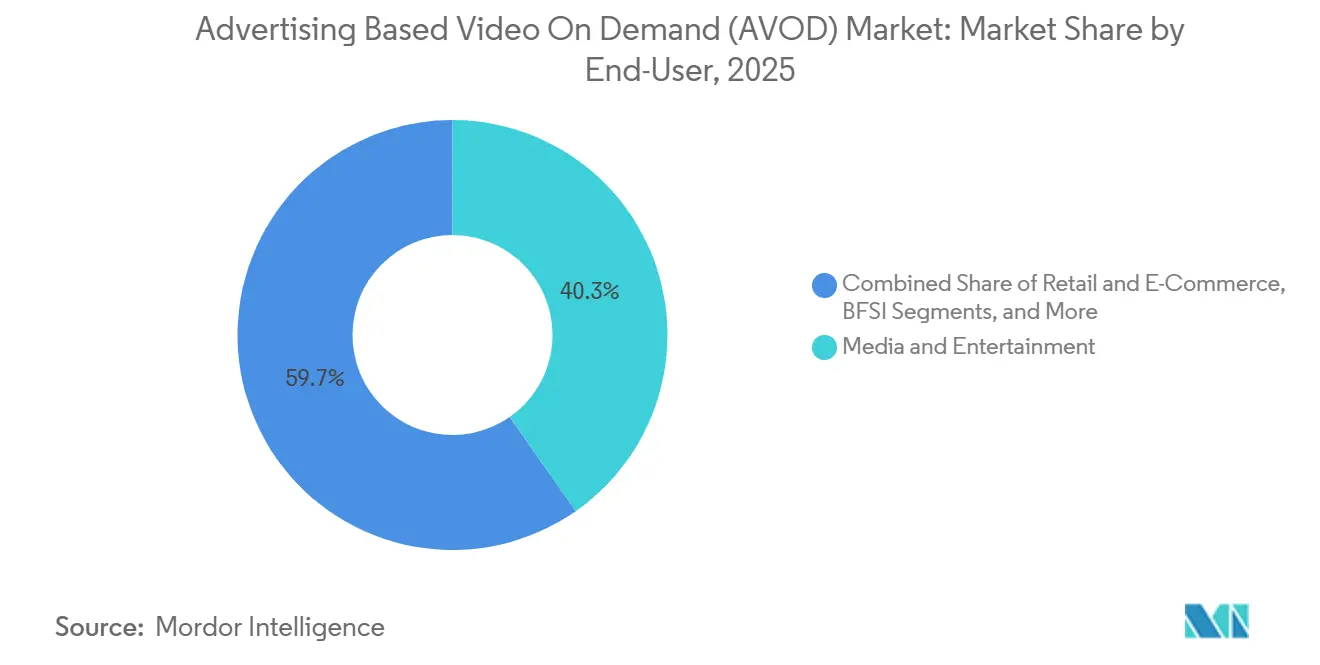

- By end-user, media and entertainment captured 40.28% share in 2025, while retail and e-commerce are projected to advance at a 12.16% CAGR through 2031.

- By ad format, pre-roll accounted for 47.52% of the market in 2025, while mid-roll is expected to expand at a 12.64% CAGR through 2031.

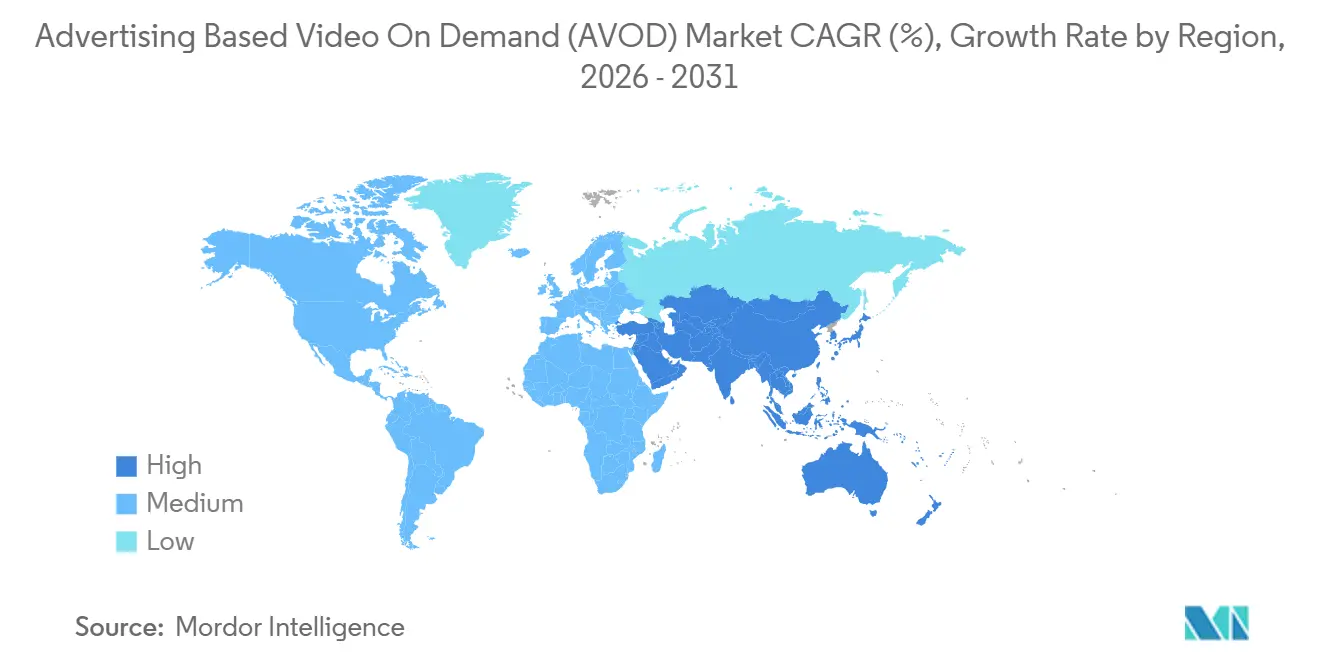

- By geography, North America held 39.54% share in 2025, while Asia-Pacific is projected to grow at an 11.93% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Advertising Based Video On Demand (AVOD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Connected TV Ad Spend Migration | +3.2% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Retail Media and Shoppable Video Convergence | +2.4% | North America and Europe, with spillover to the Asia-Pacific | Medium term (2-4 years) |

| First-Party Data Targeting Demand | +1.8% | Global, with regulatory pressure concentrated in the EU and California | Short term (≤ 2 years) |

| Streaming-Exclusive Live Sports Inventory Expansion | +1.4% | North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| AI-Led Ad Personalization and Yield Optimization | +1.1% | Global, with North America and the EU leading adoption | Long term (≥ 4 years) |

| FAST Channel Monetization Scale-Up | +0.9% | North America, with expansion to Europe and the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Connected TV Ad Spend Migration

Advertising migration from linear television to connected TV remains the strongest force shaping the advertising based video on demand (AVOD) market, because buyers now see streaming as a core television channel rather than an experimental line item. The 2026 Premion and Advertiser Perceptions survey showed that 70% of U.S. advertisers planned to increase CTV and OTT spending by an average of 17% in 2026, with 28% of that increase expected to come directly from reallocation from broadcast linear.[1] Premion and Advertiser Perceptions, “2026 CTV/OTT Advertiser Survey,” Premion, premion.com The same change is widening the buyer base, as the IAB reported that the share of small spenders with annual budgets below USD 50 million investing in CTV rose from 60% in 2024 to 85% in 2026, driven by self-serve tools. That broadening matters because it adds a long tail of recurring demand that older television sales models could not serve efficiently. The survey also found that integrated and hybrid buying teams now control 55% of CTV budgets, which shows that planning workflows are consolidating and favoring platforms with strong programmatic infrastructure.

Retail Media and Shoppable Video Convergence

Retail media integration is changing the advertising based video on demand (AVOD) market from a reach channel into a measurable sales channel with clearer purchase attribution. Criteo stated that its April 2025 rollout of Onsite Video, used by Albertsons Companies, Costco, and Walmart Mexico, produced a 280% increase in click-through rates and a 460% lift in sales when paired with sponsored product ads in early tests. Roku extended this logic in April 2026 through Roku Curate, which combined Roku audience data with verified purchase signals from Best Buy Ads, Instacart, Kroger Precision Marketing, and other retail partners inside ordinary buying workflows. This development matters because it lowers the gap between video exposure and sales measurement, which has historically limited performance budgets in streaming environments. It also increases pressure on pure-play AVOD operators, because platforms without first-party commerce signals will find it harder to match the value proposition of retail-linked inventory.

First-Party Data Targeting Demand

Demand for first-party targeting is strengthening the advertising based video on demand (AVOD) market because streaming platforms rely less on open web cookies and more on logged-in audience relationships. The IAB found that targeting capabilities became the top criterion for TV and video ad spend allocation in 2026, at 49%, ahead of content quality at 46%, indicating that data precision now drives budget allocation more directly. Acxiom, IPG Mediabrands, and IRIS.TV responded to that need in August 2025 by launching a contextual CTV solution built on IRIS_ID that spans more than 75 million IRIS-enabled videos without relying on personal identifiers. That matters because marketers want workable alternatives as privacy rules tighten and cookie-based methods weaken. As a result, platforms that can combine deterministic identity, contextual relevance, and clean-room-style matching are in a stronger position in premium streaming demand.

Streaming-Exclusive Live Sports Inventory Expansion

Exclusive live sports rights are raising the value of the advertising based video on demand (AVOD) market because they create scarce, time-sensitive inventory that attracts high advertiser urgency. PubMatic launched an AI-powered Live Sports Marketplace in July 2025, allowing advertisers to target specific game moments in real time across inventory tied to leagues such as the NBA, WNBA, MLB, NHL, and the National Women's Soccer League. EverPass also expanded the commercial distribution of digital-only sports programming in 2025, including NFL and ESPN+ rights packages for U.S. commercial venues. These moves show that streaming sports inventory is becoming more structured and easier to package for advertising demand. They also support firmer pricing because premium live-viewing moments are in limited supply and difficult for buyers to replicate at the same scale elsewhere.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ad-Load Fatigue and Viewer Churn | -1.6% | Global, with highest intensity in North America | Short term (≤ 2 years) |

| Privacy-Led Targeting Constraints | -1.2% | EU and North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Content Licensing Cost Inflation | -0.8% | North America and Europe | Medium term (2-4 years) |

| Measurement Fragmentation Across Devices | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ad-Load Fatigue and Viewer Churn

Ad-load fatigue remains the clearest operating risk for the advertising based video on demand (AVOD) market because short-term revenue gains can weaken the audience stability that ad-supported models depend on. Parks Associates reported in 2025 that 70% of streaming viewers identified repetitive ad exposure as their leading frustration, which shows that audience tolerance is being tested as ad-supported tiers expand. The user draft also noted a 9:1 churned-to-active user ratio across apps in the Samsung Tizen ecosystem, reinforcing the idea that weak ad quality and excessive repetition can damage retention. This issue is important because audience erosion reduces the scale that advertisers are paying for and weakens pricing leverage over time. Platforms that invest in frequency controls, creative rotation, and better relevance are better placed to defend both user engagement and monetization quality.

Privacy-Led Targeting Constraints

Privacy regulation is placing uneven pressure on the advertising based video on demand (AVOD) market, especially for operators that rely on granular behavioral targeting to support premium pricing. The user draft highlighted GDPR, CCPA, CPRA, and VPPA as the main policy frameworks increasing consent, matching, and disclosure requirements across key markets. The IAB reported that advertiser concern around targeting capability in CTV rose 9 points year over year in 2026, showing that signal loss is becoming a real planning issue rather than a future one. Those requirements raise operating costs because platforms need clean-room processes, identity alternatives, and more formal consent management systems. The effect favors larger streaming platforms that already have stronger data infrastructure, while smaller or regional operators face a higher relative burden to maintain campaign precision.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Episodic Programming Anchors Platform Monetization

TV shows and episodic content held 34.17% of the advertising based video on demand (AVOD) market share in 2025, reflecting how serialized viewing creates repeated ad opportunities within the same session. In the advertising based video on demand industry, this format benefits from session stacking, where viewers move from one episode to the next without leaving the platform. That pattern raises ad impression density without requiring a matching increase in content acquisition or delivery costs. Movies and films still represent an important viewing pool, but they typically feature fewer mid-roll breaks per viewing session, which limits monetization compared to episodic libraries.

Other content types in the advertising based video on demand (AVOD) market size mix are projected to grow at an 11.62% CAGR from 2026 to 2031, supported by creator-led video, sports clips, news formats, and broader FAST channel programming. This shift matters because inventory categories that were once considered unstructured are now sold to advertisers more systematically. The user draft also pointed to iQIYI's plan to release more than 100 short-form dramas in 2026 through its Nattopro platform, showing that short-form programming is becoming a dedicated monetization category. Shorter formats can support a higher ad-to-content ratio per minute, which improves yield when audience attention is strong and content costs are tightly managed.

By Device Type: Smart TVs Anchor Premium Inventory, Mobile Scales Broadly

Smart TVs captured 41.59% share in 2025, which kept the living room at the center of premium pricing in the advertising based video on demand (AVOD) market. Roku reported 38.7 billion streaming hours in Q1 2026, up 8% year over year, which confirmed continued heavy engagement on large-screen interfaces in developed markets.[2]Roku, Inc., “Form 10-Q Quarterly Report,” U.S. Securities and Exchange Commission filing archive, last10k.com Large-screen viewing remains attractive because it is associated with stronger attention, better recall, and a viewing setting that resembles traditional television. Laptops and desktops continue to lose relative importance as viewing shifts toward smart TV operating systems with stronger ad-serving capabilities.

The advertising based video on demand (AVOD) market size for smartphones and tablets is projected to expand at an 11.76% CAGR through 2031, driven by mobile-first streaming habits in Asia-Pacific and South America. The user draft linked that trend particularly to India, where ad-supported models are expected to account for more than 70% of incremental online video growth by 2030. The main challenge is that cross-device identity remains inconsistent when a household uses both mobile and connected TV devices, leading to duplication and poor frequency control. Solutions tied to authenticated household graphs and device-level identity partnerships are improving the situation, but adoption remains uneven outside the largest platform ecosystems.

By End-User: Media And Entertainment Leads, Retail and E-Commerce Reshapes Ad Economics

Media and entertainment held 40.28% share in 2025, giving it the largest end-user position in the advertising based video on demand (AVOD) market because the format naturally fits content promotion, gaming, entertainment launches, and audience context buying. Entertainment advertisers often benefit from a close alignment between what viewers are watching and the campaigns they see. BFSI also remains relevant in markets where compliant financial promotion is allowed, although regulatory standards make campaign design more complex. Education and healthcare are emerging categories, but they tend to require greater attention to audience sensitivity and message suitability.

Retail and e-commerce are forecast to grow at a 12.16% CAGR from 2026 to 2031, making it the fastest-expanding end-user category in the advertising based video on demand (AVOD) market. That growth reflects spending moving out of search and social into streaming placements that can support shoppable formats and stronger attribution loops. The user draft also noted that long-form mid-roll placements can support higher unaided brand recall than short-form pre-roll placements, underscoring the importance of content length in performance planning. Other end-users, including travel, automotive, and food service, are also shifting budgets toward streaming where video formats can support both brand visibility and direct-response goals.

By Ad Format: Pre-Roll Dominates While Mid-Roll Gains Structural Momentum

Pre-roll accounted for 47.52% share in 2025, which kept it as the largest format in the advertising based video on demand (AVOD) market because it is easy to deploy, highly viewable, and widely accepted in campaign planning. Large advertisers also favor pre-roll because measurement conventions are already well established across digital video buying. That reduces friction when campaigns run across multiple publishers or devices. Post-roll remains the smallest format because more platforms now guide viewers directly into autoplay recommendations, leaving fewer clean exit points for post-content placements.

Mid-roll represents the fastest growth path, and the advertising based video on demand (AVOD) market size for this format is projected to rise at a 12.64% CAGR through 2031. The IAB reported that targeting capability became the top spending criterion in 2026, which supports mid-roll placements where context and break timing can be more deliberately matched to content flow. Mid-roll also benefits from a natural supply limit, because it depends on content length and platform ad-load rules rather than simple content availability. That tighter supply base can support steadier pricing even as total AVOD inventory expands across the broader advertising based video on demand (AVOD) market.

Geography Analysis

North America accounted for 39.54% of the advertising based video on demand (AVOD) market share in 2025, which made it the leading regional revenue center. The region benefits from mature connected TV infrastructure, high advertiser familiarity, and a strong concentration of premium inventory across large U.S.-originated streaming platforms. Roku's filings also showed continued platform engagement and expanding monetization support, reinforcing why North America still sets the commercial standard for scale, pricing, and programmatic sophistication in the advertising based video on demand (AVOD) market. Canada and Mexico remain smaller than the U.S., but they continue to benefit from cross-border platform expansion and established advertiser workflows.

Asia-Pacific is projected to expand at an 11.93% CAGR from 2026 to 2031, giving the region the fastest growth in the advertising based video on demand (AVOD) market size. AVIA and Media Partners Asia projected that premium AVOD revenue in Asia-Pacific would increase from USD 8 billion in 2025 to more than USD 12 billion by 2030, led by India, Japan, and Australia, followed by South Korea and Indonesia.[3]AVIA and Media Partners Asia, “Asia-Pacific Video and Broadband 2026,” AVIA, avia.org India remains especially important because a high-volume, low-ARPU structure pushes platforms to maximize ad impression output rather than rely mainly on subscription pricing. Japan adds a different profile, with stronger monetization per user, premium local content, and sports-led differentiation. China remains important, but the user draft pointed to near-term advertising pressure and an active pivot toward AI-supported short-form programming as platforms adjust content economics.

Europe remains a major regional pool for the advertising based video on demand (AVOD) market, and broadcaster coordination is becoming more important as local players respond to global platform scale. The user draft also described South America as a rising opportunity centered on Brazil and Argentina, with Roku's ad platform launch in Brazil showing stronger confidence in monetization readiness. Africa is still at an earlier stage, but mobile-first viewing patterns in markets such as South Africa, Nigeria, and Egypt support long-term potential for ad-supported streaming. Across these regions, the advertising based video on demand (AVOD) market is growing where local content, lighter pricing barriers, and flexible advertising models align with consumer willingness to watch ads in exchange for access.

Competitive Landscape

The advertising based video on demand (AVOD) market operates with a moderately concentrated top tier. Alphabet, Amazon, Disney, Netflix, and Comcast hold strong advantages in premium inventory, user data, distribution reach, and buying infrastructure, while many FAST operators, broadcasters, and regional services still compete below them. This means leadership is shaped less by raw content volume alone and more by the ability to package audience identity, automation, and measurable outcomes. The result is a market where scale matters, but targeted partnerships and specialized inventory can still create room for smaller operators. That structure keeps the advertising based video on demand (AVOD) market competitive even as the largest platforms maintain clear bargaining power.

Roku's April 2026 launch of Roku Curate showed how platform operators are moving beyond inventory sales and into outcome-based advertising tools tied to retail purchase signals. PubMatic's July 2025 Live Sports Marketplace demonstrated another route to differentiation, leveraging real-time game-moment curation to make premium sports inventory more actionable for buyers. Criteo's Onsite Video rollout also demonstrated that retail-linked video placement is no longer experimental and can be sold on measurable commerce outcomes. These moves show that the strongest competitive positions are now built around data utility and transaction efficiency as much as content access.

The advertising based video on demand (AVOD) market is also being shaped by better contextual tools and stronger monetization discipline across the supply chain. Acxiom's August 2025 contextual CTV launch with IPG Mediabrands and IRIS.TV showed that privacy-aware targeting is becoming a practical commercial tool rather than a defensive workaround.[4]Acxiom, “IPG Mediabrands, Acxiom and IRIS.TV Launch Contextual CTV Solution,” Acxiom, acxiom.com Sports distribution deals through EverPass further showed that commercial venue access can widen premium ad-supported inventory beyond home viewing environments. As a result, the platforms that combine authenticated demand access, measurable outcomes, and disciplined ad experiences are likely to hold the strongest position through the forecast period.

Advertising Based Video On Demand (AVOD) Industry Leaders

Alphabet Inc.

Amazon.com, Inc.

The Walt Disney Company

Fox Corporation

Paramount Skydance Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Netflix's ad-supported tier surpassed 250 million monthly active viewers globally as of its May 2026 Upfronts presentation, with the company working with over 4,000 advertisers at end of 2025, a 70% year-over-year increase, and ad revenue projected to approximately double to USD 3 billion in 2026, with programmatic inventory poised to exceed half of the company's non-live ad business.

- April 2026: Roku Inc. introduced Roku Curate, a CTV advertising solution bundling Roku's first-party audience data with verified purchase signals from Best Buy Ads, Criteo, Fandango, Fetch, representing USD 212 billion in annual consumer spend, Instacart, spanning 2,200+ retail banners, and Kroger Precision Marketing, enabling closed-loop attribution within standard programmatic buying workflows and counting toward upfront commitments.

- February 2026: iQIYI Inc. reported its Q4 and full-year 2025 financial results, disclosing plans to launch over 100 short-form dramas in 2026 using its proprietary AI content platform Nattopro, which already hosts over 10,000 active creators, as the company pivots toward content formats that improve ad inventory density per viewing hour.

- January 2026: Amazon Ads enabled U.S. media buyers to apply Amazon Audiences when targeting Netflix campaigns through the Amazon DSP, extending the authenticated CTV targeting infrastructure announced in late 2024 and giving Netflix advertisers deterministic access to Amazon's household-level identity graph across premium streaming inventory.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the advertising-based video on demand (AVOD) market as all revenues earned from digital video streams that are made freely available to viewers in exchange for pre-roll, mid-roll, post-roll, or interactive advertisements across connected TVs, mobile devices, PCs, and gaming consoles. Advertising sold against live linear FAST channels is included because the viewer experience and monetization logic mirror on-demand inserts.

Scope exclusion: Subscription-only and pay-per-view models that do not expose an ad break are outside this scope.

Segmentation Overview

- By Content Type

- Movies and Films

- TV Shows and Episodic Content

- Documentaries

- Other Content Types

- By Device Type

- Smartphones and Tablets

- Smart TVs

- Laptops and Desktops

- Other Device Types

- By End-User

- Media and Entertainment

- Retail and E-Commerce

- BFSI

- Education

- Information Technology and Telecommunications

- Healthcare

- Other End-Users

- By Ad Format

- Pre-Roll

- Mid-Roll

- Post-Roll

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Desk Research

We first gathered foundational supply-side metrics from publicly accessible regulators and trade groups such as the Federal Communications Commission, the Interactive Advertising Bureau, Eurostat, and Ofcom, which publish granular data on streaming households, connected-TV penetration, and digital ad CPM ranges. Viewer time-spent statistics were pulled from national audience measurement panels, while macro indicators like household broadband adoption came from the World Bank and ITU. To profile industry economics, we reviewed 10-K filings, investor decks, and earnings calls of leading streamers alongside advertising spend tallies from the top media agency barometers. Select paid databases, notably D&B Hoovers for company financials and Dow Jones Factiva for deal flow, helped us validate revenue splits. The sources cited above are illustrative rather than exhaustive; many additional references informed the desk stage.

Primary Research

Mordor analysts interviewed ad-tech vendors, streaming platforms, agency buyers, and brand marketers across North America, Europe, and Asia-Pacific to stress-test inventory growth rates, average ad loads, and evolving cost-per-thousand benchmarks. They then ran short surveys with viewers to gauge tolerance for ad frequency and discover emerging devices.

Market-Sizing & Forecasting

A top-down model starts with country-level digital video ad spend, rebuilt into an AVOD pool by mapping share-of-voice data and connected-TV impression splits. Supplier roll-ups of major platform revenues and channel checks on average ad loads provide selective bottom-up cross-verification, after which totals are reconciled. Key variables include connected-TV household base, smartphone video watch minutes, average programmatic CPM, ad-load per hour norms, and live-sports streaming rights migration. Multivariate regression with lagged broadband penetration and CPM forecasts projects each driver through 2030; scenario overlays capture privacy regulation shifts and macro ad-spend cycles. Gaps where platform disclosures are thin are bridged by peer benchmarks weighted by traffic estimates.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance screens, peer comparison, and senior analyst sign-off. Reports are refreshed annually, with interim adjustments whenever a material event, such as a platform introducing an ad tier, shifts the baseline.

Why Mordor's Advertising Based Video on Demand (AVoD) Baseline Commands Reliability

Published estimates often diverge because firms choose dissimilar definitions, miss newer device classes, or apply uniform ad-load factors to all regions.

Key gap drivers include: some publishers fold hybrid SVOD with ads revenue into AVOD, others extrapolate global totals from limited U.S. samples, and several assume double-digit CPM inflation without validating with buyers. Mordor's scope, consistent refresh cadence, and dual-path modelling limit these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 45.92 B (2025) | Mordor Intelligence | - |

| USD 49.04 B (2024) | Global Consultancy A | Hybrid SVOD ad tiers blended into core AVOD; single-region CPM uplift applied globally |

| USD 40.80 B (2023) | Industry Association B | Excludes live FAST channels and connected-console viewing; uses static ad-load of four minutes per hour |

| USD 38.21 B (2023) | Regional Consultancy C | Projects spend from legacy desktop video data, undercounting CTV households |

These comparisons show that while headline numbers vary, Mordor's disciplined boundary setting, variable selection, and yearly validation deliver a balanced and transparent baseline that decision-makers can trace back to real-world signals and replicate with confidence.

Key Questions Answered in the Report

What is the size outlook for the advertising based video on demand (AVOD) market?

The advertising based video on demand (AVOD) market was valued at USD 96.72 billion in 2025, rises to USD 104.35 billion in 2026, and is projected to reach USD 175.01 billion by 2031 at a 10.90% CAGR.

What is driving ad-supported streaming growth the most?

The strongest driver is budget migration from linear TV to connected TV, supported by stronger programmatic buying, wider streaming reach, and better retail media measurement.

Which content format drives revenue in ad-supported streaming?

TV shows and episodic content led with 34.17% share in 2025 because serialized viewing creates more repeat ad opportunities within the same session.

Which device group is growing fast for AVOD viewing?

Smartphones and tablets are expected to grow the fastest at 11.76% CAGR through 2031, mainly because mobile-first streaming is expanding across Asia-Pacific and South America.

Which advertiser group is expanding spending the fastest?

Retail and e-commerce are the fastest-growing end-user segments with a 12.16% CAGR, helped by shoppable video and closed-loop attribution tools.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is projected to expand at an 11.93% CAGR, supported by ad-led video models in India, stronger AVOD monetization in Japan, and rising regional streaming demand.

Page last updated on: