Digital Publishing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

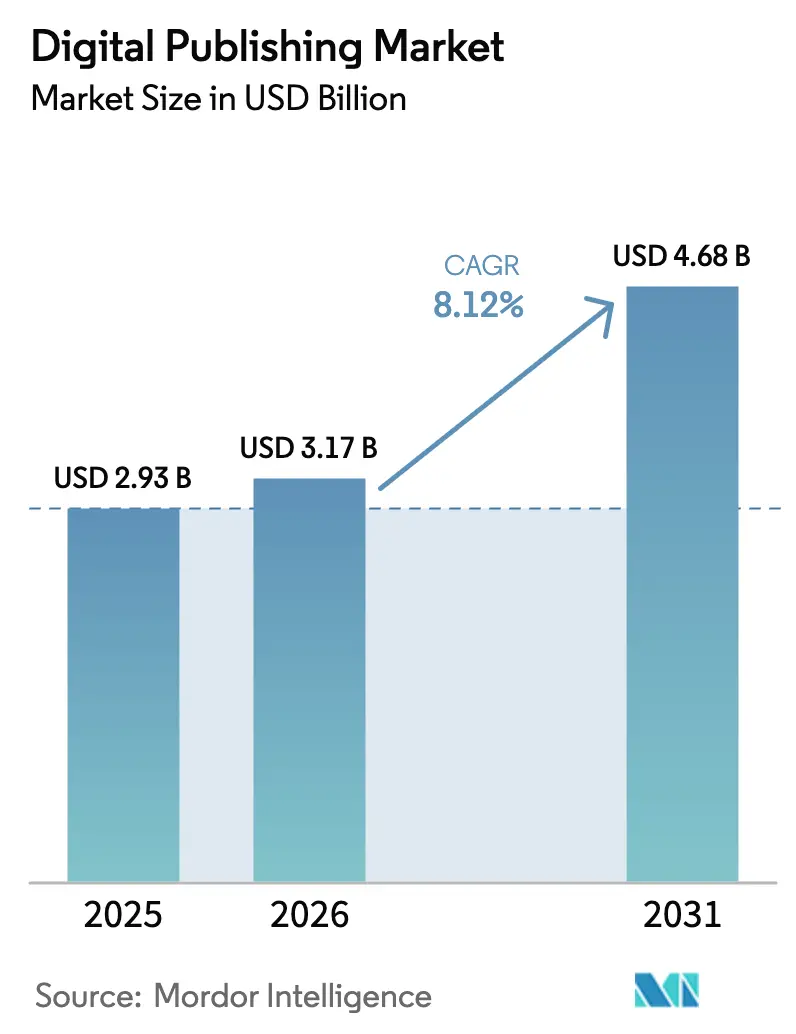

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 4.68 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

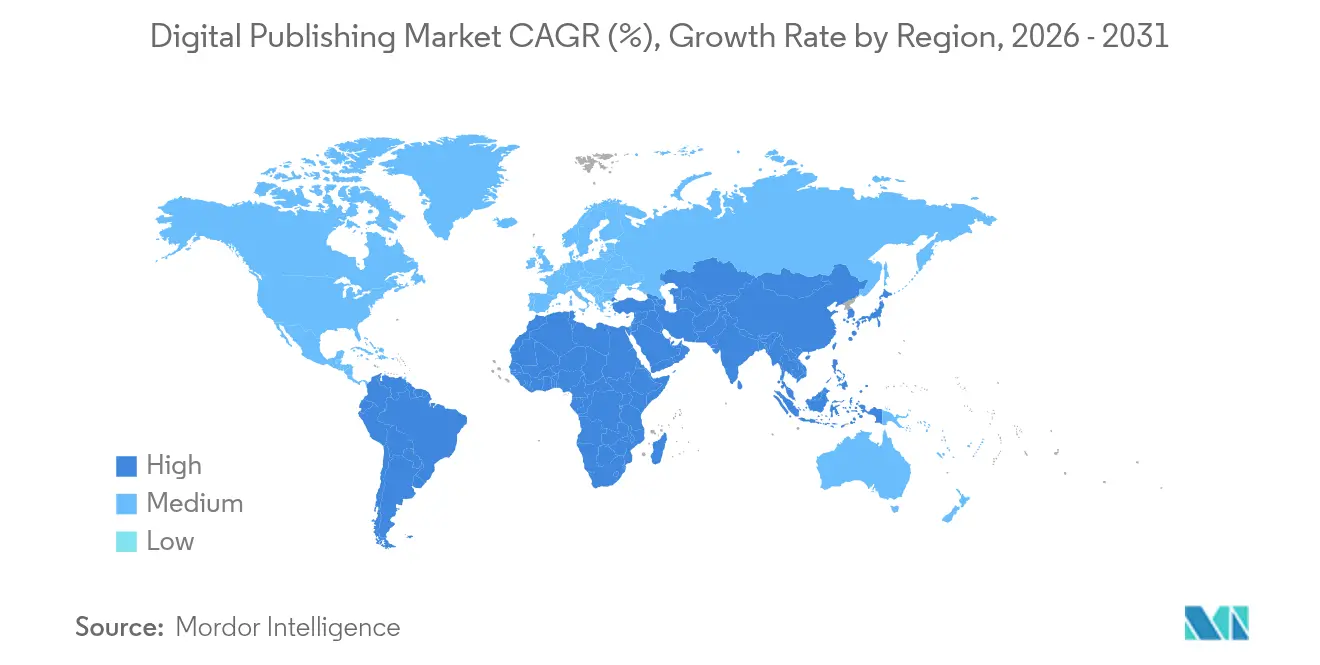

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

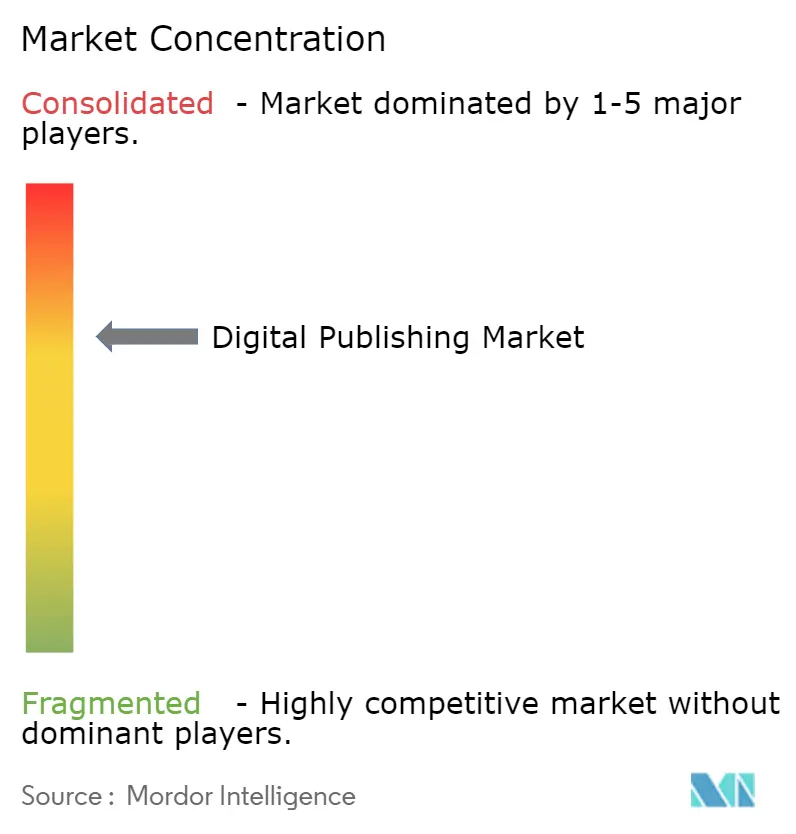

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Publishing Market Analysis by Mordor Intelligence

The digital publishing market size was valued at USD 2.93 billion in 2025 and estimated to grow from USD 3.17 billion in 2026 to reach USD 4.68 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). Steady migration from print to screen, rapid smartphone uptake and improving network quality keep expanding the digital publishing market across mature and emerging economies. AI-enabled content personalization, cloud-native production workflows and the rise of direct-to-consumer monetization are making digital formats more attractive for both creators and audiences. Platforms that bundle creation, curation and monetization tools now anchor most enterprise strategies, while programmatic advertising and hybrid revenue models widen the addressable customer base. Competition is heating up as tech incumbents, specialist SaaS vendors and AI-first start-ups race to capture new slices of the digital publishing market.

Key Report Takeaways

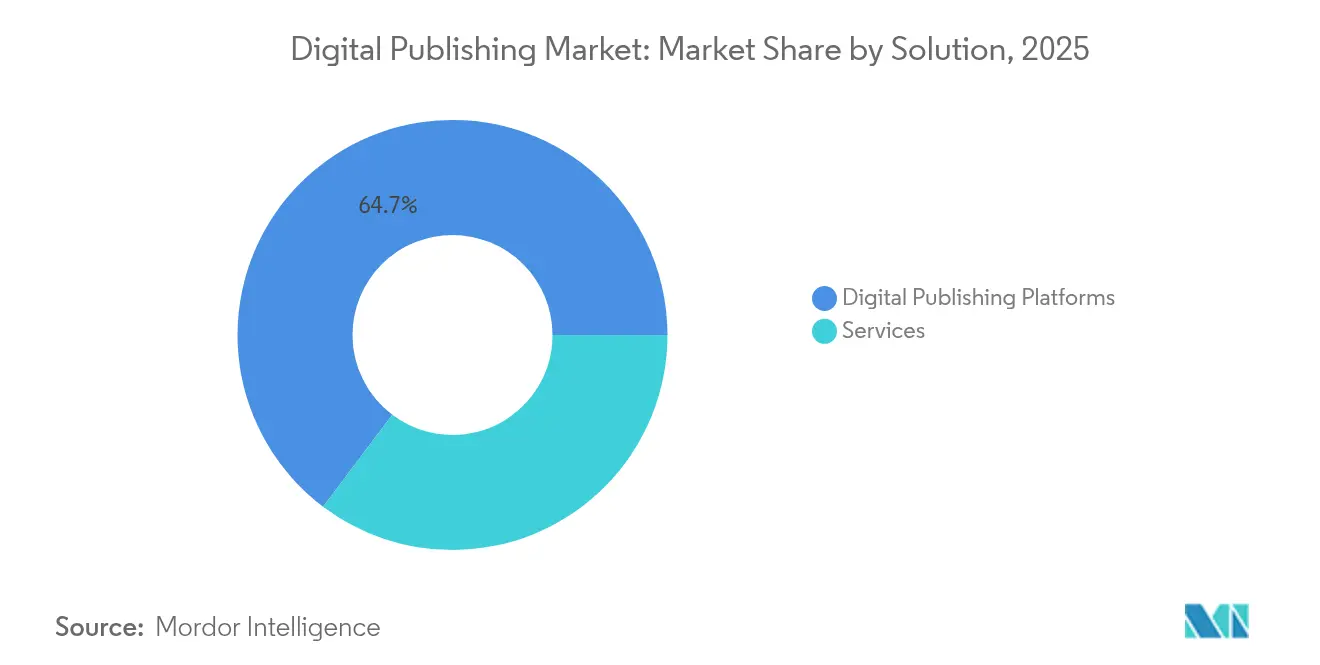

- By solution, digital publishing platforms led with 64.72% share of the digital publishing market size in 2025; while services are projected to grow at a 9.02% CAGR to 2031.

- By content type, e-books captured 41.05% of the digital publishing market share in 2025, and blogs and web-native content are advancing at an 11.12% CAGR.

- By revenue model, subscriptions commanded 53.85% share of the digital publishing market size in 2025; advertising-supported models show the fastest 10.35% CAGR through 2031.

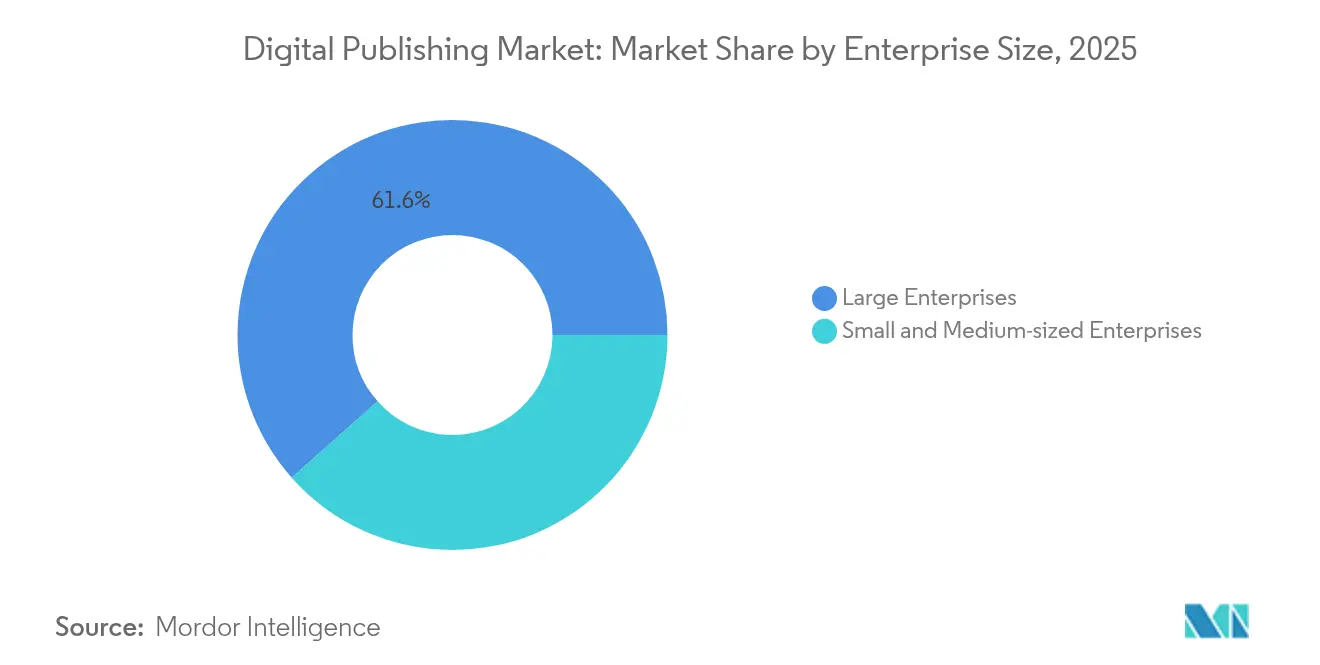

- By enterprise size, large enterprises held 61.55% share of the digital publishing market size in 2025; whereas SMEs are expanding at a 9.62% CAGR.

- By end-user industry, media and entertainment dominated with 33.35% share of the digital publishing market size in 2025, and education is forecast to post a 11.85% CAGR.

- By geography, North America accounted for 36.12% share of the digital publishing market size in 2025; Asia-Pacific is the fastest-growing region at a 10.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Publishing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Penetration of low-cost smartphones | +1.2% | Southeast Asia, India, developing Asia-Pacific | Medium term (2-4 years) |

| Shift of universities to e-textbooks | +1.8% | North America, Europe | Short term (≤ 2 years) |

| Direct-to-consumer monetization surge | +1.5% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| AI-enabled dynamic personalization | +2.1% | Global, led by North America and developed Asia-Pacific | Short term (≤ 2 years) |

| Pivot to measurable programmatic channels | +1.3% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Cloud-native publishing workflows | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Penetration of low-cost smartphones driving mobile reading adoption in Southeast Asia

Smartphone ownership now exceeds 85% in Indonesia, and 83% of respondents prefer reading on phones, a percentage far above regional peers.[1]Rakuten Insight Survey, “Indonesian Reading Preferences,” Databoks, databoks.id Cheaper devices, falling data costs and faster 5G rollouts-subscriptions could top 620 million by 2028-create fertile ground for mobile-first publishing.[2]“5G in South East Asia and Oceania: A closer look,” Ericsson Mobility Report, ericsson.com Publishers are tailoring font, layout and interactive elements specifically for small screens, prompting a structural shift in content design. Educational and self-help titles already account for one-third of mobile reads, signalling utility-driven demand. As telcos bundle e-reading perks, the digital publishing market gains new audiences without heavy acquisition spend.

Shift of academic institutions to e-textbooks under digital-campus initiatives

More than 70,000 students across 1,000+ universities now use AI-powered textbooks that update in real time.[3]Emma Hinchliffe, “70,000 students are already using AI textbooks,” Fortune, fortune.com In the United States, 78% of faculty already require digital materials for their largest courses, yet 41% still see print as more effective, revealing a pedagogical lag. Regulatory reviews of “inclusive access” billing may reshape growth trajectories, but heavy UK and EU spending on digital education infrastructure will likely sustain demand. Publishers that can integrate annotation, analytics and accessibility features inside a single platform stand to capture incremental institutional budgets.

Surge in direct-to-consumer monetization by independent authors via self-publishing platforms

Substack crossed 3 million paid subscribers in 2024 with a low 10% commission model, proving that individual writers can build viable businesses at scale. AI-native vendor Spines slashes production timelines to under three weeks and targets 8,000 titles in 2025 after securing USD 16 million in Series A funding.[4]Omer Kabir, “Spines raises $16 million Series A,” Calcalist, calcalistech.com New licensing ventures such as “Created by Humans” let authors sell content rights for AI training, creating supplementary revenue channels. These developments lower market entry barriers and fuel a swelling long-tail creator economy that further broadens the digital publishing market.

AI-enabled dynamic content personalization boosting user engagement metrics

Time Magazine’s AI toolbar now lets readers interact with marquee stories through multilingual voice chat, boosting average session duration. The Telegraph integrates automated narration and translation, widening addressable audiences without extra editorial headcount. Google Labs is piloting AI-generated summaries that adapt to reading pace, hinting at fully personalized article structures. Responsible-AI frameworks developed by JP/Politikens Media Group demonstrate that transparency and editorial oversight remain critical to trust. Collectively, these advances raise engagement, subscription conversion and ad-yield metrics, reinforcing AI as the core competitive battleground inside the digital publishing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating digital subscription fatigue | -1.4% | North America, Europe, developed Asia-Pacific | Short term (≤ 2 years) |

| Heightened data-privacy compliance costs | -0.8% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Persistent e-book price wars | -0.6% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Region-specific internet infrastructure gaps | -0.4% | Sub-Saharan Africa, rural areas in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating digital subscription fatigue limiting ARPU growth

Growth in paid readership slowed sharply in 2024, driving publishers to prioritize churn control over new sign-ups. Music streaming offers a cautionary parallel: U.S. subscriber counts stagnated last year except for Spotify and Apple Music, indicating possible saturation. For news outlets, only 23% of visitors even see a paywall offer. Diversified bundles such as The New York Times’ multi-product package are emerging to lift ARPU without large price hikes. A rebound in digital ad revenue is also helping offset slower subscription climbs, but fatigue remains a pronounced drag on the digital publishing market.

Heightened scrutiny from data-privacy regulations increasing compliance costs

Businesses spent USD 648,000 per million identities to process data-subject requests in 2022, up 72% year over year. Deletion requests alone cost more than USD 400,000 per million identities, creating a sizable expense line for publishers that rely heavily on audience data. With California accounting for over 10% of global requests, U.S. operators feel the pinch even before additional state laws take effect. Higher compliance spend diverts capital from content investment and may constrain algorithmic personalization if user-level data becomes harder to access. The net result is slower margin expansion inside the digital publishing market, especially for data-intensive segments such as targeted advertising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Platforms Drive Digital Transformation

Digital publishing platforms generated 64.72% of 2025 revenue, underscoring their role as the strategic core of enterprise content operations. Adobe’s March 2025 upgrade to GenStudio added workflow optimization agents that automate asset creation, signaling how platform vendors now embed AI throughout the supply chain. The digital publishing market continues to reward vendors that bundle creation, storage, distribution and analytics in a single layer, enabling publishers to launch, test and refine products rapidly.

Services, while capturing a smaller slice, are forecast to post a 9.02% CAGR as legacy publishers seek migration support, content optimization and AI integration expertise. Lee Enterprises’ cloud partnership with AWS illustrates how traditional news groups outsource infrastructure modernization to accelerate innovation. As AI complexity rises, consultative work around prompt engineering, model fine-tuning and compliance should keep the services lane buoyant, even as platform adoption matures in developed markets.

By Content Type: E-Books Retain the Crown

E-books preserved a 41.05% foothold thanks to continual device innovation: Amazon’s first color Kindle and AI-enhanced Scribe refresh reinvigorated consumer interest. Hardware suppliers such as E Ink and Netronix, recording double-digit revenue jumps in 2025, are expanding into foldable and large-format readers, enabling richer layouts.

Blogs and other web-native formats, growing at an 11.12% CAGR, benefit from newsletter economics that compress discovery, distribution and payment into a single channel. TikTok owner ByteDance even ventured from digital to print with 8th Note Press, proving that platform reach can spin off multi-format franchises. Multimedia embeds, interactive infographics and voice narration turn articles into experiences that deepen engagement and upsell potential, adding fresh momentum to the digital publishing market.

By Revenue Model: Subscription Plus Advertising Wins

Subscriptions retained 53.85% of 2025 revenue. Apple’s shift to direct ad sales on News, granting publishers 70% of platform-sold inventory and 100% of self-sold campaigns, illustrates how subscription hosts increasingly layer in advertising for incremental yield. The advertising-supported lane, forecast to expand at 10.35% CAGR, is buoyed by programmatic growth across Asia-Pacific where measurable channels attract brand budgets.

Hybrid models that bundle limited free reads, micropayments and sponsorships help mitigate subscription fatigue. The Daily Beast expects USD 3-4 million from Apple News+ in 2024, while Time already earns seven-figure sums, demonstrating the stability big platforms can offer amid social-traffic volatility. As advertisers push for privacy-compliant targeting, contextual and semantic tools integrated within premium content environments should further expand the digital publishing market.

By Enterprise Size: SME Momentum Accelerates

Large enterprises still controlled 61.55% of 2025 spend, yet SMEs are on track for a 9.62% CAGR as AI removes scale advantages in production speed and distribution reach. Spines can now push a manuscript to market in under three weeks at a fraction of historic cost, letting smaller houses compete on freshness and niche depth.

Cloud-native stacks allow SMEs to skip capex and tap best-in-class services via subscription, shrinking the resource gap with conglomerates. Venture and private-equity funds view content platforms as data-center demand drivers, unlocking new financing pools that could inject billions into SME-led projects. Taken together, these dynamics widen the creator pool and diversify output, enriching the digital publishing market with specialist and community-focused titles.

By End-User Industry: Education Outpaces All

Media and entertainment retained 33.35% of 2025 turnover, but the education segment’s 11.85% CAGR makes it the fastest climber. AI-textbooks that adapt to student level and learning style enhance outcomes and lower costs for universities, catalyzing broader academic adoption fortune.com. Corporate training teams mirror this trend, embedding adaptive modules into onboarding and up-skilling paths.

Retail, government and non-profit sectors also expand their digital footprints, using rich media publishing to engage audiences and drive behavior change. The convergence of entertainment production values with pedagogical objectives births “edutainment” products that blur traditional content silos. This cross-pollination enlarges addressable use cases and lifts growth prospects for the digital publishing market.

Geography Analysis

North America held 36.12% of 2025 revenue, anchored by advanced infrastructure and deep institutional budgets. U.S. regulators are reassessing “inclusive access” textbook billing, a move that could reshape academic adoption curves. Apple’s steady expansion of News and aggressive monetization initiatives show how regional tech leaders set the template for global rollouts. Consolidation talk-such as potential Houghton Mifflin Harcourt and Cambium Learning tie-ups-signals a maturing but still dynamic local ecosystem.

Asia-Pacific is the digital publishing market’s fastest-growing region, with a projected 10.42% CAGR through 2031. Indonesia’s pronounced preference for reading on smartphones and large-scale 5G buildouts create fertile conditions for mobile-first content strategies. Programmatic spend keeps climbing, offering publishers reliable ad income streams. Regional majors like VerSe Innovation acquired Magzter to integrate premium content across 60 languages, highlighting ongoing race to own gateway platforms.

Europe presents a mature but regulation-heavy environment that often sets global compliance norms. GDPR, DMA and related frameworks elevate operating costs yet raise the bar on data ethics, pushing publishers worldwide toward higher standards. Annual UK investment of roughly GBP 900 million into digital education feeds steady demand for AI-enabled learning content. Informa’s acquisition of Ascential shows how European players bulk up in B2B niches to maintain growth under tighter consumer-privacy rules.

Competitive Landscape

The digital publishing market remains moderately fragmented. Tech giants-Amazon, Apple and Google-leverage device ecosystems, app stores and cloud stacks to lock in both creators and readers. Amazon’s color Kindle launch strengthens its device moat, while Apple’s move to internal ad sales indicates a quest for end-to-end monetization control. Google continues to experiment with AI-generated summaries that could reshape consumption habits.

Specialist vendors are scaling fast around AI automation. Spines’ three-week manuscript-to-market promise undercuts traditional production cycles and illustrates how capital is flowing to workflow disruptors. Adobe’s GenStudio advancement embeds generation, orchestration and performance analytics into a single hub, betting that enterprises will pay for unified AI pipelines.

M&A activity surged late 2024: Datamatics took an 80% stake in TNQ Tech for USD 39.6 million, eyeing AI-enabled services for European and North American clients. Publishers Weekly logged seven notable deals in 1H 2024, signalling that niche capabilities and language assets are prized targets. Looking ahead, the ability to integrate real-time personalization, privacy-compliant data and cross-format syndication will define competitive advantage.

Digital Publishing Industry Leaders

Adobe Inc.

Amazon.com Inc.

Apple Inc.

Thomson Reuters Corp.

Netflix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Adobe expanded GenStudio with AI workflow and content-production agents, anticipating a fivefold jump in content demand by 2026.

- March 2025: Houghton Mifflin Harcourt’s owner opened merger talks with Cambium Learning to gain scale in digital education.

- December 2024: Datamatics subsidiary Lumina acquired 80% of TNQ Tech for USD 39.6 million, with full purchase slated by 2026.

- December 2025: Lee Enterprises chose AWS as preferred cloud to build generative-AI platforms for news and ads.

Global Digital Publishing Market Report Scope

Digital publishing, often referred to as online or web publishing, leverages online technology to produce and disseminate digital content.

The study tracks the revenue accrued through the sale of digital publishing solutions by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The digital publishing market is segmented by solution (digital publishing platforms and services), enterprise size (large enterprises and small and medium enterprises), industry (rack mount and portable), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Digital Publishing Platforms |

| Services |

| E-Books |

| Digital Newspapers and Magazines |

| Professional and Academic Reports/Journals |

| Blogs and Web-Native Content |

| Subscription |

| Advertising-supported |

| Transaction/Pay-per-Download |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Education |

| Media and Entertainment |

| Retail and E-commerce |

| Corporate Training and HR |

| Government and Non-profit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| By Solution | Digital Publishing Platforms | ||

| Services | |||

| By Content Type | E-Books | ||

| Digital Newspapers and Magazines | |||

| Professional and Academic Reports/Journals | |||

| Blogs and Web-Native Content | |||

| By Revenue Model | Subscription | ||

| Advertising-supported | |||

| Transaction/Pay-per-Download | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium-sized Enterprises | |||

| By End-user Industry | Education | ||

| Media and Entertainment | |||

| Retail and E-commerce | |||

| Corporate Training and HR | |||

| Government and Non-profit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Israel | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

Key Questions Answered in the Report

What is the current size of the digital publishing market?

The digital publishing market size reached USD 3.17 billion in 2026 and is projected to climb to USD 4.68 billion by 2031.

Which region is growing fastest in digital publishing?

Asia-Pacific leads growth with a forecast 10.42% CAGR, powered by widespread smartphone adoption and expanding 5G coverage.

How dominant are subscriptions in digital publishing revenues?

Subscriptions contributed 53.85% of 2025 revenue, but hybrid models combining ads and micropayments are rising quickly.

Which content type generates the largest share of revenue?

E-books remain the highest-earning content category, accounting for 41.05% of 2025 turnover.

Why are SMEs gaining ground in digital publishing?

AI-native tools and cloud infrastructure lower entry barriers, letting smaller publishers match larger rivals on speed and reach while keeping costs down.

What challenges does the industry face from data-privacy rules?

Compliance with GDPR, DMA and CPRA raises operating costs and limits data-driven personalization, reducing margins and slowing innovation for some publishers.

Page last updated on: