Bioinformatics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.97 Billion |

| Market Size (2031) | USD 37.03 Billion |

| Growth Rate (2026 - 2031) | 13.10% CAGR |

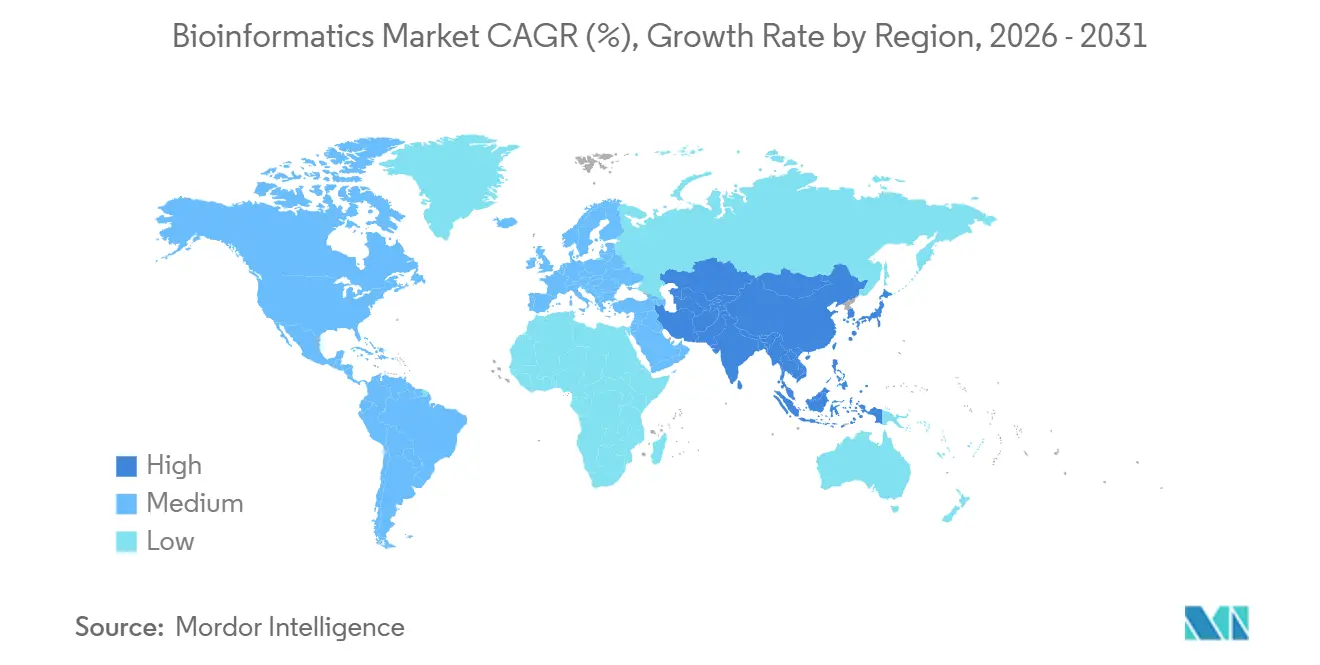

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioinformatics Market Analysis by Mordor Intelligence

The Bioinformatics Market size is estimated at USD 19.97 billion in 2026, and is expected to reach USD 37.03 billion by 2031, at a CAGR of 13.10% during the forecast period (2026-2031).

An expanding pipeline of multi-omics studies, rising regulatory pressure for precision diagnostics, and the pharmaceutical sector’s pivot toward data-centric R&D continue to reposition bioinformatics platforms from tactical tools to enterprise infrastructure. Cloud hyperscalers are embedding genomics-optimized services that shift capital expense to consumption-based models, while near-instrument analytics reduce latency and data-egress costs in clinical laboratories. Vendors that combine AI-native algorithms with elastic compute are capturing the largest share of new deployments, even as cybersecurity and workforce gaps temper near-term scalability. The resulting competitive landscape is defined by convergence: sequencing instrument makers, contract research organizations, and software start-ups now vie to own the same analytics stack.

Key Report Takeaways

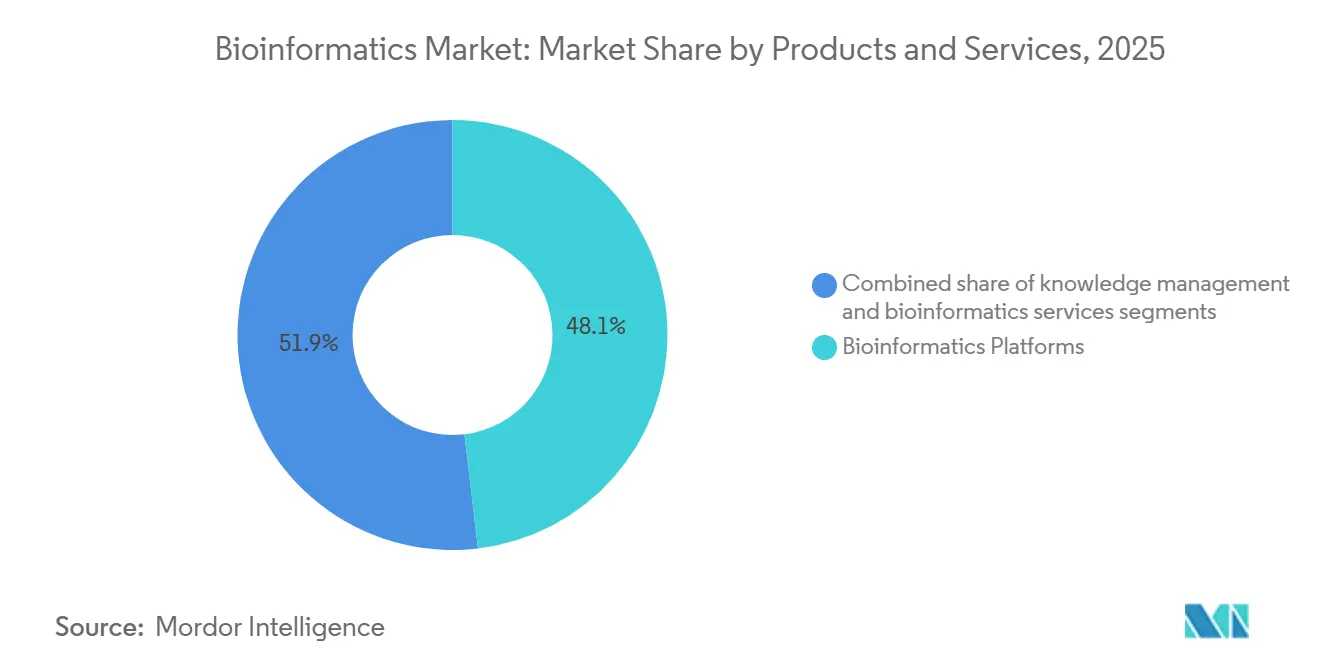

- By products and services, bioinformatics platforms led with 48.1% revenue share in 2025, whereas bioinformatics services are advancing at a 14.1% CAGR through 2031.

- By application, genomics and transcriptomics commanded a 34.6% share of the bioinformatics market size in 2025, while proteomics and metabolomics are forecast to expand at a 14.43% CAGR to 2031.

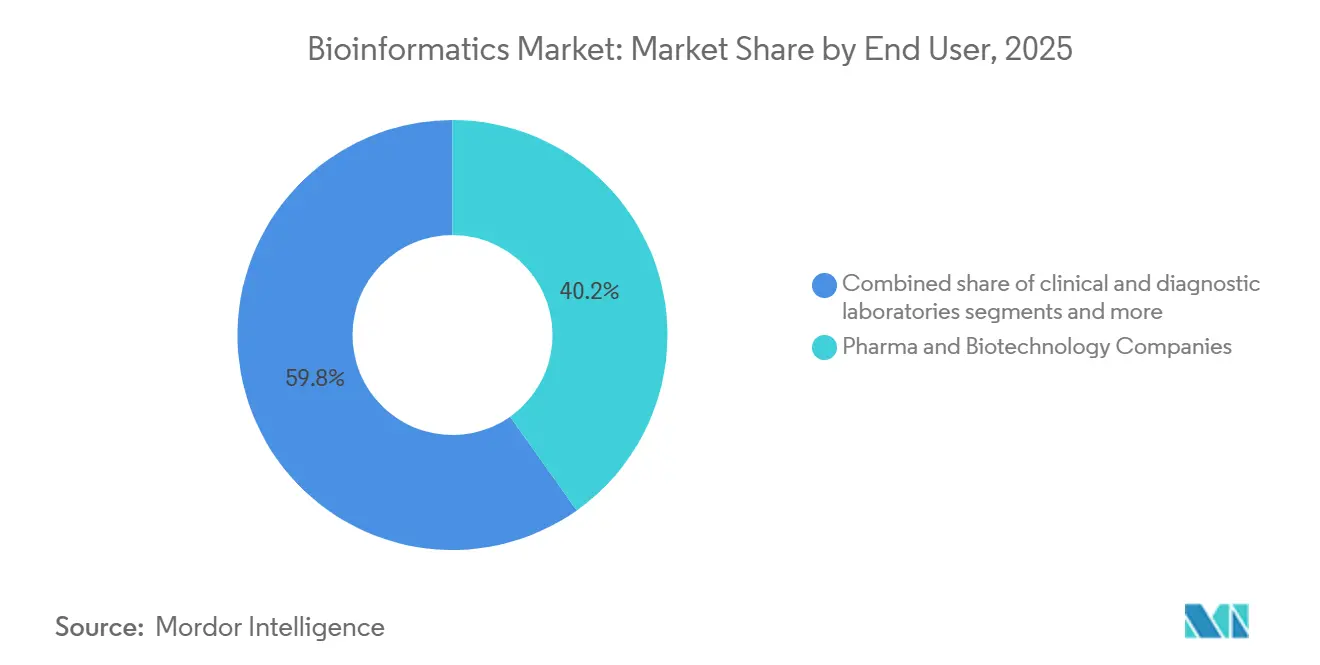

- By end-user, pharmaceutical and biotechnology companies accounted for 40.2% of the bioinformatics market share in 2025; contract research organizations are the fastest-growing segment at 13.98% CAGR to 2031.

- By geography, North America held a 39.4% share in 2025, yet Asia-Pacific is projected to register a 14.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bioinformatics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of multi-omics data volumes | +2.8% | Global, peak in North America and China | Short term (≤ 2 years) |

| Precision medicine and companion diagnostics | +2.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Pharma-biotech shift toward data-centric R&D | +2.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government-funded genomic initiatives | +1.9% | North America, UK, China, India | Long term (≥ 4 years) |

| Edge or near-instrument processing | +1.6% | North America, Europe, core Asia-Pacific | Short term (≤ 2 years) |

| AI model marketplaces | +1.4% | Global, early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion of Multi-Omics Data Volumes

Sequencing throughput has surpassed 20 petabases per instrument per year, yet storage and compute infrastructure trail demand, creating bottlenecks that bioinformatics platforms must resolve. The cost to sequence a human genome fell below USD 200 in 2024, but downstream analysis now costs three to five times that amount, driving investment in compression algorithms and federated learning that process data in situ. Pharmaceutical sponsors increasingly integrate genomic, transcriptomic, proteomic, and metabolomic datasets from identical patient cohorts, a workflow that depends on GPU clusters and object storage optimized for petabyte-scale workloads. Cloud providers such as AWS, Google Cloud, and Microsoft Azure are responding with managed pipelines that accelerate variant calling and annotation. Edge appliances embedded inside sequencers further minimize data-transfer fees by handling base-calling and primary analysis locally. Together, these dynamics sustain double-digit spending on elastic compute even as per-sample sequencing costs decline.

Precision Medicine and Companion Diagnostics Adoption

Regulatory approvals for companion diagnostics rose in 2025 as compared to 2024, owing to reinforcing the need for pipelines that detect complex genomic alterations with clinical-grade accuracy. Tumor-agnostic therapies targeting NTRK fusions and MSI-high signatures require panels interrogating more than 300 genes, shifting demand from single-gene assays toward comprehensive profiling. The European Medicines Agency finalized guidance in 2024 that obligates analytical validation across diverse ethnic cohorts, prompting expansion of reference datasets and ethnicity-aware algorithms. Japan added reimbursement codes for liquid biopsy monitoring in 2025, catalyzing the uptake of tools that track circulating tumor-DNA dynamics. Collectively, these policies anchor bioinformatics spending in oncology, yet spill into cardiology and rare disease as payers recognize the pharmacoeconomic value of stratified therapeutics.

Pharma-Biotech Shift Toward Data-Centric R&D

Pharmaceutical pipelines now lean on in-silico hypothesis generation to shorten wet-lab cycles. AlphaFold’s open release of 200 million protein structures demonstrated that years of crystallography can be compressed into hours of GPU time, accelerating structure-guided drug design. Antibody discovery particularly benefits as generative models trained on immune-repertoire data propose binders with predicted developability, trimming candidate pools significantly. Large sponsors, therefore, expand internal AI units while partnering with vendors that supply turnkey structure-prediction workflows. Contract research organizations scale similar capabilities across multiple clients, converting infrastructure into billable services and boosting adoption among cash-constrained biotech start-ups.

Government-Funded Genomic Initiatives

The NIH All of Us program released whole-genome sequences for 245,000 participants in 2025, creating the largest ethnically diverse cohort for precision-medicine research [1]National Institutes of Health, “All of Us Research Program Update,” nih.gov. The UK Biobank added proteomic and metabolomic layers for 50,000 volunteers, producing integrated datasets that academic labs mine for cardiovascular biomarkers. China's National Genomics Data Center now stores more than 10 petabytes of sequencing data, enabling the construction of population-specific reference genomes that improve variant interpretation for Asian cohorts. India’s Genome India project finished sequencing 10,000 individuals, laying groundwork for dose-optimization studies that reduce adverse events linked to CYP2C19 and CYP2D6 alleles. These large-scale initiatives stimulate domestic cloud build-outs and fuel cross-border analytics partnerships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled bioinformaticians | -1.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Fragmented data standards | -1.4% | Global, disruptive in multi-site trials | Long term (≥ 4 years) |

| Cybersecurity and genomic-data privacy risks | -1.2% | Global, high regulatory pressure in the West | Short term (≤ 2 years) |

| Rising cloud egress and long-term storage fees | -1.0% | Global, acute for population-scale projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Bioinformaticians

Academic programs graduated roughly 8,500 computational biologists in 2025, versus industrial demand for more than 15,000 new hires, widening a talent gap that inflates salaries past USD 150,000 for mid-career professionals [2]U.S. Bureau of Labor Statistics, “Occupational Outlook for Bioinformatics Scientists,” bls.gov. Companies launch in-house training to upskill molecular biologists in Python and R, while platform vendors embed no-code interfaces to widen usability. Offshore talent pools in India and Eastern Europe offer partial relief, though time-zone and data-sovereignty constraints restrict protected-health-information workflows.

Cybersecurity and Genomic-Data Privacy Risks

Ransomware attacks targeting genomic datasets rose significantly year over year in 2025, forcing laboratories to upgrade zero-trust architectures and comply with stricter HIPAA and GDPR enforcement. Insurance premiums for cyber coverage have surged, and some payers now mandate external penetration testing as a prerequisite for reimbursement of genomic assays. Encryption at rest and federated analysis mitigate exposure but add cost overhead that squeezes margins for smaller diagnostic centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Platforms Lead While Cloud Services Accelerate

Platforms accounted for 48.1% of the bioinformatics market in 2025, driven by tightly coupled sequence analysis workflows with Illumina and Oxford Nanopore instruments. Within this category, consumption-based cloud deployment is winning share as laboratories migrate away from depreciating on-premise clusters. Services grow at a 14.1% CAGR through 2031 by translating capital expenditure into variable operating expense and bundling compliance frameworks that satisfy CLIA and CE-IVDR requirements. Sequence analysis remains core, yet multi-omics integration and knowledge-management modules now bundle graph databases and text-mining engines that surface pathway insights faster than manual curation. Platform vendors that cannot deliver both cloud and edge codebases face consolidation pressure, as evidenced by recent mid-tier mergers.

Bioinformatics services capture expanding wallet share from small biotech and academic labs that lack internal computational teams. Hyperscalers amplify this trend by embedding genomics toolkits—AWS HealthOmics, Google Cloud Life Sciences API—into broader cloud offerings, often priced below cost to drive storage and compute consumption. As a result, the bioinformatics market size attributable to standalone software licenses is declining even though overall spend rises. Subscription and per-sample fees replace one-time hardware revenue, aligning vendor incentives with customer data volumes. Knowledge-management tools still monetize curation quality, yet open-access resources erode their pricing power, shifting emphasis toward proprietary algorithms that integrate with electronic lab notebooks and laboratory-information systems.

By Application: Proteomics Emerges as Growth Leader

Genomics and transcriptomics held 34.6% share of the bioinformatics market size in 2025, anchored by national sequencing programs and oncology diagnostics. Proteomics and metabolomics, however, register 14.43% CAGR through 2031 on the back of mass-spectrometry advances that quantify more than 10,000 proteins per sample. Spatial techniques overlay molecular signals onto tissue architecture, driving demand for GPU-accelerated visualization. Drug discovery pipelines integrate structure-prediction algorithms with generative chemistry to trim preclinical timelines, while microbial genomics gains urgency as governments monitor antimicrobial resistance.

Precision-medicine use cases transition from research to clinic, with FDA-approved pharmacogenomic labels surpassing 400 in 2025. Agricultural and environmental genomics also rise as regulators evaluate CRISPR-edited crops for off-target effects. Single-cell sequencing marries imaging and omics, producing terabyte-scale datasets that necessitate real-time analytics and edge computing. Collectively, these emerging applications rebalance vendor portfolios and suppress reliance on single-omics revenues.

By End-User: CROs Capitalize on Outsourcing Wave

Pharmaceutical and biotechnology enterprises generated 40.2% of demand in 2025, deploying private clouds that integrate experimental data with regulatory submissions. Contract research organizations outpace other groups at 13.98% CAGR, leveraging shared infrastructure to amortize compute across sponsors and deliver turnkey analytic reports. Academic and research institutes remain influential but lose share as grant funding plateaus.

Clinical and diagnostic laboratories embed regulated pipelines that comply with CLIA and CAP checklists, a move that elevates demand for validated variant-interpretation engines. Agri-genomic and environmental testing firms, although niche, are growing swiftly as seed companies implement genomic selection. CRO acquisitions of platform providers, such as IQVIA’s 2024 purchase of a genomics division, illustrate vertical integration that captures more value per sample.

Geography Analysis

North America commanded 39.4% of the bioinformatics market in 2025, backed by a dense cluster of pharmaceutical headquarters, academic centers, and venture funding. FDA guidance published in 2024 tightened clinical validity standards for next-generation sequencing tests, extending development cycles yet raising overall data-analysis complexity. Canada’s precision-oncology networks deploy federated platforms that comply with provincial privacy acts, and Mexico’s biosimilar producers adopt bioinformatics tools for comparability protocols, diversifying regional demand.

The Asia-Pacific region is forecast to expand at a 14.89% CAGR through 2031 as China’s state-sponsored genomics ecosystem scales sequencing capacity and vertically integrates analytics platform [3]BGI Genomics, “Investor Relations Presentation,” bgi.com India incubates start-ups that localize pipelines for South-Asian haplotypes, and Japan broadens reimbursement for 500-plus-gene panels, pushing hospital adoption of clinical-grade software. Australia and South Korea invest in national precision-medicine programs that couple cloud computing with sovereign data centers, ensuring compliance with domestic cybersecurity statutes.

Europe’s In Vitro Diagnostic Regulation, enforceable from 2024, obliges software used in diagnostics to obtain CE-IVDR certification, increasing vendor compliance costs. Germany’s National Genome Center centralizes rare-disease workflows, while the United Kingdom integrates whole-genome sequencing into the National Health Service, mandating turnaround times of less than 14 days. South America’s market centers on Brazil’s pharmacogenomics pilots and Argentina’s crop genomics programs, whereas the Middle East and Africa remain nascent, with the United Arab Emirates and Saudi Arabia funding large-scale sequencing as part of their economic diversification agendas.

Competitive Landscape

The top five suppliers, Illumina, Thermo Fisher Scientific, QIAGEN, Agilent Technologies, and Roche, held a majority share in 2025, indicating moderate concentration. Illumina continues its vertical-integration play, coupling DRAGEN acceleration with instrument sales to generate USD 450 million in recurring software revenue. Thermo Fisher pursues horizontal expansion, acquiring point solutions and folding them into a cloud platform that spans sample prep to variant interpretation.

Disruptors include AI-first firms such as Insitro and Recursion, which commercialize proprietary analytics stacks originally built for internal drug discovery. NVIDIA’s BioNeMo toolkit enables pharmaceutical companies to train foundation models on local data, reducing reliance on third-party platforms. Standards bodies like GA4GH release open APIs that could commoditize routine alignment and variant calling, heightening price competition.

Bioinformatics Industry Leaders

Illumina Inc.

Thermo Fischer Scientific

Qiagen NV

Agilent Technologies

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Illumina released its cloud-based Connected Multiomics platform. The software integrates diverse biological data types, including genomics, transcriptomics, and proteomics, into a single interface to streamline precision medicine research.

- May 2025: Illumina launched DRAGEN version 4.4 software (v4.4). The latest version of DRAGEN includes out-of-the-box oncology applications for clinical research and support for newly announced Illumina multiomics assays.

- February 2025: Qiagen acquired Bioinformatics Solutions Inc. (BSI) to strengthen its position in proteomics and mass spectrometry data analysis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global bioinformatics market as yearly revenue generated from commercial software platforms, curated biological databases, and paid analytical services used to store, manage, visualize, and interpret multi-omics data across genomics, transcriptomics, proteomics, and metabolomics.

Scope exclusions include sequencing hardware, unbundled cloud storage, and generic AI coding toolkits that sit outside this frame.

Segmentation Overview

- By Products & Services

- Knowledge Management Tools

- Bioinformatics Platforms

- Sequence Analysis Platforms

- Sequence Alignment Platforms

- Sequence Manipulation Platforms

- Structural & Functional Analysis Platforms

- Multi-omics Integration Platforms

- Bioinformatics Services

- Sequencing & Data-Generation Services

- Database Construction & Management

- Data Analysis & Interpretation Services

- Cloud-native Bioinformatics-as-a-Service

- By Application

- Genomics & Transcriptomics

- Proteomics & Metabolomics

- Drug Discovery & Development

- Microbial Genomics (Metagenomics & AMR)

- Precision & Personalized Medicine

- Other Applications

- By End-user

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Clinical & Diagnostic Laboratories

- Contract Research Organizations (CROs)

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview software product leads, pharmaceutical bioinformaticians, academic core-facility heads, and CRO managers across North America, Europe, and Asia-Pacific. These conversations validate adoption intensity, discounting habits, and unmet needs that secondary material alone cannot reveal.

Desk Research

We begin with authoritative public data. Mordor analysts follow data-volume trends through EMBL-EBI, NCBI, and clinicaltrials.gov, mine algorithm patents using Questel, and map research funding on NIH RePORTER and Horizon Europe. Trade flows from Eurostat and the US International Trade Commission hint at cross-border software exports, while company filings, investor decks, and Bio-IT World briefs enrich context. Our paid access to D&B Hoovers and Dow Jones Factiva supplies granular revenue splits.

A second pass lines up catalog prices on major cloud marketplaces, tender notices on Tenders Info, and posted service rate cards, giving our team realistic average selling prices. The sources named are illustrative; many additional references support data gathering and validation.

Market-Sizing & Forecasting

A top-down build converts global sequencing output and sample counts into expected analysis workloads. Then, blended average prices yield 2025 spending. Supplier roll-ups, channel checks, and sampled volume-price tests create a bottom-up view that is reconciled with the top-down total. Key variables like cloud migration share, multi-omics pipeline penetration, public R&D growth, bioinformatician head count, and regulatory incentives feed a multivariate regression extending results to 2030. Proxy ratios agreed during expert calls bridge any disclosure gaps.

Data Validation & Update Cycle

Outputs run through variance dashboards, multi-step peer review, and anomaly alerts before sign-off. We refresh every model each year and issue interim updates when material events shift inputs; every release receives a final fact pass.

Why Mordor's Bioinformatics Baseline Earns Extra Credibility

Published estimates differ because providers mix scopes, currency years, and refresh cadences. By anchoring strictly to revenue-earning analytics and by using fresher inputs, Mordor Intelligence offers a balanced baseline that buyers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.66 B (2025) | Mordor Intelligence | - |

| USD 31.74 B (2025) | Global Consultancy A | Adds AI tools and bundled cloud fees |

| USD 20.34 B (2025) | Trade Journal B | Uses list prices, ignores discounts |

| USD 19.51 B (2024) | Regional Consultancy C | Blends analytics with data-center services |

The comparison shows how our disciplined scope, live inputs, and blended modeling provide decision makers with an auditable, forward-looking view.

Key Questions Answered in the Report

How fast is the bioinformatics market expected to grow through 2031?

The bioinformatics market is projected to expand from USD 19.97 billion in 2026 to USD 37.03 billion by 2031, registering a 13.1% CAGR.

Which product category currently contributes the most revenue?

Bioinformatics platforms contributed 48.1% of total revenue in 2025, reflecting their central role in sequence analysis and multi-omics integration.

Why are contract research organizations gaining share?

CROs scale bioinformatics infrastructure across multiple sponsors, lowering per-project costs and achieving a projected 13.98% CAGR in demand through 2031.

Why is precision medicine important for Bioinformatics market growth?

Precision medicine depends on translating genomic data into clinical actions, and bioinformatics platforms provide the analytics that enable this translation.

Which region will see the fastest expansion by 2031?

Asia-Pacific is set to grow at a 14.89% CAGR, propelled by large-scale government genomics initiatives in China, India, and Japan.

How are vendors addressing data-security concerns?

Providers deploy zero-trust architectures, local edge processing, and federated analysis to comply with HIPAA and GDPR while reducing exposure to ransomware attacks.

Page last updated on: