Digital Printing For Flexible Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.63 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 11.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Printing For Flexible Packaging Market Analysis by Mordor Intelligence

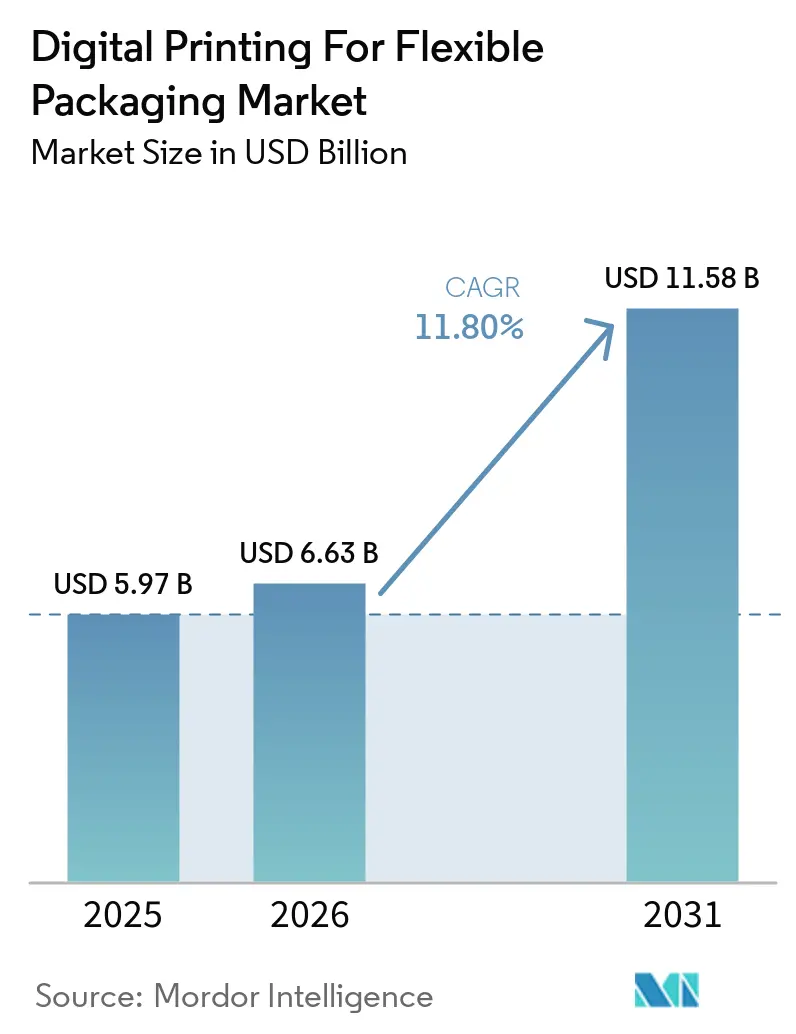

The digital printing for flexible packaging market size is projected to be USD 5.97 billion in 2025, USD 6.63 billion in 2026, and reach USD 11.58 billion by 2031, growing at a CAGR of 11.80% from 2026 to 2031. The main shift comes from shorter production runs, faster artwork changes, and broader SKU portfolios, which make conventional plate-and-cylinder economics less attractive. Brand owners are asking converters to respond faster, which is pushing digital workflows from a specialist option into a regular production tool across many packaging programs. E-commerce demand is also changing the order mix, as regional packs, language variants, and campaign-based formats require shorter lead times and more frequent changeovers. At the same time, recyclable paper structures and stricter food-contact requirements are improving the position of water-based and other compliant digital systems. The biggest opportunity sits with converters that can combine reliable throughput, compliant inks, and flexible commercial models, while the main check on adoption remains the high capital cost of production-grade presses.

Key Report Takeaways

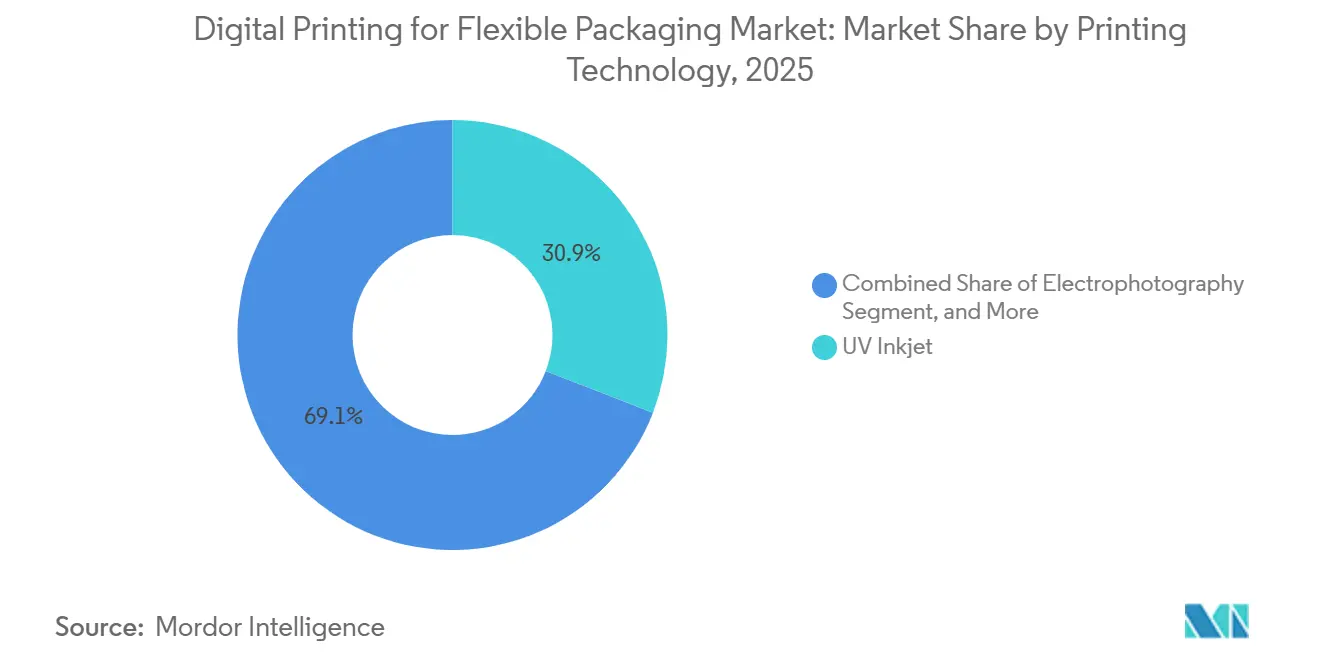

- By printing technology, UV Inkjet captured 30.88% of the digital printing for flexible packaging market share in 2025.

- By packaging type, digital printing for flexible packaging market size for pouches is projected to grow at a 12.74% CAGR between 2026-2031.

- By ink type, water-based inks captured 38.96% of the digital printing for flexible packaging market share in 2025.

- By material type, the digital printing for flexible packaging market is projected to grow at a 14.21% CAGR between 2026 and 2031 for compostable films.

- By end user industry, food applications captured 36.32% of the digital printing for flexible packaging market share in 2025.

- By geography, digital printing for flexible packaging market size for Asia-Pacific is projected to grow at a 13.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Printing For Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-Run SKU Proliferation in Flexible Packs | +2.8% | Global | Short term (≤ 2 years) |

| E-Commerce-Driven Regionalized Packaging Demand | +2.5% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Brand Demand for Variable Data and Mass Customization | +2.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Hybrid Digital Presses Reducing Changeover Waste and Lead Time | +1.9% | Global | Medium term (2-4 years) |

| Low-Migration and Food-Safe Ink Adoption in Regulated Packs | +1.3% | Europe and North America | Medium term (2-4 years) |

| Direct-To-Converter Digital Printing for Micro-Fulfillment and Personalized Medicine | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short-Run SKU Proliferation Drives Volume Economics in Flexible Packs

SKU growth has moved beyond branding activity and now affects production planning, asset use, and converter investment in the digital printing for flexible packaging market. At FTA FORUM INFOFLEX 2026, speakers from Siegwerk, GEW, and Flint Group said brands were placing smaller orders while also asking for faster design-to-shelf execution, which weakens the economics of conventional gravure changeovers. Digital systems avoid physical print forms between jobs, helping converters stay competitive in the run-length range of 10,000 to 15,000 units, which has become harder for analog assets to serve efficiently. That same shift lowers overstock risk, reduces write-offs from obsolete designs, and gives procurement teams a clearer total-cost picture when they compare suppliers in the digital printing for flexible packaging market. The ordering pattern is also changing the direction of demand, as brands are increasingly requiring digital capability as a supply requirement rather than treating it as an optional service. As a result, converter payback periods are being influenced as much by customer pull and order mix quality as by the hardware itself.

E-Commerce Logistics Reshape Regional Pack Formats

E-commerce is changing not only volume but also the number of pack versions, labeling changes, and regional formats that the digital printing for flexible packaging market must support. In China, national packaging standards for express shipments have heightened the need for rapid design updates across a large online seller base, which aligns better with digital production than repeated cylinder changes. In India, quick-commerce grocery models are driving repeat demand for lightweight pouches and sachets that require regional language support, local promotions, and short refill cycles. This matters because online demand does not flow as a single, large order stream; instead, it breaks into many geography-specific, seasonal, and campaign-led SKUs that one converter has to manage simultaneously. European brand owners face a similar issue when aligning common product structures with country-level language and labeling differences, which supports wider adoption of digital printing for flexible packaging. Digital agility, therefore, acts as a supply chain control tool, not only as a print cost tool.

Brand Demand for Variable Data and Mass Customization Accelerates Converter Migration

The center of decision-making has shifted toward brand owners, and that is tightening the adoption cycle in the digital printing for flexible packaging market. In February 2026, HP Inc. and ePac Holdings signed a USD 50 million, 3-year agreement covering the installation of more than 10 HP Indigo 200K presses across North America and Europe, and the plan is expected to place nearly one-third of ePac's global fleet on that platform. HP said the Indigo 200K delivers 30% higher print speed and 45% greater throughput than its predecessor, while also adding automated quality diagnostics and real-time defect detection.[1]HP Inc., “A Decade of Digital Momentum, How HP Indigo and ePac Are Scaling the Future of Flexible Packaging,” HP Inc., hp.com The larger message is that customers, from emerging brands to global consumer goods companies, are specifying digital production more directly, shifting the bargaining position of converters in the digital printing for flexible packaging market. Analog-only converters now face a shorter decision window, as customer expectations are advancing faster than typical equipment replacement cycles. This is likely to keep press installations tied closely to converter partnerships and recurring service revenue.

Hybrid Digital Presses Resolve the Changeover-Speed Trade-Off at Scale

Hybrid platforms are addressing one of the longest-standing objections in the digital printing for flexible packaging market, which is the speed gap between pure digital systems and analog production at medium run lengths. At Labelexpo Europe 2025, Heidelberger Druckmaschinen AG introduced the Gallus Five hybrid press, combining digital flexibility with industrial productivity for converters running mixed job queues. BOBST also presented the FLEXJET module, which enables all-digital multilayer label production with simultaneous printing on multiple surfaces in a single pass, reducing process steps and handling waste. That matters because hybrid systems do not simply replace earlier digital capacity; they extend digital economics into jobs that were previously left to flexo or gravure due to speed limits. This widens the addressable order book in the digital printing for flexible packaging market and provides converters with a more practical bridge between high-mix jobs and higher-output production. It also strengthens the case for converters that want digital benefits without giving up the familiarity of conventional process control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Payback Risk Versus Conventional Long-Run Printing | -1.9% | Global | Short term (≤ 2 years) |

| Specialty Ink and Film Substrate Price Volatility | -1.5% | Global, concentrated in Europe | Medium term (2-4 years) |

| Limited Food-Contact and Recyclability Qualification for Some Digital Ink Systems | -1.0% | Europe and North America | Medium term (2-4 years) |

| Cybersecurity and Workflow Downtime Risks in Connected Print Lines | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure Creates Payback Risk Against Long-Run Economics

Capital cost remains the clearest short-term barrier in the digital printing for flexible packaging market, especially for converters that still have usable analog assets on the floor. Production-grade presses that can run across a broad substrate range commonly cost more than USD 1 million, and workflow integration further increases the total commitment before stable output is achieved. The payback profile depends on having enough short- and medium-run orders in the order book, and many converters cannot guarantee that mix when their customer contracts were built around longer, conventional production. Flint Group Digital Xeikon has responded with its Ecolyne subscription model, which was launched globally in 2026 after its initial Asia-Pacific introduction in late 2025. The model lowers the upfront entry point by treating a large capital commitment as a recurring operating cost and allowing converters to scale more gradually. Even so, the capex question continues to slow adoption in the digital printing for flexible packaging market because many buyers still need clear proof that run mix, customer demand, and utilization will remain favorable.

Specialty Ink and Film Substrate Price Volatility Compresses Converter Margins

Input volatility remains a practical constraint because digital ink systems rely on specialty chemicals and films that do not always align with broader packaging costs. UV-curable and electron beam chemistries depend on photoinitiators, oligomers, monomers, and other specialized materials sourced through concentrated supply chains, which exposes converters to sudden cost swings. SCREEN Europe said European polyethylene spot prices moved above their 2022 crisis peak by mid-2026 following Strait of Hormuz instability, showing how fast substrate costs can move when feedstock supply tightens. At FTA FORUM INFOFLEX 2026, ink formulators also stressed that future pressrooms will need flexibility across UV, LED, EB, water-based, and solvent systems, as no single chemistry fully solves for cost stability, substrate reach, and compliance at the same time. Converters on fixed-price customer contracts face the sharpest pressure because packaging repricing usually works on quarterly or annual terms rather than real-time feedstock resets. This makes margin management challenging in the digital printing for flexible packaging market, especially when input shocks hit both the ink and substrate layers simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: UV Inkjet Anchors Revenue While Hybrid Presses Accelerate

UV inkjet held 30.88% of the digital printing market share for flexible packaging in 2025, reflecting a mature installed base, broad substrate qualification, and well-developed service support. Its strength has come from how it handles a wide range of flexible films while also fitting existing converter workflows, with fewer extra preparation steps than some competing processes. Compared with electrophotography, UV inkjet is better aligned with PE and PP film applications, where production teams want simpler substrate handling and dependable adhesion. That operational familiarity matters because converters tend to favor systems that reduce qualification time, operator retraining, and supply chain complexity when they scale output. In the digital printing for flexible packaging market, those practical factors have helped UV inkjet remain the main revenue anchor even as newer technologies expand.

Water-based inkjet is also advancing in paper-based applications, and SCREEN Europe's Truepress PAC 520P is now in full commercial production at Sacchital in Italy at 80 m/min, using food-safety-compliant water-based inks without plates or tooling.[2]SCREEN Europe, “Interpack 2026, SCREEN Digitally Printed Packaging,” SCREEN Europe, screeneurope.com Hybrid presses are projected to grow at a 14.38% CAGR through 2031, which makes them the fastest moving technology category in this market. The Gallus Five launch in 2025 showed how converters are looking for systems that preserve industrial throughput while also adding digital flexibility for mixed job streams. Hybrid systems extend digital reach into medium-run work that pure digital assets often struggle to serve profitably, so they widen the usable order mix rather than simply replacing older digital units. The tradeoff is that converters usually need stronger confidence in sustained short-to-medium run demand before they commit to this faster but more capital-intensive option.

By Packaging Type: Pouches Dominate While Stick Packs and Sachets Gain Speed

Pouches held a 37.04% share in 2025, making them the largest format in the segment and confirming their central role across food, beverage, personal care, and household applications. Their lead reflects the balance they offer between barrier performance, shelf impact, consumer convenience, and the ability to support frequent design changes. Stand-up pouches have especially benefited from digital printing, as brands can carry multiple design variants in a single campaign without absorbing the cylinder costs that make small analog runs unattractive. Wraps and rollstock still serve a broad industrial base and remain more closely linked to analog production, particularly in long-run food applications. Even so, promotional overwraps and limited-edition campaigns are drawing more digital activity because launch speed often matters more than unit cost in those programs.

Stick packs and sachets are projected to grow at a 12.74% CAGR through 2031, which gives them the strongest pace among packaging formats. Their growth aligns with single-serve nutrition, convenience-led personal care, and e-commerce fulfillment models that require compact formats and frequent artwork changes. Pharmaceutical demand is also expanding as some over-the-counter products shift to sachet-based delivery and require unit-level variable data for traceability and patient information. Domino Printech India launched the K300 variable data printing system at CPHI and PMEC 2025 for this exact intersection of serialization demand and packaging format flexibility, with speeds up to 250 m/min. Bags and other packaging types remain relevant, but their heavier exposure to commodity and bulk applications means conventional long-run print still holds a stronger economic position there.

By Ink Type: Water-Based Systems Lead Volume While Electron Beam Gains Momentum

Water-based inks held a 38.96% share in 2025, reflecting both their established food-contact profile and their fit with the move toward paper-based, recyclable structures. Their position is stronger where converters are under pressure to reduce solvent use, simplify compliance, and support brand sustainability claims with fewer operational compromises. Konica Minolta, together with FUJIPACK SYSTEM Co., Ltd. and MST Co., Ltd., developed a water-based inkjet system that prints directly onto food packaging film on the packaging machine itself, eliminating the need for label materials and a separate process step. That kind of direct integration matters because it shows water-based systems are moving deeper into line architecture rather than remaining a standalone print step. UV-curable inks still play an important role due to their fast cure and strong film adhesion, but food-contact scrutiny is tighter when migration concerns arise.

Electron beam inks are projected to grow at a 14.36% CAGR through 2031, which makes them the fastest-rising chemistry in the segment. They stand out because they do not rely on photoinitiators, which reduces one of the more sensitive issues in regulated food-contact applications. They also avoid solvents and VOC emissions, which improves their fit with recyclability and workplace safety objectives in stricter packaging environments. The main barrier is still the cost and complexity of supporting infrastructure, including nitrogen inerting and shielding, which narrows adoption among smaller converters. For the digital printing for flexible packaging market, EB therefore represents a promising but selective path that is better suited to converters with capital depth and strong compliance-driven demand.

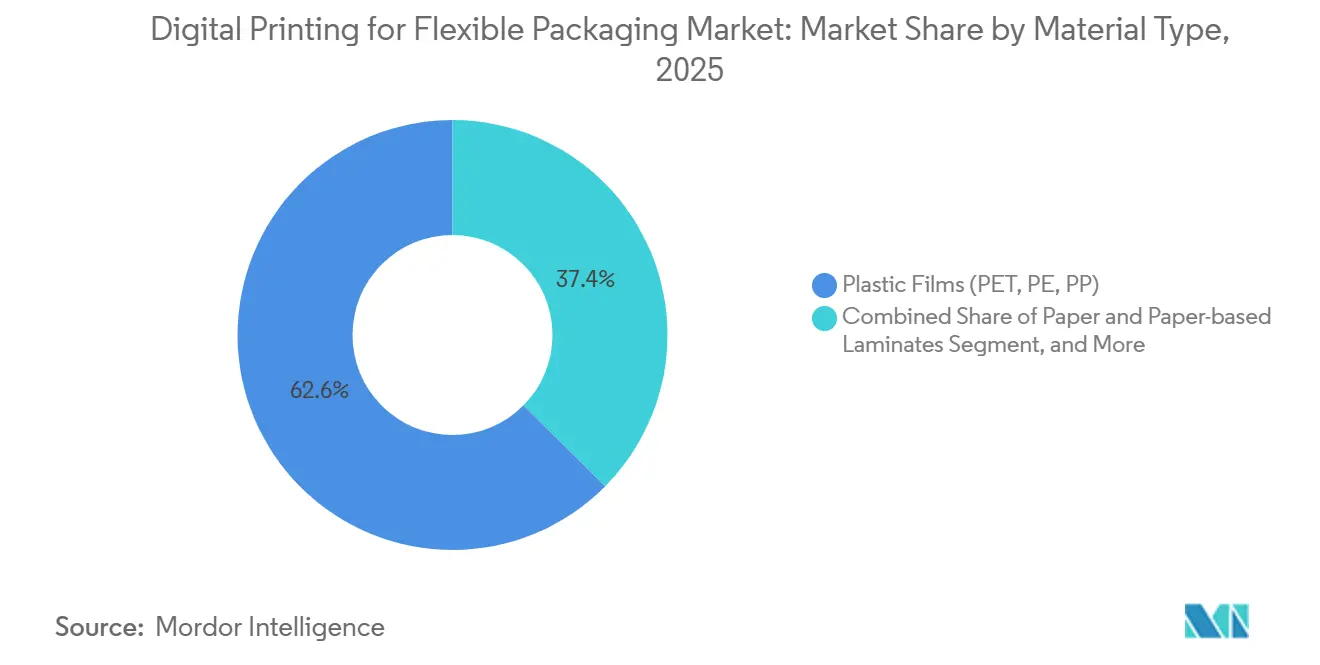

By Material Type: Plastic Films Lead Today While Compostable Films Expand Fastest

Plastic films held a 62.58% share in 2025, which showed that PET, PE, and PP still define the core substrate base for digitally printed flexible packs. Their position remains strong because barrier protection, seal performance, moisture resistance, and compatibility with current converter lines still matter more than any single sustainability feature in many applications. The largest qualified installed base in the digital printing for flexible packaging industry is still tied to these film types, especially where UV inkjet and electrophotographic platforms have built reliable performance histories. Paper and paper-based laminates are gaining support as sustainability rules tighten and as water-based digital systems prove more practical on fiber-based materials. Aluminum foil keeps its place in specialist pharmaceutical and aseptic applications, although digital progress there remains slower because qualification and printability are more demanding.

Compostable films are projected to grow at a 14.21% CAGR through 2031, making them the fastest-growing material category. EU Regulation 2025/40 entered into force in February 2025 and will require select packaging categories, including permeable tea bags, to meet EU industrial composting standards by February 2028. That rule is changing qualification roadmaps for converters that supply European food and pharmaceutical packaging because material choices now connect more directly with compliance timing. Sukano Group launched a new antiblock masterbatch for biaxially oriented PLA film in 2025 that supports printability with up to 7x transverse direction stretch on existing BOPP equipment, which lowers the technical barrier for commercial use. This gives early adopters in the digital printing for flexible packaging market a stronger position because digital production is well suited to the short qualification runs that usually come first in a material transition.

By End User Industry: Food Retains Scale While Pharmaceuticals Deliver the Fastest Growth

Food maintained a 36.32% revenue share in 2025, which kept it as the largest end-user segment and confirmed the deep embeddedness of flexible packs across fresh produce, snacks, ready meals, and condiments. The segment continues to generate digital demand because seasonal launches, promotional variants, and design refreshes are regular features of category management. The German Printing Ink Ordinance came into full force in 2026 and introduced a positive list approach, migration limits, and pigment purity requirements, raising the compliance threshold for packaging suppliers. That is pushing converters to spend more on qualification and is likely to increase switching costs around approved ink sets and supplier relationships. Beverages, personal care, and cosmetics continue to add meaningful volume, while household products move more gradually because their print runs are often longer and design turnover is less frequent.

Pharmaceuticals are projected to grow at a 13.59% CAGR through 2031, making them the fastest-growing end-user category in the digital printing for flexible packaging market. The growth is tied to serialization mandates, personalized medicine packaging, and micro-fulfillment for clinical trial material, all of which need variable data at unit level. Domino said digital transformation in pharmaceutical manufacturing is accelerating in India, particularly across corridors linked with serialization and export compliance. The next layer of demand comes from cold-chain biologics and gene therapies because their outer flexible packs need patient-specific information and precise tracking support. That turns digital capability from an efficiency tool into a regulatory and operational requirement for specialty pharma contractors.

Geography Analysis

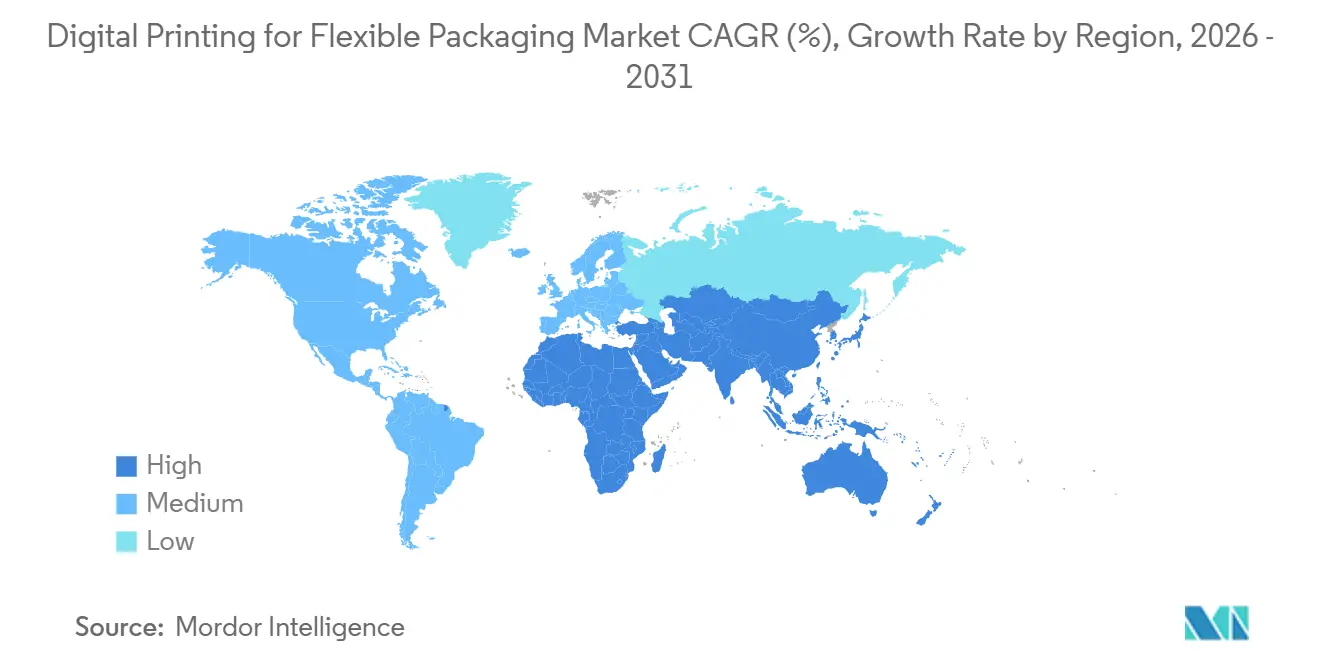

Asia-Pacific accounted for 35.95% share of the digital printing for flexible packaging market size in 2025 and is projected to expand at a 13.06% CAGR through 2031. The region combines the strongest volume base with the fastest growth, an uncommon combination that shows how closely packaging demand is tied to e-commerce scale, fast-moving consumer goods, and regional product variation. China remains central because online retail activity, fast pack updates, and standardization needs create a natural case for short-run digital output. India is also becoming a major growth center as pharmaceutical serialization, quick-commerce grocery expansion, and food-contact oversight push converters toward faster, more flexible packaging formats. BOBST underscored the regional importance of this demand by showcasing digital and sustainable flexible packaging solutions alongside Chinese converters at Chinaplas 2026 in Shanghai.

North America and Europe formed the most mature technology base for the digital printing for flexible packaging market in 2026, even though the input did not provide separate regional shares for each market. In North America, ePac opened a new facility in Phoenix in March 2026 and added capacity in Atlanta, Philadelphia, and Vancouver, showing that digital flexible packaging is moving into broader network deployment rather than isolated local expansion.[3]ePac Holdings, “HP and ePac Sign USD 50M Strategic Deal,” ePac Holdings, epacflexibles.com Europe is advancing under tighter compliance conditions because PPWR 2025/40 and the German Printing Ink Ordinance are both influencing ink and substrate qualification choices. The first HP Indigo 200K installation in EMEA at ePac's Sheffield site also showed that regional scaling is moving into a more commercial stage rather than staying in pilot mode.

South America, the Middle East and Africa, and other smaller markets remained at earlier adoption stages in 2025, and their progress depended more on packaging modernization and local brand development than on current installed digital depth. Brazil leads the South American opportunity because growing branded food and beverage demand favors better graphics, more SKU variety, and shorter launch cycles than long-run conventional systems handle well. The United Arab Emirates and Saudi Arabia are supporting more premium food and personal care packaging programs, which fit localized launches and shorter production runs. South Africa, Nigeria, and Egypt offer a longer runway, and their pace will depend on converter investment, substrate availability, and e-commerce infrastructure as the digital printing for flexible packaging market expands beyond its current core regions.

Competitive Landscape

The digital printing for flexible packaging market remains moderately fragmented, and competitive intensity changes depending on whether the focus is on presses, inks, workflow software, or conversion capacity. No single supplier has established clear control across print speed, substrate versatility, and food-contact readiness, which keeps buyer choice relatively open and preserves room for differentiated offers. BOBST has sought to address one of the market's practical adoption barriers through its Kyveris open-API environment, which enables third-party MIS, workflow, and finishing system integration without forcing converters into a closed software stack. That strategy matters because some converters have delayed digital investment as much because of integration complexity as because of print performance.

At the converter tier, ePac has built the clearest digital-only scale model, with more than 22 facilities worldwide operating around digital flexible packaging production. Its USD 50 million, 3-year agreement with HP for more than 10 Indigo 200K presses shows how equipment, service, and consumables relationships are becoming longer term and more difficult for rivals to displace. Flint Group Digital Xeikon also changed its commercial approach with the global launch of Ecolyne in 2026, lowering the entry threshold for converters that could not afford a full press purchase upfront. In the digital printing for flexible packaging market, that means competition is now being shaped by financing structures and operating models as much as by technical specifications.

The largest white space still sits with mid-sized analog-only converters because many have the SKU diversity needed for digital production but not the certainty to spend USD 1 million to USD 2 million in one step. Strategic moves in 2025 and 2026 reflected that opening, including Gallus and Heidelberg launching the Gallus Five hybrid platform and Flint Group Digital Xeikon introducing subscription access.[4]Flint Group Digital Xeikon, “Flint Group Digital Xeikon Launches Ecolyne Worldwide,” Flint Group Digital Xeikon, xeikon.com SCREEN's commercial production at Sacchital and BOBST's converter-focused demonstrations in Shanghai and Istanbul also showed that vendors are using live production proof points to reduce adoption hesitation. The digital printing for flexible packaging market is therefore rewarding suppliers that combine reliable throughput, compliance readiness, flexible pricing, and close converter support.

Digital Printing For Flexible Packaging Industry Leaders

Amcor plc

Mondi plc

Huhtamäki Oyj

CCL Industries Inc.

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Xeikon rebranded as Flint Group Digital Xeikon under the newly restructured Flint Group Packaging Solutions umbrella, formalizing the integration of digital press operations with Flint Group's broader packaging ink and consumables business as a unified commercial entity.

- May 2026: SCREEN Europe's Truepress PAC 520P entered full commercial production at Sacchital in Italy, printing paper-based recyclable flexible packaging at 80 m/min using water-based, food-safety-regulation-compliant inks without plates or tooling, and a second installation at Chiyoda Gravure Corporation in Japan was also operational.

- May 2026: BOBST hosted its second Experience Day focused on flexible packaging at its Istanbul facility, demonstrating its digital, automated, and sustainable flexible packaging solutions portfolio as part of a series of market engagement events connecting OEM innovation directly with converter production needs.

- April 2026: BOBST demonstrated digital and sustainable flexible packaging innovations at Chinaplas 2026 in Shanghai in collaboration with local converters including Tingzheng Packaging and Lucky Film, using the Changzhou Competence Center as a hub for live demonstrations and customer co-development activities.

Global Digital Printing For Flexible Packaging Market Report Scope

Digital printing for flexible packaging refers to the process of using digital technology to print designs, text, and images directly onto flexible packaging materials. This method offers high-quality printing, faster turnaround times, and customization options, making it a preferred choice in the packaging industry. It excludes conventional (plate-based) printing, digital print on non-flexible substrates such as corrugated, cartons, and rigid packaging, and printing equipment/consumables.

The Digital Printing for Flexible Packaging Market Report is Segmented by Printing Technology (Electrophotography, UV Inkjet, Water-based Inkjet, Hybrid Presses, and Other Printing Technologies), Packaging Type (Pouches, Stick Packs and Sachets, Wraps and Rollstock, Bags, Labels, and Other Packaging Types), Ink Type (UV-curable Inks, Water-based Inks, Solvent-based Inks, and Electron-beam (EB) Inks), Material Type [Plastic Films (PET, PE, PP), Paper and Paper-based Laminates, Aluminum Foil, Compostable Films, and Other Material Types), End-User Industry (Food, Beverages, Pharmaceuticals, Personal Care and Cosmetics, Household, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Electrophotography |

| UV Inkjet |

| Water-based Inkjet |

| Hybrid Presses |

| Other Printing Technologies |

| Pouches |

| Stick Packs and Sachets |

| Wraps and Rollstock |

| Bags |

| Labels |

| Other Packaging Types |

| UV-curable Inks |

| Water-based Inks |

| Solvent-based Inks |

| Electron-beam (EB) Inks |

| Plastic Films (PET, PE, PP) |

| Paper and Paper-based Laminates |

| Aluminum Foil |

| Compostable Films |

| Other Material Types |

| Food |

| Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Household |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Printing Technology | Electrophotography | ||

| UV Inkjet | |||

| Water-based Inkjet | |||

| Hybrid Presses | |||

| Other Printing Technologies | |||

| By Packaging Type | Pouches | ||

| Stick Packs and Sachets | |||

| Wraps and Rollstock | |||

| Bags | |||

| Labels | |||

| Other Packaging Types | |||

| By Ink Type | UV-curable Inks | ||

| Water-based Inks | |||

| Solvent-based Inks | |||

| Electron-beam (EB) Inks | |||

| By Material Type | Plastic Films (PET, PE, PP) | ||

| Paper and Paper-based Laminates | |||

| Aluminum Foil | |||

| Compostable Films | |||

| Other Material Types | |||

| By End user Industry | Food | ||

| Beverages | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Household | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of digital printing for flexible packaging?

The market was valued at USD 5.97 billion in 2025, stands at USD 6.63 billion in 2026, and is forecast to reach USD 11.58 billion by 2031 at an 11.80% CAGR.

Which printing technology leads revenue generation?

UV inkjet led the technology segment with a 30.88% share in 2025 because of its broad substrate compatibility and mature service and ink ecosystem.

Which packaging format is growing the fastest?

Stick packs and sachets are projected to grow at a 12.74% CAGR through 2031, supported by single-serve nutrition, convenience formats, and pharmaceutical serialization needs.

Why are water-based inks important in this space?

Water-based inks held a 38.96% share in 2025 and are benefiting from food-contact compliance needs and the shift toward paper-based recyclable packaging.

Which region offers the strongest growth outlook?

Asia-Pacific was the largest region with a 35.95% share in 2025 and is also the fastest-growing region, with a projected 13.06% CAGR through 2031.

Why is pharmaceutical demand rising so quickly?

Pharmaceuticals are projected to grow at a 13.59% CAGR through 2031 because serialization, personalized medicine packaging, and micro-fulfillment all require variable data and shorter production runs.

Page last updated on: