Flexible Liquid Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

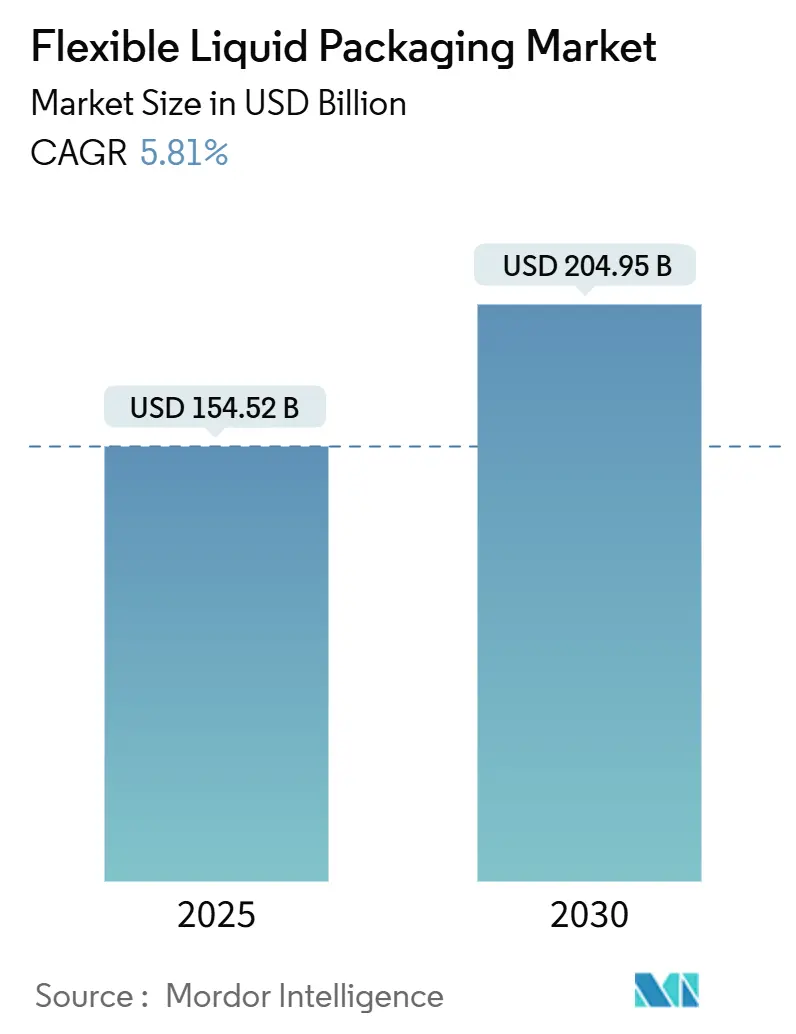

| Market Size (2025) | USD 154.52 Billion |

| Market Size (2030) | USD 204.95 Billion |

| Growth Rate (2025 - 2030) | 5.81% CAGR |

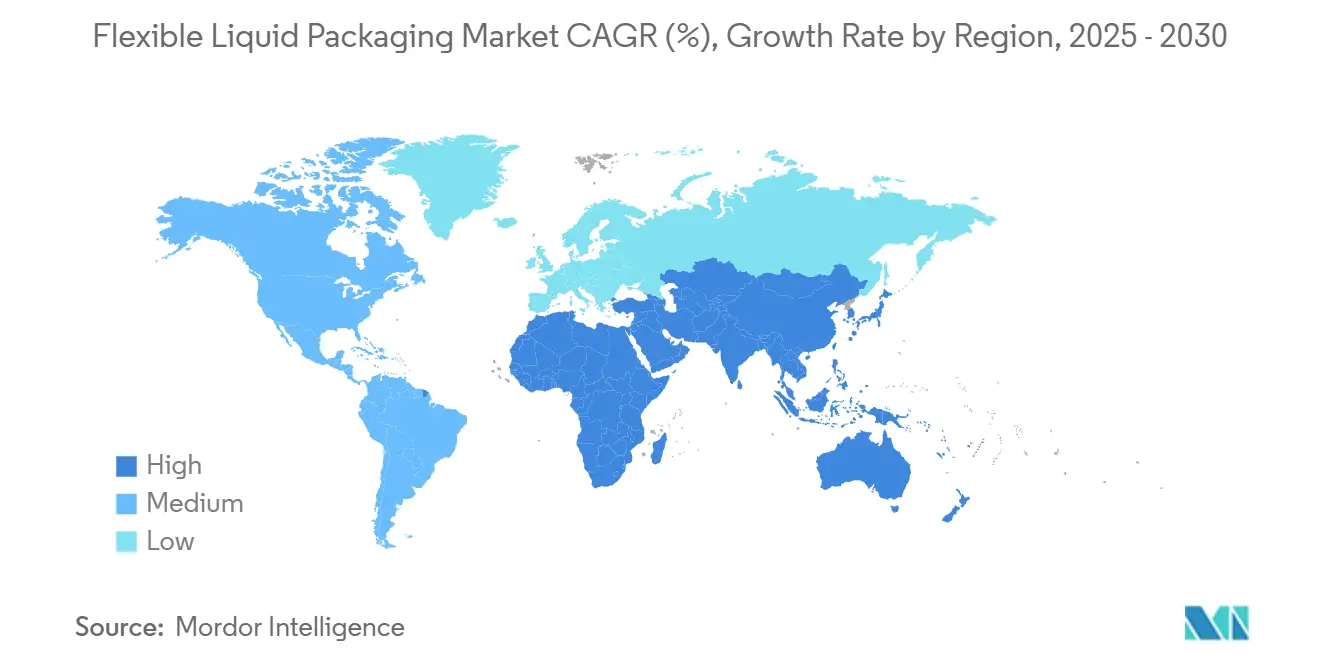

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Liquid Packaging Market Analysis by Mordor Intelligence

The flexible liquid packaging market size stands at USD 154.52 billion in 2025 and is on course to reach USD 204.95 billion by 2030, advancing at a 5.81% CAGR through the period. This performance underscores how the flexible liquid packaging market is capitalizing on consumers’ preference for lighter, convenience-driven formats and how regulatory pressure is pushing producers toward recyclable structures. E-commerce growth has amplified demand for shipping-resilient packs, positioning the flexible liquid packaging market as a logistical ally for brands seeking lower freight costs and fewer damage claims. Industry leaders are also investing in mono-material designs that meet recyclability mandates without sacrificing barrier integrity, a strategic move that is reshaping competitive positioning within the flexible liquid packaging market. Finally, raw material price volatility and an expanding patchwork of single-use plastic bans introduce cost and compliance challenges that producers must navigate to sustain profitability.

Key Report Takeaways

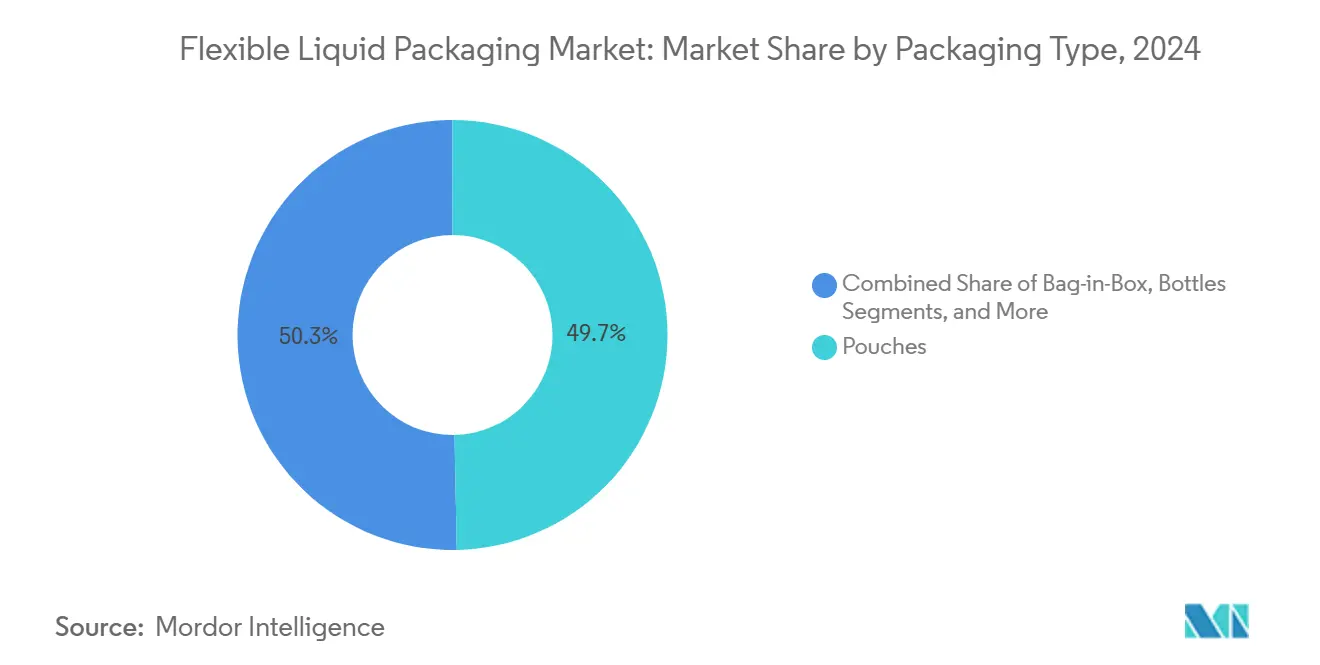

- By packaging type, the Flexible Liquid Packaging Market size for bag-in-box formats is projected to grow at a 7.13% CAGR between 2025–2030.

- By material type, the plastic films segment captured 67.18% of the Flexible Liquid Packaging Market share in 2024.

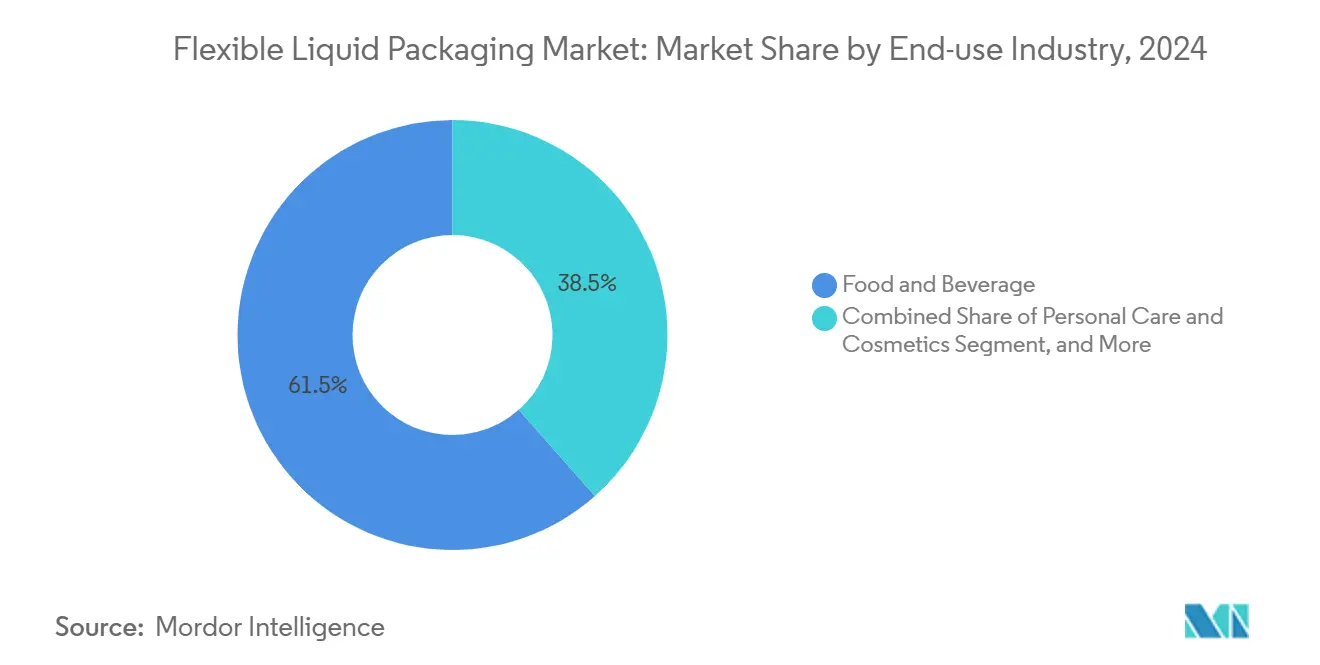

- By end-user industry, the Flexible Liquid Packaging Market size for pharmaceuticals is projected to grow at a 7.56% CAGR between 2025–2030.

- By geography, the Asia-Pacific segment captured 40.63% of the Flexible Liquid Packaging Market size in 2024.

Global Flexible Liquid Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenient lightweight beverage formats | +1.2% | Global with APAC and North America leading | Medium term (2-4 years) |

| E-commerce growth and durable flex-packs | +0.9% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Recyclable pouch mandates | +0.8% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Lower logistics and material costs | +0.7% | Global, particularly emerging markets | Medium term (2-4 years) |

| Aseptic flex-packs boosting dairy-alternative penetration | +0.5% | North America and Europe, growing in APAC | Medium term (2-4 years) |

| Refill and concentrate models adopted by CPG majors | +0.4% | Europe and North America, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient, Lightweight Beverage Formats

Single-serve pouches and squeeze packs have transitioned from a niche to a mainstream category as on-the-go consumption increases and resealable features become standard. Beverage brands have reduced transportation costs by up to 40% by switching from rigid bottles to flexible packs, a savings that directly improves margins in the flexible liquid packaging market. New barrier films approved by the European Food Safety Authority in 2024 extend shelf life for sensitive formulations, allowing premium juices and functional drinks to forgo refrigeration and reach new retail channels. Rapid line speeds of up to 1,200 pouches per minute enable manufacturers to respond to promotional spikes without stockouts, reinforcing the operational appeal of flexible options. Consumer acceptance is further buoyed by portion control, which aligns with health-focused lifestyles and curbs product waste. Consequently, multinational beverage companies have expanded flexible portfolios to lock in growth across both mass and premium tiers of the flexible liquid packaging market.

E-commerce Growth Amplifying Need for Durable Flex-packs

With online groceries posting double-digit growth, packages now endure multiple touchpoints before arriving at the consumer’s door.[1]Reuters Staff, “Packaging Industry Adapts to E-commerce Growth,” Reuters, reuters.com Flexible films, offering puncture and impact resistance, see 30% fewer damage claims compared to rigid containers, a clear logistics advantage that strengthens the flexible liquid packaging market. Amazon’s vendor guidelines favor flex-packs for liquids, catalyzing supplier investment in high-performance seals and tamper-evident closures. Bag-in-box solutions benefit subscription drink services by providing extended shelf life and concentrated formats that reduce packaging waste. Lighter weights also lower last-mile delivery emissions, helping retailers meet carbon-reduction pledges. As fulfillment centers automate, the pliability of flex-packs minimizes jam rates on conveyor belts, ensuring smooth operations even during seasonal demand peaks.

Sustainability Mandates Favoring Recyclable Pouch Designs

Europe’s Packaging and Packaging Waste Regulation requires 65% recycled content in flexible packs by 2030, compelling companies to re-engineer laminates around mono-material polyethylene. These mandates create a competitive moat for early adopters within the flexible liquid packaging market. Unilever’s pledge to achieve 100% recyclable packaging by 2025 has already accelerated the commercialization of water-based coatings that replace aluminum foil while maintaining oxygen barriers. Consumer surveys indicate a 73% willingness to pay premiums for sustainable packaging, validating the higher initial conversion costs. Investment in chemical recycling plants is also gathering pace, promising to close the loop for multilayer structures still needed in high-barrier applications. Over time, compliance readiness is expected to evolve from a differentiator to an entry ticket, shifting procurement priorities toward traceable, certified material streams.

Lower Logistics and Material Costs Versus Rigid Containers

Flexible formatting typically reduces material costs by 40-50% compared to rigid alternatives when end-to-end supply chain savings are tallied. Lighter loads reduce fuel usage, with retailers citing a 25% transportation-cost reduction after replacing glass with pouches for cooking oils. Flat shipping of pre-form rolls enables regional copackers to reduce warehouse space by 70%, improving inventory turns and working capital ratios. Advanced form-fill-seal technology now handles viscosities ranging from dairy alternatives to motor oils, expanding the addressable categories within the flexible liquid packaging market. As urban congestion charges increase, manufacturers highlight weight savings in their sustainability reports, satisfying both investor scrutiny and retailer scorecards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyolefin and barrier resin prices | -0.8% | Global with APAC most affected | Short term (≤ 2 years) |

| Expanding single-use-plastic bans | -0.6% | Europe and select APAC markets, expanding globally | Medium term (2-4 years) |

| Weak recycling streams for multilayers | -0.4% | Global, particularly developing markets | Long term (≥ 4 years) |

| Flex-crack risks in cold-chain logistics | -0.3% | Global, concentrated in temperature-sensitive applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyolefin and Barrier Resin Prices

Polyethylene and polypropylene costs swung 35% during 2024 as crude-oil price shocks ricocheted through supply contracts, squeezing converters already locked into OEM price lists. Specialized EVOH barrier resins experienced sharper 45% spikes due to limited reactors and capacity competition related to aviation fuel. Flexible packagers struggled to pass increases to dairy and juice brands that operate on thin margins, forcing margin compression across parts of the flexible liquid packaging market. Some leaders pursued backward integration or long-term take-or-pay contracts, sacrificing near-term cash to secure supply. Currency volatility further complicated forecasting, with Euro-based buyers paying premiums for USD-denominated resin.

Expanding Single-Use-Plastic Bans Worldwide

The European Union’s directive extension now captures certain pouch formats while Thailand and Malaysia implement parallel curbs, tightening market access for conventional laminates. Producers must fast-track compostable or paper-hybrid designs, yet bio-based barriers often compromise shelf life, restricting their deployment in dairy and pharmaceutical applications. Divergent testing standards across jurisdictions necessitate multi-SKU compliance strategies, which in turn inflate complexity costs by 15-20%. Smaller brands risk delisting if unable to finance redesigns, leading to consolidation in the flexible liquid packaging market. Conversely, innovators that can hit both performance and compostability targets gain a first-mover edge in restricted geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Pouches Lead While Bag-in-Box Accelerates

Pouches retained a 49.68% foothold in 2024, affirming their role as the cornerstone format across beverages, sauces, and household liquids. This dominance in the flexible liquid packaging market is underpinned by resealable closures, easy branding real estate, and lower carbon footprints compared to glass or PET. Growth will continue as smart oxygen scavengers and temperature indicators migrate from premium to mainstream SKUs, reinforcing the convenience narrative. Bag-in-box units are experiencing a 7.13% CAGR, driven by coffee concentrates and wine subscription models that value extended shelf stability and 50% freight cost savings.

Innovation is also seeping into flexible bottle concepts that mimic rigid aesthetics yet reduce weight for pharmaceutical syrups and niche craft drinks. Sachets thrive in cost-sensitive emerging markets, although evolving bans on single-serve plastics are tempering volumes in Europe and North America. Across all formats, digital features such as NFC chips enable provenance verification and consumer engagement, encouraging brands to leverage connected-pack campaigns within the flexible liquid packaging market.

By Material Type: Plastic Films Dominate Despite Sustainability Shift

Plastic films captured 67.18% share in 2024, buoyed by thin-gauge co-extrusions that drive cost efficiency without sacrificing barrier performance. These structures remain the workhorse of the flexible liquid packaging market, especially after filler lines proved compatible with ultra-thin films that reduce resin usage. Paper-based laminates are scaling at a 6.93% CAGR, propelled by retailer targets for fiber content and consumer affinity for tactile, natural aesthetics.

Aluminum-foil hybrids continue to serve applications that require extreme light and oxygen barriers, particularly in pharmaceuticals and premium juices. However, chemical recycling breakthroughs promise to rehabilitate today’s multilayer films by depolymerizing composite substrates into virgin-grade feedstock. As regulatory scoring penalizes non-recyclable packs, material innovation in mono-polyethylene and EVOH alternates is expected to recalibrate procurement priorities across the flexible liquid packaging market.

By End-use Industry: Pharmaceuticals Surge as Food Beverages Mature

Food and beverage streams supplied 61.54% of the volume in 2024; however, expansion is flattening in developed regions, where penetration has matured and alternative formats are vying for attention. Even so, line extensions into functional drinks and plant-based milks continue to drive volumes in the flexible liquid packaging market. Pharmaceuticals, by contrast, are sprinting at a 7.56% CAGR as drug-makers formulate liquids for easier pediatric and geriatric dosing. FDA clearances for 15 new barrier films in 2024 signal regulatory confidence in the safety of flex-packaging, unlocking therapies that once relied on glass.

Personal-care brands tap flexible sachets for travel-size shampoos and serums, aligning with premiumization and sampling strategies. Household-cleaner innovators introduce concentrate pouches that consumers dilute at home, reducing water freight and aligning with corporate ESG pledges. Industrial players adopt heavy-duty flex drums for chemicals, leveraging superior puncture resistance and UN certification pathways that validate safety in the flexible liquid packaging market.

Geography Analysis

Asia-Pacific’s 40.63% share in 2024 reflects the region's manufacturing scale, raw material availability, and a growing middle class embracing on-the-go beverages. The flexible liquid packaging market size for the region is poised for a 7.47% CAGR to 2030, as e-commerce platforms expand and local governments offer tax incentives for packaging investments. National regulations, however, remain fragmented, pushing multinationals to develop modular designs that can swap barrier layers to meet country-specific mandates.

North America’s mature grocery landscape continues to foster growth in premium categories, where sustainability or functional attributes command price premiums. State-level extended producer responsibility laws elevate recycling readiness to a procurement criterion, shifting the share toward mono-material pouches. European markets intensify this dynamic through mandatory recycled-content thresholds, making compliance prowess a commercial necessity in the flexible liquid packaging market.[2]Flexible Packaging Desk, “Flexible Packaging Manufacturing Economics,” Bloomberg, bloomberg.com

The Middle East and Africa, as well as South America, are forging new demand corridors as infrastructure improves and foreign direct investment in local converting capacity increases. Volatile exchange rates and limited recycling streams temper momentum, yet low per-capita packaging consumption signals upside. Brands that tailor affordable sachet formats while preparing for potential future plastics bans can seize early entrant advantage.

Competitive Landscape

The top ten converters account for roughly 45% of global revenue, giving the flexible liquid packaging market a moderate concentration score that still leaves room for regional specialists. Amcor, Mondi, and Sealed Air leverage their global footprints to offer turnkey sustainability roadmaps and invest in high-throughput digital printing, which slashes time to market. Mid-tier contenders find niches in aseptic dairy alternatives or localized pharmaceutical packs where proximity and customization trump pure scale.

Strategic integrations have accelerated: Amcor’s USD 2.3 billion acquisition of Berry Global’s flex-pack arm widens its dispersed asset base and strengthens emerging-market penetration. Larger players are also incubating recycling start-ups or licensing depolymerization IP to secure advantages in the circular economy. Patent filings related to recyclable mono-material structures topped 200 in 2024, indicating a technology arms race that will set new performance benchmarks for the flexible liquid packaging market.

Competitive differentiation is shifting toward demonstrable reductions in carbon footprint, validated through life-cycle assessment.[3]European Food Safety Authority, “Scientific Opinion on the Safety Assessment of the Substance,” EFSA, efsa.europa.eu Retailer scorecards and consumer-facing eco-labels amplify the value of traceable feedstock sourcing. As a result, converters without science-based targets risk margin erosion or loss of preferred-supplier status. White-space opportunities remain in controlled-drug packaging, nutraceutical sachets, and refill infrastructures where global incumbents have yet to cement presence.

Flexible Liquid Packaging Industry Leaders

Amcor plc

Mondi plc

Sealed Air Corporation

Smurfit WestRock plc

SIG Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Amcor completed its USD 2.3 billion acquisition of Berry Global’s flexible packaging division, forming the world’s largest flex-pack enterprise with strengthened sustainable-packaging capabilities.

- September 2024: Mondi announced a EUR 400 million (USD 440 million) investment in a new sustainable flexible-pack facility in Poland equipped with mono-material production lines and in-house recycling.

- August 2024: Sealed Air launched OptiDure barrier film technology delivering 30% material savings while retaining barrier performance for pharmaceutical and premium beverage uses.

- July 2024: Huhtamaki entered a strategic partnership with Dow Chemical to co-develop next-generation recyclable barrier films for liquid packing.

Global Flexible Liquid Packaging Market Report Scope

| Pouches |

| Bag-in-Box |

| Bottles |

| Sachets |

| Other Packaging Type |

| Plastic Films |

| Paper-Based Laminates |

| Aluminum Foil Laminates |

| Other Material Type |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Homecare and Household |

| Industrial and Chemicals |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Pouches | ||

| Bag-in-Box | |||

| Bottles | |||

| Sachets | |||

| Other Packaging Type | |||

| By Material Type | Plastic Films | ||

| Paper-Based Laminates | |||

| Aluminum Foil Laminates | |||

| Other Material Type | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Homecare and Household | |||

| Industrial and Chemicals | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the flexible liquid packaging market in 2025?

The flexible liquid packaging market size is expected to reach USD 154.52 billion by 2025, reflecting steady consumer demand for convenient and sustainable packaging formats.

What is the projected CAGR for flexible liquid packs through 2030?

The market is forecast to grow at a 5.81% CAGR, driven by e-commerce logistics needs and regulatory pushes for recyclable structures.

Which packaging type leads sales volume?

Pouches dominate the market with a 49.68% share in 2024, thanks to their resealability and lower freight costs.

Why are pharmaceuticals adopting flexible packaging quickly?

Liquid drug formulations benefit from child-resistant, tamper-evident flex-packs that reduce manufacturing costs and enhance patient compliance, driving a 7.56% CAGR.

Which region shows the fastest market expansion?

Asia-Pacific exhibits the highest 7.47% CAGR as urbanization, e-commerce, and government incentives converge.

What material innovation is most impactful for recyclability goals?

Mono-polyethylene pouches with advanced water-based coatings allow full recyclability while maintaining oxygen and moisture barriers.

Page last updated on: