Precision Oncology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

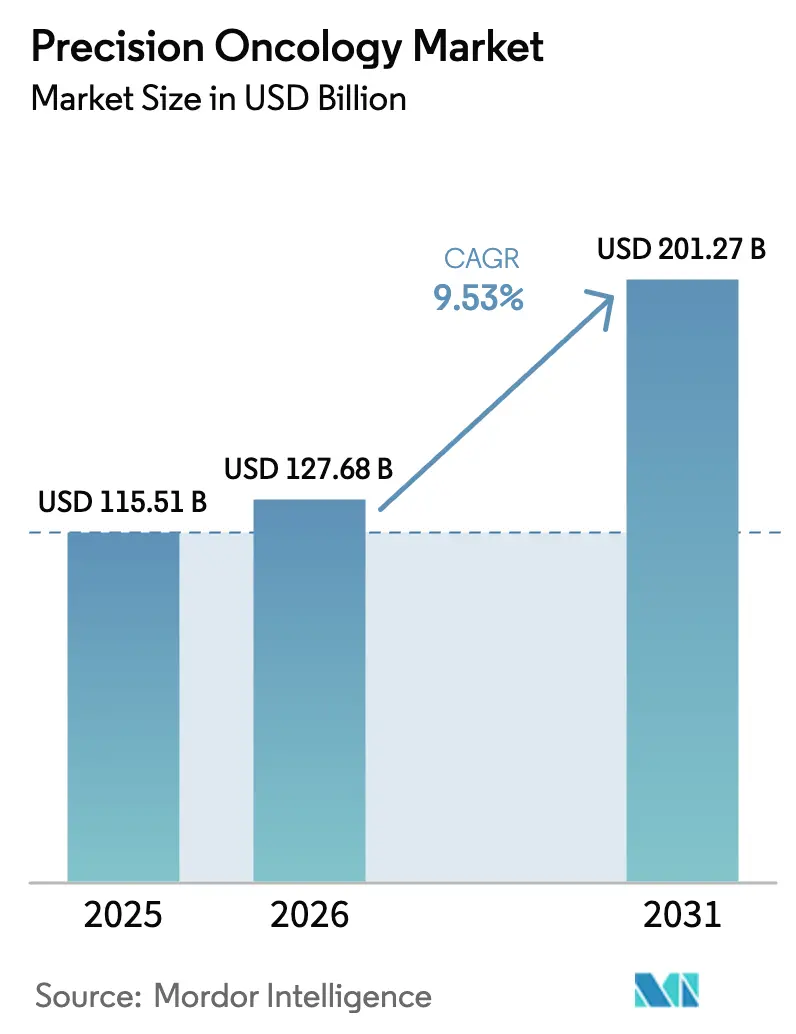

| Market Size (2026) | USD 127.68 Billion |

| Market Size (2031) | USD 201.27 Billion |

| Growth Rate (2026 - 2031) | 9.53% CAGR |

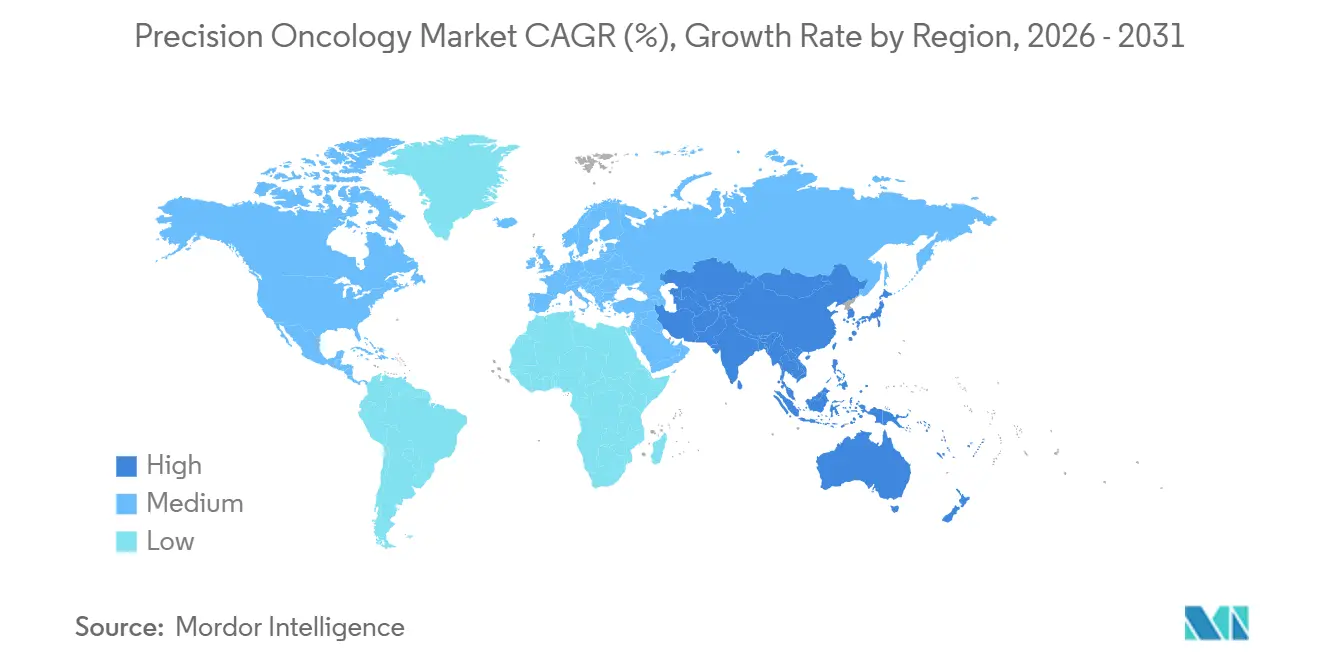

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

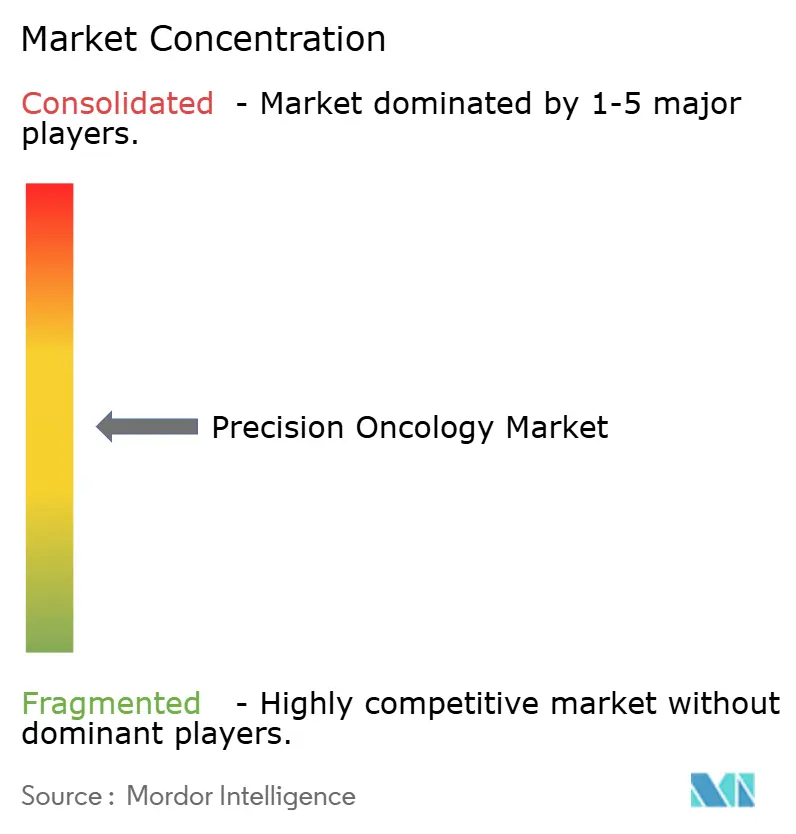

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Oncology Market Analysis by Mordor Intelligence

The Precision Oncology Market size was valued at USD 115.51 billion in 2025 and is estimated to grow from USD 127.68 billion in 2026 to reach USD 201.27 billion by 2031, at a CAGR of 9.53% during the forecast period (2026-2031).

Sequencing costs continue to fall, companion diagnostic approvals are accelerating, and payers now reimburse multi-gene panels that prolong progression-free survival, collectively driving clinical adoption. Therapeutics still generate most revenue, yet liquid-biopsy-based diagnostics are gaining ground as monitoring tools rather than single-time tests. Hospitals currently dominate test volume, but independent laboratories are scaling faster in response to decentralized workflows and point-of-care molecular platforms. North America leads in spending, while regulatory reforms in China and Japan position the Asia-Pacific for the strongest absolute growth. Competitive focus is shifting from raw sequencing capacity to interoperability among analytics, pathology images, and electronic health records.

Key Report Takeaways

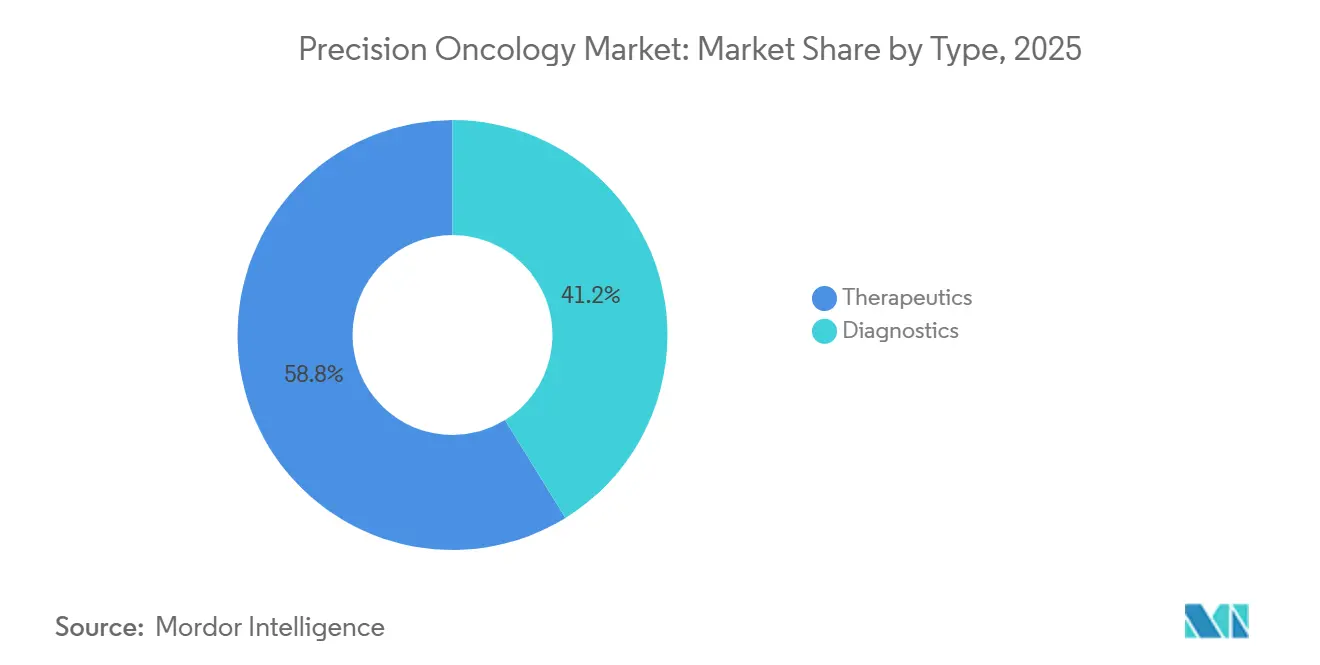

- By type, therapeutics captured 58.81% precision oncology market share in 2025, whereas diagnostics are projected to expand at a 10.06% CAGR to 2031.

- By technology, next-generation sequencing accounted for 36.73% of the precision oncology market size in 2025, while fluorescence in situ hybridization (FISH) is expected to advance at a 10.72% CAGR through 2031.

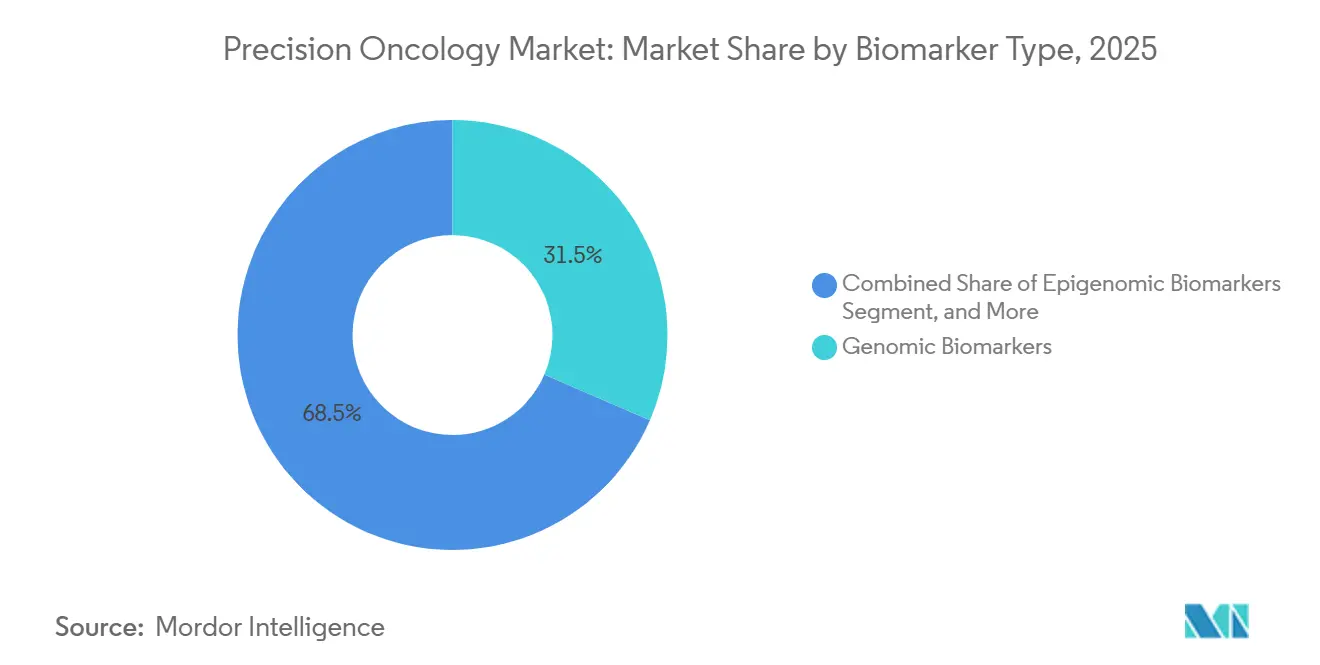

- By biomarker type, genomic biomarkers accounted for a 31.48% share of the precision oncology market size in 2025; epigenomic biomarkers are projected to grow at an 8.79% CAGR through 2031.

- By cancer type, breast cancer led with 49.26% revenue share in 2025, yet prostate cancer is forecast to grow at an 11.53% CAGR through 2031.

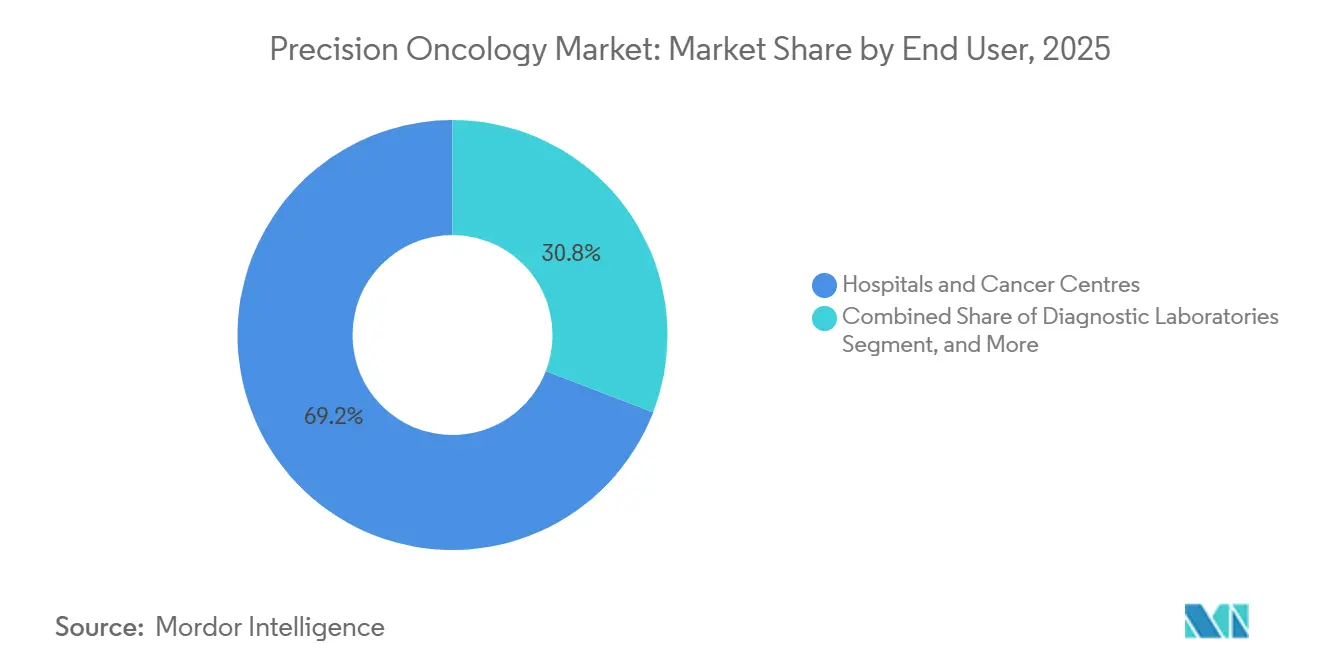

- By end-user, hospitals and cancer centers held a 69.16% precision oncology market share in 2025, while diagnostic laboratories are expected to rise at a 12.27% CAGR through 2031.

- By geography, North America accounted for 42.83% of the revenue in 2025; the Asia-Pacific region is the fastest-growing, with a 13.27% CAGR forecasted to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Precision Oncology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in NGS & AI-Driven Analytics | +1.8% | North America, Europe | Medium term (2-4 years) |

| Rising Cancer Incidence & Favorable Reimbursement | +2.1% | Global | Long term (≥4 years) |

| Companion-Diagnostic Approvals Accelerating Commercialization | +1.5% | North America, Europe, Japan | Short term (≤2 years) |

| Rapid Adoption of Liquid Biopsy Platforms | +1.4% | Global | Medium term (2-4 years) |

| Single-Cell Multi-Omics Integration | +0.9% | North America, Europe, select APAC hubs | Long term (≥4 years) |

| Decentralized Clinical-Trial Models | +0.7% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in NGS & AI-Driven Analytics

AI now reduces whole-genome interpretation from days to hours, allowing real-time therapeutic decisions in acute leukemia and aggressive solid tumors.[1]Illumina Investor Relations, “Q4 2025 Earnings Call Transcript,” illumina.com Illumina’s DRAGEN platform is deployed at more than 1,200 clinical sites and processes a genome in under 90 minutes with high accuracy. FoundationOne CDx expanded into additional tumor types in early 2025 and integrates machine-learning models trained on more than 500,000 de-identified records, yielding a 78% positive predictive value for immunotherapy response. Oxford Nanopore’s adaptive sampling further reduces the per-sample reagent cost by 40% while maintaining diagnostic sensitivity above 99%. These efficiency gains convert molecular profiling from an academic add-on into a routine decision-support tool across community oncology.

Rising Cancer Incidence & Favorable Reimbursement

New cancer cases reached 20.4 million globally in 2024, up 15% from 2020, an increase driven by aging populations and better detection in low- and middle-income nations. Medicare lifted prior-authorization hurdles and now pays up to USD 3,200 per comprehensive genomic profile, boosting test utilization by 60% in Q1 2025 alone.[2]Centers for Medicare & Medicaid Services, “National Coverage Determinations for Genomic Testing,” cms.gov Germany, Japan, and the United Kingdom followed with similar reimbursement upgrades in 2025, sending a clear market signal that molecular information is now the standard of care. As a result, insurers worldwide are increasingly covering upfront profiling for lung, colorectal, and ovarian cancers, where actionable mutations have a prevalence exceeding 60%.

Companion-Diagnostic Approvals Accelerating Commercialization

The FDA cleared a record 18 companion diagnostics in 2025, including liquid-biopsy assays that eliminate the need for tissue re-biopsy in patients with scant archival specimens. Roche’s Ventana PD-L1 SP263 assay secured expanded approval with durvalumab in early-stage non-small cell lung cancer, opening access for roughly 200,000 eligible U.S. patients each year. Guardant360 CDx became the first blood-based pan-tumor companion diagnostic, shortening test-to-treatment time and widening clinical adoption. Parallel review pathways in Europe and streamlined review processes in China further reduce approval lags, creating synchronized global launches and enabling drugmakers to reach broader markets more quickly.

Rapid Adoption of Liquid Biopsy Platforms

Liquid biopsy test volumes expanded by 85% in 2025 as oncologists utilized circulating tumor DNA assays for minimal residual disease surveillance across colorectal and breast cancers. GRAIL’s Galleri test screens for more than 50 tumors through cell-free DNA methylation and shows 67% sensitivity at 99.5% specificity in asymptomatic adults, a landmark performance that prompted England’s National Health Service to launch a 140,000-person pilot in late 2025. Natera’s Signatera now guides adjuvant therapy by detecting relapse six to twelve months before imaging, and Chinese demand is climbing as two provinces added circulating-tumor-DNA coverage to reimbursement schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Personalized Therapeutics & Testing | -1.2% | Global | Long term (≥4 years) |

| Regulatory & Payer Uncertainties | -0.9% | Global | Medium term (2-4 years) |

| Data-Privacy / Interoperability Barriers | -0.6% | Europe, North America | Medium term (2-4 years) |

| Genomic-Database Ethnic Skew | -0.5% | APAC, Africa, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Cost of Personalized Therapeutics & Testing

Targeted drugs, such as antibody-drug conjugates, regularly exceed USD 200,000 annually, far outstripping the health budget capacity in emerging economies. Comprehensive genomic profiling remains self-funded in India, Indonesia, and Brazil, where household income cannot absorb a USD 3,000 test. Even within high-income countries, payers demand real-world evidence proving cost-effectiveness at a level below USD 150,000 per quality-adjusted life year, which muddies coverage decisions for new therapies. Patent exclusivity on next-generation inhibitors delays biosimilar entry until after 2030, keeping drug prices elevated and curbing uptake.

Regulatory & Payer Uncertainties

Fragmented global regulations require separate validation studies for the same assay, extending development time and expense.[3]European Commission, “In Vitro Diagnostic Regulation Guidance,” ec.europa.eu Europe’s In Vitro Diagnostic Regulation imposed performance-study mandates that add more than a year to many submissions. At the same time, some U.S. insurers still reimburse molecular tests only after first-line therapy has failed, thereby diminishing the clinical value of early profiling. The inconsistent stance on polygenic risk scores and tumor-mutational-burden panels introduces forecasting risk for laboratories and investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diagnostics Momentum Overtakes Therapeutics

Diagnostics are expected to post a 10.06% CAGR from 2026 to 2031, even as therapeutics held 58.81% precision oncology market share in 2025. Continuous monitoring through circulating tumor DNA (ctDNA) turns testing into a recurring service, raising lifetime revenue per patient and making the diagnostics segment a structural growth driver within the broader precision oncology market. Liquid biopsy platforms, such as Signatera and Guardant360, deliver molecular insights every three to six months, creating new billing events and embedding laboratories deeper in care pathways. Exact Sciences processed over 2 million Cologuard liquid-biopsy colorectal screens within six months of its launch in 2025, demonstrating that non-invasive tests can reach a population scale when insurers reimburse first-line use.

Therapeutics growth faces mature classes and patent expiries yet still benefits from rising biomarker-defined patient pools. Twelve precision oncology therapeutics gained FDA clearance in 2025, fewer than in 2024, reflecting the maturation of the EGFR and ALK franchises. Drug developers increasingly co-develop diagnostics from early clinical phases, which improves payer confidence but lengthens timelines. Nevertheless, label expansions into adjuvant and neoadjuvant settings will support the precision oncology market as broader patient cohorts become eligible for biomarker-guided treatment.

By Technology: FISH Rebounds on Spatial Biology Needs

Fluorescence in situ hybridization is projected to grow at a 10.72% CAGR to 2031, as spatial biology demands gene-locus visualization that next-generation sequencing cannot provide. Expanded FDA clearance of Abbott’s digital-pathology-compatible ALK Break-Apart probe cuts turnaround times to less than two days, a key advantage for time-sensitive lung cancer cases. FISH also anchors multi-omics spatial platforms such as Visium HD, which overlay transcriptomic maps onto tissue architecture to decode immune-cell positioning.

Next-generation sequencing remains the mainstay, accounting for 36.73% of the precision oncology market size in 2025, with a dominant presence in academic centers. Growth now depends on adopting community practices that run far lower sample volumes yet collectively care for the majority of patients. PCR-based hotspot panels continue to serve as a rapid method for detecting EGFR or KRAS mutations, where a sub-24-hour response influences emergency therapy. Microarray and other technologies retain niche roles in germline testing and gene-expression signatures, sustaining diversified demand across the precision oncology market.

By Biomarker Type: Epigenomic Signatures Gain Share

Genomic biomarkers still accounted for 31.48% of the precision oncology market size in 2025, but epigenomic assays are projected to expand at an 8.79% CAGR through 2031. Methylation-based liquid biopsy detects cancer signal in early stages with sensitivity that eclipses traditional tumor markers, pushing adoption beyond high-risk populations. The USPSTF now recommends Cologuard’s combined methylation and mutation panel as a first-line colorectal screening option, potentially opening a vast asymptomatic segment.

Proteomic, transcriptomic, and metabolomic markers provide complementary layers that refine therapy decisions. Mass-spectrometry cytokine panels forecast immunotherapy response more reliably than PD-L1 staining. Gene-expression signatures guide chemotherapy omission in hormone-receptor-positive breast cancer, sparing thousands from cytotoxic regimens each year. Metabolomics remains research-oriented, yet early data suggest tumor lactate and glutamine levels could soon inform eligibility for metabolic-pathway inhibitors. The multidimensional trend reinforces the precision oncology market pursuit of holistic tumor characterization.

By Cancer Type: Prostate Growth Outstrips Breast Dominance

Breast cancer contributed 49.26% of 2025 revenue, anchoring the precision oncology market with mature HER2, hormone-receptor, and BRCA testing pathways. Market saturation tempers its forward CAGR, whereas prostate cancer is set to experience a 11.53% CAGR through 2031, following Medicare's decision to reimburse germline testing for every new diagnosis, which has led to a 150% increase in testing volume within six months. PARP-inhibitor companion diagnostics extend molecular targeting beyond BRCA into ATM and CHEK2 defects, further broadening precision eligibility.

Lung and colorectal cancers continue to benefit from the expansion of EGFR, ALK, and KRAS panels, particularly in Asia-Pacific, where mutation frequencies are high. Caris Life Sciences profiled more than 100,000 tumors in 2025, with lung and colorectal cancers accounting for 45% of volume. Rare tumors such as cholangiocarcinoma gain new targeted options as fibroblast growth factor receptor fusions are routinely screened. Broader genomic interrogation continues to bring small-population cancers into the revenue fold, supporting the overall expansion of the precision oncology market.

By End-User: Laboratories Capture Outsourced Volume

Hospitals and cancer centers owned 69.16% of the precision oncology market share in 2025, thanks to the integration of tumor boards and on-site pathology. Yet, independent diagnostic laboratories will outpace the market with a 12.27% CAGR through 2031, as decentralized testing lowers capital barriers for community practices. Labcorp and Quest jointly processed more than 1.5 million precision oncology tests in 2025, a 70% surge from 2024.

Research institutions drive the development of cutting-edge single-cell and spatial methods, but their commercial share remains below 5%. Drug developers increasingly outsource biomarker screening to reference labs for trial enrollment, adding another growth leg. Direct-to-consumer liquid biopsies enter routine preventive care as payers cover early detection for high-risk cohorts, expanding the addressable testing pool well beyond hospital walls and sustaining momentum in the precision oncology market.

Geography Analysis

North America commanded 42.83% of the revenue in 2025, following the expansion of Medicare's genomic test coverage and the FDA's acceleration of companion diagnostic reviews. The region maintains leadership through widespread payer reimbursement and a dense sequencing infrastructure, yet its CAGR trails that of the Asia-Pacific region because penetration already exceeds 70% of eligible patients.

Asia-Pacific is forecast to post a 13.27% CAGR from 2026 to 2031, the fastest of any region, buoyed by China’s 12 companion-diagnostic approvals in 2025 and provincial insurance that reimburses up to CNY 20,000 (USD 2,800) per comprehensive profile. BGI Genomics processed 800,000 oncology samples in 2025 and plans a 50% increase in capacity for 2026. Japan increased the payment for genomic profiling to JPY 800,000 (approximately USD 5,300), aligning with global benchmarks and encouraging domestic labs to adopt high-throughput sequencers.

Implementation of the In Vitro Diagnostic Regulation adds cost but harmonizes quality, ensuring reliable data across borders. Whole-genome sequencing within the U.K. Genomic Medicine Service doubled test volume in a year, and France launched regional molecular-tumor-board networks that mandate comprehensive profiling for advanced tumors.

South America and the Middle East & Africa together contribute less than 10% of the spend due to limited public coverage. Brazil cleared six companion diagnostics in 2025; however, without broad reimbursement, fewer than 20% of eligible patients receive the tests. South African private insurers now cover comprehensive genomic profiling, whereas government programs lag, leaving the majority excluded and limiting growth.

Competitive Landscape

Top Companies in the Precision Oncology Market

The precision oncology market is moderately concentrated, with the top five suppliers being Illumina, Roche, Thermo Fisher Scientific, QIAGEN, and Guardant Health. Illumina’s 70% installed-base share in sequencing instruments locks users into its consumables, although Oxford Nanopore is gaining traction for long-read applications that detect structural variants. Roche’s vertical integration following the acquisition of Foundation Medicine enables it to bundle tissue, liquid biopsy, and companion diagnostic services, prompting rivals to pursue similar strategies through mergers and partnerships.

Thermo Fisher maintains its strength in PCR and targeted panels, shipping more than 500,000 Oncomine Dx Target Tests in 2025 to community hospitals without a sequencing lab. Guardant Health leads in high-volume blood-based comprehensive profiling and is expanding its applications in minimal residual disease. QIAGEN differentiates itself through sample preparation and bioinformatics, while Sophia Genetics processes data from 750 hospitals across 70 countries through its cloud AI engine, democratizing analytics.

White-space opportunities emerge in multi-cancer early detection and minimal residual disease for solid tumors. Patent filings for single-cell multi-omics increased by 40% in 2025; 10x Genomics, NanoString, and BGI dominate the spatial transcriptomics IP landscape. Personalis and Adaptive Biotechnologies compete on ultra-deep tumor-informed assays with demonstrated 95% sensitivity. As payers reward early detection and recurrence monitoring, startups with scalable liquid biopsy platforms can capture a share without owning instrumentation, widening the competitive field within the precision oncology market.

Precision Oncology Industry Leaders

F. Hoffmann-La Roche AG

Illumina Inc.

Labcorp (Invitae Corporation)

Novartis AG

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Omico, a not-for-profit leader in genomics, unveiled a pioneering model aimed at making cutting-edge cancer treatments accessible and routine for Australians grappling with rare and complex cancers. The Precision Oncology Health System Incubator (PrO-HSI) charts a strategic investment route, leveraging multi-sector funding and existing policy frameworks. Its goal is to seamlessly weave advanced therapies into current cancer care, all while safeguarding public resources in light of a shrinking taxpayer base and an ageing demographic.

- December 2024: At the Aster Cancer Conclave 2024, Aster DM Healthcare, an integrated healthcare provider in India, unveiled three significant initiatives: Precision Oncology Clinics, the Aster Cancer Grid, and Onco Collect. These initiatives signify a major leap forward in India's cancer treatment landscape. The conclave, which drew prominent oncologists, researchers, and industry experts from both national and international arenas, showcased the forefront of advancements in cancer care and treatment.

- March 2024: Bayer and Aignostics GmbH unveiled a strategic partnership, harnessing artificial intelligence (AI) for precision oncology drug research and development. Aignostics, a spin-off from the renowned Charité-Universitätsmedizin Berlin hospital, stands at the forefront of computational pathology, adeptly translating intricate biomedical data into actionable biological insights.

Global Precision Oncology Market Report Scope

As per the scope of the report, precision oncology involves profiling tumors at the molecular level to pinpoint alterations that can be targeted. It is the practice of tailoring treatment plans based on a patient's genetic structure and the specific molecular traits of their cancer.

The precision oncology market is segmented by type, cancer type, end user, and geography. By type, the market is segmented into therapeutics and diagnostics. By cancer type, the market is segmented into breast cancer, lung cancer, colorectal cancer, prostate cancer, and other types of cancer. By end user, the market is segmented into hospitals, diagnostic laboratories, pharmaceutical & biotechnology companies, and research & academic institutes. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD) for the above segments.

| Therapeutics |

| Diagnostics |

| Next-Generation Sequencing (NGS) |

| Polymerase Chain Reaction (PCR) |

| Fluorescence In-Situ Hybridisation (FISH) |

| Microarray |

| Other Technologies |

| Genomic Biomarkers |

| Proteomic Biomarkers |

| Epigenomic Biomarkers |

| Transcriptomic Biomarkers |

| Metabolomic Biomarkers |

| Breast Cancer |

| Lung Cancer |

| Colorectal Cancer |

| Prostate Cancer |

| Other Cancers |

| Hospitals & Cancer Centres |

| Diagnostic Laboratories |

| Pharma & Biotech Firms |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Therapeutics | |

| Diagnostics | ||

| By Technology | Next-Generation Sequencing (NGS) | |

| Polymerase Chain Reaction (PCR) | ||

| Fluorescence In-Situ Hybridisation (FISH) | ||

| Microarray | ||

| Other Technologies | ||

| By Biomarker Type | Genomic Biomarkers | |

| Proteomic Biomarkers | ||

| Epigenomic Biomarkers | ||

| Transcriptomic Biomarkers | ||

| Metabolomic Biomarkers | ||

| By Cancer Type | Breast Cancer | |

| Lung Cancer | ||

| Colorectal Cancer | ||

| Prostate Cancer | ||

| Other Cancers | ||

| By End-User | Hospitals & Cancer Centres | |

| Diagnostic Laboratories | ||

| Pharma & Biotech Firms | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the precision oncology market?

The precision oncology market size is estimated at USD 127.68 billion in 2026 and is projected to reach USD 201.27 billion by 2031, growing at a 9.53% CAGR.

Which segment is expanding the fastest within precision oncology?

Diagnostics, propelled by liquid-biopsy monitoring, is forecast to post a 10.06% CAGR from 2026 to 2031, outpacing therapeutics.

Why is Asia-Pacific expected to grow faster than North America?

China’s rapid companion-diagnostic approvals and expanded reimbursement in multiple provinces, along with Japan’s higher payment rates, drive a 13.27% regional CAGR.

Which technologies will shape the next wave of precision oncology innovation?

Spatially resolved FISH, single-cell multi-omics, and AI-accelerated sequencing analytics are poised to deepen tumor characterization and broaden clinical use.

What challenges could hinder the growth of precision oncology?

High therapy costs, uneven regulatory pathways, and genomic database ethnic imbalance could collectively shave close to 3% off forecast CAGR if unresolved.

Page last updated on: