Stock Photography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

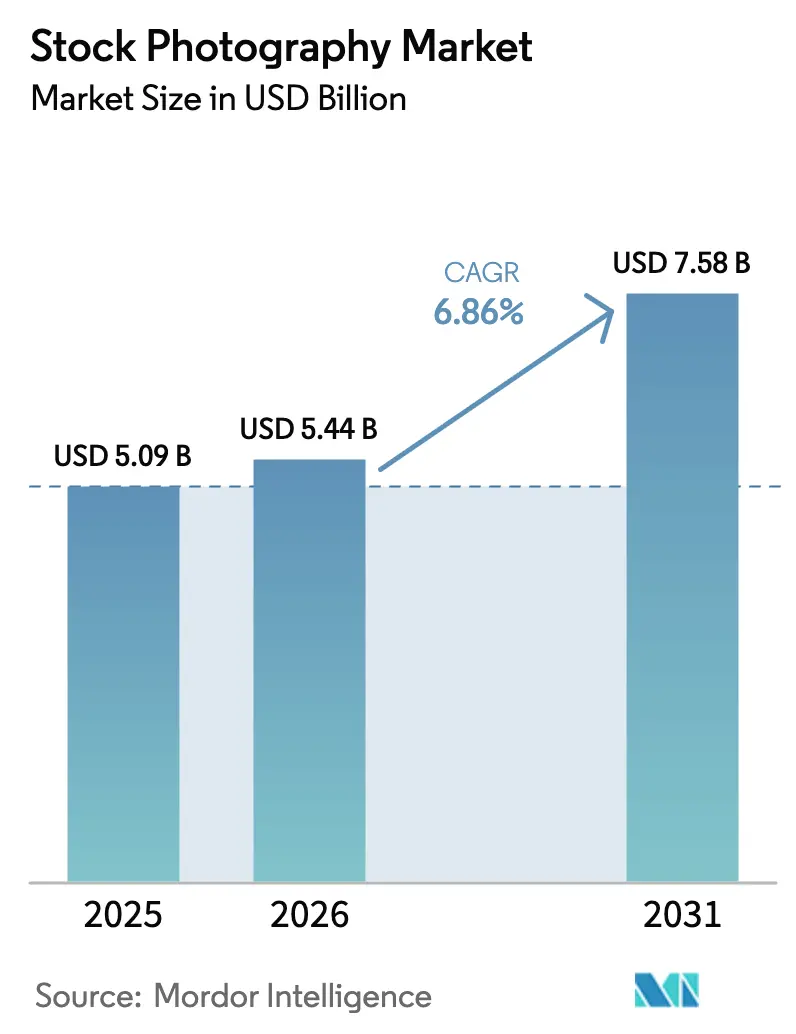

| Market Size (2026) | USD 5.44 Billion |

| Market Size (2031) | USD 7.58 Billion |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stock Photography Market Analysis by Mordor Intelligence

Stock photography market size in 2026 is estimated at USD 5.44 billion, growing from 2025 value of USD 5.09 billion with 2031 projections showing USD 7.58 billion, growing at 6.86% CAGR over 2026-2031. Demand resilience comes from marketers’ preference for licensed images in omnichannel campaigns, even as generative-AI models create inexpensive visual substitutes. Platform operators answer this competitive pressure by deepening subscription penetration, embedding image libraries inside design software, and nurturing premium collections that spotlight exclusive editorial and diverse lifestyle content. Mergers and acquisitions accelerate because scale is now central to negotiating AI-training licences and to underwriting the high fixed costs of automated tagging, search, and compliance infrastructure. Geographic growth spreads most quickly through Asia-Pacific, where mobile-commerce sellers and creator start-ups view paid imagery as a revenue lever rather than a discretionary spend item. Across segments, short-form video assets, enhanced royalty-free licence bundles, and microstock distribution channels register the steepest unit-demand curves.

Key Report Takeaways

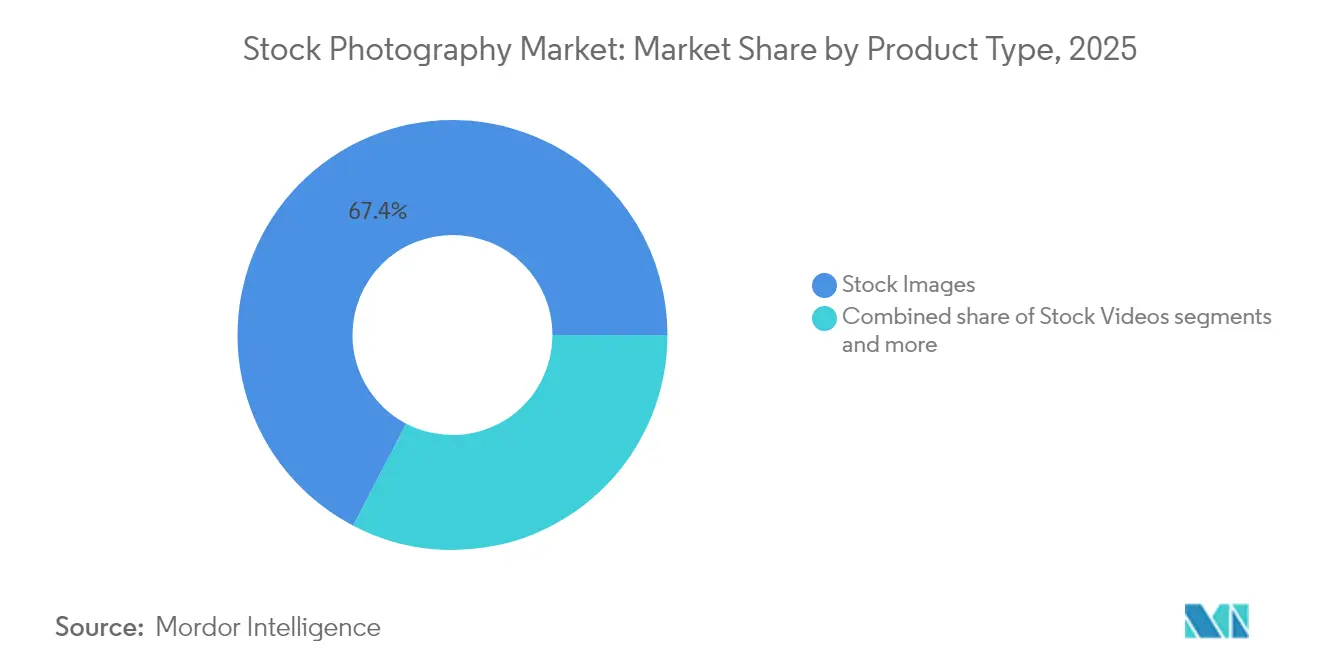

- By product type, Stock Images led with 67.35% of stock photography market share in 2025, while Stock Videos are on track for an 8.29% CAGR through 2031.

- By licence type, Royalty-Free dominated at 71.65% share in 2025; Extended RF is pacing for 7.78% CAGR to 2031.

- By source model, Macrostock held 60.35% share of the stock photography market share in 2025; Microstock is expanding at a 7.62% CAGR.

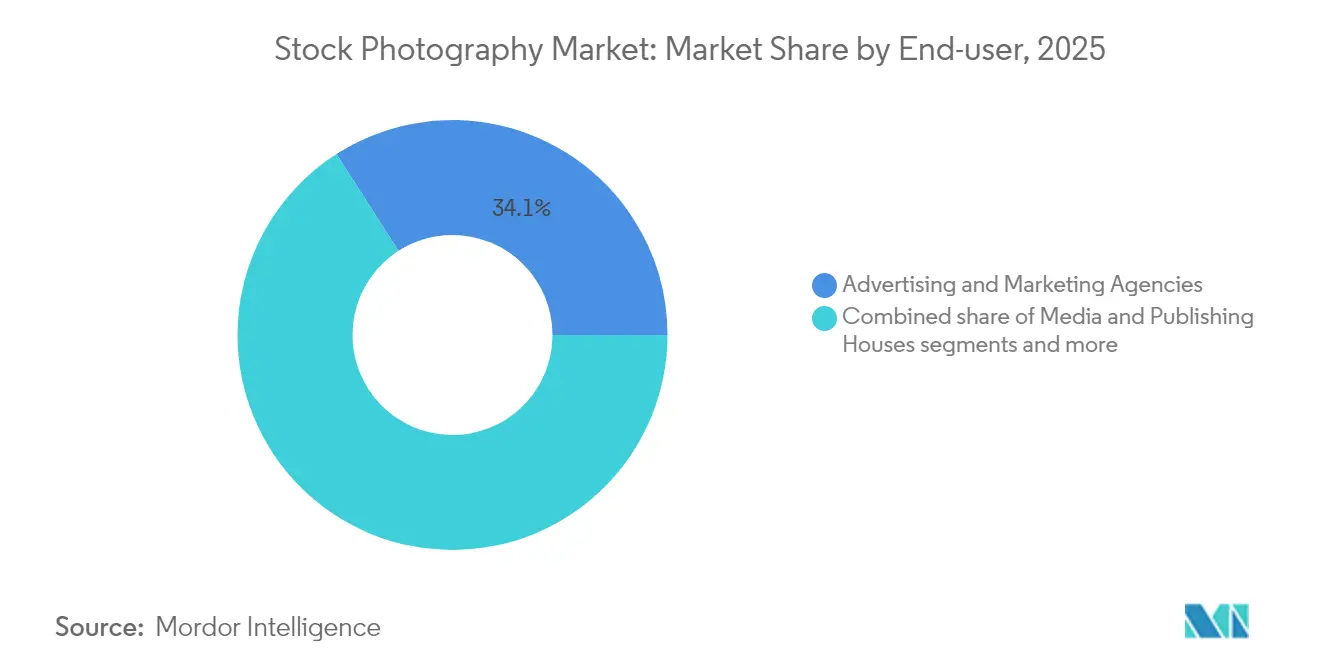

- By end-user, Advertising and Marketing Agencies accounted for 34.08% revenue share in 2025, whereas Corporate and SMB Creators show the fastest CAGR at 7.34%.

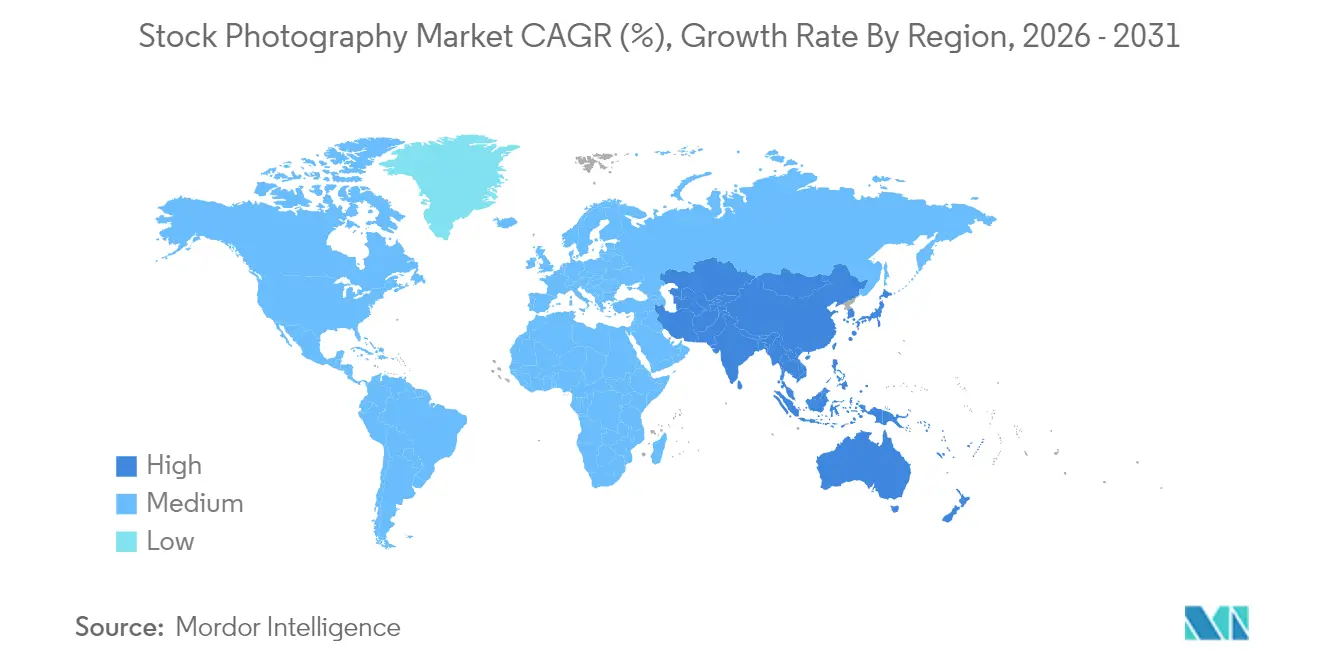

- By geography, North America retained leadership with 37.75% share in 2025; Asia-Pacific is poised for a 7.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stock Photography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for digital-first marketing content | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| SME penetration into paid visual-content marketplaces | +1.5% | Asia–Pacific core, extension into Latin America and MEA | Long term (≥ 4 years) |

| Rapid rise of subscription and credit-based pricing | +1.2% | Global, led by mature markets | Short term (≤ 2 years) |

| Surge in short-form video marketing fuels stock-video uptake | +1.0% | Global, early adoption in North America and Asia–Pacific | Medium term (2-4 years) |

| Generative-AI hallucination risks intensify need for licensed imagery | +0.8% | Global, concentrated in regulated industries | Short term (≤ 2 years) |

| ESG-driven demand for inclusive and diverse visuals | +0.6% | North America and Europe, expanding into Asia–Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for digital-first marketing content

Enterprises broaden omnichannel campaigns, placing licensed visuals at the centre of website, social, and mobile experiences. Adobe reported USD 15.86 billion in 2024 Digital Media revenue, aided by Creative Cloud users who buy images without leaving their design interface[1]Adobe, “Adobe Reports Record Fourth Quarter and Fiscal 2024 Results,” adobe.com. Always-on programmatic advertising magnifies asset turnover, so creative teams prioritise speed more than cost, favouring all-inclusive subscriptions that remove per-item approvals. As budgets shift from one-off shoots to repeat licensing, platform annual recurring revenue ratios rise, and churn falls. Demand also spills into in-house corporate studios, meaning the addressable audience now covers both professional agencies and operational marketers.

SME penetration into paid visual-content marketplaces

Small and mid-size enterprises are the fastest-scaling buyer class because low-cost design software turns marketing staff into creators. Microstock-library breadth plus transparent licence language makes paid imagery less intimidating for non-experts. Getty Images counted almost 720,000 active customers in 2024, with outsized growth in sub-USD 10,000 spend tiers. In emerging economies, merchants jump directly into social-commerce advertising and skip traditional agency intermediaries, so basic subscription bundles fit tight cash cycles. As these firms mature, they upgrade into extended usage rights, bolstering average revenue per account.

Rapid rise of subscription and credit-based pricing

Recurring licences now underwrite more than half of gross billings at leading vendors; Getty’s annual subscriptions reached 54.9% of total revenue in 2024. Customers embrace operating-expense models that match SaaS spend norms and simplify forecasting. Credit packs give intermittent users budget control, yet still lock them into a committed payment cycle. Tiered plans open upgrade paths to larger download quotas, video add-ons, or indemnification clauses, helping platforms lift lifetime value. The model reduces internal sales friction because purchases clear under standing purchase orders rather than per-project approvals.

Surge in short-form video marketing fuels stock-video uptake

Algorithm preference at TikTok, Instagram Reels, and YouTube Shorts centres on video, pushing marketers toward motion assets. Stock Videos grow at 8.7% CAGR by 2030, more than the headline stock photography market rate. Creators seek cost-effective material to avoid live shoots that require specialised equipment and talent. Software editors now automate captioning, colour correction, and aspect-ratio output, letting non-technical staff repurpose clips quickly. Libraries answer with tightly curated 15- to 60-second footage packs that mirror platform length standards, solving the creative-fit problem and commanding higher per-download fees than images.

Generative-AI hallucination risks intensify need for licensed imagery

Synthetic-image tools sometimes embed brand artefacts or yield inconsistent subject representation, exposing users to trademark and defamation threats. Regulated industries lean toward pre-cleared libraries to mitigate that legal uncertainty. Platforms respond by offering indemnification, model-release documentation, and provenance metadata that prove non-infringement. The content-verification premium protects prices even as AI lowers production costs elsewhere. AI training deals also create new revenue lanes, with Shutterstock earning USD 104 million from licensing archives to model builders in 2024.

ESG-driven demand for inclusive and diverse visuals

Brands face stakeholder scrutiny on representation accuracy, so they plan campaigns around diverse age, ethnicity, ability, and gender imagery. Suppliers invest in contributor-recruitment programs targeting under-represented communities and curate collections labelled for inclusive themes. European Union corporate-sustainability disclosure rules, rolling in over the next 2 years, embed visual inclusivity within broader reputation-risk controls, lifting demand for audited content sets. Resulting differentiation helps fend off undifferentiated free imagery that rarely meets such criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of free and freemium image libraries | -1.5% | Global, higher in price-sensitive markets | Short term (≤ 2 years) |

| Concerns over originality and visual fatigue | -0.8% | Mature markets with high stock-photo usage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of free and freemium image libraries

Open-source photo repositories and AI generators reset price anchors to zero for generic themes, forcing premium platforms to justify fee structures through exclusivity and reliability. CEPIC estimates that a 5%-15% demand shift toward free alternatives could erase USD 232 million-USD 698 million in annual industry takings[2]CEPIC, “Generative AI Impact Study,” cepic.org. Higher-value providers retaliate by investing in curation, legal indemnity, and API integrations that freemium sites rarely match. Some microstock portals lower entry-level tiers yet reserve editorial, celebrity, and rights-expanded packages as upsell shields against erosion.

Concerns over originality and visual fatigue

Audiences recognise widely circulated stock shots, diluting engagement metrics and diminishing brand distinctiveness. Agencies thus brief for imagery that feels candid, location-specific, and culturally aligned. Platforms counter fatigue with dynamic search-rank algorithms that surface new uploads more frequently and with contributor incentive schemes rewarding unique perspectives. The restraint also incubates niche micro-libraries that specialise in hyper-local or sub-cultural content. Mainstream vendors answer by incubating contributor academies and commissioning exclusive series, refreshing catalogue turnover and alleviating sameness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Videos Drive Premium Growth

Stock Images retained a 67.35% revenue lead in 2025, translating into USD 3.43 billion of stock photography market size, yet their unit-growth curve has flattened as penetration approaches maturity. The segment still benefits from fast-moving e-commerce listings, low bandwidth, and established creative workflows. Continued earnings rely on subscription renewals, AI-assisted similarity search, and contributor programmes that fill representation gaps.

Stock Videos, meanwhile, post an 8.29% CAGR that lifts the segment to USD 2.03 billion by 2031, equivalent to 26.78% of the projected stock photography market size. Marketing teams choose royalty-free clips to populate product explainers, event teasers, and user-generated content remixes without incurring studio costs. Platforms refine metadata to flag shot length, camera movement, and vertical-format readiness, reducing edit times and raising willingness to pay. Higher average selling prices and lower cannibalisation risk render the video catalogue a margin lever as still-image yields compress.

By Licence: Extended Rights Gain Traction

Royalty-Free structures commanded 71.65% of 2025 turnover, roughly USD 3.65 billion of stock photography market size, due to their simple perpetual-use promises that match enterprise risk tolerance. Vendors bundle usage-clarity assurances and AI-training opt-outs inside these agreements, maintaining perceived value even when basic pictures drift toward commoditisation.

Extended RF licences grow at 7.78% CAGR, capturing clients that syndicate campaigns across multiple geographies and media. In 2025, enhanced packages start at triple the price of basic RF yet contribute a disproportionate margin because incremental legal coverage costs little to deliver. Rights-Managed contracts now occupy a specialist niche—exclusive pharma, high-budget automotive, and prestige editorial work—where scarcity itself underpins price.

By Source Model: Microstock Democratisation Accelerates

Macrostock libraries retained a 60.35% share in 2025, equal to USD 3.07 billion of global stock photography market share, aided by hard-to-replicate editorial archives and long-running agency ties. Operators monetise those assets through subscription tiers that fold in indemnity and curation services.

Microstock channels rise at a 7.62% CAGR because low entry prices and contributor crowds scale rapidly. Flexible credit packs suit creators with uneven posting cadences, while all-you-can-download bundles entice high-volume social-media managers. Shutterstock hosts more than 771 million licensable images, videos, and music tracks on its platform, underscoring the scale advantage microstock platforms have amassed. Automated quality-control algorithms allow platforms to process tens of thousands of daily uploads without bloating manual review teams.

By End-user: Corporate Creators Emerge

Advertising and Marketing Agencies preserved the top slot with 34.08% of 2025 revenue, leveraging multibrand portfolios that generate consistent licence orders. Agencies prefer enterprise-wide subscriptions so account managers can share images across creative pods without raising procurement flags. In response, suppliers build agency-specific dashboards that show attribution, rights expiry, and client-level cost allocation.

Corporate and SMB Creators record a 7.34% CAGR into 2031, adding roughly USD 0.92 billion to the stock photography market size over the period. Brand teams internalise design tasks as template-driven software reduces technical barriers. The move shrinks project cycle times, which in turn encourages bulk-download behaviour and drives upsell to enhanced licences.

By Application: Commercial Dominance Continues

Commercial campaigns accounted for 57.55% of 2025 revenue and are set to climb at 8.12% CAGR as digital-advertising budgets widen. Always-on performance marketing consumes banner variants, social-carousel images, and vertical videos designed to refresh ad fatigue metrics every few days. Extended RF licences lower legal risks when assets appear across programmatic, out-of-home, and event channels simultaneously.

Editorial uses serve newsrooms and documentary filmmakers that need timely, exclusive captures of sports or political events. Growth is slower because output hinges on real-world events; however, pricing remains premium per image. Getty Images noted a 16.1% year-on-year rise in editorial revenue to USD 92.8 million in Q3 2024, demonstrating the enduring value of exclusivity during high-profile news cycles.

Geography Analysis

North America contributed 37.75% of global revenue in 2025, thanks to sophisticated advertising ecosystems and legal systems that make indemnified licences attractive. Enterprise buyers commit to multi-year omnichannel licences to avoid potential trademark disputes, supporting higher average deal sizes. The region’s tech platforms embed stock-image search inside collaborative design suites, streamlining checkout and encouraging platform lock-in.

Europe ranks second and balances high creative sophistication with budget vigilance. Data-privacy directives and collective-bargaining regulations push brands to secure iron-clad model releases before publication, benefiting curated suppliers. Localisation requirements foster demand for culturally specific images that reflect individual member states.

Asia-Pacific records the fastest trajectory at a 7.46% CAGR through 2031. SMB digitisation and social commerce drive constant image refresh cycles. Visual China Group has expanded its regional scale by acquiring international platforms such as 500px, giving Asian buyers easier access to global catalogues. Domestic platforms offer localisation advantages but lack the breadth of global libraries, so many buyers mix international subscriptions with regional add-ons.

Competitive Landscape

The competitive field is consolidating in response to mounting technology costs and AI-driven disintermediation threats. Getty Images announced a USD 3.7 billion agreement to acquire Shutterstock in January 2025. The union intends to secure stronger bargaining power when licensing imagery to generative-AI developers and to rationalise overlapping sales operations.

Platform strategy now orbits ecosystem integration instead of standalone libraries. Adobe integrates its Stock portal directly within Creative Cloud, ensuring designers never exit their workspace to source visuals[3]Adobe, “Adobe Stock Adds AI-Powered Search Updates,” adobe.com. This embedded positioning not only raises switching barriers but also yields granular usage data that informs future content acquisition.

Monetising archives for AI training has emerged as a defensive revenue line. Shutterstock’s USD 104 million in 2024 AI-licence sales validated the model. Smaller niche libraries explore cooperative collectives to negotiate as a bloc rather than as fragmented sellers.

Stock Photography Industry Leaders

Adobe Stock

Visual China Group

Getty Images

Shutterstock

Canva Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Getty Images posted Q4 2024 revenue of USD 247.3 million, up 9.5% year-over-year, with subscriptions at 54.9% of turnover.

- January 2025: Getty Images announced a USD 3.7 billion deal to acquire Shutterstock, forming a combined company pending regulatory approval.

- November 2024: Getty Images’ Q3 2024 filing noted editorial revenue of USD 92.8 million, a 16.1% rise linked to major sporting events coverage.

- July 2024: Shutterstock finalised its USD 245 million purchase of Envato Pty Ltd., broadening its template and digital-asset offerings.

- February 2024: Shutterstock acquired Backgrid Celebrity News Network to deepen entertainment and celebrity editorial coverage.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study measures worldwide gross billings from licensing ready-made photos, short clips, illustrations, and vectors that users download from online libraries for commercial or editorial projects. Values are stated in constant 2024 US dollars.

Scope Exclusion: Custom photo shoots, live-event coverage, and standalone editing software lie outside scope.

Segmentation Overview

- By Product Type

- Stock Images

- Stock Videos

- Stock Illustrations/Vectors

- By License

- Royalty-Free (RF)

- Rights-Managed (RM)

- Extended / Enhanced RF

- By Source Model

- Macrostock

- Midstock

- Microstock

- By End-user

- Advertising and Marketing Agencies

- Media and Publishing Houses

- Film and TV Production

- Corporate and SMB Creators

- Educational Institutions

- Others

- By Application

- Commercial

- Editorial

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Desk Research

We review public filings and investor decks of listed image platforms, usage norms from the Digital Media Licensing Association and the Graphic Artists Guild, UN Comtrade cross-border download flows, national ad-spend series, and SimilarWeb traffic. Company snapshots drawn via Dow Jones Factiva and D&B Hoovers anchor average prices and volumes. These examples are illustrative; several additional open records informed validation.

Primary Research

Mordor analysts interviewed library curators, independent contributors, media-agency buyers, and brand communication managers across North America, Europe, and Asia-Pacific. Dialogues clarified ASP tiers, payout ratios, and the rising demand for video bundles, while two brief surveys checked download frequency inside small firms.

Market-Sizing & Forecasting

We begin with a top-down build linking regional digital-ad outlays, ecommerce storefront counts, and active website-builder subscriptions to observed image-use penetration rates. We then refine totals with bottom-up checks from platform disclosures and royalty roll-ups. Key drivers include license-class ASP shifts, still-to-footage mix, paid share, contributor growth, and ad-spend elasticity. Multivariate regression blended with scenario analysis projects demand through 2030; conservative mid-points from expert calls bridge data gaps.

Data Validation and Refresh Cycle

Separate analyst pairs scan variances, benchmark outputs against external signals, and re-contact sources when quarterly earnings swing beyond ten percent. The model refreshes each year and is updated after material M&A or new rules before final sign-off.

Why Mordor's Stock Photography Baseline Commands Reliability

Published figures differ because some groups fold in AI art, music loops, or design templates; others drop footage, and several convert revenue at spot rates.

By fixing scope, updating annually, and double-checking every assumption, we at Mordor Intelligence deliver a centered, dependable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.09 B (2025) | Mordor Intelligence | - |

| USD 7.19 B (2025) | Global Consultancy A | Adds AI assets & audio loops |

| USD 4.65 B (2024) | Trade Journal B | Excludes footage & vectors |

| USD 3.74 B (2024) | Research Publisher C | Counts only paid downloads on select sites |

These contrasts show totals swing when scope or pricing shifts. Anchoring estimates to transparent variables and fresh primary insight lets our numbers give decision-makers the clearest starting point.

Key Questions Answered in the Report

What is the current value of the stock photography market in 2026?

The stock photography market size is USD 5.44 billion in 2026 and is forecast to reach USD 7.58 billion by 2031.

Which product segment is expanding the fastest?

Stock Videos lead growth, delivering an 8.29% CAGR through 2031 on the back of short-form social-media advertising trends.

How important are subscriptions to platform revenue models?

Subscriptions account for 54.9% of Getty Images’ revenue and a comparable share at other leading vendors, confirming their dominance in platform monetisation.

Why is Asia-Pacific attracting attention from global stock photo providers?

The region’s 7.46% CAGR stems from rapid SMB digitisation, social-commerce penetration, and growing creator economies that require steady volumes of licensed visuals.

How are stock photography firms responding to generative-AI disruption?

Leading companies license archives for AI-model training, embed indemnification clauses into extended licences, and invest in exclusive editorial content to preserve pricing power.

What impact will the Getty Images–Shutterstock merger have on competition?

The planned USD 3.7 billion transaction would create a combined catalogue and buyer base large enough to influence pricing and licence terms across the global market.

Page last updated on: