Stand-Up Paddle Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

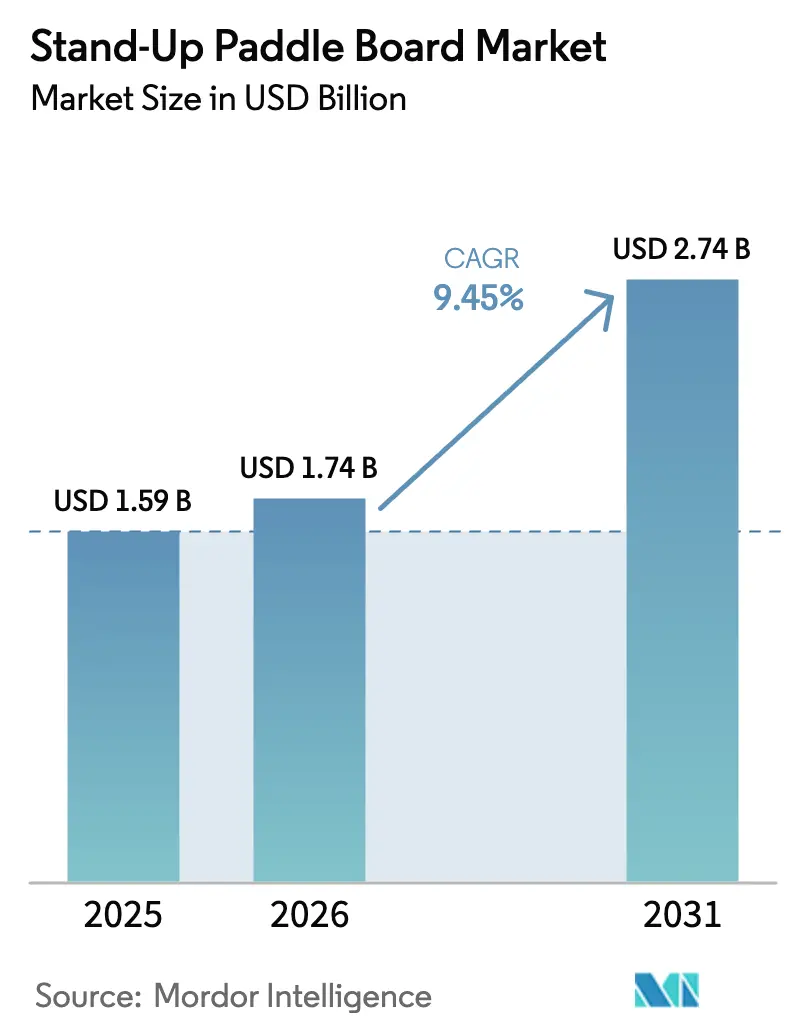

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

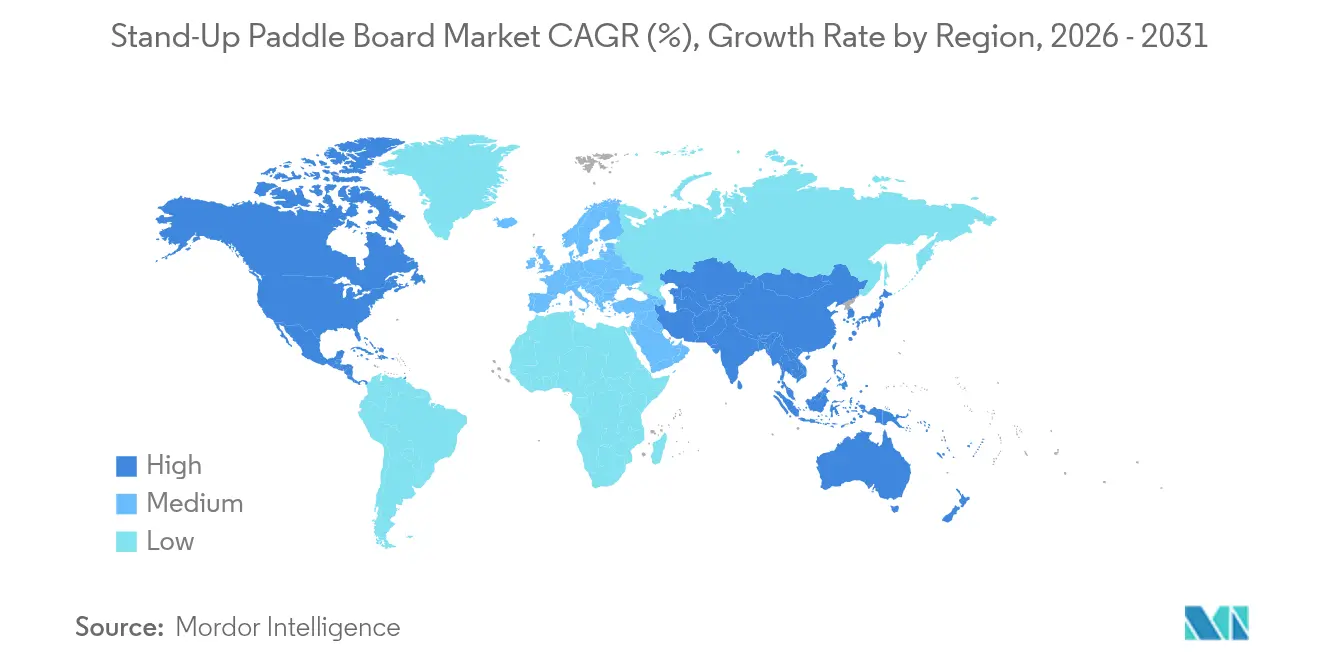

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stand-Up Paddle Board Market Analysis by Mordor Intelligence

The stand-up paddle board market size in 2026 is estimated at USD 1.74 billion, growing from 2025 value of USD 1.59 billion with 2031 projections showing USD 2.74 billion, growing at 9.45% CAGR over 2026-2031. Momentum comes from the sport’s shift into mainstream fitness, tourism and corporate wellness channels, coupled with advances in inflatable construction, carbon-fiber composites and emerging hybrid propulsion kits. Rental operators are scaling fleets to meet rising visitor volumes at lakes, rivers and coastal resorts, while government “blueway” projects in North America, Europe and Australia expand safe water access. Competitive intensity remains moderate as established brands defend share through technology upgrades and sustainability credentials, yet new entrants leverage e-foil integration and up-cycled materials to capture premium niches. These structural trends position the stand-up paddle board market for sustained expansion, even against seasonality, insurance cost pressures and evolving micro-plastics regulation[1]Fáilte Ireland, “Minister Catherine Martin announces investment in Acres Lake Water Sports facility,” failteireland.ie.

Key Report Takeaways

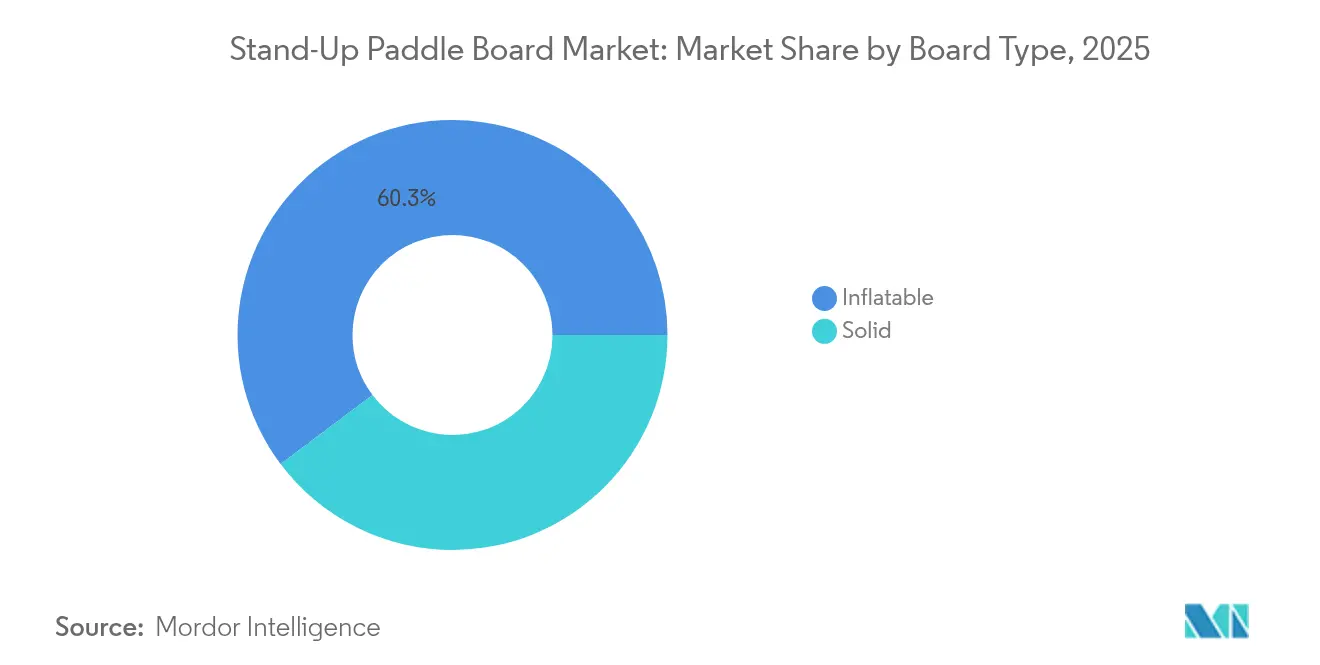

- By board type, Inflatable products led with 60.25% of the stand-up paddle board market share in 2025.

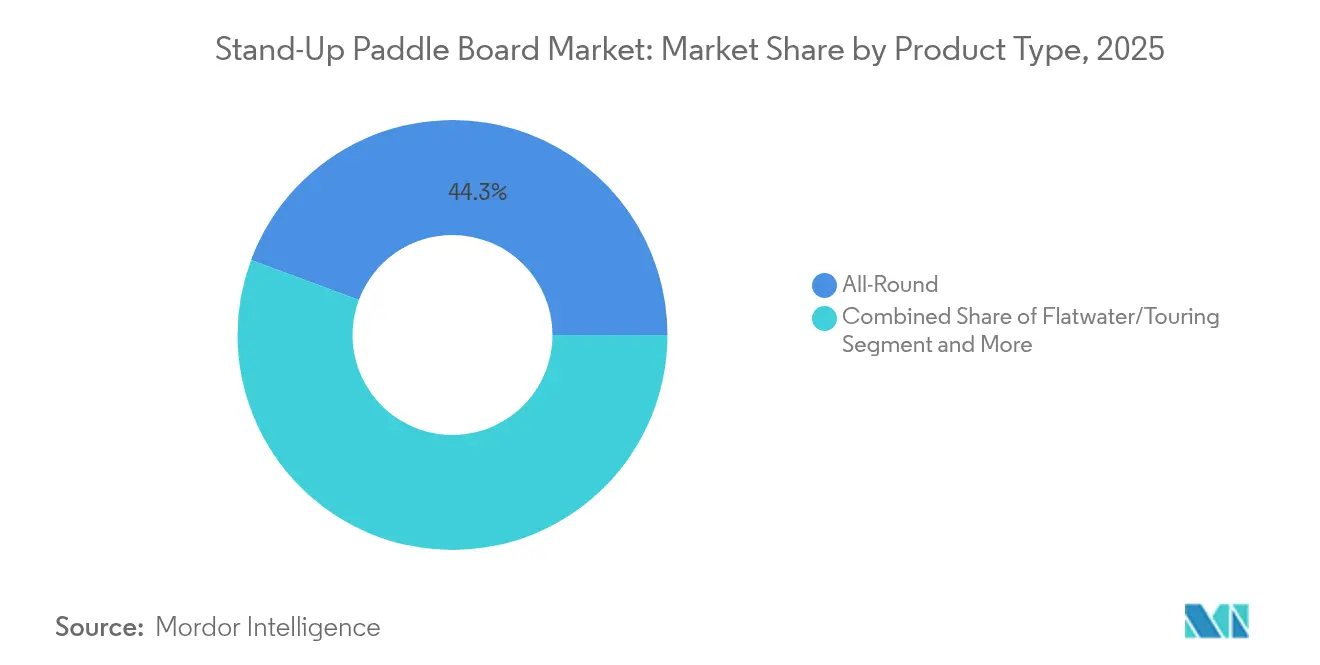

- By product category, All-round boards commanded 44.32% share of the stand-up paddle board market size in 2025, while race boards will post the fastest 10.95% CAGR to 2031.

- By material, Plastic / PVC captured a 69.20% share in 2025; carbon-fiber composites are advancing at a 11.32% CAGR.

- By application, Recreational / touring accounted for 39.40% of the stand-up paddle board market size in 2025; fitness / yoga is forecast to expand at 10.78% CAGR through 2031.

- By geography, North America held 42.60% of 2025 revenue; Asia-Pacific is the fastest-growing territory at 9.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stand-Up Paddle Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in outdoor fitness and wellness tourism | +2.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Convenience and portability of inflatable SUPs | +2.2% | Global, strong in Asia-Pacific urban markets | Short term (≤ 2 years) |

| Expanding rental fleets at coastal and lake resorts | +1.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Integration with hybrid e-foil propulsion | +1.5% | North America and Europe premium markets | Long term (≥ 4 years) |

| Corporate wellness and team-building adoption | +1.1% | Global urban centers | Medium term (2-4 years) |

| National “blueways” infrastructure investments | +0.8% | Ireland, US, Canada, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising participation in outdoor fitness and wellness tourism

Wellness tourism is expanding faster than mainstream travel, and operators now package paddleboard experiences alongside yoga, mindfulness and healthy-food retreats. Queensland and New South Wales tourism boards promote SUP classes on sheltered waterways, while European river-towns add guided excursions that extend visitor stays. Consumer discovery accelerates through social platforms showcasing balanced poses on boards, amplifying word-of-mouth reach. Lifestyle brands partner with outfitters to stage pop-up events that merge apparel launches with on-water sessions, embedding paddleboarding into aspirational fitness narratives. This year-round tourism mix smooths demand beyond summer peaks and lifts the stand-up paddle board market in shoulder seasons.

Convenience and portability of inflatable SUPs

Advances in drop-stitch, double-layer PVC and 3K carbon-rail laminates eliminate earlier rigidity gaps, letting inflatables fold into backpack-sized rollers that fit small cars and city apartments. Weight now averages 18–25 lb versus 30 lb for traditional epoxy boards, widening appeal among commuters and travelers. Urban retailers report higher conversion where storage space ranks as a top barrier to ownership. Materials such as AirLite TPU woven fabric boost tensile strength while reducing petro-chemical content, supporting sustainability claims that sway eco-conscious buyers. These improvements keep the stand-up paddle board market on a steep adoption curve in dense metros.

Expanding rental fleets at coastal and lake resorts

Rental businesses typically recover upfront board costs within one high-traffic season because durable inflatables withstand repeated use and low maintenance. Government-backed waterfront grants, such as Ireland’s Acres Lake facility, add docks, lockers and interpretive signage that lower operator capex and streamline permitting. Economic-impact studies on the Tennessee RiverLine forecast USD 48.3 million in incremental visitor spending tied to paddlesports each year[2]Garth Baker, “Tennessee RiverLine Economic Impact Study,” bakercenter.utk.edu. Start-ups leverage online booking software and mobile point-of-sale tools to optimize fleet utilization and handle dynamic pricing. These elements collectively widen market access for first-time participants and reinforce repeat usage among tourists, underpinning steady growth in the stand-up paddle board market.

Integration with hybrid e-foil propulsion

Electric propulsion kits retrofit beneath the board or foil mast, delivering silent thrust that reduces fatigue and opens the activity to older or mobility-limited enthusiasts. Lift Foils’ LIFT5 system offers modular batteries and Bluetooth hand controllers, while Foil Drive’s lightweight pod grants 40-minute assist to conventional foils. SUP brands respond by adding aluminum mount plates and watertight cable channels at the manufacturing stage. Premium pricing, often exceeding USD 10,000 for complete e-foil packages, lifts average selling prices and stimulates complementary accessories such as high-capacity chargers. As battery density improves, hybrid models may claim a distinct performance category that elevates the stand-up paddle board market’s technology profile.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality causing cash-flow volatility | -1.8% | Northern temperate regions, North America and Northern Europe | Short term (≤ 2 years) |

| Price sensitivity vs. entry-level kayaks and surfboards | -1.2% | Global, stronger in emerging markets | Medium term (2-4 years) |

| Micro-plastics regulations impacting PVC supply | -0.9% | Europe, North America | Long term (≥ 4 years) |

| Insurance premium hikes for rental operators | -0.6% | Developed markets with liability frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonality causing cash-flow volatility

Rental outlets in Canada, the northern United States and Scandinavia compress revenue into a June-to-September window, yet fixed costs such as storage leases and liability premiums accrue year-round. Daily peak-season yields can hit USD 350 per board, but winter utilization often drops to zero, stressing working-capital lines. Operators with multi-location footprints mitigate exposure by shifting surplus inventory to warmer states or Caribbean franchises, whereas single-site owners increasingly partner with ski resorts to cross-rent snow gear during off-season months. A tightening credit environment magnifies risk, prompting consolidation that ultimately favors larger participants in the stand-up paddle board market.

Price sensitivity vs. entry-level kayaks and surfboards

A first-time rigid SUP package still averages USD 900, nearly double the out-the-door cost of an entry kayak. Emerging-market consumers often select used surfboards at USD 300 rather than commit to premium inflatable kits. Manufacturers respond with value lines using single-layer PVC and aluminum paddles yet face negative reviews when durability disappoints. Subscription models and lease-to-own programs by specialty retailers aim to convert hesitant buyers, but sustained currency weakness in parts of South America and Southeast Asia continues to dampen discretionary spending. This pricing tension limits upside in the stand-up paddle board market’s lower mid-tier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Versatile All-Round Boards Anchor Adoption

All-round boards held 44.32% of 2025 revenue as their balanced width and rocker profiles cater to beginners and multi-purpose paddlers. Retailers promote bundles that combine leash, pump and adjustable paddle, simplifying first purchase decisions. The stand-up paddle board market size for all-round models is projected to grow at 7.55% CAGR, closely tracking overall industry performance. Race boards, in contrast, are expected to lift at 10.95% CAGR, catalyzed by a rising calendar of sanctioned events and growing engagement from triathletes seeking cross-training options. Brands invest in displacement hull designs and carbon sandwich laminates to shave weight and improve glide, commanding ASPs above USD 2,500.

Demand for surf-specific SUPs remains niche yet resilient in Hawai‘i, California and Portugal, where dedicated breaks and coaching services sustain year-round usage. Touring designs between 11 ft 6 in and 14 ft notice steady orders from expedition outfitters who market multi-day river trips. These sub-categories generate incremental margin by upselling dry bags, GPS mounts and carbon paddles, reinforcing accessory pull-through across the stand-up paddle board market.

By Material Type: PVC Scale Meets Carbon-Fiber Innovation

Plastic/PVC continues to dominate at 69.20% share because drop-stitch inflatables allow economical high-volume production and compact shipping. Heat-fusion methods replace glues, cutting labor input and VOC emissions while lifting bonding strength. The stand-up paddle board market share for PVC inflatables exceeded 60% in every major region during 2025. Yet, carbon-fiber composites post the fastest 11.32% CAGR as performance paddlers upgrade to stiffer, lighter constructions.

Manufacturers such as NOTOX employ reclaimed aerospace scrap blended with bio-epoxies containing 56% plant-based carbon, illustrating how ecological credentials align with top-tier race board needs. Cost remains a barrier, but scaling autoclave and vacuum-infusion capacity at Asian contract laminators is narrowing the premium. Hybrid lay-ups that sandwich flax or basalt between carbon sheets further cut material cost while appealing to environmentally mindful buyers. These advances shift perception of carbon from exotic option to attainable upgrade, setting a new trajectory within the stand-up paddle board market.

By Board Type: Inflatable Design Defines the Growth Curve

Inflatable technology captured 60.25% revenue in 2025 and is slated for 10.12% CAGR through 2031, as portability aligns with apartment living and car-share mobility. Manufacturers pioneered 3K carbon side rails that raise torsional rigidity by 25%, easing sprint starts and choppy-water stability. Many suppliers now pre-laminate graphics within PVC laminates to prevent delamination, prolonging rental life cycles. The stand-up paddle board market size for inflatable models is estimated to surpass USD 1.73 billion by 2031.

Rigid epoxy and carbon boards keep strategic importance in wave, river-surf and elite racing circuits where split-second acceleration outweighs storage convenience. Some brands deploy modular bolt-together designs that reduce shipping dimensions and permit quick deck-pad replacements after heavy commercial use. This coexistence ensures both technologies push material science forward, benefitting the wider stand-up paddle board market.

By Application: Recreation Leads, Fitness and Yoga Accelerate

Recreational/touring retained 39.40% of 2025 value because families and holidaymakers view SUPs as a safe, low-skill activity requiring minimal instruction time. Outfitters standardize on wide 32-in platforms with soft deck pads that handle diverse weight ranges. Events like full-moon paddles and wildlife viewing tours extend demand beyond midday sun hours. Conversely, fitness/yoga posted the strongest 10.78% CAGR as studios introduce floating classes that command premium session fees. Anchoring kits with detachable D-rings enable quick conversion of general-purpose boards into stable practice platforms, spurring accessory revenue.

Fishing SUPs serve a growing, if specialized, user base who appreciate stealth access to shallow flats unreachable by small boats. Add-ons such as swivel chairs and cooler mounts raise ticket size, while inflatable hulls deflect knocks from submerged logs. Racing applications interlink with national series that now stream heats on social media, raising athlete profiles and sponsor interest. This varied use-case landscape diversifies revenue streams, cushioning the stand-up paddle board market against any single segment slowdown.

Geography Analysis

North America accounted for 42.60% 2025 revenue, benefiting from decades of recreational infrastructure plus corporate wellness budgets that subsidize lessons and event days. Projects such as the Tennessee RiverLine aim to draw nearly 808,000 new paddlers annually, injecting USD 48.3 million into local economies. Urban “blueway” networks in Baltimore and Milwaukee repurpose industrial channels for human-powered craft, broadening participation among inner-city residents. Canada amplifies growth through provincial tourism grants that underwrite board purchases for outfitters in Ontario’s lake country.

Asia-Pacific delivers the fastest 9.48% CAGR to 2031, lifted by rising disposable incomes and social-media exposure that converts viewers into first-time renters. Australia remains the region’s innovation hub, pairing SUP tours with Great Barrier Reef conservation education that resonates with eco-tourists. Japan and South Korea lean toward premium composite boards aimed at wealthy hobbyists seeking lightweight performance. Meanwhile, India and parts of Southeast Asia unlock high-volume potential as coastal states improve water-quality monitoring and life-saving services, key enablers for the stand-up paddle board market.

Europe sustains balanced expansion through well-funded outdoor programs and stringent environmental policies that spur uptake of recycled materials. Ireland’s EUR 1.2 million Acres Lake facility complements a broader EUR 20 million Outdoor Recreation Infrastructure Scheme that stresses community access. Nordic nations pioneer certification standards for bio-based resins, while Mediterranean resorts lengthen paddling seasons by offering dry-suit rentals. This regulatory and climate diversity supports a resilient customer base across the stand-up paddle board market.

Competitive Landscape

The competitive field remains moderately fragmented. Top names—Red Paddle Co, Starboard and BOTE—leverage multi-channel distribution and distinct brand narratives to defend shelf space. Red Paddle Co’s patented RSS battens and MSL construction exemplify sustained R&D investment that locks in perceived quality. Starboard collaborates with the Carbon Fibre Circular Alliance to recycle manufacturing scrap, strengthening ESG scorecards that resonate with European retailers. BOTE differentiates through lifestyle storytelling around fishing and over-water camping, bundling boards with inflatable docks and modular coolers.

Contract manufacturers such as Cobra International supply lamination expertise to emerging labels, lowering entry barriers while keeping tooling costs manageable. Cobra recently hired a composites specialist to expand capacity for next-generation electric foiling surfboards, underlining vertical integration trends. Technology disruptors enter via propulsion; Lift Foils partners with marine-battery vendors to upgrade range and safety certifications, raising performance expectations across the stand-up paddle board market.

Regional players carve out niches: Germany’s Lightboardcorp emphasizes ultra-light flax-carbon hybrids; China’s Huarui Plastics scales private-label inflatables for global e-commerce sellers. Strategic moves include product-suite expansions into cooler backpacks, carbon paddles and electric pumps that fortify brand ecosystems and discourage customer churn. As top five suppliers command under 35% combined revenue, innovation cycles and marketing agility decide future rankings.

Stand-Up Paddle Board Industry Leaders

Red Paddle Co.

Tahe Outdoors (BIC Sport)

Naish International

Starboard

SUP ATX

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Paddling Magazine highlighted five material and digital innovations poised to reshape paddlesports equipment.

- February 2025: Gurit Holding AG posted CHF 431.7 million 2024 sales, outlining higher marine composites allocations toward recycled PET cores.

- January 2025: Johnson Outdoors recorded USD 592.8 million 2024 sales and reiterated commitment to watercraft innovation despite top-line softness.

- January 2025: Aqua Marina unveiled its 2025 catalogue featuring AirLite TPU woven fabrics and high-frequency-weld seams.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the stand-up paddle board market as all new boards built for standing propulsion with a single-bladed paddle, spanning hard epoxy, composite, and inflatable constructions sold through consumer and rental channels worldwide. The assessment captures value generated from the first retail sale; accessories are excluded unless bundled with the board.

Scope exclusion: used or refurbished boards, paddles sold on a standalone basis, foil-assisted craft, and kayak-conversion kits remain outside this baseline.

Segmentation Overview

- By Product Type

- All-Round

- Flatwater/Touring

- Race

- Surf

- By Material Type

- PVC

- Epoxy

- Fiberglass

- Plastics (HDPE/ABS)

- Carbon Fiber Composites

- By Board Type

- Solid

- Inflatable

- By Application

- Surfing

- Touring / Cruising

- Racing

- Fitness / Yoga

- Fishing and Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with board shapers, inflatable OEMs, specialty retailers, rental operators, and seasoned paddlers across North America, Europe, and Asia-Pacific. Interviews clarified typical average selling prices, seasonal rental ratios, and how fitness-oriented cohorts are enlarging the touring segment, letting us adjust desk findings and stress-test growth assumptions.

Desk Research

Our analysts first mapped public statistics on outdoor recreation expenditure, water-sports participation, and leisure craft imports from authorities such as the US Bureau of Economic Analysis, Eurostat tourism satellite accounts, and UN Comtrade maritime HS codes. Industry associations, notably the Outdoor Industry Association and Surf Industry Manufacturers Association, provided board shipment trends, while peer-reviewed journals offered injury incidence rates that inform safety-driven demand shifts. Paid datasets, including D&B Hoovers for company revenue splits and Dow Jones Factiva for deal flows, enriched supply-side insights. This list is illustrative rather than exhaustive, and many additional sources were consulted during validation.

Market-Sizing & Forecasting

A top-down demand pool was established from national water-sports participation counts multiplied by board ownership penetration, which is then cross-checked through sampled ASP multiplied by shipment volumes reported by leading suppliers. Core variables include tourism nights spent near calm waterways, consumer disposable income per capita, drop-stitch fabric cost trends, board replacement cycles, and seasonality indices derived from rental fleet utilization. Forecasts rely on multivariate regression supported by expert consensus, and bottom-up supplier roll-ups fill residual gaps when country customs data lack granularity.

Data Validation & Update Cycle

Model outputs pass anomaly checks, variance thresholds, and multi-analyst peer review. Reports refresh each year, and intervening material events, such as regulatory shifts on PVC or sudden tourism rebounds, trigger interim updates before client delivery.

Why Mordor's Stand-Up Paddle Board Baseline Commands Reliability

Published estimates differ because each publisher picks its own product mix, currency timing, and refresh rhythm.

We acknowledge those inevitable gaps upfront.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.59 B (2025) | Mordor Intelligence | - |

| USD 1.90 B (2025) | Regional Consultancy A | Bundles paddles and safety gear, inflates baseline demand |

| USD 1.76 B (2024) | Global Consultancy B | Uses uniform ASP uplift without shipment cross-checks |

| USD 1.45 B (2024) | Trade Journal C | Excludes rental fleet purchases and Asia-Pacific e-commerce sales |

These comparisons show that Mordor's disciplined scope selection, variable-level corroboration, and yearly refresh yield a dependable midpoint for strategic planning, giving clients transparent numbers they can retrace with ease.

Key Questions Answered in the Report

How big is the stand-up paddle board market in 2026?

The stand-up paddle board market is worth USD 1.74 billion in 2026 and is projected to reach USD 2.74 billion by 2031.

Which region leads global demand?

North America holds 42.60% of 2025 revenue thanks to mature infrastructure, extensive waterways and corporate wellness uptake.

Why are inflatable boards growing faster than rigid boards?

Portability, compact storage and advances such as 3K carbon rails make inflatables practical for city dwellers while matching performance needs.

What is the fastest-growing application segment?

Fitness and yoga sessions on paddleboards are set to grow at 10.78% CAGR because wellness tourism and corporate retreats bundle SUP classes.

Who are the top manufacturers?Who are the top manufacturers?

Red Paddle Co, Starboard and BOTE lead through proprietary technology, strong branding and broad dealer networks, but newer e-foil entrants are gaining share.

How does seasonality affect the industry?

Rental businesses in temperate zones must earn most revenue within a 3–4 month window, leading to cash-flow stress and encouraging geographic diversification strategies.

Page last updated on: