Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 405.99 Billion |

| Market Size (2031) | USD 884.43 Billion |

| Growth Rate (2026 - 2031) | 16.85% CAGR |

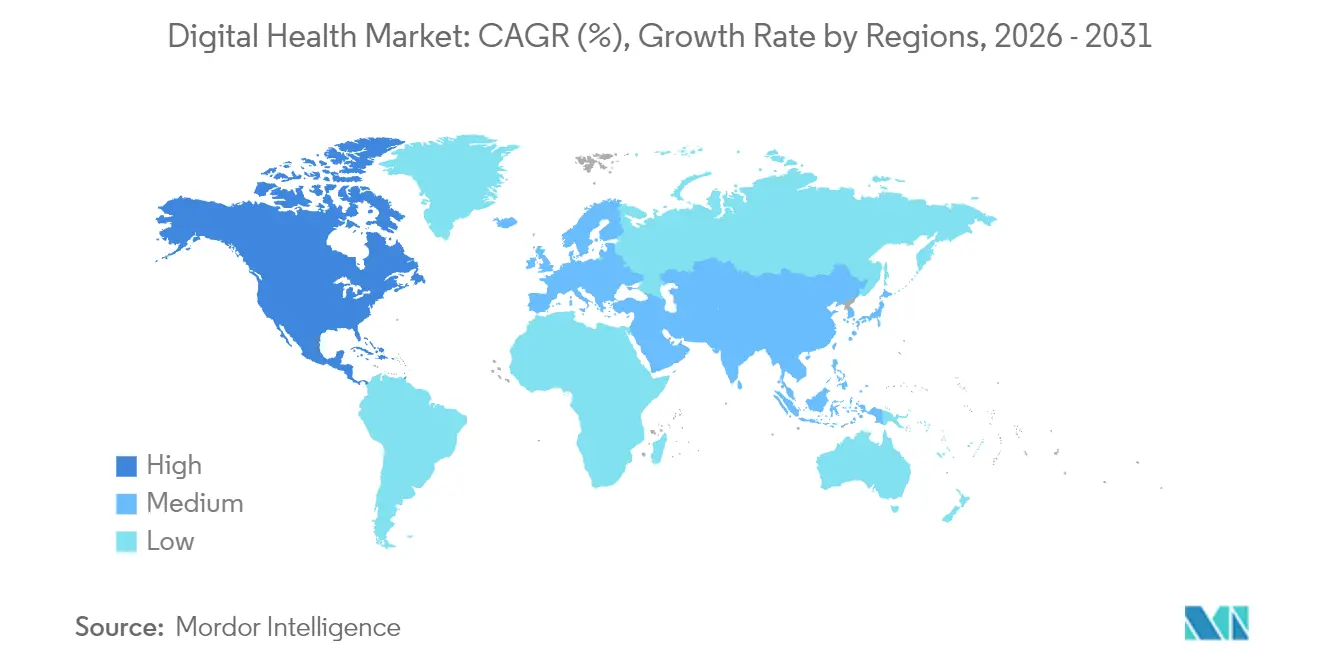

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Health Market Analysis by Mordor Intelligence

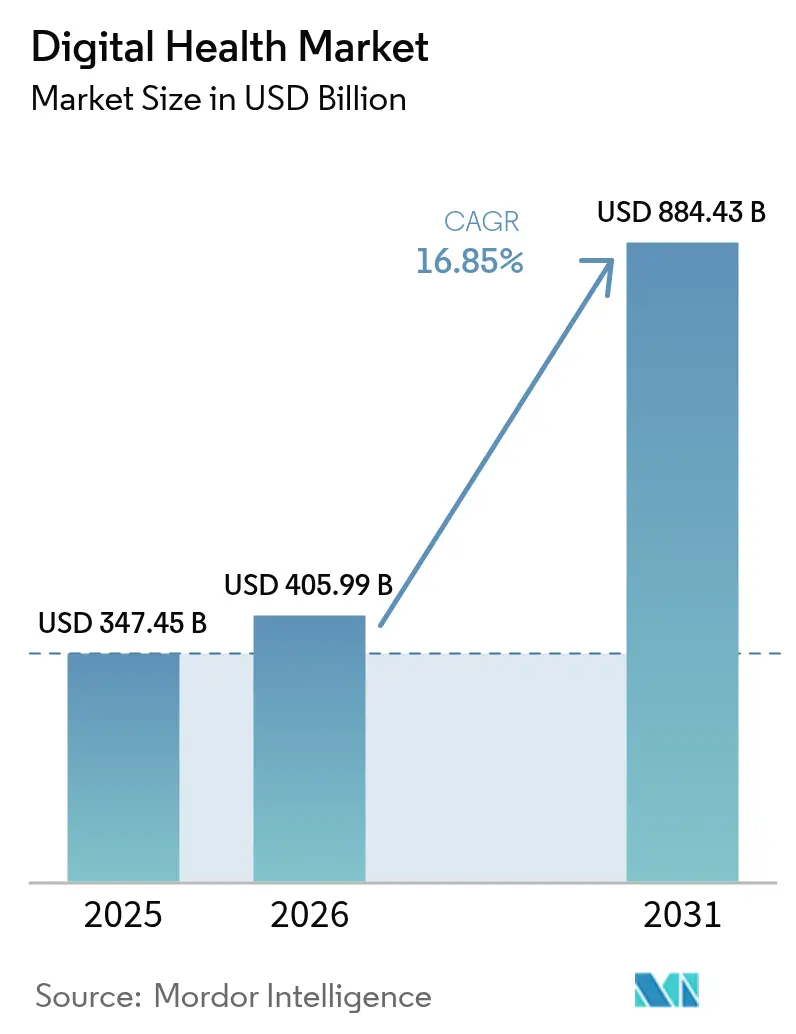

The Digital Health market size is expected to grow from USD 347.45 billion in 2025 to USD 405.99 billion in 2026 and is forecast to reach USD 884.43 billion by 2031 at 16.85% CAGR over 2026-2031.

Momentum reflects a global pivot from episodic treatment toward continuous, data-driven care supported by artificial intelligence, Internet-of-Things sensors, and advanced analytics. Regulatory agencies are keeping pace: the United States Food and Drug Administration has already given Breakthrough Device designation to 1,041 solutions and cleared 128 of them for commercial use, opening more pathways for evidence-backed digital therapeutics FDA. Wider telehealth reimbursement, national digital health strategies, and demand for remote monitoring from aging populations add further lift. At the same time, the sector remains fragmented because providers, payers, pharmaceutical firms, and big-tech entrants prefer partnership models over outright M&A, resulting in an ecosystem rich in alliances rather than consolidation. Cybersecurity threats and data-sharing barriers temper expansion but have not derailed investment, as vendors continue to embed end-to-end encryption, adopt FHIR standards, and certify cloud environments to win stakeholder trust.

Key Report Takeaways

- By technology, telehealth led with 46.78% revenue share in 2025, while mHealth applications are projected to compound at 17.62% through 2031.

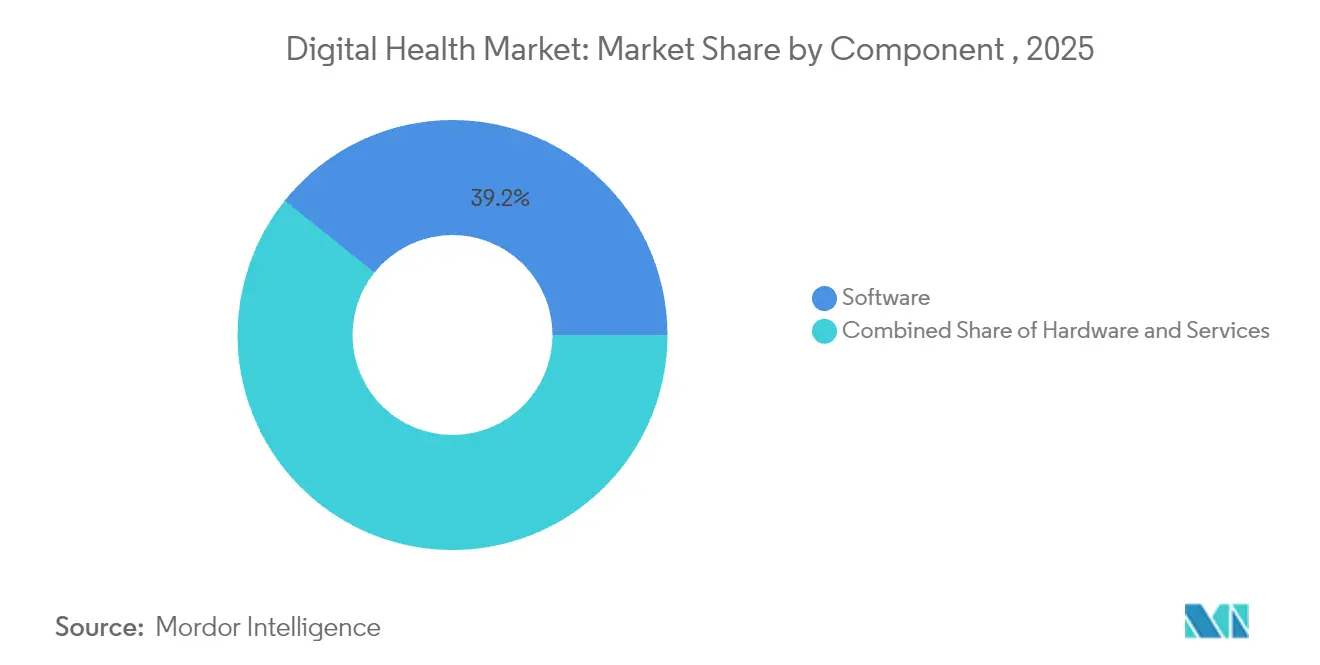

- By component, services held 38.62% of digital health market share in 2025; software is expected to advance at an 17.74% CAGR to 2031.

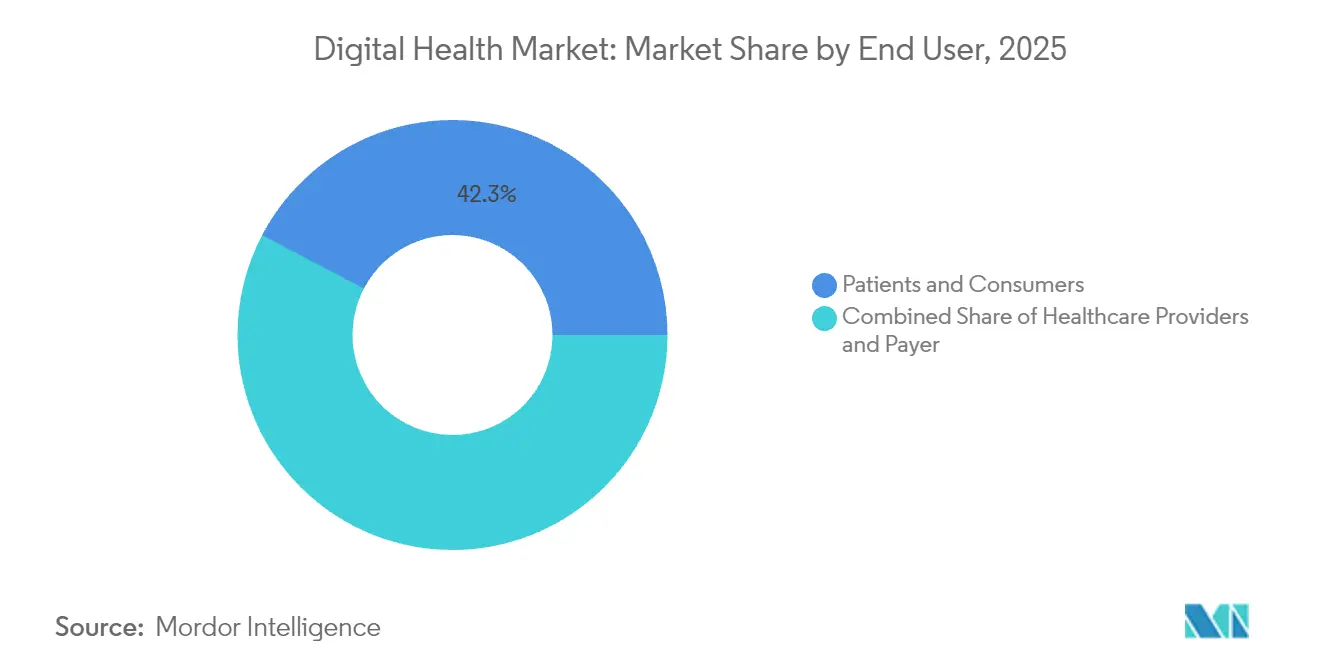

- By end user, patients & consumers commanded 42.31% of digital health market size in 2025, whereas the payer segment is set to grow 17.35% annually through 2031.

- By geography, North America captured 43.21% of digital health market share in 2025; Asia-Pacific is on track for an 18.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Digital Health Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of digital healthcare | +4.2% | Global | Medium term (2-4 years) |

| Rise in AI, IoT & Big Data integration | +3.8% | North America & EU, APAC core | Short term (≤ 2 years) |

| Growing mHealth penetration & smartphone usage | +3.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expansion of telehealth for aging & rural populations | +2.7% | Global, with early gains in North America, Europe | Long term (≥ 4 years) |

| Regulatory sandboxes accelerating digital therapeutics approval | +1.9% | North America & EU | Short term (≤ 2 years) |

| Generative-AI clinician copilots boosting productivity | +1.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing adoption of digital healthcare

Health systems are moving from reactive service delivery to preventive, always-on care models that embed remote monitoring, electronic health records, and AI-assisted diagnostics in routine practice. Pandemic-era urgency jump-started investment, but budgets have held steady because chief executives now treat digital infrastructure as essential rather than optional. Network effects surface when more institutions connect to shared data platforms, raising the utility of each additional node. This virtuous cycle encourages hospitals to procure interoperable solutions and nudges clinicians to incorporate patient-generated data into care plans, tightening the feedback loop between in-person and virtual services. As the digital health market expands, direct-to-consumer wellness apps further normalize digital interactions, creating a foundation of patient familiarity that spills over into formal medical settings.

Rise in AI, IoT & big-data integration

Artificial intelligence now underpins core hospital operations such as imaging triage, medical coding, and virtual scribing. High-fidelity IoT sensors feed continuous data streams into cloud analytics engines capable of forecasting acute events hours before they manifest at the bedside. Vendor road maps highlight synthetic-data generation, autopilot quality assurance, and multimodal reasoning, signalling a future where ambient intelligence follows patients across settings. Administrative leaders accept short-run implementation costs because returns show up in productivity gains, fewer claim denials, and lower readmission penalties. As datasets scale, predictive algorithms grow more accurate, creating a self-reinforcing improvement loop that widens the performance gap between digital leaders and laggards.

Growing mHealth penetration & smartphone usage

Asia-Pacific’s smartphone penetration passed 51% in 2024 and keeps climbing, turning the handset into the primary access node for health services [1]GSMA, “The Mobile Economy Asia Pacific 2024,” gsma.com. Rural users adopt menstruation tracking, diabetes coaching, and mental-wellness apps that fill gaps left by clinician shortages. Personalization engines adjust content and dosing reminders based on real-time behavior, lifting adherence and generating richer datasets for research. Younger demographics treat mobile channels as the default entry point, so insurers and providers follow suit, integrating claims, teleconsultations, and pharmacy delivery into unified super-apps. Payment reforms that reimburse app-based interventions further accelerate diffusion, especially across India, Indonesia, and Vietnam.

Expansion of telehealth for aging & rural populations

Demographic aging amplifies demand for low-cost, continuum-of-care models. Virtual visits and remote patient monitoring help older adults avoid specialist travel and prolonged hospital stays. Veterans’ health networks and public payers report drops in unscheduled emergency visits after scaling tele-geriatrics programs. Rural broadband initiatives shrink bandwidth constraints, and user-interface redesigns address age-related cognitive or vision limitations. Family care-giver portals invite daughters, sons, and spouses into the care loop, boosting virtual-consult follow-through and medication adherence. Over time, accumulated engagement data supports risk-stratification programs that tailor outreach intensity, improving resource allocation for overstretched primary-care teams. These developments reinforce the central role of telehealth in the digital health market, especially in regions facing clinician shortages.

Restraints Impact Analysis of Digital Health Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity & privacy concerns | -2.1% | Global | Short term (≤ 2 years) |

| Interoperability & data-silo challenges | -1.8% | Global, with acute impact in North America & EU | Medium term (2-4 years) |

| Algorithmic bias & clinician trust deficit | -1.3% | Global | Medium term (2-4 years) |

| Digital divide limiting rural & elderly access | -0.9% | Global, with concentrated impact in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity & privacy concerns

Ransomware attacks on hospital networks expose sensitive patient files and erode public trust just as virtual care volumes hit new highs. Regulatory penalties under HIPAA and GDPR inflate breach-response costs, nudging boards to prioritize security spending even when margins tighten. Implementation teams juggle the trade-off between bullet-proof encryption and clinician usability, because stricter log-in protocols can slow workflows. Insurers now request cyber-readiness certifications before underwriting liability policies, making resilience a market requirement rather than a differentiator. Vendors who can guarantee rapid threat detection and zero-trust architectures gain an edge in procurement cycles, underscoring how cybersecurity readiness is becoming a foundational expectation across the digital health market.

Interoperability & data-silo challenges

Competing electronic health-record vendors and legacy departmental systems still trap critical data behind proprietary interfaces, undermining the promise of seamless, longitudinal patient views. Although regulators mandate FHIR-compliant data exchange, integration gaps persist because hospitals lack skilled staff, and incentives to share remain weak. Middleware platforms grow in popularity, yet they add subscription costs that smaller clinics struggle to absorb. Health-information exchanges pilot shared governance models, but uptake varies by state and region. Until payer, provider, and pharmacy datasets flow freely, clinical decision support will rely on incomplete inputs, limiting the full value of advanced analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Digital Health Market Segment Analysis

By Component:

Services Strengthen While Software AcceleratesServices accounted for 38.62% of digital health market revenue in 2025 as health-system executives relied on external partners to deploy complex solutions and manage regulatory compliance. Engagements often bundle implementation, change-management, and cybersecurity, helping organizations launch tele-ICU programs or chronic-disease apps without overloading internal IT teams. Demand stays robust in markets where shortages of specialized data engineers and informaticians slow do-it-yourself rollouts. Yet the spotlight is shifting to software, which registers the fastest 17.74% CAGR to 2031. Cloud-native platforms that automate charting, surface care-gap alerts, and synthesize multimodal data scale faster than hardware-centric models, letting mid-size hospitals compete with academic centers.

The shift favors subscription pricing and continuous feature releases instead of large, one-time license deals. Vendors emphasize modular APIs that plug into existing systems, reducing rip-and-replace anxiety. As algorithms mature, user experience improves, shortening clinician onboarding curves. These benefits translate into higher renewal rates and rising average revenue per user, reinforcing the software growth arc and signaling a long-term structural shift in the digital health market.

By Technology:

Telehealth Dominance Meets mHealth MomentumTelehealth represented 46.78% of 2025 spending thanks to relaxed reimbursement rules and patients’ comfort with video visits after pandemic-era exposure. Specialists use digital stethoscopes, otoscopes, and ultrasound probes that stream high-definition images to remote hubs, extending care to under-served areas. Payers track lower readmissions and shorter length-of-stay metrics, feeding more reimbursement codes into fee schedules. mHealth grows fastest at an 17.62% rate as handset sensors, AI voice assistants, and gamified behavior-change modules transform phones into full-service clinics. Investors back app portfolios that span fertility, oncology navigation, and cardiometabolic coaching, betting on direct-to-consumer engagement and employer uptake as the digital health industry expands.

Intersections between the two segments multiply: hospital groups integrate app-generated vitals into teleconsult dashboards, while apps embed physician on-demand buttons to escalate care. Competitive positioning therefore hinges on ecosystem integration rather than stand-alone feature counts.

By End User:

Consumer Empowerment Spurs Payer InnovationPatients & consumers captured the largest 42.31% of the digital health market share in 2025, reflecting widespread comfort with self-tracking, direct-ordering lab tests, and asynchronous chat with clinicians. The proliferation of application-programming-interface gateways ensures individuals can port their data between health plans, fitness apps, and electronic health records, reinforcing user agency. Payers, however, chart the highest 17.35% CAGR to 2031 as insurers deploy digital front-doors to lower claims costs. Remote monitoring kits and medication-adherence nudges feed real-time risk scores, enabling proactive outreach before costly exacerbations occur.

Value-based contracts reward this shift. Plans issue premium credits for sustained engagement and link deductible thresholds to verified wellness milestones. Employers latch on, embedding app bundles into benefit offerings to hold down premiums. The payer-provider-patient triad thus converges around outcome-driven, tech-enabled delivery.

Geography Analysis

North America Digital Health Market

North America controlled 43.21% of 2025 spending, backed by generous payer reimbursement schedules, an installed base of electronic health records, and an active innovation pipeline. The FDA’s Breakthrough Devices Program provided 1,041 designations, with 128 commercial clears by September 2024, cementing the United States as the reference market for clinical validation and investor signalling, reinforcing its central role in the digital health market. Cross-border telehealth compacts between Canada and the United States improve specialist access, while Mexico’s social-security expansion integrates mobile triage tools to manage urban-rural resource gaps.

APAC Digital Health Market

Asia-Pacific posts the fastest 18.02% CAGR through 2031 as governments fold telemedicine into universal-coverage strategies and handset adoption unlocks massive addressable user pools. Mobile economy value reached USD 880 billion in regional GDP during 2023. India’s Ayushman Bharat Digital Mission links personal health records to national IDs; Indonesia’s JKN scheme covers remote islands with virtual clinics; and Japan subsidizes AI-based home-care robots to offset nursing shortages. Local language interfaces and lightweight data protocols accelerate adoption among first-time users, positioning the region as a rising anchor of the digital health market.

EMEA and South America Digital Health Market

Europe, South America, and the Middle East & Africa advance at mid-single-digit rates as policymakers negotiate the balance between innovation and privacy. Germany’s DiGA framework reimburses certified apps, France deploys nationwide e-prescription services, and Saudi Arabia’s Vision 2030 earmarks tele-ICU funds. Regulatory heterogeneity slows multinational rollouts, yet early movers find growth pockets in cross-border mental-health platforms and rare-disease registries.

Competitive Landscape

Consolidation Agility: Thriving Amid Industry Realignment

The dramatically slowed pace of mergers and acquisitions—with only 21 M&A deals in Q3 2024 compared to the previous year's quarterly average of 37—signals a critical competitive reset in how digital health trends are reshaping industry structure and competitive positioning. This consolidation slowdown, coupled with the overall investment decline to $8.2 billion across 379 investments so far in 2024 (compared with $10.8 billion across 500 deals in full-year 2023), indicates a market shifting from rapid expansion to strategic integration. For connected health providers, this environment rewards those with agile partnership strategies that can navigate industry realignment without relying solely on acquisition-based growth. Forward-thinking companies are restructuring their approach to market expansion through strategic alliances that enhance service offerings and extend market reach without the capital requirements of outright acquisition—similar to how transformation partners like HIMSS have built networks serving over 65,000 centers in more than 50 countries. This emerging competitive dynamic favors global digital health players who demonstrate excellence in partnership orchestration, interoperability leadership, and ecosystem integration, enabling them to achieve network effects and scalability advantages without the financial and operational burden of numerous acquisitions. Companies mastering this collaborative approach can maintain growth momentum despite constrained M&A options, while simultaneously positioning themselves as attractive partners or acquisition targets when market digital health industry conditions evolve.

Digital Health Industry Leaders

Allscripts Healthcare Solutions Inc.

Koninklijke Philips N.V.,

OTH.IO

AMD Global Telemedicine Inc.

International business Machinery Corporation (IBM)

- *Disclaimer: Major Players sorted in no particular order

Digital Health Market Companies Covered in this Report

- AdvancedMD

- Allscripts

- AT&T

- Athenahealth

- Oracle Corp. (Cerner)

- AMD Global Telemedicine

- Cisco Systems

- iHealth Labs

- IBM

- Koninklijke Philips

- Mckesson

- OTH.IO

- Teladoc Health

- Amwell

- Apple

- Google Health

- Qualcomm

- GE Healthcare

- Siemens Healthineers

- Epic Systems

- Medtronic

Recent Industry Developments in Digital Health Market

- June 2025: The Joint Commission and CHAI unveiled national standards for responsible AI in healthcare, creating a common governance template for hospital boards HIT Consultant.

- June 2025: Welldoc agreed to power the Lilly Health app with an AI-driven cardiometabolic platform, marking pharma’s deeper push into consumer digital health HIT Consultant.

- May 2025: Oracle, Cleveland Clinic, and G42 formed a strategic alliance to deploy a global AI-based delivery platform Oracle.

- May 2025: Ambience Healthcare introduced an OpenAI-powered medical-coding model that outperformed physicians by 27% in accuracy, underscoring automation’s administrative upside.

Digital Health Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the digital health market as every software platform, connected device, and service that enables the remote, data-driven, or virtual delivery of clinical care, disease management, wellness coaching, diagnostics, or administration across providers, payers, and consumers. According to Mordor Intelligence, the market was valued at USD 347.45 billion in 2025 and is projected to reach USD 768.30 billion by 2030.

Scope exclusion: Stand-alone hospital IT that supports only back-office finance or HR functions is not covered.

Segments Covered in This Report

- By Component

- Hardware

- Software

- Services

- By Technology

- Telehealth

- mHealth

- Health Analytics

- Digital Health Systems

- By End User

- Healthcare Providers

- Payers

- Patients & Consumers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interview clinicians, hospital IT heads, digital therapeutics founders, and payer policy leads across North America, Europe, Asia-Pacific, and emerging regions. These discussions validate usage cohorts, price realizations, reimbursement triggers, and adoption barriers that secondary data cannot fully reveal, and then feed directly into model refinements.

Desk Research

We begin by mapping demand and supply using openly available tier-one sources such as the WHO Global Health Expenditure Database, OECD Health Statistics, the US Centers for Medicare & Medicaid Services telehealth utilization files, FCC broadband adoption dashboards, the EU Digital Economy and Society Index, and CDC diabetes surveillance data. Company filings, investor decks, and serious trade journals enrich adoption benchmarks and pricing cues. Our team also taps paid resources, D&B Hoovers for company revenue splits, Dow Jones Factiva for deal flow, and Questel for patent velocity, to flag innovation hotspots and calibrate competitive intensity. The above list is illustrative; many additional references inform the desk study.

Market-Sizing & Forecasting

A transparent top-down build anchors the baseline: national health outlays, smartphone penetration, and broadband coverage create the potential user pool, which is then filtered through prevalence of chronic diseases, telehealth reimbursement mandates, and wearable ASP trends. Select bottom-up checks, vendor revenue roll-ups, sampled subscription prices, and channel feedback test the totals before finalizing. Forecasts to 2030 rely on multivariate regression that links uptake rates to chronic disease prevalence, 4G/5G coverage, AI regulation milestones, and household disposable income. Gap areas in fragmented device sales are bridged by weighted averages agreed during expert calls.

Data Validation & Update Cycle

Outputs pass a three-layer variance review, after which anomalies trigger re-contact with key respondents. Reports refresh annually, with interim updates if material events, regulatory or macroeconomic, shift assumptions. Before release, a fresh analyst pass ensures readers receive the most current view.

How Mordor Intelligence's Digital Health Market Size Compares to Other Published Estimates

Published figures differ because each firm picks unique disease scopes, price ladders, and refresh cadences before converting revenues into a single currency.

Key gap drivers include: some publishers bundle back-office hospital IT, others assume uniform global ASP compression, and a few apply aggressive venture-funding multipliers rather than validated usage data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 347.45 bn (2025) | Mordor Intelligence | - |

| USD 427.24 bn (2025) | Regional Consultancy A | Includes laboratory information systems and counts announced, not realized, rollout budgets |

| USD 288.55 bn (2024) | Trade Journal B | Applies universal USD pricing without regional purchasing-power parity adjustments |

| USD 199.10 bn (2025) | Global Consultancy C | Excludes consumer wellness apps and wearables, leading to an under-representation of patient-directed spend |

These comparisons show that when scope boundaries and real transaction prices are handled with care, Mordor's disciplined blend of public data, field insight, and continuous review delivers a balanced, decision-ready baseline.

Key Questions Answered in the Report

How big is the Global Digital Health Market?

The Global Digital Health Market size is expected to reach USD 405.99 billion in 2026 and grow at a CAGR of 16.85% to reach USD 884.43 billion by 2031.

Which technology segment leads the market?

Telehealth holds 46.78% of 2025 spending, reflecting its role as the backbone for remote care

Which is the fastest growing region in Global Digital Health Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Digital Health Market?

In 2026, the North America accounts for the largest market share in Global Digital Health Market.

Page last updated on: