Digital Pathology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 9.90% CAGR |

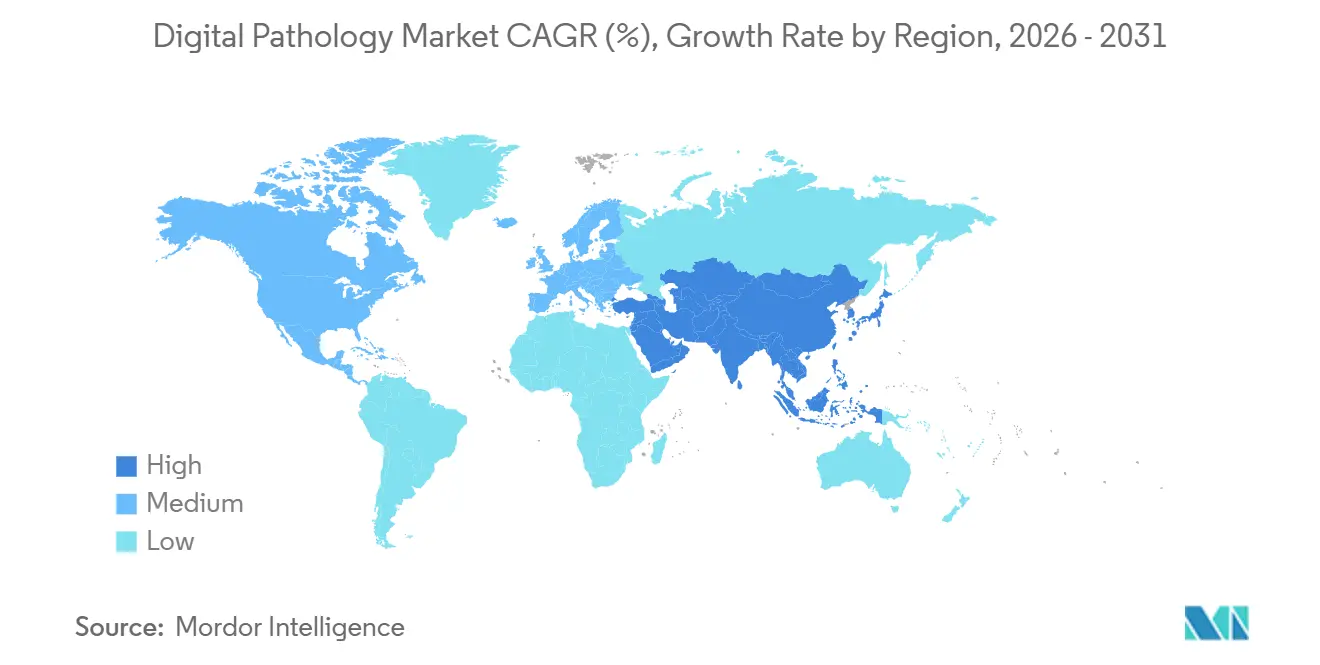

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

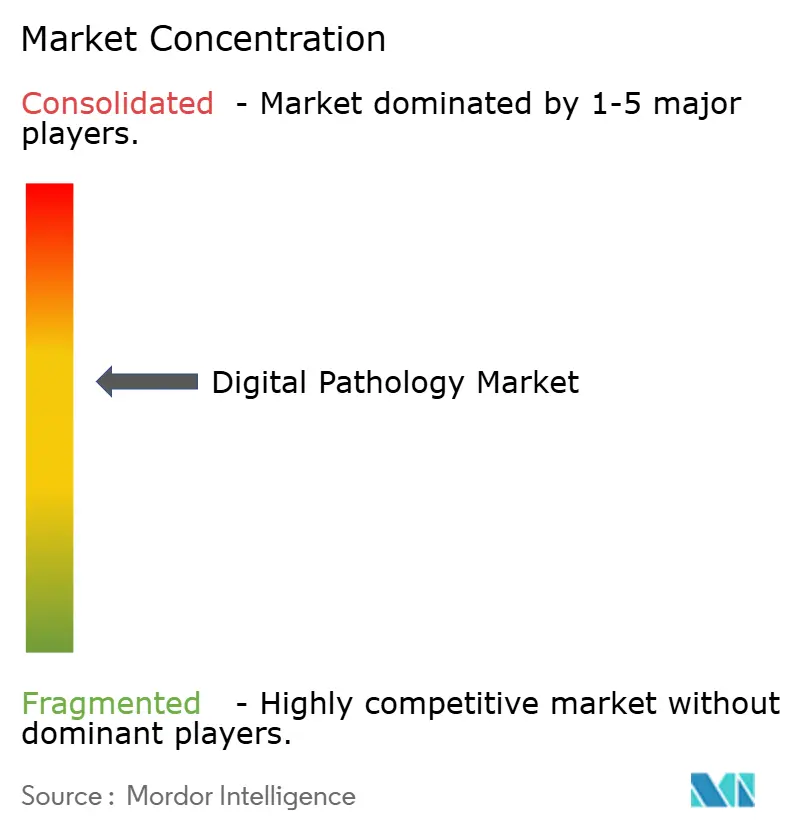

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Pathology Market Analysis by Mordor Intelligence

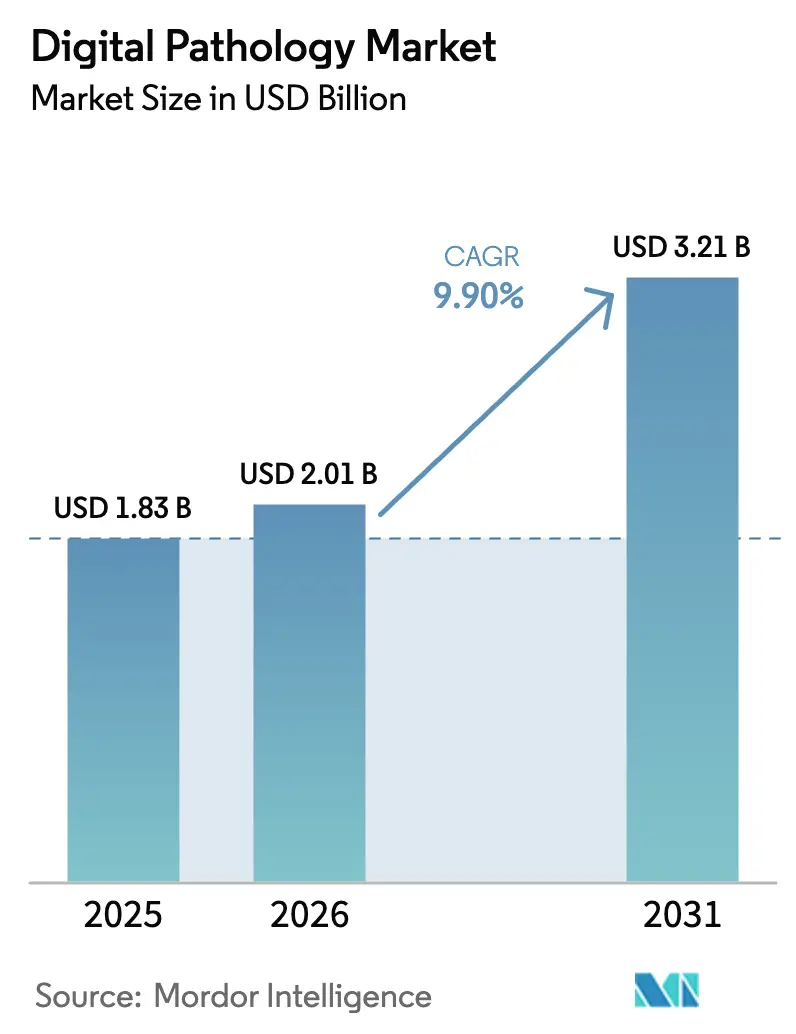

The Digital Pathology Market size is expected to increase from USD 1.83 billion in 2025 to USD 2.01 billion in 2026 and reach USD 3.21 billion by 2031, growing at a CAGR of 9.90% over 2026-2031.

Hospitals are digitizing slides to alleviate acute pathologist shortages, pharmaceutical sponsors are demanding image-based biomarker endpoints, and regulators have cleared multiple whole-slide imaging (WSI) platforms for primary diagnosis, closing historic compliance gaps [1]U.S. Food and Drug Administration, “Device Approvals,” fda.gov. Commercial momentum accelerated after the National Institutes of Health’s Bridge2AI program allotted USD 150 million in 2025 to validate pathology algorithms, while new CPT reimbursement codes began compensating remote consultations. At the same time, spatial-omics workflows that fuse morphology with proteomic or transcriptomic data are expanding scanner budgets beyond traditional brightfield devices. Scanner vendors now bundle software subscriptions instead of one-time hardware sales, shifting revenue to recurring models that laboratories find easier to justify within operating budgets.

Key Report Takeaways

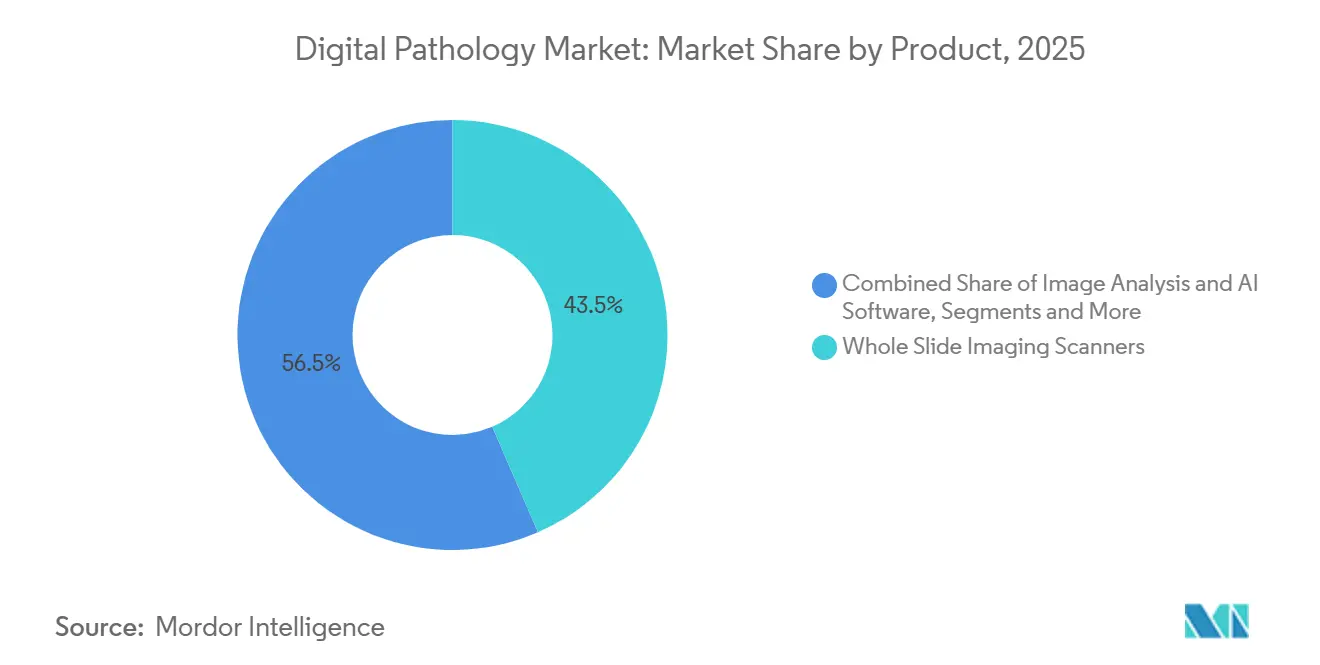

- By product, Whole Slide Imaging Scanners held 43.5% of the digital pathology market share in 2025, while Image Analysis & AI Software is forecast to grow at a 10.21% CAGR through 2031.

- By imaging technique, Brightfield accounted for an 85.1% share of the digital pathology market size in 2025, whereas Fluorescence imaging is advancing at a 10.55% CAGR.

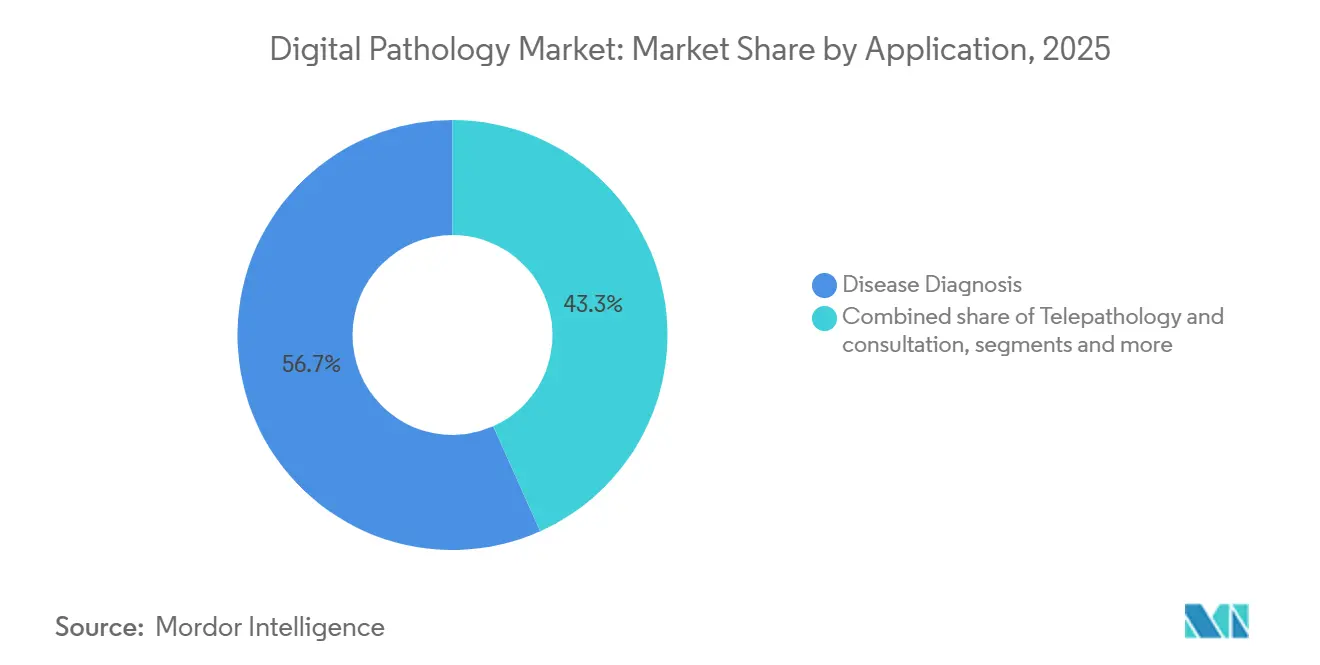

- By application, Disease Diagnosis captured 56.7% revenue share in 2025; Telepathology & Consultation is projected to expand at a 10.39% CAGR to 2031.

- By end user, Hospital & Reference Laboratories led with 38.4% of the digital pathology market share in 2025, while Pharmaceutical & Biotechnology Companies & CROs are growing at a 10.47% CAGR.

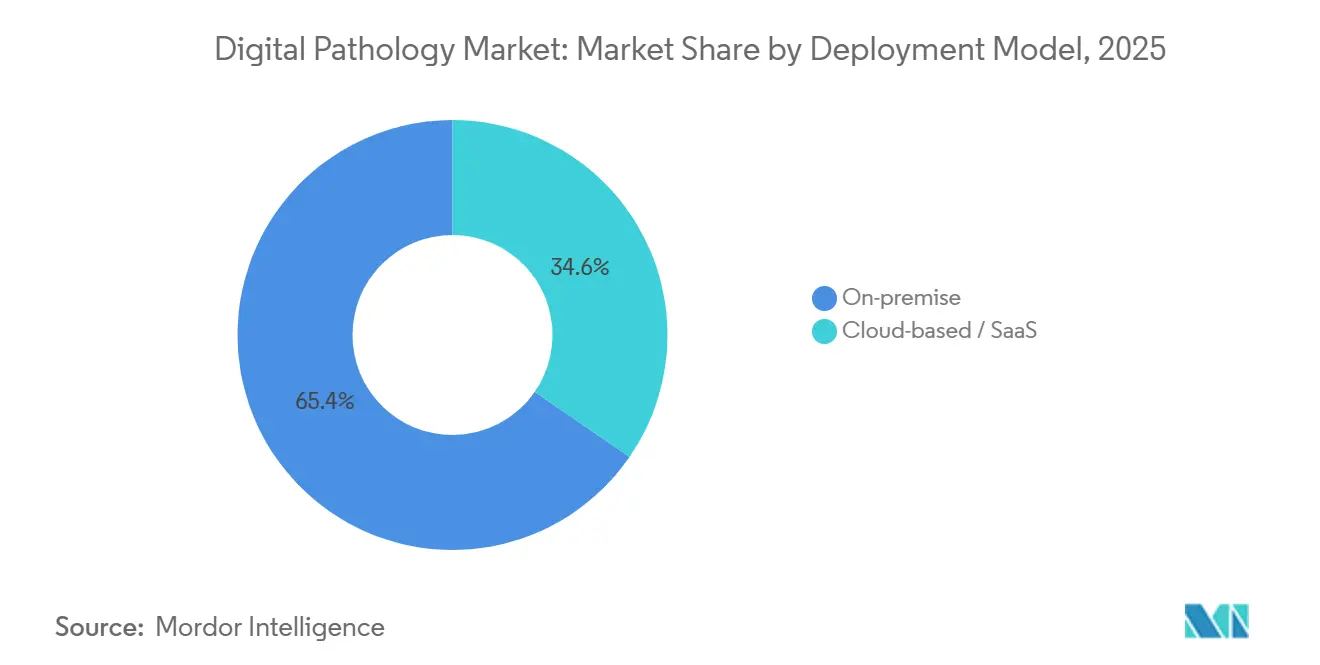

- By deployment model, On-premise installations represented 65.4% of 2025 spending, yet Cloud-based solutions are increasing at a 10.16% CAGR.

- By geography, North America commanded 47.8% revenue in 2025 and Asia-Pacific is set to post the fastest 11.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Pathology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pathologist Workforce Shortages Accelerate Automation-Enabled Digital Workflows | +2.1% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Large Oncology / Immunotherapy Trials Mandate Image-Based Biomarker Assessment | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Government Healthcare-Digitization & National AI Grants/Fast-Tracks | +1.5% | APAC core, spill-over to MEA & South America | Medium term (2-4 years) |

| Growth of Companion Diagnostics Needs Quantitative Tissue-Image Analytics | +1.3% | Global, led by North America & EU | Long term (≥ 4 years) |

| FDA Synthetic-Tissue Dataset Pilot Speeds Algorithm Approvals | +0.9% | North America, EU adoption following | Short term (≤ 2 years) |

| Spatial-Omics Integration Drives High-Plex Imaging Demand | +1.2% | North America & EU research hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pathologist Workforce Shortages Accelerate Automation-Enabled Digital Workflows

Workforce models published in 2024 predicted the United States will be short 5,900 pathologists by 2030, equal to 18% of present capacity [2]Association of American Medical Colleges, “2024 Physician Workforce Projections,” aamc.org. Forty percent of consultant positions in the United Kingdom stayed vacant for more than six months in 2025. Digital platforms let one specialist review cases from several hospitals without shipping glass slides, effectively multiplying throughput. A 2025 College of American Pathologists study confirmed that AI-guided prescreening shortened routine biopsy turnaround time significantly with high diagnostic concordance. Hospitals are therefore redirecting capital from new hires to scanners and algorithm subscriptions that cost less than annual physician salaries.

Large Oncology/Immunotherapy Trials Mandate Image-Based Biomarker Assessment

Investigational new drug filings in immuno-oncology climbed to 1,847 in 2025, and 68% required digital quantification of PD-L1, tumor mutational burden, or immune-cell density. Manual scoring shows inter-observer variability exceeding 20% for PD-L1, whereas validated AI algorithms push variability below 5%, satisfying regulatory precision thresholds. Roche revealed that 82% of its late-stage oncology studies centralized slide review on digital platforms in 2025. Contract research organizations have mirrored this shift, installing scanners at regional hubs so international sites upload images to a single repository, insulating demand from hospital budget cycles.

Government Healthcare-Digitization & National AI Grants/Fast-Tracks

China earmarked RMB 2.3 billion (USD 320 million) in 2025 to deploy AI diagnostics across 300 tertiary hospitals by 2027. India’s Ayushman Bharat Digital Mission allotted INR 15 billion (USD 180 million) in 2024 for telepathology infrastructure in 5,000 district hospitals. The European Union committed EUR 120 million (USD 130 million) to digital health under Horizon Europe, channeling EUR 35 million to AI-enabled pathology projects. The United Kingdom added GBP 180 million (USD 230 million) in 2025 to roll out scanners across all 224 National Health Service trusts. Such programs underwrite capital costs and shrink adoption timelines.

Growth of Companion Diagnostics Needs Quantitative Tissue-Image Analytics

The FDA cleared 23 companion diagnostics in 2025, 17 of which use tissue-based assays that benefit from digital scoring. Agilent’s PD-L1 22C3 pharmDx assay now ships with an AI module validated on 1,200 patient samples in 2024 [3]Agilent Technologies, “PD-L1 22C3 pharmDx Digital Companion,” agilent.com. Ventana’s HER2 test added automated HER2/CEP17 ratio calculation in 2025, cutting result time from 48 hours to 6 hours. Pharmaceutical sponsors increasingly negotiate bundled assay-plus-software deals, ensuring consistent biomarker quantification at every clinical site.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Scanner, Storage & IT Costs for Mid-Tier/Public Labs | -1.4% | Global, acute in emerging markets & rural areas | Medium term (2-4 years) |

| Lack of Universal Interoperability Across Scanners, LIS & AI Ecosystems | -1.1% | Global, fragmented vendor landscape | Long term (≥ 4 years) |

| Volatile Global Glass-Slide Supply Constrained CAPEX Planning | -0.8% | Global, supply chain concentrated in Asia | Short term (≤ 2 years) |

| Data-Center Carbon-Footprint/ESG Limits Long-Term Cloud Storage | -0.7% | North America & EU, driven by corporate ESG mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Scanner, Storage & IT Costs for Mid-Tier/Public Labs

A 40× WSI scanner costs USD 150,000–400,000 and generates roughly 50 terabytes per 10,000 slides, demanding enterprise storage of another USD 100,000–200,000 plus recurring cloud fees. Community hospitals operate on thin margins and cannot recoup capital through the USD 45 CPT 88360 reimbursement, prolonging payback periods. District hospitals in India budgeted only INR 5 million (USD 60,000) for all diagnostics in fiscal 2024-25, making WSI unattainable without grant support. Vendors now offer leasing and pay-per-slide pricing, but take-up remains slow where upfront cash constraints dominate purchasing.

Lack of Universal Interoperability Across Scanners, LIS & AI Ecosystems

Although DICOM Supplement 145 defines a WSI standard, vendors implement color calibration and compression differently, hampering seamless exchange. A 2025 Digital Pathology Association survey found 54% of multi-scanner sites reported workflow delays due to incompatible file formats, and 38% could not deploy a single AI model across brands. Laboratories often buy middleware costing USD 50,000–150,000 to bridge their LIS with imaging archives. Industry initiatives like IHE profiles exist, but adoption is voluntary and slow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Hardware Anchors Revenue, Software Captures Margin

Whole Slide Imaging Scanners generated 43.5% of 2025 revenue, reflecting the prerequisite hardware investment before any digitized workflow begins. Image Analysis & AI Software is expected to grow at a 10.21% CAGR, the fastest among products, as laboratories recognize that raw images have limited clinical value without automated quantification tools. Philips shifted to a subscription model in 2025, bundling its IntelliSite scanner and algorithms for USD 8,000 per month, lowering upfront costs that previously exceeded USD 350,000. Communication & Storage Systems also expand steadily because the College of American Pathologists mandates 10-year retention of diagnostic images, prompting multi-petabyte archives.

Slide Management Systems & Accessories, including barcode labelers and robotic loaders, reduce technician touch-time. Leica reports its GT 450 DX paired with a 400-slide loader drops handling from 45 seconds to 8 seconds per slide. AI firms increasingly embed algorithms directly into scanner firmware, blurring hardware and software revenue streams. This convergence complicates vendor positioning but enhances user experience, strengthening the digital pathology market value proposition.

By Imaging Technique: Brightfield Dominance Persists, Fluorescence Gains Share

Brightfield imaging accounted for 85.1% of 2025 revenue because most primary diagnoses rely on hematoxylin-and-eosin staining, and FDA approvals still emphasize brightfield platforms. Fluorescence imaging should grow at a 10.55% CAGR through 2031 on demand from multiplex immunofluorescence and spatial-omics assays. Akoya’s PhenoCycler, which profiles up to 100 proteins, expanded placements from 87 in 2024 to 142 in 2025, mostly at academic and pharma R&D sites. Fluorescence scanners command premiums of USD 250,000–600,000, yet grant funding and trial budgets often cover incremental costs, sustaining adoption.

Hybrid scanners that toggle between brightfield and fluorescence modes help laboratories consolidate equipment. Ventana’s DP 200 won FDA clearance in November 2025 for dual-mode primary diagnosis, signaling regulatory endorsement of integrated workflows. Confocal and light-sheet platforms enable 3D reconstruction but remain confined to research because diagnostic pathways for volumetric imaging have not been defined.

By Application: Diagnosis Leads, Telepathology Ascends

Disease Diagnosis held a 56.7% share in 2025, encompassing surgical pathology, cytology, and hematopathology. Telepathology & Consultation is poised for a 10.39% CAGR, propelled by subspecialty shortages. The American Telemedicine Association recorded a 34% increase in digital consultations in 2025, with dermatopathology and neuropathology forming 48% of cases. Frozen-section turnaround times at rural hospitals halve when remote pathologists read slides digitally, improving surgical workflow.

Drug Discovery & Companion Diagnostics usage is rising because sponsors need standardized tissue analytics for regulatory filings. Roche noted that centralized digital review now covers 82% of its late-stage oncology trials. Education & Training stays niche but growing; Harvard Medical School digitized 12,000 teaching slides in 2024, enabling global access. Lastly, Quality Assurance & Archiving remains essential for auditing diagnostic concordance and meeting record-retention rules.

By End User: Hospitals Dominate, Pharma Accelerates

Hospital & Reference Laboratories delivered 38.4% of 2025 spending, anchored by daily diagnostic volume. Pharmaceutical & Biotechnology Companies & CROs are forecast to record a 10.47% CAGR, embedding digital pathology into Phase II–III trials for reproducible biomarker assessment. Labcorp reported 41% digital-pathology revenue growth in 2025, driven by oncology contracts. Diagnostic Centers such as Quest Diagnostics adopt scanners to win hospital referrals requiring subspecialty opinions. Other End Users - including veterinary and forensic labs - remain small but benefit from scanner vendors tailoring software to non-human tissue types.

By Deployment Model: On-Premises Prevails, Cloud Gains Traction

On-premise installations accounted for 65.4% of revenue in 2025 because hospitals prefer to store patient data within their firewalls. Still, cloud-based offerings are projected to grow at a 10.16% CAGR as vendors offer consumption pricing and regulatory frameworks mature. Proscia’s Concentriq charges USD 0.50 per gigabyte of storage plus USD 2.00 per AI inference, avoiding million-dollar capital outlays. Philips launched a hybrid model in 2025 that keeps images local, but streams algorithms from secure data centers, addressing sovereignty rules while leveraging scalable compute.

Geography Analysis

North America captured 47.8% of 2025 revenue and benefits from FDA clarity, CPT reimbursement, and NIH dataset funding. Clearance of Philips IntelliSite, Leica Aperio AT2, and Hamamatsu NanoZoomer between 2017 and 2024 ended compliance uncertainty, accelerating procurement. CMS introduced CPT 88360 in 2024, providing USD 45 per digital consultation, a modest but critical catalyst. The NIH Bridge2AI program invested USD 150 million in standardized datasets during 2025, fueling algorithm R&D. Canada’s Ontario province linked 12 community hospitals to a central telepathology hub in 2025, cutting turnaround time by 38%.

Europe follows with strong regulatory push. The EU Medical Device Regulation requires CE-IVD certification for AI software by mid-2027, prompting hospitals to validate workflows early. The United Kingdom committed GBP 180 million in 2025 to digitize pathology across all NHS trusts by 2028. Germany’s health ministry opened a EUR 50 million grant program in 2025 for university hospitals, while France’s regulator approved seven AI algorithms for clinical use, the highest in Europe.

Asia-Pacific posts the fastest 11.21% CAGR. China’s Healthy China 2030 plan mandates county-level telepathology links and funds scanner rollouts worth RMB 2.3 billion. India’s Ayushman Bharat Digital Mission awarded INR 15 billion for 5,000 hospitals. Japan began reimbursing AI-assisted diagnosis at JPY 8,000 (USD 55) per case in April 2025, outpacing U.S. payment rates. Australia published national practice guidelines in 2025, giving hospitals a clear compliance roadmap. Middle East & Africa and South America lag due to infrastructure gaps. The UAE piloted digital pathology at eight hospitals in 2025 to test nationwide feasibility. South Africa’s National Health Laboratory Service connected rural clinics via telepathology in 2024 but struggles with bandwidth. Brazil invested BRL 120 million (USD 24 million) in 2025 to equip 50 cancer centers, focusing on high-mortality regions.

Regulatory Landscape

In the United States, clinical whole-slide imaging (WSI) and associated digital pathology software are regulated as medical devices under FDA oversight, with device classification anchored in 21 CFR 864.3750 for software algorithm devices for digital pathology alongside controls applied to WSI systems. In January 2026, the FDA updated guidance on Clinical Decision Support (CDS) software, reinforcing that software which analyzes digital pathology images to generate diagnostic output falls within regulated medical-device scope, which in turn affects expectations for validation, cybersecurity, and change management for deployed algorithms.

Global standardization is also tightening interoperability and workflow expectations. ISO 12052:2026 (published February 2026) updates the DICOM framework used to structure image and related data exchange, supporting pathology image communication and data management across systems. At the same time, IHE and DICOM working efforts continue to operationalize end-to-end digital pathology acquisition and specimen context. Laboratories still manage a dual compliance reality, with FDA-cleared platforms for primary diagnosis alongside CLIA/CAP quality systems for operational controls and retained-image requirements, while pipeline workflow standards (including ISO/CD 24051-2 for digital pathology workflows and AI-based image analysis) influence longer-cycle procurement and validation planning.

Competitive Landscape

The digital pathology market exhibits moderate concentration: the top five scanner vendors, Danaher (Leica Biosystems), Koninklijke Philips, Roche Ventana, Hamamatsu Photonics, and 3DHISTECH, held the majority of 2025 scanner revenue, while more than 30 software firms compete for algorithm contracts. Established hardware suppliers leverage global service networks and long hospital relationships, but software-first firms like PathAI, Paige, and Proscia bypass capex barriers through subscription models.

Strategic moves focus on AI integration and open ecosystems. Philips bought a minority stake in Paige in 2024 to embed algorithms into IntelliSite. Roche Ventana partnered with Visiopharm in 2025 to combine quantitative analysis with its BenchMark stainers. Sectra launched an open API in 2025, attracting 12 third-party AI partners within six months. Proscia’s cloud pricing resonates with budget-limited labs that cannot commit USD 500,000–1 million upfront.

Regional players also emerge. South Korea’s DeepBio raised USD 44 million in 2025, touting superior performance on Asian cohorts. Interoperability remains a differentiator: vendors holding both FDA and CE-IVD clearances command price premiums and dominate tenders, whereas research-use-only suppliers face smaller budgets and longer sales cycles. Mid-tier community hospitals and emerging markets remain under-penetrated, offering growth whitespace for vendors that can deliver low-cost, turnkey systems.

Digital Pathology Industry Leaders

Hamamatsu Photonics KK

3DHistech Ltd

Danaher Corporation (Leica Biosystems Nussloch GmbH)

F. Hoffmann-La Roche Ltd

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and workflow standardization remain a practical whitespace where vendors and health systems are investing to reduce lock-in from proprietary WSI formats and fragmented LIS integrations. The March 2026 IHE PaLM Digital Pathology Image Acquisition (DPIA) Profile offers a concrete template for standardized acquisition messaging from physical slides, complementing the market push toward DICOM-aligned storage and exchange described in 2026 academic and standards discussions. This supports near-term demand for scanner-neutral image management platforms, middleware, and enterprise services that enable multi-vendor sites to maintain a consistent archive, quality workflow, and AI toolchain without re-scanning or duplicative storage.

A second opportunity involves clinical scale-up programs that move departmental pilots into system-wide digital sign-out and AI-enabled workflows. Named deployments and collaborations reflect this shift: NYU Langone Health completed a transition to digital sign-out for all clinical cases in September 2025 using Philips IntelliSite scanners, and Mayo Clinic announced implementation of Techcyte Fusion AP in July 2026 to unify WSI, AI, and clinical data into a single workflow. On the supply side, consolidation and platform-building activity, including Roche signing a definitive merger agreement to acquire PathAI in May 2026, also points to continued demand for integrated solutions spanning scanning, image management, and regulated AI modules, alongside higher value placed on open APIs and standards-based connectivity for hospitals and reference labs operating mixed fleets and multi-site workflows.

Recent Industry Developments

- June 2026: Leica Biosystems announced an expanded strategic collaboration with AstraZeneca and Daiichi Sankyo to develop an IHC assay and paired image analysis algorithm using the Aperio GT 450 scanner and Aperio HALO AP system. The program links biopharma assay development with digital workflow tooling, reinforcing companion-diagnostic style use cases that align scanner and software buying decisions.

- May 2026: Roche entered into a definitive merger agreement to acquire PathAI, adding AI-driven diagnostics capabilities and image management assets to its digital pathology portfolio. The transaction points to continued platform consolidation and increases competitive pressure on standalone software vendors to differentiate via interoperability, validated algorithms, and enterprise deployment support.

- June 2025: PathAI received FDA 510(k) clearance for its AISight Dx digital pathology image management system for primary diagnosis, including a Predetermined Change Control Plan to streamline certain future updates. The clearance expands the set of FDA-cleared options for clinical digital sign-out and supports faster iteration within an explicitly agreed regulatory framework for software changes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the digital pathology market covers revenues earned from solutions that digitize pathology slides and enable viewing, sharing, and analysis of whole-slide images for clinical and research workflows.

Scope exclusions: We exclude conventional microscopes, generic image archives not tied to pathology workflows, and outsourced specimen-processing services.

Segmentation Overview

- By Product

- Whole Slide Imaging Scanners

- Image Analysis & AI Software

- Communication & Storage Systems

- Slide Management Systems & Accessories

- By Imaging Technique

- Brightfield

- Fluorescence

- By Application

- Disease Diagnosis

- Drug Discovery & Companion Diagnostics

- Telepathology & Consultation

- Education & Training

- Quality Assurance & Archiving

- By End User

- Hospital & Reference Laboratories

- Pharmaceutical & Biotechnology Companies & CROs

- Diagnostic Centers

- Other End Users

- By Deployment Model

- On-premise

- Cloud-based / SaaS

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and to anchor it to observable healthcare and diagnostics indicators. We referred to public sources such as the US FDA database for cleared devices and software, the US Centers for Medicare and Medicaid Services for reimbursement and payment signals, and OECD and World Health Organization statistics for broader healthcare capacity context.

To keep the assumptions realistic, we also reviewed sources such as National Cancer Institute publications, peer-reviewed pathology informatics journals, and trade association pages covering lab quality and digital adoption. Company annual reports, investor presentations, and reputable press were used to understand product positioning, route-to-market, and pricing direction. Where helpful, we also used paid subscriptions for company financials and intelligence and for patent databases to cross-check innovation intensity. These sources are illustrative, and many other public and paid references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased and deployed in labs, and what the typical expansion path looks like after initial pilots. We spoke with a mix of pathology lab leaders, hospital stakeholders, software and workflow specialists, and channel-side participants across major regions to stress-test adoption, pricing, and replacement cycles before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | APAC: 39% |

| Mid tier: 55% | Functional/Unit leaders: 38% | EMEA: 36% |

| Smaller Players: 17% | Managers: 46% | Americas: 25% |

Market-Sizing & Forecasting

Sizing started with a top-down build where pathology testing activity and lab digitization readiness were translated into an addressable install base for whole-slide imaging, and then converted into annual spending. To keep the totals grounded, selective bottom-up checks were run using sampled scanner placements, typical software subscription ranges, and service and maintenance attachment patterns, which were then adjusted when they did not align with the demand-side story.

Inputs used in the model included the pace of whole-slide imaging adoption in routine diagnostics, the share of cases suitable for remote review, scanner utilization rates and replacement cycles, average software price progression by deployment type, and the portion of labs expanding from single-site to network rollouts. Forecasts were built using scenario analysis, where these variables were shifted based on what interviewees expected for regulation comfort, reimbursement signals, and lab staffing constraints. When bottom-up inputs were missing for smaller countries, we bridged gaps using proxy indicators such as hospital and lab counts and relative pathology workload, and then rechecked the implied spend per lab for reasonableness.

Data Validation & Update Cycle

Outputs were validated through multiple checks so that any single assumption could not drive the full result. We compared implied spending per lab and per scanner against interview feedback, looked for step-changes that did not align with regulatory and reimbursement timelines, and then reworked any outliers before sign-off.

Each draft goes through a structured analyst review where inputs, calculations, and logic are independently rechecked, followed by targeted re-contact when a key variable shows a large variance. Reports are refreshed annually, and interim updates are made when material events shift adoption or pricing. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Digital Pathology Market Size Versus Other Published Estimates

Published market sizes for digital pathology do not always match because the category boundary is set differently, and because base years and pricing assumptions change from one publisher to another. Differences also come from whether models lean on installed base expansion, procedure-linked demand, or broad IT spending proxies.

The benchmark table shows a noticeable spread, and in Mordor Intelligence's model the total is built from whole-slide scanners plus imaging software and related communication tools, while conventional microscopes, generic archives outside pathology workflows, and outsourced specimen-processing services are left out to avoid inflating spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.01 B (2026) | |

| Trade Journal A | USD 1.29 B (2024) | Uses an earlier base year and typically blends broader storage and general image-management spend into digital pathology, which can shift the total downward on scanners while overstating software-related scope. |

| Global Consultancy B | USD 1.02 B (2024) | Counts a wider set of applications and countries with lighter validation on lab-level deployment speed, and it often relies on uniform ASP growth that can understate premium clinical deployments in mature markets. |

Looking across the three figures, the gap is mainly explained by base-year choice and what is treated as in-scope software and workflow spending versus adjacent IT. Our approach stays traceable to lab adoption, utilization, and pricing signals, which makes the final number easier to reproduce and recheck when conditions change.

Key Questions Answered in the Report

What is the projected value of the digital pathology market in 2031?

The market is forecast to reach USD 3.21 billion by 2031, expanding at a 9.90% CAGR.

Which product segment is expected to grow fastest?

Image Analysis & AI Software is anticipated to deliver a 10.21% CAGR through 2031 as laboratories seek automated quantification.

Why is Asia-Pacific the fastest-growing region?

Government digitization mandates in China, India, and Japan underpin an 11.21% regional CAGR by funding scanners and reimbursement for AI-assisted reads.

What restrains adoption in community hospitals?

High upfront costs for scanners and enterprise storage, coupled with limited reimbursement, hinder deployments in budget-constrained labs.

How are vendors addressing interoperability challenges?

Industry leaders are publishing open APIs and embracing DICOM standards so laboratories can run third-party AI tools across multi-vendor scanner fleets.

Page last updated on: