Metal Print Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 124.70 Billion |

| Market Size (2031) | USD 160.33 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Print Packaging Market Analysis by Mordor Intelligence

The metal print packaging market size was valued at USD 118.82 billion in 2025 and is estimated to grow from USD 124.70 billion in 2026 to reach USD 160.33 billion by 2031, at a CAGR of 5.15% during the forecast period (2026-2031). Demand is rising as direct-to-can digital presses remove minimum-order barriers for craft beverage producers, while the European Union Carbon Border Adjustment Mechanism (CBAM) rewards low-carbon local production. Beverage brands are also adopting AI-enabled inline vision systems that cut defect waste below 0.5% at speeds above 2,000 cans per minute, improving line economics. Rapid adoption of infinitely recyclable aluminium, coupled with lightweighting programs that trim average can weight to 12.8 g, positions the substrate as the market’s value growth engine. Competitive strategies now focus on vertically integrating recycled-aluminium supply and deploying digital print capacity close to demand hubs to serve sub-10,000-unit runs profitably.

Key Report Takeaways

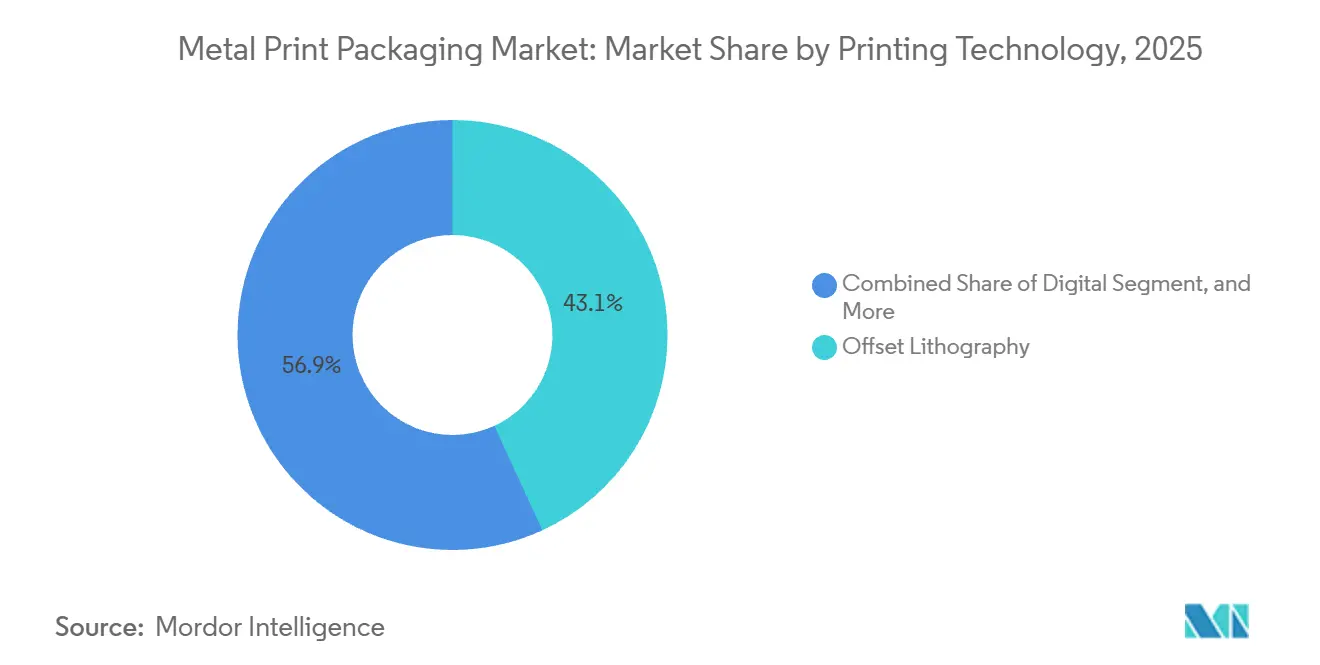

- By printing technology, offset lithography led with 43.14% of market share in 2025, while digital printing is set to advance at a 6.12% CAGR through 2031.

- By substrate material, aluminium accounted for 45.32% of the metal print packaging market share in 2025 and is forecast to expand at a 6.38% CAGR to 2031.

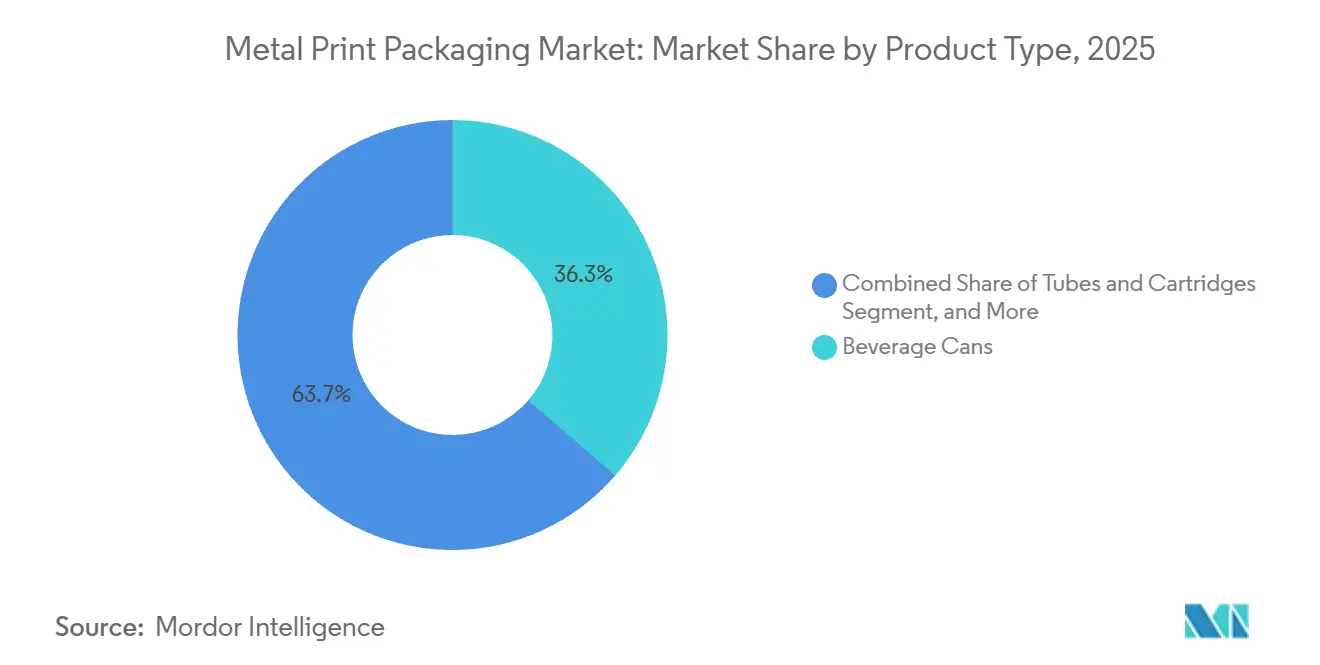

- By product type, beverage cans comprised 36.34% of market share in 2025, whereas tubes and cartridges are projected to post the fastest 6.46% CAGR to 2031.

- By end-use application, food and beverage held 40.42% market share in 2025, yet personal care and cosmetics will accelerate at a 7.19% CAGR through 2031.

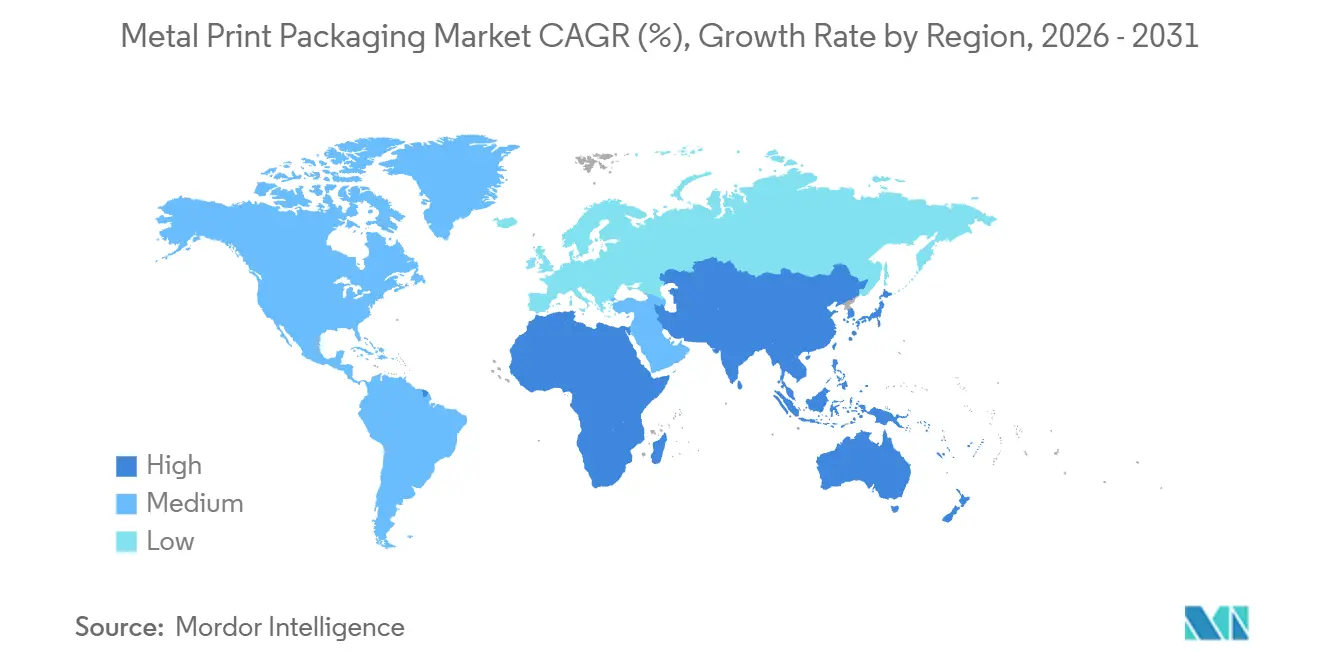

- By geography, North America generated 39.31% of market share in 2025, but Asia-Pacific is positioned for the highest 7.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Print Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Evolution of Digital Print Technology | +0.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Growth in Canned Beverage Consumption (Beer, Energy Drinks) | +1.2% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Sustainability-Driven Demand for Infinitely Recyclable Metal | +1.0% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Direct-to-Can High-Resolution Inkjet Unlocking SKU Proliferation | +0.7% | North America and Europe, craft beverage segment | Medium term (2-4 years) |

| AI-Driven Inline Vision Systems Cutting Defect Waste | +0.5% | Global, led by Europe and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| EU CBAM Favouring Low-Carbon Domestic Can Production | +0.6% | Europe, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Evolution of Digital Print Technology

Digital presses eliminate the USD 8,000-12,000 plate cost that long made offset uneconomic for small jobs, enabling converters to profit on 2,500-unit lots. Koenig and Bauer’s 600-dpi MetJET ONE delivers production-line color accuracy with inline spectrophotometry, pairing agility with premium graphics.[1]Koenig and Bauer, “MetJET ONE Direct-to-Can System,” koenig-bauer.com Craft brewers now launch twelve seasonal SKUs per year instead of four, compressing design-to-shelf cycles to 48 hours and boosting portfolio freshness. European service NOMOQ prices runs of 204 cans at USD 0.267 each, undercutting shrink sleeves and extending experimentation budgets. Crown Holdings leverages Velox inkjet lines across six sites, positioning the metal print packaging market for deeper penetration of digital economics in personal-care and RTD coffee channels.

Growth in Canned Beverage Consumption

Energy drinks in the United States expanded 8.2% by volume in 2024, aided by slim 16-oz cans commanding USD 0.15 higher retail margins than standard formats. India’s per-capita aluminium-can use reached six units in 2025 and is projected to double by 2031 as tier-2 cities gain cold-chain access. China produced 42 billion beverage cans in 2024, with baijiu-cocktail RTDs and imported-beer premiumization driving 9% output growth.[2]MIIT China, “Domestic Can Production,” miit.gov.cn Brazil’s Ambev will source 100% domestic aluminium cans by 2027, adding 2 billion units of local demand and spurring South America capacity investments .[3]Ambev, “Domestic Aluminium-Can Sourcing Commitment,” ambev.com.br These dynamics diversify the metal print packaging market beyond saturated North American volumes and reinforce medium-term expansion.

Sustainability-Driven Demand for Infinitely Recyclable Metal

The EU achieved a 23.4% circular material-use rate for aluminium in 2023, yet scrap deficits still approach 1.2 million t annually. Novelis’ USD 2.5 billion Bay Minette mill delivers 600,000 t of 90% recycled can-stock per year, tightening the scrap loop. Germany’s deposit-return scheme collects 98.5% of beverage cans, assuring high-purity alloy 3104 feed to converters. Ball’s Real Alloy integration secures recycled supply and lets European brand owners avoid CBAM penalties. Combined, these actions elevate aluminium’s role and keep the metal print packaging market aligned with corporate Scope 3 emission targets.

Direct-to-Can High-Resolution Inkjet Unlocking SKU Proliferation

Onpack Australia saves 1.1 t of shrink-sleeve film per million digitally printed cans, helping retailers meet plastic-reduction pledges. Nevertheless, ALNA Packaging notes humidity-driven dot-gain and gloss loss, mandating inline color correction to preserve brand standards. Print Design Academy finds 12% lower gloss and 8% weaker scratch resistance than offset, acceptable for limited editions but not for core SKUs. DigiCan’s 260 million-can annual capacity sits at 65% utilization, reflecting mixed customer confidence. Crown addresses finish gaps by layering digital base coats under offset overprints, blending flexibility with high-impact metallic visuals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Metal and Ink Input Prices | -0.9% | Global, acute in regions dependent on imported aluminium | Short term (≤ 2 years) |

| Competition from Alternative Packaging Substrates | -0.6% | Global, strongest in Asia-Pacific flexible-packaging markets | Medium term (2-4 years) |

| Emerging PFAS Bans Disrupting Fluoropolymer Can Coatings | -0.7% | North America and Europe, regulatory spillover to Asia-Pacific | Medium term (2-4 years) |

| Scarcity of High-Purity Recycled Aluminium Feedstock | -0.5% | Global, most acute in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Metal and Ink Input Prices

Aluminium three-month futures ranged from USD 2,340-2,760 /t in 2025, stressing converters locked into fixed-price supply contracts. Titanium dioxide hit USD 3,850 /t after Chinese plant shutdowns, forcing formulators to use heavier-coat, lower-opacity grades. A 10% Congolese cobalt export levy lifted UV-ink drier costs by USD 0.008 per can in Europe. Regional converters without hedging saw margin erosion exceeding 150 basis points, curbing capital spending. Integrated producers mitigate exposure via tolling deals, yet smaller firms in South America and Southeast Asia remain vulnerable, tempering metal print packaging market investment.

Emerging PFAS Bans Disrupting Fluoropolymer Can Coatings

U.S. FDA rules terminate PFAS in food-contact paper by 2026, and ECHA proposes extending restrictions to metal substrates by 2027. Sherwin-Williams’ fluoropolymer-free epoxy-phenolic formulas add USD 0.02-0.04 per can and cut throughput 5-8% during cure cycles. Food-safety tests reveal 10% higher oxygen ingress versus legacy coatings, shortening shelf life for nitrogenated coffee and fruit juice. Aerosol formats using propane-butane propellants face even stricter chemical-resistance hurdles, lengthening validation times. Staggered global timelines create compliance complexity that diverts engineering resources and slows new-line installations within the metal print packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Offset Dominance Meets Digital Disruption

Offset lithography contributed 43.14% of market share in 2025, capitalizing on mature presses that drop per-can costs under USD 0.05 once runs exceed 500,000 units. Digital systems, advancing at 6.12% CAGR, thrive on short-run agility, helping the metal print packaging market serve craft brewers, boutique skincare lines, and seasonal energy drinks. Gravure and flexography continue in luxury spirits and aerosols, yet VOC regulations and cylinder-engraving fees erode their competitiveness. Pad printing and hot stamping occupy ultra-premium niches, representing less than 3% of market revenue but commanding high margins through embossed metallic effects. AI-enabled registration control on new offset lines keeps waste low, stretching the installed base’s relevance while digital press count rises.

Velox-equipped Crown facilities now satisfy 18,000 new U.S. craft-beer SKUs launched during 2024, showing digital’s role as a growth lever. Koenig and Bauer’s MetalStar 3 with inline defect detection brings offset waste below 0.5%, narrowing digital’s sustainability edge. Hybrid workflows that print digital undercoats and offset top layers balance flexibility with premium gloss, accelerating technology convergence. Equipment suppliers bundle software subscriptions with hardware, moving the revenue model toward service-based uptime guarantees. Overall, printing-technology mix shifts reinforce the evolution of the metal print packaging market toward mass customisation without abandoning high-speed legacy assets.

By Substrate Material: Aluminium Leads Value And Velocity

Aluminium secured 45.32% of market share in 2025 and is expanding at a 6.38% CAGR, driven by recyclability, lighter transport weight, and CBAM-linked demand for low-carbon packaging. Tinplate remains entrenched in soups, tomatoes, and pet food, where internal pressure resistance outweighs the 15% weight penalty, but its carbon footprint is 40% higher than aluminium, pressuring European food brands to seek alternatives. Tin-free steel offers USD 80-100/t savings but suffers reduced formability, limiting its adoption in necked beverage cans. Hybrid bi-metal designs have a share of less than 2% because seam integrity between dissimilar metals complicates high-speed filling. Lifecycle studies consistently show recycled-content aluminium cutting greenhouse-gas emissions by 95%, solidifying its place in the metal print packaging market’s growth story.

Baosteel Packaging’s 2025 decision to pivot tinplate lines toward aluminium beverage-can stock underscores the trend toward lighter substrates. Novelis, Ball, and Trivium collectively commissioned over 1.5 million t of new aluminium rolling and can-sheet capacity between 2024-2026, anchoring supply for ready-to-drink expansions. Lightweighting continues, with average can walls thinning from 0.097 mm in 2020 to 0.088 mm in 2025 while maintaining buckle strength through alloy optimisation. These advances allow converters to achieve the metal print packaging market size targets without proportionally increasing primary metal demand. Circularity commitments from global brands keep aluminium investment pipelines strong despite commodity-price headwinds.

By Product Type: Beverage Cans Scale, Tubes Accelerate

Beverage cans captured 36.34% of market share in 2025 as energy-drink and hard-seltzer brands value cold-chain efficiency and premium metallic appearance. Personal-care tubes and cartridges will post the fastest 6.46% CAGR through 2031, benefiting from airless aluminium designs that protect oxygen-sensitive serums and eliminate propellants. Aerosol containers hold steady as aluminium’s compatibility with hydrocarbon gases supports deodorant and household cleaner lines, though new eco-propellant blends call for updated liner chemistries. Bottles and growlers remain a niche due to glass’s dominance in on-premise channels, but metal options gain interest for outdoor events where shatter resistance matters. Industrial pails and paint cans compete on price and account for less than 5% of the metal print packaging market.

Silgan’s 2025 Amplify pump-on-tube lets viscous formulations dispense without build-up, attracting premium skincare launches. CCL Industries added 150 million aerosol units in Mexico to meet a USD 2.7 billion U.S. body-spray market that now leans 70% aluminium. Regulatory pushes for plastic-reduction in Europe and Canada accelerate tube conversions away from laminate to collapsible metal. Beverage cans see incremental lightweighting that offsets material cost, preserving their share even as unit prices climb. Together, these shifts keep product-mix evolution central to the expansion of the metal print packaging market.

By End-Use Application: Personal Care Outpaces Food And Beverage

Food and beverage accounted for 40.42% of market share in 2025 on the strength of 320 billion aluminium beverage cans consumed globally. Personal care and cosmetics will advance at a 7.19% CAGR through 2031 as luxury fragrance, hair-care, and skincare brands adopt embossed tubes and anodised aerosols to signal premium positioning. Pharmaceuticals gain from aluminium ointment tubes that resist moisture ingress and ensure dose accuracy, yet stringent FDA 21 CFR 211 validation slows substitution cycles. Industrial chemicals continue to rely on tinplate aerosols for cost efficiency, though aluminium variants make inroads where solvent compatibility and lightweight shipping offset higher unit price. Other uses, including confectionery tins and gift boxes, stay below 8% share but benefit from seasonal demand spikes that exploit digital print’s agility.

L’Oréal’s 2024 pledge to shift half of its skincare packaging to aluminium or glass by 2028 intensifies momentum. Nielsen data show millennials and Gen Z paying 23% more for sustainable packaging, translating into price elasticity that absorbs aluminium’s premium. Unilever’s Dove aluminium deodorant sticks, launched in 2025 with 85% recycled content, set a precedent for other beauty majors. Deposit-return infrastructure growth in Asia promises higher post-consumer scrap availability, lowering cost spreads versus plastic. Altogether, evolving consumer preferences guarantee that end-use mix will continue reshaping the metal print packaging market landscape.

Geography Analysis

North America produced 100 billion beverage cans in 2025 and retained 39.31% of market share in 2025, thanks to mature deposit-return laws in ten U.S. states and every Canadian province. Craft breweries contribute high-margin short runs that digital decorators capitalize on, and AI-enabled inspection rollouts across 12 U.S. lines lowered scrap costs by USD 4.2 million annually. Recycling infrastructure delivers 75% recovery of aluminium cans, feeding domestic remelt furnaces and reducing reliance on imported primary metal. Nevertheless, labour shortages elevate operating costs, prompting converters to automate palletisation and logistics. Incremental capacity expansions by CANPACK and Ball in New York and Georgia maintain regional supply-demand balance and reinforce North America’s contribution to the metal print packaging market.

Asia-Pacific will post a 7.08% CAGR through 2031, driven by India’s projected rise to 12 cans per capita and China’s 2024 production footprint of 42 billion units. Government incentives in Guangdong and Jiangsu support state-backed can-line expansions that target RTD cocktails, energy drinks, and imported craft beers. Toyo Seikan’s 500 million-unit Guangdong joint venture offsets Japanese export declines and supplies premium offset-decorated cans to domestic breweries. Southeast Asian nations such as Vietnam and Indonesia register double-digit canned coffee growth, while Australia’s craft beer boom fuels demand for digital runs that Onpack’s Rocklea line now fulfills. Rising middle-class purchasing power and rapid cold-chain rollout ensure that Asia-Pacific remains pivotal to the long-term growth of the metal print packaging market.

Europe represents a mature yet transforming landscape where CBAM’s phased tariffs spur re-shoring of can-sheet sourcing. Germany, France, and the United Kingdom consumed 35 billion beverage cans in 2024, but new investments focus on carbon-optimized furnaces powered by wind and solar. Ardagh and Crown both committed to 50% Scope 1 and 2 cuts by 2030, aligning with corporate buyer emissions targets. Eastern Europe sees capacity growth in Poland and Romania as converters seek lower-cost labour while remaining inside the EU carbon-trade perimeter. Middle East and Africa, though currently the smallest regional contributor, accelerates with Saudi Arabia’s Vision 2030 incentives and South Africa’s 62% first-year can recovery rate, setting the stage for future aluminium-centric plant announcements that will broaden the geographic reach of the metal print packaging market.

Competitive Landscape

The Market is fragmented with players like Ball Corporation, Crown Holdings, Ardagh Metal Packaging and Others. Ball’s 2026 Real Alloy integration raised recycled content to 90%, allowing European customers to avoid virgin-metal EPR surcharges and pay USD 0.03-0.05 premiums for low-carbon cans. Crown partnered with Velox to field six direct-to-shape inkjet lines, targeting sub-5,000-unit craft runs priced at EUR 0.25 (USD 0.27) per can and undercutting shrink sleeves by USD 0.15. Ardagh’s decarbonization roadmap centers on renewable-powered furnaces and closed-loop water systems, with a USD 180 million Huizhou plant commissioned in 2025 delivering a 45% Scope 1 cut.

Regional challengers such as CANPACK, Envases Universales, and Toyo Seikan defend share through proximity to fillers and rapid artwork turnaround. CANPACK’s USD 200 million Nichols, New York expansion added 1.2 billion cans and integrated AI vision, trimming defect waste to 0.5% while serving Northeastern craft brewers. Envases Universales grew tinplate food-can capacity in Monterrey to tap South America's ready-meal demand, balancing its aluminium exposure. Toyo Seikan’s Guangdong venture fuses Japanese print quality with Chinese market access, capturing premium RTD beverage accounts that demand 600-line-per-inch resolution. These moves illustrate how local responsiveness tempers the global consolidation of the metal print packaging market.

Upstream and downstream partners also influence competition. Novelis’ 600,000 t Bay Minette rolling mill and Sun Chemical’s 60% lower-energy GREENLEAF UV-LED inks shift cost curves in favour of integrated players. Krones’ AI inspection subscriptions create ecosystems where converters pay for performance improvements rather than one-time capital, tying plant upgrades to vendor service contracts. Digital disruptors NOMOQ and DigiCan challenge incumbents by quoting per-can prices that enable hobby-scale runs, though utilization challenges persist. Collectively, these strategic vectors keep the competitive intensity of the metal print packaging market moderate yet dynamic, sustaining innovation across substrates, coatings, and press technology.

Metal Print Packaging Industry Leaders

Crown Holdings, Inc.

Ball Corporation

Ardagh Metal Packaging S.A.

CCL Industries Inc.

Toyo Seikan Group Holdings, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ball Corporation completed Real Alloy integration, achieving 90% recycled-content cans across North America.

- January 2026: Crown Holdings installed three additional Velox inkjet presses in Germany, the United Kingdom, and Poland.

- December 2025: Ardagh commissioned a USD 180 million Huizhou can plant powered by renewable energy.

- November 2025: Novelis fully commissioned its USD 2.5 billion Bay Minette rolling mill with 90% recycled content.

Global Metal Print Packaging Market Report Scope

The report tracks the adoption of different printing processes used for metal printing, such as offset lithography, gravure, flexography, digital, and other printing technologies. Metallic printed packaging relies on materials such as aluminum, tin, or steel to make packaging containers for various products. It is easy to use and unbreakable and can withstand extreme pressures and temperatures.

The Metal Print Packaging Market Report is Segmented by Printing Technology (Offset Lithography, Gravure, Flexography, Digital, and Other Printing Technologies), Substrate Material (Aluminium, Steel Tinplate, Tin-free Steel, and Other Substrate Materials), Product Type (Beverage Cans, Aerosol Containers, Bottles and Growlers, Tubes and Cartridges, and Other Product Types), End-Use Application (Food and Beverage, Personal Care and Cosmetics, Pharmaceuticals and Healthcare, Industrial and Household Chemicals, and Other End-use Applications), and Geography (North America, South America, Europe, Asia-Pacific,and Middle East and Africa). The Market Forecasts are Provided in Terms of Value USD.

| Offset Lithography |

| Gravure |

| Flexography |

| Digital |

| Other Printing Technologies |

| Aluminium |

| Steel (Tinplate) |

| Tin-free Steel |

| Other Substrate Materials |

| Beverage Cans |

| Aerosol Containers |

| Bottles and Growlers |

| Tubes and Cartridges |

| Other Product Types |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals and Healthcare |

| Industrial and Household Chemicals |

| Other End-use Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Printing Technology | Offset Lithography | ||

| Gravure | |||

| Flexography | |||

| Digital | |||

| Other Printing Technologies | |||

| By Substrate Material | Aluminium | ||

| Steel (Tinplate) | |||

| Tin-free Steel | |||

| Other Substrate Materials | |||

| By Product Type | Beverage Cans | ||

| Aerosol Containers | |||

| Bottles and Growlers | |||

| Tubes and Cartridges | |||

| Other Product Types | |||

| By End-Use Application | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceuticals and Healthcare | |||

| Industrial and Household Chemicals | |||

| Other End-use Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of global metal print packaging by 2031?

It is forecast to reach USD 160.33 billion, reflecting a 5.15% CAGR between 2026-2031.

Which substrate is expanding fastest in metal print formats?

Aluminium leads with a 6.38% CAGR, buoyed by lightweighting, high recycled-content targets, and CBAM incentives.

How does digital direct-to-can printing benefit brand owners?

Eliminating plate costs lets converters profit from 2,500-unit runs, cutting lead times to days and supporting rapid SKU launches.

Why is Asia-Pacific considered the highest-growth region?

Rising per-capita beverage-can use in India and large-scale capacity additions in China drive a 7.08% CAGR through 2031.

What impact will PFAS bans have on can coatings?

U.S. and EU restrictions compel a switch to fluoropolymer-free epoxy-phenolic systems, adding up to USD 0.04 per can and reducing line speed by as much as 8%.

How are leading suppliers securing recycled aluminium feedstock?

Strategies include Ball’s Real Alloy vertical integration, Crown’s multi-year scrap contracts, and Novelis’ 600,000 t Bay Minette rolling mill focused on 90% recycled content.

Page last updated on: