Digital Pathology Image Analysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 457.59 Million |

| Market Size (2031) | USD 704.08 Million |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

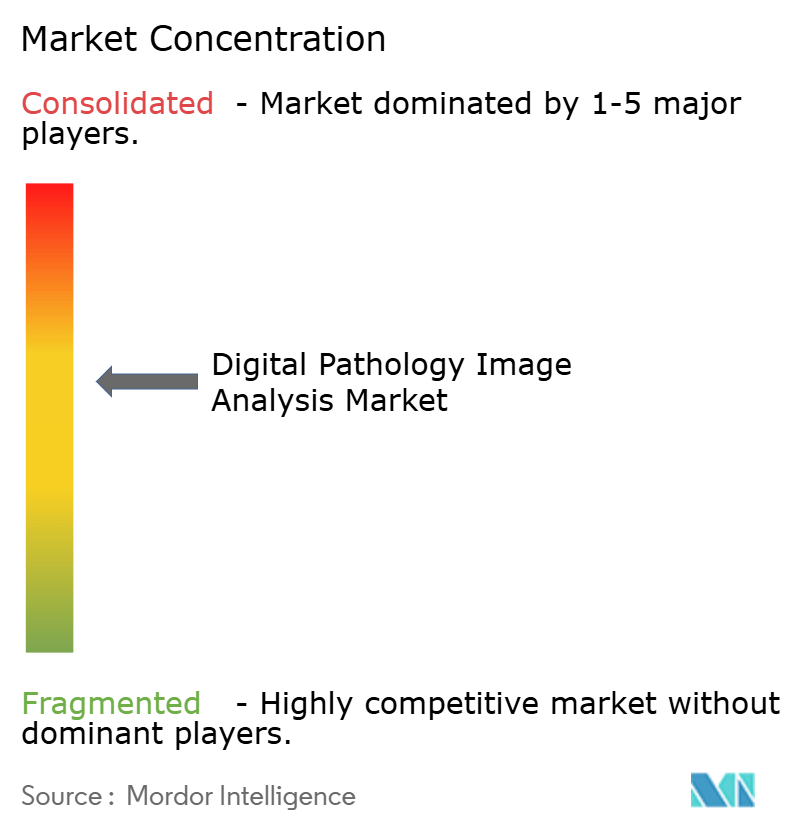

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Pathology Image Analysis Market Analysis by Mordor Intelligence

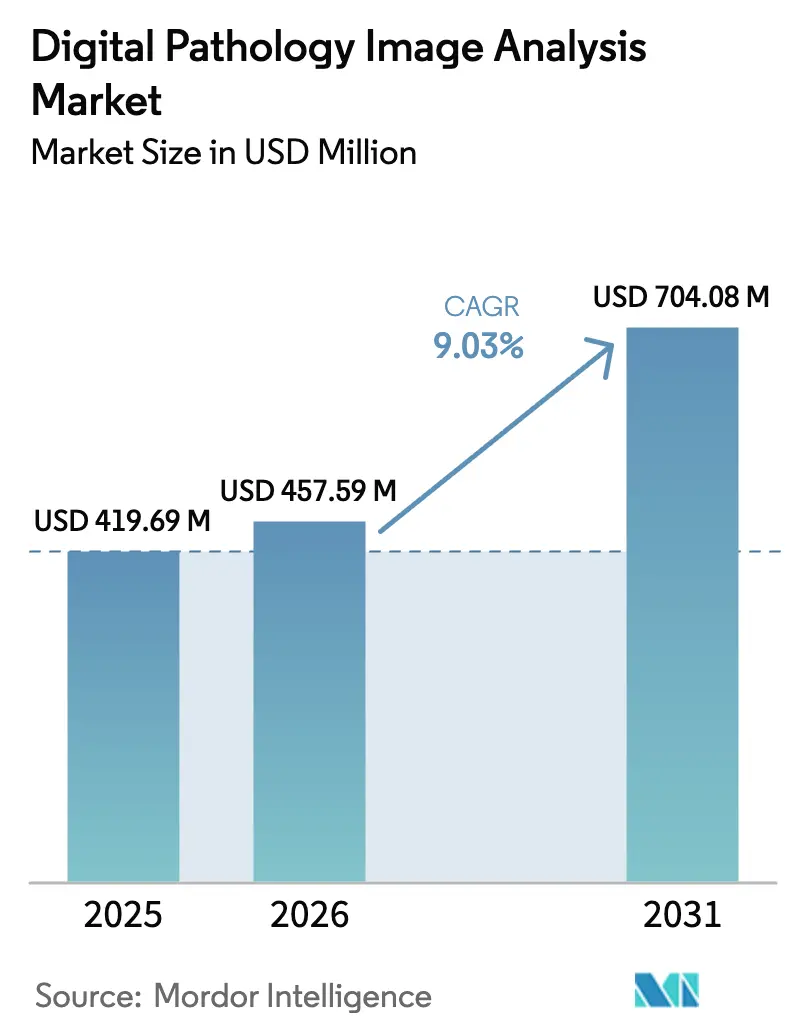

digital pathology image analysis market size in 2026 is estimated at USD 457.59 million, growing from 2025 value of USD 419.69 million with 2031 projections showing USD 704.08 million, growing at 9.03% CAGR over 2026-2031. Steady growth stems from expanding adoption of artificial-intelligence tools that cut diagnostic turnaround times, improve slide-level quality control and offset a widening pathologist shortage. North America keeps its lead through early FDA clearances, favourable reimbursement policies and long-standing telepathology networks, whereas Asia-Pacific accelerates fastest on the back of national AI programmes and hospital network modernisation. Software innovation is shifting from rule-based algorithms to large-vision foundation models, opening opportunities in multi-modal tissue analytics and spatial-omics integration. Competitive dynamics remain fragmented, yet recent acquisitions—such as Quest Diagnostics taking over PathAI’s clinical assets—signal a move toward platform consolidation. Implementation costs and data-privacy regulations temper immediate expansion, but updated reimbursement guidance and federated-learning frameworks continue to unlock fresh addressable demand.

Key Report Takeaways

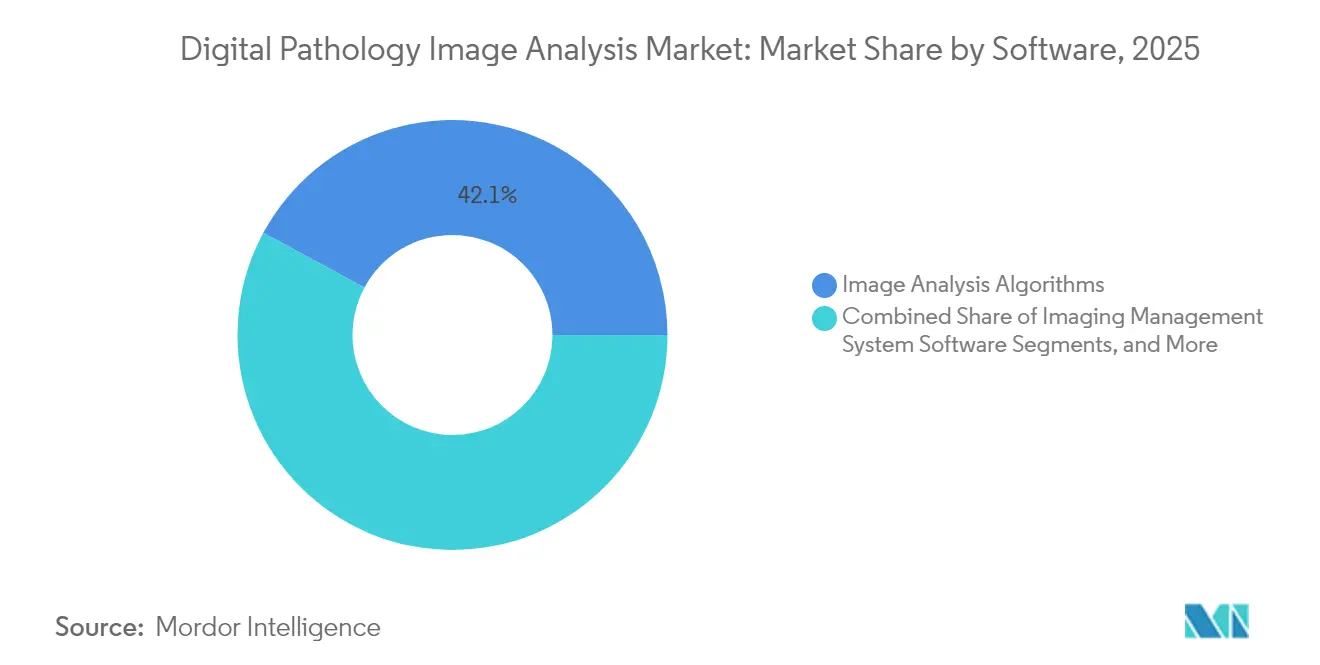

- By software, image analysis algorithms held 42.12% of the digital pathology image analysis market share in 2025, while AI-powered decision-support suites are set to log a 9.78% CAGR to 2031.

- By application, disease diagnosis captured 51.62% of the digital pathology image analysis market size in 2025; drug discovery is projected to expand at a 9.44% CAGR between 2026-2031.

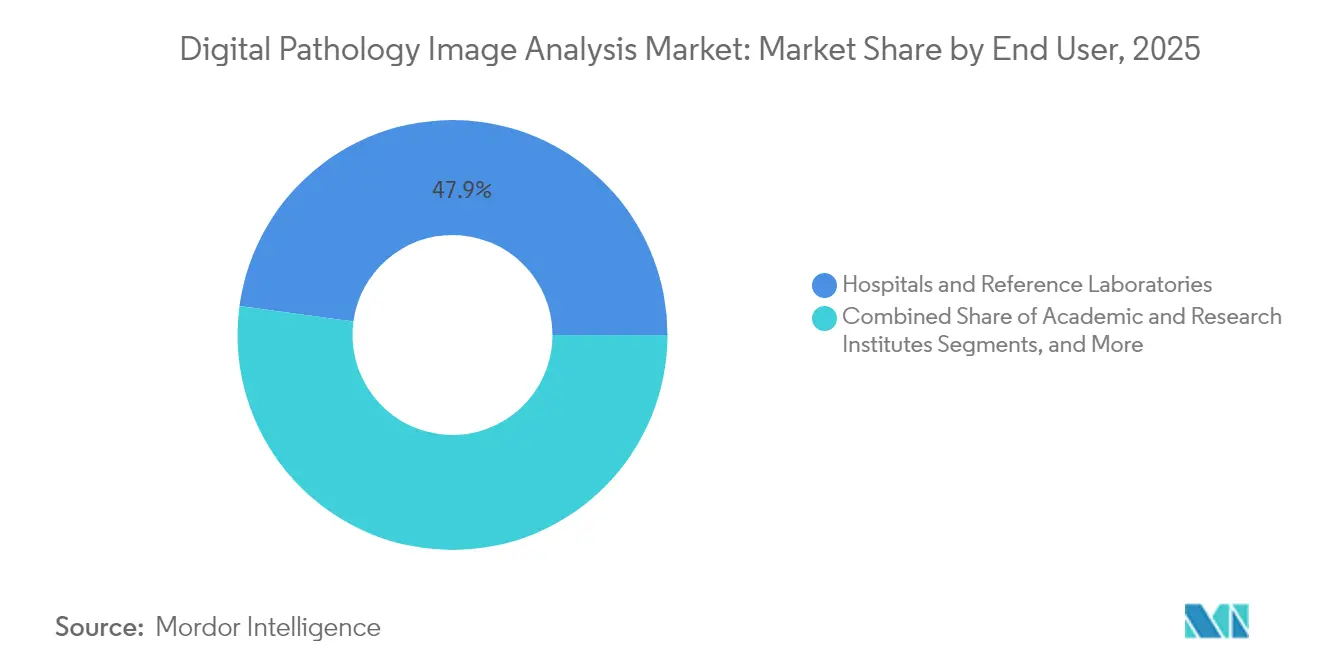

- By end user, hospitals and reference laboratories commanded 47.85% of the digital pathology image analysis market size in 2025, whereas pharmaceutical and biotechnology firms are forecast to grow 9.21% through 2031.

- By geography, North America led with 48.06% of the digital pathology image analysis market share in 2025; Asia-Pacific is set to post a 9.95% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Pathology Image Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising digital-pathology adoption for lab efficiency | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Drug-discovery and companion-diagnostic uptake | +1.8% | North America & EU core, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Growth in cancer and chronic-disease prevalence | +1.5% | Global | Long term (≥ 4 years) |

| AI integration for automated image analysis | +2.3% | North America, Europe and major APAC metros | Short term (≤ 2 years) |

| Spatial-omics adoption for multimodal insights | +0.9% | North America, Europe research hubs | Long term (≥ 4 years) |

| Federated-learning deployments | +0.6% | Global, with regulatory focus in EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Digital-Pathology Adoption to Enhance Lab Efficiency

Laboratories worldwide implement whole-slide imaging to cut reporting backlogs and standardise quality. Mayo Clinic’s enterprise-wide rollout demonstrated 30% faster case turnaround and sustained concordance with glass-slide diagnosis. Vietnamese–US collaboration data further recorded similar gains across 40,000 slides processed for remote expert review [1]UTH Health, “Telepathology Collaboration Outcomes,” uth.edu. AI-driven QC modules flag out-of-focus or tissue-missing tiles with 99.6% sensitivity and 96.7% specificity, preventing costly recuts. Despite upfront scanner and storage investment, institutions with >200,000 annual slides achieve payback inside four years through reduced consumables and shorter inpatient stays. Productivity benefits are most evident in tertiary-care and oncology centres coping with rising caseload complexity.

Increasing Application in Drug Discovery & Companion Diagnostics

Roche’s FDA-cleared TROP2 companion diagnostic combines immunohistochemistry with digital-image analysis, paving a path for algorithm-quantified biomarkers to guide targeted therapies. Novartis and Deciphex jointly validate AI lesion-detection tools for preclinical studies, aiming to shorten regulatory reviews and improve GLP compliance [2]Quest Diagnostics, “Acquisition of PathAI Assets,” questdiagnostics.com. Spatial transcriptomics overlays are uncovering immune-microenvironment patterns predictive of checkpoint-inhibitor response, accelerating precision-oncology pipelines. Approved digital pathology endpoints now appear in early-phase trials, shrinking enrolment cycles through automated patient stratification. As clinical-trial costs fall, pharmaceutical spending on digital pathology image analysis market solutions is expected to climb steadily.

Expanding Prevalence of Cancer & Chronic Diseases

Global cancer incidence surpassed 20 million new cases in 2024, raising demand for highly reproducible tissue assessments. Digital pathology platforms facilitate large-field quantification of tumour-infiltrating lymphocytes and mitotic indices, improving prognostic accuracy in breast and lung cancers. Multi-modal datasets from spatial transcriptomics reveal intermediate tumour-cell states linked to relapse risk, insights seldom achievable by light microscopy alone. Chronic-disease comorbidities in ageing populations further elevate biopsy volumes, supporting sustained adoption across cardiometabolic and renal-disease specialties.

Growing Integration of AI for Automated Image Analysis

Foundation models such as UNI and CONCH, trained on 200 million tiles, now outperform bespoke algorithms on 34 pathology benchmarks and are rapidly adaptable to rare indications. Federated learning tests across five EU cancer centres achieved AUROC parity with pooled-data models while sidestepping cross-border data-sharing constraints. PathAI’s PathChat obtained FDA Breakthrough Device status for conversational assistance that contextualises slide features and clinical metadata in real time. Multi-omic AI layers combine histology, genomics and radiology to predict treatment response with AUCs above 0.90 in pilot lung-cancer studies, pushing the digital pathology image analysis market toward comprehensive decision-support ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory demands for primary diagnosis | -1.2% | Global, varying intensity | Medium term (2-4 years) |

| High upfront costs & ROI uncertainty | -1.8% | Global, more acute in emerging markets | Short term (≤ 2 years) |

| Data-privacy limits on slide exchange | -0.9% | EU & North America core | Medium term (2-4 years) |

| Shortage of curated rare-disease datasets | -0.7% | Global research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Concerns for Primary Diagnosis

Europe’s In-Vitro Diagnostic Regulation reclassifies most image-analysis software as Class C, demanding notified-body audits and post-market performance studies [3]European Commission, “In-Vitro Diagnostic Regulation (IVDR),” ec.europa.eu. The US FDA requires robust accuracy concordance to glass slides plus failure-mode analysis, extending clearance timelines to 24-36 months for AI-rich systems. Differing evidence standards across Japan, China and Canada oblige vendors to conduct multi-region validations, raising development costs. Interpretability rules in the EU AI Act add complexity, particularly for deep-learning models. These variations slow multi-national launches and moderate near-term revenue.

High Upfront Costs & ROI Uncertainty for Smaller Labs

Entry-level whole-slide scanners cost USD 200,000–500,000, with enterprise rollouts surging past USD 1 million once storage clusters, secure networks and software licences are included. Annual support and cloud-archive fees add 20–30% to operating expenses. A 2024 Labcorp survey showed only 33% of community labs had adopted digital pathology, citing limited reimbursement and unclear payback horizons. Without high case volumes, small centres struggle to justify investment despite workflow benefits, restraining the broader digital pathology image analysis market in cost-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software: AI-Powered Solutions Drive Market Evolution

The image-analysis-algorithm segment represented 42.12% of 2025 revenue, forming the functional core of most deployments in the digital pathology image analysis market. Continuous enhancements in tile-wise tissue detection, nuclear segmentation and H-score quantification keep this segment indispensable, but revenue growth is slower than AI-driven decision suites. The latter log a 9.78% CAGR, fuelled by FDA breakthroughs for prostate-cancer grading and lung-cancer biomarker quantification. As a result, AI-powered suites are expected to account for 30.4% of the digital pathology image analysis market size by 2031. Middleware and integration tools secure adoption by bridging laboratory information systems and cloud archives, while open-source environments such as QuPath extensions lower barriers for academic research. Large vision models from HistAI trained on 1.1 million slides shorten development cycles for niche algorithms, driving differentiation.

A parallel shift emerges toward multi-modal orchestration, where image analysis plugs into genomic-variant callers and radiomics dashboards. Vendors offering seamless API layers find favour among enterprise buyers seeking scalable “plug-and-play” ecosystems. Scanners bundled with embedded AI workflows deliver recognisable value propositions to resource-limited hospitals that prefer turnkey packages. Over the forecast window, pricing models are expected to pivot from perpetual licences to annualised software-as-a-service subscriptions, aligning revenue streams with usage volumes and lowering capital hurdles for mid-tier institutions.

By Application: Drug Discovery Accelerates Beyond Traditional Diagnosis

Disease diagnosis retained a 51.62% share of the digital pathology image analysis market size in 2025, underpinned by national cancer-screening programmes and hospital modernisation. Automated mitosis counts, PD-L1 scoring and Gleason-grading modules are increasingly standard in tertiary centres. Drug discovery, however, is projected to grow fastest at 9.44% CAGR through 2031 as pharma companies rely on high-throughput digitisation for toxicology studies, image-based biomarkers and adaptive-trial enrichment. Partnerships such as Novartis–Deciphex underline sponsor appetite for validated AI lesion detection in regulated GLP environments. Companion-diagnostic algorithms integrating histology and AI-quantified immunomarkers underpin precision-therapy launches, encouraging broader investment. Educational and teleconsultation subsectors add resilient demand, especially in emerging markets adopting cloud-based curricula to mitigate pathologist shortages.

Remote-second-opinion services record turnaround-time reductions of 30% compared with glass-slide shipping, expanding reach to under-served provinces. Quality-control modules score over 99% sensitivity in flagging artefacts and out-of-focus regions, helping laboratories comply with tightening accreditation norms. Collectively these trends broaden the application spectrum and cement the role of the digital pathology image analysis market in multidisciplinary precision-medicine workflows.

By End User: Pharmaceutical Sector Drives Innovation Adoption

Hospitals and reference laboratories generated 47.85% of 2025 spending, reflecting routine histopathology needs and mandated quality-improvement initiatives. Their demand profile centres on whole-slide scanners, integrated LIS connectors and on-premise archives. Pharmaceutical-biotechnology companies, in contrast, are set to post the highest growth at 9.21% CAGR, propelling algorithm validation and cloud-native infra purchases. Their use cases range from toxicologic-pathology readouts to global study-site harmonisation. Academic institutes leverage open-source tools for spatial-omics research, while contract research organisations capture outsourced study volumes by integrating AI scoring into regulatory submissions. Smaller local labs remain cautious adopters, constrained by capex realities, but new pay-per-scan business models are emerging from platform vendors eager to penetrate this untapped pool of potential users.

Emerging partnership paradigms—such as Charles River teaming with Deciphex—underscore CRO appetite for turnkey AI panels that reduce observer variability and improve lesion-detection time. In parallel, integrated health networks negotiate multi-year enterprise licences that bundle hardware refreshes, maintenance and AI upgrades into predictable operating-expense structures, lowering per-slide costs over contract lifetimes.

Geography Analysis

North America maintained 48.06% of 2025 revenue, anchored by FDA clearances, early reimbursement frameworks and extensive hospital networks deploying whole-slide imaging at scale. Programmes like Mayo Clinic’s enterprise digital pathology initiative show institutional resolve to embed AI across all subspecialties. Quest Diagnostics’ acquisition of PathAI’s clinical assets deepens platform synergies and speeds AI diffusion in community oncology settings. Barriers persist in independent labs, where a 2024 industry poll revealed just 33% had gone fully digital owing to cost concerns. Nonetheless, cloud-storage price declines and CPT code updates are expected to ease adoption friction.

Asia-Pacific is projected to record a 9.95% CAGR to 2031, the highest among all regions. China’s DeepSeek AI has scaled to over ninety tertiary hospitals, illustrating sovereign AI programmes’ power in transforming care pathways. India’s National Digital Health Mission earmarks funds for telepathology nodes that integrate image archives with electronic-health-record backbones, paving pathways for rural biopsy review. Japanese start-ups such as Medmain raised USD 13.3 million in Series B financing to expand AI-based pathology services, buoyed by growing venture-capital confidence. Infrastructure gaps and disparate regional regulations remain obstacles, yet consortium-led pilots demonstrate that public-private models can overcome resource limitations.

Europe sustains a sizeable footprint despite regulatory headwinds from IVDR and the AI Act. 3DHISTECH secured CE-IVD registration for its PANNORAMIC 1000 scanner, signalling that compliance pathways, though stringent, are navigable. Funding rounds—Visiopharm’s USD 26.3 million raise, for instance—bolster continuous product improvements targeting workflow standardisation. The European Society of Pathology published consensus guidelines emphasising QC metrics, sustainability goals and data-sharing frameworks, aiding harmonised implementation across member states. Telepathology solutions address the continent’s rural-pathologist deficit, although smaller facilities face capital constraints similar to peers elsewhere.

Competitive Landscape

The digital pathology image analysis market shows moderate fragmentation with visible consolidation momentum as diagnostic majors integrate AI upstarts to secure end-to-end portfolios. Quest Diagnostics closed on PathAI’s Memphis lab and licensed the AISight platform, positioning the nation’s largest reference lab to embed algorithmic grading across 7,000 hospitals. LeicaBiosystems’ strategic investment in IndicaLabs pairs the Aperio GT450 scanner family with HALOAP software, offering DICOM-native streaming, remote sign-out, and an AI-apps marketplace under one brand.

Competition now pivots on three axes. First, breadth of AI pipelines: Paige’s Virchow and PRISM foundation suites span17 tissue types, giving early-mover hospitals an avenue to one-contract coverage for multiple cancers. Second, interoperability: open-API designs earn preference as multi-modal datasets flow into cloud laboratory information systems; Aiforia’s2025 pact with Paige demonstrates the vendor-neutral ethos demanded by enterprise buyers. Third, regulatory velocity: Ibex secured CE-IVDR and FDA clearances in rapid succession, winning first-mover contracts at five U.S. integrated-delivery networks.

Emerging disruptors inject fresh capabilities. PictorLabs raised USD48.8million to commercialize AI-based virtual staining that could bypass traditional dyes and save 20minutes per slide. Clarapath amassed USD75million to automate tissue grossing with SectionStar robots, shaving hours off upstream processing and feeding cleaner images downstream. Foundation-model suppliers like HistAI open license programs that let regional vendors fine-tune pretrained weights, eroding entry barriers and spurring localized algorithm ecosystems. Regional specialists persist, providing language-localized interfaces and on-site support; Pathcore in Canada and Deciphex in Ireland illustrate how service proximity preserves competitive tension despite global consolidators.

Digital Pathology Image Analysis Industry Leaders

Danaher Corporation

Koninklijke Philips NV

PathAI, Inc.

Visiopharm A/S

Paige AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Leica Biosystems announced a strategic investment in Indica Labs to combine Aperio scanners with HALO AP software, targeting AI-enabled companion diagnostics and biomarker discovery applications.

- September 2024: Proscia partnered with Fimlab Laboratories to deploy its Concentriq platform, enabling AI-backed pathology reporting across Finland’s largest regional lab.

- June 2024: Quest Diagnostics agreed to acquire selected PathAI Diagnostics assets to accelerate AI-supported cancer-diagnosis workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the digital pathology image analysis market as revenue generated from commercially packaged software suites and algorithm libraries that process whole-slide images and related metadata to deliver quantitative, diagnostic-support outputs for tissue-based pathology workflows. It captures licenses, SaaS subscriptions, and managed-analysis services used across clinical, research, and drug-development settings.

Scope exclusion: Hardware scanners, storage appliances, laboratory information systems, and stand-alone telepathology viewers fall outside this valuation.

Segmentation Overview

- By Software

- Imaging Management System Software

- Image Analysis Algorithms

- AI-powered Decision-Support Suites

- Integration / Middleware Tools

- Open-Source & Community Platforms

- Others

- By Application

- Disease Diagnosis

- Drug Discovery

- Companion Diagnostics

- Education & Training

- Teleconsultation & Remote Second Opinion

- Quality Control & Regulatory Compliance

- By End User

- Hospitals & Reference Laboratories

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations (CROs)

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and short surveys with pathologists, lab IT leads, and product managers across North America, Europe, and Asia-Pacific clarified algorithm validation timelines, slide-per-day throughput after digitization, and typical AI budget allocations. These discussions closed information gaps and anchored assumptions surfaced during desk work.

Desk Research

Analysts began with public datasets, including FDA 510(k) clearances, European CE-Mark listings, National Cancer Institute SEER cancer incidence, and slide-digitization counts from the College of American Pathologists. They then layered in WHO policy papers, patent families mined through Questel, and customs codes for scanner imports from Volza. Company 10-Ks, investor presentations, and reputable trade press supplied pricing cues and installed-base disclosures. Paid repositories such as D&B Hoovers and Dow Jones Factiva supported revenue mapping. The sources named are illustrative; numerous others informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with global histology test volumes and cancer incidence, then applies digitization penetration and image-analysis attachment rates to build demand. Selective bottom-up roll-ups of supplier revenues and sampled ASP × license counts validate and adjust totals. Key variables include average slides scanned per instrument, AI-enabled workstations per lab, algorithm price erosion, regional oncology caseload growth, and cloud migration share. Five-year forecasts blend multivariate regression with scenario analysis, guided by expert consensus on regulatory and reimbursement milestones. Where supplier data are patchy, moderated channel checks bridge gaps.

Data Validation & Update Cycle

Outputs undergo anomaly scans, variance checks against independent markers such as NIH grant trends, and a two-step peer review before sign-off. Models refresh annually, with interim updates triggered by material events. Before delivery, an analyst reruns critical queries so clients receive the latest view.

Why Our Digital Pathology Image Analysis Baseline Commands Reliability

Published estimates often diverge because firms choose different product mixes, pricing cascades, and refresh cadences, a reality our team addresses head-on.

Key gap drivers include others folding scanners and storage revenue into software totals, or conversely tracking AI-only modules; reliance on disparate cancer incidence datasets; currency conversion timing; and less frequent updates compared with Mordor's annual cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 419.7 M | Mordor Intelligence | - |

| USD 1.17 B | Global Consultancy A | Includes hardware and LIS; uses list prices without volume discounts |

| USD 168.3 M | Trade Journal B | Tracks AI algorithms only, excludes visualization and service revenues |

The comparison shows that, by selecting a precise software-only scope and cross-validating volumes with end-user budgets, Mordor Intelligence offers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

How big is the Digital Pathology Image Analysis Market?

The Digital Pathology Image Analysis Market stands at USD 457.59 million in 2026 and is projected to reach USD 704.08 million by 2031 at a 9.03% CAGR over 2026-2031.

Which region leads in revenue, and which grows fastest?

North America leads with 48.06% of 2025 revenue, while Asia-Pacific is forecast to grow at 9.95% CAGR to 2031.

Who are the key players in Digital Pathology Image Analysis Market?

Danaher Corporation, Koninklijke Philips NV, PathAI, Inc., Visiopharm A/S and Paige AI, Inc. are the major companies operating in the Digital Pathology Image Analysis Market.

Which is the fastest growing region in Digital Pathology Image Analysis Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What software segment shows the highest growth?

AI-powered decision-support suites post the fastest 9.78% CAGR, reflecting rising demand for intelligent automation.

Page last updated on: