Video Editing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 4.99 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

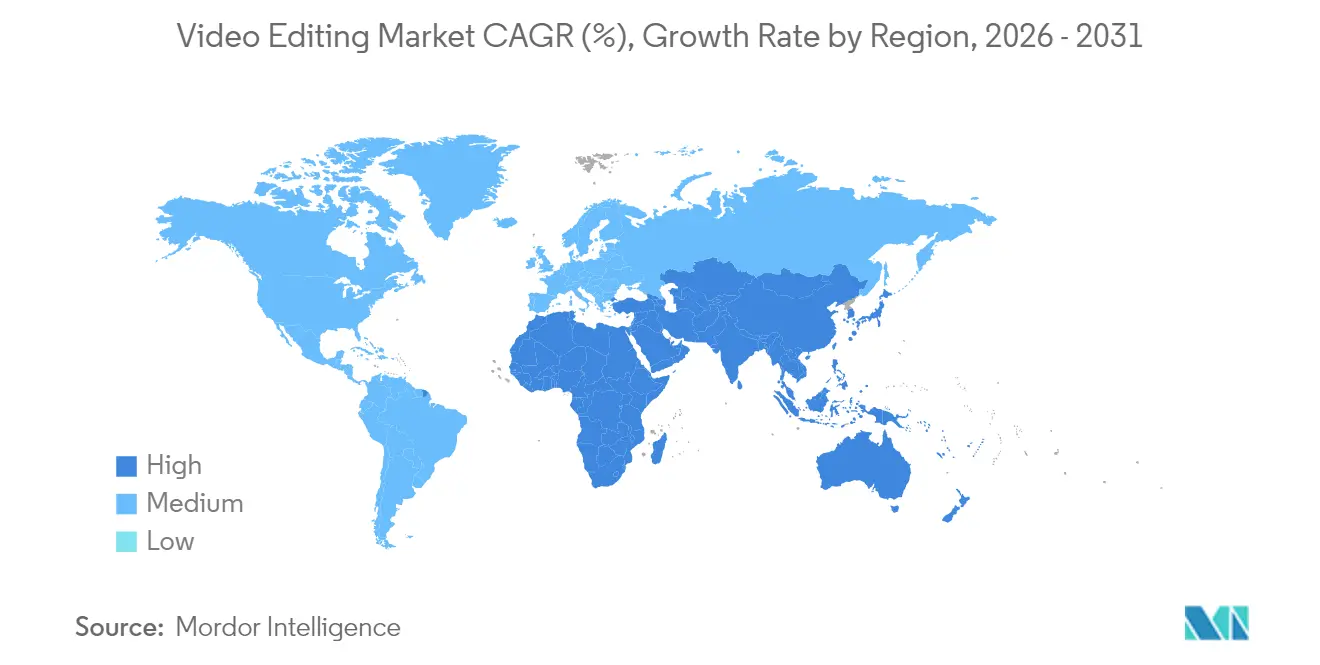

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Editing Market Analysis by Mordor Intelligence

The Video Editing Market size was valued at USD 3.54 billion in 2025 and estimated to grow from USD 3.75 billion in 2026 to reach USD 4.99 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031). Demand continues to rise as cloud deployment, AI-assisted workflows, and mobile-first creation reshape competitive priorities. Vertically integrated device makers benefit from control over silicon, while software vendors accelerate feature releases, lowering the skill threshold for polished output. Asia-Pacific’s rapid smartphone adoption fuels a regional leapfrog in mobile editing, and cloud-native collaboration compresses production timelines for over-the-top (OTT) studios. Semiconductor supply constraints amplify the advantages of firms able to optimise hardware–software integration, further differentiating user experience across the video editing market.

Key Report Takeaways

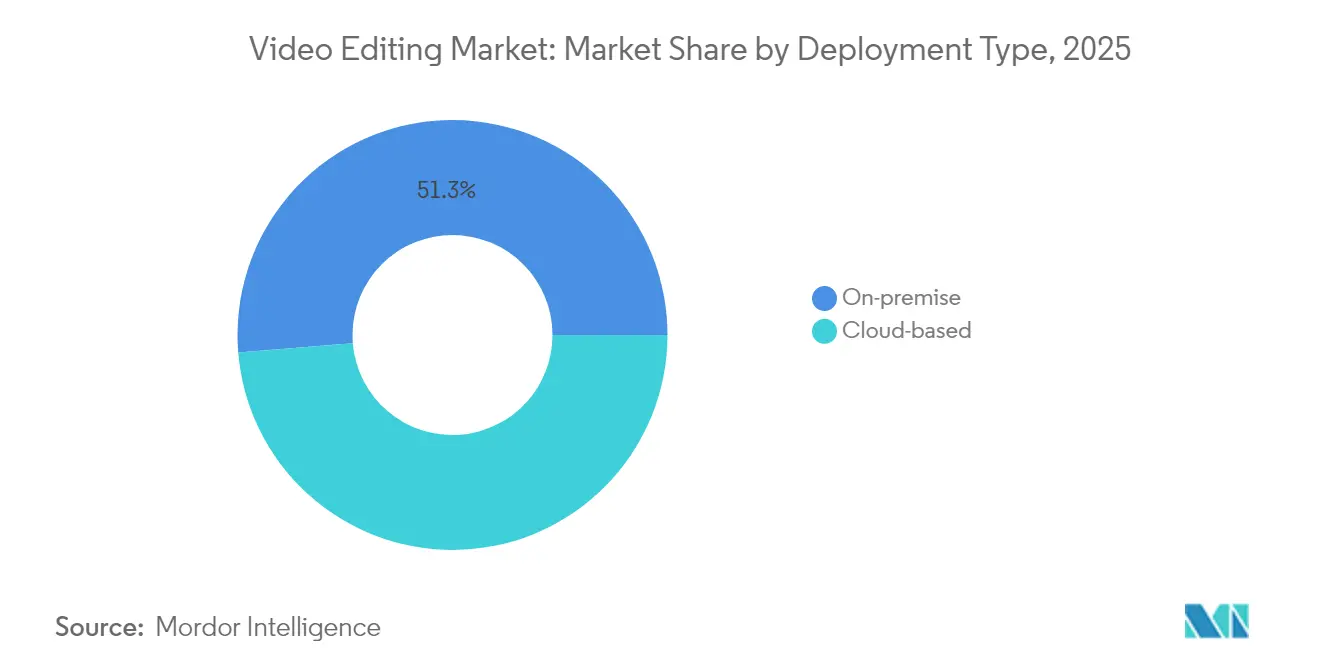

- By deployment type, on-premise solutions held 51.30% of the video editing market share in 2025, whereas cloud-based workflows are forecast to expand at a 8.23% CAGR to 2031.

- By enterprise size, large organisations commanded a 64.20% share of the video editing market size in 2025, while small and medium-sized enterprises (SMEs) are projected to grow at 7.88% annually through 2031.

- By end-use, the professional/commercial segment accounted for a 59.10% share of the video editing market size in 2025, yet personal creators are advancing at a 6.78% CAGR over the same period.

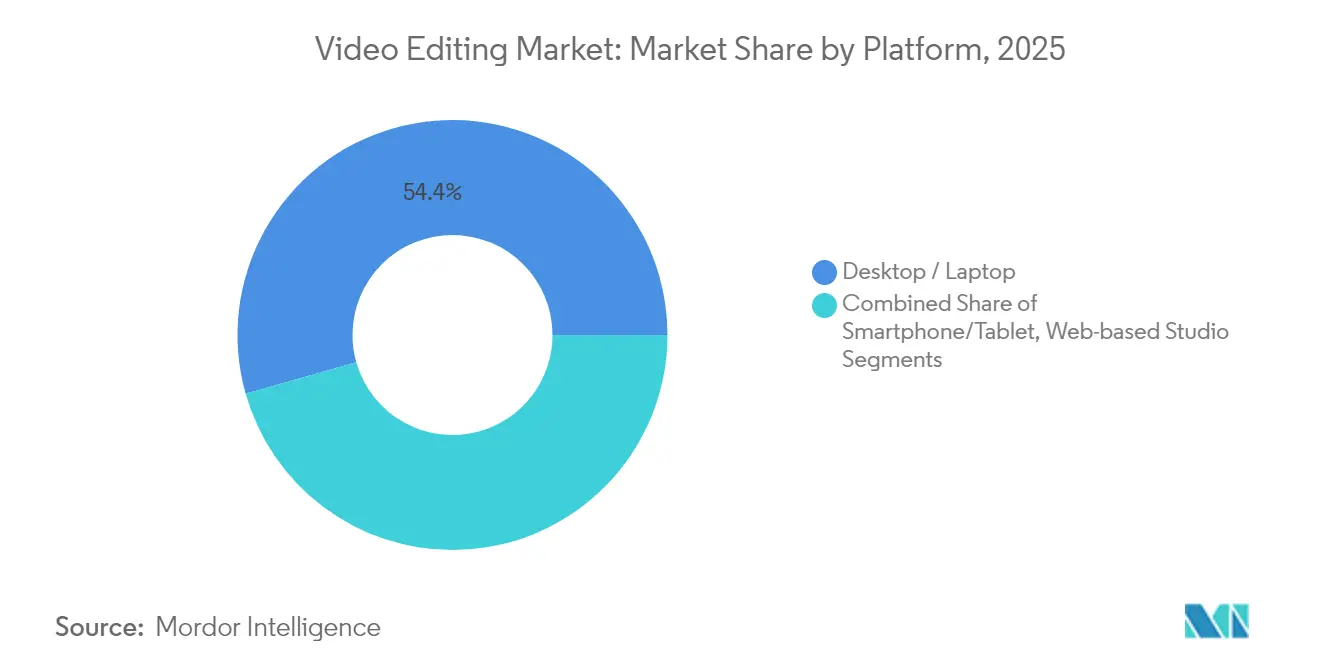

- By platform, desktop/laptop environments led with 54.40% revenue share in 2025; smartphone/tablet workflows are set to climb at 8.62% CAGR to 2031.

- By operating system, Windows captured 45.50% of the video editing market share during 2025, whereas iOS/iPadOS is poised for 8.95% annual growth to 2031.

- By region, North America held 37.60% of the video editing market in 2025, while Asia-Pacific is expected to record a 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Video Editing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Creators’ monetization surge on short-form video platforms | +1.2% | North America, Asia-Pacific | Medium term (2-4 years) |

| AI-assisted editing driving DIY adoption in APAC | +1.0% | Asia-Pacific | Medium term (2-4 years) |

| OTT studios’ shift to cloud-native post-production pipelines | +0.8% | Global, led by North America | Medium term (2-4 years) |

| Social commerce video adoption by SMB retailers | +0.7% | China, Southeast Asia, North America | Short term (≤ 2 years) |

| Government subsidies for domestic creative industries | +0.5% | South Korea, UAE, United Kingdom | Long term (≥ 4 years) |

| 8K and HDR content demand from sports broadcasting rights | +0.3% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Creators’ Monetization Surge on Short-form Video Platforms

Short-form ecosystems enable direct revenue streams that incentivise frequent uploads and tighten feedback loops between content quality and earnings potential. Platforms such as TikTok and YouTube report that 91% of companies treat video as a core marketing channel, while 88% of marketers deem it indispensable. [1]Olivia Huang, “2024年视频营销指南:如何做好海外营销视频?,” Shopify, shopify.com These economics motivate businesses to seek editors that deliver platform-specific templates, automated captioning and aspect-ratio presets, sustaining a robust pipeline of upgrades within the video editing market.

OTT Studios’ Shift to Cloud-native Post-Production Pipelines

Distributed teams favour browser-based workstations that remove location constraints and reallocate capital from servers to subscriptions. Early uptake is visible in Blackbird plc’s elevate.io, which added a paid tier and secured 100 subscribers weeks after its February 2025 launch. [3]Blackbird plc Investor Relations, “Final Results and Platform Update,” Blackbird plc, investormeetcompany.com Real-time review, version control and parallel rendering on shared cloud storage accelerate turnaround, raising expectations across the video editing market for seamless collaboration.

Social Commerce Video Adoption by SMB Retailers

Short video integrated with checkout shortens the path from discovery to purchase. Conversion-linked creation tools let resource-constrained retailers produce promotional footage that feels native to social feeds. Surveys show 82% of consumers are persuaded by branded video and 89% prefer more video content from brands. The trend underpins SME demand curves within the video editing market.

AI-assisted Editing Driving DIY Adoption in APAC

Generative AI saves professionals up to 200 hours yearly and lowers the barrier for newcomers. China’s AI-generated content sector alone is tracking toward RMB 260 billion in 2025 on a 70% CAGR, signalling strong spillover into editing workflows. Automated rough-cut creation, noise removal and subtitle generation widen creator participation and push software vendors to embed AI co-pilots as default features across the video editing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising SaaS stack fatigue among freelance editors | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Inter-operability gaps between mobile and desktop workflows | -0.6% | Global | Medium term (2-4 years) |

| Pirated software depressing paid uptake in emerging markets | -0.5% | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Data-sovereignty regulations limiting cross-border cloud rendering | -0.3% | Europe, China, Russia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising SaaS Stack Fatigue among Freelance Editors

Freelancers juggle multiple licences for motion graphics, colour grading and collaboration, inflating monthly overhead. Consolidated suites such as Adobe Express debuted packages bundling Clip Maker, Generate Video and Enhance Speech to counter subscription overload. [2]Adobe Communications Team, “Adobe Introduces New AI-Powered Video Tools in Adobe Express,” Adobe, news.adobe.com Vendors that rationalise pricing tiers stand to regain churn-risk accounts across the video editing market.

Inter-operability Gaps between Mobile and Desktop Workflows

Capture often begins on phones yet finishing touches require desktop horsepower. Review of leading apps notes persistent latency in asset synchronisation and feature parity, slowing turnaround for hybrid creators. Bridging this gap remains a priority as mobile content volumes rise within the video editing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Disrupts Traditional Models

On-premise installations retained 51.30% of the video editing market in 2025 thanks to control over hardware and security. However, cloud subscriptions are expanding at 8.23% annually, propelled by collaborative review portals and elastic rendering that suit peak-load production. Sub-second proxy streaming and AI-based compression temper bandwidth pain points, inching parity closer for high-resolution workflows.

Cloud adoption narrows the capability divide between boutique creators and major studios. OTT producers exploit browser timelines to keep global teams in sync, while SMEs appreciate pay-as-you-go hosting that converts capital spending into operational outlays. The video editing market size for cloud deployments is projected to command an extra 9.2 percentage-point share by 2031 as trust in security certifications spreads.

By Enterprise Size: SMEs Drive Innovation Adoption

Large organisations contributed 64.20% of 2025 revenue, yet their growth aligns with the 5.88% market average. In contrast, SMEs are scaling at 7.88%, reflecting how template-based editing and AI-guided storyboards unlock production without specialist staff. This acceleration highlights how the video editing market size for SMEs gains momentum through social commerce campaigns and targeted vertical video advertising.

Product-led onboarding, freemium trials and community tutorials reduce perceived complexity for first-time adopters. Vendors embedding contextual learning modules observe higher activation rates among small teams. As marketing budgets tilt toward snackable content, SMEs’ cumulative volume materially influences roadmap priorities across the video editing market.

By End-use: Personal Creators Challenge Professional Dominance

Professional or commercial users still dominate revenue with 59.10% share, but personal creators post a 6.78% CAGR as monetisation avenues proliferate. AI-powered colour matching, noise suppression and auto-captioning now appear even in entry-level tiers, eroding the historical skills gap. The resulting content parity forces agencies to differentiate via advanced compositing and real-time collaboration features within the video editing market.

Higher creator volumes attract plug-in developers who extend core apps with platform-specific export presets, interactive overlays and audience analytics. This ecosystem growth reinforces personal adoption and pushes average revenue per user upward, further expanding the video editing market.

By Platform: Mobile Challenges Desktop Dominance

Desktop workstations maintained 54.40% share in 2025 because multitier timelines and GPU-accelerated rendering remain resource-intensive. Yet smartphone and tablet editors are advancing at 8.62% CAGR as silicon improvements deliver H.265 hardware encoding and HDR playback. The video editing market size for mobile workflows benefits from touch-optimised interfaces that accelerate rough cuts during travel or on location.

Hybrid models see editors sequence clips on phones, then hand off to cloud or desktop for colour grading and spatial audio. Apple’s Final Cut Pro for iPad 2 illustrates the trajectory, combining gesture-based trimming with multicam sync in a fanless device. This evolution blurs lines between platform categories inside the video editing market.

By Operating System: iOS Gains on Windows Leadership

Windows secured 45.50% share thanks to entrenched enterprise fleets, while macOS retains loyalty among design-led agencies. iOS/iPadOS, however, is rising 8.95% each year as purpose-built tablet apps unlock high-end features. The video editing market share for Apple mobile operating systems benefits from vertical optimisation between M-series chips and Metal-accelerated codecs.

Linux powers render farms in VFX houses and open-source environments but remains niche. Android/ChromeOS serves cost-sensitive creators in emerging regions, where lightweight web studios provide an entry ramp to the broader video editing market.

Geography Analysis

North America contributed 37.60% of 2025 revenue, anchored by Hollywood studios, sports broadcasters and software giants. The ecosystem’s scale fosters rapid adoption of AI toolkits and cloud licences, yet market maturity tempers growth to mid-single digits. Tax incentives for digital media in states like Georgia continue to attract production, sustaining a deep customer base for the video editing market.

Asia-Pacific is the fastest-growing region at a 7.22% CAGR, driven by smartphone penetration and government support for creative industries. Korea’s 15% tax credit for small producers and China’s thriving short-video economy funnel additional creators into paid editing tiers. India records high app download volumes as vernacular content gains traction. Collectively, these drivers elevate Asia-Pacific’s strategic weight inside the video editing market size trajectory.

Europe benefits from rich cultural output and supportive policies such as the United Kingdom’s 39% Audio-Visual Expenditure Credit, stimulating spend on visual-effects heavy projects. Data-sovereignty statutes, however, compel vendors to establish in-region hosting, elongating procurement cycles. Latin America and the Middle East and Africa add incremental growth through rising internet access and film-commission rebates like Abu Dhabi’s 35% cashback, broadening geographic diversity across the video editing market.

Competitive Landscape

Industry concentration remains moderate. Adobe leads with Creative Cloud’s integrated suite, continuously infusing Sensei AI to refine automated edits and speech enhancement. Apple leverages chip-to-software control for hardware-accelerated timelines that rival desktop rigs, giving the firm defensible advantages in the video editing market. Blackbird plc differentiates via codec efficiencies optimised for low-bandwidth collaboration, while Wondershare Filmora targets cost-conscious prosumers with AI co-pilot features.

Strategic moves include:

- Adobe’s April 2025 rollout of Clip Maker and Generate Video, bundling multiple functions into a single license to address SaaS fatigue.

- Blackbird’s March 2025 launch of a paid elevate.io tier, validating willingness to pay for browser-based editing.

- Apple’s February 2025 release of Final Cut Pro for iPad 2, extending professional toolkits into mobile devices.

Consolidation is likely as incumbents acquire niche AI startups to fast-track research, while specialised vendors explore alliances to integrate cross-platform synchronisation. Market barriers now revolve less around codec support and more around machine-learning pipelines, steering R&D budgets throughout the video editing market.

Video Editing Industry Leaders

Adobe Inc.

Apple Inc.

Blackmagic Design Pty Ltd

Avid Technology Inc.

Corel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Adobe introduced AI-powered video functions in Adobe Express, including Clip Maker, Generate Video and Enhance Speech.

- March 2025: Blackbird plc unveiled the Creator tier for elevate.io, adding 100 paid subscribers within weeks.

- February 2025: Apple released Final Cut Pro for iPad 2, integrating multicam recording and refined touch controls.

- January 2025: The Abu Dhabi Film Commission raised its cashback rebate to 35%, prompting equipment suppliers to expand regional inventories.

Global Video Editing Market Report Scope

Video editing software is a program or application designed to manipulate and modify video files. This enables users to create, edit, and produce professional-quality video content. The software offers tools for cutting, splicing, merging, enhancing, and applying effects to video footage. These capabilities make it suitable for diverse purposes, including filmmaking, social media content creation, marketing, entertainment, and educational materials.

The study tracks the revenue accrued through the sale of the video editing software by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The video editing market is segmented deployment type (on-premise, and cloud-based), end use (personal, and professional), geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| On-premise |

| Cloud-based |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Personal |

| Professional / Commercial |

| Desktop / Laptop |

| Smartphone / Tablet |

| Web-based Studio |

| Windows |

| macOS |

| Linux |

| iOS / iPadOS |

| Android / ChromeOS |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Deployment Type | On-premise | |

| Cloud-based | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End-use | Personal | |

| Professional / Commercial | ||

| By Platform | Desktop / Laptop | |

| Smartphone / Tablet | ||

| Web-based Studio | ||

| By Operating System | Windows | |

| macOS | ||

| Linux | ||

| iOS / iPadOS | ||

| Android / ChromeOS | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global video editing market?

The video editing market generated USD 3.75 billion in 2026 and is forecast to grow to USD 4.99 billion by 2031.

Which region is growing fastest in the video editing market?

Asia-Pacific is projected to lead growth with a 7.22% CAGR through 2031, supported by smartphone proliferation and supportive government incentives.

How quickly are cloud-based editing deployments expanding?

Cloud workflows are expected to post an 8.23% CAGR between 2026 and 2031, outpacing on-premise setups due to collaboration and scalability advantages.

Why are SMEs important to future demand?

SMEs are adopting video at an 7.88% annual rate, using AI-guided tools to produce professional-quality content without large in-house teams.

What role does AI play in redefining editing workflows?

AI accelerates tasks such as clipping, colour matching and audio enhancement, saving professionals around 200 hours per year and enabling newcomers to create polished output.

How concentrated is vendor control in the video editing market?

The top five companies hold about 60% of revenue, yielding a concentration score of 6 and leaving room for niche and mobile-first innovators.

Page last updated on: