Online Therapy Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

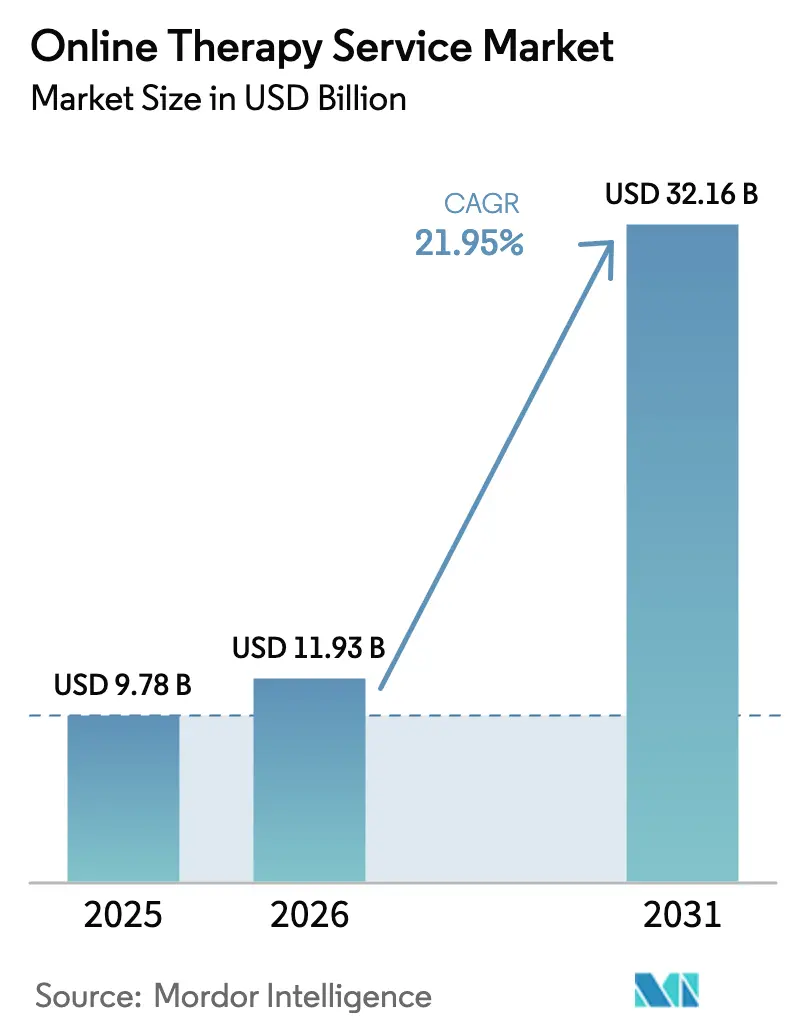

| Market Size (2026) | USD 11.93 Billion |

| Market Size (2031) | USD 32.16 Billion |

| Growth Rate (2026 - 2031) | 21.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Therapy Service Market Analysis by Mordor Intelligence

The Online Therapy Service Market size was valued at USD 9.78 billion in 2025 and estimated to grow from USD 11.93 billion in 2026 to reach USD 32.16 billion by 2031, at a CAGR of 21.95% during the forecast period (2026-2031).

Rising mental-health prevalence, rapid smartphone diffusion, expanding reimbursement parity and the arrival of fully regulated prescription digital therapeutics combine to propel demand. Regulatory milestones such as the FDA’s clearances for Rejoyn and DaylightRx signal institutional confidence in software-based interventions. Medicare’s new payment codes for digital mental-health devices lower payer friction and create sustainable economics for providers. At the same time, immersive virtual-reality (VR) exposure tools, AI-driven triage engines and multilingual conversational interfaces are redefining engagement, while corporate employee-assistance programs (EAPs) use productivity analytics to justify larger budgets. Compliance urgency remains high after the FTC action against BetterHelp underscored data-privacy risk, yet robust encryption standards and dynamic consent portals strengthen patient trust.

Key Report Takeaways

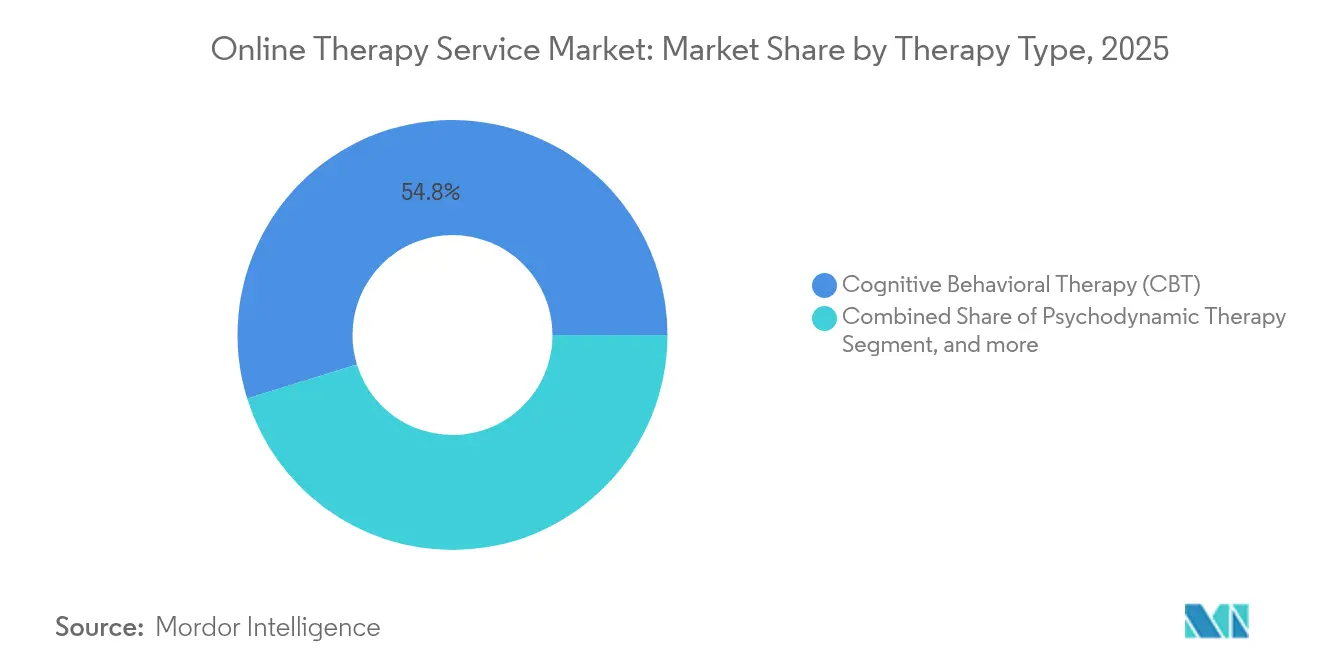

- By therapy type, cognitive behavioral therapy led with 54.78% revenue share in 2025, whereas VR-based exposure and other emerging modalities are projected to expand at a 24.02% CAGR to 2031.

- By delivery platform, mobile app services accounted for 26.32% of the online therapy service market share in 2025, while AI chatbot-led hybrid models record the highest expected CAGR at 25.85% through 2031.

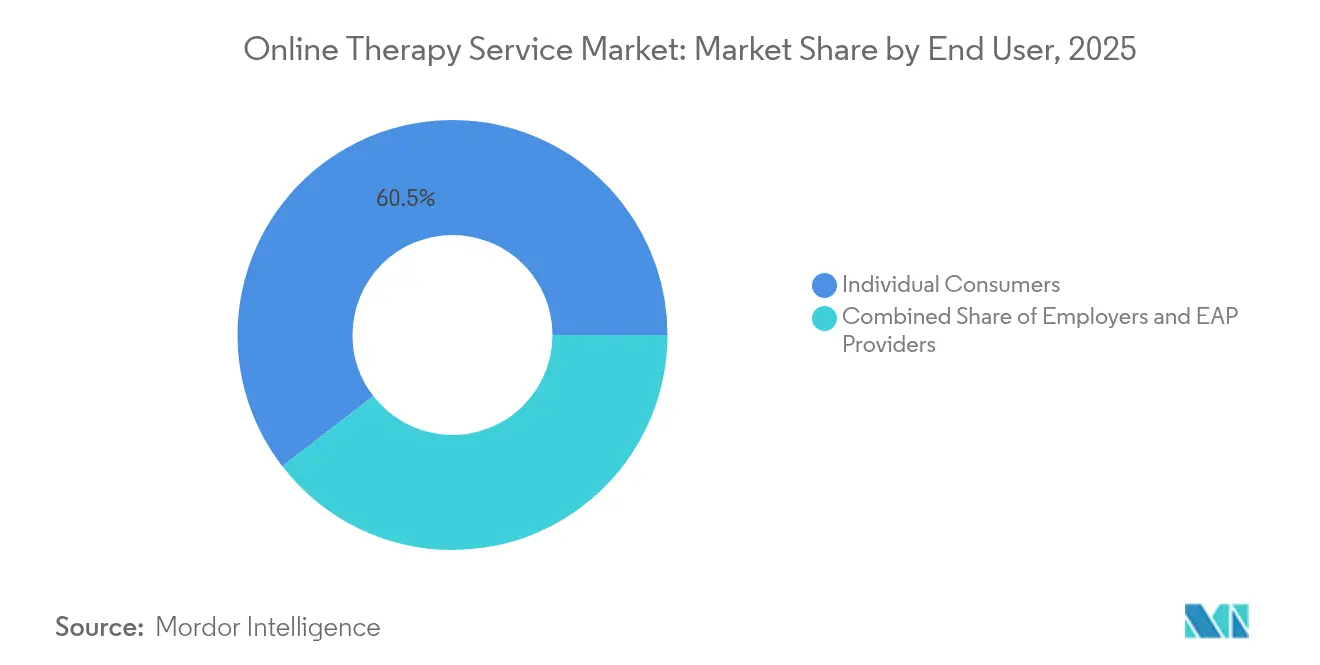

- By end user, individual consumers contributed 60.46% of 2025 revenue, yet employers and EAP providers exhibit a 22.15% CAGR over the forecast horizon.

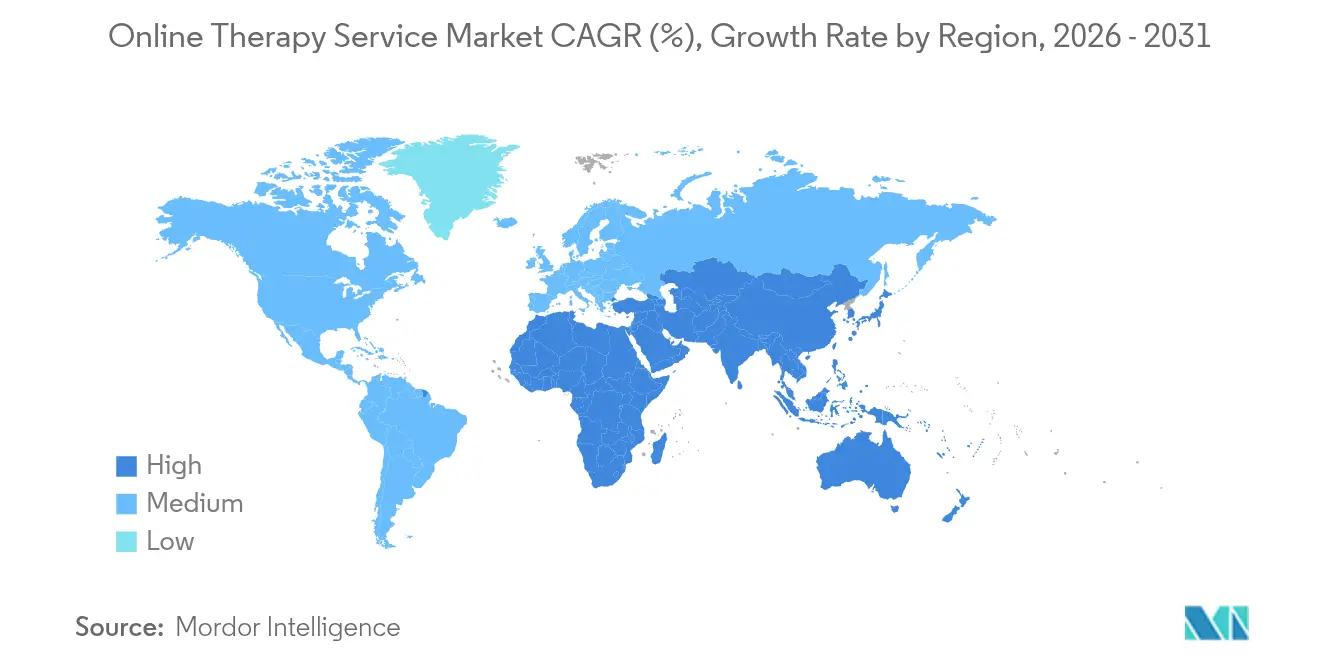

- By geography, North America controlled 38.66% of 2025 revenue, and Asia-Pacific is on track to post a 27.20% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Therapy Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of mental-health disorders | +4.2% | Global (acute in North America and Europe) | Long term (≥ 4 years) |

| Increasing technological and smartphone penetration | +3.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Expanded reimbursement parity and lower delivery cost | +3.1% | North America and EU, early adoption in Australia | Medium term (2-4 years) |

| Corporate EAP demand tied to productivity analytics | +2.9% | North America, expanding to Asia-Pacific corporates | Short term (≤ 2 years) |

| AI-driven personalised therapy and triage engines | +4.5% | Global, led by North America and China | Long term (≥ 4 years) |

| Multilingual platforms addressing diaspora markets | +2.1% | Global, concentrated in multicultural urban centres | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Mental-Health Disorders

The WHO identified a 25% jump in anxiety and depression cases after COVID-19, a shift that persists into 2025.[1]World Health Organization, “COVID-19 Pandemic Triggers 25% Increase in Anxiety and Depression,” who.int In the United States, CuraLinc found that 42% of 85,000 screened employees showed clinical anxiety before intervention, with each affected worker losing 64.4 productive hours monthly. These figures drive policy makers, payers and employers alike toward scalable online solutions that can match soaring demand without limit on geographic reach.

Increasing Technological & Smartphone Penetration

Asia-Pacific hosts 1.8 billion mobile subscribers, equating to 63% population penetration and 51% mobile-internet access, which provides a ready gateway for therapy apps.[2]GSMA, “Mobile Economy Asia Pacific 2024,” gsma.com Fifth-generation networks and edge computing slash latency, enabling VR exposure programs that adapt in real time to biometric feedback collected by wearables. Carnegie Mellon University reported that participants using VR stress-management simulations improved self-awareness and intended to continue practice with more realistic future avatars.[3]Carnegie Mellon University, “Immersive VR for Stress Management,” cmu.edu Multilingual safety work by Wysa across 20 languages targets cultural and linguistic hurdles that once limited access. As bandwidth improves, emerging economies can leapfrog desktop-era constraints and adopt advanced modalities immediately.

Expanded Reimbursement Parity & Lower Delivery Cost

Medicare introduced three permanent payment codes for digital mental-health devices beginning in 2025, removing a core adoption barrier. UnitedHealthcare followed with coverage for audio-only sessions and remote monitoring, broadening the list of reimbursable services. Cost dynamics favour online channels because they eliminate facility overhead, reduce no-show rates and allow asynchronous touchpoints that raise therapist capacity. Larger providers have begun buying smaller, insurance-enabled start-ups to integrate coverage options; Teladoc acquired UpLift for USD 30 million to convert cash-pay users to insured memberships, aiming for 30% longer member tenure. State-level telehealth parity laws now span most US jurisdictions, supporting sustained growth.

Corporate EAP Demand Tied to Productivity Analytics

Modern EAPs combine clinical care with dashboards that isolate absenteeism, presenteeism and turnover risk. A peer-reviewed analysis of 85,000 employee cases showed 78% anxiety recovery and 87% depression recovery after EAP engagement, confirming quantifiable value. Johns Hopkins Healthcare screened 56,442 staff via an app-based assessment and routed 418 high-risk individuals to care concierge support, demonstrating at-scale triage. Academic reviews place EAP return on investment at between USD 5.17 and USD 6.47 for every dollar spent. Asia-Pacific surveys reveal only 29% employee awareness of available EAP tools, highlighting headroom for outreach through familiar mobile channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and privacy compliance hurdles | -2.8% | Global (acute in EU and North America) | Short term (≤ 2 years) |

| Uneven reimbursement and regulatory patchwork | -3.2% | Global, varies by jurisdiction | Medium term (2-4 years) |

| Cross-border licensing and credential reciprocity gaps | -1.9% | International markets, US interstate commerce | Long term (≥ 4 years) |

| Digital fatigue reducing session adherence | -2.1% | Global, higher in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Security & Privacy Compliance Hurdles

The FTC fined BetterHelp USD 7.8 million for sharing protected health information with third-party advertisers, a case that sharpened industry focus on consent management and encryption. Mental-health platforms must reconcile HIPAA, GDPR and a patchwork of state statutes while also delivering frictionless user onboarding. Surveys show 73% of consumers rate privacy as a top criterion when selecting a mental-health app. Compliance requires business-associate agreements, incident-response plans and periodic penetration tests. Smaller companies often lack capital for round-the-clock security operations, tilting competitive advantage toward better funded incumbents.

Uneven Reimbursement / Regulatory Patchwork

Therapists still juggle licence requirements state by state; PSYPACT eases reciprocity yet gaps remain in non-member states. Internationally, 17 nations introduced special telepsychiatry rules during the pandemic, many of which expire or demand renegotiation in 2025. China permits internet diagnosis only for follow-up chronic-disease visits via licensed hospitals, illustrating the nuance of regional frameworks. Payer policies remain inconsistent despite Medicare leadership; some commercial insurers still exclude synchronous chat or digital prescriptions, creating billing risk. These inconsistencies increase administrative overhead and slow expansion for otherwise scalable platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Digital CBT Still Dominates but VR Drives Momentum

The online therapy service market size for cognitive behavioural therapy accounted for 54.78% of total revenue in 2025. VR-based exposure solutions hold a smaller base yet register a forecast CAGR of 24.02%, the highest among modalities. CBT’s digital dominance stems from a vast evidence foundation and modular format that translates smoothly into app and portal delivery. VR addresses shortcomings of screen-based exposure by immersing patients in controlled simulations that replicate trauma triggers with millisecond latency. Clinical trials at Carnegie Mellon University verify meaningful reductions in self-reported stress after repeated VR sessions.

Immersive programs now integrate machine-learning models that escalate or de-escalate stimuli based on real-time heart-rate variability, delivering personalised exposure gradients that human therapists could not manually orchestrate at scale. Psychodynamic and interpersonal approaches maintain smaller, stable niches serving patients seeking deeper relational exploration. Dialectical behaviour therapy and humanistic frameworks continue to expand modestly where emotional regulation or non-directive support are paramount. As VR headsets cross sub-USD 300 price points, hardware barriers fall and home-based exposure therapy becomes viable for mainstream users, eroding CBT’s share in high-anxiety and phobia sub-segments.

By Delivery Platform: Apps Hold the Line as AI Hybrids Surge

Mobile applications captured 26.32% of revenue in 2025, the largest share by platform, because always-on smartphones offer low-friction entry into care. Yet AI chatbot-led hybrid services exhibit a 25.85% CAGR through 2031, setting the growth pace. Web portals stay relevant for content-heavy programs that benefit from larger displays, while audio-only phone counselling remains critical in bandwidth-poor regions. VR and augmented-reality channels sit at the early stage yet post double-digit growth as headset ownership expands.

Hybrid architecture answers two persistent pain points: labour economics and engagement decay. Talkspace’s AI Insights engine reduces clinician document time by summarising session transcripts and recommending next-step interventions, thereby freeing therapists to handle more clients. Wysa’s FDA-recognized agent uses conversational reinforcement to triage users and escalate high-risk cases to licensed counsellors, extending coverage beyond business hours.

By End User: Consumer Volume Meets Employer Velocity

Direct-pay individual users generated 60.46% of 2025 revenue, confirming that self-motivation and convenience remain the primary entry points to digital care. Employers and EAP providers, however, represent the fastest growing customer block at a 22.15% CAGR. Corporate buyers shift spend from broad wellness stipends toward clinically validated therapy subscriptions because productivity dashboards link mental health to output metrics. Payers and insurers are a smaller cohort today but expand rapidly as reimbursement codes mature and claims data prove cost offsets.

CuraLinc analytics reveal that anxiety afflicted employees log 64.4 lost work hours monthly, a statistic that nudges leadership to fund confidential therapy benefits. Johns Hopkins demonstrated that proactive digital screening finds high-risk staff early, shortening absence and turnover windows. Healthcare providers integrate online tools to triage overflow demand, while universities adopt student-specific modules that address stress, peer relations and exam anxiety. The online therapy service market share of employer-funded plans is expected to climb as human-resource teams hard-wire mental health into broader productivity platforms.

Geography Analysis

North America delivered 38.66% of global 2025 revenue, supported by a mature payer system, advanced broadband networks and regulatory leadership in prescription digital therapeutics. The FDA’s clearance of Rejoyn and DaylightRx legitimises software treatment pathways, and Medicare’s permanent codes solidify economic foundations. Canada’s decentralised provincial licensing still introduces friction, yet pilot compacts foster gradual reciprocity. Mexico offers emerging upside as internet connectivity climbs and mental-health stigma recedes.

Asia-Pacific is the velocity engine of the online therapy service market, clocking a 27.20% CAGR through 2031. China’s 1 600 internet hospitals supply follow-up psychological care to some 300 million citizens under defined telemedicine rules, while Japan and South Korea align coverage policies with digital innovation. India mandates therapist identification, patient consent and encryption in its Telemedicine Guidelines, fostering responsible growth. Public-private capital flows continue, typified by Halodoc’s USD 100 million raise for Southeast Asia expansion, illustrating investor faith in long-run addressable demand.

Europe advances steadily on the back of GDPR-compliant architectures and publicly funded health systems. The United Kingdom’s NHS distributes AI-guided CBT from suppliers such as Wysa, building outcome data that inform procurement decisions. Germany and France extend reimbursement parity to include remote sessions, while the EU’s Digital Markets Act pushes platform accountability and user data portability. The Middle East and Africa trail in absolute size but gain momentum as 4G coverage improves and ministries allocate budget for e-mental-health pilots. South America, spearheaded by Brazil, issues telepsychology guidelines yet faces macro-economic swings that affect consumer spending.

Competitive Landscape

Competitive structure remains fragmented, placing the online therapy service market in a mid-consolidation phase. Large telehealth incumbents such as Teladoc, Amwell and Doctor on Demand coexist with mental-health specialists like Talkspace, BetterHelp, Wysa and Spring Health. Technology differentiation now carries more strategic weight than marketing spend. Talkspace’s AI summarisation slashes clinical paperwork, while Wysa pursues regulator-validated conversational care that scales without proportional therapist headcount.

Capital markets reward provable outcomes and payer relationships. Spring Health achieved a multibillion-dollar valuation after publishing data on anxiety remission rates for covered employees, demonstrating that clinical depth boosts enterprise contracts. Teladoc’s USD 30 million UpLift acquisition reflects a pivot toward insured models that lengthen member tenure and mitigate pure consumer churn. Prescription digital therapeutics form a nascent but high-barrier segment where firms like Click Therapeutics and Curio partner with pharmaceutical distributors to commercialise FDA-cleared treatments for migraine and postpartum depression. Multilingual expertise and VR capability remain white-space opportunities for new entrants willing to invest in cultural adaptation and hardware integration.

Online Therapy Service Industry Leaders

BetterHelp

Calmerry

Regain

Brightside Health

Sesame Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Curio received FDA approval for Mamalift, a digital therapeutic for postpartum depression, marking the first FDA-approved digital treatment specifically designed for maternal mental health.

- April 2025: Click Therapeutics received FDA marketing authorization for CT-132, the first prescription digital therapeutic for preventive treatment of episodic migraine, expanding the prescription digital therapeutics category beyond mental health into neurological conditions.

- July 2024: RedBox Rx, a telehealth and online pharmacy provider, launched Online Talk Therapy Services on its platform. This service offering helps expand access to mental health care treatment across the United States.

- April 2024: Headspace, a digital mental health company, reported that it will offer direct-to-consumer mental health coaching to its subscribers. Consumers can obtain three 30-minute online mental health coaching sessions for USD 99.99 per month.

Global Online Therapy Service Market Report Scope

As per the scope of the report, online therapy refers to mental health services and counseling that are provided via the internet or phone rather than in person. The online therapy service market is segmented into therapy type, application, and geography. By therapy type, the market is segmented into cognitive behavioral therapy, psychodynamics therapy, virtual psychotherapy, and personal-centered therapy. By application, the market is segmented into commercial and residential use. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (in USD) for the above segments.

| Cognitive Behavioral Therapy (CBT) |

| Psychodynamic Therapy |

| Dialectical Behavior Therapy |

| Interpersonal Therapy |

| Humanistic / Person-centred |

| VR-based Exposure & Other Emerging Modalities |

| Mobile App-based |

| Web-based Portals |

| Audio-only Telephonic |

| VR/AR Immersive |

| AI Chatbot–led Hybrid Models |

| Individual Consumers |

| Employers & EAP Providers |

| Payers & Insurers |

| Healthcare Providers & Hospitals |

| Educational Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Cognitive Behavioral Therapy (CBT) | |

| Psychodynamic Therapy | ||

| Dialectical Behavior Therapy | ||

| Interpersonal Therapy | ||

| Humanistic / Person-centred | ||

| VR-based Exposure & Other Emerging Modalities | ||

| By Delivery Platform | Mobile App-based | |

| Web-based Portals | ||

| Audio-only Telephonic | ||

| VR/AR Immersive | ||

| AI Chatbot–led Hybrid Models | ||

| By End User | Individual Consumers | |

| Employers & EAP Providers | ||

| Payers & Insurers | ||

| Healthcare Providers & Hospitals | ||

| Educational Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the online therapy service market?

The market is valued at USD 11.93 billion in 2026 and is forecast to reach USD 32.16 billion by 2031.

How fast is the online therapy service market expected to grow?

It is projected to expand at a CAGR of 21.95% during 2026-2031, driven by rising mental-health incidence, improved reimbursement and technological innovation.

Which therapy modality generates the most revenue online?

Digital cognitive behavioural therapy holds 54.78% of 2025 revenue, making it the leading modality.

Which region shows the fastest growth in online therapy services?

Asia-Pacific records the highest forecast CAGR at 27.20% owing to rapid smartphone adoption and supportive regulatory frameworks.

What are the main challenges that could slow market growth?

Key obstacles include privacy compliance, fragmented licensure rules, inconsistent reimbursement and user dropout due to digital fatigue.

How are employers influencing the online therapy service industry?

Employers invest heavily in EAP platforms that link mental-health improvement to productivity gains, a segment growing at 22.15% CAGR through 2031.

Page last updated on: