Digital Music Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 39.02 Billion |

| Market Size (2031) | USD 56.22 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

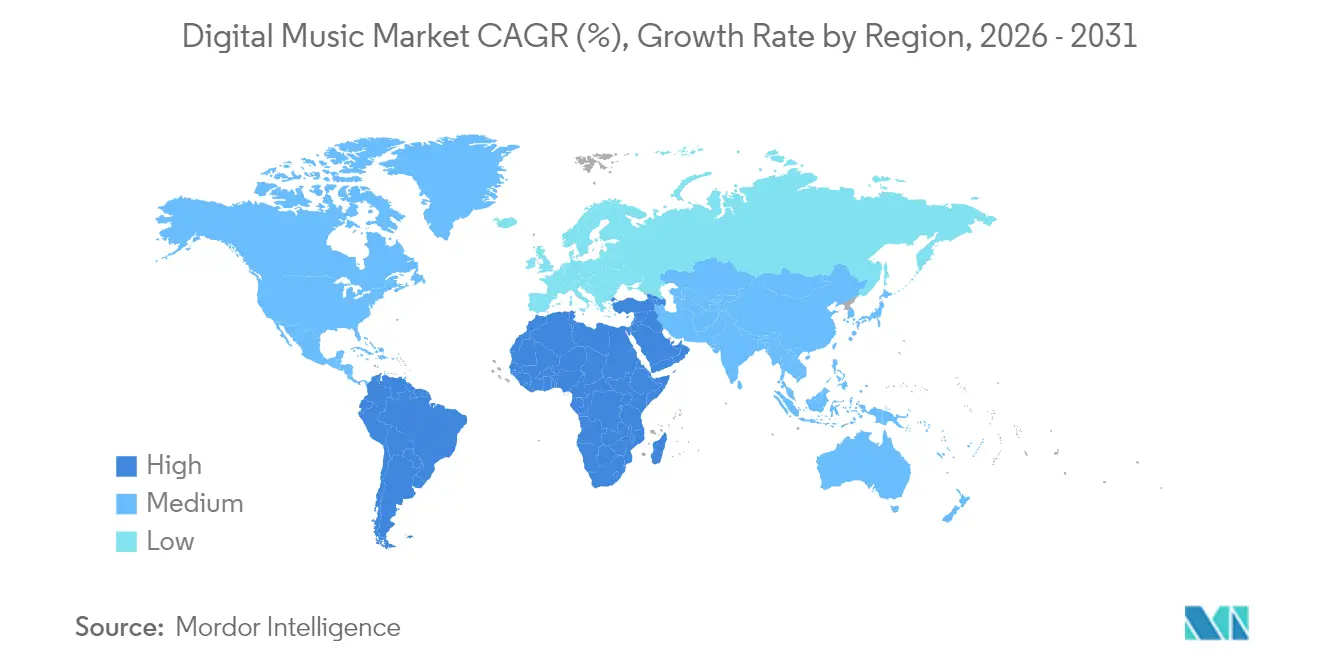

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

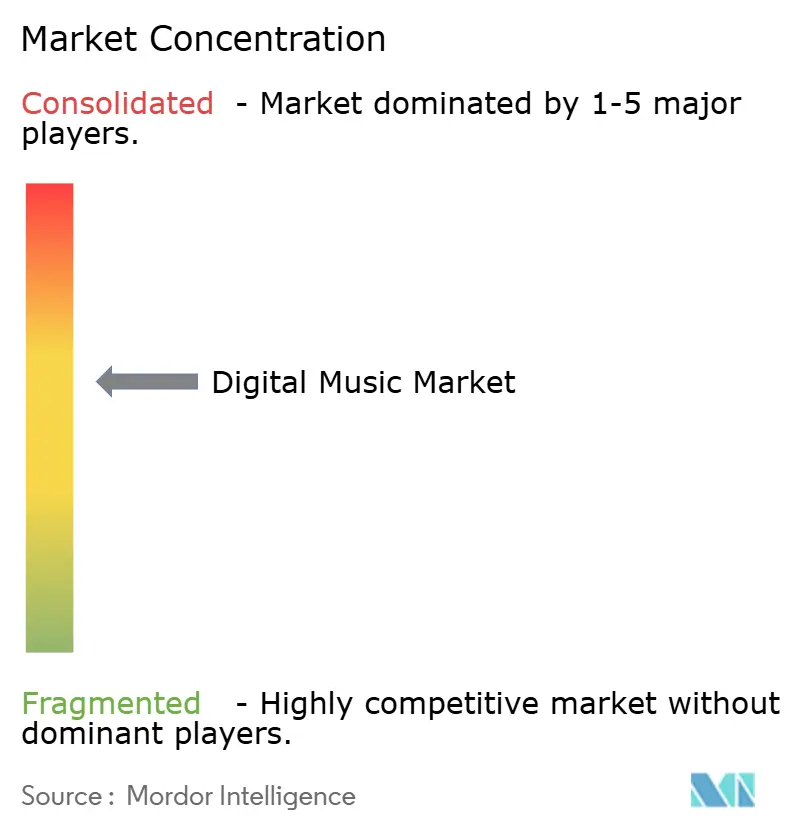

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Music Market Analysis by Mordor Intelligence

The Digital Music Market size was valued at USD 36.27 billion in 2025 and estimated to grow from USD 39.02 billion in 2026 to reach USD 56.22 billion by 2031, at a CAGR of 7.58% during the forecast period (2026-2031). The expansion reflects a continued shift from ownership to access-based listening, as streaming dominates consumer spending patterns. Wider 5G coverage is lifting average bit-rates, which in turn pushes listeners toward higher-fidelity formats. Partnerships between telecom operators and music services are converting large prepaid user pools into first-time subscribers, particularly in emerging economies. Labels and platforms are also experimenting with immersive audio and short-form video tie-ins to raise time-spent-per-user, while direct-to-fan platforms broaden monetization avenues for independent artists. Automakers are embedding premium audio and always-connected dashboards, enlarging the addressable listening window when consumers are on the road.

Key Report Takeaways

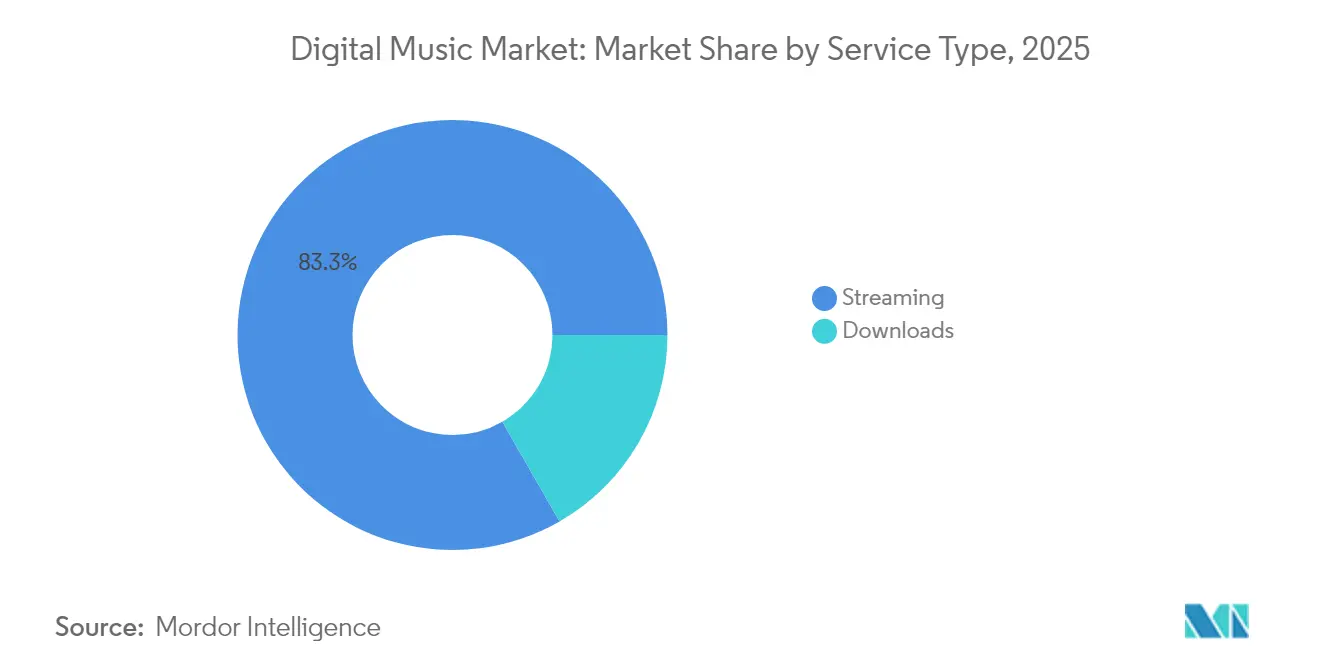

- By service type, streaming held 83.30% revenue share of the digital music market in 2025, while live streaming is set to register a 15.1% CAGR through 2031.

- By revenue model, subscription-based offerings captured 74.10% of the digital music market share in 2025; advertisement/freemium models are projected to grow at a 12.1% CAGR to 2031.

- By platform, mobile devices commanded 59.20% share of the digital music market size in 2025, whereas smart speakers and home assistants are forecast to expand at an 17.3% CAGR between 2026-2031.

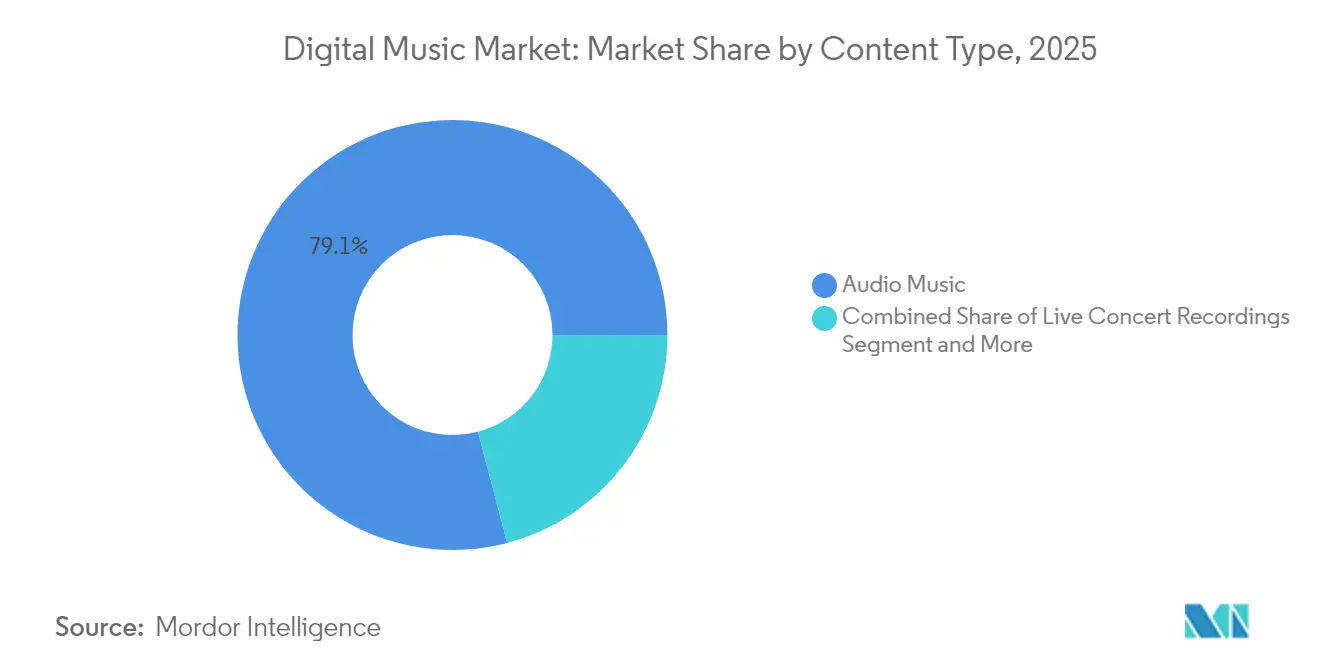

- By content type, audio music led with 79.10% of the digital music market in 2025; podcasts and spoken word are expected to climb at a 18.2% CAGR through 2031.

- By end-user, individual consumers accounted for 62.60% of the digital music market in 2025; commercial establishments exhibit a 11.6% CAGR outlook to 2031.

- By geography, North America contributed 33.75% to 2025 revenue, while the Middle East and Africa is the quickest-growing region with a 16.8% CAGR forecast.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Music Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G and edge computing | +1.30% | Global | Medium term (2-4 years) |

| Telco-music bundles in MENA | +0.90% | Middle East and North Africa | Short term (≤2 years) |

| AI-curated playlists lifting ARPU | +1.10% | Asia-Pacific | Medium term (2-4 years) |

| Immersive audio formats driving upgrades | +0.80% | North America and Europe | Long term (≥4 years) |

| Independent artist direct-to-fan platforms | +0.60% | North America and Europe | Medium term (2-4 years) |

| In-car connected infotainment demand | +0.70% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Telco-Music Bundles Accelerating Paid Subscriptions in Middle East and North Africa

Regional operators bundle weekly music passes into prepaid recharge packs that cost less than USD 1, cutting price barriers for youth segments. Direct carrier billing also bypasses card penetration gaps, raising conversion rates. Several local labels offer Arabic catalog exclusives, making bundled plans culturally relevant. As zero-rating of data traffic remains common, streaming becomes effectively free of data charges, solidifying daily listening habits. These tactics boost the digital music market’s paid subscriber base and stabilize churn across MENA.[2]GSMA, “The Mobile Economy Middle East & North Africa 2025,” gsma.com

AI-Curated Playlists User Engagement and ARPU in Asia-Pacific

Services apply graph neural networks to cluster behavior signals across language, device, and contextual tags, generating hyper-personal daily mixes. Users in Japan and Korea spend 23% more minutes on platform when served AI mixes, driving ad load as well as upsell to family plans. AI also localizes playlist text in multiple scripts, easing adoption in Indonesia and Thailand. Higher engagement raises retention, which directly enhances the digital music market revenue outlook. Spotify claims discovery session share rose after rolling out AI DJ in the region. [3]Spotify, “AI DJ Expands Across Asia,” spotify.com

Adoption of Immersive Audio (Dolby Atmos, Spatial) Boosting Premium Tier Upgrades

Major distributors now master over 200,000 tracks in object-based formats, with catalog breadth growing 40% year-on-year. Listeners with AirPods Pro or similar headsets report higher satisfaction scores, propelling households to shift from individual to family premium plans. Streaming services position immersive audio behind higher price ladders, supporting yield management. Concert archives remixed in spatial audio also extend the life of back catalogs. The digital music market thus finds a fresh lever for top-line expansion

Proliferation of 5G and Edge Computing Enabling Lossless Mobile Streaming

Wider millimeter-wave and sub-6 GHz roll-outs permit stable 1 Gbps downlink speeds, removing the bandwidth ceiling that previously capped streaming quality. Platforms now promote 24-bit/96 kHz files without buffering, a shift converting casual users into premium tiers. Edge caching further lowers latency so interactive features such as real-time lyrics and fan votes integrate smoothly. Device makers preload high-resolution DACs, creating a virtuous cycle of hardware and content upgrades. The digital music market is therefore gaining higher ARPU as listeners pay extra for tiered fidelity.[1]3GPP, “Release 18 Highlights,” 3gpp.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU copyright-linked royalty inflation | -0.70% | Europe | Medium term (2-4 years) |

| Stream-ripping and piracy platforms | -0.60% | Southeast Asia | Short term (≤2 years) |

| High payment-gateway fees | -0.40% | Sub-Saharan Africa | Short term (≤2 years) |

| App-store commission policies | -0.50% | Global/iOS ecosystem | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Stream-Ripping and Piracy Platforms Undermining Revenues in Southeast Asia

YouTube-DL clones and Telegram bots convert on-demand streams into downloadable MP3s at scale. Countries such as Indonesia block domains, yet mirror sites reappear within days. The cost of enforcement remains high relative to ARPU, so services absorb revenue cannibalization estimated at 10% of addressable spend. Piracy dampens willingness to pay and skews advertiser ROI models, tempering digital music market growth in the region. Rights alliances lobby for stronger intermediary liability, but progress is uneven

Royalty Cost Inflation From Evolving EU Copyright Directive Compressing Margins

Directive (EU) 2019/790 obliges platforms to secure “best-effort” licenses for user-uploaded content and introduces liability extensions. Negotiated rates with collecting societies therefore escalate, lifting cost of revenue. Smaller services struggle to pass prices to consumers in saturated European markets, compressing gross margins by up to 250 basis points. Some independent labels also invoke article 18 to renegotiate royalty splits, further pressuring hosts. Without offsetting ARPU gains, the digital music market margin profile in Europe deteriorates

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Streaming Dominance and Live Streaming Upside

Streaming contributed USD 30.22 billion, equal to 83.30% of 2025 revenue. On-demand listening combines unrestricted catalog access with offline caching, locking users into multi-device ecosystems. The digital music market size for live streaming is still modest, but its 15.1% CAGR signals rapid scale as artists simulcast concerts directly to fans. Labels partner with event promoters to bundle digital tickets that include limited-edition merch, lifting spend per fan. Meanwhile, downloads continue to decline because cloud storage renders local files redundant. As cellular data tariffs fall, emerging markets leapfrog downloads and move directly into streaming.

A rising share of licensed live events carry tipping and virtual gifting tools enabling real-time monetization. Established streaming apps integrate live modules rather than building separate destinations, keeping audience retention high. Hardware firms place low-latency audio codecs in new phones to improve the live experience. These shifts sustain the digital music market trajectory toward experiential formats beyond static catalog consumption.

By Revenue Model: Subscription Resilience Outpaces Advertising Cycles

Subscription frameworks locked in 74.10% of 2025 gross revenue, supported by bundled billing and student discounts. Medium-bundle family plans yield predictable cash flow, which platforms reinvest in exclusive sessions. Ad-supported free tiers deliver reach but face cyclical advertiser budgets and signal-loss from tracking restrictions. Nonetheless, a 12.1% CAGR points to healthier brand spending in developing economies where CPM baselines remain lower.

The digital music market share for subscriptions is preserved as services tier offerings by audio quality, offline usage and simultaneous log-ins. Introductory three-month trials shorten decision cycles and cut acquisition costs. Mixed monetization, such as premium-podcast “channels,” adds upsell layers under the same wallet. Conversely, pay-per-download remains niche, serving audiophiles who demand perpetual ownership.

By Platform: Mobile First, with Smart Speaker Momentum

Mobile devices captured 59.20% of listening hours in 2025. OEM preload contracts and lightweight progressive web apps expand reach among budget smartphone segments. In-app adaptive streaming scales bitrate based on network quality to preserve session stability. Smart speakers, growing at an 17.3% CAGR, transform kitchen and living room audio habits. Voice search lowers friction and triggers incremental discovery when users ask for mood-based playlists.

The digital music market size tied to desktop/laptop persists among productivity users who listen during work hours, but its relative share slips as hybrid work shifts soundscapes back to home assistants. Connected cars increasingly feature Android Automotive or CarPlay dashboards, embedding music apps natively. Automakers join revenue-sharing to convert driver dwell time into streaming revenue.

By Content Type: Audio Music Core with Podcast Upsurge

Audio music commanded 79.10% of 2025 receipts, reflecting the core value proposition of on-demand track play. Catalog depth across global and local repertoire differentiates services. Podcasts and spoken word grow at 18.2% CAGR, attracting distinct advertising formats such as host-read endorsements. Serialized investigative shows and language-learning programs widen demographic reach. The digital music market size for music videos is modest on audio-first platforms but grows on social-video hybrids that pay both music and video royalties.

Live concert recordings get renewed shelf life as remastered spatial tracks, adding high-margin content without new studio costs. Smart speakers steer users toward news briefings and short podcasts, elevating spoken-word share during morning routines. As rights frameworks standardize, licensing friction for these formats declines.

By End-User: Consumer Foundation and Commercial Upsell

Individual consumers represented 62.60% of spending in 2025. Personal playlists, recommendations and social integrations sustain engagement loops. Commercial establishments, including cafés and gyms, sign blanket performance licenses bundled by service providers, posting a 11.6% CAGR outlook. Centralized dashboards let chain retailers program store ambience across regions.

The digital music market benefits from automotive OEM partnerships that preload time-bound trials, converting vehicle buyers into long-tail subscribers. Airlines experiment with in-flight streaming over Ku-band links, hinting at future travel-segment revenue. Rights holders negotiate distinct tariffs for these B2B contexts, diversifying income beyond household use.

Geography Analysis

North America delivered 33.75% of 2025 revenue, buoyed by high per-capita spend and early adoption of immersive audio. Average revenue per user remains the sector’s highest, exceeding USD 7 per month, owing to extensive family and multi-service bundles. Major labels maintain robust local repertoire, reinforcing catalog stickiness. The digital music market size in the United States especially benefits from car connectivity integrations and tipping features during live online events.

Europe shows mixed momentum as royalty obligations increase. Markets such as Germany exhibit stable premium penetration but slower unit growth. Meanwhile, Southern Europe sees renewed adoption through low-priced telco partnerships. The digital music market share in Europe faces erosion from stream-ripping; yet enforcement collaboration between platforms and ISPs gradually curtails illicit traffic.

The Middle East and Africa is the fastest-growing region with a 16.8% CAGR projection. Operators in Saudi Arabia and the United Arab Emirates push competitively priced weekly passes bundled with zero-rated data, rapidly onboarding youth populations. African startups localize UI into Swahili and Hausa, capturing cultural niches. Asia-Pacific shows diverse patterns: Japan’s physical-media legacy slows digital acceleration, whereas India’s mass adoption of budget smartphones has propelled ad-supported models. Collectively, rising disposable income and smartphone penetration underpin a strong demand curve for the digital music market across emerging economies.

Competitive Landscape

The market hosts global leaders such as Spotify, Apple Music, Amazon Music and YouTube Music, each leveraging ecosystem synergies. Spotify increases conversational interfaces and AI DJ features to lengthen session times. Apple cross-bundles Music with TV+ and Fitness+, defending wallet share among iPhone owners. Amazon integrates Music into Prime, framing it as an added value for fast shipping subscribers. YouTube Music capitalizes on its vast video archive to offer seamless audiovisual switching.

Regional champions carve defensible niches. Tencent Music holds exclusive Chinese catalogue deals and bundles karaoke functionalities. Anghami focuses on Arabic repertoire and telecom billing relationships across MENA, while Boomplay targets sub-Saharan Africa through lightweight app builds. Each regional specialist exploits cultural and language localization to fend off global rivals and contributes to a fragmented tail of offerings.

Independent artist distribution intermediaries such as TuneCore, DistroKid and RouteNote help musicians retain ownership by collecting royalties across multiple DSPs for a flat fee or commission. Their growth reflects the surge in self-released tracks, estimated at 120,000 daily uploads industry-wide. Label services firms like LANDR and Amuse provide mastering and marketing dashboards, deepening service bundles. M&A activity centers on catalog acquisition as funds seek predictable cash flows; this trend intensifies catalog pricing and fuels race for exclusive rights within the digital music market.

Digital Music Industry Leaders

TuneCore Inc.

iHeartMedia Inc.

LANDR Audio Inc.

Tencent Music Entertainment Group

Spotify Technology S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Create Music Group acquired indie electronic label Monstercat and pledged an additional USD 50 million investment over the next two years, expanding its global reach in electronic music and gaming

- April 2025: Concord completed its acquisition of music distribution platform Stem, addressing the 'graduation problem' faced by artists who outgrow smaller platforms while allowing them to retain autonomy

- April 2025: Hungama Music shut down operations in India, signaling significant consolidation in the Indian music streaming market despite booming demand for music streaming services

- January 2025: Dolby showcased in-car entertainment innovations at CES 2025, highlighting the expansion of Dolby Atmos to over 20 automotive manufacturers and reporting that 93% of Billboard's 2024 Top 100 Artists have released music in Dolby Atmos

Global Digital Music Market Report Scope

The digital music market encompasses the creation, distribution, and consumption of music via digital platforms and technologies. This spans digital downloads, streaming services, online music stores, and various platforms granting consumers access to electronic music. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The digital music market is segmented by downloads (website, apps, social media, music streaming and streaming subscription), by end-users (individual users, commercial users and other end-users) and by geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Downloads | Websites |

| Mobile Apps | |

| Social Media | |

| Streaming | On-Demand Streaming |

| Live Streaming |

| Subscription-Based |

| Advertisement / Freemium |

| Pay-Per-Download |

| Mobile Devices |

| Desktop / Laptop |

| Smart Speakers and Home Assistants |

| Connected Cars and Infotainment Systems |

| Audio Music |

| Podcasts and Spoken Word |

| Live Concert Recordings |

| Music Videos (Audio-Visual) |

| Individual Consumers |

| Commercial Establishments |

| Automotive OEM and In-Car Services |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East and Africa | |

| Africa | South Africa |

| Rest of Africa |

| By Service Type | Downloads | Websites |

| Mobile Apps | ||

| Social Media | ||

| Streaming | On-Demand Streaming | |

| Live Streaming | ||

| By Revenue Model | Subscription-Based | |

| Advertisement / Freemium | ||

| Pay-Per-Download | ||

| By Platform | Mobile Devices | |

| Desktop / Laptop | ||

| Smart Speakers and Home Assistants | ||

| Connected Cars and Infotainment Systems | ||

| By Content Type | Audio Music | |

| Podcasts and Spoken Word | ||

| Live Concert Recordings | ||

| Music Videos (Audio-Visual) | ||

| By End-User | Individual Consumers | |

| Commercial Establishments | ||

| Automotive OEM and In-Car Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the digital music market?

The digital music market is valued at USD 39.02 billion in 2026.

How fast is the digital music market expected to grow?

It is forecast to expand at a 7.58% CAGR, reaching USD 56.22 billion by 2031.

Which service segment is growing the quickest?

Live streaming is projected to grow at a 15.1% CAGR between 2026-2031.

Which region shows the highest future growth?

The Middle East & Africa is expected to post a 16.8% CAGR, the fastest worldwide.

How significant are podcasts in the overall spending mix?

Podcasts and spoken word content are set to rise at a 18.2% CAGR, gradually increasing their share of total revenue.

Who are the leading players in the digital music market?

Spotify, Apple Music, Amazon Music and YouTube Music remain the global leaders, complemented by regional specialists such as Tencent Music and Anghami.

Page last updated on: