Ad Tech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.99 Trillion |

| Market Size (2031) | USD 1.59 Trillion |

| Growth Rate (2026 - 2031) | 10.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

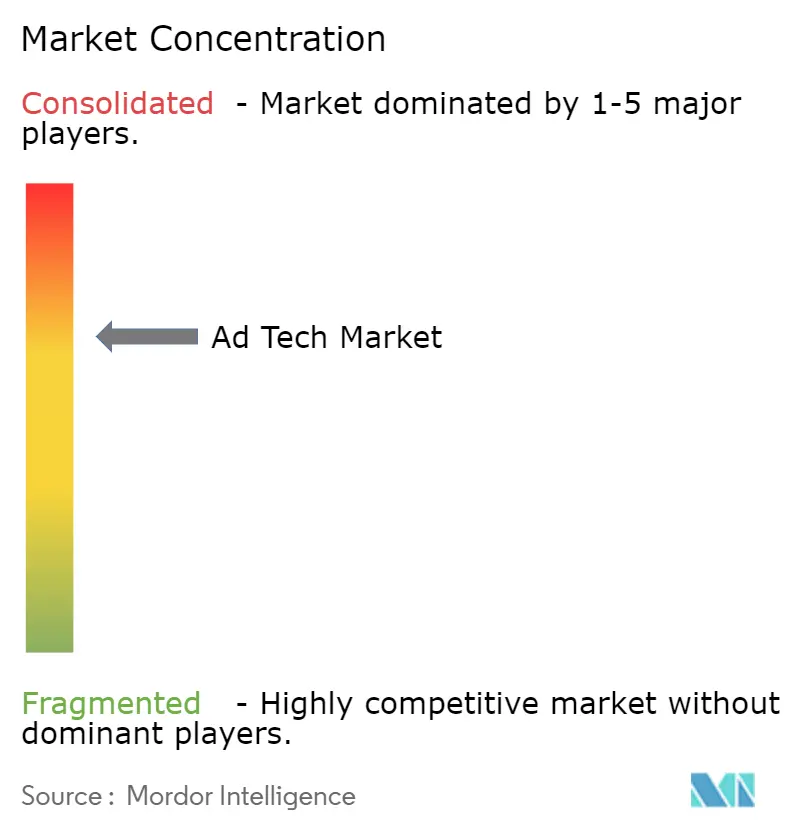

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ad Tech Market Analysis by Mordor Intelligence

The advertising tech market size was valued at USD 0.898 trillion in 2025 and estimated to grow from USD 0.99 trillion in 2026 to reach USD 1.59 trillion by 2031, at a CAGR of 10.05% during the forecast period (2026-2031). The acceleration reflects enduring demand for privacy-compliant programmatic tools, sharp growth in connected-television (CTV) budgets, and large-scale monetisation of retail first-party data. Artificial-intelligence optimisation continues to compress media-buying cycles, while 5G roll-outs in Asia-Pacific unlock high-definition mobile video inventory. Growing scrutiny of opaque supply paths is prompting fee rationalisation across demand-side platforms, and the shortage of data-engineering talent gives well-funded technology vendors a structural edge. Persistent regulatory action in Europe is simultaneously restricting cross-device identifiers and nurturing contextual alternatives, giving rise to a more diversified competitive field.

Key Report Takeaways

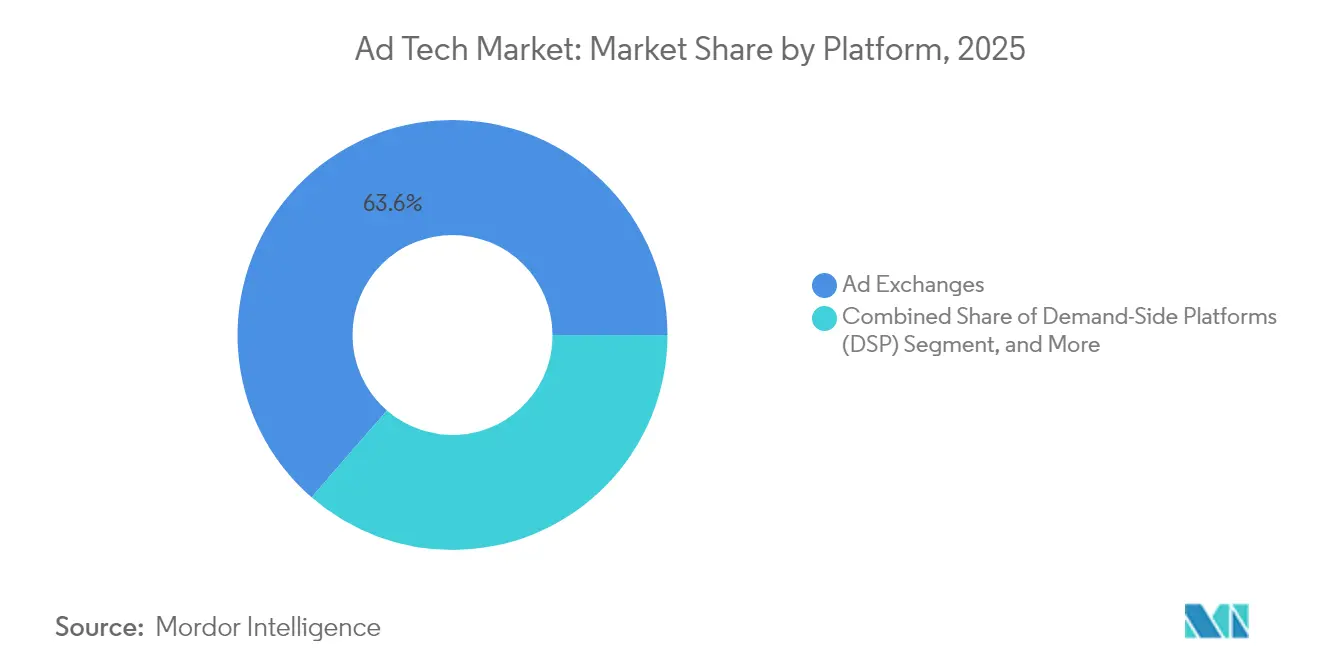

- By platform, Ad Exchanges led with 63.62% of advertising tech market share in 2025; Demand-Side Platforms posted the highest CAGR at 12.08% through 2031.

- By ad format, search advertising held 38.15% revenue share in 2025, while the same category is projected to expand at a 11.92% CAGR to 2031.

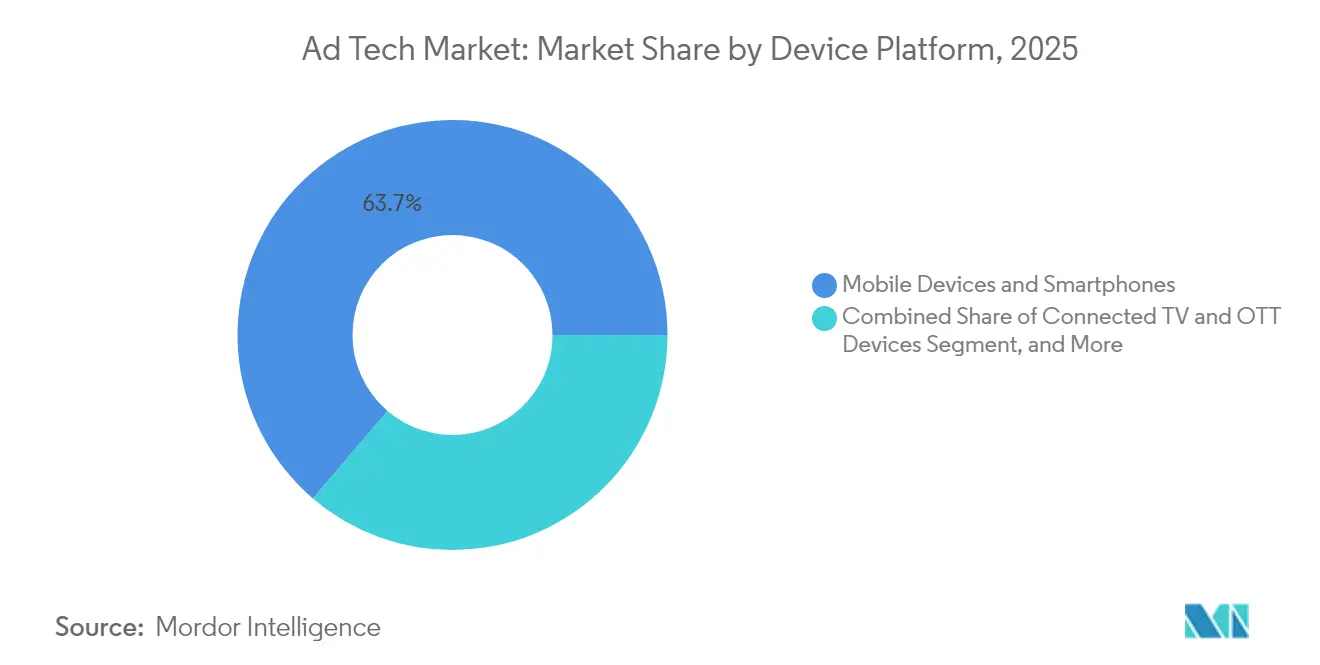

- By device, smartphones accounted for 63.75% of the advertising tech market size in 2025; the “other devices” segment, including smart speakers and wearables, is advancing at a 13.74% CAGR.

- By end-user industry, services represented 51.45% of 2025 spending, whereas telecommunications is forecast to record the fastest 13.88% CAGR.

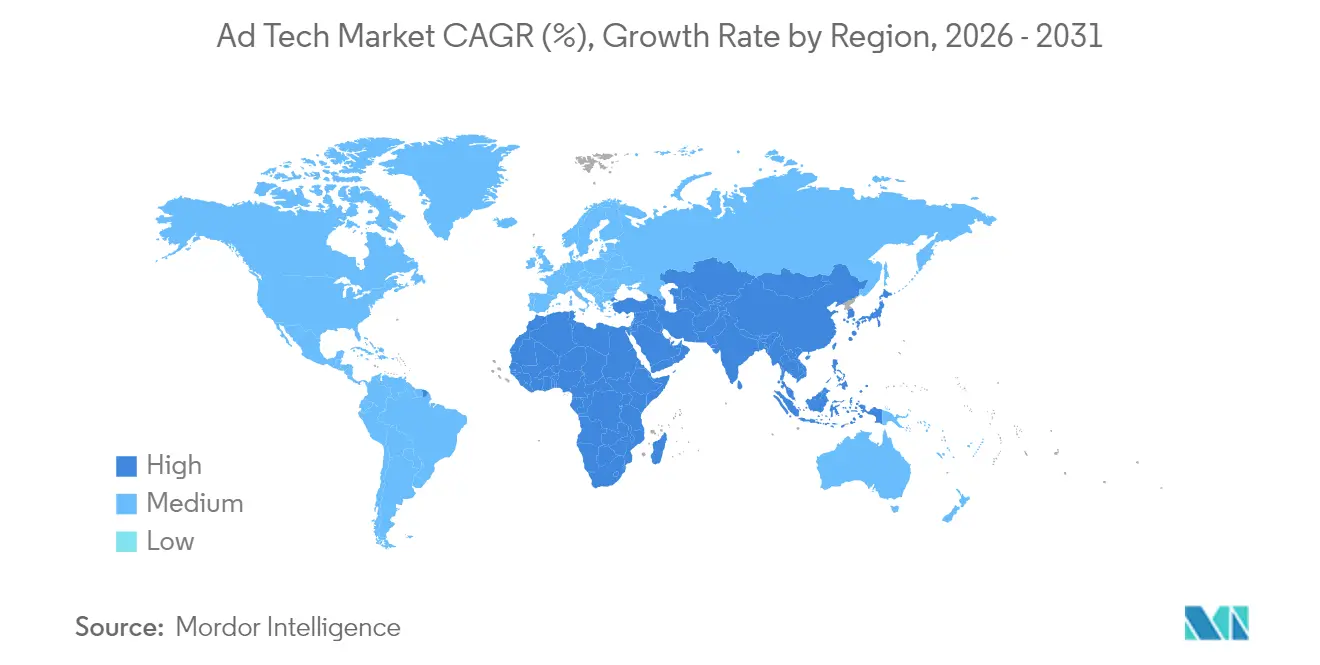

- By geography, North America controlled 40.12% of 2025 revenue, yet Asia-Pacific is set to grow at a 12.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Ad Tech Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CTV-led programmatic surge | +2.1% | North America, global spill-over | Medium term (2-4 years) |

| Deprecation of third-party cookies | +1.8% | Global, early EU adoption | Short term (≤ 2 years) |

| AI-driven dynamic creative optimisation | +1.5% | Global, led by North America & APAC | Medium term (2-4 years) |

| Retail-media monetisation of first-party data | +1.4% | Global, strongest in North America | Long term (≥ 4 years) |

| 5G roll-outs enabling rich mobile video ads | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| GDPR-style regulations fuelling contextual targeting | +0.9% | Europe, expanding to Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CTV-led programmatic surge

Streaming publishers are shifting inventory from direct insertion orders to open auctions, and programmatic CTV now attracts 17% of total brand budgets. The Trade Desk’s Ventura operating system improves frequency capping and audience reach for buyers while lowering publisher tech spend. Convergence with retail-media datasets delivers deterministic attribution that ties viewership to purchases. Over 95% of surveyed advertisers plan to maintain or expand CTV allocations, highlighting resilient demand even amid economic volatility. Platforms with unified ID frameworks gain priority access to premium video placements, which in turn accelerates supply-path optimisation across the advertising tech market.

Third-party-cookie deprecation

Chrome’s phased withdrawal of cookies and the EU’s consent string ruling are accelerating migration to first-party identifiers. Google’s Privacy Sandbox faces yield gaps of up to 33% for publishers during early testing phases.[1]Google, “Frequently Asked Questions Related to Third-Party Cookie Deprecation in Chrome,” google.com Marketers are therefore increasing contextual targeting budgets and adopting clean-room integrations that retain addressability without personal identifiers. Retailers with authenticated transaction data benefit from surging advertiser interest, while smaller publishers exploit semantic-signal models to preserve CPMs. Customer-data-platform deployments have become standard practice for omni-channel brands aiming to future-proof activation workflows.

AI-driven dynamic creative optimisation

Distributed learning algorithms can adapt copy and creative to individual auction contexts in milliseconds, driving double-digit lifts in return on ad spend. Meta has outlined plans to automate the full creative cycle by 2026. The Trade Desk’s Kokai platform pushes predictive clearing logic that continuously reallocates bids toward impressions demonstrating better predicted outcomes. Early adopters report 25% improvements in relevance scores on large retail-media networks. As generative agents become commonplace, future advertising placements are likely to be negotiated directly between brand and consumer AIs, relegating manual optimisation to legacy status.

Retail-media monetisation of first-party data

Retailers are converting high-margin advertising services into core profit pools, with spending expected to exceed USD 100 billion globally by 2027. Amazon alone generated USD 46.9 billion in advertising revenue during 2024, ranking third among digital platforms.[2]Amazon, “Amazon Unveils Simplified Product Launch, Optimisation, and Measurement Solutions,” amazon.com Onsite ad units deliver 70%-90% gross margins and are extending into off-site ecosystems through clean-room collaborations. Standardised attribution frameworks from the IAB now underpin large supermarket networks, improving comparability and attracting incremental brand budgets. Integration with CTV environments closes the loop on omnichannel measurement, driving sustained tailwinds for the advertising tech market.

Restraints Impact Analysis of Ad Tech Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global privacy laws limiting cross-device graphs | -1.3% | Global, strongest in EU | Short term (≤ 2 years) |

| Rising sophistication of ad-fraud | -0.8% | Emerging markets, global spread | Medium term (2-4 years) |

| Supply-path complexity elevating transparency costs | -0.6% | Global, acute in North America | Short term (≤ 2 years) |

| Acute data-engineering talent shortages | -0.5% | Global, most severe in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global privacy laws limiting cross-device graphs

The March 2024 Court of Justice ruling classifies consent strings as personal data, making IAB Europe a joint controller and raising compliance burdens across the supply chain. New obligations under the Digital Markets Act demand clear opt-ins for every data use, eroding performance of cross-device identifiers. Gatekeeper platforms must provide click-level transparency, shifting competitive advantage toward privacy-native contextual solutions. Many large advertisers have capped EU retargeting spend and diverted incremental funds to curated marketplaces, diminishing short-term growth potential in the advertising tech market.

Rising sophistication of ad-fraud

Global fraud losses stood at USD 84 billion in 2023 and are forecast to double by 2028. DoubleVerify logs a 23% rise in new schemes targeting CTV inventory, where higher CPMs amplify pay-off for fraudsters.[3]MediaPost, “DoubleVerify: Generative AI Driving Increase in Ad Fraud,” mediapost.com Generative-AI botnets increasingly mimic human scroll and click patterns, making pattern-based detection harder. Residential IP obfuscation tools provide further cover, raising verification costs. Advertisers that lack unified brand-safety protocols experience up to 17% fraudulent impression rates, directly suppressing effective campaign reach and increasing working-media dilution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ad Tech Market Segment Analysis

By Platform:

Programmatic tools recalibrate buying economicsAd Exchanges delivered 63.62% of 2025 spend, anchoring liquidity across open auctions. Demand-Side Platforms, while smaller, are growing at 12.08% annually as buyers prefer automated optimisations that cut operational overheads. The advertising tech market size captured by DSPs is projected to widen materially through 2031 as enterprise advertisers migrate bulk budgets into self-serve workflows. Amazon’s DSP already accounts for almost one-third of the retailer’s ad turnovers, underscoring the synergies of commerce data with programmatic bidding.

Supply-Side Platforms respond by deepening supply-path optimisation, with PubMatic funnelling more than half of traded impressions through preferential pipes that carry reduced take-rates. Smaller data-management-platform vendors lose relevance when third-party cookies vanish and are either shuttered or absorbed by larger stacks. Microsoft’s planned exit from stand-alone DSP operations illustrates the capital intensity required to keep pace with machine-learning innovation. As competitive barriers climb, platform consolidation is expected, compressing the long-tail provider base inside the advertising tech market.

By Ad Format:

Search retains scale while video acceleratesSearch captured 38.15% of revenue in 2025 and is still expanding at a 11.92% CAGR, leveraging AI-driven multimodal query interpretation to surface commerce-adjacent results. Video formats, buoyed by CTV and mobile apps, siphon incremental brand dollars away from static display. Social media growth is flattening due to tighter content policies, particularly within sensitive health and financial categories.

In-game and augmented-reality placements are embryonic yet show high engagement, attracting exploratory budgets from consumer-electronics brands. Email remains resilient thanks to authenticated data sets that circumvent identifier restrictions. Google’s Gemini platform is expected to embed native search ads into conversational responses, creating fresh inventory pools without disrupting user intent. The advertising tech market continues to evolve from banner impressions toward experience-centric formats that promise measurable outcomes across immersive environments.

By Device Platform:

Smartphones dominate, ambient endpoints emergeMobile devices generated 63.75% of spend in 2025 and will retain the top position through 2031 as 5G services deepen video penetration. Desktop impressions trend marginally downward, reflecting workplace mobility and changing content-consumption patterns. Connected-TV devices benefit from rapid cord-cutting in North America and growing subscription uptake in Asia-Pacific, offering lean-back, brand-safe canvases.

Smart speakers and wearables collectively grow at a 13.74% CAGR, introducing voice and haptic touchpoints that challenge traditional creative workflows. Cross-device measurement is complicated by privacy constraints, prompting the rise of probabilistic modelling within the advertising tech market. Platforms with unified clean-room integrations are therefore best placed to deliver incremental reach without breaching consent frameworks.

By End-user Industry:

Diversification widens the demand baseServices industries captured 51.45% of 2025 budgets, driven by banking, insurance, and professional-services firms competing for digitally native customers. Telecommunications operators are the fastest risers at a 13.88% CAGR as spectrum owners emulate hyperscalers by monetising subscriber graphs. Retail and e-commerce brands expand allocations through onsite sponsored products and off-site display retargeting supported by clean rooms.

Healthcare advertising is cautiously rebalancing creative strategies after large platforms introduced granular limitations on health-condition targeting. Automotive manufacturers pivot messaging toward electric-vehicle benefits, while education providers adapt campaigns to rising online-learning demand. The advertising tech market benefits from this broadening vertical mix, which insulates total spend from cyclical shocks in any single sector.

Geography Analysis

North America Ad Tech Market

North America retained 40.12% of 2025 turnover, supported by mature infrastructure, deep advertiser sophistication, and robust CTV adoption that lifted streaming spend to USD 30.1 billion. Large retail-media networks and advanced identity frameworks reinforce the region’s primacy, even as emerging state privacy statutes add compliance friction. Technology vendors headquartered in the United States account for the majority of intellectual-property filings and attract the bulk of venture funding, further entrenching leadership within the advertising tech market.

APAC Ad Tech Market

Asia-Pacific is the fastest-growing territory at a 12.16% CAGR, propelled by mobile-first consumer behaviour, accelerated 5G coverage, and surging e-commerce activity. GSMA estimates mobile technology contributed USD 880 billion to regional GDP in 2023, with a USD 1 trillion forecast for 2030. China’s super-app ecosystems integrate payments, social, and content, creating blueprints that advertisers in India, Indonesia, and Vietnam are now adopting. Regulatory approaches remain heterogeneous, but most jurisdictions continue to encourage foreign investment in digital media, sustaining long-term momentum for the advertising tech market.

EMEA and South America Ad Tech Market

Europe shows moderate growth as comprehensive privacy laws squeeze cross-device targeting but encourage innovation in contextual and cohort-based models. Retail-media spending is projected to reach EUR 25 billion by 2026 on the back of harmonised measurement protocols. South America and the Middle East and Africa represent early-stage adoption curves characterised by improving broadband penetration and rising local content production. Programmatic spend in South America climbed from USD 5.2 billion in 2017 to USD 16.8 billion in 2023, while the MENA region’s digital advertising outlay is on track to quintuple between 2022 and 2025. These trends confirm a broadening global footprint for the advertising tech market.

Competitive Landscape

Despite ongoing consolidation, the advertising tech market remains moderately fragmented. Oracle’s 2024 exit erased a USD 1.7 billion revenue stream and opened white-space for agile independents. Major deals-Outbrain’s USD 1 billion purchase of Teads, Mediaocean’s USD 500 million Innovid buy, and Equativ’s merger with Sharethrough-highlight the strategic value of vertical integration and differentiated data assets. Technology giants such as Google, Meta, and Amazon retain scale advantages through native user bases and control over key operating-system layers.

Independent platforms differentiate on transparency and privacy leadership. The Trade Desk continues to out-invest peers in machine learning, evidenced by its Kokai and Ventura releases, and maintains open-internet partnerships that bypass walled gardens. Supply-side players prioritise supply-path optimisation to defend publisher yields, while omnichannel measurement providers seek interoperability with retail-media networks. Regulatory pressure intensifies competition around consent-management expertise, prompting traditional agencies to partner with specialised tech vendors to fill capability gaps.

The acute shortage of programmatic engineers amplifies barriers to entry. Larger firms offer superior compensation and remote-work flexibility, draining talent from mid-tier agencies and slowing their roadmap delivery. As AI agents take over manual optimisation, vendors that control proprietary algorithms and authenticated data stand to outpace rivals. The ongoing realignment suggests that by 2030 the advertising tech market will feature a handful of scaled full-stack operators complemented by a layer of vertical specialists focused on identity, creative automation, and outcome-based measurement.

Ad Tech Industry Leaders

Google LLC

Amazon.com, Inc.

Meta Platform, Inc.

Quantcast

Adobe

- *Disclaimer: Major Players sorted in no particular order

Ad Tech Market Companies Covered in this Report

- Alphabet Inc.

- Meta Platforms, Inc.

- Amazon.com, Inc.

- The Trade Desk, Inc.

- Microsoft Corporation

- Adobe Inc.

- Yahoo Inc. (Owned by Apollo Global Management)

- Magnite, Inc.

- PubMatic, Inc.

- Criteo S.A.

- Oracle Corporation

- Index Exchange Inc.

- MediaMath Inc.

- InMobi Pte. Ltd.

- AppLovin Corporation

- Zeta Global Holdings Corp.

- Adform A/S

- Quantcast Corporation

- Rakuten Group, Inc.

- IronSource Ltd. (Merged with Unity Software Inc.)

- StackAdapt Inc.

- Xandr Inc. (Acquired by Microsoft)

- Mediaocean LLC

- OpenX

Recent Industry Developments in Ad Tech Market

- June 2025: Publicis Groupe agreed to acquire Lotame, expanding authenticated identity reach to 4 billion profiles.

- May 2025: Microsoft Advertising confirmed a shift toward conversational formats and will sunset Microsoft Invest DSP by 2026.

- April 2025: The Trade Desk launched Kokai, an AI-powered media-buying platform.

- March 2025: Adobe and Microsoft integrated AI agents within Microsoft 365 Copilot for audience activation.

- February 2025: Equativ merged with Sharethrough, creating one of the largest independent advertising platforms.

- January 2025: T-Mobile announced a USD 600 million acquisition of Vistar Media to boost digital-out-of-home reach

Global Ad Tech Market Report Scope

Advertising technology, or ad tech, is a collection of software and tools advertisers use to reach audiences, analyze their effectiveness, and conduct digital advertising campaigns. Ad tech focuses on developing data-driven marketing strategies tailored to the target audience.

The Ad tech market is segmented by platform (supply-side platform (SSP), demand-side platform (DSP), ad exchange, and data management), by ad format (video advertising, social media, search advertising, email, and other ad formats), by device platforms (desktop, mobile devices and smartphones, and other device platforms), by end-user industry (retail and e-commerce, healthcare, BFSI, services [hospitality, tourism, and legal services], telecommunications, and other end-user industries), and by geography (North America (United States, and Canada), Europe (United Kingdom, Germany, France, Spain, Italy, and Rest of Europe), Asia-Pacific (China, India, Japan, Australia, South Korea, New Zealand, and Rest of Asia-Pacific), Middle East and Africa (Saudi Arabia, United Arab Emirates, South Africa, Nigeria, Egypt, and Rest of Middle East and Africa), and Latin America (Brazil, Mexico, Argentina, Colombia, and Rest of Latin America). The report offers market forecasts and size in value (USD) for all the above segments.

Segmentation Overview

| Demand-Side Platforms (DSP) |

| Supply-Side Platforms (SSP) |

| Ad Exchanges |

| Data Management Platforms (DMP) |

| Others |

| Search Advertising |

| Display/Banner |

| Video Advertising |

| Social Media |

| Others |

| Mobile Devices and Smartphones |

| Desktop and Laptop |

| Connected TV and OTT Devices |

| Other Devices (Smart Speakers, Wearables) |

| Retail and E-commerce |

| BFSI |

| Healthcare and Pharmaceuticals |

| Media and Entertainment |

| IT and Telecommunications |

| Services |

| Automotive |

| Education |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Platform | Demand-Side Platforms (DSP) | |

| Supply-Side Platforms (SSP) | ||

| Ad Exchanges | ||

| Data Management Platforms (DMP) | ||

| Others | ||

| By Ad Format | Search Advertising | |

| Display/Banner | ||

| Video Advertising | ||

| Social Media | ||

| Others | ||

| By Device Platform | Mobile Devices and Smartphones | |

| Desktop and Laptop | ||

| Connected TV and OTT Devices | ||

| Other Devices (Smart Speakers, Wearables) | ||

| By End-user Industry | Retail and E-commerce | |

| BFSI | ||

| Healthcare and Pharmaceuticals | ||

| Media and Entertainment | ||

| IT and Telecommunications | ||

| Services | ||

| Automotive | ||

| Education | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the advertising tech market?

The advertising tech market stood at USD 988.25 billion in 2026 and is forecast to pass USD 1.59 trillion by 2031.

Which region is growing the fastest?

Asia-Pacific leads growth with a 12.16% CAGR through 2031, fuelled by 5G adoption and mobile-first consumer behaviour.

Why are Demand-Side Platforms expanding quickly?

DSPs automate media buying, reducing manual workload and improving bidding efficiency, which drives their 12.08% CAGR.

How are privacy regulations affecting ad-tech?

New laws limit cross-device tracking and force platforms to adopt first-party and contextual approaches, trimming short-term growth but spurring innovation.

What role does retail media play in future growth?

Retail media networks monetise authenticated shopper data and are on track to exceed USD 100 billion in global spend by 2027, adding long-term momentum to the sector.

How significant is ad-fraud to overall spend?

Fraud absorbed USD 84 billion in 2023 and threatens to double by 2028, prompting rising demand for verification and brand-safety solutions within the advertising tech market.

Page last updated on: