Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

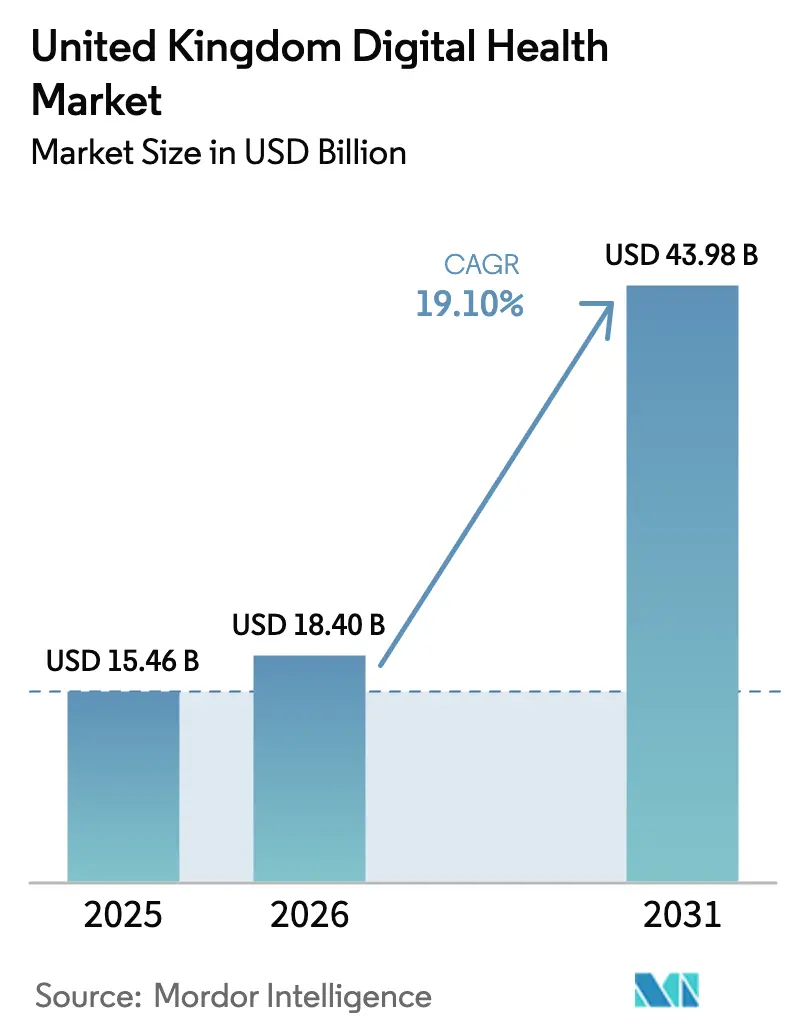

| Base Year Market Size (2025) | USD 15.46 Billion |

| Market Size (2026) | USD 18.40 Billion |

| Market Size (2031) | USD 43.98 Billion |

| Growth Rate (2026 - 2031) | 19.10% CAGR |

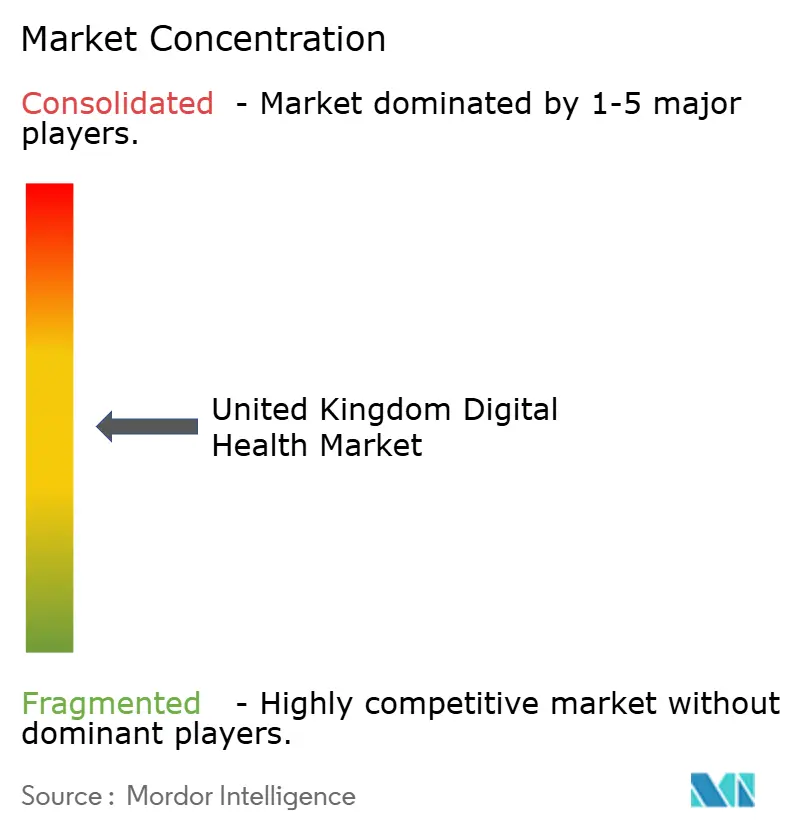

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Digital Health Market Analysis by Mordor Intelligence

The United Kingdom Digital Health Market size was valued at USD 15.46 billion in 2025 and is estimated to grow from USD 18.40 billion in 2026 to reach USD 43.98 billion by 2031, at a CAGR of 19.10% during the forecast period (2026-2031).

Driving forces include sustained National Health Service (NHS) investment in electronic patient records (EPRs), fast-growing virtual ward capacity, the expanding user base of the NHS App, and an emerging wave of AI-enabled analytics that optimizes care pathways while reducing administrative burden. Incumbent vendors defend entrenched software estates, yet cloud-native challengers use data-platform contracts to seed adjacent analytic and workflow tools, fragmenting the competitive field. Procurement frameworks that deliberately favor multivendor awards create openings for smaller suppliers with specialized capabilities, while cybersecurity incidents and interoperability gaps temper near-term hardware demand and elevate cloud migration as a lower-risk alternative. In parallel, carbon-reduction mandates force providers and vendors to favor energy-efficient architectures, a shift that reinforces the long-term pivot toward hyperscale cloud hosting and software-as-a-service delivery.

Key Report Takeaways

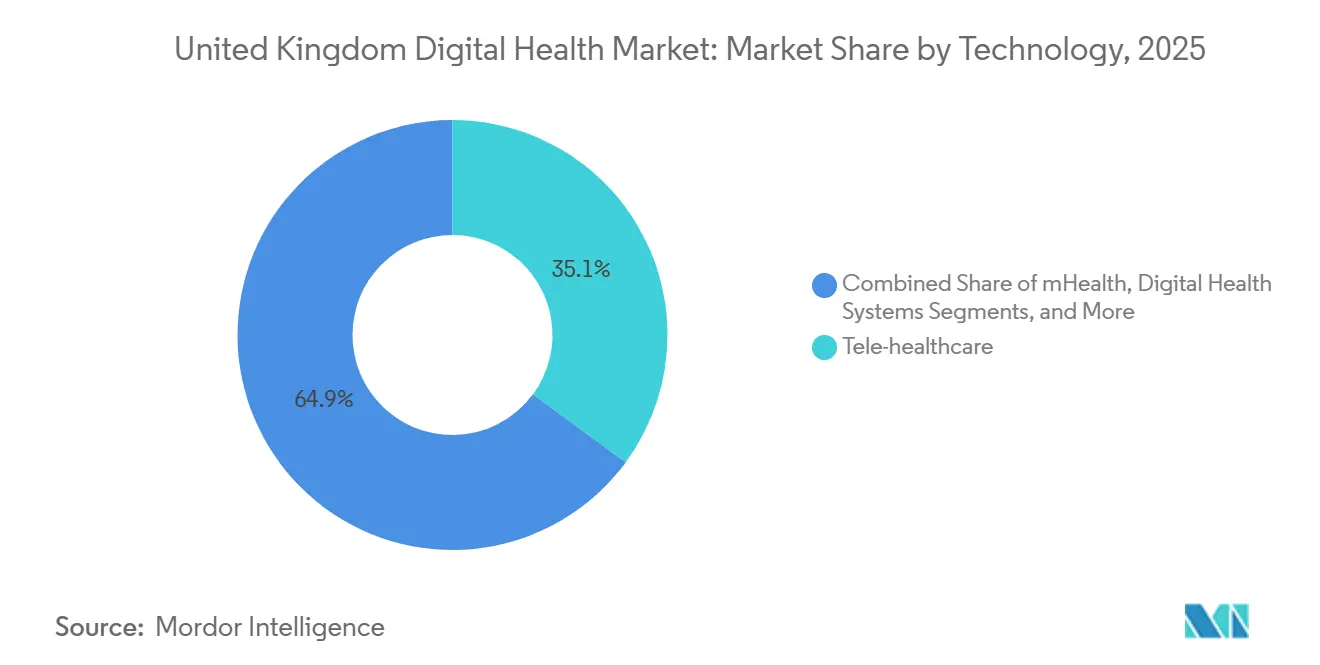

- By technology, Tele-Healthcare led with 35.12% revenue share in 2025; Healthcare Analytics & AI is forecast to advance at a 19.80% CAGR through 2031.

- By component, Software accounted for 59.18% of the United Kingdom digital health market share in 2025, while services are expected to show the highest projected CAGR at 20.35% during 2026-2031.

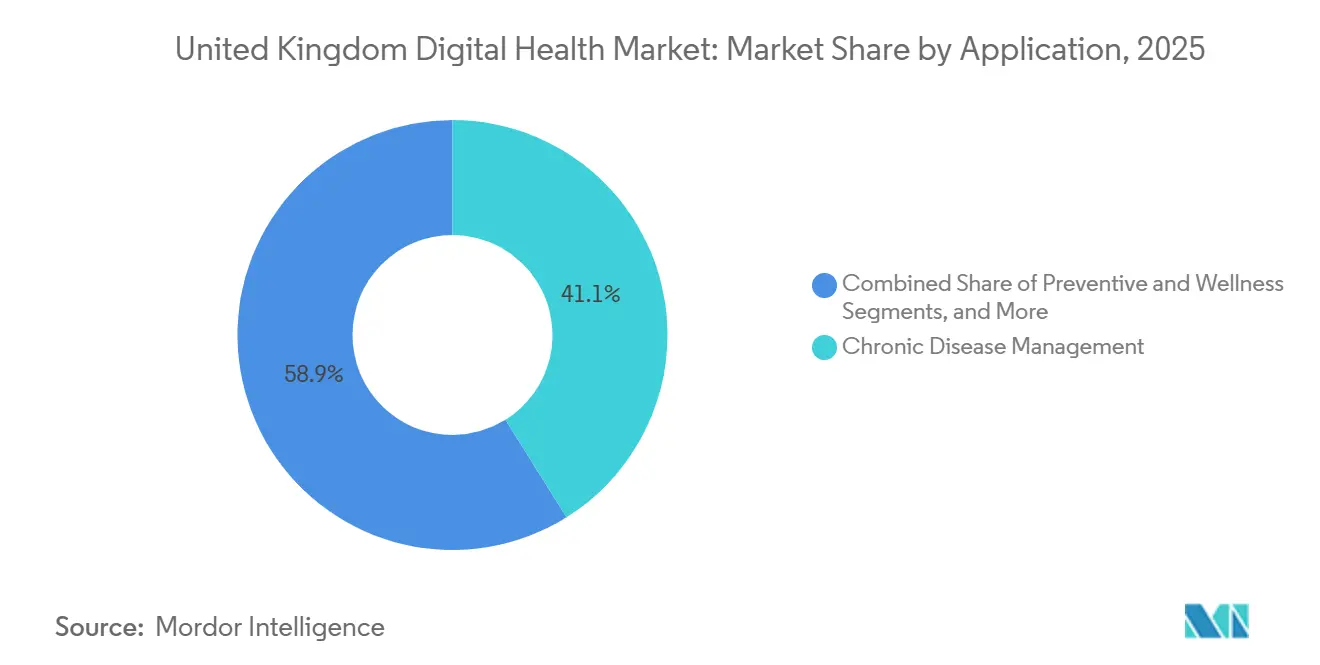

- By application, Chronic Disease Management captured 41.13% of 2025 spend; Diagnostics & Decision Support is set to expand at a 21.28% CAGR to 2031.

- By end-user, Hospitals & NHS Trusts represented 60.47% of expenditure in 2025, whereas Patients/Home-Care Settings are growing at a 20.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Digital Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NHS Long-Term Digital Funding Commitments | +4.2% | England (primary), Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Accelerating EPR Roll-Outs Across Secondary Care | +3.8% | England acute trusts, Scotland regional boards, Wales health boards | Short term (≤2 years) |

| Majority of Population’s Monthly Use Target for NHS App | +3.1% | UK-wide | Medium term (2-4 years) |

| Expansion of Virtual Wards & Remote Monitoring | +3.5% | England ICSs, Scotland, Wales | Short term (≤2 years) |

| Federated Data Platform-Enabled AI “App-Store” Ecosystem | +4.6% | England (national), pilots in Scotland and Wales | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

NHS Long-Term Digital Funding Commitments

NHS England’s GBP 13.4 billion digital transformation allocation through 2025 created a predictable procurement pipeline that underpinned vendor investment, allowing trusts to replace patient-administration systems averaging 15 years of age in 2020 with software only eight years old by 2025.[1]NHS England, “Virtual Wards Programme,” england.nhs.uk Scotland added GBP 300 million and NHS Wales GBP 200 million for comparable programs, producing parallel opportunities for suppliers capable of multi-jurisdiction deployment. Front-loaded funding compressed implementation timetables, increasing demand for managed-service partners that can absorb short-term staffing peaks.

Accelerating EPR Roll-Outs Across Secondary Care

EPR coverage in English acute trusts rose from 43% in 2023 to an anticipated 80% by mid-2026, propelled by elective-recovery incentives and integrated care system (ICS) maturity metrics. Oracle Health’s Millennium went live at Newcastle Hospitals under a GBP 32.5 million deal, and a multi-trust London deployment consolidated three standalone records into one, illustrating economies of scale in larger footprints. Early adopters are now layering population-health analytics onto mature data sets, widening capability gaps between digital leaders and late adopters.

Majority of Population’s Monthly Use Target for NHS App

The NHS App reached 36 million users by June 2025, equal to 54% of U.K. adults. Added functionality such as vaccination booking, organ-donation registration, and NHS 111 triage extends the app’s utility, reducing call-center workload by 20% in high-adoption practices. Usage skews toward digitally literate patients; only 18% of over-65s are active users, indicating that broader impact requires assisted-digital programs targeting older cohorts.

Expansion of Virtual Wards & Remote Monitoring

Virtual-ward capacity exceeded 10,000 beds by late 2024, and NHS England targets 15,000 beds by 2027. Remote-monitoring platforms capture oxygen saturation, heart rate, and blood pressure, escalating deteriorating cases for early intervention while converting fixed-estate cost into variable technology spend. Connectivity gaps accounted for 12% of monitoring lapses during a 2025 audit, highlighting the fragility of infrastructure in rural regions.[2]National Audit Office, “Virtual Wards Audit Report,” nao.org.uk

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security & Data-Privacy Concerns | -1.8% | UK-wide | Short term (≤2 years) |

| Interoperability Gaps in Legacy NHS IT | -1.5% | England acute trusts, Scotland boards, Wales boards | Medium term (2-4 years) |

| Clinician “Shadow-IT” Workarounds | -1.2% | UK-wide | Medium term (2-4 years) |

| Rising Carbon-Reduction Compliance Costs | -0.9% | UK data-center estates | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security & Data-Privacy Concerns

Ransomware disrupted several trusts in 2024-2025, forcing temporary reliance on paper records and delaying elective procedures.[3]National Cyber Security Centre, “Cyber Security Incidents in Healthcare,” ncsc.gov.uk Annual Data Security and Protection Toolkit assessments now require trusts to exceed baseline cyber-maturity standards, adding GBP 0.5 million in annual compliance costs. Extended procurement due diligence cycles particularly strain smaller vendors that lack formal security certifications.

Interoperability Gaps in Legacy NHS IT

A 2025 Royal College of Physicians survey found 68% of clinicians still re-enter data when handing off patients between primary and secondary care. Coexistence of HL7 v2, FHIR, and proprietary APIs forces middleware deployments that multiply points of failure and inflate technical debt. Mandatory adoption of FHIR UK Core will take several years to retrofit across installed systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: AI and Analytics Outpace Legacy Tele-Health

Healthcare Analytics & AI is projected to grow at a 19.80% CAGR, outstripping the mature Tele-Healthcare segment that held a 35.12% share of the United Kingdom digital health market in 2025. Trusts redirect budgets from pandemic-era video-consultation tools to predictive analytics that forecast emergency-department volumes and allocate staff accordingly, demonstrated by 85% prediction accuracy in early FDP pilots. Tele-Healthcare remains essential for GP and specialist consultations but faces slower incremental growth as adoption reaches saturation in urban areas.

The digital health systems layer, dominated by Oracle Health and Epic, anchors hospital workflows, while remote monitoring & wearables gain momentum through virtual-ward expansion. mHealth applications, epitomized by the NHS App, provide a ubiquitous patient front door yet generate lower revenue per user than AI-powered analytics. Data-platform apps built on the FDP create a marketplace that diffuses innovation across multiple vendors instead of consolidating power within EPR incumbents.

By Component: Services Surge as Integration Complexity Mounts

Software licenses and SaaS subscriptions delivered 59.18% of United Kingdom digital health market revenue in 2025, but Services implementation, integration, and managed support are forecast to rise at a 20.35% CAGR through 2031, almost matching overall market growth. Migration from legacy databases, workforce training, and ongoing interoperability maintenance drive sustained demand for professional services long after initial go-lives.

Infosys’s GBP 1.17 billion Electronic Staff Record contract exemplifies bundled software-plus-services engagements that transfer operational risk to the vendor. Hardware sales shrink as trusts shift workloads to hyperscale cloud platforms. Service providers also absorb the cost of retrofitting HL7 interfaces to FHIR and decommissioning shadow-IT workarounds, reinforcing their strategic role throughout the transformation cycle.

By Application: Diagnostics AI Gains as Chronic Care Plateaus

Chronic Disease Management retained 41.13% of 2025 spending, but growth moderates as diabetes and cardiovascular programs near coverage saturation in major ICSs. Diagnostics & Decision Support leads future expansion with a 21.28% CAGR, catalyzed by AI algorithms that prioritize images for radiologist review and cut reporting backlogs.

Preventive & Wellness apps remain underfunded, absorbing less than 8% of spend despite policy emphasis on prevention. Administration & Workflow Automation grows steadily, highlighted by AI-based clinical-note tools that reduce documentation time by 40%. Mental health, precision medicine, and virtual care carve smaller but rising allocations as reimbursement models scale.

By End-User: Home-Care Settings Accelerate as Hospitals Consolidate

Hospitals & NHS Trusts held 60.47% of 2025 spending, anchored by EPR roll-outs, yet growth slows as roll-out waves crest and budgets shift toward optimization. Patients/Home-Care Settings lead future expansion with a 20.63% CAGR, driven by wearables and virtual wards that relocate monitoring to living rooms.

Primary Care & GP Practices gain purchasing autonomy through the GBP 400 million Digital Services Framework, encouraging workflow and decision-support pilots that challenge historical incumbents. Payers & Commissioners wield indirect power by linking funding to digital-maturity criteria, effectively mandating EPR and interoperability compliance across provider networks.

Geography Analysis

England comprises the bulk of the United Kingdom's digital health market spend by virtue of its population and centrally managed NHS England procurement programs. Forty-two ICSs function as semi-autonomous purchasers, and early FDP pilots in five of them provide reference deployments that neighboring regions often emulate. Scotland’s GBP 300 million Digital Health & Care Strategy funds a national shared-care record that minimizes vendor fragmentation but increases platform risk if deployments falter.

Wales pursues a Once for Wales single-platform model that awarded an EPR contract in 2024, while Northern Ireland leverages its combined health-and-social-care structure to trial unified clinical and social-care workflows. Rural broadband deficits below 10 Mbps limit video consultations and remote monitoring in parts of Scotland, Wales, and Northern Ireland, an issue the UK Government’s Project Gigabit aims to resolve by 2030.

Interregional patient flows expose interoperability gaps: only 60% of Scottish acute hospitals ran modern EPRs by mid-2025 versus 80% in England, complicating data exchange when patients cross borders for specialist services. Vendors that secure flagship deployments in high-population English ICSs frequently leverage those references to win contracts in smaller devolved markets, reinforcing a first-mover advantage.

Regulatory Landscape

The United Kingdom digital health market operates under a combination of medical-device regulation, NHS commissioning requirements, and mandatory information governance. Software as a Medical Device (SaMD), including AI as a Medical Device, sits within the UK Medical Devices Regulations 2002 under the Medicines and Healthcare products Regulatory Agency (MHRA), along with national guidance on software and AI as medical devices and ongoing reforms that tighten expectations around evidence, safety, and post-market surveillance.

For NHS adoption, compliance with NHS standards is a practical gateway to procurement, particularly for patient-facing identity and access controls, clinical safety, and information-sharing. NHS England mandated the DAPB3051 Identity Verification and Authentication Standard (Version 3.1.0 active from 23 December 2025) for digital, data, analytics, and technology use, while digital clinical safety assurance is enforced through DCB0129 (manufacturer) and DCB0160 (deployment/use) requirements under the Health and Social Care Act 2012. Interoperability and shared-record readiness are reinforced by standards such as the Core Information Standard, managed through the NHS Standards Directory from 01 January 2026, and by the national focus on FHIR-aligned data exchange in legacy environments.

Value Chain Analysis

The value chain begins with solution design and product development, covering EPR platforms, tele-healthcare, analytics and AI, remote monitoring devices, and mHealth apps. It then moves into clinical validation and evidence generation required for NHS market access. Vendors proceed through regulatory and assurance gates, including MHRA pathways where products qualify as medical devices, plus NHS procurement readiness steps such as meeting Digital Technology Assessment Criteria (DTAC) expectations and aligning with NICE Evidence Standards Framework requirements for digital health technologies.

Distribution and scaling depend heavily on NHS procurement routes and multi-year framework awards, with implementation partners and managed service providers central to deployment, integration, and ongoing operations across NHS Trusts and Integrated Care Systems. The downstream chain also includes interoperability and identity components (for example, services built to DAPB3051 and clinical safety cases under DCB0129/DCB0160), data-platform integration (including national platform strategies such as the Federated Data Platform), and continuous cybersecurity and post-market maintenance. Supply and delivery risks center on legacy-system integration capacity, security accreditation readiness, and reliance on global cloud and sub-component sourcing, with post-Brexit trade and customs friction affecting device-linked remote monitoring programs more than software-only deployments.

Competitive Landscape

EPR and primary-care software remain moderately concentrated, with two vendors covering the majority of GP practices, yet no single supplier exceeds 15% share in the rapidly expanding AI analytics, remote monitoring, or virtual-care niches. High switching costs and data-network effects help incumbents retain hospitals that invested GBP 20 million-50 million per deployment, but cloud-native entrants sidestep entrenched systems by offering adjacent analytic or workflow tools that integrate via open APIs.

NHS procurement policy now encourages fragmentation: the 2026 Primary Care Digital Services Framework split GBP 400 million across 12 vendors, lowering entry barriers for specialized suppliers. Global platform providers pursue multi-tens-of-millions acute trust deals, while U.K.-native companies focus on task-specific SaaS offerings that scale rapidly through low-friction adoption models. Regulatory requirements such as the Digital Technology Assessment Criteria favor vendors with established compliance processes, subtly disadvantaging early-stage startups.

United Kingdom Digital Health Industry Leaders

EMIS Health (Optum)

TPP (SystmOne)

Cerner (Oracle Health)

Epic Systems

Alcidion

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in scaling productivity-focused AI and automation capabilities on top of expanding EPR coverage and national platform implementation. NHS England has set out digitisation milestones, including 96% of trusts having implemented an EPR and 70% reaching the core digitisation standard referenced in the "What Good Looks Like" policy, shifting supplier focus toward optimisation layers, workflow automation, and analytics that can operate across heterogeneous EPR estates rather than only replacing core records. The NHS App also provides a high-reach channel for clinically oriented digital services, and NHS England highlighted triage tools and conversational AI for clinical transcriptions and summaries as part of its July 2026 AI rollout programme.

Procurement and platform changes are creating additional addressable spend for vendors that can show evidence, safety, and interoperability while reducing implementation friction. NHS England has been rolling out value-based procurement guidance following pilots in 13 trusts, emphasizing measurable effectiveness and long-term impact rather than lowest upfront cost, which increases the commercial relevance of outcomes data, service wrap, and operational assurance. At the system level, planning guidance and national statements that reference multi-year technology, digital, and data investment, including a published £10 billion three-year investment referenced by NHS England in July 2026, support continued demand for cloud migration, cybersecurity uplift, and data-platform integrations that enable multi-site AI deployment and NHS-wide service transformation.

Recent Industry Developments

- June 2026: Digital Health and Care Wales completed the migration of all 193 GP practices in Wales to EMIS Web, ending the use of Vision in Welsh primary care. This standardises the core clinical system footprint across Welsh general practice and supports the baseline for national interoperability and shared-care record initiatives.

- April 2026: Lewisham and Greenwich NHS Trust signed a 10-year, GBP 52 million contract with Epic for a new electronic patient record, with a planned go-live in April 2027. The award reinforces the shift toward single, trust-wide EPR platforms and creates a downstream services pipeline for integration, training, and data migration.

- December 2024: Essex trusts announced plans to deliver a GBP 65 million Oracle Health EPR programme. This highlights continued large-scale replacement of legacy acute IT estates and raises demand for associated interoperability and analytics tooling across multi-trust footprints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the UK digital health market covers digital tools that support clinical care and health system workflows, including software, connected monitoring devices, and related services used across the NHS and private healthcare to diagnose, treat, monitor, or manage patients.

Scope exclusions: We exclude stand-alone wellness and fitness apps or devices when they are not used for clinical decision-making or regulated medical use.

Segmentation Overview

- By Technology

- Tele-Healthcare

- mHealth Applications

- Digital Health Systems (EPR, PAS, Shared-Care Records)

- Healthcare Analytics & AI

- By Component

- Software

- Hardware

- Services

- By Application

- Chronic Disease Management

- Preventive & Wellness

- Diagnostics & Decision Support

- Administration & Workflow Automation

- Mental & Behavioural Health

- Genomics & Precision Medicine

- Virtual Care & Hospital-at-Home

- By End-User

- Hospitals & NHS Trusts

- Primary Care & GP Practices

- Patients / Home-Care Settings

- Payers & Commissioners (ICBs, NI HSC, NHS Wales, NHS Scotland)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the market boundary and find anchors that can be checked over time, especially around NHS digitization and tech-enabled care delivery. We referred to public sources such as NHS England and the UK Department of Health and Social Care publications, Office for National Statistics releases, MHRA guidance for software and AI as medical devices, and NICE resources for digital health technologies.

We also used supporting evidence from company annual reports, investor decks, reputable news coverage, peer-reviewed healthcare IT studies, and procurement and tender portals that indicate purchasing patterns. Where helpful, paid subscriptions that compile company financials, patent filings, and shipment-level trade records were used to speed up validation, but the market model was not built from any single database. These desk sources are illustrative only, and many other public references were also used for data collection, cross-checking, and clarifying assumptions.

Primary Interviews and Surveys

Primary work was used to test adoption reality in the UK, confirm which solutions are budgeted inside NHS trusts versus purchased by private providers, and understand typical pricing patterns for software, devices, and services. We spoke with a mix of solution providers, healthcare delivery leaders, channel and implementation partners, and informed buyers, and then used their inputs to tighten penetration, utilization, and ASP assumptions across the country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | |

| Mid tier: 55% | Functional/Unit leaders: 40% | |

| Smaller Players: 17% | Managers: 45% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs the UK demand pool from healthcare delivery activity and digital adoption, and then splits it into monetized spending on relevant software, connected devices, and services. To keep it realistic, the totals are corroborated with selective bottom-up checks such as sampled supplier revenue ranges, channel feedback on deployment volumes, and ASP x volume approximations for remote monitoring and telehealth use cases.

Key inputs used in the model include NHS digital funding and rollout signals, the share of care pathways that can be delivered virtually, active user volumes for remote monitoring and teleconsultations, software subscription and implementation pricing patterns, and device attach rates for clinically used wearables and monitoring kits. Where company disclosures do not separate UK revenue cleanly, we use geography splits discussed in interviews and triangulate them with known customer footprints, before adjusting for double counting between software and bundled service contracts.

For forecasting, we rely mainly on scenario analysis, since the pace of NHS procurement cycles and regulatory clearance timing can shift year to year. Growth scenarios are driven by variables like digitization spend continuity, workforce pressure that increases virtual care, AI and analytics uptake in clinical workflows, and replacement cycles for monitoring hardware, and then these are rechecked with expert consensus so the path stays practical.

Data Validation & Update Cycle

Validation is done through a set of cross-checks where modeled outputs are compared with independent signals, such as procurement activity, adoption indicators shared by practitioners, and the direction of reported revenues for exposed players. Outliers are reviewed, assumptions are reworked, and follow-up questions are triggered when pricing, adoption, or mix shifts do not match what multiple respondents see in the field.

Before sign-off, the model goes through step-by-step analyst review, including variance checks across years and sanity checks against the expected size of adjacent healthcare IT spend in the UK. The report is refreshed annually, and interim updates are made when material events occur, such as major NHS policy changes or reimbursement shifts. Right before delivery, we run a fresh update pass so clients receive the latest view rather than an older stored estimate.

Mordor Intelligence's United Kingdom Digital Health Market Size Measured Against Other Published Estimates

Published market sizes for UK digital health can look far apart, even when the topic sounds the same, because the boundary between clinical digital tools and broader health IT is not drawn in a consistent way. Differences also come from how prices are normalized, which year is treated as the reference point, and whether the estimate is updated when procurement timing shifts.

The biggest gap drivers usually come from refresh cadence and currency timing, where delayed updates can miss recent contract re-pricing, and from ASP logic that either assumes list pricing or accounts for public-sector discounting and multi-year deals. In this study, those checks are re-run each cycle, with NHS-led demand signals used as guardrails, which is why the 2025 value in Mordor Intelligence aligns tightly to the addressable clinical spending pool rather than wider IT budgets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.46 B (2025) | |

| Industry Research Outlet A | USD 2.40 B (2025) | Uses a narrower eHealth-only lens that leans toward software categories like EHR and telemedicine, and it appears to exclude sizable connected monitoring hardware and broader analytics spending. |

| Healthcare IT Brief B | USD 11.98 B (2024) | Tracks healthcare IT spend more broadly and anchors to a different base year, which can mix non-clinical IT services with digital health solutions and apply slower pricing changes across years. |

Overall, the spread is explained by what is counted as digital health, how pricing is treated across public and private buyers, and whether the base year is kept current. By tying the model to repeatable demand and spending drivers, the approach produces a practical number that can be rechecked as adoption and budgets move.

Key Questions Answered in the Report

How big will be the UK digital health market in 2026?

The UK digital health market size is USD 18.40 billion in 2026.

Which technology segment is growing fastest?

Healthcare Analytics & AI leads growth, advancing at a 19.80% CAGR on the back of predictive models and AI-driven decision support.

What share do hospitals hold in overall spending?

Hospitals and NHS Trusts account for 60.47% of 2025 spending, though home-care settings are expanding more quickly.

How many users are on the NHS App?

The NHS App registered 36 million users by mid-2025, covering more than half of the U.K. adult population.

What is the biggest restraint on adoption?

Cyber-security and data-privacy concerns remain the foremost barrier, with ransomware adding cost and slowing procurement cycles.

Page last updated on: