Digital Art Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.69 Billion |

| Market Size (2031) | USD 13.26 Billion |

| Growth Rate (2026 - 2031) | 14.66% CAGR |

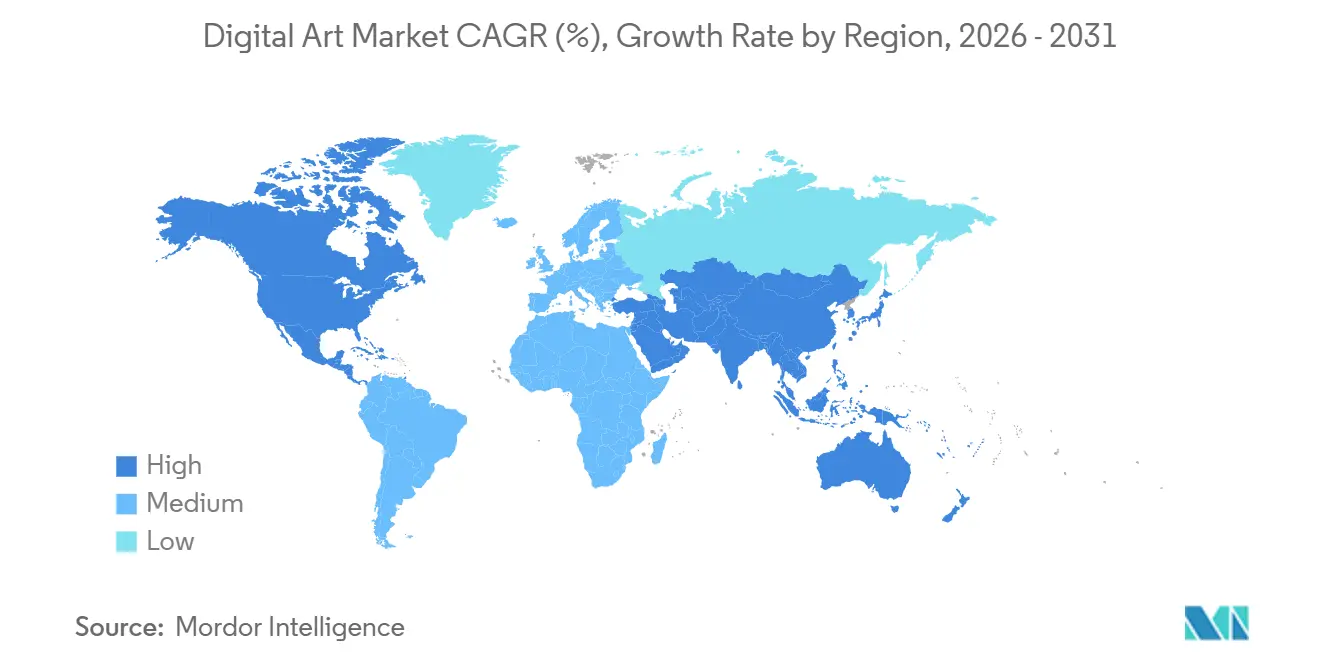

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

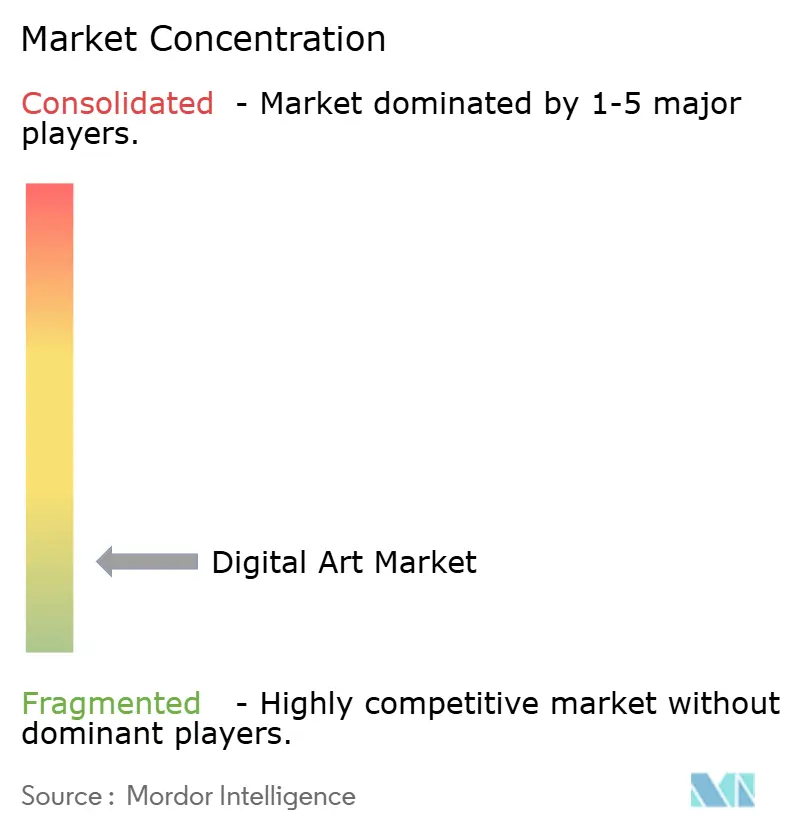

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Art Market Analysis by Mordor Intelligence

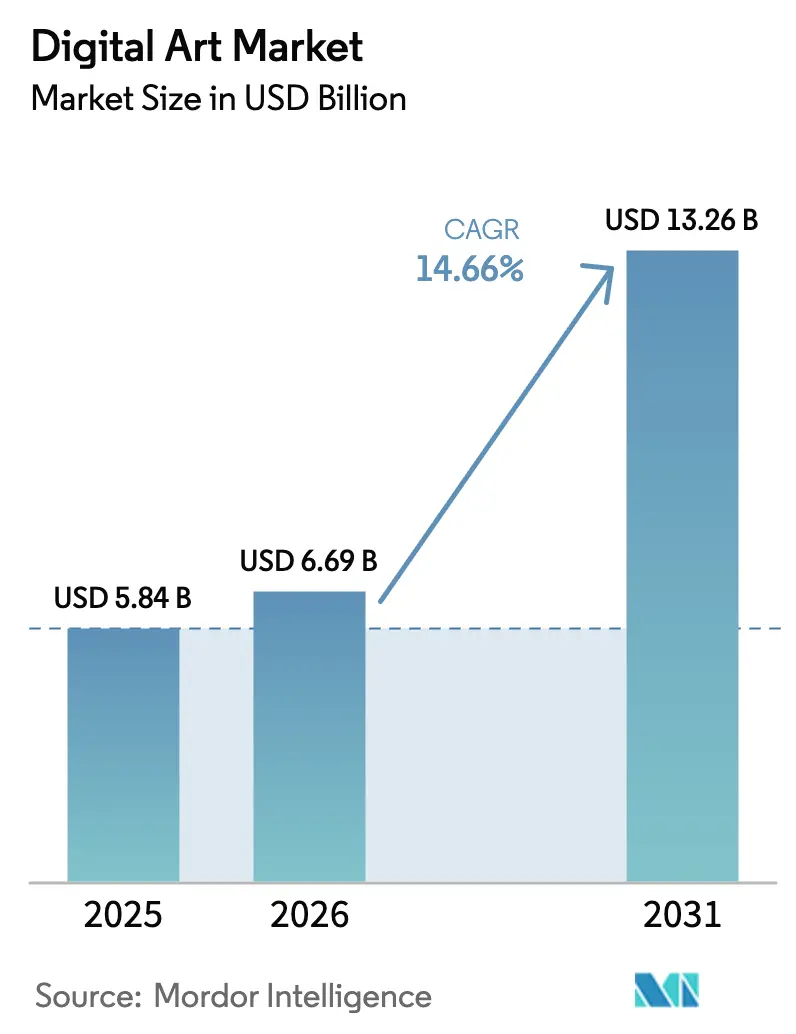

The digital art market size is projected to be USD 5.84 billion in 2025, USD 6.69 billion in 2026, and reach USD 13.26 billion by 2031, growing at a CAGR of 14.66% from 2026 to 2031. Robust growth reflects corporate reallocation of brand-experience budgets toward immersive content, wider collector acceptance of tokenized provenance, and the mainstreaming of blockchain-based royalty flows that keep artists financially engaged. Generative artificial intelligence cuts production cycles from weeks to hours, letting agencies test multiple visual concepts before any client meeting, while advances in spatial computing hardware enlarge the canvas for interactive storytelling. Online marketplaces continue to deepen liquidity because they pair instant provenance verification with global reach, giving buyers confidence that previously came only from in-person gallery visits.

Key Report Takeaways

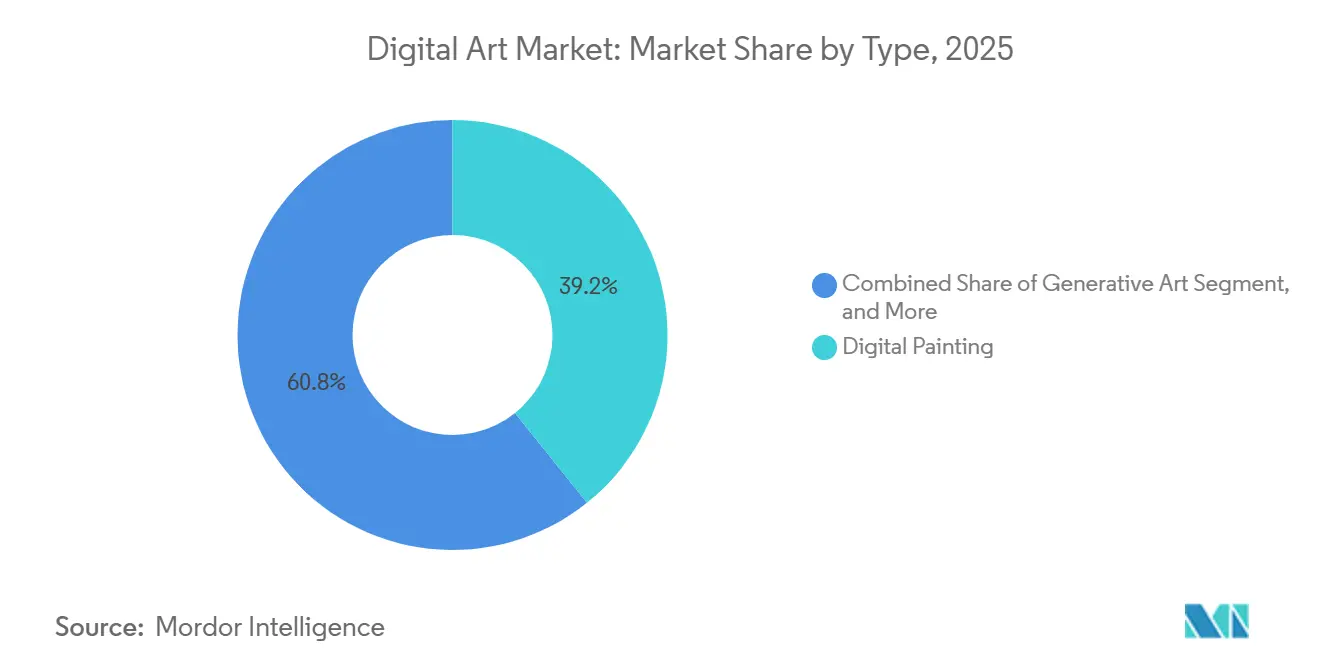

- By type, digital painting led with 39.24% revenue share in 2025, while generative art is advancing at a 15.87% CAGR through 2031.

- By medium, 2D illustration captured 47.39% of revenue in 2025, whereas AR/VR interactive formats are projected to expand at 15.61% CAGR to 2031.

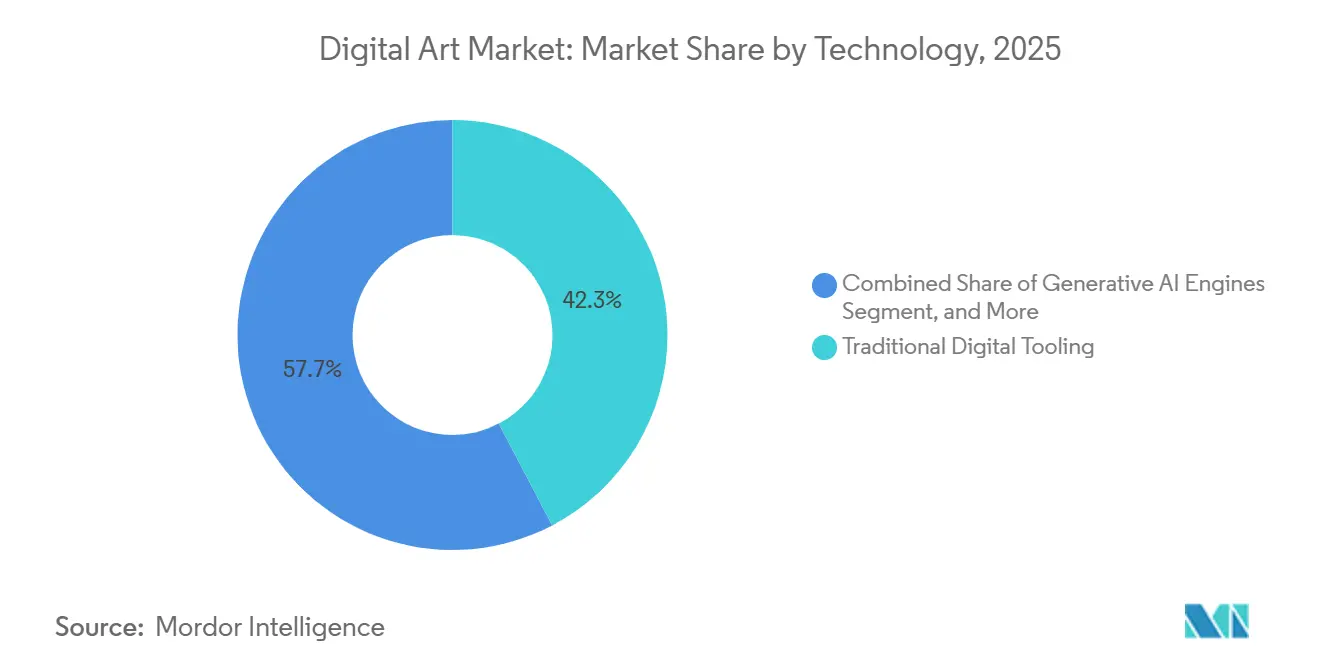

- By technology, traditional digital tooling held 42.33% of spending in 2025, and generative AI engines register the strongest outlook at 15.44% CAGR over the forecast period.

- By sales channel, online marketplaces controlled 61.46% of 2025 turnover and are forecast to grow at 15.07% CAGR to 2031.

- By geography, North America accounted for 36.73% of value in 2025, while Asia-Pacific is set to rise at a 15.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Art Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of NFT-based collectibles | +3.2% | Global, concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Corporate demand for immersive brand storytelling via AR/VR | +2.8% | North America and Europe, expanding to Middle East | Short term (≤ 2 years) |

| Adoption of generative AI tools | +2.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Blockchain-enabled royalty smart contracts | +2.1% | Global, early traction in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising digital-native buyer base | +1.9% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Growth of immersive art venues | +1.5% | North America, Europe, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion of NFT-Based Collectibles Driving Digital Art Monetization

NFT collectibles reshaped the digital art market by embedding smart contracts that return primary and secondary proceeds to creators. Liquidity rose sharply in late 2025 when institutional buyers started using tokens chiefly as provenance tools rather than speculative chips, decoupling demand from short-term cryptocurrency swings. Adobe embedded cryptographic credentials directly into Creative Cloud workflows, allowing artists to prove originality before minting, which reduced onboarding friction for galleries.[1]Adobe Inc., “Content Credentials Overview,” adobe.com Even so, weekly trading volumes on leading exchanges still fluctuate in tandem with Ether’s spot price, illustrating that speculative sentiment remains a latent risk for near-term sales.

Corporate Demand for Immersive Brand Storytelling via AR/VR Installations

Brands now allocate larger shares of experiential budgets to AR and VR activations that turn static narratives into interactive venues. Luxury houses used head-mounted displays and in-store spatial installations throughout 2025, reporting double-digit gains in dwell time and conversion. Museums license temporary AR overlays because digital refreshes cost less than physical re-hangs, expanding revenue per visitor. Hardware costs, however, keep adoption clustered in flagship sites as mid-tier galleries struggle to amortize high-brightness screens. Apple’s Vision Pro rollout widened consumer awareness of spatial content but also raised expectations for production quality, pressuring agencies to master real-time engines.[2]Apple Inc., “Apple Vision Pro,” apple.com

Adoption of Generative AI Tools Boosting Content Velocity for Agencies

Generative AI compresses ideation cycles, letting creative teams deliver dozens of mock-ups within a single day. A 2024 Adobe survey found 73% of professionals had woven AI into daily tasks, with the fastest uptake among agencies that serve fast-moving consumer goods. Smaller studios leverage open-source models such as Stable Diffusion to match the output volume of larger competitors, intensifying price-based rivalry. Yet client differentiation has begun to move up-stream to concept originality and narrative strategy, emphasizing skills still anchored in human authorship. Enterprises internalize these engines to lower outsourcing costs, but they must also address model-training compliance to avoid future copyright disputes.

Blockchain-Enabled Royalty Smart Contracts Attracting Emerging Artists

Automated royalties lower entry barriers for emerging artists by ensuring perpetual revenue capture on every resale. Platforms embed 10-15% royalty splits within NFT metadata, giving creators a sustainable upside even after the initial drop. Asia-Pacific collectors gravitate to this mechanism as a means of direct artist support, helping regional talent bypass traditional gatekeepers. However, enforceability requires that sales remain on-chain; peer-to-peer transfers outside supported exchanges can still dodge contract execution, undercutting revenue certainty. The European Union’s phased MiCA rollout in 2025 provided legal footing for royalty clauses, but also raised compliance costs for smaller platforms.[3]European Union, “Markets in Crypto-Assets Regulation,” europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cryptocurrency prices | -2.4% | Global, particularly North America and Asia-Pacific | Short term (≤ 2 years) |

| Copyright ambiguity for AI-generated works | -1.8% | Global, with acute challenges in North America and Europe | Medium term (2-4 years) |

| Limited high-resolution display infrastructure | -1.2% | Europe, Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Regulatory uncertainty around digital-asset classes | -1.1% | Global, varying across jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cryptocurrency Prices Disrupting NFT Transaction Volumes

Sharp token price swings undermine buyer confidence because many art NFTs are denominated in Ether. When Ethereum fell from USD 4,000 to USD 2,400 in early 2024, weekly volumes on OpenSea collapsed by 60%. High-value collectors waited on the sidelines, while platforms struggled to maintain minimum bid thresholds. Emerging stablecoin-denominated marketplaces partially eased this risk during 2025, yet adoption remains thin outside corporate buyer circles. Lack of hedging tools comparable to commodities futures leaves galleries without a reliable mechanism to smooth revenue, forcing them to swallow currency risk or pass it to artists.

Copyright Ambiguity for AI-Generated Works Limiting Commercial Use

Current U.S. guidance states that content produced without substantial human input is ineligible for copyright, making brand licensors wary of AI-first imagery. Enterprise buyers seek indemnity against claims that a model may have replicated copyrighted material found in its training data. Europe’s AI Act adds transparency mandates but still leaves ownership undefined, creating a patchwork of compliance hurdles across member states. Agencies are adopting hybrid pipelines where AI drafts early concepts and humans refine final assets, yet this dilutes most of the cost and speed benefits that originally justified generative adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Generative Art Outpaces Traditional Formats

Generative art is expanding at a 15.87% CAGR, the fastest tempo among all categories, while digital painting secured a 39.24% digital art market share in 2025. The pace reflects corporate enthusiasm for algorithmically generated visuals that populate product launches and spatial interfaces. Established painting communities retain a loyal collector base, but agencies focused on rapid iteration now view generative outputs as default starting points. Digital collage continues to thrive in editorial storytelling, whereas 3D sculptures gain traction in metaverse showrooms where volumetric depth drives engagement.

Generative workflows reorient artist career paths from manual production to prompt design and model fine-tuning. Those who adapt command premium project-director fees, while holdouts risk margin erosion as clients benchmark their rates against AI-enabled alternatives. Experimental niches such as bio-art and data visualizations remain too small to influence overall digital art market size, yet they foster innovation around sensor inputs and live data feeds that could migrate into mainstream channels.

By Medium: AR/VR Interactive Formats Gain Momentum

AR/VR interactive works are set to rise at 15.61% CAGR, outpacing legacy formats, whereas 2D illustration accounted for 47.39% of the 2025 digital art market size. Demand for immersive storytelling is strongest among luxury retailers and museums that rely on experiential differentiation to justify higher ticket prices. Animation remains vital for video platforms that monetize through dynamic advertising slots, and 3D illustration gains favor in product visualization because spatial accuracy aids consumer decision-making.

Hardware availability and creator skills ultimately govern medium choice. Premium headsets from Apple and Meta increase consumer appetite, but supply bottlenecks in real-time talent slow content rollout. Middleware plugins that auto-convert 2D layers into AR-ready assets lower these barriers, promising to broaden contributor pools over the next three years. Until then, the bulk of revenue will still accrue to studios able to meet technical specifications for flagship installations.

By Technology: AI Engines Disrupt Traditional Tooling

Traditional software suites drew 42.33% of spending in 2025, yet AI engines are forecast to log a 15.44% CAGR, narrowing the gap in the digital art market. Blockchain-enabled provenance tools, while smaller in value, introduce trust mechanisms that older platforms cannot match. Emerging solutions such as neural style transfer and AI-assisted rigging each hold single-digit shares but signal where feature roadmaps are heading.

Integrate generative modules or risk user flight. Adobe rolled out Firefly across Photoshop and Illustrator to maintain ecosystem gravity, and Corel appended AI color harmonization in its Painter upgrade. Open-source models accelerate commoditization, shifting competition toward user experience and cloud performance guarantees. Enterprises prefer integrated licenses for compliance and collaboration, while freelance creators accept a patchwork of best-of-breed tools optimized by task.

By Sales Channel: Online Marketplaces Dominate Distribution

Online platforms captured 61.46% of sales in 2025, securing the largest slice of the digital art market share and are positioned to grow at 15.07% CAGR. Instant provenance checks and global reach outweigh the social cachet that drives buyers to physical openings. Traditional galleries still command premium commissions among ultra-high-net-worth clients seeking curatorial narratives and in-person networking.

Hybrid models emerged as winning propositions during 2025. Galleries launched password-gated viewing rooms for serious collectors, while NFT exchanges organized temporary pop-ups at art fairs and fashion weeks. Bloomberg tracking shows that omnichannel dealers record 30% higher customer lifetime value than single-channel peers. Jurisdictions experimenting with classifying NFTs as securities complicate channel economics, give scale advantages to well-capitalized portals, and reinforce the need for compliance toolkits.

Geography Analysis

North America held 36.73% of 2025 value, with United States retailers, museums, and corporate campuses showcasing flagship AR installations that differentiate visitor experiences. Venture funding reached USD 2.8 billion across NFT exchanges and creative-tech startups, sustaining a tight innovation loop. SEC guidance in 2024 clearly separated collectible NFTs from securities, reducing compliance gray areas for marketplaces. Canada and Mexico contribute smaller slices but show rapid growth around Montreal’s animation cluster and Mexico City’s digital art festivals.

Asia-Pacific is projected to compound at 15.67% CAGR through 2031, the fastest regional pace in the digital art market. China’s state-curated digital-collectible platforms reach hundreds of millions of users, even though content remains tightly regulated. India’s creator economy leverages lower production costs and robust smartphone adoption to tap global audiences, while Japan transitions iconic manga IP to tokenized editions that monetize fandom. Singapore’s tax clarity positions it as an operational hub, whereas South Korea’s integration of NFTs into K-pop merchandising exemplifies entertainment-driven adoption.

Europe, the Middle East, and Africa display heterogeneous momentum. MiCA raises operating costs for NFT venues yet attracts institutional capital by clarifying rules. The United Arab Emirates and Saudi Arabia commission monumental immersive installations to diversify tourism revenue, fueling hardware and content demand. Sub-Saharan Africa’s growth centers on mobile-first creators, though limited gallery infrastructure slows premium pricing. Latin America, led by Brazil and Argentina, participates heavily on global portals but domestic sales remain sensitive to currency swings.

Competitive Landscape

The digital art market remains visibly fragmented, with creative software publishers, NFT-native exchanges, hardware suppliers, and immersive venue operators all capturing different slices of value. Adobe and Autodesk protect legacy user bases through subscription bundling that keeps freelancers and agencies inside closed ecosystems even as open-source AI tools narrow historical feature advantages. OpenSea, SuperRare, and Rarible monetize secondary sales that traditional galleries cannot easily track, giving them revenue resilience when primary drops slow. Authentication specialists such as Verisart and Arianee fill a critical trust gap by attaching tamper-proof certificates to works that move across multiple platforms. The overall effect is strong rivalry on both product capabilities and fee structures, with no single firm able to dictate standards across creation, distribution, and display.

Competitive energy intensified after 2024 as incumbents raced to bolt generative functions onto established workflows. Adobe’s Firefly 3.0 rollout placed prompt-based image generation inside Photoshop and Illustrator, limiting leakage to stand-alone engines like Midjourney. Autodesk used the Wonder Dynamics acquisition to automate 3D character animation, courting film and game studios that value shorter production cycles. OpenSea’s alliance with Christie’s married blockchain provenance to blue-chip curatorial vetting, attracting high-net-worth collectors who had sat on the sidelines.

Disruptors continue to probe white spaces where neither software giants nor marketplaces move fast enough. Listing aggregators scrape multiple NFT venues to create unified search dashboards, eroding the network effects that once locked buyers into a single portal. Hardware makers, including Wacom, introduce AI-assisted sketch suggestions that differentiate premium tablets amid rising price pressure on commodity display gear. Immersive venue groups such as Meow Wolf secure real estate in major cities, positioning large-format installations as the next experiential retail anchor. Cross-platform interoperability remains a contested frontier because open standards would enlarge the total addressable market but dilute proprietary moats. Regulatory tightening around royalties and digital asset custody favors well-capitalized players, yet also raises compliance costs that can crowd out smaller innovators. Talent scarcity in real-time 3D content creation grants Unity and Unreal Engine specialists premium rates, further segmenting supplier power across the chain.

Digital Art Industry Leaders

Adobe Inc.

Epic Games Inc.

Behance LLC

DeviantArt Inc.

Nifty Gateway LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Autodesk unveiled a cloud-native generative animation engine that automates character rigging for VR experiences, aiming for commercial rollout by Q3 2026.

- October 2025: Apple began shipping the Vision Pro developer kit, giving studios advance access to spatial design libraries and monetization frameworks.

- September 2025: Adobe activated Content Credentials across its Creative Cloud suite, letting artists embed cryptographic provenance data prior to NFT minting.

- April 2025: Rarible added USD Coin and Tether settlement options, enabling collectors to transact without exposure to Ether price swings.

Global Digital Art Market Report Scope

The Digital Art Market refers to the buying, selling, and trading of artworks created or distributed in digital form. These artworks are made using digital tools such as graphic tablets, design software, AI tools, or 3D programs, and they are sold through online platforms or marketplaces.

The Digital Art Market Report is Segmented by Type (Digital Collage, Digital Painting, Generative Art, 3D Modeling and Sculptures, AR/VR Immersive Works, Other Types), Medium (2D Illustration, 3D Illustration, Animation and Motion Graphics, AR/VR Interactive, Other Mediums), Technology (Traditional Digital Tooling, Blockchain/NFT-Enabled, Generative AI Engines, Other Technologies), Sales Channel (Online Marketplaces, Offline Galleries and Pop-Ups), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Digital Collage |

| Digital Painting |

| Generative Art |

| 3D Modeling and Sculptures |

| AR/VR Immersive Works |

| Other Types |

| 2D Illustration |

| 3D Illustration |

| Animation and Motion Graphics |

| AR/VR Interactive |

| Other Mediums |

| Traditional Digital Tooling |

| Blockchain / NFT-Enabled |

| Generative AI Engines |

| Other Technologies |

| Online Marketplaces |

| Offline Galleries and Pop-Ups |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Digital Collage | ||

| Digital Painting | |||

| Generative Art | |||

| 3D Modeling and Sculptures | |||

| AR/VR Immersive Works | |||

| Other Types | |||

| By Medium | 2D Illustration | ||

| 3D Illustration | |||

| Animation and Motion Graphics | |||

| AR/VR Interactive | |||

| Other Mediums | |||

| By Technology | Traditional Digital Tooling | ||

| Blockchain / NFT-Enabled | |||

| Generative AI Engines | |||

| Other Technologies | |||

| By Sales Channel | Online Marketplaces | ||

| Offline Galleries and Pop-Ups | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the digital art market be by 2031?

It is forecast to reach USD 13.26 billion, supported by a 14.66% CAGR between 2026 and 2031.

Which format is growing fastest in digital art?

Generative art leads with a 15.87% CAGR because enterprises favor algorithm-driven content for rapid testing.

Why are online marketplaces dominant in digital art sales?

They captured 61.46% of 2025 revenue by offering global reach and instant provenance checks that physical galleries cannot match.

What regional market is expanding most quickly?

Asia-Pacific is projected to advance at a 15.67% CAGR through 2031, driven by supportive regulation in Singapore and rapid creator adoption in India and China.

How does cryptocurrency volatility affect digital art sales?

Price swings reduce NFT transaction volumes, as collectors often wait for token stability before committing to high-value purchases.

What key technology trend should artists watch?

The rise of generative AI engines, which are predicted to grow at a 15.44% CAGR, will redefine skill requirements toward prompt design and concept leadership.

Page last updated on: