Media Streaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

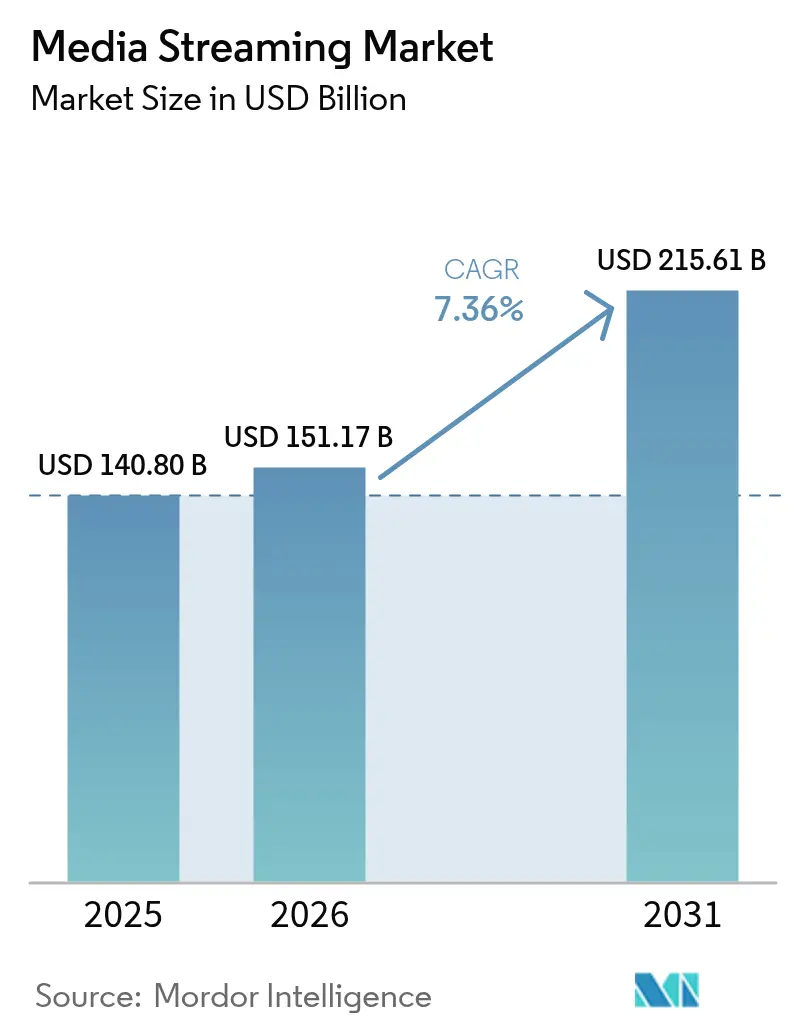

| Market Size (2026) | USD 151.17 Billion |

| Market Size (2031) | USD 215.61 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

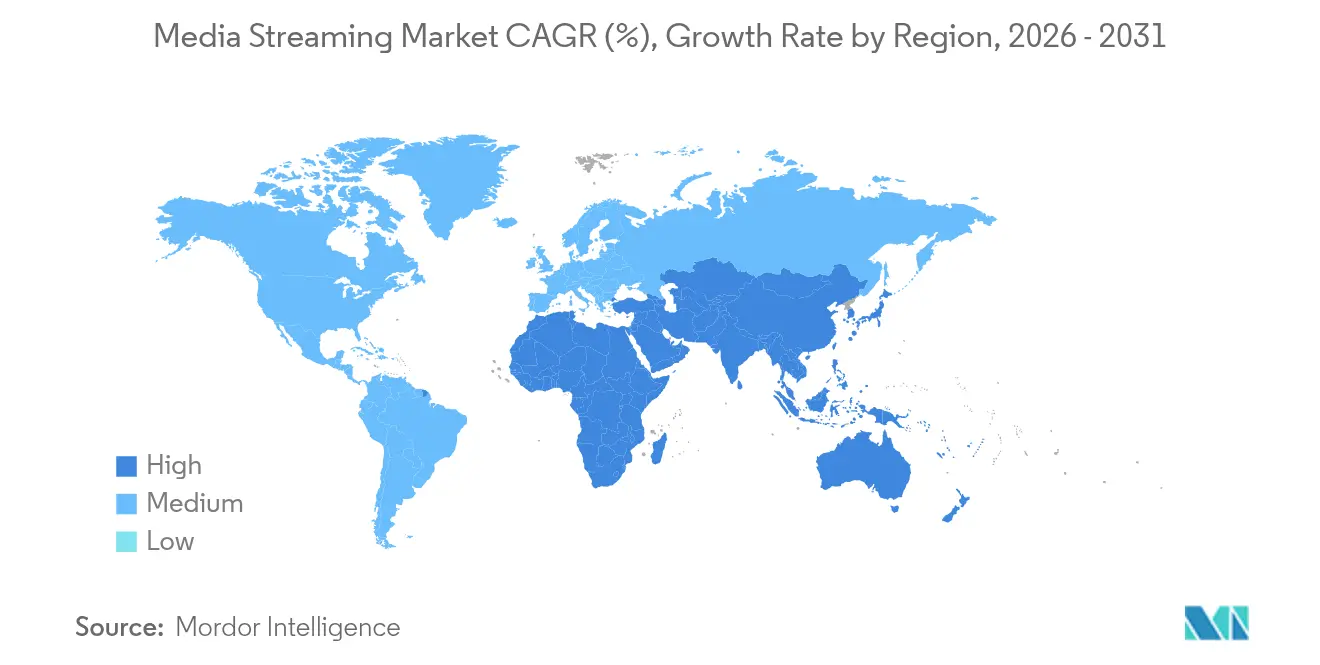

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

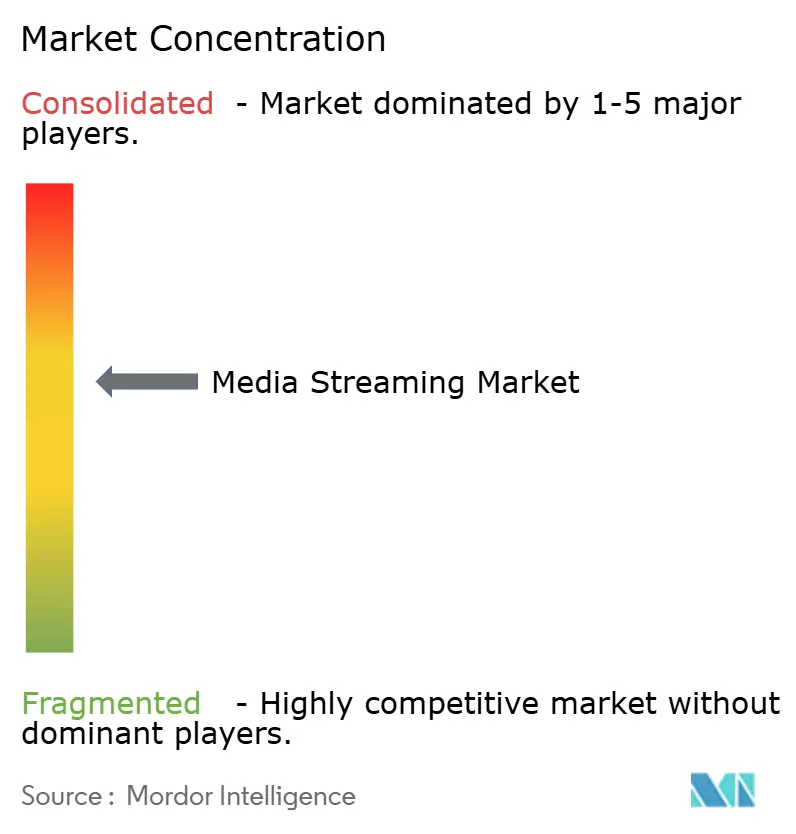

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Media Streaming Market Analysis by Mordor Intelligence

The media streaming market size was valued at USD 140.80 billion in 2025 and estimated to grow from USD 151.17 billion in 2026 to reach USD 215.61 billion by 2031, at a CAGR of 7.36% during the forecast period (2026-2031). This strong outlook rests on a decisive pivot from subscription-only propositions toward hybrid monetization that combines paid tiers with advertising inventory, enabling platforms to offset rising customer-acquisition costs and improve profitability. Competitive differentiation increasingly stems from control of advertising technology stacks, real-time recommendation engines, and exclusive content rights that secure premium pricing. Network upgrades—in particular 5G rollouts—support higher-bitrate delivery, while edge compute adoption cuts latency, allowing 4K and 8K streams to reach mobile users without buffering. Sports rights fragmentation drives event-led subscriber spikes and higher CPMs, whereas localized content libraries draw new viewers in under-penetrated rural markets. At the same time, margin pressure from USD 18 billion annual content budgets forces operators to balance original production with catalog sharing pacts, accelerating a sector-wide shift toward revenue-per-user optimization.

Key Report Takeaways

- By content type, video streaming led with 77.35% revenue share in 2025; music streaming is projected to expand at an 8.82% CAGR to 2031.

- By service type, on-demand viewing accounted for 86.76% of the media streaming market share in 2025, while live streaming is advancing at a 9.44% CAGR through 2031.

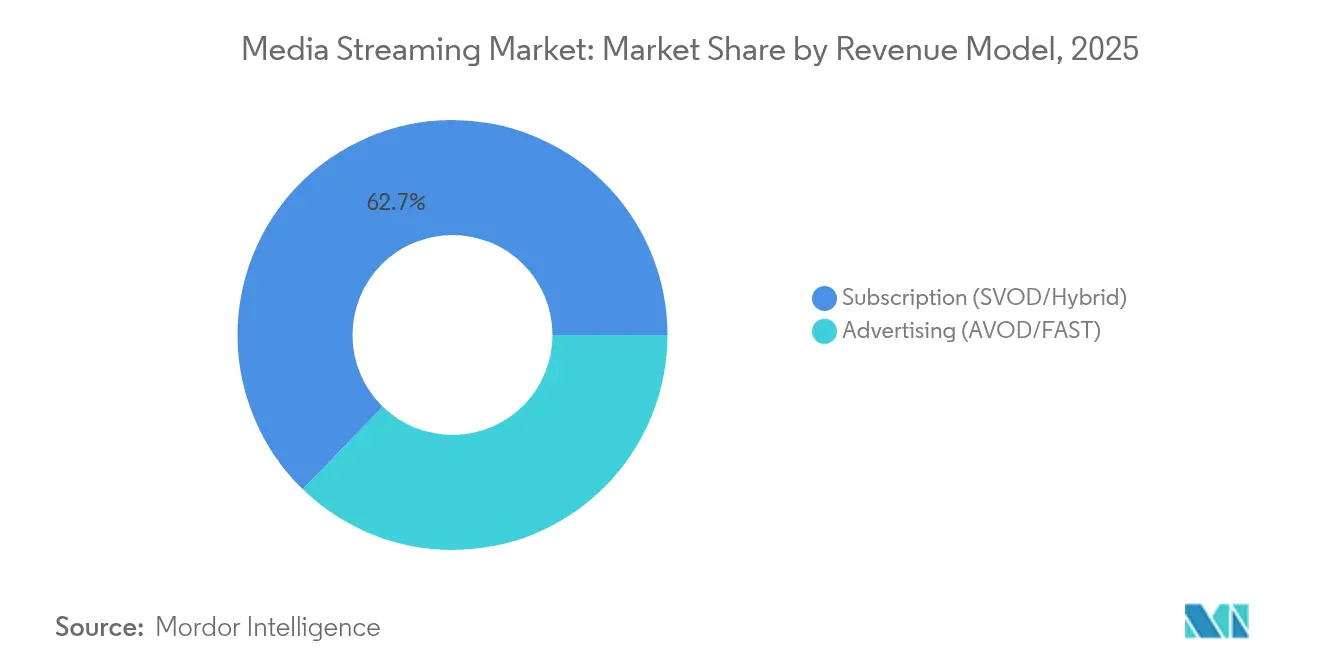

- By revenue model, subscription plans commanded 62.74% share of the media streaming market size in 2025; advertising-supported tiers are forecast to post an 8.39% CAGR to 2031.

- By geography, North America contributed 34.48% of revenue in 2025, whereas Asia-Pacific is set to grow fastest at a 8.97% CAGR to 2031.

- By streaming quality, HD retained 55.05% share of the media streaming market size in 2025; 8K viewing is accelerating at an 17.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Media Streaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of low-cost 5G data plans | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| SVOD expansion into tier-II/III cities | +0.8% | North America and EU | Short term (≤ 2 years) |

| Exclusive sports-rights wars | +1.5% | Global | Long term (≥ 4 years) |

| Cloud-native CDN and edge compute adoption | +0.9% | Global | Medium term (2-4 years) |

| Rise of FAST channels | +1.1% | North America core, expanding to APAC | Short term (≤ 2 years) |

| Telco-media bundling | +0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Low-Cost 5G Data Plans Across Asia-Pacific

Deployment of affordable 5G networks has reshaped consumption patterns by supporting uninterrupted HD and 4K streams on mobile connections. Operators subsidize data packages because elevated video traffic monetizes premium network investments, creating a feedback loop that spurs both infrastructure build-out and content engagement. Edge nodes positioned close to viewers further trim latency, enabling personalized recommendations to refresh in real time. The result is sustained growth for the media streaming market in price-sensitive emerging economies.

SVOD Platform Expansion into Tier-II/III Cities in North America and Europe

Having saturated major metropolitan areas, leading services are targeting secondary cities where fiber rollout and improved rural broadband have lowered delivery cost. Localized production budgets are modest relative to global tent-pole titles, yet culturally tailored series drive higher loyalty among underserved audiences. Sophisticated recommendation algorithms that account for regional dialects and viewing times maintain engagement without raising content outlays, adding incremental revenue to the media streaming market.

Exclusive Sports-Rights Wars Driving Premium Pricing

Exclusive control of marquee tournaments underpins premium subscription tiers and attracts lucrative advertising slots. Netflix’s acquisition of FIFA Women’s World Cup rights demonstrates how event programming can offset seasonal churn and elevate average revenue per user. Live sports command higher CPMs than library titles, allowing platforms to recoup rights fees via both ads and higher priced plans. As traditional broadcasters lose exclusivity, streaming operators wield greater negotiation leverage with advertisers and leagues.

Integration of Cloud-Native CDN and Edge Compute for Ultra-Low-Latency Live Streams

Operators such as Comcast deploy edge compute clusters that halve latency versus legacy CDNs, ensuring synchronized playback during high-traffic events. Cloud-native architectures scale automatically, containing bandwidth spend while preserving quality. Enhanced reliability differentiates service offerings and sustains growth across the media streaming market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating content-licensing costs | -1.8% | Global | Short term (≤ 2 years) |

| Fragmented rights management | -0.9% | Global | Medium term (2-4 years) |

| Persistent last-mile latency in emerging markets | -1.2% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Heightened regulatory scrutiny on data privacy and localization | -0.7% | EU, APAC core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Content-Licensing Costs Compressing Margins

Netflix’s USD 18 billion outlay in 2025 underscores an inflationary spiral that squeezes profitability even for scale leaders. Fierce bidding for premium libraries diminishes differentiation because rival services can only pass a portion of costs to subscribers. Sharing agreements reduce immediate cash burn but blunt exclusivity advantages that underpin subscriber acquisition, challenging overall economics of the media streaming market.

Heightened Regulatory Scrutiny on Data Privacy and Localization

Jurisdictions imposing data-storage mandates compel platforms to duplicate infrastructure and restrict global recommender systems, inflating compliance budgets. Fragmented data silos degrade personalization accuracy, potentially lowering engagement metrics. Smaller entrants face disproportionate burdens, curbing competitive diversity within the media streaming market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Video Dominance Faces Music Streaming Disruption

Video maintained a commanding 77.35% revenue slice in 2025, reflecting entrenched viewing habits and heavy investment in exclusive series that anchor user retention. Music services, however, are expanding at an 8.82% CAGR aided by compact file sizes that stream reliably on constrained networks. The media streaming market size for audio is swelling as AI-driven playlists raise daily listening frequency and enlarge ad inventory.

Lower production costs and borderless appeal allow music platforms to monetize global audiences rapidly, while video players shoulder rising budgets for long-form content. This cost asymmetry encourages cross-format bundling, signalling a future where audio and video propositions converge within a single app to protect market share.

By Service Type: Live Streaming Monetization Accelerates

On-demand libraries accounted for 86.76% of 2025 revenue, yet live streaming’s 9.44% CAGR illustrates growing appetite for real-time experiences. Sporting fixtures and tent-pole reality shows create appointment viewing that advertisers value, lifting revenue per stream above on-demand averages.

Technical complexity strengthens competitive moats: edge compute and custom protocols manage traffic spikes, ensuring latency below the two-second psychological threshold. Platforms mastering these capabilities are positioned to capture incremental media streaming market share during peak global events.

By Revenue Model: Advertising Growth Reshapes Economics

Subscription plans retained 62.74% share in 2025 as consumers continued to favour ad-free environments, yet ad-supported tiers are rising at an 8.39% CAGR, supported by Netflix’s report that more than 55% of new sign-ups now choose the lower-priced, ad-bearing tier. FAST channels add scale by recycling existing libraries into linear-style feeds, fueling a 42% two-year jump in global channel.

Advanced targeting delivers higher CPMs, allowing platforms to subsidize content costs. Sustained advertiser migration from linear television strengthens the media streaming market’s grip on brand budgets, but success depends on balancing ad load against viewer tolerance.

By Streaming Quality: 8K Adoption Accelerates Infrastructure Investment

HD streams held 55.05% of 2025 usage thanks to favorable bandwidth-to-quality compromise. Nonetheless, 8K content is forecast to rise at an 17.7% CAGR on the back of codec breakthroughs that cut bitrates by 40% . Intel’s 8K Olympic broadcast proved technical viability, catalyzing device makers to integrate compatible chipsets.

Edge compute nodes cache ultra-high-definition assets nearer to viewers, easing backbone congestion. Platforms delivering seamless 8K experiences during marquee sports will command price premiums, bolstering long-term growth for the media streaming market.

Geography Analysis

North America generated 34.48% of 2025 revenue but is maturing, prompting operators to pivot from user acquisition toward higher lifetime value. Bundling with fiber and mobile contracts, as demonstrated by Verizon’s convergence strategy, locks in households and widens ARPU without heavy marketing spend. Sports-rights competition inflates programming costs, yet the presence of established ad markets sustains hybrid-tier profitability.

Asia-Pacific is projected to expand at a 8.97% CAGR, buoyed by governmental encouragement of local content creation and accelerating 5G coverage. Netflix recorded a 20% regional viewing surge after debuting culturally tailored originals, confirming that local narratives unlock outsized engagement. Governments are offering creator funds—India’s USD 1 billion initiative is emblematic—that feed fresh catalogs and stimulate the media streaming market. Nonetheless, diverse data-localization rules compel parallel infrastructure builds, raising entry barriers for smaller brands. Europe shows uneven growth as GDPR compliance and fragmented language markets inflate operational overheads. Carriage agreements such as Netflix’s tie-up with TF1 illustrate a hybrid model where streaming and traditional broadcasters collaborate to satisfy regulators and audiences. Latin America’s fiber penetration—77.2% in Brazil and 70.9% in Chile—has started translating into higher-resolution streaming uptake, creating fresh addressable revenue. Africa remains mobile-first; low-bandwidth optimizations and downloadable content options are crucial to unlock latent demand.

Competitive Landscape

The media streaming market hosts a moderately concentrated field where the top five players control a significant share yet face vigorous competition from regional specialists. Netflix, Disney, and Amazon leverage global distribution footprints and in-house production pipelines to secure premium talent, while local champions focus on linguistic and cultural niches. Investment priority has shifted to advertising technology; Netflix’s April 2025 rollout of an in-house ad platform illustrates the pivot toward monetization depth over subscriber breadth.

Technology is a decisive battleground. Edge compute deployments by Comcast and similar operators foster exclusive quality guarantees that smaller rivals struggle to replicate.[1]Comcast via Qwilt, “Edge Compute Deployment,” qwilt.com Patent filings reveal ongoing work on AI-driven content adaptation that auto-adjusts encoding profiles scene by scene, reducing bitrates without noticeable quality loss and saving millions in delivery fees.[2]Stephen Follows, “What Netflix’s Patents Reveal,” stephenfollows.com Strategic moves underline intensified jockeying: Disney’s 70% purchase of Fubo TV merges live sports strength with a vast on-demand library, while Roku’s acquisition of Frndly TV extends its family-oriented channel bundle.[3]Streaming Media, “H.267: A Codec for Future,” streamingmedia.com

White-space opportunities persist in interactive formats and creator-economy partnerships that shorten time-to-market for niche stories. The entrance of social media giants into longer-form video could squeeze traditional players unless they leverage existing subscriber bases to test new formats quickly. Consolidation remains likely as rising content and compliance costs favor scale, meaning that the media streaming market may trend toward a higher concentration ratio over the next five years.

Media Streaming Industry Leaders

Spotify Technology S.A.

Apple Inc.

Amazon Prime (Amazon.com Inc.)

Tencent Holdings Limited

AT&T Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Netflix strikes a carriage arrangement with TF1 that will add five linear channels and 30,000 on-demand hours to French subscribers in July 2026

- June 2025: Amazon Ads and Roku announce a partnership granting brands access to 80% of connected-TV households, integrating measurement across both platforms

- May 2025: Roku acquires Frndly TV for USD 185 million, adding 50+ live channels to its line-up and expanding lower-priced subscription options

- April 2025: Netflix reports Q1 revenue of USD 10.54 billion and unveils its proprietary ad-tech stack that enhances targeting for its growing ad tier

Global Media Streaming Market Report Scope

Media streaming refers to any media content, live or recorded, to be delivered to computers, mobile, and other devices via the internet, and played back in real-time. Podcasts, webcasts, movies, TV shows, and music videos are common forms of streaming content.

The media streaming market is segmented by content type (music Streaming, video streaming), revenue model (advertising, subscription), streaming platform (smartphone & tablet, laptop, and desktop, smart TV, gaming console), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa).

The market sizes and forecasts are provided in terms of value USD for all the above segments.

| Video Streaming |

| Music Streaming |

| Live Streaming |

| On-Demand Streaming |

| Subscription (SVOD/AVOD/Hybrid) |

| Advertising (AVOD/FAST) |

| SD |

| HD |

| 4K / UHD |

| 8K |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Mexico | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East and Africa | |

| Africa | South Africa |

| Rest of Africa |

| By Content Type | Video Streaming | |

| Music Streaming | ||

| By Service Type | Live Streaming | |

| On-Demand Streaming | ||

| By Revenue Model | Subscription (SVOD/AVOD/Hybrid) | |

| Advertising (AVOD/FAST) | ||

| By Streaming Quality | SD | |

| HD | ||

| 4K / UHD | ||

| 8K | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the media streaming market?

The media streaming market generated USD 151.17 billion in 2026 and is projected to reach USD 215.61 billion by 2031.

Which content type dominates revenue?

Video streaming led with 77.35% of revenue in 2025, though music streaming is growing fastest at an 8.82% CAGR.

How quickly is live streaming growing?

Live streaming revenue is forecast to expand at a 9.44% CAGR through 2031, driven mainly by exclusive sports coverage and event-based viewing.

What region will contribute the fastest growth?

Asia-Pacific is poised for the highest regional CAGR at 8.97% thanks to 5G rollouts and local content production scaling.

Why are advertising-supported tiers gaining traction?

Ad-supported plans address price-sensitive viewers and deliver higher CPMs for platforms; over half of Netflix’s new 2026 subscribers selected an ad tier.

How important is 8K streaming to future growth?

Although HD still prevails, 8K streams are expected to rise at an 17.7% CAGR as advanced codecs reduce data loads and edge compute infrastructure matures.

Page last updated on: