Base Paper For Flexible Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

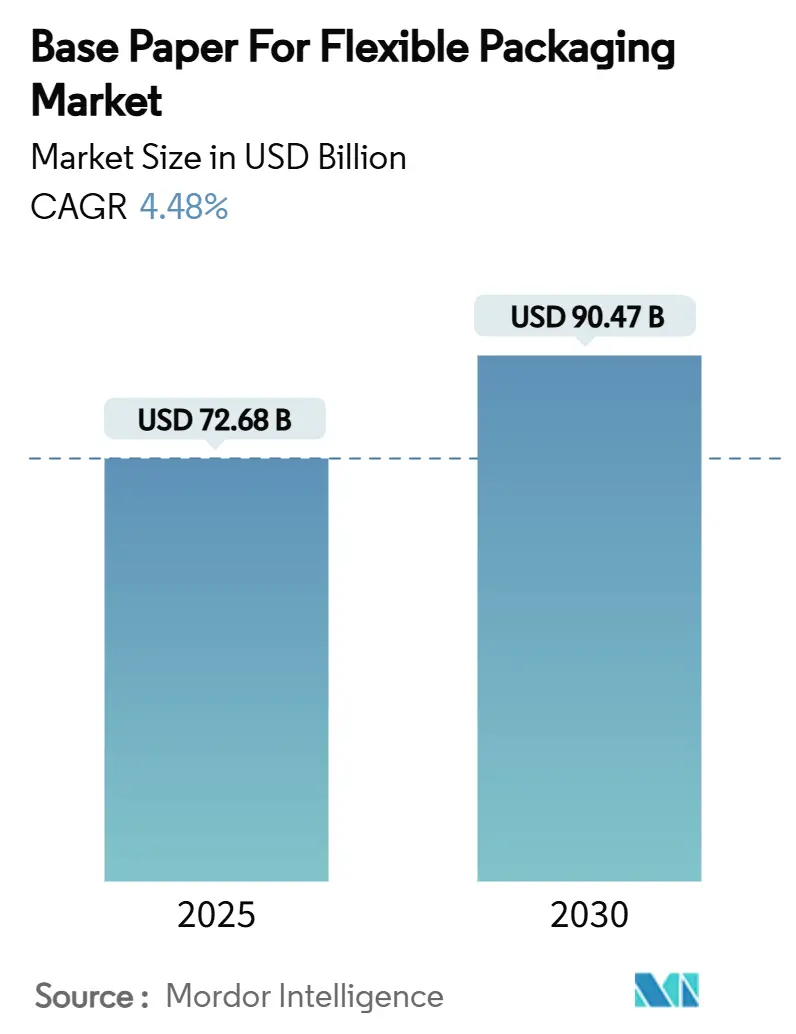

| Market Size (2025) | USD 72.68 Billion |

| Market Size (2030) | USD 90.47 Billion |

| Growth Rate (2025 - 2030) | 4.48% CAGR |

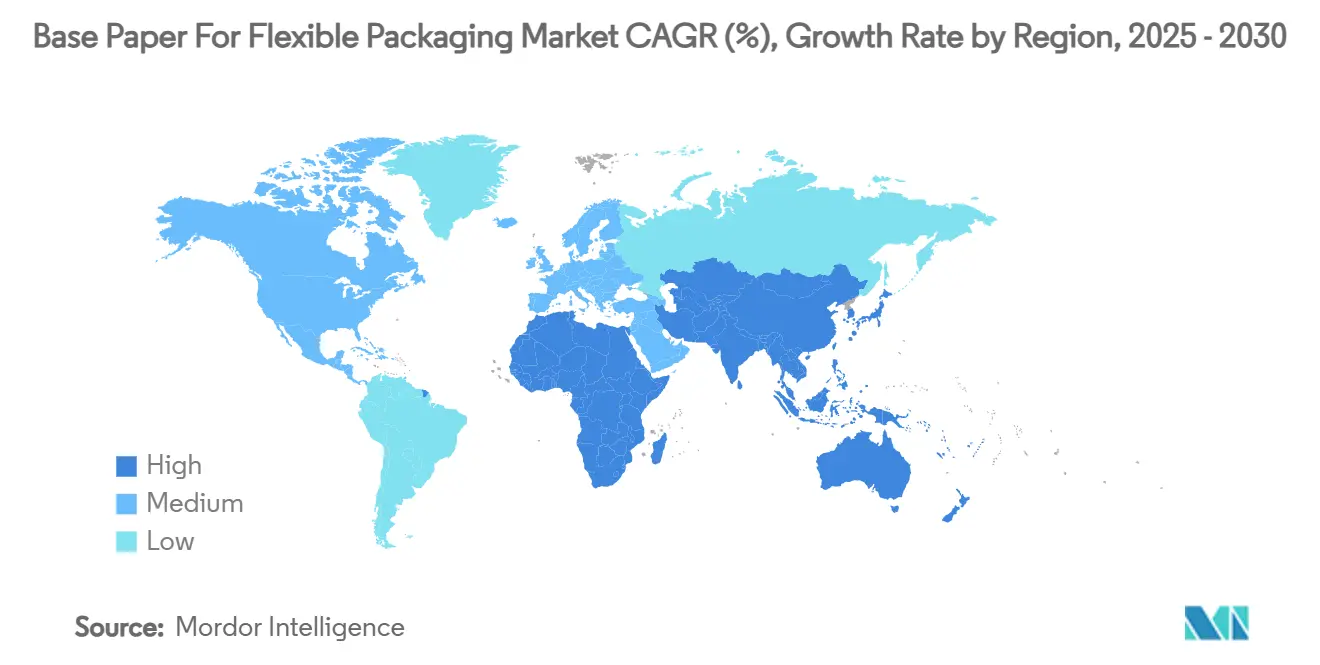

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Base Paper For Flexible Packaging Market Analysis by Mordor Intelligence

The base paper for the flexible packaging market size is USD 72.68 billion in 2025 and is projected to climb to USD 90.47 billion by 2030, reflecting a 4.48% CAGR. Regulatory mandates favoring recyclable substrates, corporate decarbonization targets, and rapid advances in high-barrier coating technologies collectively anchor demand for fiber-based alternatives across consumer goods. Breakthroughs that marry paper substrates with digital-printing compatibility improve pack differentiation at lower minimum order quantities, encouraging brand experimentation in dynamic retail channels. E-commerce accelerates the adoption of paper mailers in North America and China, while pulp supply diversification strategies help converters hedge against raw-material price volatility. Competitive intensity rises as integrated paper majors invest in capacity and as bio-based polymer innovators position for overlapping sustainability budgets.

Key Report Takeaways

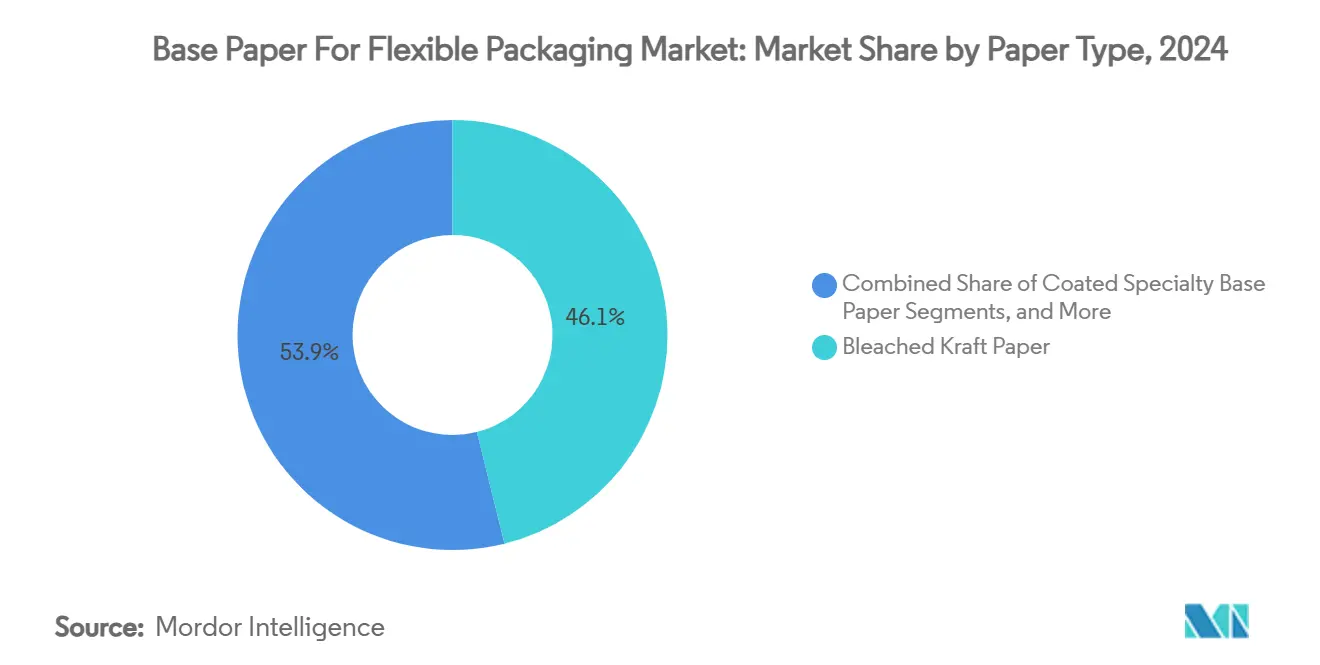

- By paper type, base paper for the flexible packaging market size for the coated specialty base paper segment is projected to grow at 8.21% CAGR between 2025-2030.

- By basis weight, the 40–80 gsm range captured 51.87% of the base paper for the flexible packaging market share in 2024.

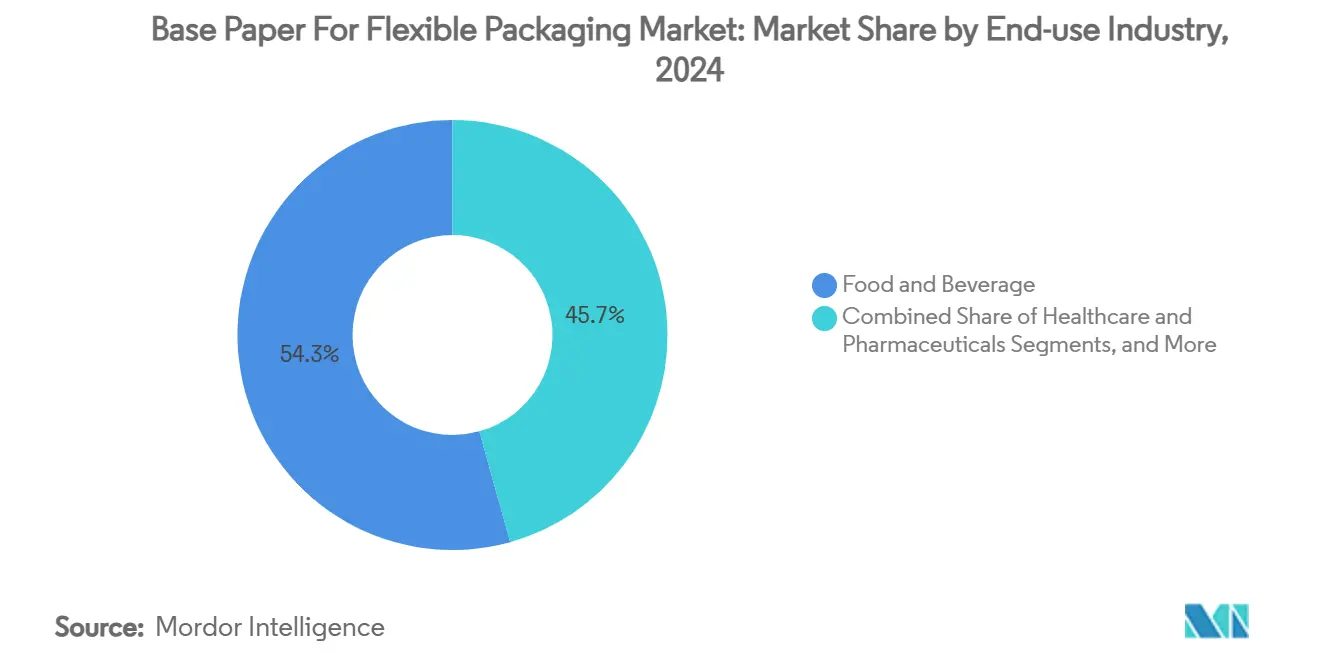

- By end-use industry, base paper for the flexible packaging market size for the healthcare and pharmaceuticals segment is projected to grow at a 9.11% CAGR between 2025-2030.

- By packaging format, pouches captured 47.65% of the base paper for the flexible packaging market share in 2024.

- By geography, the base paper for flexible packaging market size for the Asia-Pacific segment is projected to grow at a 9.35% CAGR between 2025-2030.

Global Base Paper For Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward sustainable packaging materials | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| Growth in on-the-go snacking and convenience foods | +0.7% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Advances in high-barrier coating technologies | +0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Digital-printing compatibility enabling short runs | +0.4% | North America and EU primarily | Short term (≤ 2 years) |

| E-commerce adoption of paper-based mailers | +0.3% | Global, led by North America and China | Short term (≤ 2 years) |

| CPG decarbonization targets pushing fiber adoption | +0.2% | Global, corporate-driven initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward sustainable packaging materials

Policy convergence is rewriting material playbooks as the EU Packaging and Packaging Waste Regulation becomes effective in 2025, mandating 100% recyclable packs by 2030 and raising recycled-content thresholds.[1]European Commission, “New EU Regulation Promotes the Procurement of Sustainable Packaging,” europa.eu Similar rules in Australia require 60% recycled fiber, amplifying paper’s structural advantage because it meets recyclability thresholds without chemical recycling plants. Brands accelerate the transition; Amazon removed 95% of plastic air pillows from its North American network in 2024, switching to recycled-paper cushioning that delivers equal protection at comparable cost. The first-mover response by global retailers reinforces an already favorable regulatory backdrop, solidifying the base paper for flexible packaging market as a principal beneficiary of circular-economy legislation.

Growth in on-the-go snacking and convenience foods

Urban consumers gravitate toward portion-controlled formats such as sachets and stick packs that demand lightweight, printable substrates. Paper versions offer sharper graphics and natural feel, traits that resonate in premium snack positioning and reinforce brand authenticity. These single-serve packs account for the fastest growth at 10.41% CAGR, complementing ultra-thin basis-weight papers engineered for automated filling lines. Rising disposable incomes across Southeast Asia and Latin America enlarge the addressable pool, ensuring that the base paper for flexible packaging market captures momentum across both mature and emerging food channels.

Advances in high-barrier coating technologies

Laboratory breakthroughs ranging from boric-acid-crosslinked PVOH layers that biodegrade in marine settings to plasma-polymerized plant-oil coatings narrow the performance gap with multilayer plastic films. Oxygen-transmission rates below 1 cc/m²/day let paper compete in moisture-sensitive snack and powdered-beverage segments, while recyclable chemistries bypass end-of-life barriers. The rapid commercialisation cycle shortens time-to-market for premium offerings and boosts value capture for converters owning proprietary barrier IP.

Digital-printing compatibility enabling short runs

Paper’s superior ink hold-out and dimensional stability underpin a cost advantage for digital presses that brands exploit for late-stage customisation. Shorter setup times permit SKU proliferation and region-specific campaigns without the tooling charges associated with gravure-printed plastic webs. The resulting agility encourages on-shelf experimentation, making the base paper for flexible packaging market an essential part of rapid-turn retail strategies in cosmetics, seasonal confectionery, and limited-edition beverages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance limits vs multi-layer plastic films | -0.6% | Global, most acute in high-barrier applications | Medium term (2-4 years) |

| Virgin fiber and pulp price volatility | -0.4% | Global, supply concentrated in key regions | Short term (≤ 2 years) |

| Limited recycling streams for coated papers | -0.3% | North America and EU primarily | Medium term (2-4 years) |

| Competition from bio-based polymer films | -0.2% | Global, accelerating in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance limits vs multi-layer plastic films

Ultra-high-barrier needs in coffee, medical devices, and oxygen-sensitive nutraceuticals still favor oriented polypropylene or EVOH-lined laminates. Cellulose-nanomaterial layers fall short in humid conditions above 65% relative humidity, undermining shelf-life targets in tropical supply chains. This technical ceiling slows migration within the base paper for flexible packaging market for certain premium SKUs until next-generation coatings emerge.

Virgin fiber and pulp price volatility

Global eucalyptus pulp hit USD 545 per tonne in early 2025 after a 26% surge in 2023, unsettling cost forecasts for converters pricing annual contracts. The US wood-pulp Producer Price Index reached 219.835 in May 2024, reflecting persistent supply shocks and energy-linked swings. Such gyrations erode paper’s price advantage versus plastics, thereby tempering short-term adoption curves in the base paper for flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Paper Type: Kraft leadership meets specialty-coating momentum

Bleached kraft accounted for 46.12% of 2024 revenues within the base paper for flexible packaging market and remains the print-quality benchmark for branded consumer packs.[2]Mondi Group, “Half-Year Results Announcement 2024,” mondigroup.com Coated specialty grades, supported by patents such as Amcor’s AmFiber Performance Paper, are accelerating at 8.21% CAGR thanks to oxygen- and grease-barrier innovations.

Reliance on unbleached kraft persists in industrial and natural-look retail segments, but the narrative shifts toward functional differentiation. Uncoated specialty papers carve a mid-tier niche by balancing moderate barrier performance with straightforward recyclability, avoiding the de-inking challenges of high-coat weights. Suppliers emphasise tailored chemistries over volume plays, creating pricing power and underpinning value growth across the base paper for flexible packaging market.

By Basis Weight: Mid-range dominance under pressure from ultra-thin grades

The 40–80 gsm band generated 51.87% of the base paper for flexible packaging market size in 2024 as it offers mechanical strength compatible with FFS lines. Sub-40 gsm papers gain traction at 7.93% CAGR as converters deploy advanced fiber-bonding to preserve tear resistance while reducing material use.

Above-80 gsm papers retain relevance in luxury goods and high-impact retail promotions where tactile heft equates to quality. Yet cost and carbon accounting tilt procurement decisions toward lighter gauges when functional parity is proven, a shift that broadens substrate selection for sachet, label, and e-commerce mailer formats integral to the expanding base paper for flexible packaging market.

By End-use Industry: Food core buttressed by healthcare surge

Food and beverage occupied 54.32% of 2024 demand as regulatory-approved food-contact kraft dominates dry-goods, confectionery, and on-the-go snacks. Healthcare and pharmaceuticals, led by Billerud’s sterile-grade lines, are forecast to progress at a 9.11% CAGR, leveraging controlled porosity and microbial-barrier papers for medical device wraps.

Personal care and cosmetics use premium coated papers to deliver sensory cues aligned with natural formulations, while home-care detergents favour moisture-proof wraps that withstand wet environments. Industrial niches such as electronics or agro-chemicals require anti-static or grease-resistant treatments, pushing technical frontiers and enriching the solution set inside the base paper for the flexible packaging market.

By Packaging Format: Pouch ubiquity complemented by sachet dynamism

Pouches held 47.65% share in 2024 by accommodating diverse product viscosities and enabling reclose features, reaffirming their status as the workhorse format of the base paper for flexible packaging market. Sachets and stick packs expand at a double-digit CAGR through 2030 as portion-control and single-dose therapeutics proliferate in emerging metros.

Wraps and reels cater to continuous-process food plants and QSR bakery operations, while labels and wrap-around bands combine identification with point-of-sale storytelling. The format mix showcases paper’s versatility and its capacity to support multiple brand narratives under one converting infrastructure, deepening supplier engagement across customer portfolios.

Geography Analysis

Asia-Pacific dominated the base paper for flexible packaging market with a 36.78% revenue share in 2024 and is advancing at 9.35% CAGR through 2030, underpinned by China’s GB 43352-2023 express-packaging rules and India’s USD 204.81 billion packaging outlook.[3]Invest India, “Paper & Packaging,” investindia.gov.in Integrated pulp-to-pack converting ecosystems anchor cost competitiveness, allowing rapid scaling of coated grades that comply with evolving national standards. Southeast Asian snack and personal-care brand launches compound regional consumption, while local mills add capacity to avoid import dependence.

North America leverages mature e-commerce infrastructure to drive kraft mailer uptake. Amazon’s plastic-free fulfillment re-design validates fiber cushions, cultivating downstream demand for ultra-thin base sheets. The United States and Canada also push PFAS phase-out, nudging converters toward plant-oil barrier alternatives now commercialised in Europe. Europe’s Packaging and Packaging Waste Regulation effective February 2025 mandates recyclable solutions, stimulating multilayer-paper R&D and propelling premium pricing that offsets raw-material cost spikes.

South America and Middle East and Africa offer incremental growth where urban population expansion and commodity exports spur demand for moisture-resistant pouches and bulk commodity liners. Regional mills tap abundant forestry resources in Brazil and Chile to supply lightweight kraft to domestic and export converters, extending the footprint of the base paper for flexible packaging market beyond traditional high-income regions.

Competitive Landscape

The base paper for the flexible packaging market displays moderate fragmentation. Mondi, Stora Enso, and Smurfit WestRock combine forest resources with converting assets, creating cost synergies and speed-to-market on innovation programs. Smurfit WestRock reported USD 7.656 billion Q1 2025 net sales and plans USD 400 million synergy capture after its 2024 merger. Mondi invests EUR 400 million (USD 432 million) in a new kraft machine in Štětí, aiming for 210,000 tpa by 2025. Stora Enso ramps a EUR 1 billion (USD 1.08 billion) board line in Oulu, extending premium capacity for barrier-coated papers.

Specialty players target high-barrier niches; Amcor secured a European patent for AmFiber Performance Paper, signalling IP-driven differentiation. Billerud touts 98% fossil-free European production to win climate-conscious healthcare clients. Price swings in pulp generate margin risk, prompting converters to hedge with integrated forestry or offtake agreements while exploring alternative fibers such as bagasse or wheat straw to widen supply options.

Bio-based polymer startups emerge as indirect rivals, pitching compostable films that overlap with paper’s sustainability narrative. However, the paper incumbents leverage recycling familiarity, curb-side infrastructure, and strong brand trust to retain procurement preference. M&A momentum persists as packaging majors chase scale to fund R&D and navigate regulation, ensuring active portfolio realignment inside the base paper for flexible packaging market.

Base Paper For Flexible Packaging Industry Leaders

Stora Enso Oyj

UPM-Kymmene Corporation

Nippon Paper Industries Co., Ltd.

Smurfit Westrock PLC

Ahlstrom Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit WestRock reported USD 7.656 billion Q1 2025 net sales and announced 500,000 tons of North American paper capacity closures to optimise its mill system.

- April 2025: Packaging Corporation of America posted USD 204 million Q1 2025 net income on USD 2.1 billion sales after a 2.5% rise in corrugated shipments.

- February 2025: The EU Packaging and Packaging Waste Regulation took effect, enforcing 100% recyclable packaging by 2030 and limiting PFAS in food contact.

- January 2025: Amcor received European patent protection for AmFiber Performance Paper, enabling high-barrier recyclable packs for food and healthcare uses.

Global Base Paper For Flexible Packaging Market Report Scope

| Bleached Kraft Paper |

| Unbleached Kraft Paper |

| Coated Specialty Base Paper |

| Uncoated Specialty Base Paper |

| Below 40 gsm |

| 40-80 gsm |

| Above 80 gsm |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Home Care and Detergents |

| Industrial and Others |

| Pouches |

| Sachets and Stick Packs |

| Wraps and Reels |

| Labels and Wrap-around Bands |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Paper Type | Bleached Kraft Paper | ||

| Unbleached Kraft Paper | |||

| Coated Specialty Base Paper | |||

| Uncoated Specialty Base Paper | |||

| By Basis Weight | Below 40 gsm | ||

| 40-80 gsm | |||

| Above 80 gsm | |||

| By End-use Industry | Food and Beverage | ||

| Healthcare and Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Home Care and Detergents | |||

| Industrial and Others | |||

| By Packaging Format | Pouches | ||

| Sachets and Stick Packs | |||

| Wraps and Reels | |||

| Labels and Wrap-around Bands | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the base paper for flexible packaging market?

The base paper for flexible packaging market size stands at USD 72.68 billion in 2025 and is forecast to reach USD 90.47 billion by 2030.

Which paper type leads market revenue?

Bleached kraft paper leads with 46.12% 2024 revenue share owing to superior print quality and food-grade certifications.

Which end-use industry is growing fastest?

Healthcare and pharmaceuticals are advancing at a 9.11% CAGR through 2030 on the back of sterile-grade and medical-device applications.

How are regulations influencing material choice?

The EU Packaging and Packaging Waste Regulation effective 2025 requires 100% recyclable packaging by 2030, accelerating fiber adoption across brand portfolios.

Which region shows the highest growth rate?

Asia-Pacific registers the fastest regional CAGR at 9.35% through 2030, driven by China’s express-packaging law and India’s expanding packaged-goods sector.

Page last updated on: