Flexible Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 280.15 Billion |

| Market Size (2031) | USD 341.06 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

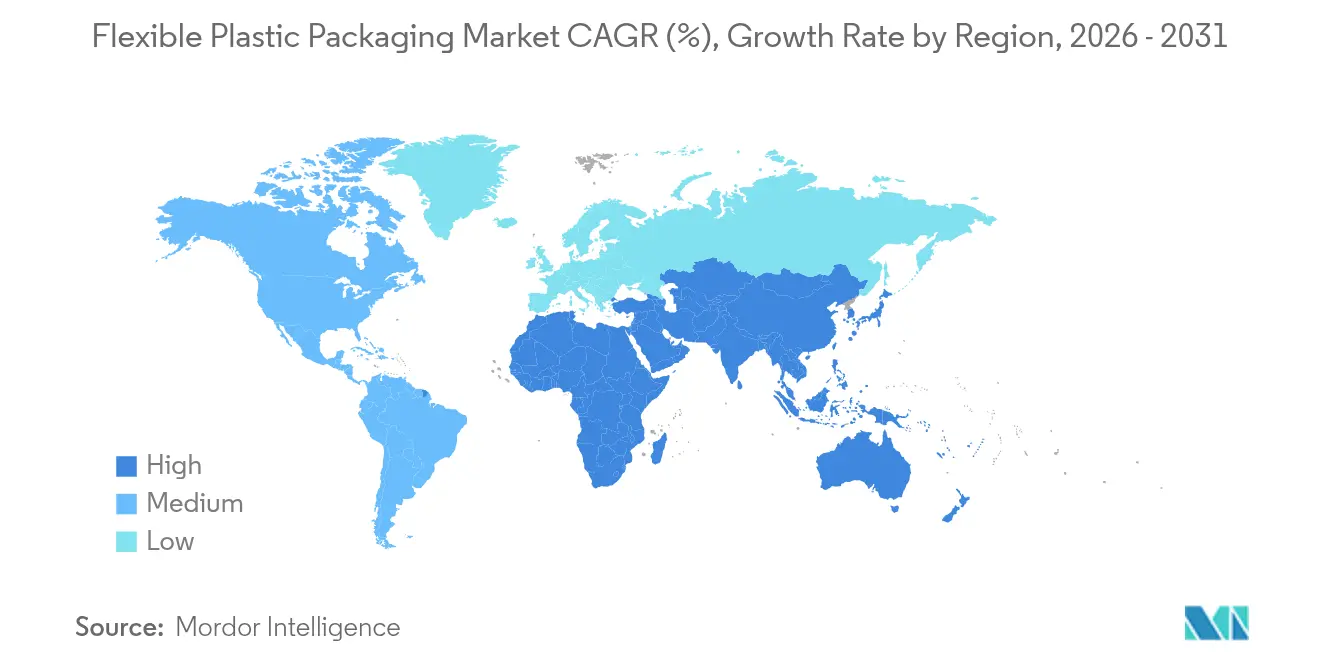

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Plastic Packaging Market Analysis by Mordor Intelligence

The flexible plastic packaging market size is expected to grow from USD 269.35 billion in 2025 to USD 280.15 billion in 2026 and is forecast to reach USD 341.06 billion by 2031 at 4.01% CAGR over 2026-2031. Demand resilience stems from e-commerce fulfilment, high-speed snack lines, and pharmaceutical cold-chain expansion, all of which reward suppliers able to combine durability with circular-economy compliance. Regulatory pressure—most visibly the EU’s Packaging and Packaging Waste Regulation—accelerates the shift toward mono-material structures rich in post-consumer recycled (PCR) polyethylene. Brand owners also prize digital printing for short-run customization, while resin price volatility forces converters to refine hedging strategies and pursue vertical integration. Consolidation, capped by the Amcor–Berry Global merger, intensifies competition around sustainable designs and recycling infrastructure.

Key Report Takeaways

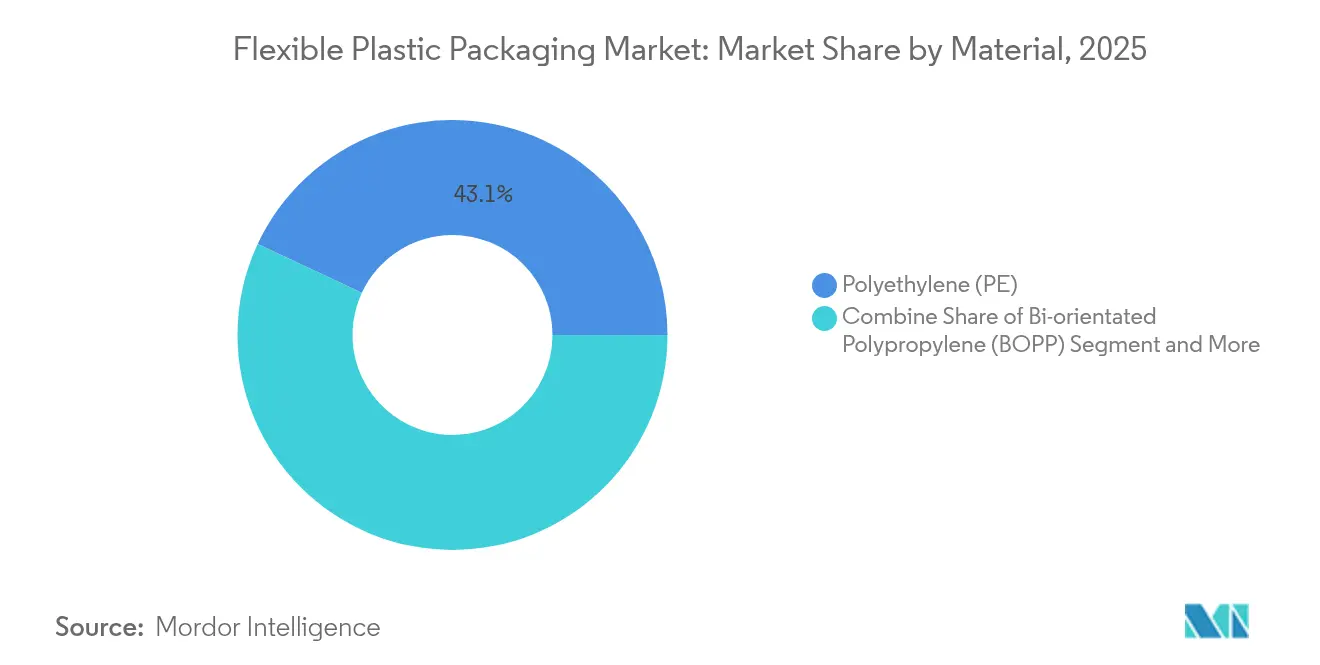

- By material, polyethylene held 43.05% of flexible plastic packaging market share in 2025; biaxially oriented polypropylene is projected to grow at a 4.65% CAGR through 2031.

- By product type, pouches commanded 45.12% revenue in 2025, while films and wraps are advancing at a 3.6% CAGR to 2031.

- By printing technology, flexography led with 39.68% share in 2025; digital printing is expanding at a 7.45% CAGR to 2031.

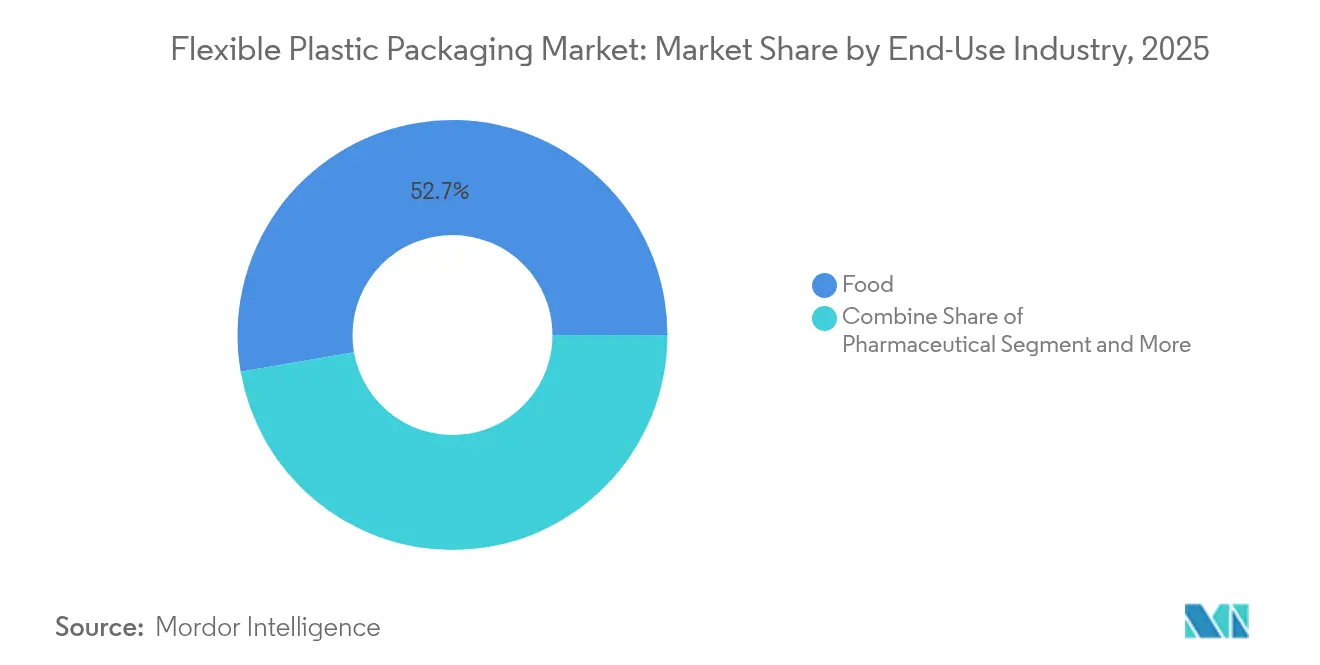

- By end-use industry, food accounted for 52.74% of the flexible plastic packaging market size in 2025, whereas pharmaceuticals are poised for a 6.05% CAGR through 2031.

- By distribution channel, direct sales led with 58.3% share in 2025; indirect sales is expanding at a 5.5% CAGR to 2031.

- By geography, Asia-Pacific captured 41.45% revenue in 2025 and is expected to expand at a 4.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of High-Speed F/F/S Lines in Asian Snack‐Food Plants | +0.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| E-commerce-Led Demand for Durable Mailer Films in North America | +0.6% | North America & EU | Short term (≤ 2 years) |

| EU "Plastic Tax" Accelerating Shift to Recyclate-Rich PE Films | +0.7% | Europe, with regulatory spill-over to Global | Medium term (2-4 years) |

| Pharma Cold-Chain Expansion Requiring High-Barrier EVOH Laminates | +0.5% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Demand Surge for Stand-Up Pouches in RTD Beverages (ASEAN) | +0.4% | ASEAN core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Brand-Owner Switch to Mono-Material Structures for Circularity Targets | +0.6% | Global, led by EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of High-Speed F/F/S Lines in Asian Snack-Food Plants

Snack manufacturers across India, China, and ASEAN are installing next-generation form/fill/seal units capable of 180 packs per minute, cutting human intervention and downtime. Balaji Wafers’ adoption of collaborative palletizing robots illustrates a region-wide shift that raises demand for heat-sealable polyethylene films able to retain integrity at elevated sealing jaws Intralox. Faster lines compel converters to fine-tune slip, coefficient-of-friction, and hot-tack performance to avoid stoppages that erode operating margins. Secondary packaging is equally affected because automated case packers need consistent film stiffness to ensure smooth forming. As brand portfolios multiply, flexible plastic packaging market suppliers that offer rapid color changes and shorter lead times gain a competitive edge.

E-commerce-Led Demand for Durable Mailer Films in North America

Parcel volumes in the United States surpassed 24 billion in 2024, pressuring retailers to replace corrugated shippers with lighter co-extruded mailer films that survive automated sortation belts. Producers now engineer three-layer polyethylene structures featuring >30% PCR without sacrificing puncture resistance, thereby satisfying retailer mandates and How2Recycle store-drop-off criteria EcoEnclose. The need for branding flexibility fosters adoption of white-ink digital presses that print barcodes and variable data in a single pass. Consequently, the flexible plastic packaging market benefits from higher value-added film specifications even as resin tonnage grows modestly.

EU Plastic Tax Accelerating Shift to Recyclate-Rich PE Films

The Packaging and Packaging Waste Regulation introduces modulated eco-fees that reward mono-material designs and penalize difficult-to-recycle laminates, effectively adding EUR 800 per tonne to multilayer waste streams SGS. Brand owners therefore pivot toward all-PE stand-up pouches that incorporate EVOH below the 5% threshold to remain recyclable. Reifenhäuser’s blown-film lines with inline MDO create clear PE replacement for BOPET, helping converters achieve 35% recycled content targets by 2030 Reifenhauser. The regulation’s influence extends globally because multinational FMCGs standardize artwork and specifications to streamline procurement.

Pharma Cold-Chain Expansion Requiring High-Barrier EVOH Laminates

Global spending on temperature-controlled pharmaceutical logistics is projected to hit USD 26.2 billion by 2030, underpinned by biologic therapies and mRNA vaccines. Multilayer films pairing EVOH with PE or PP achieve <0.2 cc/m²-day oxygen transmission at 23 °C, a benchmark demanded by regulators for parenteral drugs. Kuraray’s EVAL™ grades meet these thresholds while retaining clarity and gamma-sterilization compatibility Kuraray. Validation cycles are lengthy, locking in supplier relationships and granting price premiums that lift overall flexible plastic packaging market profitability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Pass-Through Pressure from Volatile C6 Monomer Pricing | -0.5% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Limited PCR Supply Hindering Food-Grade Recyclate in EU | -0.4% | Europe, with regulatory spill-over effects | Medium term (2-4 years) |

| Proposed U.S. Extended-Producer-Responsibility (EPR) Fees | -0.3% | North America, with state-level variations | Medium term (2-4 years) |

| Rising Adoption of Molded-Fiber Trays in Premium Produce | -0.2% | Global, led by North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Pass-Through Pressure from Volatile C6 Monomer Pricing

Surging US ethane exports and new Chinese steam-cracker startups whipsaw C6 hexene costs, forcing film converters to renegotiate monthly resin surcharges. In 2024, HDPE film values in China fell 12% while LLDPE slipped 7%, squeezing converters tied to fixed-price contracts ChemOrbis. Lacking scale, small processors absorb margin erosion or risk losing shelf space due to rapid quotation changes. Some hedge via multi-year off-take agreements, but credit requirements limit participation.

Limited PCR Supply Hindering Food-Grade Recyclate in EU

Meeting the EU’s 30% recycled-content mandate by 2030 hinges on food-contact PCR streams, yet certified volumes cover barely one-quarter of demand. Contamination and color variability push food-grade PP pellet prices 25% above prime resin, prompting brand owners to seek chemical-recycling feedstock despite higher carbon intensity Cirplus. Converter uncertainty delays investment in de-inking and washing capacity, slowing flexible plastic packaging market adoption of full-loop materials. Regulatory bottlenecks at EFSA further extend approval timelines, complicating supply planning for multinational FMCGs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PE Dominance Faces BOPP Innovation

Polyethylene retained 43.05% flexible plastic packaging market share in 2025, underpinning vast volumes of snack pouches and shipping films. Its cost-to-performance ratio and evolving mono-material laminates keep adoption high even as price volatility persists. The flexible plastic packaging market size for polyethylene is projected to grow at a steady pace as converters commercialize all-PE barrier webs incorporating minimal EVOH. BOPP, however, records the quickest gains with a 4.65% CAGR to 2031, thanks to its tensile strength and gloss that attract premium snack and tobacco brands.

BOPP’s orientation process delivers down-gauging potential of up to 20%, cutting material usage and transit weight. Hub investments by Asian producers shorten lead times, improving supply certainty for Western brand owners. Specialty resins, notably EVOH and compostable biopolymers, address niche pharmaceutical and regulatory environments. While polyvinyl chloride continues to decline amid food-contact bans, cast PP and metallized PET maintain roles where moisture and aroma barriers outweigh recyclability concerns.

By Product Type: Pouch Leadership Meets Film Innovation

Pouches captured 45.12% revenue in 2025, cementing their position through convenience features like tear notches and recloseable spouts. The flexible plastic packaging market size attributed to pouches remains robust given stand-up formats that maximize shelf presence. Film-based solutions, however, deliver the fastest 3.6% CAGR as e-commerce replaces corrugated shippers with co-extruded mailers and bubble films.

High-speed horizontal form/fill/seal machines, now topping 2,000 units per minute, demand tight gauge tolerances to prevent tearing at knife cut-off points. Bag and sack applications in fertilizer and animal feed preserve demand for thicker laminated constructions, while specialty wrap formats enter medical drape and diagnostic test-kit markets. Manufacturers prioritize mono-material pouch replacements to keep multi-layer functionality without sacrificing circularity.

By Printing Technology: Digital Disruption Accelerates

Flexography held a 39.68% slice of the flexible plastic packaging market in 2025 by excelling at high-volume SKUs with four-color graphics. Even so, digital printing races ahead at a 7.45% CAGR, underpinned by HP Indigo 200K installations that run 30% faster than prior models American Packaging Corporation. Digital presses support variable data, versioning, and design-to-ship cycles under seven days, satisfying retailer promotion calendars.

Hybrid workflows merge flexo white lay-downs with digital CMYK finishes, optimizing cost per impression while curbing waste. Rotogravure persists in ultra-long-run confectionery wraps where 8+ color precision justifies cylinder investment. Water-based ink and UV-LED curing in both flexo and digital systems reduce volatile organic compounds, aligning print technology choices with carbon-reduction goals.

By End-Use Industry: Food Dominance Meets Pharma Growth

Food retained 52.74% revenue in 2025, with emerging Asia’s snacking culture and single-serve portions driving incremental volume. Convenience foods, fresh produce, and dairy adopt resealable pouch formats that extend shelf life without secondary tubs. The flexible plastic packaging market size for pharmaceutical uses is projected to expand at 6.05% CAGR through 2031 as biologics pipelines mature.

Thermoformed blister webs and IV bag laminates use co-extruded structures with EVOH and cyclic olefin copolymer layers to satisfy oxygen and moisture thresholds. Beverage brands shift from rigid PET bottles to spouted pouches, cutting transport emissions by up to 60%. Personal and home-care segments pursue refill pouches that reduce plastic intensity, while industrial bulk sacks rely on woven PP to withstand 25 kg load requirements.

By Distribution Channel: Direct Sales Efficiency Drives Growth

Converters distribute roughly 58.3% of output via direct relationships, optimizing lead-time control and technical service. Contract lengths average three years, covering film development, print management, and on-site troubleshooting. Distributors, however, post the highest 5.5% CAGR as global suppliers court mid-tier regional brands across Latin America and Africa.

Digital ordering portals allow smaller bakeries or agri-exporters to configure artwork online, receive dieline proofing, and track production slots—an advance that levels access once reserved for large multinationals. Strategic alliances with logistics providers shorten last-mile delivery, enhancing distributor relevance. The flexible plastic packaging industry increasingly combines virtual quoting with regional warehouses to balance customization and throughput.

Geography Analysis

Asia-Pacific accounted for 41.45% flexible plastic packaging market share in 2025 and registers a 4.12% CAGR on the back of rising middle-class consumption. India alone targets 25 million tonnes of polymer processing capacity by 2030, while China brings 5 million tonnes of new PE lines onstream in 2025, sustaining feedstock supply. ASEAN governments embed extended producer responsibility into waste-management bills, steering procurement toward recyclable mono-material solutions.

North America remains an innovation hub, blending brand scrutiny of packaging life-cycle footprints with state-level EPR schemes that levy eco-fees on non-recyclable materials. E-commerce parcel volumes alone enlarge demand for protective co-ex films that shield goods against temperature swings. Europe’s regulatory rigor enforces 30% PCR levels in contact-sensitive applications, pushing chemical-recycling pilots into commercial scale.

The Middle East and Africa absorb pouch technology for fortified powdered milk and condiments, supported by improved cold chains. Latin American markets align with MERCOSUR labeling rules, aiding cross-border FMCG supply. Although smaller in size, both regions exhibit double-digit uptake of stand-up pouches due to lightweight shipping advantages and limited recycling infrastructure.

Mordor Intelligence provides coverage of the flexible plastic packaging market across other key regional markets, including Europe, North America, Latin America, Middle East and Africa, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Spain, United States, Argentina, Egypt, and China incorporating local coverage and market participation, as required.

Competitive Landscape

Industry is fragmented. Amcor merged with Berry Global, forming a USD 30 billion revenue entity with unmatched resin purchasing leverage. The enlarged group pairs surface-print expertise with closed-loop recycling plants, enabling cradle-to-cradle client solutions. Private-equity interest also sharpened as One Rock Capital Partners acquired Constantia Flexibles, underscoring the sector’s cash-flow resilience Constantia Flexibles.

Technology investment differentiates incumbents. American Packaging’s digital hub cuts SKU launch lead times to five days, winning contracts from craft snack start-ups. ExxonMobil collaborates with converters on proprietary PE tie-layer resins that eliminate laminated PET, decreasing carbon intensity by 18%. European players like Mondi pilot paper-flexibles hybrids aiming for curbside recyclability, although performance parity with plastic remains inconsistent.

Competitive dynamics increasingly revolve around PCR sourcing contracts, life-cycle-assessment transparency, and additive manufacturing of custom sealing jaws that extend machine uptime. Market entrants focusing on bio-circular feedstocks such as used-cooking-oil-derived PP (Braskem WENEW) gain attention, yet scalability hurdles temper near-term volume. Overall, top-five suppliers command roughly 45% combined revenue, indicating moderate concentration and room for regional specialists.

Flexible Plastic Packaging Industry Leaders

Amcor PLC

Mondi PLC

Sealed Air Corporation

Huhtamaki Oyj

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Amcor and Berry Global shareholders approved their business combination, forming a packaging giant with expanded recycling assets.

- January 2025: American Packaging Corporation launched its end-to-end flexible packaging digital unit powered by HP Indigo 200K presses.

- January 2025: DS Smith introduced TailorTemp, a recyclable fiber-based cold-chain pack designed to maintain 2–8 °C for 36 hours.

- December 2024: Carton Pack acquired Clifton Packaging Group, extending snack and protein pouch capabilities in Europe.

Global Flexible Plastic Packaging Market Report Scope

Flexible plastic packaging optimizes sustainability, product safety during transit and storage, and space efficiency by blending film and plastic materials. The study covers the flexible packaging market tracked in terms of consumption and is limited to flexible packaging products made from plastic. The study analyzes the factors that impact geopolitical developments in the studied market based on the prevalent base scenarios, key themes, and end-user industries-related demand cycles. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period.

The Flexible Plastic Packaging Market Report is Segmented by Material (Polyethene [PE], Bi-Oriented Polypropylene [BOPP], Cast Polypropylene [CPP], Polyvinyl Chloride [PVC], Ethylene Vinyl Alcohol [EVOH], and Other Material Types [Polycarbonate, PHA, PLA, Acrylic, and ABS]), Product Type (Pouches, Bags, Films and Wraps, and Other Product Types), End-User Industry (Food [Frozen Food, Dry Food, Meat, Poultry, and Sea Food, Candy & Confectionery, Pet Food, Dairy Products, Fresh Produce and Other Food (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)], Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End User Industry [Automotive, Chemical, Agriculture ]), and Geography (North America [United States and Canada], Europe [France, Germany, Italy, United Kingdom,Spain, Poland, Nordic and Rest of Europe], Asia-Pacific [China, India, Japan, Thailand, Indonesia, Vietnam, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, Egypt, South Africa, Nigeria, Morocco and Rest of Middle East and Africa]). The report offers market forecasts and size in volume (tonnes) for all the above segments.

| Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) |

| Cast Polypropylene (CPP) |

| Polyvinyl Chloride (PVC) |

| Ethylene-Vinyl Alcohol (EVOH) |

| Other Materials |

| Pouches |

| Bags and Sacks |

| Films and Wraps |

| Other Product Types |

| Flexography |

| Rotogravure |

| Digital (Inkjet, Electrophotography) |

| Food | Confectionery and Snacks |

| Breads and Cereals | |

| Fresh Produce | |

| Dairy based products | |

| Other Food | |

| Beverages | |

| Medical and Pharmaceutical | |

| Personal and Home Care | |

| Other End -Use Industry |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Polyethylene (PE) | ||

| Biaxially Oriented Polypropylene (BOPP) | |||

| Cast Polypropylene (CPP) | |||

| Polyvinyl Chloride (PVC) | |||

| Ethylene-Vinyl Alcohol (EVOH) | |||

| Other Materials | |||

| By Product Type | Pouches | ||

| Bags and Sacks | |||

| Films and Wraps | |||

| Other Product Types | |||

| By Printing Technology | Flexography | ||

| Rotogravure | |||

| Digital (Inkjet, Electrophotography) | |||

| By End-Use Industry | Food | Confectionery and Snacks | |

| Breads and Cereals | |||

| Fresh Produce | |||

| Dairy based products | |||

| Other Food | |||

| Beverages | |||

| Medical and Pharmaceutical | |||

| Personal and Home Care | |||

| Other End -Use Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current market size of flexible plastic packaging?

The flexible plastic packaging market size is USD 280.15 billion in 2026, with expansion projected to USD 341.06 billion by 2031.

Which region leads demand for flexible plastic packaging?

Asia-Pacific holds 41.45% revenue share, driven by rapid manufacturing growth and rising consumer spending.

Why is digital printing growing so quickly in flexible packaging?

Digital presses enable short runs, variable data, and faster design-to-shelf cycles, posting a 7.45% CAGR through 2031.

How are EU regulations shaping material choices?

The Packaging and Packaging Waste Regulation imposes recycled-content quotas and eco-fees, pushing converters toward mono-material PE films with PCR content.

What segment shows the fastest growth rate?

Pharmaceutical applications lead with a 6.05% CAGR, reflecting cold-chain expansion and stringent barrier requirements.

Page last updated on: